Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

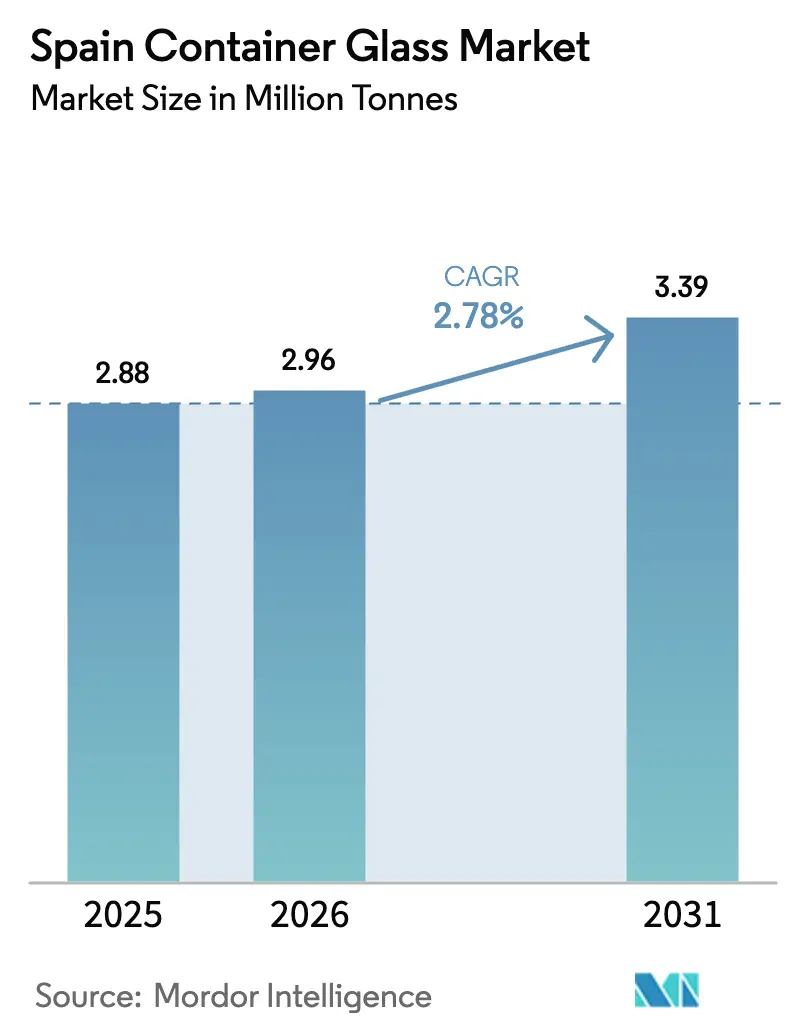

| Base Year Market Size (2025) | 2.88 Million tonnes |

| Market Volume (2026) | 2.96 Million tonnes |

| Market Volume (2031) | 3.39 Million tonnes |

| Growth Rate (2026 - 2031) | 2.78% CAGR |

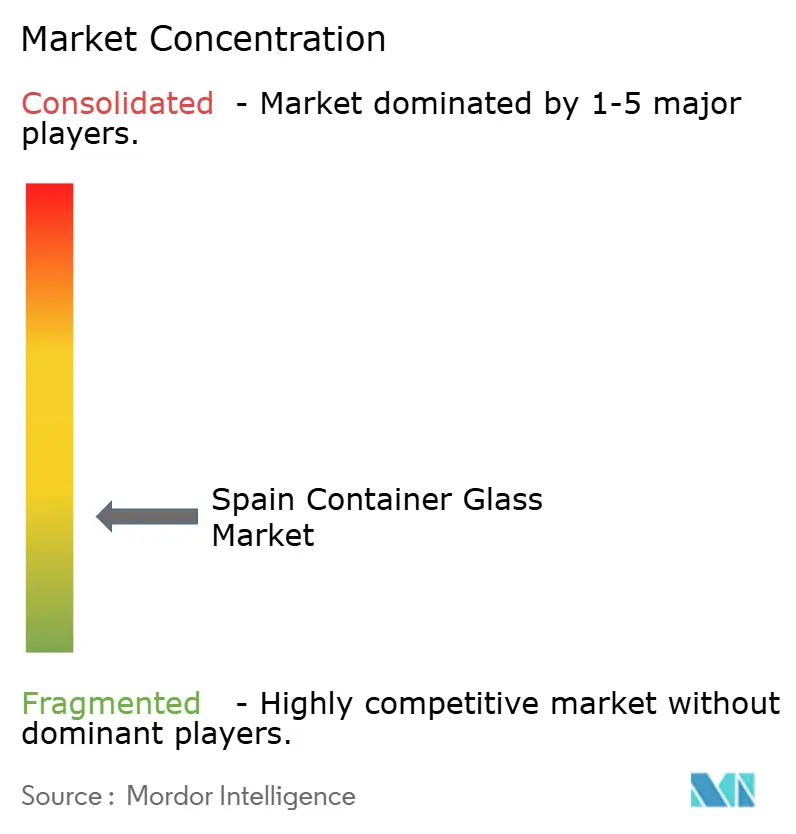

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Container Glass Market Analysis by Mordor Intelligence

The Spain Container Glass Market size was valued at 2.88 million tonnes in 2025 and estimated to grow from 2.96 million tonnes in 2026 to reach 3.39 million tonnes by 2031, at a CAGR of 2.78% during the forecast period (2026-2031). Consistent policy pressure for closed‐loop recycling, premiumization in wine, olive oil, and beauty packaging, and strong cullet availability underpin this measured trajectory for the Spain container glass market. Brand owners in beverages, cosmetics, and gourmet foods now specify lightweight eco-designed bottles, accelerating technology investments in oxygen-fueled furnaces and inline AI inspection. Sector resilience also stems from Spain’s stature as the world’s third-largest wine producer and the largest olive-oil supplier, both of which favor glass to convey authenticity and preserve product integrity. Nonetheless, energy price volatility and competition from plastics and metal packaging continue to pressure margins. Consolidation is intensifying as Vidrala, O-I Glass, and Verallia optimize capacity, while mid-tier specialists pursue design-led niches to defend share in the Spain container glass market.

Key Report Takeaways

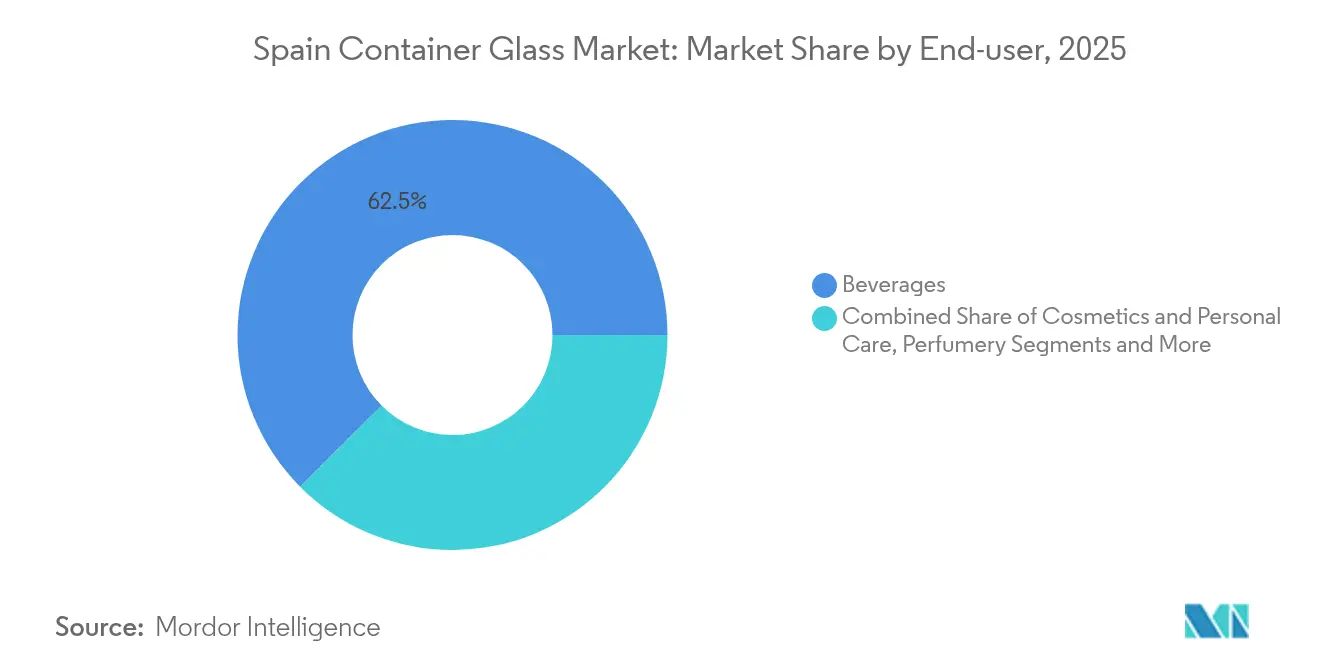

- By end-user, beverages captured 62.46% of the Spain container glass market share in 2025.

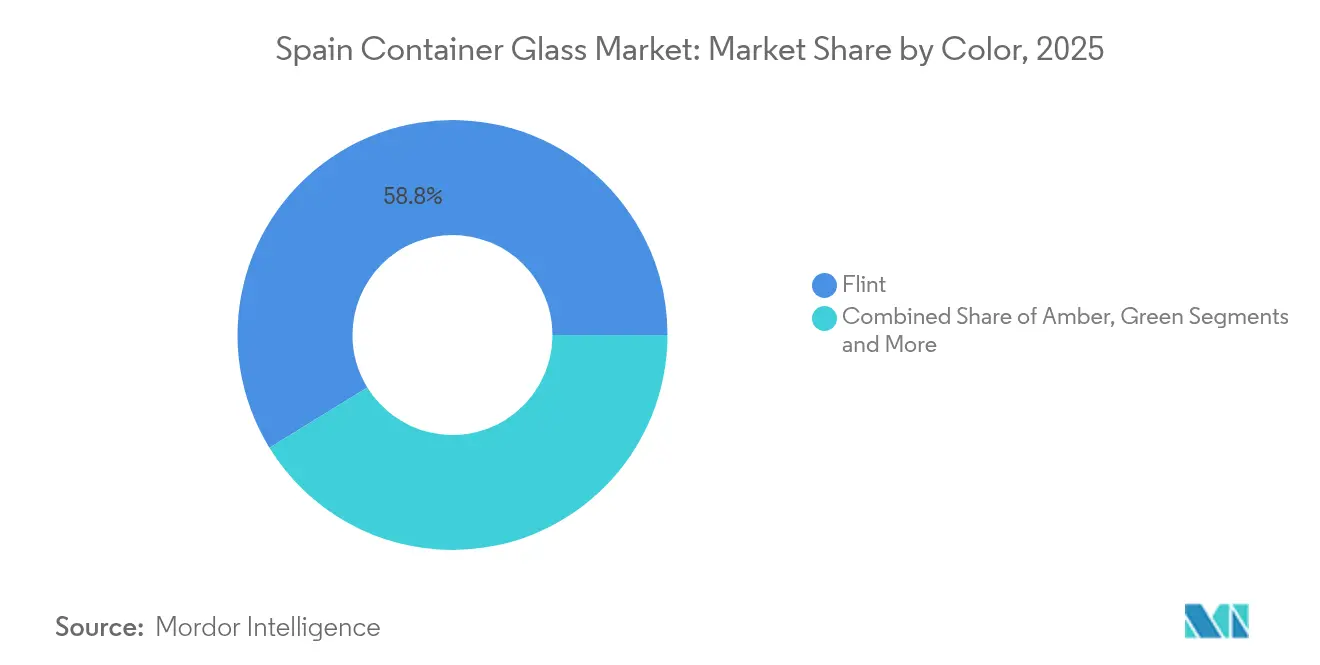

- By color, the Spain container glass market for amber glass is projected to grow at a 4.07% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for sustainable packaging solutions | +0.8% | National (Madrid, Barcelona, Valencia) | Medium term (2-4 years) |

| Growing preference for recyclable and eco-friendly glass | +0.6% | Urban centers nationwide | Long term (≥ 4 years) |

| Rising consumption of alcoholic beverages | +0.4% | Rioja, Ribera del Duero, Catalonia | Short term (≤ 2 years) |

| Premiumization trends in wine, olive oil and cosmetics | +0.4% | Nationwide with export pull | Medium term (2-4 years) |

| Government Incentives for Circular Economy and Recycling | +0.5% | National, with EU-wide regulatory influence | Long term (≥ 4 years) |

| Premiumization Trends in Wine, Olive Oil, and Cosmetics Packaging | +0.4% | National, with export market implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Sustainable Packaging Solutions

EU legislation mandating 90% collection and 85% recycling of glass by 2030 amplifies corporate sustainability targets, steering brand owners toward the Spain container glass market. Premium wine producers such as Torres have switched to 15-20% lighter bottles, reducing scope 3 emissions while retaining shelf appeal. Manufacturers able to deliver lighter yet structurally robust containers gain priority in supplier rosters. This alignment of regulatory pull, investor scrutiny, and consumer sentiment collectively lifts baseline demand despite higher unit costs than plastic, sustaining growth momentum for the Spain container glass market.

Growing Preference for Recyclable and Eco-Friendly Glass

Consumer surveys show willingness to pay price premiums for products in infinitely recyclable glass, particularly among health-conscious demographics in Spain’s larger cities. Glass retains flavor and aroma better than plastics that degrade after limited recycling loops, reinforcing quality perceptions. Ecovidrio’s network of 240,302 green bins underpins Spain’s 79.8% glass collection rate, ensuring an abundant cullet supply that lowers furnace energy by 2-3% per 10% cullet usage.[1]Ecovidrio, “Memoria de Sostenibilidad 2024,” ecovidrio.es As virtuous collection-recycling cycles strengthen, cost competitiveness improves, further anchoring glass as the preferred premium pack in the Spain container glass market.

Rising Consumption of Alcoholic Beverages in Spain

Domestic beer and craft cider volumes rebounded post-pandemic, while wine exports to the United States and Asia registered high-single-digit growth in 2024. Producers favor glass for shelf differentiation, oxidation resistance, and the premium cues essential in crowded international aisles. Region-specific denominations such as Rioja and Ribera del Duero rely on fast lead times from nearby plants, supporting local capacity utilization in the Spain container glass market.

Premiumization Trends in Wine, Olive Oil, and Cosmetics Packaging

Spain’s olive-oil sector targets production of 4 million tonnes by 2040, with top brands adopting customized flint or emerald bottles that lift retail pricing by 20-30%. Cosmetics leader Puig reported rising demand for sculpted heavy-glass flacons, inflating glass spend per unit. These shifts provide margin upside for manufacturers offering complex shapes, specialty colors, embossing, and acid-etched textures, reinforcing value capture in the Spain container glass market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs of glass containers | –0.5% | Nationwide | Short term (≤ 2 years) |

| Intense competition from plastic and metal packaging | –0.4% | Nationwide | Medium term (2-4 years) |

| Energy-Intensive Manufacturing Process | -0.3% | National, concentrated in major production hubs | Long term (≥ 4 years) |

| Supply Chain Disruptions and Raw Material Volatility | -0.2% | National, with import dependency for certain materials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs of Glass Containers

Energy accounts for 35-39% of glass production costs, and although Spanish industrial electricity averaged EUR 0.17/kWh (USD 0.19/kWh) in 2023 29% below the broader EU, furnaces operating at 1,600 °C remain exposed to price spikes. O-I Glass absorbed USD 175 million in incremental expenses in 2024, prompting its “Fit to Win” plan to shed at least 7% European capacity by mid-2025. Soda-ash and silica volatility compounds the pressure, forcing relentless efficiency drives across the Spain container glass market.

Intense Competition from Plastic and Metal Packaging

PET bottles cost 60-70% less per unit and weigh a fraction of glass, translating into reduced logistics emissions and expenses. Aluminum cans offer production speed and durability, winning share in carbonated beverages. Carton innovator Elopak is edging into juice and dairy aisles with fiber-based packs that combine sustainability cues with cost savings. While lightweighting narrows the freight gap, glass continues to cede volume in mass-market segments, moderating expansion prospects for the Spain container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Market Leadership

Beverages accounted for 62.46% of Spain's container glass market share in 2025, led by wine, beer, and spirits. The alcoholic-beverage subsegment benefits from premium cues, oxygen impermeability, and export authenticity requirements, ensuring stable demand. Craft brewers also prefer embossed amber bottles that protect against UV and reinforce artisanal positioning. Non-alcoholic drinks lean on glass for niche organic juices and kombucha, where provenance matters. Cosmetics and personal care are the fastest-growing applications at a 3.95% CAGR to 2031, buoyed by luxury skincare, perfumery, and wellness products packaged in heavy, custom-shaped jars.

The Spain container glass market size for cosmetics is projected to rise steadily as deluxe brands favor tactile heft and sustainable storytelling. Food applications such as olive oil, jam, and gourmet sauces sustain stable tonnage, underpinned by Spain’s agricultural export engine. Pharmaceuticals retain moderate demand for neutral borosilicate bottles outside vial niches, while perfumery leverages intricate glass sculpting to bolster brand equity. Segment diversity shields the Spain container glass market from cyclical shocks in any single end-use stream.

By Color: Flint Glass Maintains Dominance

Flint held 58.78% of the Spain container glass market size in 2025, thanks to its clarity, versatility, and ability to spotlight product color, crucial for olive oil and rosé wines. Winemakers prize flint for showcasing shade and sediment, enhancing shelf appeal. Gourmet food brands use clear jars to demonstrate purity, while cosmetics rely on transparency to display textures. Amber is the fastest-growing color at 4.07% CAGR through 2031, propelled by pharmaceutical and craft-beer demand that requires UV protection.

Beer bottlers favor amber to minimize light-struck flavor deterioration, and drug makers package light-sensitive formulations similarly. Green glass sustains relevance in red-wine bottles that convey heritage cues in export markets, whereas cobalt and specialty tints occupy niche premium roles, commanding higher margins within the Spain container glass market.

Geography Analysis

Catalonia anchors the Spain container glass market with multiple furnaces clustered around Barcelona’s port, granting export reach and feedstock access. Andalusia hosts plants tied to the olive-oil belt, ensuring swift supply to bottlers during harvest peaks. Valencia marries manufacturing capacity with agricultural demand for jam, citrus preserves, and specialty sauces.

Northern regions, the Basque Country and Castile & León, share proximity with celebrated wine appellations Rioja and Ribera del Duero, lowering freight costs and enabling just-in-time bottle dispatch. BA Glass Iberia’s León and Villafranca sites generated EUR 201.76 million (USD 228 million) sales in 2021 with 654 staff, underscoring regional employment and specialization.

Madrid’s central logistics hub channels finished containers nationwide to FMCG headquarters, sustaining balanced load factors. Proximity between plants and demand nodes trims transportation, which can weigh 10-15% of delivered cost, reinforcing domestic incumbents against imports.

Competitive Landscape

The Spain container glass market is moderately consolidated. Vidrala, O-I Glass, and Verallia jointly secured roughly 65% revenue in 2024, while BA Glass and regional niche players hold the remainder.[3]FindingMoats Research, “Vidrala Competitive Edge 2025,” findingmoats.substack.comO-I’s “Fit to Win” plan targets a 7% reduction in European furnace capacity by mid-2025, tightening supply but releasing USD 250 million in cost savings. Vidrala has pioneered 260-gram lightweight wine bottles, blending lower emissions with premium aesthetics and cushioning margins amid energy volatility.

Verallia focuses on recycled-content furnaces to match retailer decarbonization scorecards. Strategic themes span lightweighting, cullet integration, waste-heat recovery, and digital quality control. Larger groups leverage capital to modernize furnaces, whereas smaller firms hedge via custom molds and artisan short runs.

M&A activity centers on geographic diversification; BA Glass’s 60% stake in Mexico’s Vidrio Formas expanded its global footprint to surpass EUR 1.8 billion (USD 2.03 billion) revenue. With end-market defensiveness, incumbents will prioritize throughput, energy hedging, and high-margin premium accounts to protect profitability in the Spain container glass market.

Spain Container Glass Industry Leaders

Verallia Spain S.A.

O-I Manufacturing Spain, S.L.

Saverglass Iberica S.A.U.

Ardagh Group S.A.

Gerresheimer Zaragoza S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: O-I Glass posted 4.4% global shipment growth and confirmed USD 250 million “Fit to Win” savings target, incurring USD 80 million restructuring charges but unlocking USD 61 million Q1 benefits.

- April 2025: Saint-Gobain recorded EUR 11.7 billion (USD 13.2 billion) Q1 sales, up 3.2%, retaining >11% operating-margin ambition despite soft European volumes.

- January 2024: SGD Pharma unveiled a JV with Corning for Indian borosilicate tubing and a furnace retrofit to curb CO₂ by 20%.

- November 2023: BA Glass bought 60% of Vidrio Formas, targeting global revenue above EUR 1.8 billion (USD 2.03 billion).

Spain Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

The Spain container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current size of the Spain container glass market?

The market stands at 2.96 million tonnes in 2026 and is projected to reach 3.39 million tonnes by 2031.

Which end-user segment dominates demand?

Beverages hold 62.46% share, led by wine, beer and spirits that rely on premium glass for brand integrity.

Why is flint glass so prevalent?

Flint accounts for 58.78% share because its transparency showcases product color, vital for olive oil, wines and cosmetics.

How are manufacturers reducing costs amid high energy prices?

Firms deploy waste-heat recovery, oxy-fuel furnaces and lightweighting to trim energy use 10-15% and material inputs.

Which color segment grows fastest?

Amber glass is rising at a 4.07% CAGR on the back of UV-sensitive beer and pharmaceutical applications.

What drives premiumization in Spanish glass packaging?

Upmarket wine, olive oil and luxury beauty brands demand custom shapes and heavier bottles that command 20-30% price uplifts.

Page last updated on: