France Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.12 Billion |

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 3.42 Billion |

| Growth Rate (2026 - 2031) | 1.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Containerboard Market Analysis by Mordor Intelligence

The France containerboard market size is projected to expand from USD 3.12 billion in 2025 and USD 3.19 billion in 2026 to USD 3.42 billion by 2031, at a CAGR of 1.41% over 2026-2031. The France containerboard market is growing slowly because large new capacity at Alizay and Golbey has increased domestic supply faster than corrugated demand has recovered, keeping recycled-grade pricing under pressure. French paper and board mills produced 6.5 million tonnes in 2025, and the early 2026 backdrop already showed closures and commercial strain at some operations, which points to weaker cost absorption across the sector. The France containerboard market still has a long-term demand floor, as the AGEC law and the EU Packaging and Packaging Waste Regulation are pushing brand owners away from single-use plastics toward fiber-based formats. Energy costs remain a clear risk because mills still exposed to elevated power prices face tighter margins than operators that have already shifted toward biomass or biogas. Integrated producers with captive recycled-fiber loops, low-cost mills, and premium-grade exposure are better positioned than smaller converters, keeping growth opportunities centered on higher-specification food, e-commerce, and consumer goods packaging rather than broad-based volume expansion.

Key Report Takeaways

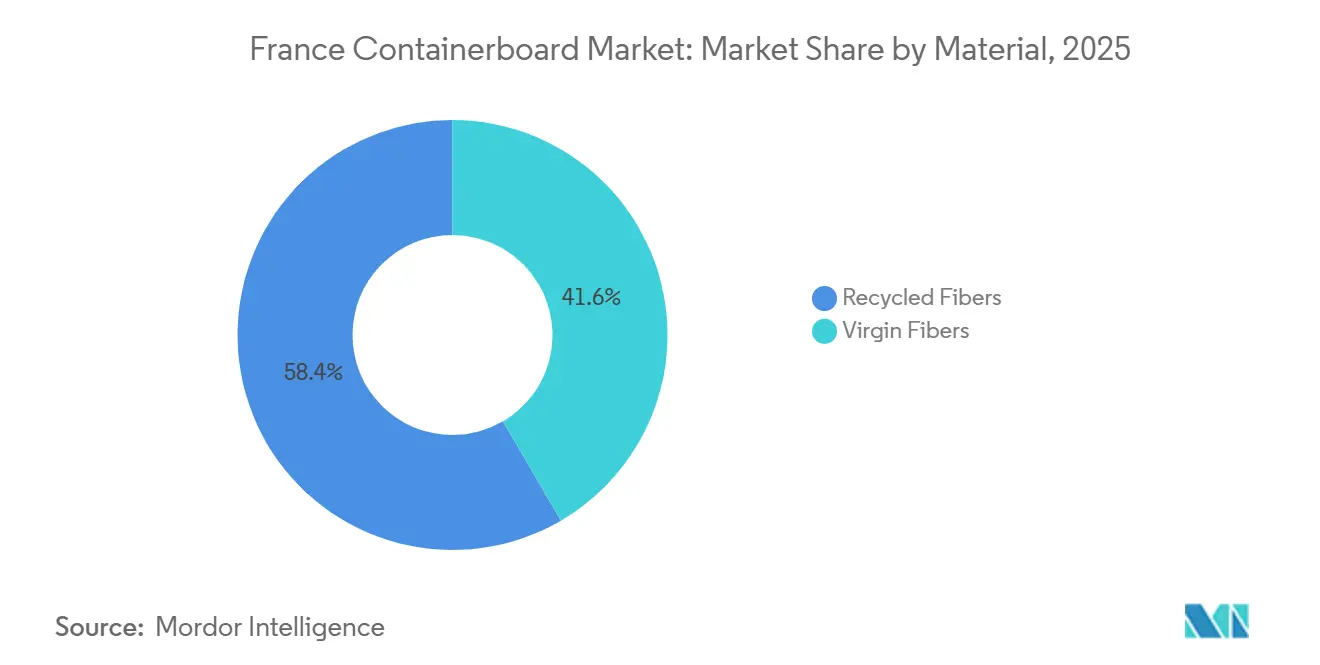

- By material, recycled fibers captured 58.41% of the France containerboard market share in 2025.

- By product type, the France containerboard market size for the kraftliners segment is forecast to advance at a 1.79% CAGR through 2031.

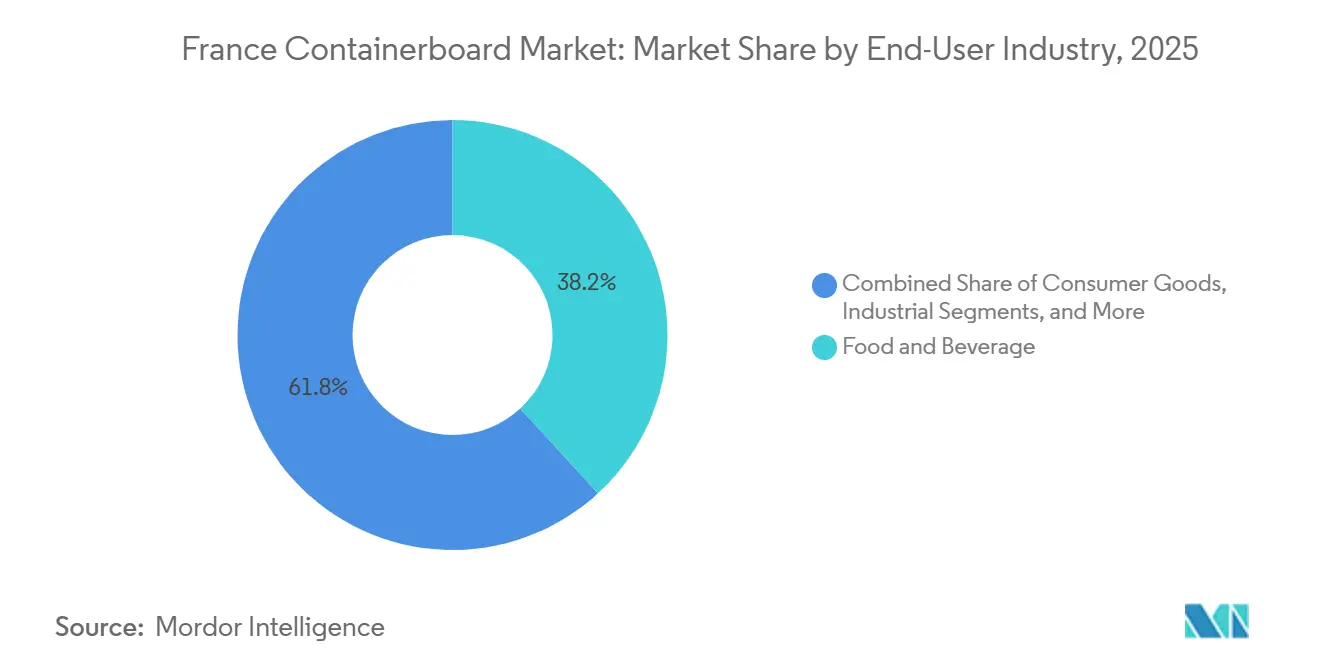

- By end-user industry, food and beverage captured 38.16% of the France containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Fiber Substitution Under AGEC And PPWR | +0.5% | France-wide, with spill-over to EU export markets | Medium term (2-4 years) |

| E-Commerce And Shelf-Ready Packaging Optimization | +0.4% | France-wide, concentrated in Ile-de-France and Lyon logistics corridors | Medium term (2-4 years) |

| Food And Beverage Corrugated Demand Resilience | +0.3% | France-wide, strongest in Bretagne and Auvergne-Rhone-Alpes food production clusters | Short term (≤ 2 years) |

| Alizay And Golbey Capacity Reshaping Domestic Supply | +0.2% | Northern and Eastern France, including Normandy and the Vosges | Short term (≤ 2 years) |

| Biomass-Led Decarbonized Mill Economics | +0.1% | Normandy, the Vosges, and Rhone-Alpes | Long term (≥ 4 years) |

| Rising Demand For Sustainable Packaging Solutions | +0.1% | Global, with concentrated impact in French retail and FMCG end markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Fiber Substitution Under AGEC And PPWR

France’s AGEC framework and the EU Packaging and Packaging Waste Regulation adopted in 2025 remain the clearest medium-term support for the France containerboard market. Decree No. 2022-748 requires producers and importers above the stated thresholds to disclose recyclability characteristics and recycled-content percentages from January 1, 2025, thereby making packaging composition more visible to buyers and regulators. The same policy direction increases the commercial appeal of recyclable fiber grades in secondary and transit packaging, especially where plastic formats face weaker compliance economics. It is also expanding the addressable space for higher-value grades, such as white-top testliner and coated containerboard, in food, cosmetics, and other presentation-sensitive uses. This keeps regulatory demand support in place even while the near-term volume picture for the France containerboard market remains restrained.

E-Commerce And Shelf-Ready Packaging Optimization

Online retail continues to support the France containerboard market because corrugated use per shipment is higher than in traditional store-led distribution. E-commerce accounted for 13% of French retail sales in 2025, and parcel volumes exceeded 1 billion units, while packaging intensity per shipment was up to 60% above in-store requirements. VPK Group has already aligned part of its Alizay strategy with that demand by deploying a high-definition digital printing platform for fanfold corrugated formats used in right-sized shipping.[1]VPK Group, “Sustainability Report 2024,” VPK Group, vpkgroup.com Shelf-ready packaging is also gaining ground in French food retail, and that shift favors higher-specification liner grades that combine better print performance with recyclability. Over time, this channel mix is likely to support value growth in the France containerboard market more than simple tonnage growth.

Food And Beverage Corrugated Demand Resilience

Food and beverage remained the largest end-user base for the France containerboard market, with a 38.16% share in 2025. France’s food and beverage manufacturing sector reached EUR 176.7 billion (USD 188.5 billion) in 2025, providing corrugated packaging with a broad and steady demand base across fresh produce, dairy, frozen foods, and transit applications. Norske Skog Golbey states that its containerboard grades are certified for food-contact applications and are produced under ISO 9001 and ISO 14001 systems, which helps the mill compete for more specification-sensitive packaging demand.[2]Norske Skog ASA, “Milestone Event With Start Of Containerboard Production At Norske Skog Golbey,” Norske Skog ASA, norskeskog.com That matters because food demand is more closely linked to routine consumption than to the industrial cycle, making it more stable than several other corrugated end markets. This segment, therefore, continues to act as an anchor for the French containerboard market even while broader recycled-grade pricing remains weak.

Alizay And Golbey Capacity Reshaping Domestic Supply

VPK Group’s Alizay mill and Norske Skog’s Golbey PM1 have changed the supply profile of the French containerboard market by adding two large recycled containerboard platforms within a short period. VPK’s Alizay project involved EUR 200 million (USD 215 million) and used 100% recycled fiber sourced within a 250-kilometer radius, and operated a 50 MW biomass power plant.[3]Valmet, “Aiming For Net-Zero With Every Decision, VPK Group’s Grade Conversion In Alizay, France,” Valmet, valmet.com Norske Skog’s Golbey investment, totaling EUR 400 million (USD 453 million), started containerboard production in May 2025 and was operating at 50-60% utilization by the end of 2025, with 95% utilization targeted for H1 2027.[4]Norske Skog Golbey, “Containerboard Manufacturer, Norske Skog Golbey,” Norske Skog Golbey, norskeskog-golbey.com Both assets were built around low-carbon mill economics, which improves their long-run cost position as customer scrutiny on emissions rises. Saica’s 3 French mills together add 1,045,000 tonnes of annual production capacity, making France a dense cluster of large integrated supply within Western Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Recycled Containerboard Overcapacity | -0.5% | France-wide, with pressure from Belgian, German, and Spanish imports | Short term (≤ 2 years) |

| EPR, EUDR, And Traceability Cost Stack | -0.3% | France-wide, concentrated on converters and brand owners | Medium term (2-4 years) |

| Energy-Price Volatility And Weak Industrial Output | -0.2% | France-wide, with notable exposure for Normandy and Alsace mills | Medium term (2-4 years) |

| Margin Pressure From Imported Brown Recycled Fiber | -0.1% | France-wide, strongest for mills dependent on spot-market OCC procurement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

European Recycled Containerboard Overcapacity

European supply additions have outpaced demand recovery, and this remains the main brake on the French containerboard market. Industry reporting shows that containerboard operating rates across Europe fell below historical norms after 2022 as new capacity arrived before the market had fully recovered from destocking. In France, the Alizay and Golbey start-ups intensified domestic competition in recycled grades and kept brown corrugated case material prices under pressure through 2025. Norske Skog confirmed that Golbey PM1 posted negative EBITDA during the ramp-up phase in 2025 because lower sales prices were only partly offset by lower OCC costs. This means the France containerboard market is unlikely to regain healthier pricing conditions until demand improves materially or more capacity exits the broader European system.

EPR, EUDR, And Traceability Cost Stack

France extended EPR obligations to industrial and commercial packaging from January 2026, adding a new compliance cost layer for converters and brand owners active in the French containerboard market. The French order requires eco-organizations to achieve paper and cardboard recycling rates of 75% by 2028 and 85% by 2030, while imposing penalties for poor recyclability performance and mandating R&D funding of up to EUR 5 million (USD 5.6 million) annually in 2026-2027. EUDR compliance adds additional documentation requirements for virgin-fiber supply chains, increasing the administrative burden on packaging businesses handling traceability-sensitive grades. Large integrated groups can spread those compliance costs across multiple mills and convert sites more easily than smaller regional operators can. The result is a tighter operating environment for the French containerboard market, especially for converters without internal compliance and sourcing infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Tested By Structural Overcapacity

Recycled fibers held 58.41% of the French containerboard market share in 2025, supported by France’s established recovered-paper system and the usual cost advantage that recycled feedstock provides under normal conditions. Recycled grades remain central to the French containerboard industry because testliners and corrugating media still form the core of supply for food, retail, and e-commerce corrugated applications. The rapid start-up of Alizay and Golbey increased the domestic supply of recycled containerboard and prolonged price pressure on brown grades during 2025. Blue Paper SAS also showed how mid-sized mills are adjusting by changing procurement and transport choices, after adopting river transport for recovered paper shipments in partnership with Voies Navigables de France in April 2026.

Virgin fibers are projected to grow at a 1.68% CAGR in the France containerboard market size outlook through 2031, even though they remained the smaller material segment in 2025. That growth is tied to stronger demand for premium kraftliner in e-commerce outer boxes and shelf-facing applications where strength, print quality, and lower basis weight matter more than lowest-cost input selection. Smurfit Westrock described its Facture site in France as one of the group’s largest and lowest-cost kraftliner mills globally, providing a useful platform for premium linerboard supply. EUDR-related traceability requirements can also make sourcing and documenting some non-EU virgin-fiber imports less straightforward. That could leave French and other EU producers with certified supply chains in a stronger position as buyers place more weight on traceability and compliance.

By Product Type: Kraftliner Growth Signals A Premium Packaging Shift

Testliners accounted for 41.12% of the French containerboard market in 2025, making them the leading product grade across food, consumer goods, and industrial corrugated uses. Their large installed base reflects their broad role as outer and inner liner layers in standard corrugated boxes across the French containerboard industry. White-top testliner has also gained relevance in retail-facing and food-related uses where appearance, print performance, and recyclability must be balanced in the same pack format. AGEC disclosure rules reinforce this position because buyers increasingly want liner grades with clear recycled-content credentials and easy communication on recyclability.

Kraftliners are projected to grow at a 1.79% CAGR through 2031, making them the fastest-expanding product type in the French containerboard market. The main reason is a gradual shift toward stronger, more print-ready outer liners for premium e-commerce packs, shelf-ready retail packaging, and chilled-food transit formats. Smurfit Westrock’s French kraftliner position at Facture gives the country a meaningful domestic base in this higher-value grade category. Klingele’s climate target validation in December 2025 also shows that carbon reporting and mill-level energy choices are becoming more important in premium board purchasing decisions. As that shift continues, product competition in the French containerboard market is likely to become more clearly differentiated between commodity recycled grades and premium liner offerings.

By End-User Industry: Food Anchors Demand, Consumer Goods Accelerates

Food and beverage accounted for 38.16% of the French containerboard market share in 2025, giving it the largest share among end-user industries. France’s EUR 176.7 billion (USD 188.5 billion) food and beverage manufacturing base supports steady corrugated demand across fresh produce, dairy, frozen foods, and distribution packaging. Norske Skog Golbey’s food-contact-certified output gives the mill direct access to this more specification-sensitive demand base as its ramp-up continues. Industrial end users such as automotive components, chemicals, and building materials remain less supportive in the near term because softer French manufacturing activity limits broader corrugated demand.

Consumer goods are projected to expand at a 1.74% CAGR through 2031, which makes it the fastest-growing end-user segment in the French containerboard market. FMCG brands are pushing harder to replace plastic secondary and transit packaging before tighter PPWR compliance timelines become more binding. Saica’s partnership with Unilever, announced in January 2026, replaced plastic shrink film on Axe deodorant twin-packs sold in France with a paper banding solution made at Saica’s French facilities. Pharmaceuticals, cosmetics, and electronics remain smaller contributors, but they also benefit from the broader move toward paper-based secondary packaging. This growth matters because it supports demand for higher-specification, print-ready grades rather than only the lower-value brown recycled products, which face the strongest price pressure.

Geography Analysis

France hosts one of Western Europe’s densest clusters of recycled containerboard capacity, centered on Normandy, the Vosges, Alsace, and the Rhone-Alpes corridor. VPK’s Alizay site in Normandy combines large recycled-paper capacity with biomass energy and river-linked logistics, giving the region a strong cost and circularity profile. In the Vosges, Norske Skog Golbey added 550,000 tonnes of annual capacity in May 2025 and processes more than 1 million tonnes of locally collected wastepaper each year. Alsace remains relevant through assets such as Klingele Strasbourg and Blue Paper SAS, which keep eastern France important to both production and regional trade flows. The Rhone-Alpes region also matters through Saica’s Champblain-Laveyron complex and its ongoing biomass-led energy transition.

France is a mid-sized market in Europe by value, but it is a first-rank location for newly installed recycled containerboard capacity, and that shapes the French containerboard market even when domestic box demand is soft. Across the CEPI region, packaging grades output rose 6.5% in 2024, while containerboard output rose 4.3%, indicating that regional supply recovery has outpaced the French demand picture. France’s own paper and paperboard packaging demand base remains constructive, but containerboard growth is slower because industrial activity and corrugated consumption have not recovered at the same pace as installed capacity. Smurfit Westrock reported that energy costs in its Europe, Middle East and Africa, and Asia-Pacific segment rose 45% in 2025, which shows that even well-positioned French assets still operate under significant cost pressure. Even so, France’s power mix gives mills a steadier structural base than some more gas-exposed European peers, which partly cushions the downside for the French containerboard market.

Normandy and the Vosges are now the clearest strategic centers of France’s recent production shift. VPK planned to supply 415,000 tonnes of low-CO2-intensity paper from Alizay into its European converting network by 2026, which ties French output more closely to cross-border internal demand. Norske Skog is also reviewing a Golbey biogas expansion that would raise annual output from 16 GWh to 70-90 GWh by 2028 and add EUR 8 million (USD 9.02 million) in annual revenue, further strengthening the site’s long-term position. The broader French packaging market, valued at USD 32.88 billion in 2026, provides the French containerboard market with supportive long-term demand fundamentals as paper-based packaging continues to take share from single-use plastics.

Competitive Landscape

The France containerboard market is moderately consolidated at the mill level, while the converter tier remains much more fragmented across regional and family-owned businesses. Smurfit WestRock, Saica Group, and VPK Group account for much of French mill output, and Norske Skog has emerged as a clearer fourth force since Golbey entered production. Smurfit Westrock said in its 2025 annual report that it operates 2 recycled containerboard mills and 1 kraftliner mill in France, while its broader segment produced 6.4 million tonnes of containerboard in 2025. Across the leading producers, the common strategy is to pair scale with biomass or biogas investment, converting integration, and sustainability credentials that smaller competitors struggle to match. That matters more now because regulation is pushing customers to ask for lighter packs, clearer traceability, and faster packaging redesign cycles.

One open opportunity is food-contact-certified recycled containerboard, where Golbey can now challenge the imported supply with certified local output. Another is white-top and high-print-quality linerboard for FMCG packs, where brand owners need better presentation without moving away from recyclable fiber formats. A third is lightweight corrugating solutions for e-commerce right-sizing, where packaging performance is closely tied to automation and pack optimization rather than solely to tonnage. VPK’s Alizay corrugator and digital printing setup support Z-fold fanfold production for on-demand, size-optimized packaging, reducing changeover friction and increasing pressure on conventional converting models. These moves show that competition in the French containerboard market is shifting toward service capability and pack design speed as much as toward paper production cost.

Saica has also used commercial partnerships and customer-facing investment to strengthen its position in France. It's January 2026. Unilever's agreement on paper banding showed how large suppliers are using regulation-driven plastic substitution to enter adjacent packaging uses. Saica also opened its first Customer Experience Center in France in November 2025 at Venizel, indicating a stronger emphasis on co-development and packaging design support. Klingele’s validated climate targets, including energy progress at Strasbourg, show that carbon accounting is becoming a more visible part of competitive positioning for the French containerboard market.

France Containerboard Industry Leaders

Saica Group

VPK Group

Smurfit Westrock plc

Norske Skog ASA

Palm Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Saica Group completed its acquisition of Thimm Group, a major manufacturer of corrugated packaging and displays operating across Europe, significantly expanding Saica's pan-European converting footprint and adding strategic capacity in corrugated display packaging adjacent to its French paper mill network.

- April 2026: Norske Skog reported record recycled containerboard deliveries of 106,000 tonnes in Q1 2026 from its packaging paper segment including Golbey PM1 in France, with segment operating revenue rising 89% year-over-year to NOK 398 million (USD 37.5 million); losses at Golbey PM1 narrowed significantly to EBITDA of NOK -43 million (USD -4.2 million) from NOK -124 million (USD -12.3 million) in Q4 2025, confirming the ramp-up trajectory toward full utilization by H1 2027.

- April 2026: Norske Skog disclosed a review of a biogas expansion project at the Golbey mill to increase annual green biogas output from 16 GWh to between 70 and 90 GWh, with commissioning targeted for 2028 and potential additional revenues of EUR 8 million (USD 9.02 million) annually, deepening the mill's decarbonized energy model.

- January 2026: VPK Group increased its equity stake in Ribble Packaging Limited, a UK-based fanfold corrugated cardboard company, from 30% to 50%, establishing joint control; VPK produces fanfold at its Alizay facility in France and at Zetacarton in Italy, aiming to build a vertically integrated pan-European fanfold network serving e-commerce and distribution centers.

France Containerboard Market Report Scope

The France Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The France Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the France containerboard market size outlook through 2031?

The France containerboard market was valued at USD 3.12 billion in 2025 and is forecast to reach USD 3.42 billion by 2031, growing at a 1.41% CAGR over 2026-2031, according to Mordor intelligence.

What is driving demand for containerboard in France?

The main supports are plastic-to-fiber substitution under AGEC and PPWR, e-commerce packaging demand, shelf-ready retail formats, and resilient food and beverage corrugated use.

Which material segment leads in France, and which one grows fastest?

Recycled fibers led with a 58.41% share in 2025, while virgin fibers are projected to grow fastest at a 1.68% CAGR through 2031.

Why are kraftliners growing faster than testliners in France?

Kraftliners are benefiting from demand for stronger, more print-ready outer liners in e-commerce, shelf-ready packaging, and food logistics, which supports a 1.79% CAGR through 2031.

Which end-user segment has the strongest base in France?

Food and beverage remains the largest end-user segment with a 38.16% share in 2025 because France has a large food manufacturing base and steady transit packaging demand.

How are new mills changing competition in the France containerboard market?

New capacity at Alizay and Golbey has improved domestic supply and low-carbon production capability, but it has also added pricing pressure in recycled grades while raising the competitive bar for smaller converters.

Page last updated on: