Malaysia Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.84 Billion |

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

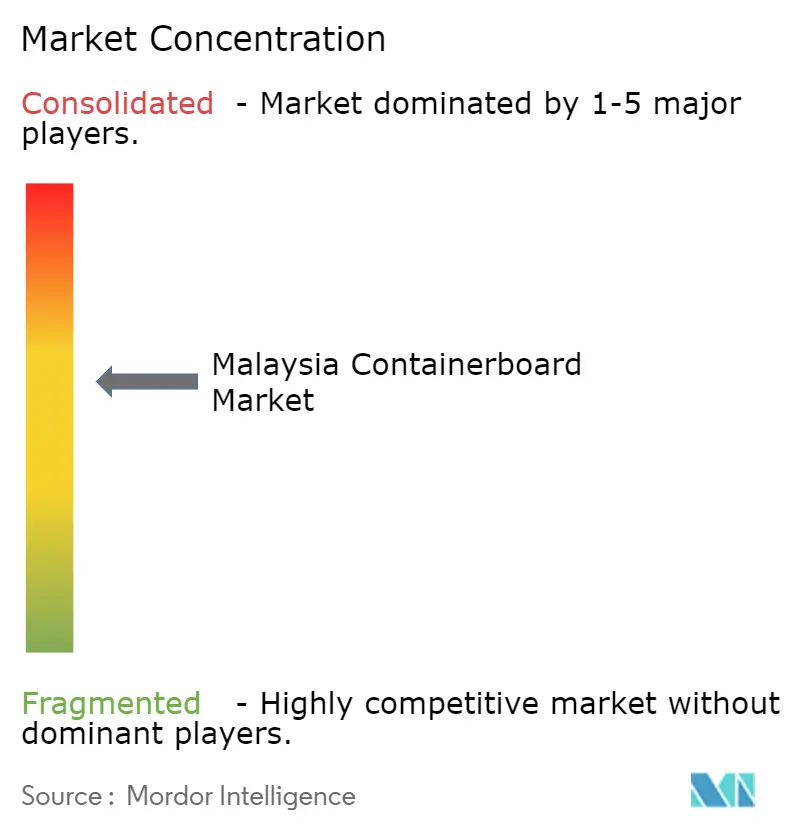

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Containerboard Market Analysis by Mordor Intelligence

The Malaysia containerboard market size is projected to expand from USD 2.84 billion in 2025 and USD 2.96 billion in 2026 to USD 3.81 billion by 2031, registering a CAGR of 5.18% between 2026 to 2031. Demand is moving on a firmer footing as Malaysia becomes more important in regional logistics, export manufacturing, and consumer goods distribution. The country also benefits from a packaging ecosystem that is tied more to local converting demand than to large export-driven mill cycles, which gives the Malaysia containerboard market a different risk profile from some neighboring producers. Industry expectations that Malaysia can emerge as a larger packaging manufacturing hub are also supported by stronger regional trade linkages and a solid ASEAN growth outlook over 2025 and 2026. The most durable opportunity sits in higher-performance corrugated formats for electronics, food distribution, and branded retail packaging, where quality and reliability matter more than price alone. Competition is therefore shifting toward lightweight board development, improved print performance, tighter quality control, and more resilient raw-material sourcing.

Key Report Takeaways

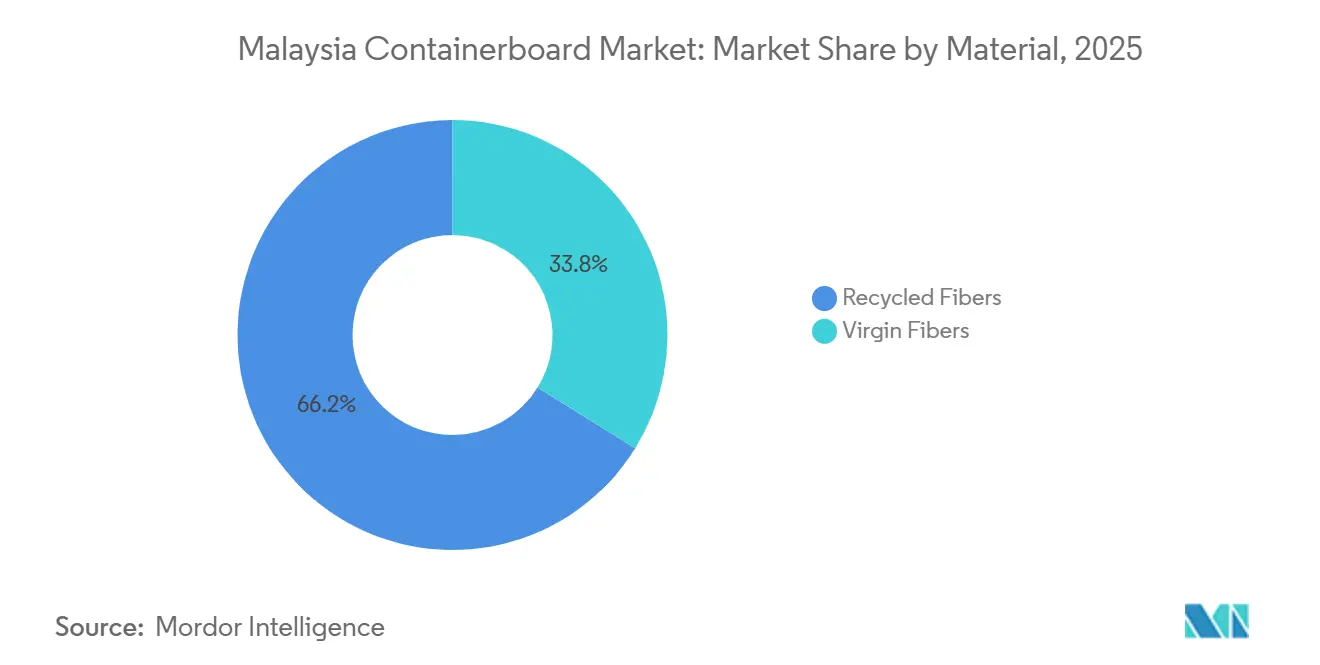

- By material, recycled fibers captured 66.18% of the Malaysia containerboard market share in 2025.

- By product type, the Malaysia containerboard market size for the kraftliners segment is forecast to advance at a 5.78% CAGR through 2031.

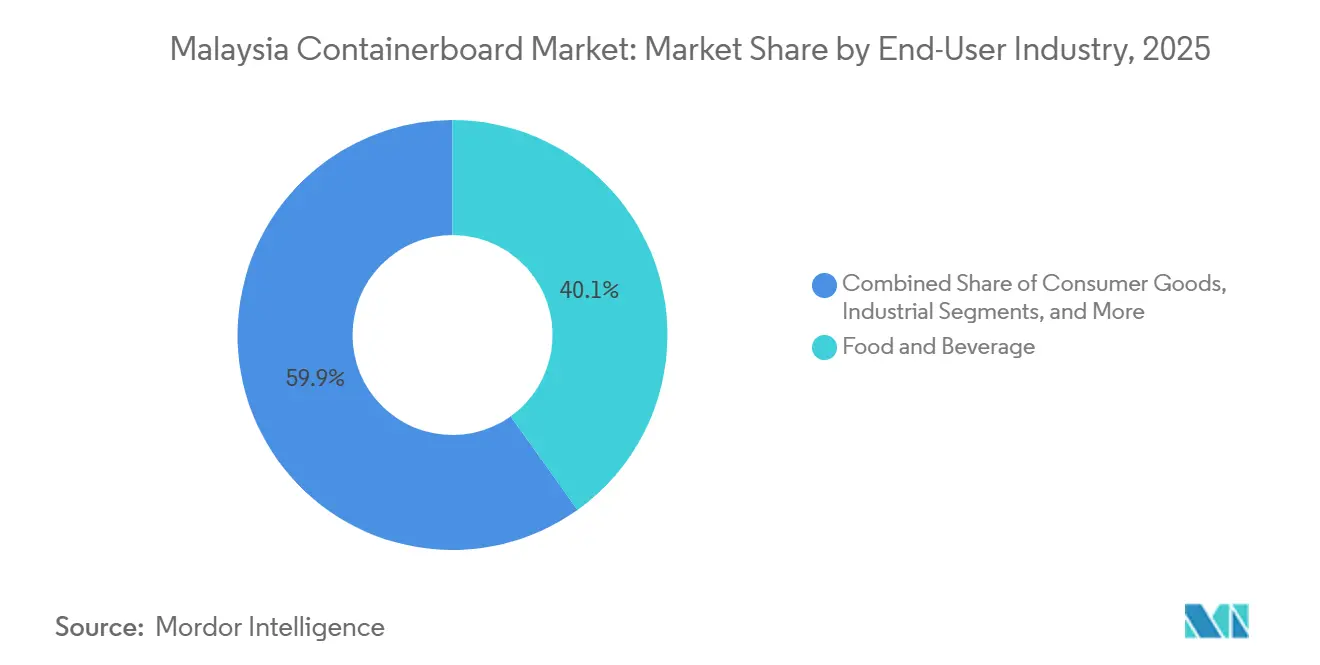

- By end-user industry, food and beverage captured 40.12% of the Malaysia containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Parcel Volumes | +1.4% | National, with concentration in Selangor, Kuala Lumpur, and Johor logistics corridors | Short term (≤ 2 years) |

| Food And Beverage Packaging Premiumization | +1.1% | National, with early gains in Selangor and Johor food-processing clusters | Medium term (2-4 years) |

| Electronics And E&E Export Strength | +0.9% | Penang, Selangor, and Kedah, spill-over to Negeri Sembilan | Medium term (2-4 years) |

| Shift Away From Single-Use Plastics | +0.7% | National, accelerated enforcement in Selangor, Penang, and Negeri Sembilan | Medium term (2-4 years) |

| China-Plus-One Manufacturing Spillover Into Malaysia | +0.5% | Selangor, Johor, and Penang industrial parks | Long term (≥ 4 years) |

| Lightweight Recycled Board Upgrades At Domestic Mills | +0.3% | National, with technology leadership concentrated in Selangor mills | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Parcel Volumes

Parcel demand continues to lift the Malaysian containerboard market, as online retail creates a steady flow of secondary and transit packaging across urban and suburban delivery networks. Ninja Van Malaysia projected 5% to 10% growth in domestic parcel volumes in 2026 versus 2025, after already reaching more than 20 million parcel recipients nationwide. Malaysia’s courier market was valued at MYR 6.8-6.9 billion (USD 1.6-1.7 billion) in 2025, underscoring the growing role of delivery services in the local packaging flow.[1]Bernama, “Courier Market Projected To Reach RM6.9 Bln This Year - Fahmi,” Bernama, bernama.com This is changing box specifications as well, because many marketplace sellers now want single-wall corrugated boxes with cleaner print surfaces that improve shelf appeal and the delivery experience. E-commerce demand also supports shorter production runs and more frequent design changes, giving mills and converters an edge by pairing consistent board quality with fast turnaround.

Food And Beverage Packaging Premiumization

Food and beverage remains a core volume base for the Malaysia containerboard market, but the mix is moving toward higher-value box formats rather than simple brown transit packaging. Malaysia was described as a stable market that targets 2% to 3% annual value growth within the broader regional food and beverage opportunity. Retail-ready corrugated formats with pre-printed surfaces and controlled-tear features command clear pricing premiums over standard regular slotted containers, which means board consumption per unit can rise even when shipment volume grows at a slower pace. The demand pattern is also supported by chilled products, premium snacks, and branded grocery distribution, all of which require better presentation and more consistent performance in humid conditions. Cold-chain activity adds another layer, because moisture resistance and surface quality matter more when food packaging must move through longer logistics chains.

Electronics And E&E Export Strength

The Malaysia containerboard market is also being supported by the country’s strong electronics and electrical export base, especially in packaging that protects higher-value shipments. Malaysia ranked among the world’s major E&E exporters, and E&E products accounted for 48% of export value in January 2026. AT&S started high-volume manufacturing of IC substrates at its Kulim campus in May 2025, tied to an investment of MYR 5 billion (USD 1.12 billion), which is expected to strengthen demand for specialized transport packaging for semiconductor and advanced component flows.[2]AT&S, “AT&S Starts High Volume Manufacturing at New Plant in Kulim/Malaysia,” AT&S, ats.net AT&S Electronics packaging needs a tighter board caliper, better burst strength, and more reliable surface uniformity than many standard consumer applications, so higher-grade linerboard gains a structural advantage in this channel. This matters for the Malaysia containerboard market because suppliers that meet these performance needs can protect margins more effectively than those competing only in commodity board grades.

Shift Away From Single-Use Plastics

Policy pressure against plastic waste is gradually becoming an important support for the Malaysian containerboard market, especially in courier, retail, and fast-moving consumer goods packaging. Malaysia’s Natural Resources and Environmental Sustainability Ministry agreed in April 2025 to ban single-use plastic bags at national parks, forest reserves, marine parks, and fixed retail premises nationwide. The Ministry of Housing and Local Government was also finalizing an Extended Producer Responsibility framework that entered a voluntary phase in 2026 and is set to become mandatory by 2030 for six packaging materials, including paper and plastic. A peer-reviewed study on Malaysia’s courier sector found that more than 80% of the packaging materials used by domestic logistics companies were non-recyclable in 2025, indicating clear room for fiber-based substitution.[3]Corporate Author, “Circular Economy and Sustainable Packaging in the Malaysian Courier Service Industry, Transforming Supply Chains for a Greener Future,” International Journal of Sustainable Development and Planning, iieta.org The shift will not be immediate, but it improves the long-term cost case for corrugated paper formats as recyclability becomes more visible in procurement and compliance decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Old Corrugated Container Price And Supply Volatility | -1.2% | Global, with elevated sensitivity in Malaysia due to high OCC import dependence from the US and Japan | Short term (≤ 2 years) |

| Competition From Low-Cost Plastic Packaging Formats | -0.9% | National, with concentration in FMCG, quick-service restaurant, and e-commerce mailer segments | Medium term (2-4 years) |

| Chinese Capacity Influx And Regional Oversupply Pressure | -0.7% | ASEAN-wide, with concentrated price pressure on Malaysian testliner and fluting grades | Medium term (2-4 years) |

| Mill Automation And Technical Talent Gaps | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Old Corrugated Container Price And Supply Volatility

Old corrugated container volatility remains the clearest short-term pressure point for the Malaysian containerboard market, as recycled-grade mills are exposed to swings in imported fiber costs. Industry coverage in 2025 described volatility in OCC and mixed paper markets as a persistent condition rather than a temporary disruption, with supply and demand often falling out of step for several months.[4]Corporate Author, “PPRC 2025, Examining the Volatility of OCC, Mixed Paper Markets,” Recycling Today, recyclingtoday.com This creates planning difficulties for mills that buy heavily in the spot market and then struggle to quickly pass higher costs through to box customers. The issue becomes more serious when energy costs also rise, because recycled-board economics then come under pressure from both fiber and utilities simultaneously. In practice, mills with stronger domestic collection ties or longer procurement contracts have a more durable margin position than mills that depend mainly on imported OCC cargoes.

Competition From Low-Cost Plastic Packaging Formats

Low-cost plastic formats still limit substitution in parts of the Malaysian containerboard market, even as regulation and sustainability goals become more visible. The same peer-reviewed study on Malaysia’s courier sector found that 65% of courier firms cited the high initial cost of sustainable materials as a barrier, which helps explain why procurement teams do not shift away from plastics as quickly as policy goals suggest. Plastic mailers and insulated formats still hold an advantage for lightweight delivery, certain foodservice uses, and cold-chain applications, where moisture performance and unit cost remain critical. This matters because buyers often compare total delivered cost, not just recyclability, when they choose between corrugated formats and flexible plastics. For the Malaysia containerboard market, that means innovation in lightweighting, coatings, and higher recycled-content performance is more important than simple price competition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Scale Meets Virgin Fiber Specification Demand

Recycled fibers held 66.18% of the Malaysian containerboard market share in 2025, confirming that the local system still relies on long-established OCC collection, recycled-medium production, and testliner capacity. The Malaysian containerboard industry has spent years building mill economics around recycled inputs, keeping recycled grades central to volume demand even as product requirements become more complex. Malaysia’s recovered paper trade also reflected improving quality premiums for sorted domestic grades relative to mixed household collections in recent periods. This part of the Malaysia containerboard market benefits from cost efficiency, shared fiber lines, and established downstream acceptance across standard box applications. It also fits the country’s role as a converting and consuming base, where broad domestic box demand supports a steady pull for recycled liners and mediums.

Virgin fibers are the fastest-growing material segment, with a forecast CAGR of 5.63% from 2026 to 2031, driven by increased demand from electronics exports, cold-chain food packaging, and retail-ready formats that require stronger, cleaner board surfaces. GS Paperboard and Packaging’s PM3 in Selangor, built with a MYR 1.2 billion (USD 0.29 billion) investment, produces lightweight testliner grades from 100% recycled material at up to 450,000 tonnes annually, demonstrating that domestic producers are still raising the performance ceiling of recycled board. At the same time, Nextgreen IOI Pulp and Xiamen C&D Paper and Pulp Group announced Malaysia’s first 150,000-tonne integrated pulp facility in Pahang in April 2025, with Phase 1 capital expenditure of MYR 900 million (USD 202 million) using palm biomass feedstock. If that project scales well, it could ease import dependence in the Malaysia containerboard market and improve the local cost base for kraftliner production over time.

By Product Type: Testliner Anchors Volume While Kraftliner Gains Premium Demand

Testliners accounted for 43.59% of the Malaysian containerboard market in 2025, underscoring how firmly this grade remains tied to standard corrugated box output across logistics, fast-moving consumer goods, and e-commerce applications. Testliner remains the default volume grade because recycled OCC-based production usually delivers a lower cost position than virgin-fiber linerboard in everyday shipping applications. Lee and Man Paper’s Malaysian base added a sixth PrimePress X shoe press in May 2025 at the Banting mill, integrated into PM26 to support high-speed production of testliner at 70-160 g/m² with better energy use and runnability. That investment matters because lightweight yet strong testliner is becoming increasingly attractive as box buyers seek to reduce material use without sacrificing stacking strength or print performance. For the Malaysian containerboard market, this keeps testliner at the center of volume demand even as end-use needs become more differentiated.

Kraftliners are forecast to grow at a 5.78% CAGR from 2026 to 2031, making them the fastest-rising product type in the Malaysian containerboard market. The shift reflects a stronger pull from electronics exports, premium retail-ready formats, and packaging systems that require better moisture resistance and cleaner outer surfaces than recycled grades can consistently deliver. Fluting remains essential because it aligns closely with corrugated box output and is co-produced alongside other grades at most domestic mills, so its role is stable even if it draws less attention than liners. The Malaysian containerboard industry is also seeing a product-mix shift toward micro-flute grades for shelf-ready and display uses, where digital print compatibility and board appearance carry more value than in standard transport packaging. The result is a market where testliner anchors scale, while kraftliner captures a larger share of premium growth and specification-led demand.

By End-User Industry: Food And Beverage Leads Scale While Consumer Goods Adds Faster Growth

Food and beverage accounted for 40.12% of the Malaysian containerboard market in 2025, making it the largest end-user segment for corrugated packaging demand. This segment remains resilient because it spans fresh produce, processed foods, beverages, and ready-to-eat formats, each with distinct but recurring needs for moisture control, stacking strength, and reliable delivery performance. In the Malaysian containerboard market, food packaging also tends to support better value realization than basic industrial brown-box demand because print quality, hygiene, and handling conditions matter more. Malaysia’s position within the wider Asia Pacific food and beverage market supports domestic processor demand for export packaging for ASEAN and Gulf markets. The spread of cold-chain distribution adds another layer of demand, as packaging must withstand longer, more complex product journeys.

Consumer goods are forecast to grow at a 5.85% CAGR from 2026 to 2031, which makes it the fastest-growing end-user segment in the Malaysian containerboard market. Growth is being supported by household care, personal care, and subscription-box retail formats that increasingly use paper-based outer packaging to enhance brand presentation and meet sustainability targets. Industrial and other end users still matter, particularly in export-linked supply chains such as automotive parts, furniture, and electronics, where packaging decisions follow original equipment manufacturer logistics standards more than local retail preferences. Net foreign direct investment into Malaysia reached 2.3% of GDP in 2025, the highest share in a decade, which supports factory additions and warehouse activity that feed back into packaging demand. For the Malaysian containerboard market, the strongest long-term position lies with suppliers that can serve food and beverage, consumer goods, and industrial accounts with different board grades, service models, and quality levels, rather than chasing volume in a single channel.

Geography Analysis

Demand in the Malaysian containerboard market is centered on Peninsular Malaysia’s west coast industrial corridor, with Selangor standing out as the main production and consumption base. Selangor hosts GS Paperboard and Packaging and the Lee and Man Paper base at Banting, and it also has a dense concentration of corrugated box plants serving fast-moving consumer goods, logistics, and manufacturing customers. This concentration matters because production, converting, warehousing, and delivery infrastructure sit close together, which lowers response times and improves service consistency for domestic buyers. Net foreign direct investment rose to 2.3% of GDP in 2025, compared with an average of 0.9% from 2020 to 2024, and Singapore’s investments grew to represent 27% of Malaysia’s FDI stock. That broader industrial buildout supports the Malaysian containerboard market by driving additional demand for industrial packaging, warehouse supplies, and transport packaging around new facilities.

Penang forms a distinct demand cluster within the Malaysian containerboard market because its packaging needs are more closely tied to electronics and semiconductor activity than to mass consumer distribution. Malaysia’s E&E exports climbed sharply in early 2026, with January 2026 shipments rising 39% year over year, reinforcing the weight of northern manufacturing in the national packaging mix. Facilities around Penang and nearby Kulim require higher-specification board, precision die-cut formats, and dependable moisture control, which favors kraftliner and better-performing corrugated solutions. Johor is another large consumption zone because its food-processing, pharmaceutical, and manufacturing base benefits from close logistics links with Singapore.

East Malaysia remains a smaller part of the Malaysian containerboard market, but Sabah and Sarawak are expanding as modern retail, commodity exports, and industrial development programs gather pace. These states still rely heavily on converted products supplied from Peninsular Malaysia or nearby Indonesian sources, which reflects both freight realities and limited local mill infrastructure. The Sarawak Corridor of Renewable Energy has been a visible part of the region’s industrial push, and improving transport links should support faster, proportional growth in packaging demand from a smaller base over time. Even so, the national demand mix remains relatively balanced because the Malaysian containerboard market draws on electronics, food and beverage, consumer goods, and logistics rather than on a single dominant end use. That balanced structure helps reduce the risk that a slowdown in any single sector will fully define national containerboard demand.

Competitive Landscape

The Malaysia containerboard market is moderately concentrated at the mill level and highly fragmented at the converting level. A limited group of integrated producers, including GS Paperboard and Packaging, Lee and Man Paper’s Malaysian base, and ND Paper Malaysia entities, accounts for most domestic board capacity, while more than 400 converting plants compete across Peninsular Malaysia. This structure gives the Malaysia containerboard market a split competitive pattern, because upstream scale matters strongly in board production, while downstream relationships and service quality matter more in box conversion. The leading mills are therefore competing on technology upgrades, cost control, certification, and regional reach rather than on price alone. That balance helps explain why large producers still invest heavily in automation and product improvement even though the downstream customer base remains fragmented.

GS Paperboard and Packaging illustrates the technology-led path in the Malaysia containerboard market through its digital transformation program with FPT Software, announced in May 2026, which moved operations from SAP ECC to SAP S/4HANA Private Cloud and added AI-driven automation tools. Lee and Man’s Banting upgrade with the PrimePress X shoe press shows a second pattern, which is scale and efficiency improvement aimed at stronger lightweight testliner production with lower energy use. Can-One Berhad’s 2024 lightweighting project at its Batu Caves carton plant, which improved yield by 3.3% and saved 20 metric tonnes of paper per cycle, shows how process discipline can create both cost gains and a stronger customer proposition. These examples show that the Malaysia containerboard market is rewarding operating quality and conversion efficiency as much as raw capacity.

A third competitive pattern is the attempt to serve more complex customer requirements across Southeast Asia from Malaysian facilities. Box-Pak continued to serve fast-moving consumer goods, food and beverage, electronics, and industrial customers from plants in Selangor and Johor, supported by high-speed corrugating lines at Batu Caves and broader regional capacity of 175,000 metric tonnes across Malaysia, Vietnam, and Myanmar. Industries also strengthened its position in food-related packaging by attaining FSSC 22000 certification in December 2025, which improved its ability to serve multinational food and beverage customers. The open space in the Malaysia containerboard market remains the area between certified recycled-content board and premium high-graphics retail-ready packaging, where local capabilities still do not fully cover every buyer need. At the same time, potential expansion by larger Chinese-linked producers remains the main pricing risk in standard grades, because added offshore capacity could tighten margins in testliner and fluting even if local demand stays firm.

Malaysia Containerboard Industry Leaders

GS Paperboard & Packaging Sdn Bhd

Muda Paper Mills Sdn. Bhd.

ND Paper (Malaysia) Sdn. Bhd.

Lee & Man Paper Manufacturing Ltd.

Rengo Packaging Malaysia Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: FPT Software announced a partnership with GSPP Holding Sdn. Bhd. (GS Paperboard and Packaging, Oji Group) to implement full-scale digital transformation across Oji's Malaysian paper and packaging plants. The project migrates operations from SAP ECC to SAP S/4HANA Private Cloud, integrates AI Agentic Automation via FPT's Akabot platform, and replaces existing RPA and e-invoicing systems, targeting enhanced revenue through AI adoption and optimized manpower across Malaysian operations.

- January 2026: Muda Paper Mills commissioned a second, higher-capacity biomass-fired boiler at a second facility, following its first biomass installation, developed with Wasco Greenergy, that cut Scope 1 emissions by over 20% in the first year. This positioned Muda Paper among the first Malaysian containerboard producers to systematically replace fossil-fuel steam generation across multiple production sites, reducing exposure to natural gas price volatility.

- December 2025: KYM Industries (M) Sdn Bhd attained FSSC 22000 food safety system certification, making it one of the early corrugated carton box manufacturers in Malaysia to hold this standard, thereby qualifying for supply agreements with multinational food and beverage brand owners.

- May 2025: ANDRITZ successfully started up its ninth PrimePress X shoe press globally and sixth in Malaysia for Lee and Man Paper Manufacturing at the Banting mill, Best Eternity Recycle Technology Sdn. Bhd. The shoe press, operating at 1,250 N/mm and integrated into the PM26 machine running at up to 1,000 m/min, produces high-quality testliner at 70-160 g/m², delivering significant energy savings and improved paper strength, enabling high-speed lightweight-grade production that supports Malaysia's shift to lower-basis-weight board.

Malaysia Containerboard Market Report Scope

The Malaysia Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Malaysia Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and outlook for containerboard demand in Malaysia?

The Malaysia containerboard market was valued at USD 2.84 billion in 2025, reaches USD 2.96 billion in 2026, and is forecast to reach USD 3.81 billion by 2031 at a 5.18% CAGR.

Which material type leads demand in this space?

Recycled fibers led with a 66.18% share in 2025 because local mills have long operated around OCC-based production and established recycled-board converting demand.

Which product type is growing fastest?

Kraftliners are forecast to grow at a 5.78% CAGR through 2031, supported by electronics exports, premium retail-ready formats, and stricter packaging performance needs.

Which end-user group matters most for box demand?

Food and beverage remained the largest end-user segment with 40.12% share in 2025, while consumer goods is the faster-growing segment with a 5.85% CAGR through 2031.

Why are electronics exports important for board producers?

Electronics and semiconductor shipments require stronger, cleaner, and more consistent corrugated packaging, which supports higher-grade linerboard demand and better pricing discipline.

What is the main operating risk for local mills?

OCC price and supply volatility remains the clearest risk because recycled-grade mills are sensitive to imported fiber swings and cannot always pass cost increases through quickly.

Page last updated on: