Italy Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.10 Billion |

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 2.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Containerboard Market Analysis by Mordor Intelligence

The Italy containerboard market size is expected to increase from USD 3.10 billion in 2025 to USD 3.18 billion in 2026 and reach USD 3.62 billion by 2031, growing at a CAGR of 2.63% over 2026-2031. Italy remained the second-largest corrugated cardboard producer in Europe in 2025, which reflects the depth of its fiber recovery system and the close link between paper packaging supply and agri-food packaging demand. Domestic demand is also shifting toward single-item protective packaging as e-commerce volumes keep rising across retail categories and more parcels move through last-mile channels. At the same time, the new EU packaging and packaging waste framework entered into force in early 2025 and starts applying from August 2026, which supports recyclable mono-material paper formats over harder-to-recycle alternatives. New capacity at major sites such as Verzuolo and Duino has improved supply depth, but import pressure in higher-performance grades and persistent energy costs still limit how quickly domestic producers can recover share. This leaves the strongest opportunities in higher-strength liners, export-oriented food packaging, and logistics applications where board quality matters more than simple volume growth.

Key Report Takeaways

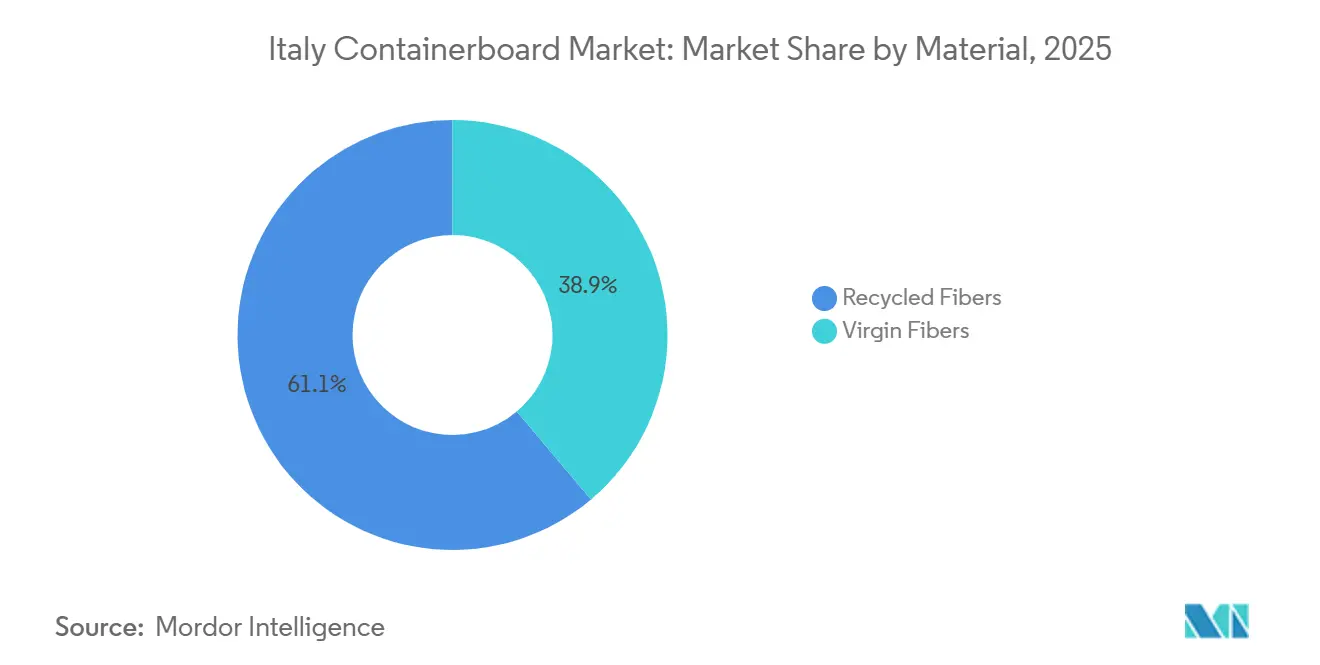

- By material, recycled fibers captured 61.13% of the Italy containerboard market share in 2025.

- By product type, the Italy containerboard market size for the kraftliners segment is forecast to advance at a 3.08% CAGR through 2031.

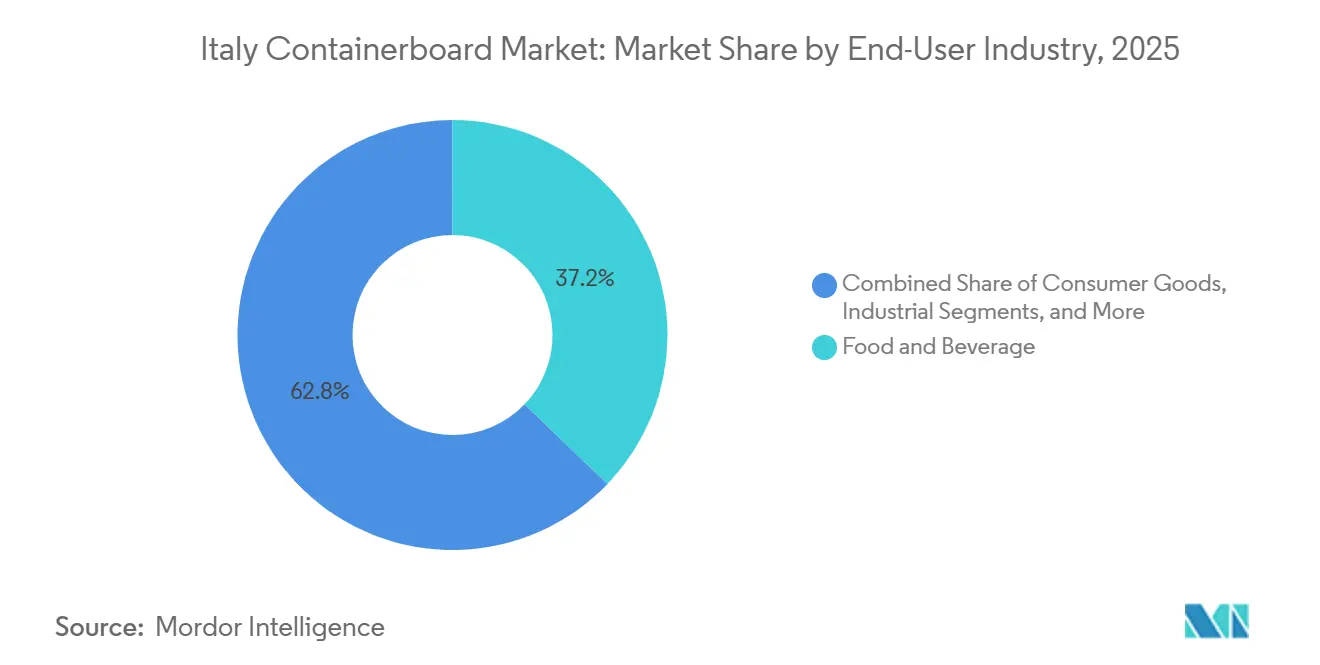

- By end-user industry, food and beverage captured 37.19% of the Italy containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce and Omnichannel Corrugated Demand | +0.8% | Italy-wide, concentrated in Northern Italy logistics hubs including Lombardy, Emilia-Romagna, and Veneto, with growing spillover to Central Italy | Short term (≤ 2 years) |

| Plastic-to-Paperboard Substitution in Secondary Packaging | +0.6% | Italy-wide, strongest in packaging-dense industrial districts of Emilia-Romagna, Veneto, and Tuscany | Medium term (2-4 years) |

| High Recovered Fiber Collection and Recovery Rates in Italy | +0.4% | Italy-wide, with the north leading and the south improving collection performance | Short term (≤ 2 years) |

| Food and Beverage Export and Fresh Produce Logistics Demand | +0.3% | North-central Italy agri-food districts and export corridors into Central and Northern Europe | Medium term (2-4 years) |

| PPWR Readiness Favoring Recyclable Mono-Material Packs | +0.2% | EU-wide regulation directly applicable to Italy from August 12, 2026 | Medium term (2-4 years) |

| Lightweighting Economics After New Recycled Capacity Start-Ups | +0.1% | Global, with Italy among the primary beneficiaries of new low-grammage lines commissioned in 2025 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce and Omnichannel Corrugated Demand

The Italian containerboard market is receiving steady support from parcel growth, as B2C e-commerce continued to expand in 2025 and online penetration rose across product categories.[1]Netcomm and Politecnico di Milano, “Cresce l'Ecommerce B2C in Italia, +6% Nel 2025, a Quota 62 Miliardi di Euro,” Engage, engage.it Italy’s B2C e-commerce product segment reached EUR 40 billion (USD 45.1 billion) in 2025, while online penetration of retail product sales rose to 11.2% from 10.7% in the prior year. Single-item shipment formats use 30% to 50% more board per unit than consolidated pallet formats, allowing board demand to rise faster than the merchandise base itself. Demand is also spreading geographically, as daily online use in southern regions and the islands reached 60.6% of adults in 2026, narrowing the long-standing digital divide with the north.[2]Casaleggio Associati, “Ecommerce Italy 2026,” Ecommerce Italy, ecommerceitalia.info Research presented in early 2026 also showed that 75% of Italian consumers viewed the parcel receipt as their primary physical point of contact with corrugated cardboard, keeping paper-based shipping formats central to last-mile retail.[3]Redazione Converting, “Il Ruolo Strategico Dell'Imballaggio in Cartone Ondulato,” Converting Magazine, convertingmagazine.it

Plastic-to-Paperboard Substitution in Secondary Packaging

The Italy containerboard market is also benefiting from a broader switch away from plastic in secondary and transit packaging, especially where easier recycling and simpler reverse logistics matter to buyers. Research released in January 2026 showed that 51% of Italian user companies had replaced flexible plastics with corrugated cardboard, while 55% of consumers said corrugated had become more common than bubble wrap and rigid plastic components in delivered packages. This change is not tied solely to regulation, because corrugated packaging also reduces sorting friction and fits more easily into the paper recycling stream after use. Secondary packaging substitution often requires heavier, stronger board grades that support value growth in testliner and other specifications that can handle higher stacking loads. The policy backdrop is becoming more favorable as well, as the European Commission’s PPWR guidance establishes a framework that favors easily recyclable packaging and will apply in Italy from August 2026.[4]European Commission Directorate-General for Environment, “Guidance Document on Packaging and Packaging Waste Regulation (PPWR),” European Commission, europa.eu

High Recovered Fiber Collection and Recovery Rates in Italy

The Italian containerboard market continues to benefit from a clear cost and supply advantage stemming from the country’s recovered fiber system. Separate collection of paper and cardboard reached 3.8 million tonnes in 2024, up 3.5% from 2023, and the recycling rate for cellulosic packaging reached 92.5%. That result was more than 7 percentage points above the European Union’s 2030 target of 85%, which shows how far the national system is already operating ahead of the regulatory threshold. The country also had 346 Comieco-managed sorting and pressing facilities, and commercial and industrial collection exceeded 2.3 million tonnes, which is especially relevant for containerboard furnish quality. Another favorable shift appeared in trade flows, because exports of collected paper to overseas mills fell by 16% to 1.41 million tonnes in 2025, leaving more recovered fiber available for domestic mill use.

Food and Beverage Export and Fresh Produce Logistics Demand

The Italian containerboard market remains closely tied to the food and beverage chain, where box performance under humidity and long-distance handling matters more than in many other end uses. Food applications accounted for 62.7% of Italian corrugated packaging output in 2024, confirming that food-related demand remains the primary load-bearing use for board producers and converters. That mix stayed resilient even when broader production conditions were softer, so the category acts more like a demand floor than a swing factor. Smurfit WestRock’s Italian operations have developed temperature-stable corrugated formats for fruit, vegetables, and gastronomy, demonstrating how suppliers are aligning product design with cold-chain and fresh produce needs. As retailers expand omnichannel food distribution, more produce units move in individually packed formats, which lifts demand for stronger liner and fluting grades across export and domestic routes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Electricity and Gas Cost Burden | -0.5% | Italy-wide, most acute for continuous-process recycled fiber mills, with a structural gap versus Germany, France, and Spain | Short term (≤ 2 years) |

| Recovered Paper Price and Quality Volatility | -0.3% | Italy-wide, with higher contamination rates in parts of Southern Italy | Short term (≤ 2 years) |

| PPWR Compliance and Documentation Costs for Smaller Converters | -0.1% | EU-wide, amplified for Italy’s large base of small and medium corrugated converters | Medium term (2-4 years) |

| Imported Kraftliner Pressure in High-Performance Grades | -0.1% | Italy-wide, with exposure to exchange-rate and freight movements in imported virgin fiber papers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Electricity And Gas Cost Burden

The Italy containerboard market still faces a structural cost burden from energy, and that pressure is stronger than in the main competing paper-producing countries in Europe. Confindustria reported that Italian industrial electricity prices in 2025 were around 30% above the EU average and remained higher than those in Germany, France, and Spain. This matters deeply for paper mills because energy has historically accounted for more than 40% of operating costs in Italian paper production. The sector also depends on natural gas for more than 95% of its heat requirements, so producers cannot easily absorb wide differences in national power and fuel pricing. Industry representatives warned in early 2025 that this gap threatened competitiveness across a supply chain employing 700,000 workers, underscoring that the issue extends beyond individual mills.

Recovered Paper Price And Quality Volatility

The Italy containerboard market is also exposed to swings in recovered paper costs, which are especially difficult for recycled board producers to absorb when selling prices adjust more slowly than input prices. EUWID reported that a rise in ordinary recovered paper grades in March 2025 increased cost pressure for recycled corrugated case material producers and that published mark-ups were not enough to offset it. Quality adds a second layer of pressure, because Comieco noted that around 40% of household paper collection in Southern Italy carried contamination levels above the national average of under 3%. That means mills and sorting facilities face extra work to secure usable fiber, which raises effective raw material cost per tonne. Comieco’s EUR 3.5 million (USD 3.8 million) Piano Straordinario per il Sud aims to intercept 350,000 tonnes of paper and cardboard that still enter unsorted waste streams, underscoring both the size of the current gap and the room for improvement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Shaped By Infrastructure Depth

Recycled fibers held 61.13% of Italy's containerboard market share in 2025, reflecting infrastructure depth more than simple price preference. Italy used recycled paper for 63% of its fiber mix in paper production, ranking second in Europe for total recovered fiber consumption after Germany. This supply base helps the Italy containerboard market keep a strong domestic position in recycled grades, because furnishes can be sourced through a mature national collection and sorting system. Mondi’s EUR 200 million (USD 214 million) conversion of the Duino mill to 420,000 tonnes per year of recycled containerboard, completed in April 2025, showed that a major producer viewed the Italian recovered fiber chain as dependable enough for a flagship project.

Virgin fibers are forecast to grow at a CAGR of 2.94% between 2026 and 2031, which makes them the fastest-expanding material base, even from a smaller starting point. The Italy containerboard market is seeing this pull from exporters of fresh produce and premium consumer goods that need stronger burst performance, better printability, and a more uniform surface quality than recycled grades can consistently deliver at lighter weights. Italy also remained highly exposed to imported virgin kraft paper, indicating that this part of the supply chain still has a structural domestic gap. Certification standards already appear well established, because 90% of virgin fibers used in Italian mills carried FSC or PEFC certification in 2024, which supports procurement transparency for larger buyers.

By Product Type: Testliner Scale, Kraftliner Growth Premium

Testliners accounted for 42.35% of the Italy containerboard market in 2025, reflecting their close fit with a production system centered on recovered fiber and broad-use corrugated applications. The Italy containerboard industry relied heavily on integrated domestic mills for this grade, which helped testliners remain the standard material across food, industrial, and consumer goods box formats. Smurfit WestRock’s Verzuolo mill alone had 551,000 tonnes per year of recycled containerboard capacity in 2025, with its output mix weighted toward testliner and corrugating medium. That capacity depth gives the Italy containerboard market a practical advantage in high-volume recycled grades where local mills and box plants remain tightly linked.

Kraftliners are forecast to grow at the fastest CAGR of 3.08% through 2031, supported by demand from food exporters and by the move away from plastic secondary packaging in applications that require stronger box performance. The Italy containerboard market is also seeing increased demand for consistent burst strength across longer export routes, which favors kraftliner, as box failure carries a higher logistics risk. Flutings remain essential as the middle layer in single-wall and double-wall formats, and Mondi’s Duino machine started up with waste-based fluting from 80 gsm upward to address lightweighting needs without sacrificing compression strength. The Italy containerboard industry therefore has a broad product base, but premium-grade liners still offer the clearest room for value growth, as converters continue to rely on imports to meet some high-performance requirements.

By End-User Industry: Food And Beverage As The Floor, Consumer Goods As The Growth Pocket

Food and beverage accounted for 37.19% of Italy's containerboard market share in 2025, making it the sector's core demand base. GIFCO data presented in 2025 showed that 62.7% of total Italian corrugated output by volume served food applications in 2024, covering fresh produce, ambient food, beverages, meat, and fish. The Italy containerboard market, therefore, depends on a use case that holds up better than many discretionary categories during weaker industrial periods. Smurfit Westrock’s Italian portfolio includes temperature-management corrugated formats and horticultural packaging for the food and gastronomy segment, which shows how leading suppliers have built product design around this base demand.

Consumer goods are forecast to grow at the fastest CAGR of 3.01% from 2026 to 2031, supported by the spread of single-item e-commerce fulfillment in categories such as beauty, pharma, electronics, accessories, and home living products. The Italy containerboard market is seeing this channel become more important because parcel packaging requires repeat board use even when basket sizes are small. Industrial end users remain a stable outlet for heavier-weight kraftliner and double-wall specifications tied to machinery parts, spare components, and materials handling. Other categories, such as pet food and hobbies and leisure, are also opening smaller but meaningful pockets of demand, and GIFCO identified pet food as a new growth area for the Italian corrugated segment, as it requires stronger, more moisture-resistant board grades.

Geography Analysis

Northern Italy accounted for the largest share of demand and production in the Italy containerboard market in 2025, supported by the dense industrial arc across Lombardy, Emilia-Romagna, and Veneto. Emilia-Romagna recorded a recovered paper collection of close to 100 kg per inhabitant in 2024, while Lombardy collected more than 613,000 tonnes, underscoring the maturity of the northern supply base. Major mill assets are also concentrated there, including Smurfit Westrock’s Verzuolo mill in Cuneo, Mondi’s Duino site near Trieste, and DS Smith’s Porcari mill near Lucca. This cluster effect gives northern producers better access to recovered fiber, conversion capacity, and export infrastructure than other parts of the country. The north also serves as a key route for agri-food exports into Central and Northern Europe, which keeps demand firm for humidity-resistant liners and fluting across fresh produce and dairy logistics.

Central Italy is emerging as the fastest-rising sub-national demand zone in the Italy containerboard market, especially as logistics and conversion activity spread beyond the traditional northern base. Corrugated manufacturing volumes in Lazio, Umbria, and Abruzzo rose 13.1% during a period when Lombardy’s share of national production declined, which points to a broader geographic rebalance in box demand. Rome’s metropolitan area collected more than 258,000 tonnes of paper and cardboard in 2024, up by around 11,000 tonnes, signaling improvement in a market that had long lagged behind stronger collection regions. This shift reduces the Italy containerboard market’s reliance on a single northern production center and creates more balanced demand around central fulfillment hubs.

Southern Italy and the islands remain less developed in terms of mill density, but the Italian containerboard market is gradually gaining support from improved collection performance in these regions. Southern Italy crossed the 50 kg per-capita recovered paper collection threshold for the first time in 2024 and moved toward 1 million tonnes of annual collected volume. Even so, 350,000 tonnes of paper and cardboard remained outside differentiated collection systems, indicating that the region still has a raw material gap and a clear expansion opportunity. Southern converters remain more exposed to imported board because the domestic mill supply is thinner there, and Italian producers continue to face energy-cost disadvantages compared to other European sources.

Competitive Landscape

The Italy containerboard market is moderately concentrated around a small group of large integrated producers, but it still includes a broad field of specialized mid-scale suppliers and a downstream base of around 300 corrugated converter enterprises. Smurfit Westrock and Mondi hold some of the most important mill positions, with Smurfit Westrock operating in Verzuolo and Ania, and Mondi adding 420,000 tonnes per year of recycled containerboard capacity at Duino in April 2025. Smurfit Westrock strengthened backward integration in April 2025 by opening a new recovered fiber recycling plant at Verzuolo, which became its second recovered paper processing facility in Italy. Mondi followed a different but equally significant route by converting Duino into a large recycled containerboard site that serves Italy and nearby export markets through Adriatic access. Progroup added another competitive model through its sheetfeeder plants in Drizzona and Cessalto, using containerboard produced at German mills and supplying the Italian market through a tightly integrated corrugated format.

The clearest white space in the Italy containerboard market remains in higher-performance grades where domestic production is still limited. Italian converters continue to depend on imported virgin-fiber kraftliner, specialty fluting with moisture resistance, and white-top testliner for premium printing and food-service applications, because no local mill has commissioned a primary kraft fiber line in the last 2 decades. Burgo Group has shown that repositioning is possible, as its Avezzano and Sora sites produced recycled testliner and fluting grades with Blue Angel and EU Ecolabel certification, but the 2024 output of 184,000 tonnes remained modest relative to the overall market. Pro-Gest, the country’s largest independent containerboard manufacturer, signed a binding debt restructuring agreement in January 2026, which preserved continuity but also limited near-term room for large capacity upgrades.

Smaller domestic firms face a more challenging operating backdrop in Italy's containerboard market because compliance costs, raw material swings, and energy pressures are easier to absorb at scale than in family-owned conversion businesses. VPK Group’s acquisition of Open Imballaggi in April 2025 showed that international players still see room to expand through local conversion assets rather than only through paper machine investment. Competition is therefore being shaped by a mix of recovered fiber integration, certified sustainable packaging, and selective expansion into value-added grades rather than by simple volume additions alone. This keeps the market active and prevents dominance by a single group, even though the largest operators still set the pace for investment, sourcing, and product development.

Italy Containerboard Industry Leaders

Pro-Gest S.p.A.

Smurfit Westrock plc

Mondi plc

International Paper Italia S.r.l.

Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Pro-Gest signed a binding debt restructuring agreement with its principal financial creditors through Italy's out-of-court CNC mechanism. Debt maturity was extended to 2030, with a creditor option to extend to 2032, while the Zago family retained 100% ownership. The agreement involved interest rate reprofiling, partial write-off of accrued interest, and an asset disposal program covering approximately EUR 80 million (USD 86 million) of real estate and selected operating units.

- December 2025: DS Smith idled one of the two existing recycled corrugated case material machines at its Porcari mill near Lucca to prepare for the new PM3 machine installation, temporarily reducing the site's operational capacity ahead of the new line's commercial startup.

- September 2025: Mondi held the official commercial inauguration ceremony for its Duino recycled containerboard mill in Italy, with international customers in attendance. The facility, which started mechanical operations in April 2025 following a EUR 200 million (USD 214 million) conversion investment, began supplying waste-based fluting from 80 gsm and testliner from 90 gsm to regional customers in Italy, Central Europe, and Turkey via nearby Adriatic port access.

- September 2025: Mondi Group reorganized its business units effective October 1, 2025, combining its Uncoated Fine Paper business unit with Corrugated Packaging to form an enlarged Corrugated Packaging business unit, which includes Italian operations at Duino and multiple converting sites.

Italy Containerboard Market Report Scope

The Italy Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The Italy Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Italy containerboard market?

The Italy containerboard market was valued at USD 3.10 billion in 2025 and is valued at USD 3.18 billion in 2026. It is projected to reach USD 3.62 billion by 2031 at a 2.63% CAGR, according to Mordor intelligence.

Which material type leads containerboard demand in Italy?

Recycled fibers led the market in 2025 with a 61.13% share, supported by Italy's strong paper collection and recycling system.

Which product type is growing fastest in Italy?

Kraftliners are forecast to grow at the fastest pace, with a 3.08% CAGR through 2031, as exporters and higher-strength packaging uses expand.

Why does food and beverage matter so much for demand in Italy?

Food and beverage accounted for 37.19% of consumption in 2025 and remained the largest end-user base, giving the sector a steady source of demand.

What is the main cost challenge for producers in Italy?

Energy remains the biggest structural pressure, because Italian mills continue to face electricity and gas costs above major European peers.

Which regions matter most for production and demand?

Northern Italy remains the main production and demand center, while Central Italy is becoming a faster-growing area as logistics and box conversion spread outward from the traditional northern base.

Page last updated on: