Europe Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

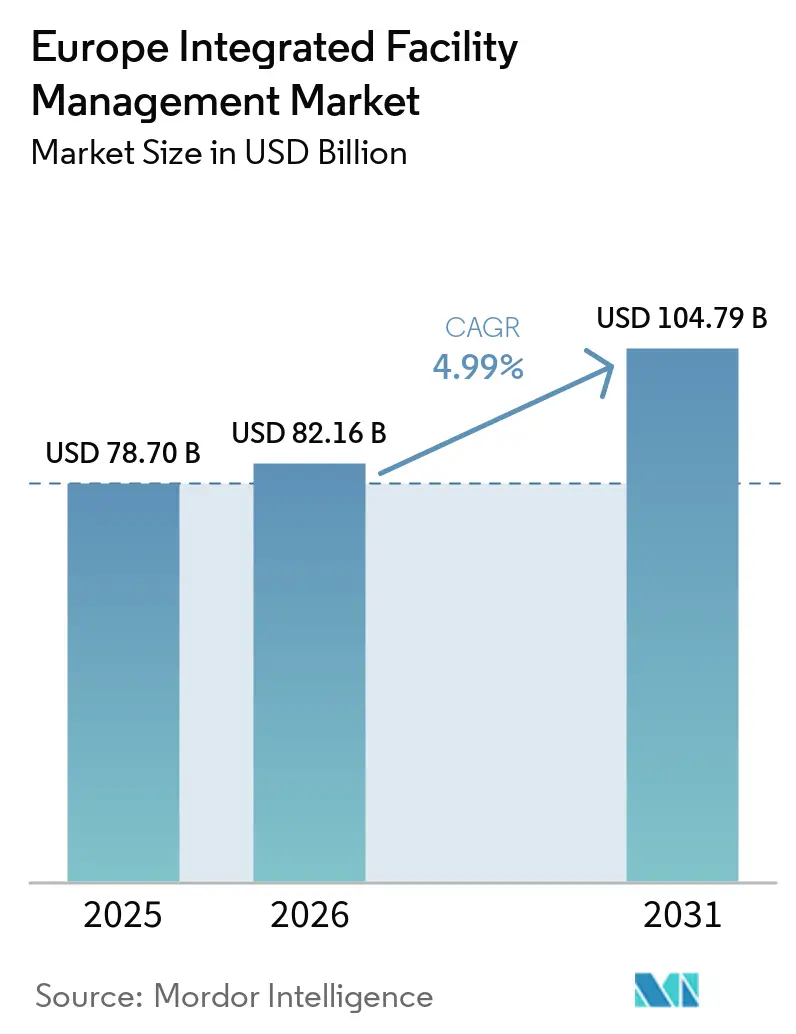

| Base Year Market Size (2025) | USD 78.70 Billion |

| Market Size (2026) | USD 82.16 Billion |

| Market Size (2031) | USD 104.79 Billion |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Integrated Facility Management Market Analysis by Mordor Intelligence

The Europe integrated facility management market size is projected to be USD 78.70 billion in 2025, USD 82.16 billion in 2026, and reach USD 104.79 billion by 2031, growing at a CAGR of 4.99% from 2026 to 2031. The market is being supported by regulatory deadlines that are pulling energy upgrades, controls installation, commissioning work, and ongoing compliance monitoring into broader service contracts. The Europe integrated facility management (IFM) market is also gaining from higher use of connected building tools, because owners now expect operating data, maintenance visibility, and measurable efficiency gains from outsourced partners. Data center expansion across major European hubs is adding a separate stream of technical demand that requires round-the-clock engineering support and stronger self-delivery capability. At the same time, portfolio consolidation in commercial and public estates is reducing interest in fragmented supplier structures and is pushing buyers toward wider contract scopes and longer service relationships. Labor shortages, wage inflation, and building-system cyber exposure are still limiting margins, yet the Europe IFM market continues to benefit from regulation-led demand and a deeper need for single-account accountability.

Key Report Takeaways

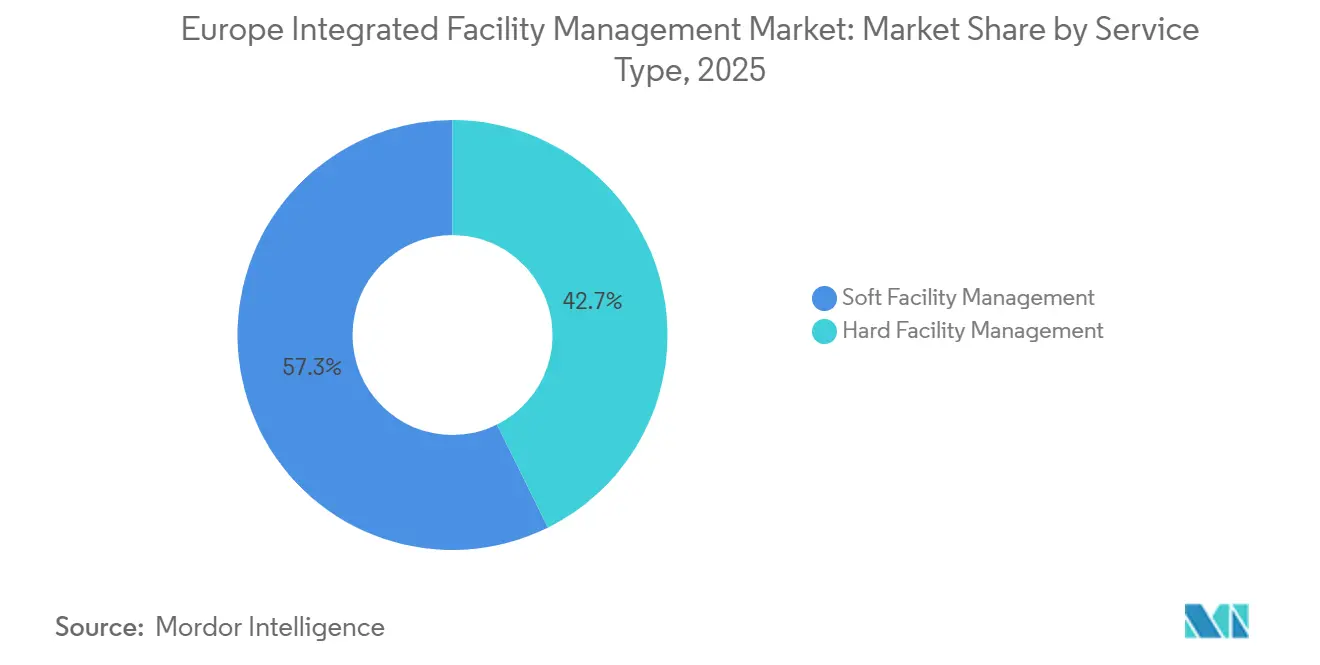

- By service type, soft facility management held 57.32% of the Europe integrated facility management market share in 2025, while hard facility management is projected to expand at a 5.71% CAGR through 2031.

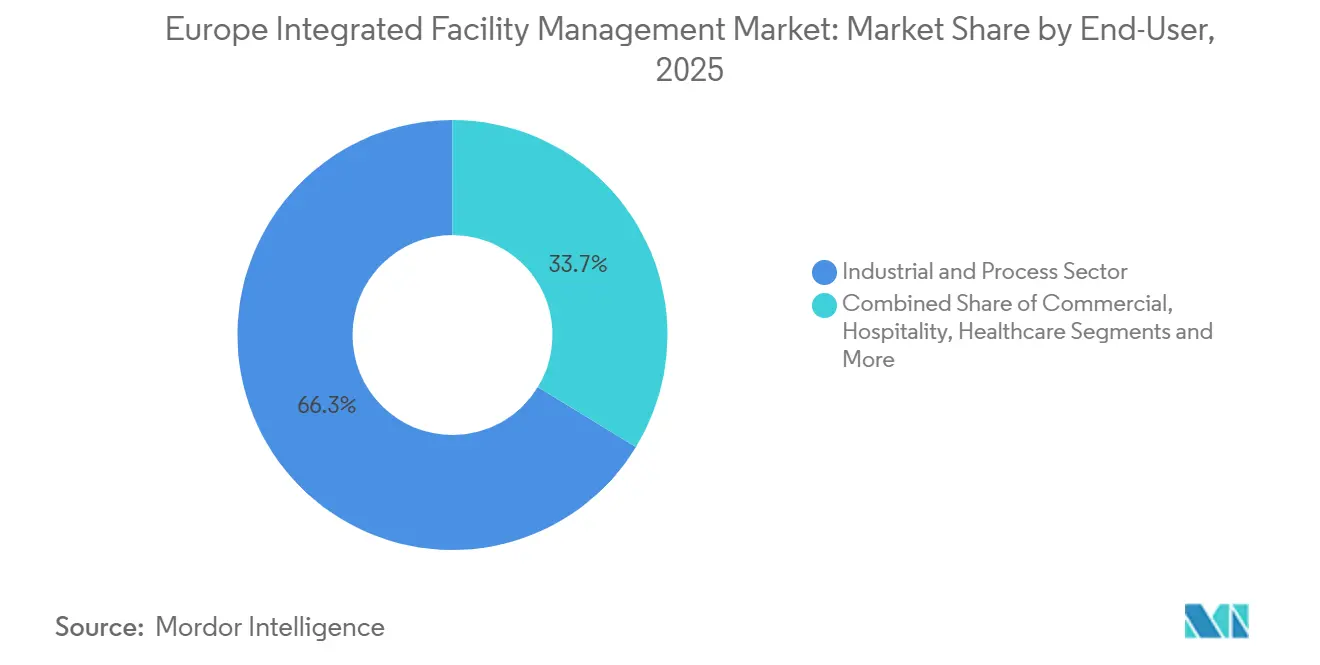

- By end user, the industrial and process sector accounted for 33.72% share of the Europe integrated facility management (IFM) market size in 2025, while the commercial sector is forecast to advance at a 5.43% CAGR through 2031.

- By geography, Germany held a 21.69% share of the Europe IFM market in 2025, while Spain is forecast to record the fastest growth at a 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EU Energy-Efficiency and Decarbonization Mandates | +1.2% | EU-27, with concentrated near-term impact in Germany, France, Netherlands, and Italy | Short term (≤ 2 years) |

| Growing Adoption of AI-Enabled Predictive Maintenance Platforms | +0.9% | UK, Germany, Netherlands, and Nordic countries, with gradual spillover to Spain and Italy | Medium term (2-4 years) |

| Expansion of Outsourcing in Commercial Real Estate Portfolios | +0.8% | UK, Germany, France, Spain, and Italy | Short term (≤ 2 years) |

| Digital Twin and IoT Penetration in Aging Building Stock | +0.5% | DACH region, Nordics, UK, France, and Spain | Medium term (2-4 years) |

| Performance-Linked ESG Financing for Retrofit-Driven Contracts | +0.4% | Netherlands, Germany, Nordic countries, France, and Spain | Medium term (2-4 years) |

| Rise of Integrated FM in Mission-Critical Data-Center Clusters | +0.6% | Frankfurt, London, Amsterdam, Paris, Dublin, Madrid, Milan, and Warsaw | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening EU Energy-Efficiency and Decarbonization Mandates

The Europe integrated facility management market is being pulled forward by the recast Energy Performance of Buildings Directive, which entered into force in 2024 and set a firm timetable for national implementation and building upgrades. Non-residential buildings above 290 kW were required to install building automation and control systems by December, 2024, and Member States must transpose the broader directive by May, 2026.[1]European Parliament and Council, “Directive (EU) 2024/1275 of the European Parliament and of the Council of 24 April 2024 on the Energy Performance of Buildings (recast),” Official Journal of the European Union, eur-lex.europa.eu The same directive requires the worst-performing 16% of non-residential stock to meet minimum energy performance standards by 2030, and 26% by 2033, which keeps owners focused on staged improvement plans rather than one-time capital work. This matters for integrated operators because compliance now includes monitoring, commissioning, asset documentation, controls management, and coordination of mechanical and electrical upgrades while buildings remain occupied. The public estate is under added pressure because the Energy Efficiency Directive requires annual renovation of a share of public buildings and continued energy reduction efforts across the public sector. As a result, the Europe IFM market is benefiting from a shift toward longer contracts in which one provider is expected to link building performance, day-to-day operations, and compliance reporting under a single framework.

Growing Adoption Of AI-Enabled Predictive Maintenance Platforms

The Europe integrated facility management market is also benefiting from wider use of predictive maintenance tools that turn building telemetry into earlier fault detection and tighter intervention planning. A March 2026 peer-reviewed study in Frontiers in Built Environment validated a hybrid machine-learning framework for HVAC fault detection in non-residential buildings and reported diagnostic accuracy above 99.6% with random forest models trained on air handling unit telemetry. A June 2025 REHVA Journal case from Breda in the Netherlands showed that an AI-driven model predictive control upgrade reduced peak building demand by 28% and lowered peak demand charges by 24% to 30% without major physical intervention.[2]Jan-Willem Dubbeldam, Petros Zimianitis, Shalika Walker, and Joep van der Velden, “Towards Open-Structure BMS, AI for Forecasting and Predictive Control,” REHVA Journal, rehva.eu Those results are changing buyer expectations because hard-service contracts are now judged more often on avoided downtime, operating visibility, and energy performance than on the volume of reactive callouts alone. The labor effect is equally important, since connected diagnostics reduce routine inspection workloads while increasing the value of technicians who can interpret data streams and manage connected assets across multiple sites. That shift is widening the capability gap inside the Europe integrated facility management (IFM) market, because larger operators can spread software and analytics costs across national portfolios while smaller firms remain more exposed to manual service models.

Expansion Of Outsourcing In Commercial Real Estate Portfolios

The Europe integrated facility management market is seeing broader use of single-provider structures as occupiers and landlords simplify vendor oversight across office, retail, and mixed-use estates. Buyers are placing more weight on service consistency, governance, and reporting quality because leaner internal teams now need one operating partner that can coordinate workplace, technical, and support functions across several locations. In March 2026, ISS renewed and expanded its integrated facilities services contract with Virgin Media O2 in the UK and added a two-year transformation program focused on savings and improved data visibility across corporate, technical, and retail sites. That type of mandate shows how portfolio management has shifted away from isolated work orders and toward service models that combine operational delivery with platform oversight, workflow visibility, and performance management. Apleona’s August 2025 acquisition of Corrigenda in the UK also points to the same direction, because technical self-delivery has become more valuable when clients want fewer subcontracting layers across larger estates. The outcome is a Europe IFM market where switching costs are rising, since a new provider must take over site data, local compliance routines, asset knowledge, and service governance at the same time.

Rise Of Integrated FM In Mission-Critical Data-Center Clusters

The Europe integrated facility management market is receiving another clear lift from data-center buildout, because these sites require uninterrupted engineering coverage and deeper technical specialization than standard commercial assets. The European Data Centre Association projected European IT power demand to grow at a 17% CAGR through 2031, which signals sustained build activity and more operating complexity across colocation and hyperscale footprints.[3]European Data Centre Association, “State of European Data Centres 2026,” European Data Centre Association, eudca.org The same study identified EUR 176 billion (approximately USD 205 billion), in cumulative colocation and hyperscale construction investment from 2026 to 2031, giving FM providers a large pipeline of new and expanding facilities that will need managed support after commissioning. Frankfurt, London, Amsterdam, Paris, and Dublin remain the core hubs, while Madrid and Milan are becoming stronger secondary nodes within the same regional growth story. These sites depend on thermal management, electrical resilience, uptime routines, incident response, and structured maintenance windows that are difficult to manage through single-trade contracts alone. This operating profile is steering more mission-critical work toward multi-discipline providers, which keeps technical scope expansion firmly tied to the Europe IFM market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Multi-Trade Technician Shortage and Wage Inflation | -0.9% | Germany, Switzerland, Netherlands, UK, France, and Italy | Short term (≤ 2 years) |

| Fragmented EU Regulatory Framework Increasing Compliance Costs | -0.5% | EU-27, with concentrated impact on cross-border integrated FM operators | Medium term (2-4 years) |

| Cybersecurity Exposure in Connected Building Systems | -0.3% | UK, Germany, Netherlands, and Ireland | Short term (≤ 2 years) |

| Margin Pressure from Commoditization of Soft Services | -0.2% | UK, Germany, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Multi-Trade Technician Shortage and Wage Inflation

The Europe integrated facility management market is facing its most immediate operating constraint in the shortage of technicians who can combine mechanical, electrical, and digital building skills in the same role. The EURES shortage map identified high-severity gaps for air-conditioning and refrigeration mechanics, building electricians, and plumbers across several European labor markets that matter directly to hard-service delivery. DIHK reported for 2025-2026 that 36% of German companies had difficulty filling vacancies and that 63% expected higher labor costs, which points to sustained cost pressure in one of the region’s most important operating markets.[4]Association of German Chambers of Commerce and Industry, “Skilled Labour Report 2025-2026, Challenges Persist,” DIHK, dihk.de A September 2025 European Parliament study added that only 1 in 10 heating engineer roles in Germany could be adequately filled through conventional recruitment channels, showing how tight specialist labor has become in building-related trades. Eurostat recorded a 4.7% year-over-year rise in EU construction hourly labor costs in the third quarter of 2025, while the wider business economy rose 3.8%, which illustrates why labor-intensive contracts are becoming harder to price over multiple years. The result is a Europe integrated facility management (IFM) market where providers are accelerating automation, improving workforce planning, and becoming more selective on contracts that combine high technical intensity with weak inflation pass-through.

Fragmented EU Regulatory Framework Increasing Compliance Costs

The Europe integrated facility management market also has to operate through a fragmented compliance structure even when the broad EU policy direction is consistent across member states. Directive (EU) 2024/1275 still requires national transposition, which means minimum energy performance rules, building inventories, disclosure formats, and enforcement practices will differ from one country to another. That matters most for providers running healthcare, institutional, and commercial portfolios across borders, because they need separate documentation workflows and audit trails even when the client wants a single European contract. The burden grows further in public estates, where building renovation obligations under the Energy Efficiency Directive must be managed alongside national compliance requirements and local procurement rules. Each local variation raises governance and reporting costs, which weakens part of the savings case that originally made cross-border integrated contracting attractive to large occupiers and public bodies. That is why scale on its own does not ensure margin expansion in the Europe integrated facility management (IFM) market, especially when pan-European delivery still depends on locally compliant teams and country-specific controls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Services Pull Ahead On Regulatory Tailwinds

Hard Facility Management (Hard FM) is the faster-growing service category in the Europe integrated facility management market, advancing at a 5.71% CAGR from 2026 to 2031 as compliance work, controls rollout, and aging building systems keep technical demand elevated. The growth is being driven by sustained needs in asset management, MEP services, HVAC, fire systems, and building automation, because regulatory obligations are now tied more closely to operating performance than before. The BACS rollout extends that opportunity further, since the EPBD framework will widen the set of buildings that need more structured technical oversight over the next several years. This is shifting contract value toward lifecycle planning, condition-based maintenance, replacement scheduling, and compliance documentation rather than simple break-fix support. As a result, the Europe integrated facility management industry is leaning more heavily toward technical scopes that can connect energy outcomes, asset uptime, and reporting needs inside one operating model.

Soft Facility Management (Soft FM) remained the largest service segment and held 57.32% of revenue in 2025, which shows how important cleaning, catering, security, and office support still are across every major end-user group. The segment keeps a broad demand base because many occupiers continue to focus on workplace experience, hygiene standards, and day-to-day service continuity even when office footprints are being rationalized. Security-related soft services are also becoming more sensitive as access control, visitor flows, and connected monitoring systems move deeper into digital building environments. That creates a more technical operating layer inside what was once treated mainly as a labor-led service bundle, especially in assets with higher compliance requirements and larger visitor volumes. Even so, the Europe integrated facility management industry still depends on soft services for site coverage and occupant continuity, while pricing remains tighter because many activities are easier for buyers to benchmark and rebid.

By End User: Industrial Anchors Revenue While Commercial Clients Accelerate Demand

The industrial and process sector held the largest end-user position with 33.72% of revenue in 2025, reflecting the high service intensity of manufacturing plants, chemicals sites, and process-heavy facilities where safety, uptime, and compliance are tightly linked. These locations typically need hard and soft FM under one operating framework, because utility systems, fire and gas controls, maintenance planning, and site services all have to work in a coordinated way. Integrated delivery fits well in this setting since asset failures can disrupt production, raise compliance risk, and increase operating losses much faster than in standard office environments. The scale of technical work is also higher, which supports stronger contract values per site and rewards operators that can self-deliver more specialist services. In practice, this keeps industrial accounts central to the Europe integrated facility management market because complex operating environments continue to favor multi-service providers over fragmented vendor rosters.

Commercial end users are the fastest-growing segment, and Europe integrated facility management (IFM) market size for commercial portfolios is projected to expand at a 5.43% CAGR through 2031. The retained office space across leading cities is becoming more performance-led, with occupiers placing greater weight on energy efficiency, air quality, amenity standards, and reporting visibility in the buildings they keep. This favors operators that can connect technical maintenance, workplace services, and compliance documentation rather than offering these functions through separate contracts. Healthcare and institutional facilities are also adding durable demand because hospitals need stronger HVAC validation and public estates must continue to improve building performance under EU energy rules. The Europe integrated facility management industry is therefore drawing growth from upgraded offices, critical care environments, and public-sector assets at the same time, which broadens demand beyond any one client category.

Geography Analysis

Germany held 21.69% of the Europe integrated facility management market share in 2025, which kept it in the leading national position across the region. The country’s weight reflects dense industrial activity, mature outsourcing practices, and a regulatory setting that already places high importance on technical building performance and compliance management. Germany also sits close to the center of the region’s retrofit and controls agenda, because EPBD requirements are pushing owners toward more structured asset oversight and higher-value technical contracts. That combination keeps Germany important not only for revenue concentration, but also for contract design, service standard setting, and consolidation activity across the wider market.

Spain is the fastest-growing country in the Europe integrated facility management market and is forecast to record a 6.65% CAGR through 2031. Growth is being supported by wider outsourcing acceptance, a strong hospitality base, and rising demand for multi-site service coordination in urban commercial portfolios. Southern Europe, including Spain, Italy, and Portugal, is expected by EUDCA to be the fastest-growing data-center region through 2031, which raises the strategic importance of Madrid and Barcelona as technical service locations. That matters because new digital infrastructure still requires mature FM execution in power, cooling, uptime support, and emergency response, even when the regional market is earlier in its outsourcing cycle. Spain also stands to benefit from the same EU building-performance obligations shaping the rest of the region, which should keep retrofit-linked technical work moving into integrated contract structures.

The United Kingdom remains a core Europe integrated facility management market with a long outsourcing tradition and dense corporate and public-estate demand. ISS renewed and expanded its contract with Virgin Media O2 in March 2026, which illustrates continued appetite for integrated delivery across corporate, technical, and retail sites in the. France and Italy continue to offer above-average opportunity because both have large aging commercial and institutional building stocks that will need modernization, controls upgrades, and stronger energy-performance management under EU rules. The rest of Europe combines mature Nordic demand with rising activity in Central and Eastern Europe, where manufacturing expansion and new digital infrastructure are broadening the addressable service base for integrated operators.

Competitive Landscape

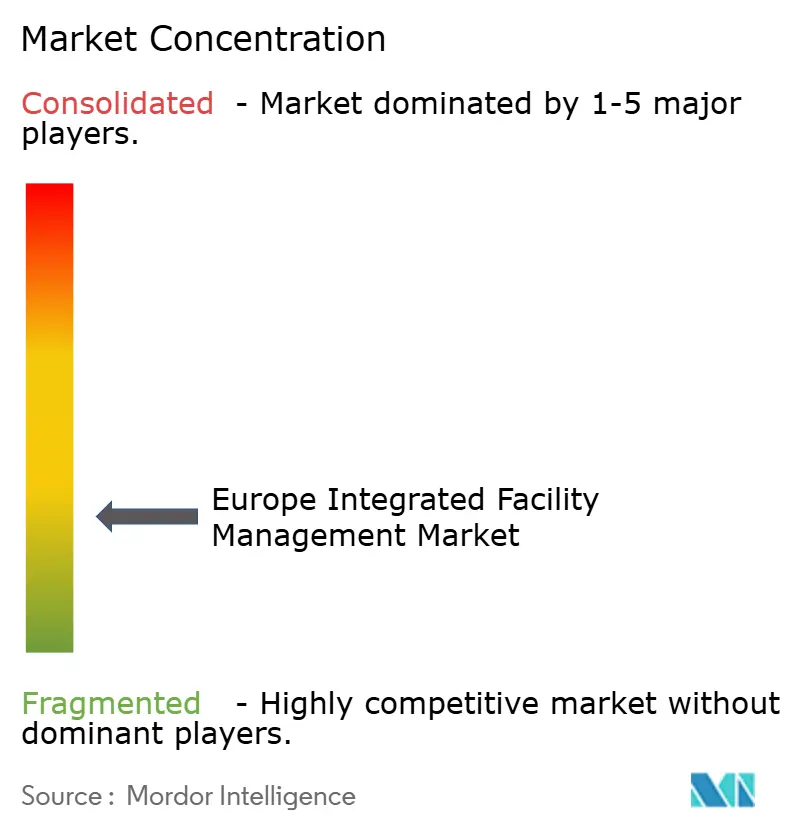

The Europe integrated facility management market remains moderately fragmented, with multinational operators such as ISS A/S, Sodexo S.A., CBRE Group, Inc., Compass Group plc, and Apleona GmbH active across several countries and service lines, while many regional firms still hold strong local positions. Fragmentation is visible in Germany, where the top 10 providers accounted for only 17.5% of national sector revenue in 2024, leaving a large mid-market field and limiting concentration at the regional level. This structure keeps pricing power uneven and makes investment capacity highly variable from one provider group to another. It also means that large buyers often compare vendors on self-delivery depth, vertical specialization, governance quality, and digital reporting rather than on headline scale alone.

Apleona strengthened its footprint in Ireland in April 2024 through the acquisition of Neylons Facility Management, which added local service capability in a market that continues to professionalize outsourced delivery. In August 2025, Apleona also acquired Corrigenda in the UK, which expanded technical capability in public sector and education facilities and added more self-delivered engineering capacity. ISS renewed and expanded its integrated facilities services contract with Virgin Media O2 in March 2026, pairing the operating mandate with a transformation program aimed at better data visibility and service transparency. In January 2026, ISS also moved from subcontractor to primary partner for a major life sciences and pharmaceutical customer in Switzerland, broadening its role across technical maintenance, cleaning, logistics, and laboratory services. These moves show that leading companies are not relying on scale alone, because they are building denser technical capability, wider geographic coverage, and more control over specialist service delivery.

Technology is becoming a stronger separator in the Europe integrated facility management market as buyers expect predictive maintenance, energy monitoring, and clearer operating data from large service partners. Claroty’s June 2025 review of more than 467,000 building management systems found that 75% of organizations had BMS devices affected by known exploited vulnerabilities and that 51% had systems insecurely connected to the internet, which raises the delivery threshold for operators managing connected assets. Techem’s August 2025 Green Contracting project in Eschborn combined heat pumps, photovoltaics, and AI-enabled monitoring under a 20-year contract, reflecting the market shift toward performance-linked and technology-supported building operation. The clearest opening now sits in retrofit-led sustainability services, mission-critical facilities, and digitally underserved mid-sized portfolios where only a limited set of operators can combine technical depth with platform capability.

Europe Integrated Facility Management Industry Leaders

ISS A/S

Sodexo S.A.

CBRE Group, Inc.

Compass Group Plc

Mitie Group Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Claroty Team82 disclosed two critical vulnerabilities (CVE-2026-20761, CVSS 8.1) in EnOcean SmartServer IoT platforms used in building management systems, allowing unauthenticated remote code execution, a finding that directly implicates FM operators responsible for managing BMS security and reinforces demand for operators with embedded OT cybersecurity capability.

- March 2026: ISS renewed and expanded its Integrated Facilities Services contract with Virgin Media O2 in the UK, including a two-year transformation program to deliver financial savings and a digitalization strategy to improve data visibility and transparency across corporate, technical, and retail sites.

- January 2026: ISS won a full Integrated Facilities Services contract with a major life sciences and pharmaceutical company in Switzerland, valued at nearly DKK 300 million (approximately USD 47 million) annually across four Swiss locations, transitioning ISS from subcontractor to primary partner for technical maintenance, cleaning, logistics, and laboratory services.

- January 2026: GEFMA (the German Association for Facility Management) published its GEFMA 140 guideline on Integrated Facility Management, providing a regulatory and commercial framework for clients, service providers, and consultants to structure IFM contracts, evaluate governance models, and adapt international IFM approaches to German market conditions, with ESG requirements, digitalization, and AI explicitly identified as key shaping forces.

- August 2025: Apleona acquired Corrigenda, a technical FM company in the UK specializing in public sector and education facility management with approximately 200 employees including 140 technicians, marking Apleona's third UK acquisition since 2022 as it builds self-delivering technical capability for decarbonization-linked contracts.

Europe Integrated Facility Management Market Report Scope

The Europe Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels),Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)), and Geography (UK, Germany, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

| By Geographic | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current and forecast size of the Europe integrated facility management market?

The Europe integrated facility management market was valued at USD 78.70 billion in 2025, stands at USD 82.16 billion in 2026, and is forecast to reach USD 104.79 billion by 2031 at a 4.99% CAGR.

Which service type leads revenue in Europe integrated facility management?

Soft facility management led the market in 2025 with a 57.32% revenue share, supported by recurring demand for cleaning, catering, security, and workplace support across end-user groups.

Which end-user group generates the highest demand?

The industrial and process sector held the largest end-user share at 33.72% in 2025, reflecting the high service intensity of manufacturing, chemicals, and process-heavy facilities.

Which country is growing the fastest in Europe?

Spain is forecast to be the fastest-growing country through 2031 with a 6.65% CAGR, supported by wider outsourcing acceptance and rising technical demand from new data-center clusters.

What is driving growth in integrated facility management across Europe?

Growth is being supported by tighter energy-efficiency rules, wider use of predictive maintenance, deeper outsourcing across large estates, and stronger demand from mission-critical data centers.

What is the main challenge facing service providers?

The biggest operating constraint is the shortage of multi-trade technicians, which is increasing wage pressure and making it harder to staff technically complex multi-site contracts.

Page last updated on: