Mexico Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

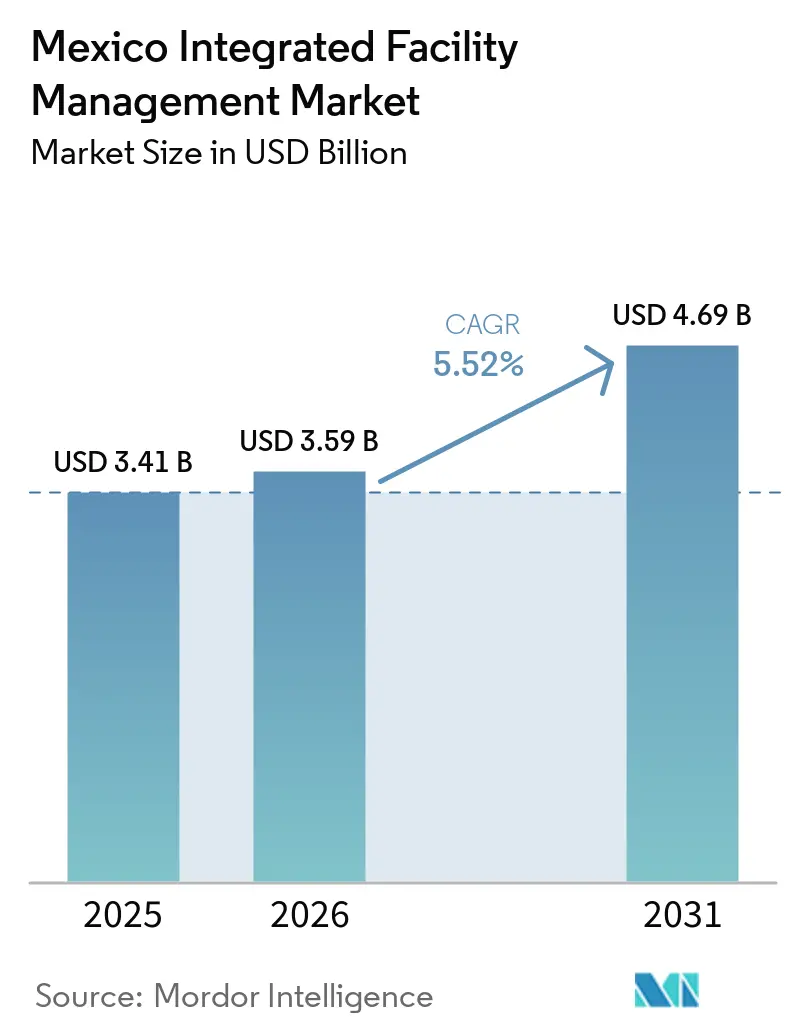

| Base Year Market Size (2025) | USD 3.41 Billion |

| Market Size (2026) | USD 3.59 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Integrated Facility Management Market Analysis by Mordor Intelligence

The Mexico integrated facility management market size was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.59 billion in 2026 to reach USD 4.69 billion by 2031, at a CAGR of 5.52% during the forecast period 2026-2031. The Mexico integrated facility management (IFM) market is expanding because enterprises are moving non-core functions into bundled service contracts that cover maintenance, cleaning, security, and energy management under one operating model. Nearshoring continues to widen the installed base of factories, logistics sites, and commercial assets, which keeps recurring demand firm across technical and support services in the Mexico integrated facility management market. Compliance obligations, uptime standards, and digital building systems are also pushing buyers toward providers that can deliver hard and soft services through a single governance structure. Skilled labor shortages and higher electricity costs are tightening delivery economics, yet those same pressures are increasing demand for predictive maintenance, energy optimization, and stronger contract oversight in the Mexico IFM market.

Key Report Takeaways

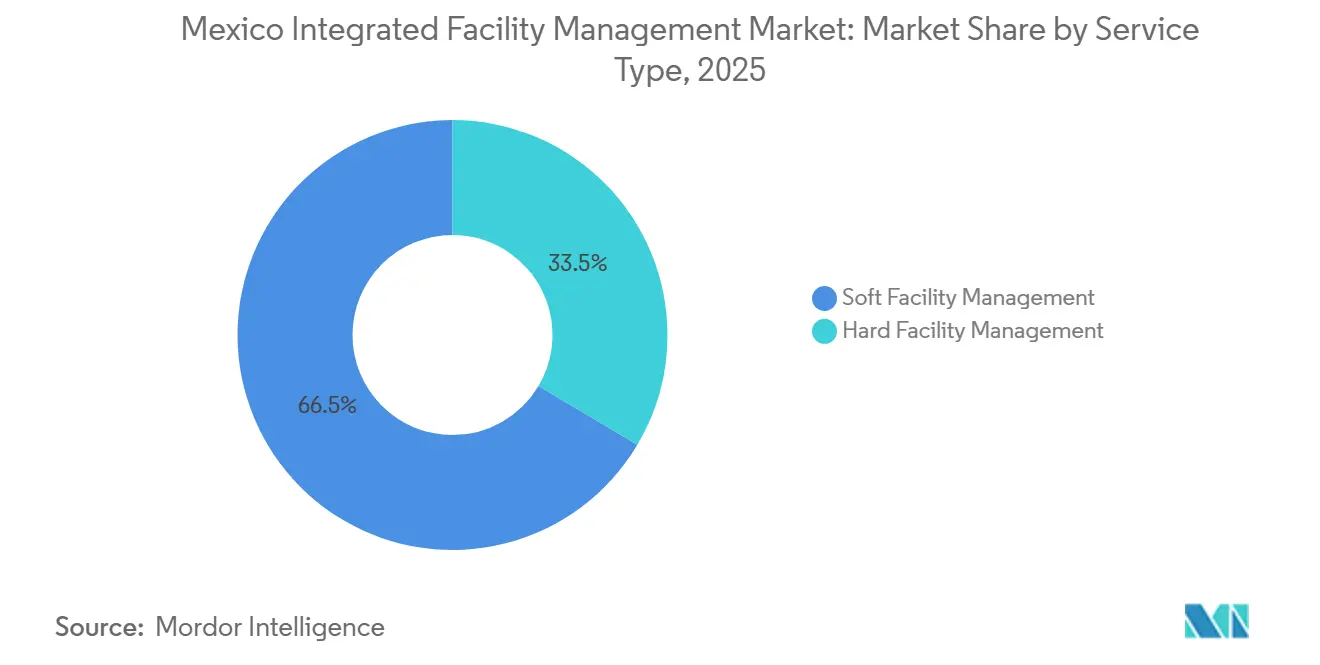

- By service type, Soft Facility Management (soft FM) led with a 66.47% share of the Mexico integrated facility management market in 2025, while Hard Facility Management (hard FM) recorded the fastest projected growth at a 6.04% CAGR through 2031.

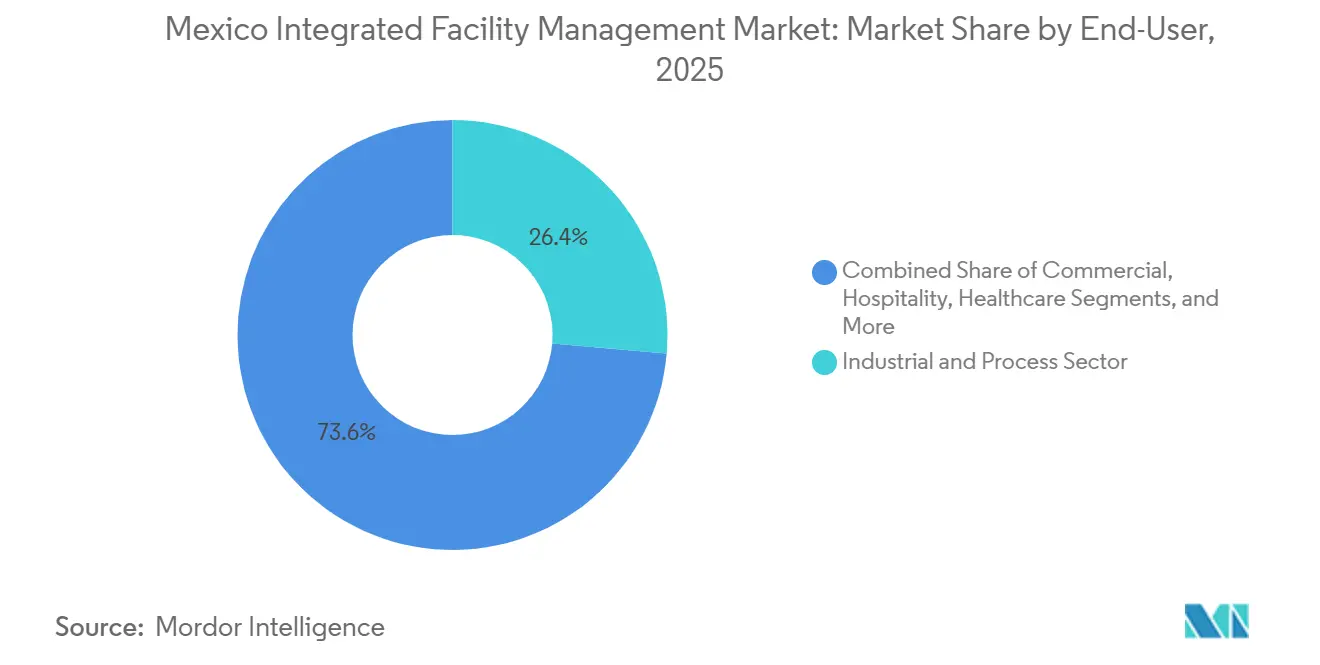

- By end user, industrial and process held a 26.37% share of the Mexico integrated facility management (IFM) market in 2025, while commercial is forecast to expand at a 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing Of Facility Management And Strategic Delegation Of Non-Core Services | +2.0% | Global, highest concentration in Mexico City, Monterrey, Guadalajara | Short term (≤ 2 years) |

| Smart Building And IoT Adoption For Efficiency And Energy Optimization | +1.3% | Mexico City, Monterrey, Guadalajara, Tijuana | Medium term (2-4 years) |

| Nearshoring-Led Industrial And Commercial Expansion | +1.0% | Monterrey, Querétaro, Saltillo, Tijuana, Bajío corridor | Short term (≤ 2 years) |

| Occupational Safety Standards And Compliance Requirements | +0.5% | National, early gains in Nuevo León, Guanajuato, Chihuahua | Medium term (2-4 years) |

| Shift From Business Continuity To Intelligent Organizational Goals | +0.3% | Mexico City and major commercial centers | Medium term (2-4 years) |

| AI And Data-Centric Analytics For Predictive Maintenance | +0.2% | Mexico City, Monterrey, Querétaro | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Of Facility Management Converts Operating Cost into Strategic Value

Outsourcing is gaining ground because buyers now treat facility management as an operating lever instead of a stand-alone expense line. The Mexico integrated facility management (IFM) market is benefiting from contracts that combine cleaning, maintenance, security, and energy oversight inside one measurable service framework. Clients are also moving away from many small vendor relationships because integrated governance improves accountability and reduces coordination gaps across large sites. Mexico’s REPSE framework has reinforced this shift by making subcontracting compliance more demanding for end users that manage specialized services directly.[1]Secretaría del Trabajo y Previsión Social, “REPSE And Specialized Service Compliance,” Gobierno de México, gob.mx In practice, larger integrated providers are better placed to absorb documentation, labor, and audit obligations on behalf of customers. That is raising the appeal of multi-year outsourced agreements across offices, industrial parks, healthcare facilities, and education networks in the Mexico IFM market.

Smart Building and IoT Adoption Reshapes Facility Operations

Digital building systems are changing how service scope is defined inside the Mexico integrated facility management market. Green-certified offices and modern commercial assets increasingly require providers to manage building automation, sensors, connected access control, and energy performance tools as part of daily operations. Johnson Controls’ retrofit of Torre Mayor involved more than 6,000 monitored control points across HVAC, lighting, and security systems, which shows how technical the maintenance layer has become.[2]Johnson Controls, “Advancing energy efficiency and sustainability at Torre Mayor through HVAC and BAS upgrades,” Johnson Controls, johnsoncontrols.com Siemens and Microsoft also announced a 2025 collaboration linking Building X with Azure IoT Operations, reducing integration effort by up to 80% and lowering a key adoption barrier for connected building services. As integration costs fall, the same digital capabilities are likely to move from premium towers into mid-tier commercial and industrial properties. This supports higher-value contracts in the Mexico integrated facility management (IFM) market because providers are no longer judged only on labor execution, but also on system visibility, energy control, and uptime performance.

Nearshoring And Industrial Expansion Sustain Critical FM Demand

Nearshoring continues to enlarge the addressable base for the Mexico integrated facility management (IFM) market because every new industrial asset adds long-term maintenance and support requirements. Industrial parks need electrical upkeep, HVAC servicing, civil maintenance, fire safety readiness, and security operations from the point of commissioning. AMPIP projected that nearshoring could generate up to 8 million square meters of new industrial space by 2027, which points to a durable flow of service demand rather than a temporary build cycle. Demand is also spreading beyond legacy border locations into corridors such as Monterrey, Querétaro, Saltillo, Tijuana, and the Bajío region. This geographic broadening matters because it creates a larger renewal base for national providers that can mobilize teams across several states. The Mexico integrated facility management market is therefore gaining from industrial expansion not only through new site openings, but also through the recurring service intensity of more complex facilities.

Occupational Safety and Compliance Raise The Value Of Formal FM Programs

Compliance requirements are making informal or lightly managed service models harder to sustain in the Mexico IFM market. NOM-001-STPS-2008 requires safe building conditions, documented inspections, and maintenance records that must be retained for 12 months, while structural safety assessments must be renewed every 5 years or after seismic events. The 2024 publication of NOM-006-STPS-2023 also added a mandatory inspection and maintenance program for material-handling machinery used in warehouses and industrial facilities. Penalties under NOM-001-STPS-2008 range from 50 to 5,000 UMA units per violation, which makes non-compliance a direct operating risk for companies that self-manage technical building functions. STPS’s 2025 Federal Labor Inspection Program covered 43,000 inspections nationwide and used AI-based scheduling systems, which signals firmer enforcement rather than symbolic oversight. This environment supports established providers in the Mexico integrated facility management market because certified documentation, preventive routines, and audit readiness have become part of the value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Scarcity In Technical FM Roles | -0.8% | National, most acute in Nuevo León, Chihuahua, Baja California | Short term (≤ 2 years) |

| Rising Energy Costs And Service Delivery Challenges | -0.5% | National, most severe in Centro Occidente, Jalisco, Centro Sur | Medium term (2-4 years) |

| Price Competition And Margin Compression | -0.4% | National, concentrated in Mexico City and Monterrey | Short term (≤ 2 years) |

| Fragmented Maintenance Standards And Uneven Enforcement Across States | -0.2% | National, with variation across Mexico’s 32 states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Scarcity Limits Delivery Capacity

Labor remains the clearest operating constraint on the Mexico integrated facility management market. As of early 2026, 67% of Mexican employers reported difficulty filling key roles, with manufacturing and operations positions among the hardest to staff.[3]ManpowerGroup Mexico, “Talent Shortage Findings for Mexico,” ManpowerGroup, manpowergroup.com.mx That shortage reaches directly into electricians, HVAC technicians, fire safety specialists, controls engineers, and other trades needed for integrated FM delivery. When wage inflation in those roles moves faster than contract escalators, providers face margin pressure even when revenue growth stays healthy. The result is slower ramp-up on new contracts, tighter scheduling, and a greater need for apprenticeship pipelines and certification-led training. The Mexico IFM market will keep growing, but firms that secure technical labor early will have a clear advantage over operators that still treat labor as a flexible commodity.

Rising Energy Costs and Service Delivery Challenges Pressure Margins

Energy costs are another structural restraint because many contracts in the Mexico integrated facility management market include HVAC, power systems, and energy-intensive operating hours. CFE’s 2025 tariff adjustments raised electricity costs by 8%-12% for large industrial consumers in the GDMTH and DIST categories, which increased delivery costs for FM providers serving factories and large campuses. Service execution is also harder where power quality and grid connection delays affect industrial timelines and asset performance. AMPIP reported that 91% of industrial parks encountered electricity supply issues, posing risks to uptime commitments and complicating maintenance planning. Providers are addressing these challenges through energy-as-a-service models, backup power strategies, and enhanced load profile monitoring. Schneider Electric’s EcoStruxure Energy Hub, launched in Mexico in 2024, claimed up to 50% lower software-related OPEX and up to 25% lower implementation costs than conventional building management setups, which shows why energy optimization is moving closer to the center of the Mexico integrated facility management (IFM) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Advances While Soft FM Keeps Scale Leadership

Hard Facility Management (Hard FM) is the fastest-growing service category in the Mexico integrated facility management market, with a 6.04% CAGR projected through 2031. Technical maintenance scope is widening because industrial and commercial assets now depend on more advanced electrical systems, HVAC controls, fire protection equipment, and connected building infrastructure. Preventive and corrective maintenance are also becoming more frequent because multinational occupiers expect tighter uptime standards across Mexico operations. Johnson Controls’ 2024 Torre Mayor retrofit and its 2025 access-control deployment at Puerta Polanco show how one facility contract can now span automation, security, and operational continuity rather than one isolated task. This is pushing the Mexico integrated facility management industry toward higher skill density, stronger digital oversight, and more measurable technical outcomes.

Soft Facility Management (Soft FM) held 66.47% of the Mexico integrated facility management (IFM)market share in 2025, which kept it as the largest service segment. Cleaning remained the largest soft FM sub-segment, supported by healthcare, education, corporate, and public-sector demand patterns. The IPN awarded a MXN 2.3 billion contract, equivalent to USD 115 million, for national cleaning services in May 2025, which reflects the scale and duration that soft FM procurement can reach in Mexico. Catering, office support, and security services are also benefiting from higher occupancy expectations and standardized service requirements across multi-site portfolios. A gradual shift toward outcome-based pricing is improving revenue quality in the Mexico IFM market because buyers are increasingly paying for audit performance, cleanliness consistency, and user satisfaction instead of labor inputs alone.

By End User: Industrial Demand Anchors Volume While Commercial Use Cases Broaden

Industrial and Process accounted for 26.37% of the Mexico integrated facility management market size in 2025, making it the largest end-user category. This base is tied to factories, warehouses, and process facilities that cannot operate continuously without electrical maintenance, HVAC servicing, civil upkeep, and fire safety compliance. Automotive, electronics, aerospace, and food and beverage plants all require formal maintenance routines because downtime, safety failure, and utility disruption carry direct production costs. Nearshoring has added to this demand by increasing the number of newly commissioned facilities that need immediate operating support after handover. The end-user mix confirms that the Mexico integrated facility management industry remains closely linked to the health of industrial real estate and export-oriented production corridors.

Commercial is forecast to post the fastest growth, with the Mexico integrated facility management market size for commercial end users expanding at a 6.11% CAGR through 2031. Hybrid work stabilization is driving smart office retrofits, space management changes, and hospitality-style service expectations in Mexico City, Monterrey, and Guadalajara. Mexico’s 2026 FIFA World Cup role is also supporting interest in smart venue operations, predictive maintenance, and connected district management for large-footfall assets. Healthcare demand remains important because operators must meet occupational safety obligations alongside healthcare-specific facility requirements. Warehouses, laboratories, retail properties, and tourism-linked assets are adding further depth to the Mexico integrated facility management market because they need repeatable service quality across distributed locations. This broader commercial mix makes growth less dependent on one asset class and raises the value of providers that can standardize service delivery at scale.

Geography Analysis

Mexico City remained the main concentration point for the Mexico integrated facility management market because it combines corporate offices, government sites, hospitals, universities, and high-specification commercial buildings in one metro area. The city also had one of the tightest disclosed industrial vacancy levels, at 5.3% in Q3 2025, which reflected sustained demand for well-managed space. Green-certified office stock in the capital raises technical requirements for service providers because building automation, energy performance, and audit readiness matter more in premium assets. Mexico City is also where many international providers test workplace experience tools, digital maintenance workflows, and more integrated soft FM programs before scaling them elsewhere. For these reasons, the Mexico integrated facility management market in the capital tends to set service expectations for the rest of the country.

Monterrey and the northern corridor form the fastest-moving operating belt within the Mexico integrated facility management (IFM) market. Monterrey’s industrial inventory surpassed 203 million square feet by Q3 2025, while Tijuana also recorded stronger absorption and more construction activity over the same period. Facilities in these northern locations often need bilingual coordination and tighter alignment with international engineering teams, which makes technical execution more demanding. Automotive and electronics clusters in Nuevo León also support repeat contract renewals because uptime and compliance are treated as core operating conditions rather than optional services. Power reliability remains a key issue in this corridor, which increases the appeal of providers that can combine maintenance with backup power planning and load management.

The Bajío region is emerging as the next growth frontier for the Mexico IFM market because it continues to attract manufacturing, logistics, and technology-linked investment. Querétaro, Guanajuato, San Luis Potosí, and Jalisco are generating new demand for maintenance, cleaning, security, and utility management across expanding industrial and mixed-use footprints. Guadalajara is also becoming more relevant for data center FM, healthcare facilities, and technology campuses, with the data center segment outperforming expectations in early 2026. Southern states, the Yucatán Peninsula, and the Interoceanic Corridor still contribute smaller volumes, but they present meaningful opportunity for providers that can mobilize certified subcontractors and manage REPSE complexity across less mature local labor pools.

Competitive Landscape

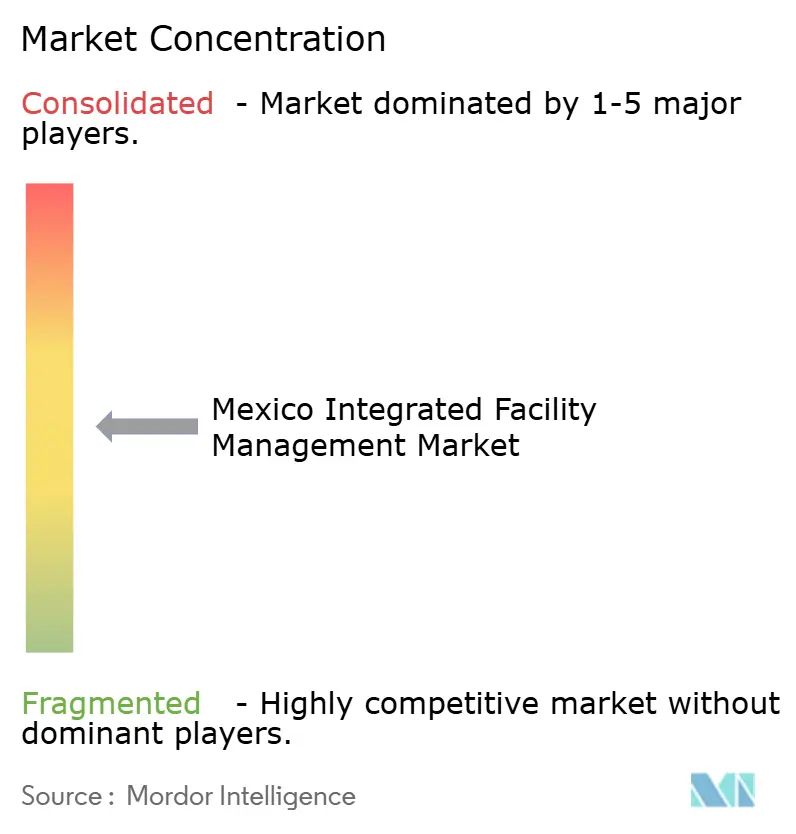

The Mexico integrated facility management market shows moderate concentration among global IFM operators, while the domestic mid-market remains fragmented. ISS, Sodexo, Aramark, CBRE, and Johnson Controls compete most directly for multinational tenants that want standardized service delivery across several properties. In that top tier, contract wins depend less on basic labor supply and more on whether a provider can combine technical maintenance, soft services, reporting, and compliance inside one service structure. Technology platforms have become a major differentiator because buyers increasingly expect predictive maintenance, energy analytics, occupancy visibility, and faster incident response. The Mexico integrated facility management (IFM) market is therefore separating into integrated operators that can defend pricing and single-service firms that compete mainly on cost.

Johnson Controls uses its OpenBlue ecosystem to position itself around connected operations, energy optimization, and digital maintenance rather than labor-only execution. CBRE also moved deeper into operations through its USD 400 million acquisition of Industrious in January 2025, creating a building operations and experience segment that brings property management, workplace experience, and operating support closer together. Turner & Townsend, under CBRE’s majority ownership, then announced a goal to double its Mexico workforce by the end of 2026, which shows how providers are aligning resources with industrial and data center demand. These moves suggest that scale providers increasingly want to own more of the asset lifecycle rather than compete only for a narrow FM work package.

Regional firms such as Grupo Eulen México and SLC Group still matter because they move quickly, price competitively, and understand local labor and compliance conditions. That gives them room in secondary cities and in contracts where buyers prioritize mobilization speed over a global operating model. At the same time, preferred-provider status is becoming harder to secure without integrated governance, stronger documentation, and evidence of digital capability. The Mexico IFM market still offers white space in healthcare FM, energy-as-a-service contracts for industrial parks, and the growing data center maintenance niche, but access to those opportunities will favor companies with technical depth and reliable labor pipelines.

Mexico Integrated Facility Management Industry Leaders

ISS Facility Services México

CBRE Group, Inc.

Sodexo México

Grupo EULEN México

JLL México

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Turner & Townsend, operating under CBRE's majority ownership, announced a target of 100% workforce growth in Mexico by end-2026, reaching approximately 400 employees, with the industrial sector identified as the largest near-term opportunity alongside data centers and hospitality FM. The expansion reinforces CBRE's strategy of vertically integrating project management and FM capabilities to capture nearshoring-driven demand.

- April 2026: Mexico has signed a significant agreement with CAF, the Development Bank of Latin America and the Caribbean, to inject new funds into industrial, energy, and infrastructure projects. This initiative enhances financing options for nearshoring, regional value chains, and sustainable development. The deal expands Mexico’s development financing capabilities, targeting key industrial and strategic projects. It adds a new source of long-term capital, complementing existing institutions like Banobras, Bancomext, and NAFIN, along with financial tools such as FONADIN, CKDs, and CERPIs. Specialists like Luis F. Miranda, who focus on industrial tenant representation, play a vital role in shaping the Integrated Facility Management (IFM) sector in Mexico. Leasing decisions in major hubs like Monterrey and Querétaro drive demand for hard and soft services, addressing operational risks by identifying compliant, high-tech infrastructure. This alignment allows IFM providers to meet the growing needs of nearshoring and foreign direct investment.

- April 2026: Siemens, in collaboration with Latinometrics, has launched an initiative at its Mitras manufacturing facility in Nuevo León. This plant is the first Siemens site globally to receive the prestigious LEED Platinum certification. The partnership establishes the facility as a practical laboratory for local Facility Management providers, demonstrating the effective scaling of IoT automation, carbon footprint reduction, and compliance with strict energy-efficiency standards in large industrial operations.

- January 2026: ISSSTE awarded a MXN 2,412 million (approximately USD 120 million) integrated cleaning and disinfection services contract for its national hospital and administrative facility network, covering the full-year 2026 period. The contract was awarded to Hurga Sanitización y Limpieza S.A. de C.V. in a joint venture structure and highlights the scale of public-sector soft FM procurement as a sustained revenue stream in Mexico.

Mexico Integrated Facility Management Market Report Scope

The Mexico Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End Users |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End Users | ||

Key Questions Answered in the Report

What is the expected value of the Mexico integrated facility management sector by 2031?

The Mexico integrated facility management market is forecast to reach USD 4.69 billion by 2031, rising at a 5.52% CAGR over 2026-2031.

Which service category leads in Mexico?

Soft FM led in 2025 with a 66.47% share, supported by cleaning, security, catering, and office support across public and private facilities.

Which service line is growing fastest through 2031?

Hard FM is projected to grow the fastest at a 6.04% CAGR because buildings and industrial sites require more technical maintenance and controls expertise.

Which end-user group contributes the most demand?

Industrial and process sites held the largest share at 26.37% in 2025 because factories and logistics assets need continuous maintenance, compliance, and uptime support.

Why are more companies choosing integrated providers instead of many vendors?

Buyers are looking for one provider that can manage compliance, maintenance, cleaning, security, and reporting under one contract, which reduces coordination risk and improves accountability.

Page last updated on: