France Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

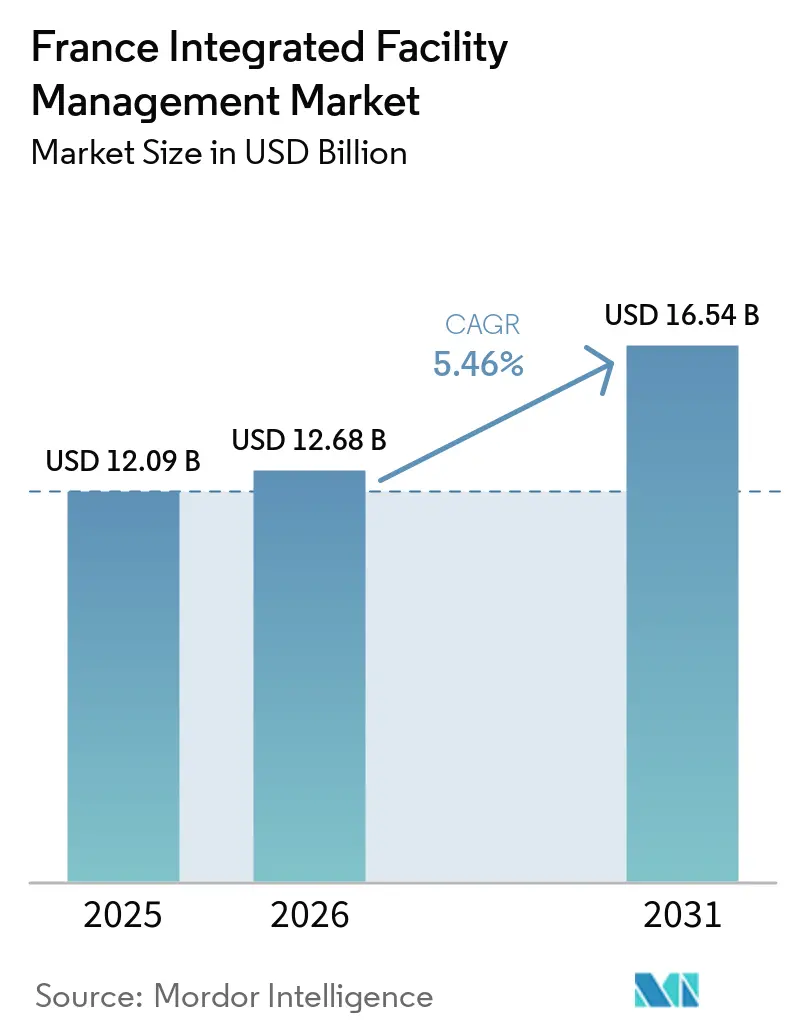

| Base Year Market Size (2025) | USD 12.09 Billion |

| Market Size (2026) | USD 12.68 Billion |

| Market Size (2031) | USD 16.54 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Integrated Facility Management Market Analysis by Mordor Intelligence

The France integrated facility management market size is expected to increase from USD 12.09 billion in 2025 to USD 12.68 billion in 2026 and reach USD 16.54 billion by 2031, growing at a CAGR of 5.46% over 2026-2031. The France integrated facility management (IFM) market is being supported by public sector decarbonization mandates, broader use of healthcare performance contracts, and a growing pipeline of hyperscale and regional data center projects. Outsourcing penetration for non-core services remains below Northern European levels, which leaves room for longer-duration integrated contracts to replace fragmented single-service arrangements. Competitive conditions remain intense because more than 1,200 providers operate across national and regional tiers, which keeps margin pressure high and pushes providers to compete on measurable outcomes instead of price alone. Digital monitoring, energy reporting, and guaranteed performance clauses are becoming more important in contract design as building owners prepare for tighter carbon and efficiency rules. Labor shortages in HVAC and MEP trades, together with rising payroll costs in public contracts, are also shaping how quickly the France IFM market can convert regulatory demand into delivered service capacity.

Key Report Takeaways

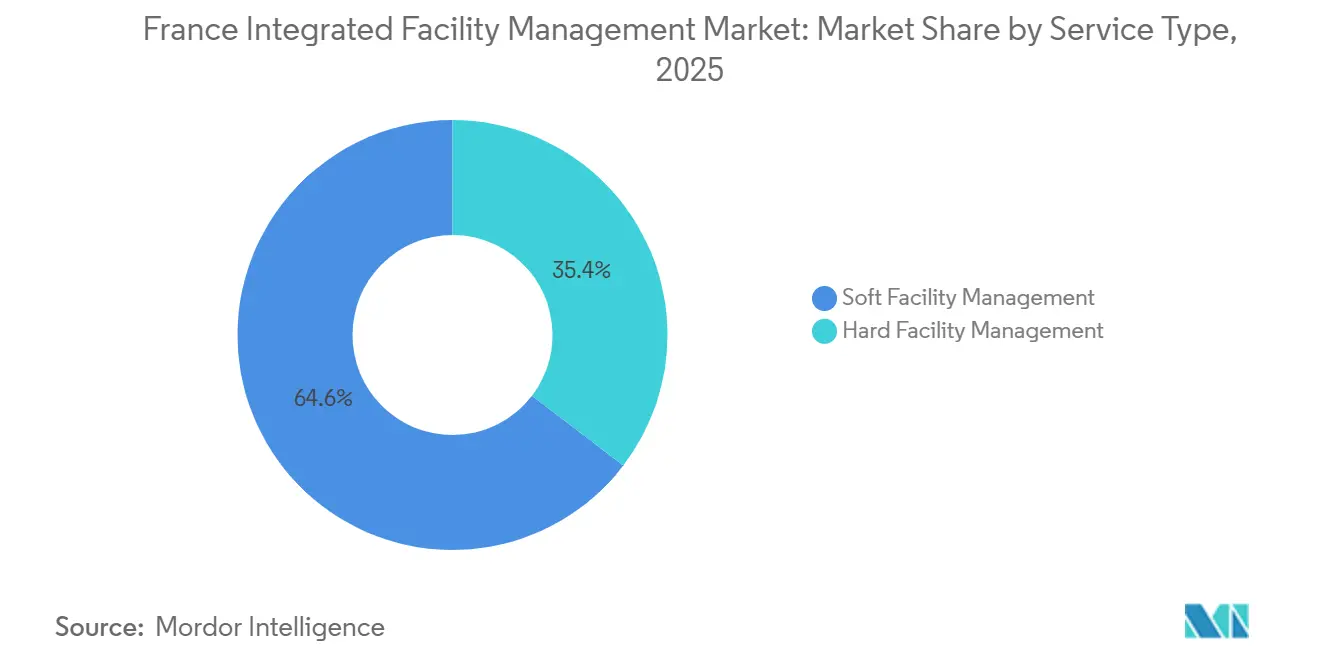

- By service type, soft facility management led with 64.61% revenue share of the France integrated facility management market in 2025, while hard facility management is forecast to expand at 6.22% through 2031.

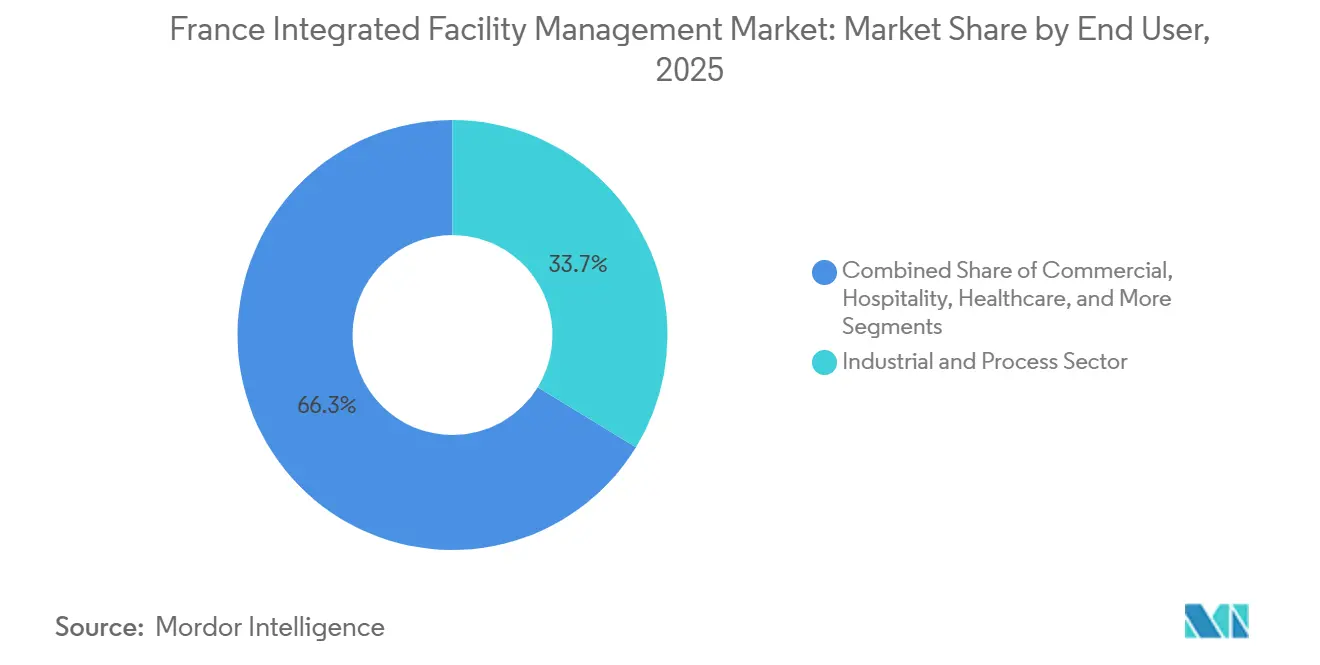

- By end user, the industrial and process sector held 33.74% of the France integrated facility management (IFM) market share in 2025, while the Commercial segment is forecast to grow at 6.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Outsourced Integrated Services in Public Infrastructure | +1.5% | National, with early gains in Île-de-France, Grand Paris corridor, and major urban communes | Short term (≤ 2 years) |

| Accelerating Shift to Performance-Based Contracts in Healthcare Facilities | +1.0% | National, concentrated in CHU networks and multi-site hospital groups | Short term (≤ 2 years) |

| Growth of Smart Buildings Enabling Predictive FM via IoT Sensors | +0.9% | National, with intensity in Île-de-France, Lyon, and Marseille | Medium term (2-4 years) |

| Heightened Regulatory Pressure on Energy Efficiency Targets | +0.7% | National, across tertiary buildings above 1,000 m², with spillover to multinational portfolios | Short term (≤ 2 years) |

| Rapid Expansion of Data Centers Requiring Specialized FM | +0.5% | Île-de-France and Marseille cores, with emerging nodes in Bordeaux, Valence, and Grand Est | Medium term (2-4 years) |

| Emerging Hotelization Trend in Office Spaces Driving Soft FM Bundling | +0.3% | Île-de-France led, followed by Lyon, Nantes, and Bordeaux tertiary districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Outsourced Integrated Services in Public Infrastructure

France’s public sector owns 90 million m² of government real estate and manages thousands of municipal and institutional sites that still depend heavily on in-house teams or fragmented contracts. The Tertiary Decree requires 40% energy consumption cuts by 2030 and 50% by 2040 for tertiary buildings above 1,000 m², with annual OPERAT reporting and penalties that can reach EUR 7,500 (USD 8,475), per legal entity for non-compliance.[1]Service Public Entreprendre, “Décret Tertiaire – Obligations OPERAT Et Sanctions,” Service Public Entreprendre, entreprendre.service-public.fr Those obligations are difficult to manage without centralized monitoring and reporting tools, which is pushing more public buyers toward bundled contracts in the France integrated facility management market. The December 2026 verification milestone against 2030 targets is turning a regulatory requirement into active procurement rather than a long-range planning exercise. Municipal leaders also face public visibility risk when non-compliant buildings appear on official registers, so outsourcing decisions are being shaped by political exposure as well as operating cost pressure in the France integrated facility management (IFM) market.

Accelerating Shift to Performance-Based Contracts in Healthcare Facilities

French hospitals are moving away from legacy P1-P2-P3 maintenance structures and toward Marché Public Global de Performance contracts that combine technical services with energy guarantees. A 2025 tender at CHU de Nice, Hôpital Pasteur covered HVAC, electrical, and fire systems under a EUR 30 million contract (USD 33.9 million), with energy and environmental performance carrying 15% of award criteria. In January 2026, Centre Hospitalier de Martigues awarded a 108-month energy performance contract worth EUR 7,464,341 (USD 8.4 million), to Equans Services Bâtiments and Infrastructures. The CPOM framework continues to reinforce budget discipline across EHPADs and other healthcare settings, which supports longer and more integrated service models in the France integrated facility management market. Providers that can contractually guarantee savings instead of offering only best-effort maintenance are likely to secure longer tenures and better retention in the France IFM market.

Growth of Smart Buildings Enabling Predictive FM Via IoT Sensors

The BACS Decree required building automation and control systems of at least Class C since January 2025, for non-residential buildings with HVAC capacity above 290 kW. The French BACS market grew 5% in 2025, while the service segment rose 5.8%. IoT-enabled FM platforms have delivered energy savings of 15-25% on HVAC systems through real-time anomaly detection and predictive scheduling, which improves the contract case for multi-year maintenance programs. In Roubaix, an AI-driven HVAC management program produced annual savings of EUR 600,000 (USD 648,000), and targeted a 30% cut in CO₂ emissions.[2]Accenta, “City Of Roubaix AI-Driven HVAC Program – EUR 600,000 Annual Savings,” Accenta, accenta.ai Once sensors, dashboards, and behavior baselines are embedded into client assets, switching costs rise and providers gain a stronger retention position in the France integrated facility management market.

Heightened Regulatory Pressure on Energy Efficiency Targets

RE2020 expanded in January 2026 to 10 additional tertiary building categories, including hotels, restaurants, retail, universities, healthcare facilities, and airport terminals. This widened the service need for technical operators that can combine maintenance, carbon tracking, and compliance reporting in the France integrated facility management market. France also tightened implementation of energy performance certificate rules in 2025, with legal entities facing strict fines for non-compliance. Tertiary buildings account for 249TWh of annual final energy consumption in France, and 37% of that total still comes from fossil fuels, which keeps pressure high on retrofit and performance contracts.[3]RTE (Réseau de Transport d'Électricité), "Annual Electricity Review 2025 – Key Findings," RTE France, analysesetdonnees.rte-france.com Providers that can support ADEME OPERAT filings and produce auditable carbon and energy records offer a clear compliance advantage that helps expand the France integrated facility management market beyond single-service maintenance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural Skills Shortage in HVAC and MEP Trades Constraining Hard FM Delivery Capacity | -0.8% | National, most acute in Île-de-France, Lyon, and PACA | Medium term (2-4 years) |

| Escalating Public Sector Payroll Costs From CNRACL Employer Contribution Increases Constraining FM Contract Renewal Pricing | -0.5% | National, concentrated in public-sector FM contracts with municipalities, hospital groups, and EHPADs | Short term (≤ 2 years) |

| Margin Squeeze From Rising Labor Costs | -0.6% | National, across labor-intensive FM segments | Medium term (2-4 years) |

| Cybersecurity Risks in Connected FM Systems | -0.4% | National, higher exposure in smart buildings and digitally integrated portfolios | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Structural HVAC And MEP Skills Shortage Constraining Hard FM Delivery

The France integrated facility management market faces a structural mismatch in technical labor because the sector needs 15,000 new CVC technicians each year while training programs produce only 8,000 graduates. That leaves a yearly deficit of 7,000 profiles before accounting for retirements, and nearly 30% of active CVC technicians are already older than 55 years. The problem is becoming more acute because BACS compliance and low-GWP refrigerant rules now require digital controls knowledge, protocol familiarity, and updated F-Gaz certification. Hard FM providers are therefore being asked to guarantee energy and uptime outcomes while facing higher hiring costs and tighter staffing availability in the France IFM market. Early investment in remote diagnostics and AI-assisted monitoring is becoming a practical response because it reduces technician intensity per site and helps providers protect contract delivery capacity.

Escalating Public Sector Payroll Costs From CNRACL Employer Contribution Increases

A January 2025 decree raised CNRACL employer contribution rates from 31.65% in 2024 to 34.65% in 2025, and the rate now stands at 37.65% in 2026 with further increases scheduled through 2028.[4]Légifrance, "Décret n° 2025-86 du 30 janvier 2025 relatif au taux de cotisations vieillesse des employeurs des agents affiliés à la CNRACL," Journal Officiel de la République Française, 31 January 2025, legifrance.gouv.frFor labor-intensive public FM contracts, where payroll accounts for 50-60% of total cost, these annual contribution increases are colliding with fixed-price agreements that often run for 3-6 years. This creates a contract renewal problem in the France integrated facility management (IFM) market because providers cannot always pass through rising employment costs while public buyers are also being asked to commit to longer performance-based agreements. Some communes are therefore delaying or scaling down outsourcing decisions, which slows the conversion of regulatory demand into signed integrated contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Adoption Accelerated by Compliance Mandates

Soft facility management held 64.61% of the France integrated facility management market share in 2025, which reflects the scale of cleaning, catering, security, reception, and office support demand across institutional, healthcare, and corporate sites. The France IFM market has continued to favor Soft FM because post-pandemic hygiene protocols remain embedded in-service specifications across many client categories. Flexible workspace expansion also widened the addressable base for bundled soft services, with more than 1.4 million m² of flex office space in France in 2026 and 850,000 m² located in Île-de-France. Operated office models are also changing service content because a single provider may now deliver reception, cleaning, catering, and workplace coordination under an all-inclusive operating model. Security and pest control remain smaller lines within Soft FM, but they are gaining scope as clients with longer operating hours ask for constant monitoring and higher service continuity.

Hard facility management is projected to expand at 6.22% CAGR, representing the fastest France integrated facility management (IFM) market size growth by service type through 2031. The France integrated facility management industry is seeing this acceleration because the BACS Decree, the Tertiary Decree, and the 2026 RE2020 expansion all require deeper technical delivery than a soft-only model can provide. The 2024 OPERAT assessment showed that many obligated companies were still behind the path needed for the 2030 target, which keeps retrofit urgency high and shortens conversion timelines for multi-technical contracts. Providers with in-house MEP engineering, sensor deployment capability, and reporting competence are better placed to win this work because clients increasingly want one provider to install, maintain, measure, and report. The result is that complexity-weighted demand is rising faster than volume-led demand, which is gradually changing service mix across the France IFM market.

By End User: Industrial Demand Anchored, Commercial Growth Broadening the Base

The Industrial and Process sector accounted for 33.74% of the France integrated facility management market size in 2025, making it the largest end-user group. Industrial sites support that position because manufacturing, power, oil and gas, and process facilities require continuous uptime, layered safety routines, and specialized technical support rather than basic site maintenance. Those contracts tend to generate higher revenue per site because they combine compliance, mechanical upkeep, electrical support, and continuity planning in one service package. They are also sticky once a provider is embedded, since plant operators are less willing to disrupt established technical workflows and safety procedures. Smaller end-user groups such as retail, education, and transportation add steady volume, especially as more tertiary categories fall under expanded environmental rules from 2026 onward.

The Commercial segment is forecast to grow at 6.34% CAGR, marking the fastest France integrated facility management market size growth among end users through 2031. That pace reflects the data center build-out and the reconfiguration of office portfolios under hybrid work, both of which are pushing clients toward more integrated service models in the France IFM market. France had 283MW of data center capacity under construction in the first quarter of 2025 and a 1.8GW early-stage pipeline, which is creating a stream of long-duration contracts for cooling, power, redundancy systems, and 24-7 monitoring. Healthcare remains another major base because hospitals are moving toward performance-led maintenance and energy contracts, while public institutions are accelerating procurement ahead of OPERAT filing requirements. This means end-user growth is not being driven by one building type alone, but by a broader shift toward sites that need measurable outcomes, high uptime, and integrated reporting.

Geography Analysis

Île-de-France held the dominant regional position in the France integrated facility management market in 2025 because it concentrates headquarters, public institutions, healthcare systems, and the country’s largest digital infrastructure cluster. The Greater Paris area hosted 85% of national data center capacity, and the region had 283MW under construction with a 1.8GW early-stage pipeline as of the first quarter of 2025. The South Paris corridors around Villebon-sur-Yvette, Marcoussis, and Les Ulis are taking a larger share of incremental hyperscale investment as inner-zone land becomes harder to secure. The 2026 publication of annual OPERAT attestations is also converting latent compliance pressure into active contract demand across the Paris basin in the France integrated facility management (IFM) market. A notable pattern is that some of the strongest new opportunities sit 30-75km outside Paris, where former industrial sites are being repurposed into high-power digital assets that still need national-grade service coverage.

Auvergne-Rhône-Alpes was the second most important contributor to the France IFM market in 2025, with Lyon acting as the main urban anchor. Secondary-city flex office growth has been rising steadily, and Lyon sits among the largest markets outside Île-de-France for coworking and operated office capacity. The region also has a dense hospital base that is moving toward performance-linked technical contracts, which supports demand for providers with stronger Hard FM capabilities. A shopping center near Lyon invested EUR 1.47 million (USD 1.6 million), in energy upgrades and achieved a 23% reduction in energy use, which shows how tertiary compliance is feeding regional retrofit work.

PACA, Nouvelle-Aquitaine, Grand Est, and other regional markets make up the remaining national opportunity set in the France IFM market. Marseille has strengthened its role as the second major data center node because of its submarine cable position and new facility commitments tied to international connectivity. UltraEdge’s 2026 plan for up to nine connected facilities and EDF’s push to repurpose former thermal plant locations both point to broader regionalization of high-specification FM demand beyond Paris and Marseille. This shift is important because it extends demand into cities that historically needed only maintenance-level integrated services and now require more advanced technical, energy, and critical-systems support.

Competitive Landscape

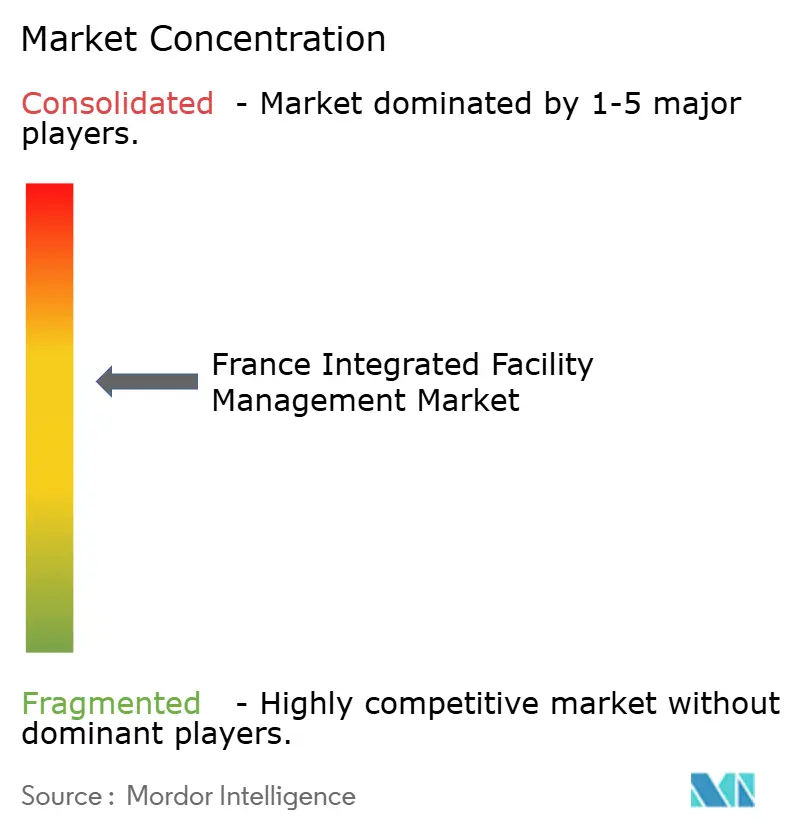

The France integrated facility management market remained moderately consolidated in 2026, with more than 1,200 providers operating across national, regional, and specialist categories. The top national groups have visible scale, but no single operator holds dominant control, meaning buyers still have multiple alternatives for soft services, technical delivery, and specialist maintenance. Competition is increasingly centered on digital reporting, energy guarantee credibility, and proof of operational outcomes rather than broad service menus alone.

Onet’s acquisition of ISS France’s cleaning, logistics, and facility management activities in April 2024 added EUR 384 million (USD 423 million) in revenue and 14,000 employees, strengthening its position within the consolidated national landscape for bundled soft and multiservice delivery. GSF also expanded its multiservice position through the Ithaque acquisition in 2025, lifting consolidated turnover to EUR 1.6 billion (USD 1.8 billion) and increasing its exposure to reception, hospitality, and adjacent service lines.

Technology-led positioning is reshaping competition in this moderately consolidated market structure, as building owners increasingly demand data visibility and measurable service outcomes. Otis closed the acquisition of a majority stake in WeMaintain in April 2026, strengthening access to AI- and IoT-enabled service capability across elevators and escalators. SPIE Facilities also renewed and expanded its data center maintenance relationship with Bouygues Telecom in 2025, covering 34 Île-de-France sites and additional locations in Southwest France. These moves reflect how leading providers in a consolidated but still multi-player market are differentiating through digital service layers and technical specialization, rather than relying on scale alone.

The France integrated facility management market still has open space in mid-market healthcare below the largest CHU systems and in provincial data center clusters outside the Paris–Marseille axis. These segments require cross-service integration and are less suited to providers offering only labor-heavy soft services or single-trade technical work. Dalkia’s 25-year Paris district heating concession win highlights that major energy-linked service structures are still being realigned across France, influencing adjacent procurement relationships over time. The broader outcome in this consolidated market is that scale still matters, but competitive advantage now depends more on engineering depth, digital capability, and the ability to manage compliance risk within long-duration service models.

France Integrated Facility Management Industry Leaders

-

Sodexo S.A.

-

ENGIE Cofely

-

VINCI Facilities

-

ISS A/S

-

Bouygues Energies & Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Otis Worldwide Corporation has closed the acquisition of a majority stake in WeMaintain, a Paris-founded AI- and IoT-based elevator and escalator service platform with 350 employees. The deal gives Otis a proprietary data-layer facilities management technology with agnostic, multi-brand capability, marking a strategic shift in OEM positioning toward long-term service relationships in France and Europe. going forward in sector growth.

- April 2026: Dalkia, EDF Group, Eiffage, and RATP Solutions Ville signed a 25-year concession contract with the City of Paris for the Parisian urban heating network, effective January 1, 2027, involving nearly EUR 3.4 billion (USD 3.8 billion), in total investment. The contract mandates increasing renewable and recovery energy from 50% to 76% by 2034, directly reshaping the landscape for large-scale energy FM in the capital.

- September 2025: GSF finalized the acquisition of the Ithaque Group, which includes Pénélope Group, national leader in reception and hospitality, with EUR 140 million revenue, and FMG Sales and Marketing, with EUR 80 million revenue and 1,000 employees. The combined group reached EUR 1.6 billion, or USD 1.8 billion, in consolidated turnover, marking a significant step in soft FM service bundling and consolidation.

- December 2025: Bouygues Energies and Services secured a EUR 6 million, 5-year renewable contract with RATP Group to deploy more than 550 new EV charging points across 60 Île-de-France sites and assume operation of 150 existing charging points. The contract can be extended to all RATP Group sites nationally.

France Integrated Facility Management Market Report Scope

The France Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the France integrated facility management market in 2026?

The France integrated facility management market stands at USD 12.68 billion in 2026 and is projected to reach USD 16.54 billion by 2031 at a 5.46% CAGR.

Which service line leads facility management demand in France?

Soft facility management led in 2025 with 64.61% share, supported by cleaning, catering, security, and office support across institutional, healthcare, and corporate sites.

What is driving faster growth in Hard FM contracts across France?

Hard facility management is expanding faster at 6.22% because BACS rules, RE2020 expansion, and Tertiary Decree compliance are increasing demand for technical, multi-system contracts.

Which end-user group contributes the most revenue in France?

Industrial and Process led with 33.74% share in 2025 because high-up-time facilities in manufacturing, energy, and oil and gas require more complex and durable FM contracts.

Why is the commercial segment growing faster than other end users?

Commercial demand is rising at 6.34% through 2031 because data centers and hybrid-work office reconfiguration need integrated support for power, cooling, security, and occupancy-led services.

What rules are shaping outsourcing decisions in French buildings?

The Tertiary Decree, the BACS Decree, and RE2020 are raising compliance pressure on energy, automation, and reporting, which is pushing buyers toward integrated and measurable service contracts.

Page last updated on: