Qatar Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

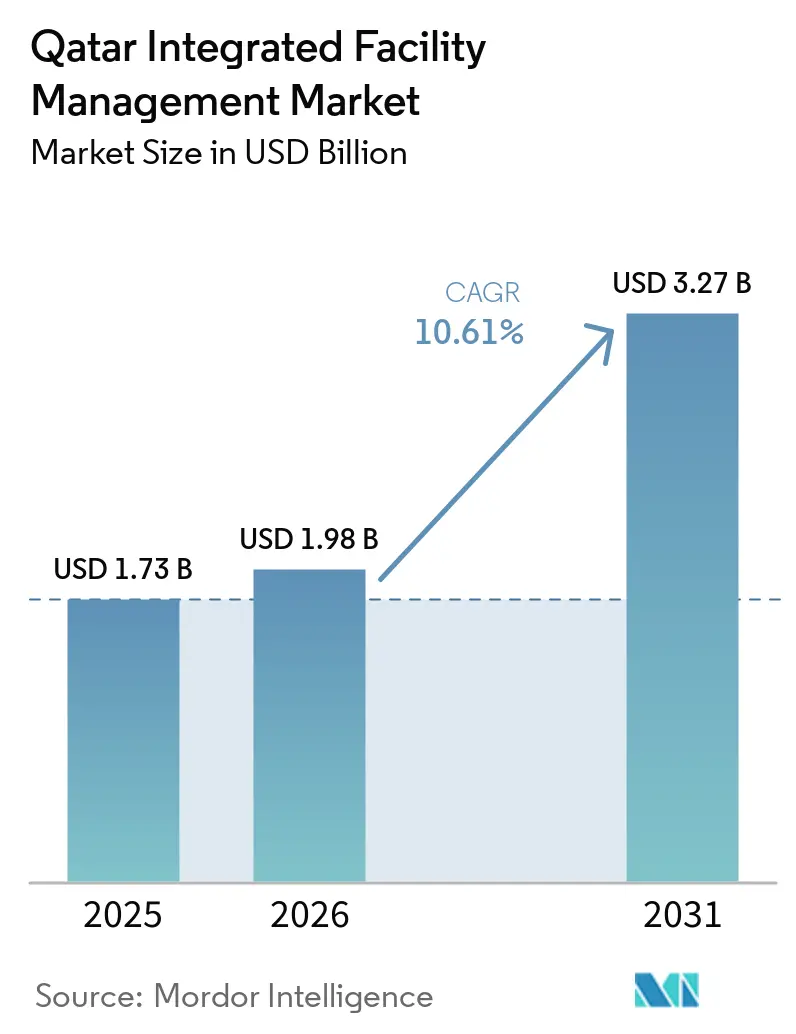

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 10.61% CAGR |

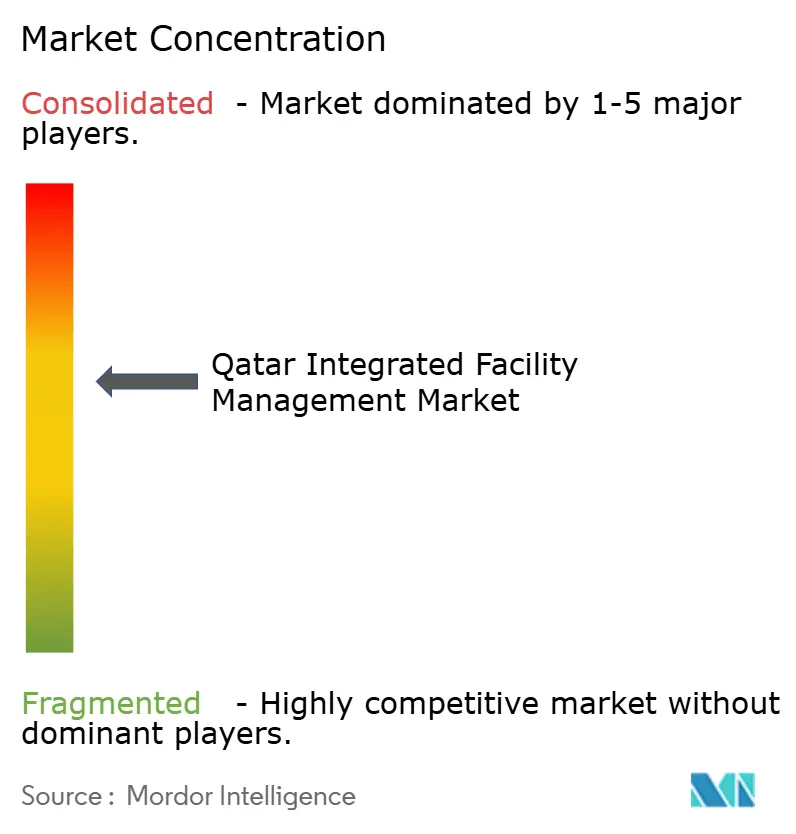

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Integrated Facility Management Market Analysis by Mordor Intelligence

The Qatar integrated facility management market size is projected to expand from USD 1.73 billion in 2025 and USD 1.98 billion in 2026 to USD 3.27 billion by 2031, registering a CAGR of 10.61% between 2026 to 2031. Qatar’s Third National Development Strategy 2024-2030 is sustaining this expansion through its focus on 4% average annual GDP growth, USD 100 billion in cumulative foreign direct investment by 2030, and a broader shift toward non-hydrocarbon activity.[1]General Secretariat of the Council of Ministers, “Third Qatar National Development Strategy 2024-2030,” General Secretariat of the Council of Ministers, cm.gov.qa The Qatar integrated facility management market is also benefiting from continued investment in smart infrastructure, economic zones, industrial assets, and public facilities that require integrated operations, maintenance, and compliance oversight. As more public services move to digital platforms and buildings become more sensor-led, the Qatar integrated facility management (IFM) market is shifting toward contracts that combine technical maintenance, energy management, and service coordination in a single scope. The operating backdrop remains supportive because Qatar continues to position itself as a stable investment destination for long-duration service contracts across commercial, industrial, and institutional assets. At the same time, the Qatar IFM market is becoming harder for smaller operators to serve because compliance requirements, in-country value standards, and workforce localization rules are raising both bidding thresholds and delivery complexity.

Key Report Takeaways

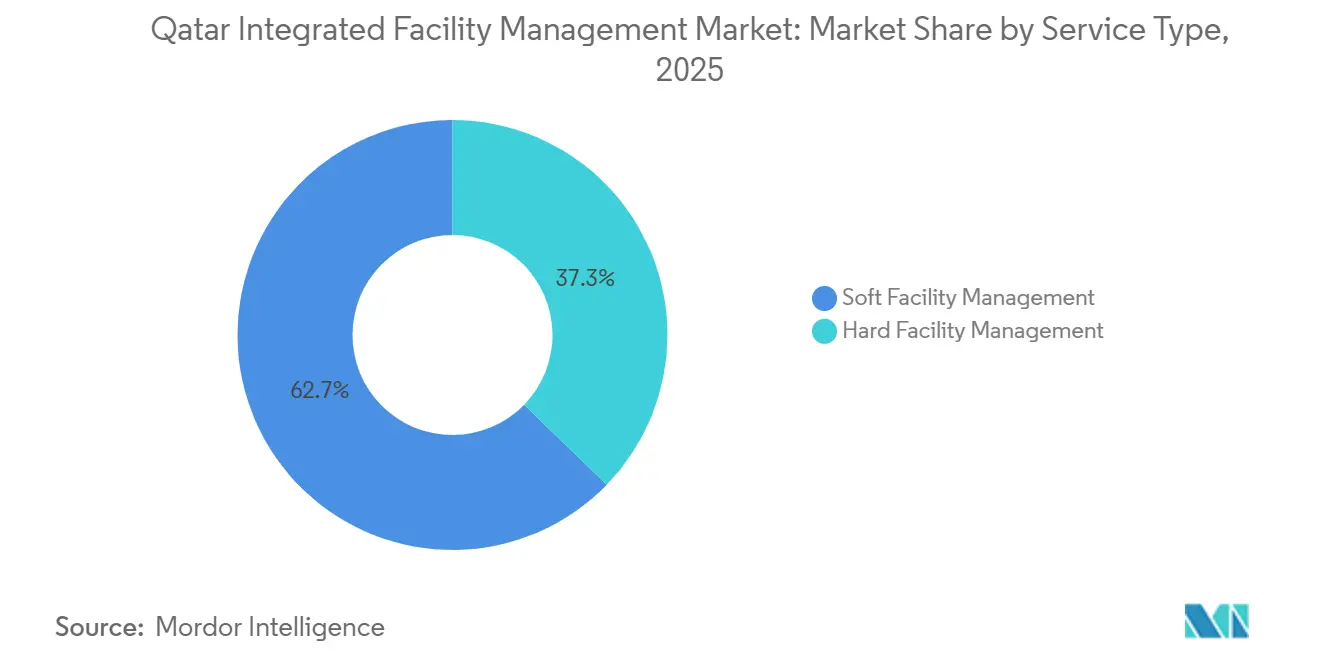

- By service type, soft facility management held 62.73% share of the Qatar integrated facility management market in 2025, while hard facility management is projected to expand at 10.85% CAGR through 2031.

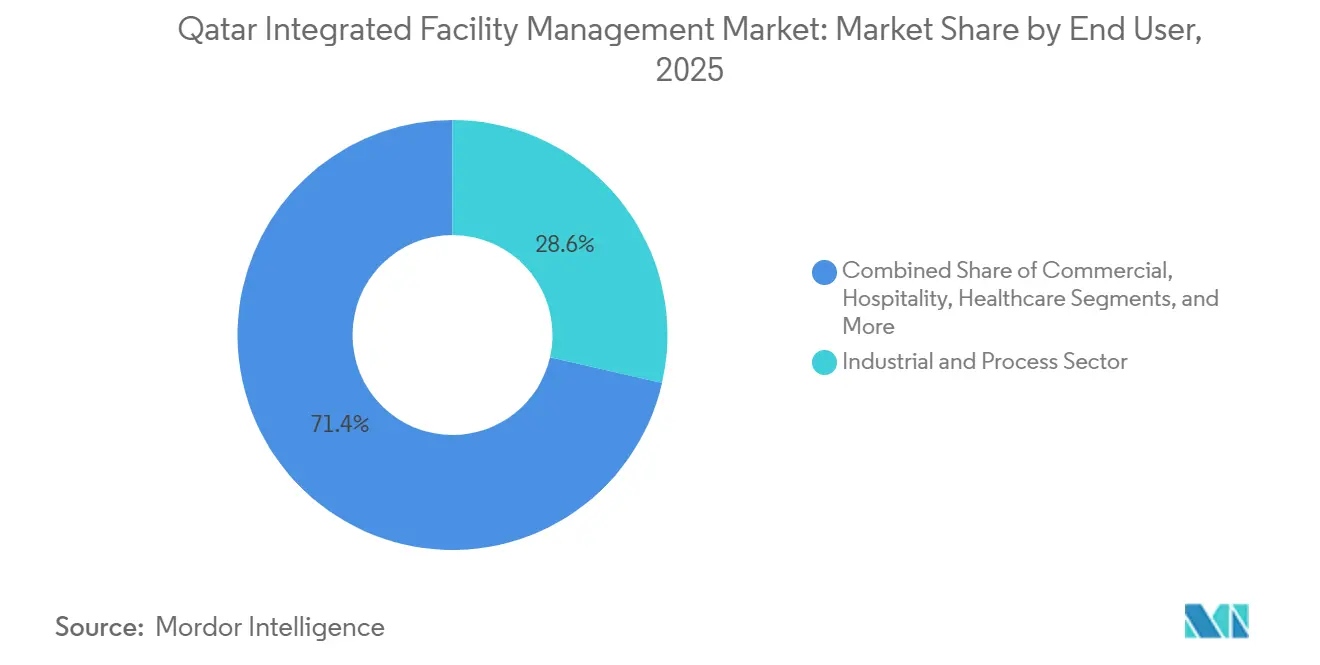

- By end-user, industrial and process accounted for 28.59% share of the Qatar integrated facility management (IFM) market in 2025, while commercial is projected to grow at 11.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing FM Workforce Demand and Professional Capability Expansion by 2030 | +2.0% | National, with concentration in Doha, Lusail, and Mesaieed | Long term (≥ 4 years) |

| Mandatory Data Facility Audits Driving Client Retention and Contract Renewals | +1.8% | National, with early gains in Doha West Bay and Qatar Free Zones | Medium term (2-4 years) |

| Rapid Expansion of Data Centers Driving Specialized FM Needs | +1.5% | Qatar Free Zones, Doha | Medium term (2-4 years) |

| Growing Adoption of IoT-Based Predictive Maintenance | +1.2% | Lusail City, Msheireb Downtown Doha, industrial zones | Short term (≤ 2 years) |

| Accelerated Development of Special Economic Zones | +1.0% | Manateq zones, Qatar Free Zones, QFZA | Long term (≥ 4 years) |

| Demand for Integrated, On-Site FM Software Among Millennial Workforce | +0.6% | National, concentrated in Doha commercial and mixed-use districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing FM Workforce Demand and Professional Capability Expansion by 2030

The Qatar integrated facility management market is being pushed forward by the country’s stated goal of improving labor productivity and raising the share of skilled workers in the labor base by 2030. This matters because the asset mix in Qatar is no longer limited to routine building upkeep, and it now includes digitally managed sites that need teams able to handle building systems, monitoring tools, and structured maintenance programs. Commercial activity has also stayed active, with strong growth in registrations and new licenses during 2025, and that creates a wider base of offices, mixed-use assets, and industrial facilities that need organized FM support from the start. The quality of the labor pool is also being shaped by labor reforms that improve employment standards and make trained frontline roles more formalized across service delivery. For the Qatar IFM market, that combination is lifting demand for certified operators that can staff large contracts consistently rather than rely on low-cost labor alone.

Mandatory Data Facility Audits Driving Client Retention and Contract Renewals

The Qatar integrated facility management market is moving further toward documented performance because periodic audits are becoming more important in public-private projects and long-duration institutional contracts. Operators that can show compliance with Kahramaa’s service regulations and conservation standards have an advantage at renewal time because clients increasingly want measurable evidence on safety, maintenance quality, and system performance. Formal contractor licensing rules for electrical, HVAC, and related technical functions also reduce the pool of bidders that can compete on equal terms in regulated facilities. A January 2026 integrated FM award to Elegancia, valued at QAR 233.7 million (USD 64.2 million), shows how documented capability can translate into long visibility on contract revenue and delivery scope.[2]MUQAWLAT QATAR, “Elegancia Awarded Integrated Facilities Management Contract Worth QAR 233.7 million,” qa.muqawlat.com In the Qatar IFM market, this is making incumbency more durable because a proven audit trail now carries more weight than price-only competition in many re-bids.

Rapid Expansion of Data Centers Driving Specialized FM Needs

The Qatar integrated facility management (IFM) market is gaining a higher-value service layer as data center investment expands faster than the country’s physical size would usually suggest. A January 2026 transaction involving Ooredoo Group's and Syntys announced that Syntys added 12.5 MW of hyperscale capacity in Qatar Free Zones and increased live IT capacity in Qatar to 26 MW, which directly broadens demand for cooling, uptime management, and power assurance services.[3]Ooredoo Group, “Ooredoo Group announces Syntys acquisition of Q Data facilities in Qatar,” ooredoo.com These facilities need operating models that differ from standard commercial buildings because downtime tolerance is low, environmental control is tighter, and technical staffing must be available around the clock. The revenue profile is also stronger because data center FM contracts generate materially higher value per square meter than standard office or retail FM. That changes the service mix in the Qatar IFM market and helps hard FM and specialized technical operations take a larger role inside integrated contracts.

Growing Adoption of IoT-Based Predictive Maintenance

The Qatar integrated facility management market is also being reshaped by the spread of AI and IoT tools that allow operators to act on condition data rather than fixed maintenance schedules. In February 2026, Msheireb Properties, Ooredoo Qatar, and Honeywell announced a city platform in Msheireb Downtown Doha with more than 650,000 IoT sensors for real-time monitoring and predictive incident management. Ooredoo Qatar also expanded its IoT Connect ecosystem in November 2025, which improved remote diagnostics across commercial and industrial environments through 5G, NB-IoT, and LTE-M connectivity. Qatar University’s integrated building management deployment across 72 buildings showed that digital control systems can reduce energy use and improve operational visibility in large public assets. As a result, the Qatar integrated facility management )IFM) market is seeing clients place more value on predictive maintenance capability, centralized asset data, and digital response models that lower avoidable service disruption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Certified, Capable FM Professionals | -1.3% | National, most acute in technical hard FM and data center segments | Long term (≥ 4 years) |

| Volatility of Expatriate Labor Regulations and Operational Costs | -0.8% | National, affecting all labor-intensive FM segments | Medium term (2-4 years) |

| Low Awareness of Total Cost of Ownership Among Local SMEs | -0.5% | National, with highest impact outside Doha’s core commercial districts | Medium term (2-4 years) |

| Consolidated Utility Tariffs Reducing Energy Management ROI | -0.3% | National, affecting commercial and industrial FM operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Certified, Capable FM Professionals

The Qatar integrated facility management market still faces a shortage of qualified technical personnel, especially in roles linked to building systems integration, data center infrastructure, and advanced HVAC commissioning. The issue is most visible in complex assets across Lusail, free zones, and industrial locations where newly commissioned infrastructure needs specialist teams rather than general maintenance staff. The scale of this capability gap was openly discussed at the Qatar International Facility Management Conference and Exhibition in October 2025, which brought together more than 40 speakers from 11 countries. Kahramaa’s licensing requirements also narrow the field because electrical and HVAC practitioners must meet formal qualification and renewal standards before deployment. In the Qatar integrated facility management market, this creates a practical growth ceiling for smaller firms because they may win interest from clients but still lack the certified workforce needed to deliver regulated contracts.

Volatility of Expatriate Labor Regulations and Operational Costs

The Qatar integrated facility management market remains sensitive to labor policy because the operating model still depends heavily on migrant workers across cleaning, security, landscaping, catering, and technical support functions. Qatar’s Law No. 12 of 2024 on Qatarization of private sector jobs raised localization expectations from April 2025 onward, and that added another layer of planning and cost pressure for operators managing large headcounts. At the same time, labor reforms backed through the ILO framework increased minimum employment standards and formal compensation obligations across the workforce. Seasonal outdoor work limits also compress delivery windows for façade maintenance, landscaping, and civil support activities during the hottest months. For the Qatar integrated facility management (IFM) market, these rules improve labor conditions, but they also raise service costs, complicate shift planning, and reduce flexibility in labor-intensive contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Gains Technical Weight While Soft Facility Management Retains Scale

Soft facility management held 62.73% of Qatar integrated facility management market share in 2025, which reflects the broad and recurring demand for cleaning, catering, pest control, and front-of-house support across nearly every asset class in the country. This segment remains the volume anchor because it is needed in commercial towers, education sites, hospitality venues, public buildings, and mixed-use projects from the first day of occupancy. Elegancia Facilities Management alone managed 4 million square meters across nearly 250 sites by 2025, and more than 800,000 square meters of that portfolio sat in the education segment, which shows how large service footprints support recurring soft FM demand.[4]Estithmar Holding, “Elegancia Facilities Management,” Estithmar Holding, estithmarholding.com The Qatar integrated facility management industry also places growing weight on ISO 9001, ISO 45001, and ISO 41001 credentials, which makes service consistency and process control more important in tenders that once focused mainly on labor pricing.

Hard facility management is forecast to grow at 10.85% CAGR from 2026 to 2031, ahead of the overall Qatar integrated facility management market, because technical operations are becoming more central to contract design. This segment is being lifted by assets that require HVAC optimization, fire and life safety upkeep, MEP support, digital building management, and structured preventive maintenance rather than basic repair work alone. ST Engineering’s October 2024 contract exceeding SGD 60 million, or USD 45.3 million, for Lusail City’s AI-powered operating system shows how technical FM is moving into multi-year managed service arrangements with deeper system integration. The same trend raises the role of CAFM software, analytics, and sensor-led monitoring inside service bundles, which improves margin potential for firms that can manage both technical labor and digital tools. For the Qatar integrated facility management market, that means hard FM is not only the faster-growing service type, but also the segment most likely to widen the gap between well-capitalized integrated providers and smaller subcontract-led competitors.

By End-User: Industrial Demand Provides Depth While Commercial Sites Expand Fastest

The industrial and process segment held 28.59% of Qatar integrated facility management market share in 2025, making it the largest end-user category in the country. Its lead comes from the scale and continuity of oil and gas infrastructure, petrochemical facilities, power assets, logistics parks, and production sites that need planned maintenance, safety compliance, and technical reliability over long operating cycles. Manateq’s 13 economic zones operated across more than 48 million square meters at 94% occupancy, which supports a large installed base for FM delivery in industrial and logistics settings. The North Field expansion and the broader industrial push also keep the Qatar integrated facility management industry tied to heavy-asset environments where certified providers are preferred over in-house service models.

Commercial end users are projected to grow at 11.27% CAGR from 2026 to 2031, which makes them the fastest-expanding customer group in the Qatar IFM market size over the forecast period. This category is being pushed by office demand, retail and hospitality activity, warehousing, and the broader push to attract technology, logistics, and financial services investment into Qatar. Invest Qatar’s USD 1 billion incentives program, launched in May 2025, directly supports new site commissioning across target sectors that need professional FM support from setup through stabilized operations. Healthcare and education add further stability because specialist operators are increasingly engaged through public-private frameworks, as shown by Elegancia’s October 2025 appointment to manage 14 new public schools. Sports, leisure, transportation, and public infrastructure round out the end-user mix, and they help keep the Qatar integrated facility management market broad-based rather than dependent on a single demand center.

Geography Analysis

Doha remains the main value center within the Qatar integrated facility management market because the country’s densest concentration of office towers, hospitality assets, public institutions, and mixed-use developments sits in and around the capital. West Bay stands out inside this geography because it houses key corporate, energy, and hotel assets that tend to require higher service standards, larger teams, and wider technical scope than average properties. The Qatar integrated facility management market also has a strong operational cluster in central Doha through districts such as Msheireb Downtown Doha, where smart city systems are bringing building automation, parking, surveillance, and emergency coordination into one service environment. This matters because digitally managed urban districts raise the value of operators that can combine control-room visibility with field execution across multiple asset systems. The Doha concentration therefore supports both scale and sophistication, which is why many large contracts are still anchored in the capital even as new sites emerge elsewhere.

Lusail City is one of the fastest-rising service territories in the Qatar integrated facility management (IFM) market because it was designed as a large mixed-use city and is still moving deeper into operational maturity. Lusail spans 38 square kilometers across 19 districts and is planned to accommodate 450,000 residents, so the service requirement extends across residential, commercial, mobility, and leisure assets in a single urban system. Qatar Free Zones at Ras Bufontas and Umm Alhoul add another layer of geographic momentum because they are structured to attract foreign investment with ownership flexibility and long tax holidays, which supports a steady pipeline of occupied facilities that need integrated support. In practical terms, these locations are helping the Qatar integrated facility management market move beyond a Doha-only profile by expanding demand for industrial, logistics, data center, and technology-linked FM scopes.

Industrial zones in Mesaieed, Al Wakra, and Jery Al Samr add long-duration demand because their operational profile depends on uptime, safety, and preventive maintenance rather than short leasing cycles. Manateq’s broad land allocation across industrial and logistics assets creates a durable installed base for heavy-duty FM services tied to material handling, utility systems, workshops, and support facilities. The national investment pipeline also points to wider geographic dispersion over time because Qatar continues to promote new projects and foreign investment through 2030 under its development strategy. As these projects move from construction into operations, the Qatar IFM market is likely to see more balanced demand between core Doha districts and the country’s industrial and special-zone corridors.

Competitive Landscape

The Qatar integrated facility management market shows moderate consolidation, with a relatively small set of vertically integrated operators competing for the largest government, education, energy, and institutional contracts. Elegancia Facilities Management and Waseef remain prominent local names, while international participants such as Serco and Al Futtaim Engineering and Technologies compete were global operating frameworks and technical specialization matter more. The market is not controlled by a single provider, but scale, certification, and multi-service capability clearly matter more now than they did when subcontract-led delivery was enough for most sites. That shift means the Qatar integrated facility management market increasingly rewards firms that can control both hard and soft services inside one operating model.

Elegancia’s contract wins announced in May 2026 at Qatar University, QatarEnergy headquarters towers, Lusail Promenade, and a major media network show how portfolio breadth can become a strong competitive moat in the Qatar integrated facility management market. Waseef has also strengthened its bid profile through an in-country value certification score of 60.9%, which is important in tenders where national contribution carries formal scoring weight. Earlier, Waseef secured a three-year agreement with Kahramaa for Abu Hamour, which highlights the value of aligned delivery in public utility environments. Another strategic move came from Elegancia’s January 2025 BICSc training accreditation, which supports workforce standardization and signals a stronger quality proposition in labor-intensive services. These steps show that competition in the Qatar integrated facility management market is no longer shaped by manpower scale alone, because training systems, ICV standing, and multi-site delivery experience now influence how contracts are awarded and renewed.

There is still open space in parts of the market where technical specialization is scarce, especially in data center FM and mid-market integrated services for newer office and mixed-use occupiers. That gap exists because not every operator can meet the staffing, licensing, digital monitoring, and compliance demands required for higher-value technical sites. The use of CAFM platforms, predictive maintenance tools, and centralized monitoring is moving from a differentiator to a baseline requirement in large bids, which raises the threshold for firms that still depend on manual workflows. In the Qatar integrated facility management market, this creates room for consolidation among second-tier companies because the cost of staying compliant and digitally capable is rising faster than many smaller operators can absorb.

Qatar Integrated Facility Management Industry Leaders

G4S Qatar LLC

Mosanada Facilities Management Services

Sodexo Qatar Services LLC

CBRE Group Inc.

Al Asmakh Facilities Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Elegancia Facilities Management (Estithmar Holding) secured major FM contracts in Qatar, including O&M for QatarEnergy headquarters in West Bay, campus FM for Qatar University (~8 million sqm), integrated FM for Lusail Promenade, and a contract with a Qatari media network. The wins expand its education portfolio beyond 9 million sqm and grow its workforce to over 17,000 across 9 countries.

- February 2026: Msheireb Properties, Ooredoo Qatar, and Honeywell have partnered to automate Msheireb Downtown Doha using Honeywell’s City Suite AI platform. The system integrates 650,000+ IoT sensors, 10,000 CCTV cameras, and 10,000 smart parking spaces under a five-year managed services model, positioning Doha as a Gulf benchmark for AI-driven urban FM.

- January 2026: Syntys, backed by Ooredoo Group, completed the acquisition of Q Data QFZ LLC from Doha Venture Capital, adding 12.5 MW of hyperscale Tier III-certified data center capacity within Qatar Free Zones and increasing Syntys' total live IT capacity in Qatar to 26 MW. The transaction directly expands the specialized FM demand for data center operations, precision cooling, and power assurance services.

- January 2026: Elegancia Facilities Management was awarded an integrated FM contract valued at QAR 233.7 million (USD 64.2 million), effective January 1, 2026 through May 31, 2031, covering full hard FM scope including MEP preventive and corrective maintenance, HVAC, fire protection, solar heating, automated waste collection, water treatment, medical gas, chiller management, generators, UPS, and AV systems.

Qatar Integrated Facility Management Market Report Scope

The Qatar Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the 2031 outlook for facility management services in Qatar?

The sector is projected to reach USD 3.27 billion by 2031 from USD 1.98 billion in 2026, with 10.61% CAGR over 2026-2031.

Which service category leads demand in Qatar?

Soft FM led in 2025 with 62.73% share because cleaning, catering, pest control, and client-facing services are required across most property types.

Which service category is growing the fastest in Qatar?

Hard FM is the fastest-growing category, with 10.85% CAGR through 2031, supported by smart buildings, digital monitoring, and technical maintenance needs.

Which end-user group creates the largest revenue base in Qatar?

Industrial and process facilities led with 28.59% share in 2025 due to oil and gas assets, economic zones, and heavy infrastructure requiring long-cycle maintenance.

Why are digital tools becoming more important in Qatar facilities operations?

AI platforms, IoT sensors, and predictive maintenance systems are helping operators reduce reactive work, improve visibility, and manage complex mixed-use and institutional assets more effectively.

What is shaping competition among leading providers in Qatar?

Large contracts now favor operators with integrated delivery, certified technical teams, ISO-aligned processes, digital tools, and stronger in-country value positioning.

Page last updated on: