Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

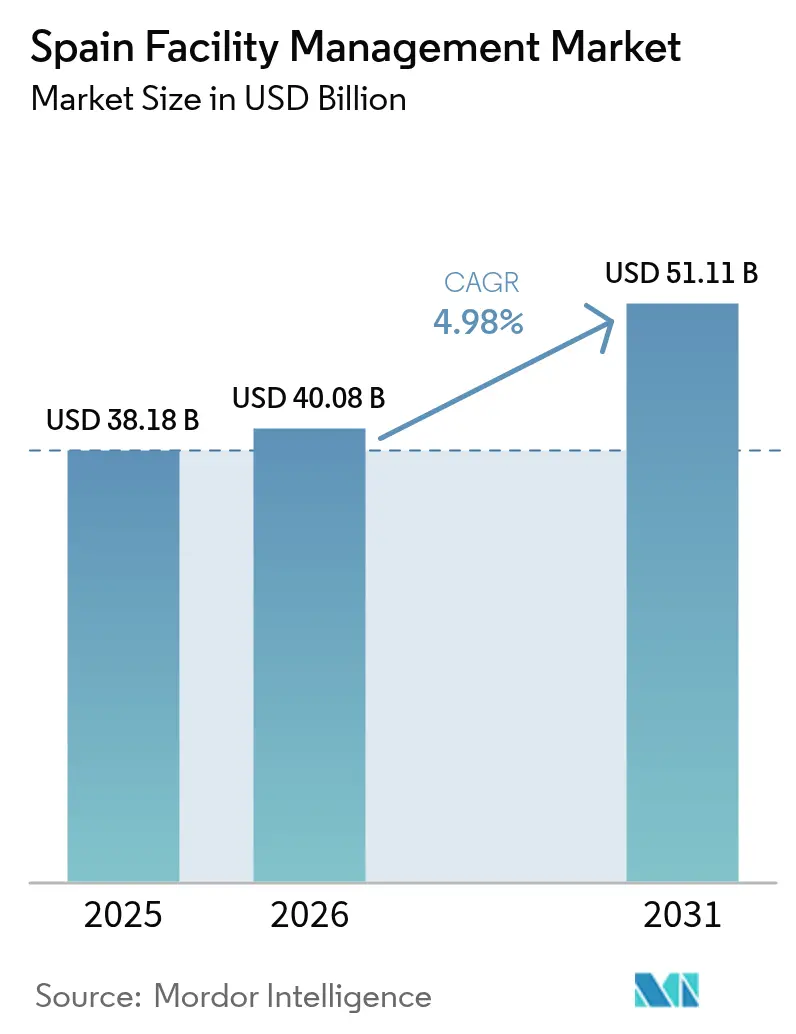

| Base Year Market Size (2025) | USD 38.18 Billion |

| Market Size (2026) | USD 40.08 Billion |

| Market Size (2031) | USD 51.11 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

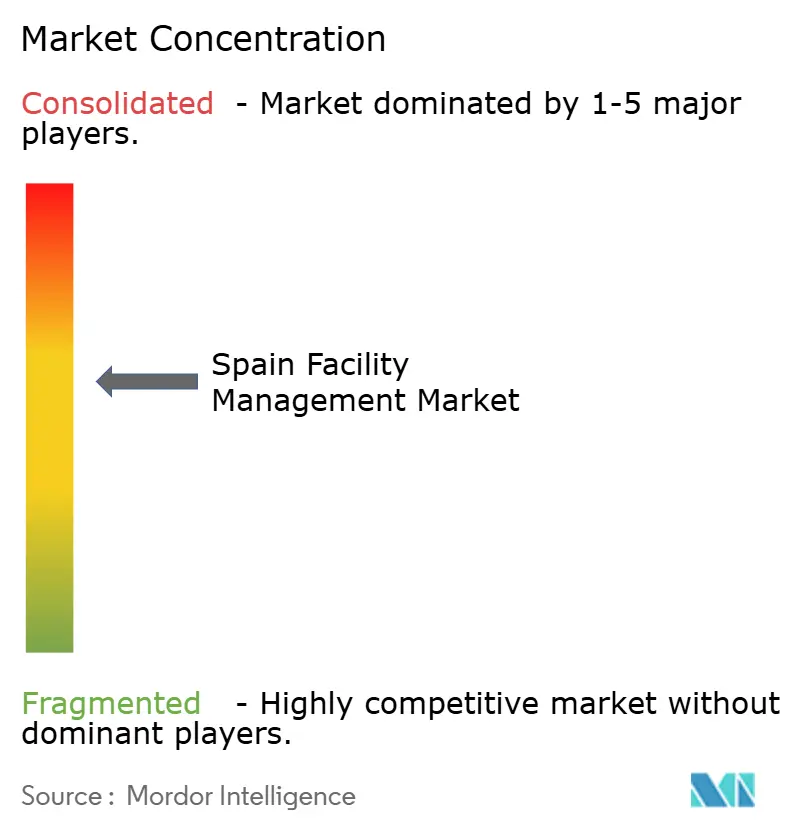

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Facility Management Market Analysis by Mordor Intelligence

The Spain facility management market size is expected to grow from USD 38.18 billion in 2025 to USD 40.08 billion in 2026 and is forecast to reach USD 51.11 billion by 2031 at 4.98% CAGR over 2026-2031. Robust NextGenerationEU allocations, growing smart-building adoption and higher outsourcing penetration underpin this trajectory. Hard services dominate today because Spain’s aging building stock requires HVAC, MEP and fire-safety upgrades to meet European energy directives. Soft services are gaining momentum as hybrid work models elevate employee-experience priorities, while electricity-price volatility strengthens the business case for specialist energy-efficiency solutions. A steady pipeline of public-private partnership infrastructure projects and data-center construction deepens long-term demand, yet rising labor costs and short-term energy-price swings tighten provider margins. Competitive intensity remains moderate but consolidation pressure is rising as scale, technology capability and ESG credentials become decisive for major contract awards.

Key Report Takeaways

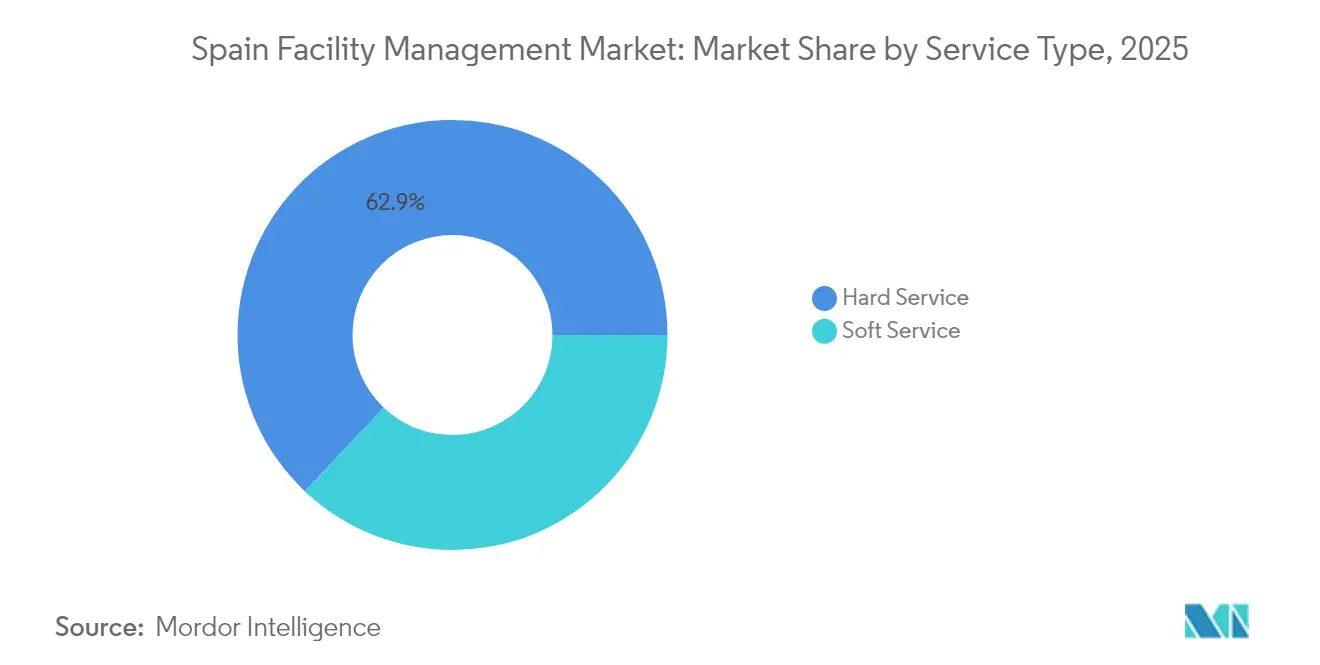

- By service type, hard services led with a 62.94% share of Spain facility management market size in 2025, whereas soft services are projected to post the fastest 5.08% CAGR through 2031.

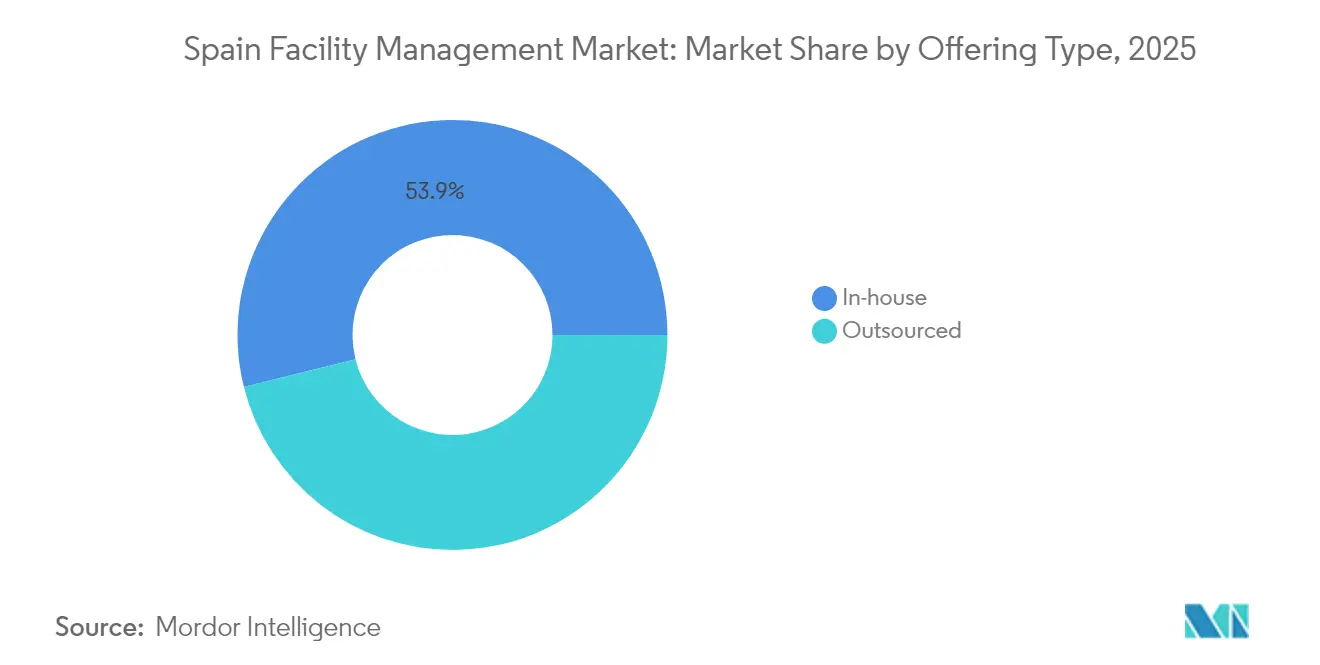

- By offering type, in-house operations accounted for 53.89% of Spain facility management market share in 2025; the outsourced model is forecast to grow at a 5.21% CAGR to 2031.

- By end-user industry, the commercial segment held 41.11% revenue share in 2025 and is set to expand at a 5.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward integrated FM contracts among large enterprises | +1.2% | Madrid, Barcelona, Valencia and other national hubs | Medium term (2-4 years) |

| Hospitality and tourism rebound | +0.8% | Coastal regions, Balearic Islands, Canary Islands, major cities | Short term (≤ 2 years) |

| E-commerce logistics and data-center expansion | +1.0% | Madrid, Barcelona, Valencia, Zaragoza corridors | Medium term (2-4 years) |

| PPP social-infrastructure projects | +0.7% | Andalusia, Catalonia, Madrid and nationwide | Long term (≥ 4 years) |

| NextGenerationEU retrofit funding | +1.1% | Northern regions with older stock and nationwide | Medium term (2-4 years) |

| Flexible-workspace micro-contracts | +0.5% | Madrid, Barcelona, Valencia, Bilbao urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift toward integrated facility management (IFM) contracts among large enterprises

Spanish corporations are consolidating multiple vendors into single-source IFM agreements to gain real-time building analytics, unified service levels and ESG compliance assurance. A notable case is Hotelatelier, which achieved an 88% guest-satisfaction index after switching to an integrated model that merges HVAC optimization with front-of-house service orchestration. [1]“Driving Results: How Reputation Management Transformed Customer Experience and Revenue,” Hospitality Net, hospitalitynet.org The move is strongest in multi-site office portfolios, but hospital and data-center operators are also beginning to bundle technical and soft scopes to improve uptime and simplify governance. Greater contract size and duration improve provider revenue visibility, yet require advanced digital-platform and change-management capability to meet stringent key-performance indicators.

Hospitality and tourism rebound

Spain welcomed a sharp rise in international arrivals in 2024 and early 2025, restoring room-occupancy levels in the Balearic and Canary Islands as well as the Costa del Sol. Hotels outsource cleaning, security and concierge functions to withstand seasonal labor swings and focus on guest experience technologies such as automated check-in, which reached 60% adoption at Kora Living properties. Sustainability targets linked to NextGenerationEU retrofits further widen the service scope to include energy benchmarking and waste-reduction programs. Outsourcing peaks during peak travel months, reinforcing the need for agile contract structures and performance-based pricing mechanisms.

E-commerce logistics and data-center expansion

Spain’s logistics corridors and metropolitan campuses host a growing fleet of automated warehouses and hyperscale data centers, spurred by EUR 300 billion (USD 320 billion) regional pipeline investments from contractors such as ACS, Acciona and Ferrovial. [2]“ACS, Acciona y Ferrovial se lanzan a por 300.000 millones en ‘data centers’,” Expansión, expansion.com Facilities demand 24/7 HVAC, critical-power monitoring and ISO-trained technical personnel, creating premium revenue pools for hard-service specialists. Predictive maintenance, IoT-enabled asset registers and remote-command centers shift delivery from reactive repair to uptime assurance, raising average contract values. The trend clusters around Madrid’s Getafe-Illescas axis, Barcelona’s El Prat hub and Valencia’s Sagunto logistics district.

PPP social-infrastructure projects

Municipalities increasingly package lifecycle facility management into twenty-to-thirty-year PPP concessions covering hospitals, schools and municipal arenas. The Madrid 12 de Octubre Hospital expansion illustrates the model, embedding long-term MEP maintenance targets alongside construction milestones. [3]“Public-Private Partnership in Spanish Local Governments,” Springer, link.springer.com Providers gain stable recurring cash flows but also assume stringent penalty clauses tied to availability and energy-performance metrics. EU-funded climate-adaptation programs amplify the opportunity set in Andalusia and Catalonia, where aging public buildings require deep retrofits and structured performance guarantees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labor costs under new collective-bargaining agreements | -0.9% | Catalonia, Basque Country, Madrid and nationwide | Short term (≤ 2 years) |

| Volatile energy prices | -0.7% | Industrial regions and nationwide | Short term (≤ 2 years) |

| Legacy building stock with poor documentation | -0.4% | Historic city centers nationwide | Long term (≥ 4 years) |

| Chronic late payment in public sector | -0.3% | Regional-government contracts nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising labor costs under new collective-bargaining agreements

The V Agreement for Employment and Collective Bargaining mandates wage increases of 4% for 2025, lifting the largest cost element in Spain facility management market contracts. Providers whose revenue mix tilts toward soft services face the greatest exposure because automation options are limited, while regional wage differentials intensify margin pressure in Catalonia and the Basque Country. Companies respond by accelerating robotics in cleaning, renegotiating service-level scopes and bundling services to dilute overhead.

Volatile energy prices

Electricity tariffs are projected to rise 13% in 2025 after higher system charges and grid-reinforcement levies under Real Decreto-ley 7/2025. Hard-service contracts covering HVAC, boiler maintenance and street lighting suffer immediate cost swings, especially when price-escalation clauses are absent. Providers mitigate exposure through energy-performance contracts, on-site solar deployment and digital sub-metering that identifies waste for rapid corrective action.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Market Foundation

Hard services commanded 62.94% of Spain facility management market size in 2025, mirroring the imperative to modernize decades-old HVAC, electrical and fire-safety installations. Asset-management subcontracts dominate as owners deploy predictive analytics to counter unplanned downtime. A chemical plant in Murcia cut energy use by almost 50% over ten years after pairing energy-management and maintenance-management systems. Technical-service providers secure multiyear agreements that couple capital-expenditure planning with day-to-day operations and maintenance tasks, improving revenue stability.

Soft services are forecast to outpace at 5.08% CAGR, fueled by hybrid workplaces and hospitality recovery. Security and office-support functions gain complexity as occupancy fluctuates weekly, prompting demand for access-control integrations and desk-booking analytics. Cleaning contracts face cost headwinds from wage inflation but also benefit from sensor-driven scheduling that aligns labor hours with real-time footfall. Catering rebounds on return-to-office trends and tourism demand, although menu-cost pressure from food inflation necessitates dynamic pricing models.

By Offering Type: Outsourcing Gains Momentum

In-house delivery still controls 53.89% of Spain facility management market share in 2025, anchored in sectors with sensitive data or patient-care requirements. Large banks and hospital groups keep strategic oversight while subcontracting specialized hard-services tasks that demand certifications. Cost creep, talent shortages and digitization gaps are prompting board-level reviews of legacy in-house models.

The outsourced model is expanding at a 5.21% CAGR as CFOs prioritize variable-cost structures. Single-service contracts remain an entry point, yet bundled and integrated FM formats are scaling quickly because they cut procurement cycles and harmonize key-performance metrics. Providers with national coverage and robust vendor-management systems win multi-region mandates, illustrating a shift from price-based tenders to capability-based selection.

By End-user Industry: Commercial Sector Leads Growth

Commercial real estate captured 41.11% of market revenue in 2025 and is on track for a 5.3% CAGR through 2031. Hybrid office adoption drives space re-stacking, sensor-based energy management and tenant-experience apps that slot seamlessly into hard- and soft-service offerings. Data-center ramps in Madrid and Barcelona boost demand for Tier III and Tier IV facility-operations expertise signed under uptime-linked SLAs.

The hospitality segment is rebounding on tourism tailwinds, pushing demand for housekeeping automation, touchless guest services and LEED-aligned energy retrofits that lower operating expenses. Institutional and public-infrastructure clients provide predictable long-term revenue via PPP frameworks, while healthcare facilities maintain premium pricing due to stringent compliance and critical-care uptime standards. Industrial plants target predictive-maintenance roadmaps and compressed-air optimization to cushion energy volatility.

Geography Analysis

Spain facility management market value clusters around Madrid, Barcelona and Valencia, which together generated nearly 59% of 2025 contract spend. Madrid hosts multinational headquarters, ministries and a growing colocation-data-center footprint, generating steady integrated FM pipelines. Barcelona couples port logistics and life-science clusters with tourism-driven soft-service peaks, while Valencia’s Mediterranean logistics hub sparks warehouse-maintenance and security contracts.

Northern regions such as the Basque Country and Catalonia are accelerating facility upgrades using NextGenerationEU grants for energy-efficient retrofits, bolstering hard-service volumes. The Balearic and Canary Islands exhibit seasonal demand spikes tied to tourism cycles, favoring flexible workforce models and short-notice micro-contracts. Andalusia’s broad economic base, including agriculture processing and solar farms, sustains year-round technical-service needs and PPP hospital concessions.

Secondary cities including Zaragoza, Seville and Bilbao are emerging growth nodes as logistics investment, urban-renewal schemes and renewable-energy projects expand. Smart-city programs foster demand for IoT-enabled street-lighting, waste-management and mobility-hub maintenance, thereby widening the addressable opportunity beyond core metros. Providers with national branch networks and unified digital platforms are best positioned to capitalize on the geographic dispersion of opportunity.

Competitive Landscape

Spain facility management market remains moderately fragmented, with no single provider exceeding a double-digit share. Global firms such as ISS leverage data-driven platforms and cross-border procurement to win multi-site contracts, reporting USD 12.1 billion global revenue in 2024. Local champions like ILUNION post USD 1.22 billion revenue and differentiate through inclusive-employment models and regional intimacy. Construction conglomerates continue to divest service arms; ACS’s planned sale of Clece, valued at up to USD 961 million, underscores capital-allocation shifts toward core infrastructure concessions.

Technology is the frontline of competition. IoT retrofits across 370 Spanish buildings showcase how remote-monitoring dashboards and digital twins cut energy bills and fault-diagnosis time. Providers able to integrate building-management systems with ESG reporting are favored by multinational clients bound by EU taxonomy disclosure. Scale procurement, standardized workflows and cybersecurity safeguards further separate leaders from regional independents.

Consolidation is expected to intensify as private-equity funds target predictable cash flows and cross-sell synergies. Service breadth, contract-portfolio diversity and balance-sheet resilience will therefore decide winners in the next investment cycle. Providers lacking digital capability or multi-region reach risk marginalization to subcontract status within integrated FM ecosystems.

Spain Facility Management Industry Leaders

Licuas SA

CBRE

Sacyr Facilites

The Mail Company

LD Facility

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PAI Partners pursues acquisition of Avanta and Aspy to create a leading labor-risk-prevention group exceeding USD 53.4 million pro-forma EBITDA and USD 534 million deal value.

- June 2025: Indra negotiates sale of its BPO division to Servinform for USD 107 million; the asset contributes USD 16 million EBITDA, reinforcing Servinform’s digitalization scope in energy and telecom verticals.

- April 2025: AS Equity Partners acquires 60% of Servinform to fund international expansion in BPO solutions.

- April 2025: CBRE posts 16% rise in facilities-management net revenue for Q1 2025 as technology and life-science clients expand portfolios.

- February 2025: Clariane achieves USD 131 million Spain revenue with 13.9% organic growth, lifting EBITDAR margin to 19.2%.

Spain Facility Management Market Report Scope

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres. Hard services comprise mechanical and electrical maintenance, fire safety and emergency services, building management systems controls, elevator/lifts and conveyer maintenance, etc. Soft services include cleaning, recycling, security, pest control, handyman services, ground maintenance, and waste disposal. Both in-house facility management and outsourced FM services are considered in the scope.

The Spain facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Spain facility management market?

The market was valued at USD 40.08 billion in 2026 and is projected to reach USD 51.11 billion by 2031 at a 4.98% CAGR.

Which service type holds the largest share?

Hard services led with a 62.94% share in 2025, reflecting significant demand for HVAC, MEP and fire-safety upgrades.

Why is outsourcing gaining traction in Spain facility management market contracts?

Organisations seek variable-cost structures, advanced technology and multi-service coordination, driving outsourced models at a 5.21% CAGR through 2031.

Which end-user segment is the fastest growing?

The commercial sector is expanding at a 5.3% CAGR owing to hybrid-workspace optimisation and data-center growth.

How do energy-price fluctuations affect FM providers?

A forecast 13% electricity-price rise in 2025 compresses margins on energy-intensive contracts, prompting efficiency retrofits and energy-performance clauses.

What is the competitive outlook for the market?

Moderate fragmentation persists, but digital capability and scale are poised to trigger consolidation as providers vie for integrated IFM contracts.

Page last updated on: