Italy Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

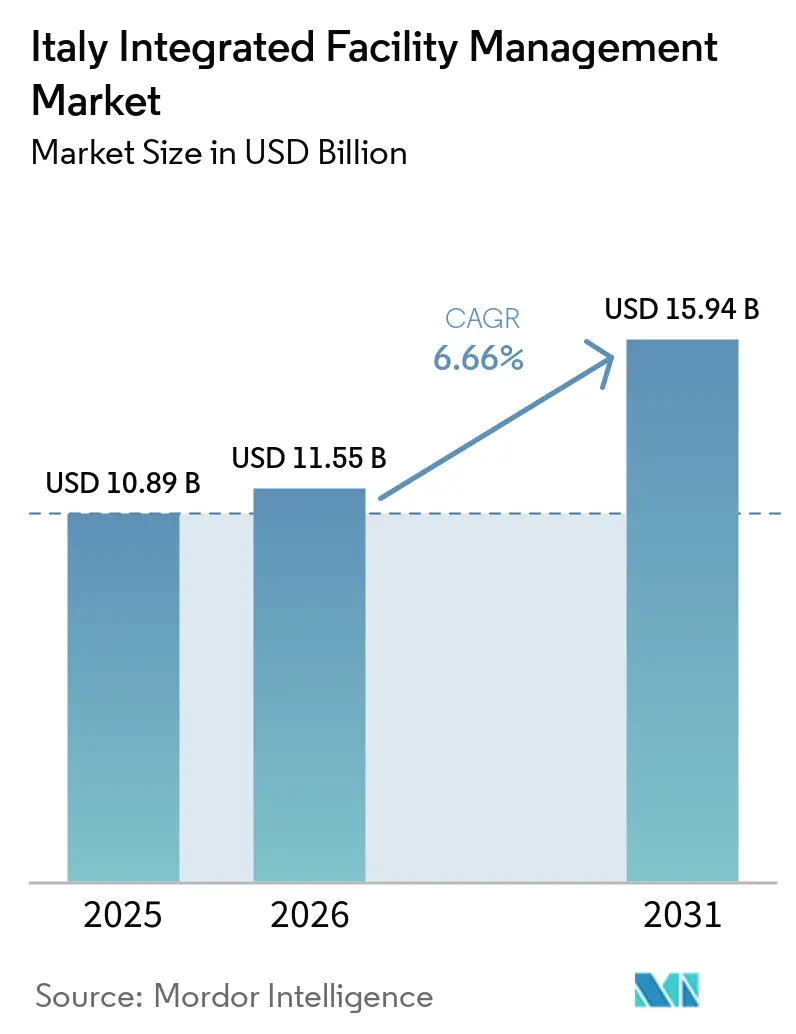

| Base Year Market Size (2025) | USD 10.89 Billion |

| Market Size (2026) | USD 11.55 Billion |

| Market Size (2031) | USD 15.94 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

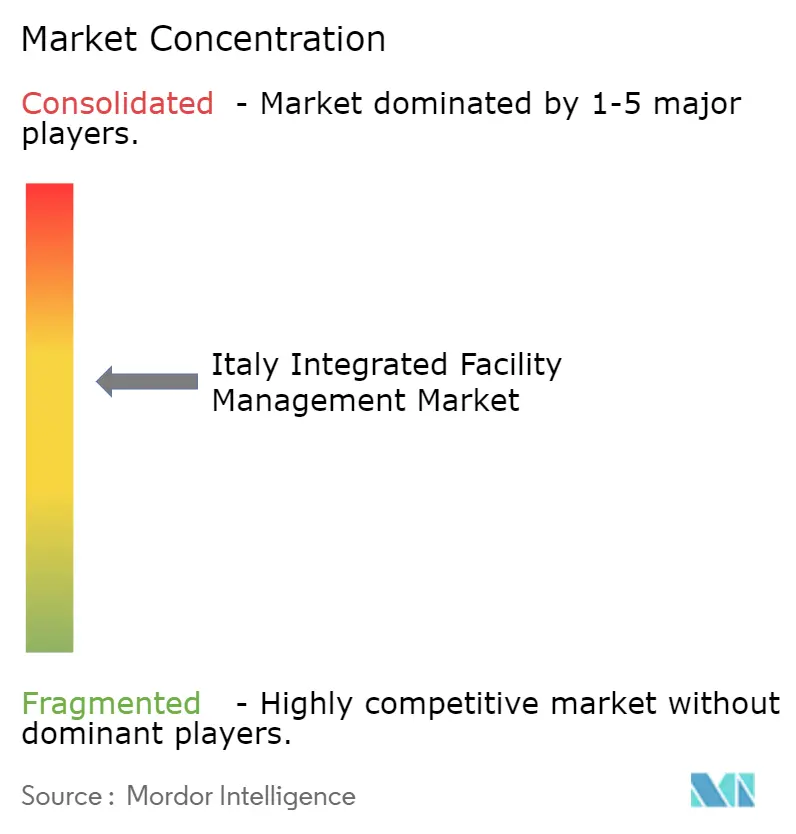

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Integrated Facility Management Market Analysis by Mordor Intelligence

The Italy Integrated Facility Management Market size is projected to expand from USD 10.89 billion in 2025 and USD 11.55 billion in 2026 to USD 15.94 billion by 2031, registering a CAGR of 6.66% between 2026 to 2031.

The Italy integrated facility management market still has meaningful room to deepen outsourcing, because integrated contracts represented only 26% of total FM revenue in January 2025, which means a large share of spend is still tied to fragmented service models that can move into bundled mandates over time. That conversion is being reinforced by D.Lgs. 36/2023 and Consip-led public procurement, which are pushing public administrations toward centralized, multi-service, and longer-duration contracting structures instead of scattered single-service buying. Italy’s PNRR adds a durable project base for the Italy integrated facility management market, because EUR 191.5 billion (USD 216.4 billion), was allocated under the national recovery plan and 37% of that envelope was directed toward ecological transition and infrastructure renewal, both of which pull facility demand into schools, hospitals, and judicial estates. The operating backdrop is also becoming more favourable for large, technically capable providers, because energy performance obligations, digital governance requirements, and measurable service outcomes are shifting procurement toward compliance capacity and away from basic unit-price competition. The main risk to the forecast remains service delivery capacity, since shortages in technical profiles across Italian industry are worsening and that pressure is especially relevant for HVAC, electrical maintenance, and IoT-linked building services that now sit at the center of modern IFM contracts.

Key Report Takeaways

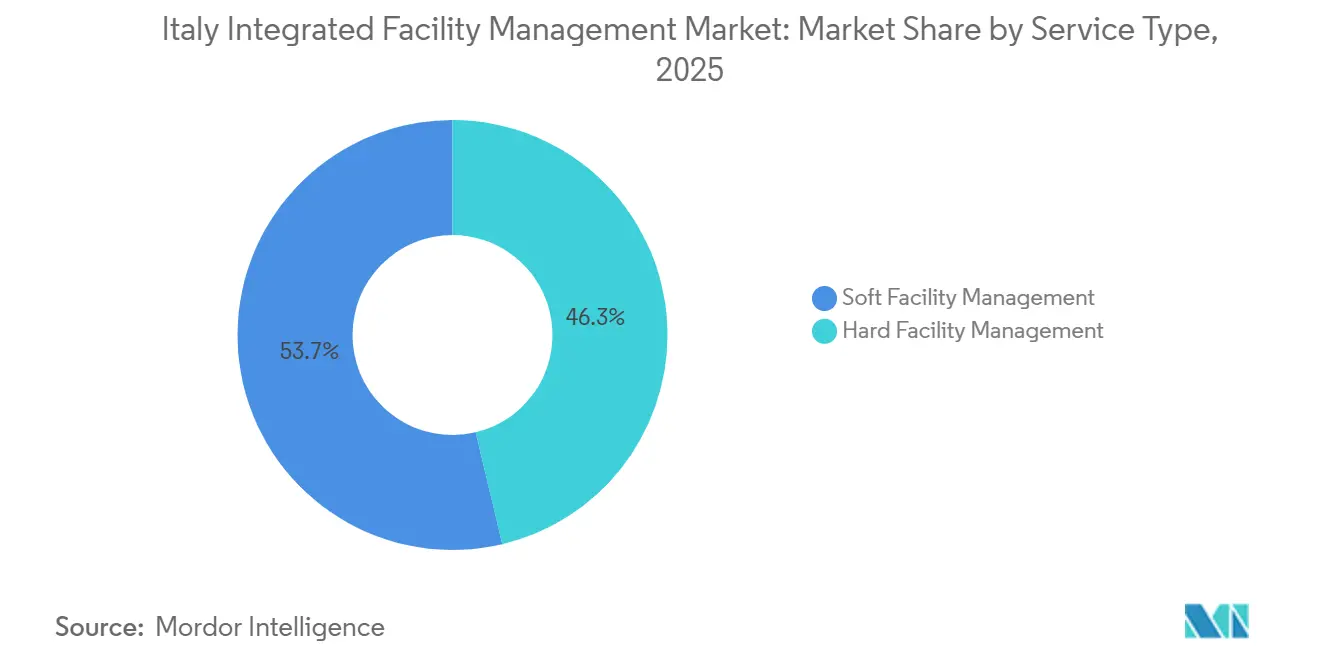

- By Service Type, Soft Facility Management held 53.7% of the Italy integrated facility management market in 2025, while Hard Facility Management is forecast to expand at a 7.4% CAGR through 2031.

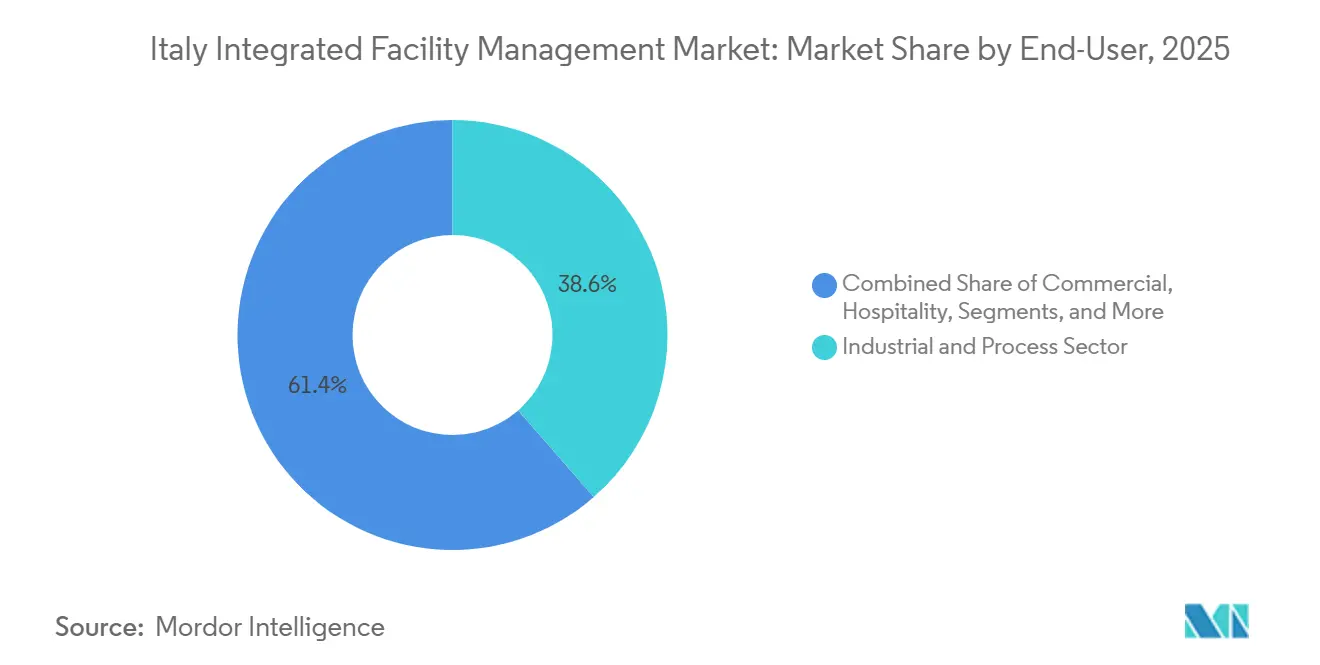

- By End-User, the industrial and process sector captured 38.6% of the Italy integrated facility management market in 2025, while the Commercial segment is projected to grow at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic Shift from Single Service Outsourcing to Integrated FM | +1.5% | National, with strongest acceleration in large urban centers, including Milan, Rome, and Turin | Medium term (2-4 years) |

| Increasing Energy Efficiency Regulations with ESG Mandates | +1.2% | National, with PNRR public-building activity concentrated in Central and Southern Italy | Long term (≥4 years) |

| Growing Adoption of Smart Building IoT Platforms | +1.0% | Northern Italy industrial and commercial corridors, with early adoption in Milan and Lombardy | Medium term (2-4 years) |

| Post-Pandemic Demand for Hygiene and Sanitation Services | +0.8% | National, with the strongest sustained effect in healthcare, institutional, and food-processing segments | Short term (≤2 years) |

| Public Infrastructure Privatization and PNRR-Linked Investment | +0.7% | Southern Italy for energy investment, and national for healthcare and judiciary estates | Medium term (2-4 years) |

| Rising Demand for Outsourced Non-Core Services in the Public Sector | +0.6% | National, driven by Consip FM4 aggregation across public administrations and universities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Strategic Shift from Single Service Outsourcing to Integrated FM

The Italy integrated facility management market is moving through a structural conversion phase because integrated contracts still accounted for only 26% of total FM revenue in January 2025 and that leaves a broad base of legacy single-service spending open to consolidation.[1]IFMA Italia, “IFMA Italia,” IFMA Italia This matters because fragmented contracting creates too many vendors, too many operating interfaces, and too little accountability when buyers need measurable service results across complex estates. Research from Politecnico di Milano supports that direction, showing that fragmented multi-vendor FM models can carry a higher total cost of ownership than integrated structures, which gives both finance teams and operating leaders a stronger case for service bundling. The shift is no longer limited to basic cost reduction, because public and private buyers increasingly want one provider to manage performance dashboards, asset visibility, service sequencing, and audit-ready reporting under one commercial framework. That is changing the shape of bidding in the Italy integrated facility management market, since providers that can combine soft services, technical services, digital tools, and verification methods are better placed to capture contracts that previously sat across separate procurement lots. Over time, this should lift contract duration, improve retention, and widen the gap between scale operators and firms that remain tied to narrowly defined service lines.

Increasing Energy Efficiency Regulations with ESG Mandates

Energy efficiency rules are becoming a direct source of demand in the Italy integrated facility management market, because regulation has moved from voluntary improvement toward mandatory action in both public and non-residential buildings.[2]European Parliament and Council, “Directive (EU) 2023/1791 on Energy Efficiency,” EUR-Lex Directive 2023/1791 requires a 1.9% annual reduction in final energy consumption for public entities against a 2021 baseline, and it extends the 3% annual renovation target across public entities that together cover an estimated 209 million m² of public building surface.[3]ODYSSEE-MURE, “Energy Efficiency and Public Building Renovation Data,” ODYSSEE-MURE Italy’s August 2024 CAM rules add another layer, because they require class B or higher automation, BEMS integration, BIM-based contract management, and at least 10% verified annual primary energy savings in first contracts, which means technical competence is now built into tender compliance rather than treated as an optional service add-on. ENEA’s 2025 building energy certification reporting adds urgency, since 56% of Italian public residential buildings were still rated in energy class F or G, showing the depth of the retrofit burden that remains in the national building stock. In practice, this gives Hard FM providers a clearer and more durable work pipeline across public assets, while also strengthening the case for outcome-based contracts that link facility management with measured energy results. It also explains why the Italy integrated facility management market is becoming more capability-led, because procurement now rewards proof of savings, system integration, and compliance management more than low standalone service pricing.

Growing Adoption of Smart Building IoT Platforms

Digital building tools are becoming a stronger differentiator in the Italy integrated facility management market, because owners now want energy, occupancy, and maintenance data to flow into daily service delivery rather than sit in disconnected technical systems. Politecnico di Milano’s smart building and IoT tracking showed that Italy’s smart building IoT segment reached EUR 1.37 billion (USD 1.55 billion), in 2024 and grew 6% year on year within a total Italian IoT market of EUR 9.7 billion (USD 11 billion), which shows that digital infrastructure is already moving beyond pilot stage. The best illustration in commercial real estate remains the Pirelli 35 transformation in Milan, where Siemens and COIMA completed a 45,000-square-meter retrofit by June 2025 that delivered 60% energy savings, cut annual CO₂ by 2,000 tons, and achieved LEED Platinum certification. That kind of project matters because it links integrated facility management directly to measurable asset performance, not just to service execution, and that raises the value of providers that can run connected building systems over time. At the same time, the adoption gap remains wide, because IFMA Italia reported that only 20% of Italian FM companies were using advanced monitoring tools and fewer than 10% had started AI-related projects, which leaves early movers with a real opening to capture premium contracts. The result is that digital maturity is starting to separate firms inside the Italy integrated facility management market, with better-positioned operators able to compete on performance evidence while others remain tied to labour-based and price-led scopes.

Post-Pandemic Demand for Hygiene and Sanitation Services

Post-pandemic hygiene standards continue to support the Italy integrated facility management market, because cleaning and sanitation are now treated as embedded service requirements in healthcare, institutional, and public-sector contracts rather than temporary emergency measures. The clearest example is ARIA’s healthcare FM framework for Lombardy, where a EUR 99.8 million (USD 112.8 million), program moved into contract awards in April 2026 and included building maintenance, environmental hygiene, and technical systems across hospital lots. This shows that hygiene is no longer being procured in isolation, because buyers increasingly package it with maintenance and service governance when they want tighter quality control across sensitive facilities. The same pattern appears in public administration procurement, where Consip FM4 and local adherence acts such as the Comune di Parma decree place environmental hygiene alongside plant maintenance and service verification within one monitored framework. That broader scope supports the Italy integrated facility management market by making soft services stickier within multi-year contracts, even when pricing stays under pressure. It also raises staffing pressure, because hygiene-heavy contracts still depend on labour availability at a time when broader shortages across technical and service roles are making workforce planning harder for operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and Price-Sensitive Market Dampening Competition | -1.4% | National, with the sharpest effect in Central and Southern Italy where SME operators dominate mid-market bids | Long term (≥4 years) |

| High Market Entry and Lifecycle Expenses for IFM Platforms | -1.0% | National, with a disproportionate effect on non-metropolitan operators without scale | Medium term (2-4 years) |

| Digital Transformation Capabilities Limiting Flexibility | -0.8% | National, with lower IoT penetration more visible in Southern Italy | Medium term (2-4 years) |

| Insufficient Labor Coverage | -0.6% | National, concentrated in Northern industrial and hospital corridors where technical skill demand is highest | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented And Price-Sensitive Market Dampening Competition

A major constraint on the Italy integrated facility management market is that a large share of the sector still operates through fragmented regional competition, where price remains the first screening tool and that weakens the business case for deeper capability investment. In that environment, many firms can still win smaller contracts without building the digital platforms, certification systems, and engineering depth that are needed for larger integrated mandates. Politecnico di Milano research also shows that fragmentation of systems is one of the most common barriers to ICT adoption in Italian FM settings, which means organizational complexity continues to slow change even when the technology itself is available. This has a direct effect on service quality, because contracts shaped too heavily by upfront price leave less room for BEMS installation, smart metering, certified energy management, and ongoing data verification. Public buyers are starting to respond by placing more weight on technical quality in some tender structures, yet that shift is still uneven across the country and has not fully displaced price-led buying behaviour. Until that balance changes more widely, the Italy integrated facility management market will keep showing a two-speed pattern, with a sophisticated top tier and a cost-driven middle layer.

Digital Transformation Capabilities Limiting Flexibility

Digital readiness remains a second major restraint on the Italy integrated facility management market, because contract requirements are advancing faster than the average provider’s ability to deliver them in a reliable and scalable way. Politecnico di Milano has described the wider Italian AECO field, including FM, as a moderate digital innovator with a fragmented enterprise base and limited innovation investment among smaller operators, which fits the structure visible in facility services. IFMA Italia’s 2024 findings make that gap clearer, since only 27% of Italian FM companies had a structured AI strategy and fewer than 10% had moved AI pilots into operational use, even while large public contracts were already demanding information systems, live registries, and monitored service workflows. The problem is no longer limited to productivity, because the NIS2 Directive expands cybersecurity obligations across critical sectors and that raises the operating threshold for FM providers that touch building management systems, access control, and sensor networks. Smaller firms can still compete in local and narrowly defined scopes, but they have less flexibility when clients want full integration across technical assets, digital controls, compliance reporting, and cyber-safe operating environments. This leaves the Italy integrated facility management market exposed to a widening capability divide between national-scale providers and firms that have not yet funded their digital transition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Facility Management Leads While Hard Facility Management Expands Faster

Soft Facility Management (FM) held 53.7% of the Italy integrated facility management (IFM) market share in 2025, while Hard FM is forecast to grow at a 7.4% CAGR through 2031. Soft FM stayed larger because it remains the usual starting point for outsourcing in public administration, healthcare, and corporate occupier settings, where cleaning, hygiene, reception, porterage, and routine support services are often the first scopes to move outside the organization. Hard FM is rising faster because energy rules, compliance obligations, and the age profile of Italian buildings are turning technical maintenance into a continuous operating need rather than a delayed capital decision. The 3% annual public-building renovation target and the broader energy reduction requirements across public entities support that shift by giving technical services a clearer demand base across schools, hospitals, and other state-owned estates. Within Hard FM, asset management and MEP services remain central because they sit closest to uptime, energy efficiency, and statutory compliance, while fire safety and security systems are gaining relevance as connected building infrastructure becomes more common.

Hard FM is also part of the Italy IFM market size that stands to benefit most from capability-led procurement during the forecast period. Cleaning and janitorial services still carry steady demand, because healthcare and institutional buyers continue to keep hygiene standards high inside contract specifications and service audits. Security services are also gaining ground as access control, surveillance, and technical systems are more often managed inside one operating model, which reduces handoffs and improves accountability for site performance. This is changing how the Italy IFM industry packages service bundles, because Soft FM operators now need stronger digital coordination and reporting tools if they want to protect contract scope against broader IFM rivals. Consip FM4 has reinforced that shift by making call-center support, asset registries, governance tools, and real-time monitoring part of contract execution rather than optional overlays. Academic work from Politecnico di Milano also supports the direction of travel, showing that IoT data linked to building management systems can improve FM efficiency, even if many organizations still struggle more with internal readiness than with the technology itself.

By End-User: Industrial Base Supports Scale While Commercial Space Grows Faster

The Industrial and Private Sector accounted for 38.6% of the Italy IFM market in 2025. This segment remains the largest because factories, energy assets, utilities, and other capital-intensive sites need coordinated maintenance, safety checks, plant reliability control, and compliance management across large and technically demanding portfolios. Buyers in this group also place a high value on integrated electrical, MEP, fire safety, and HSE oversight, which makes fragmented single-service contracts less practical once asset complexity rises. Retrofit activity across industrial sites adds another layer of demand, because energy upgrades require ongoing commissioning, monitoring, and verification after the physical work is completed, and those tasks fit naturally inside integrated technical FM. Pharmaceutical and food-processing facilities further support demand in the Italy integrated facility management industry, because hygiene discipline, process continuity, and audit readiness are embedded into facility operations and cannot be separated from daily service execution.

The Commercial segment is forecast to grow at a 7.2% CAGR, making it one of the clearest expansion pockets within the Italy IFM market size through 2031. Hybrid working has changed office utilization patterns, so providers are moving away from static service schedules and toward occupancy-responsive models that adjust cleaning, maintenance, and workspace support to actual building use. Retail, office, and logistics owners are also demanding more auditable performance data, because energy use, indoor environment quality, and tenant-facing service levels now influence asset positioning more directly than before. Public and institutional estates remain important as well, since PNRR-backed renovation activity supports demand across schools, judiciary buildings, and other public assets that need bundled technical and support services over long delivery windows. The Other segment remains smaller in revenue terms, but premium residential, entertainment, and sports facilities are adopting more formal service models as owners look for tighter control of cost, asset condition, and operating standards. This is also pushing the Italy integrated facility management industry toward more flexible labour planning and more data-led service design in end-user settings where occupancy and usage patterns change more often than they did before 2024.

Geography Analysis

Northern Italy accounted for an estimated 55%-60% of Italy IFM market share in 2025. Lombardy, Piedmont, Liguria, and Veneto dominate the national picture because they contain the highest concentration of corporate headquarters, industrial facilities, logistics corridors, and high-value commercial real estate. That mix gives the Italy integrated facility management market its largest volume base in the north, and it also raises average contract complexity because buyers there are more likely to request integrated technical, digital, and support services under one operating model. Veneto’s adherence to Consip FM4 Lot 5, valued at EUR 8.5 million, or USD 9.6 million, over six years shows how regional administrations are shifting from bilateral maintenance structures toward digitally governed multi-service frameworks. Milan further strengthens Northern Italy’s lead, because projects such as the Pirelli 35 retrofit show that commercial owners are willing to fund integrated building intelligence when energy savings and certification outcomes are visible and measurable.

Central Italy represented an estimated 25%-30% of national activity in the Italy integrated facility management market. Rome supports that position through its concentration of public administration buildings, while Tuscany adds healthcare and museum assets that require structured upkeep and energy-focused modernization. ENGIE Italia’s January 2026 contract with the Municipality of Florence covers more than 400 public buildings, including 152 schools and 7 museums, with nearly EUR 20 million (USD 22.6 million), in planned investment and targeted reductions of 30% in thermal consumption and 23% in electrical consumption. That profile gives Central Italy a stable pipeline, because large public estates with weaker energy performance are being drawn into formal renovation and service programs under EU and national policy pressure.

Southern Italy and the islands held an estimated 15%-20% share, so this region still starts from a smaller private-sector base within the Italy integrated facility management market. The growth outlook is stronger than the starting share suggests, because national and cohesion funding is increasingly directed toward energy upgrades, hospital projects, and public infrastructure renewal in southern regions. Impresa Pizzarotti’s EUR 114 million (USD 132.6) PNRR contract with INVITALIA for hospital construction and eco-sustainable building requalification across Lombardy, Liguria, Emilia-Romagna, Tuscany, and Sicily shows that these pipelines are moving from planning into execution. As those programs progress, the regional mix of the Italy integrated facility management market should become less concentrated in the north, even if Northern Italy remains the national volume center through the forecast period.

Competitive Landscape

The Italy integrated facility management market is moderately concentrated at the top end, but it remains widely fragmented below that level. Rekeep S.p.A., Apleona Italy, Engie Servizi, Dussmann Service, and ISS Facility Services compete for the largest public and corporate mandates, while a broad layer of smaller regional operators continues to serve local and sub-threshold contracts where scale is less decisive. Rekeep reported FY2024 revenue of EUR 1.26 billion (USD 1.4 billion), a backlog of EUR 2.7 billion (USD 3.05 billion), and a return to net profit at EUR 1.2 million (USD 1.36 million), after the FY2023 loss, which confirms its position as the largest domestic-scale operator in the field. The company also launched H2H Digital Solutions S.r.l. and H2H Document Solutions S.r.l. in October 2024, showing that it is trying to widen its role from traditional service provision into digital FM and document-linked support for private and healthcare clients. Apleona Italy has taken a similarly targeted route, using its positions in SIE4 and FM4 to align itself with energy-performance contracting and public-sector efficiency programs that increasingly shape large IFM awards.

In the Italy integrated facility management market, technology capability is becoming a more visible dividing line between firms that can pursue complex contracts and firms that cannot. Consip FM4 requires information systems, technical asset registries, and real-time service monitoring, so digital governance is now part of the base operating requirement in large public contracts rather than a premium differentiator. NIS2 raises the threshold further, because providers involved with building systems, sensor networks, and access-control environments need stronger cybersecurity governance and documented response capability. This makes platform investment, interoperability, and compliance management much more important in competition, while smaller firms often remain confined to narrower scopes, local subcontracting, or price-led contracts if they cannot fund that transition.

Strategic moves in 2025 and 2026 show that leading firms are expanding by geography, service breadth, and project type in the Italy integrated facility management market. Rekeep entered Uzbekistan in May 2026 through a consortium contract for the design, construction, and management of a hospital in the Fergana region, extending its healthcare capability beyond its existing operating base. ISS strengthened its multinational account position through a December 2025 expansion with a European financial services customer and through a seven-year global integrated FM contract with COWI, both of which support its role in large cross-border mandates. ENGIE Italia’s public-building energy efficiency program in Florence also shows how major operators are using performance-led municipal projects to deepen local capability, strengthen public references, and build longer-term service visibility in Italy.

Italy Integrated Facility Management Industry Leaders

Rekeep S.p.A.

Coopservice Società Cooperativa per Azioni

ISS Facility Services S.r.l.

Sodexo S.A.

CBRE Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Rekeep S.p.A. entered the Uzbekistan market through a new consortium contract for the design, construction, and management of a hospital in the Fergana region, marking the group's first operational footprint in Central Asia and extending its healthcare FM capability beyond its existing Italy, Poland, France, Turkey, and Middle East operations.

- April 2026: ARIA (Azienda Regionale per l'Innovazione e gli Acquisti S.p.A.) awarded multiple lots of its EUR 99.8 million (approximately USD 112.8 million) healthcare FM framework for Lombardy's Servizio Sanitario Regionale, with Lot 2 going to ELETECNO ST S.p.A., Lot 3 to Axioma Energy Services S.r.l., and Lot 5 to VEOLIA ITALIA S.p.A., the framework covers building and systems maintenance for major hospital and cancer research entities across the region.

- January 2026: ENGIE Italia secured a contract with the Municipality of Florence for energy efficiency improvements across more than 400 public buildings, including 152 schools and 7 museums, at a total investment of nearly EUR 20 million (approximately USD 22.6 million), with projected outcomes of 30% thermal and 23% electrical consumption reductions and more than 45,000 tons of CO₂ avoided annually.

- January 2026: Veneto Region commenced services under its Consip FM4 Lot 5 adherence agreement with Engie Servizi S.p.A. and consortium partners, valued at EUR 8.52 million (approximately USD 9.63 million) over six years, covering governance, maintenance, and digital monitoring services across regional administration buildings, elevator maintenance commences in December 2026 upon expiry of the existing TK Elevator Italia agreement.

Italy Integrated Facility Management Market Report Scope

The Italy Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the projected value of the Italy integrated facility management space by 2031?

It is projected to reach USD 15.9 billion by 2031, up from USD 10.9 billion in 2025, with a 6.7% CAGR during 2026-2031.

Which service category is growing fastest in Italy integrated facility management?

Hard FM is the fastest-growing service category, with a projected 7.4% CAGR through 2031, supported by energy compliance, technical maintenance needs, and public-building renovation programs.

Why does Soft FM still hold the largest 2025 share in Italy?

Soft FM led with 53.7% share in 2025 because outsourcing often starts with cleaning, hygiene, and support services, especially in public administration, healthcare, and institutional settings.

Which end-user group generates the most demand in Italy?

The Industrial and Private Sector was the largest end-user segment in 2025 with 38.6% share, driven by technically demanding facilities that need integrated maintenance, safety, and compliance support.

Which part of Italy creates the most facility management volume today?

Northern Italy remains the main volume center, with an estimated 55%-60% share, supported by its concentration of headquarters, factories, logistics assets, and complex commercial buildings.

What is the biggest risk to delivery over the forecast period?

The most important operating risk is the shortage of technical labour in roles tied to HVAC, electrical maintenance, and IoT-enabled building services, which can slow execution even when demand remains strong.

Page last updated on: