Morocco Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

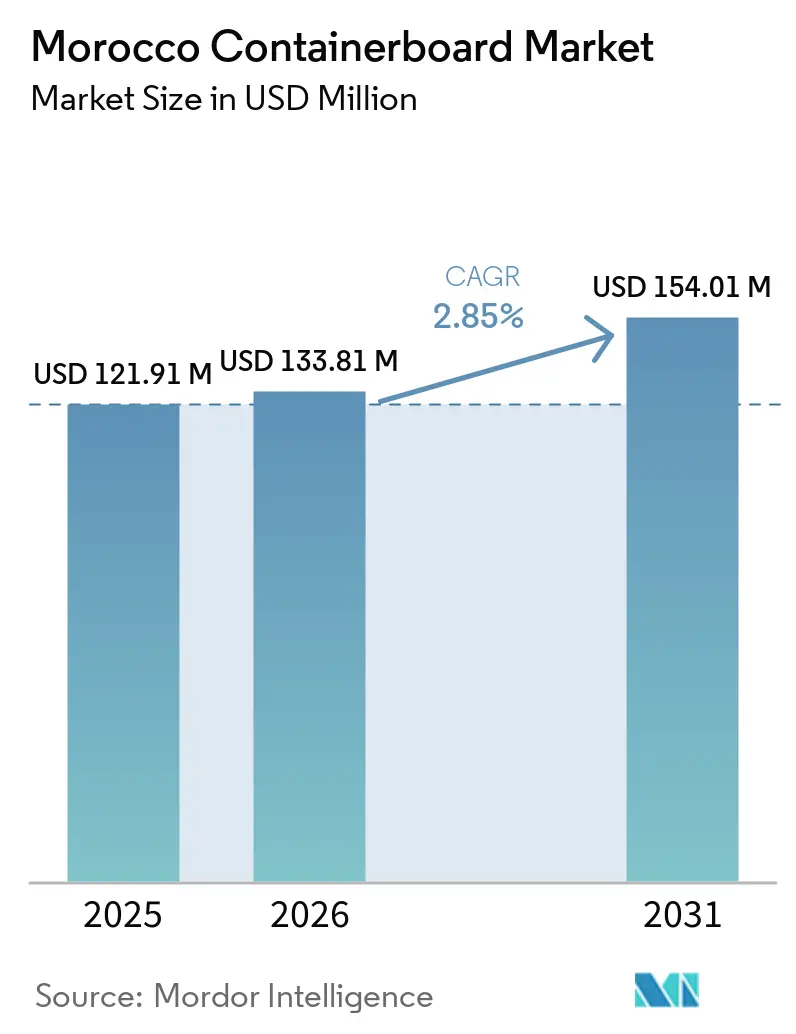

| Base Year Market Size (2025) | USD 121.91 Million |

| Market Size (2026) | USD 133.81 Million |

| Market Size (2031) | USD 154.01 Million |

| Growth Rate (2026 - 2031) | 2.85% CAGR |

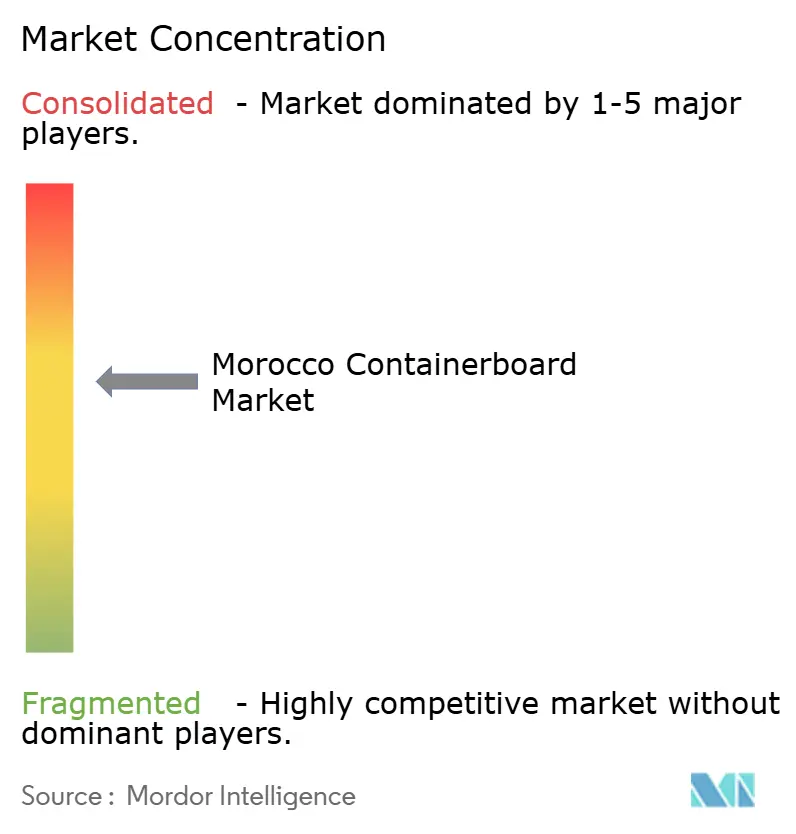

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Containerboard Market Analysis by Mordor Intelligence

The Morocco containerboard market size is projected to expand from USD 121.91 million in 2025 and USD 133.81 million in 2026 to USD 154.01 million by 2031, registering a CAGR of 2.85% between 2026 to 2031. The Morocco containerboard market is supported by a broader export base in fresh produce, stronger industrial packaging demand around Tanger Med, and a steady shift away from single-use plastic formats in retail and transit packaging. Morocco also stands apart in North Africa because it has a deeper corrugated conversion base than most neighboring countries, giving local suppliers a stronger position in both domestic delivery and regional exports. Demand is also shifting toward more complex box specifications, especially in food, automotive, and formal retail channels, where humidity resistance, traceability, print quality, and food-safety compliance matter more than they did in standard brown-box applications. That change is improving value per ton even when overall volume growth remains measured, which is important for mills and converters trying to protect margins. At the same time, the Morocco containerboard market still faces pressure from uneven recovered-fiber supply, water stress in key operating zones, and rising compliance expectations that are widening the gap between integrated players and smaller converters.

Key Report Takeaways

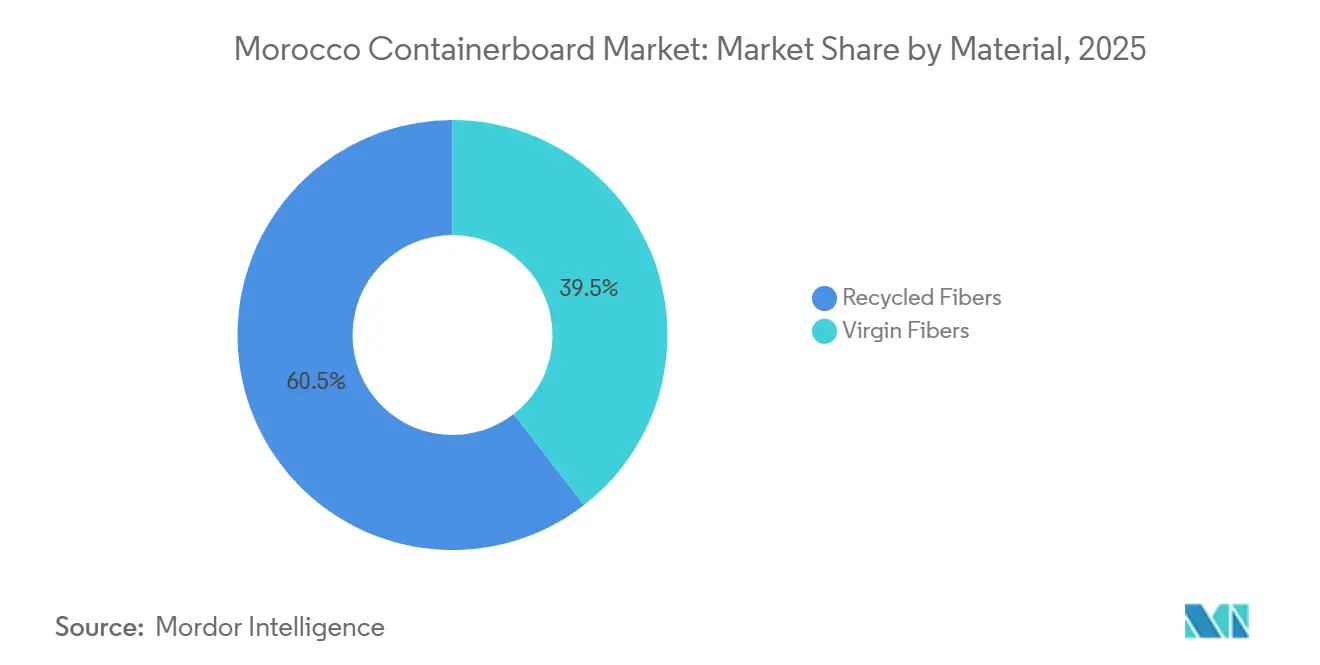

- By material, recycled fibers captured 60.48% of the Morocco containerboard market share in 2025.

- By product type, the Morocco containerboard market size for the kraftliners segment is forecast to advance at a 3.24% CAGR through 2031.

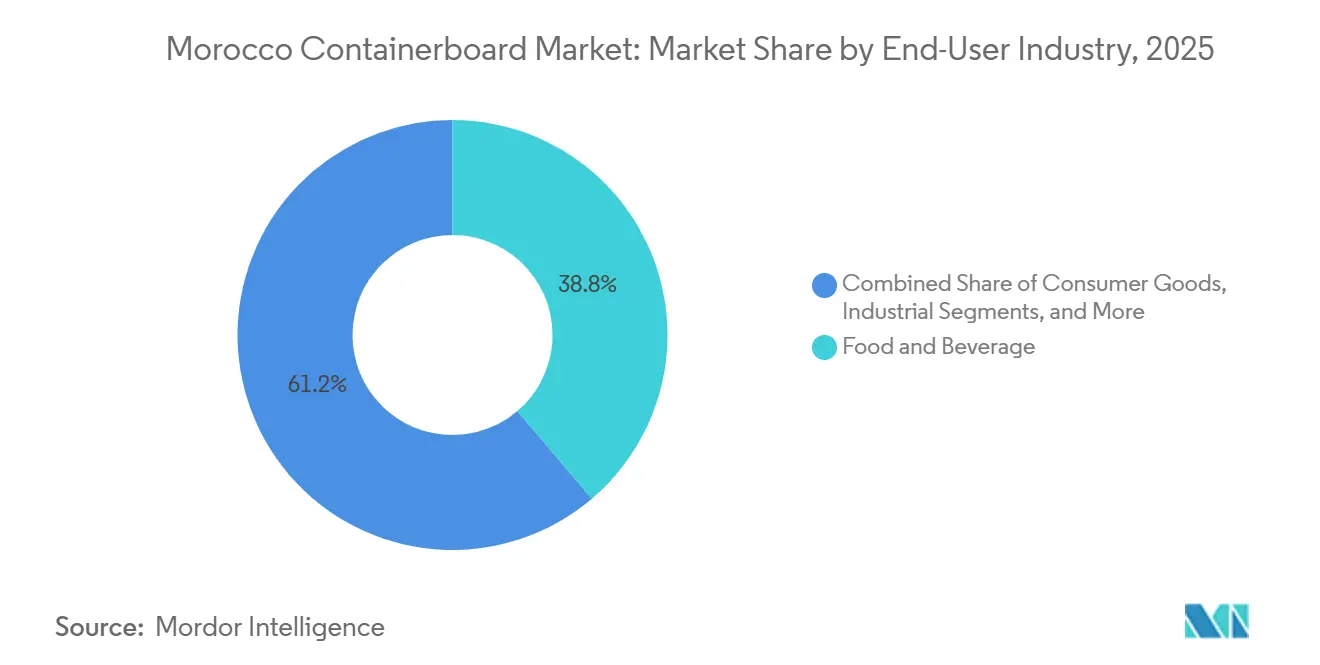

- By end-user industry, food and beverage captured 38.77% of the Morocco containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Morocco Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-Led Fresh Produce and Processed Food Packaging Demand | +1.2% | Souss-Massa, Gharb, Loukkos, and Tadla-Azilal agricultural corridors, spill-over to Agadir and Kenitra logistics hubs | Short term (≤ 2 years) |

| Shift Toward Recycled and Plastic-Substitute Transit Packaging | +0.6% | National, with early intensity in Casablanca, Tanger, and Agadir retail and logistics zones | Medium term (2-4 years) |

| Automotive and Industrial Nearshoring Around Tanger Med | +0.5% | Northern Morocco, Tanger Med Industrial Platform, spill-over to Kenitra | Medium term (2-4 years) |

| Capacity Additions in Recycled Containerboard and Corrugated Conversion | +0.3% | Mohammedia, Kenitra, Tanger, Agadir, and Meknes converting clusters | Medium term (2-4 years) |

| E-commerce Formalization and Parcel-Ready Box Demand | +0.2% | Casablanca-Rabat urban corridor, spill-over to Fes, Marrakech, and secondary cities | Long term (≥ 4 years) |

| Export-Grade Graphics, Traceability, and Food-Safety Compliance Needs | +0.1% | National, early adoption in Souss-Massa and Tanger Med supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-Led Fresh Produce And Processed Food Packaging Demand

Fresh produce exports remained one of the clearest demand anchors for the Morocco containerboard market, as each export cycle requires a new corrugated tray or box and does not rely on reusable packaging loops as much as some industrial formats. The move toward premium tomato varieties and other higher-value produce also raised the need for better humidity resistance, stronger burst performance, and more reliable food-contact compliance in corrugated packaging. That shift mattered because growers and packinghouses were no longer buying only low-cost transport cartons; they were increasingly buying packaging that could withstand longer transit and stricter buyer inspections. CMCP-International Paper invested more than MAD 100 million (USD 10.1 million) to expand its Ait Melloul facility near Agadir to support customer demand for sustainable corrugated packaging in Morocco, which shows how closely agricultural packaging capacity follows export activity in the south.[1]International Paper, “Morocco,” International Paper, internationalpaper.com As this demand base continues to grow, the Morocco containerboard market is likely to benefit more from higher-spec produce boxes than from simple volume gains alone.

Shift Toward Recycled And Plastic-Substitute Transit Packaging

The gradual replacement of single-use plastic formats has created a durable opening for paper-based transit and secondary packaging across the Moroccan containerboard market. Morocco’s circularity agenda has moved beyond waste collection and now includes reducing plastic pollution and strengthening packaging accountability, which supports containerboard demand across retail, logistics, and export supply chains. This shift also aligns with the needs of exporters selling into Europe, where packaging documentation and end-of-life considerations are increasingly difficult to ignore in buyer specifications. Financing channels are starting to move in the same direction, with modernization support for Moroccan paper and board recovery businesses indicating that capital is available for packaging systems linked to better material recovery and reuse.[2]EBRD Green Economy Financing Facility, “Modernization of Industrial Equipment for a Moroccan SME Specialized in Collection and Recovery of Paper and Board,” EBRD GEFF, ebrdgeff.com Over time, this makes paper-based secondary packaging easier to justify on both compliance and cost grounds, which gives the Moroccan containerboard market a broader base than food and industrial demand alone.

Automotive And Industrial Nearshoring Around Tanger Med

The industrial build-out around Tanger Med has become an important growth driver for the Moroccan containerboard market, as automotive and supplier packaging demand higher-grade board than standard agricultural cartons. The Tanger Med Industrial Platform hosted more than 120 automotive operators, including 11 of the world’s top 20 automotive companies, and generated more than 40,000 direct jobs with an investment base of over USD 4 billion.[3]Tanger Med Special Agency, “Automotive,” Tanger Med Industrial Platform, tangermed.ma In 2024, the platform attracted MAD 3.63 billion (USD 366.7 million) in new private industrial investments and confirmed 95 new industrial projects, creating 11,239 jobs. The third expansion of Tanger Automotive City, completed in September 2025, added 140 hectares and delivered 105 hectares to the market with more than 70 developed lots under a MAD 300 million (USD 30.3 million) infrastructure commitment. That concentration of Tier 1 and Tier 2 suppliers supports demand for double-wall constructions, custom die-cuts, anti-static liners, and higher edge-crush performance, which is one reason kraftliner growth is running ahead of the broader Morocco containerboard market.

Capacity Additions In Recycled Containerboard And Corrugated Conversion

The Morocco containerboard market is in its strongest investment cycle in more than a decade, and new capacity is changing who can compete for higher-value contracts. GPC Papier et Carton announced in September 2025 a MAD 500 million (USD 50 million) expansion of its Mohammedia site, aiming to raise annual corrugated production capacity from 90,000 to 160,000 tons by 2030. At SIAM 2026, GPC also confirmed a MAD 200 million (USD 20 million) investment in a new Agropolis Meknes industrial unit that was already more than 50% complete and scheduled for commissioning by the end of 2026. Smurfit Westrock’s investment in its Rabat plant also exceeded MAD 400 million (USD 40.4 million), adding high-definition printing capability and a packaging Experience Center that raises the technical bar for premium corrugated conversion. These additions matter because they widen the gap between integrated groups with modern print and converting lines and smaller converters that still compete mostly on price in lower-spec box formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Fiber Supply Gaps and Import Dependence | -0.4% | National, with acute pressure on Kenitra and Mohammedia recycled-fiber mills | Short term (≤ 2 years) |

| Water Stress and Utility-Cost Volatility | -0.3% | Souss-Massa, Tensift, and Moulouya basin mill locations | Medium term (2-4 years) |

| High Customer Concentration in Export Agriculture | -0.2% | Atlantic coastal agricultural corridors, Souss-Massa and Gharb | Medium term (2-4 years) |

| Informal Waste-Collection Frictions and Tax Traceability Pressure | -0.1% | National, with higher exposure in peri-urban industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Fiber Supply Gaps And Import Dependence

Recovered fiber availability remains a real operating constraint for the Morocco containerboard market because recycled-fiber mills need a more dependable local stream of old corrugated containers than the country currently recovers. A World Bank review of Morocco’s waste flows indicated that household paper recycling remained limited relative to the needs of downstream recycling users, which helps explain the pressure on the domestic fiber balance.[4]World Bank, “Sourcing of Post-Industrial Cotton Textile Waste in the Tangier Area - Paper Waste Management Section,” World Bank, worldbank.org International Paper stated that its Kenitra mill processes around 90,000 tons of locally sourced recovered paper each year, which shows the scale of demand placed on the domestic collection system by just one major site. When local recovery weakens, mills turn to imported recovered paper from Europe, and that exposes margins to freight costs and tighter fiber markets outside Morocco. Smaller recycled-fiber producers are usually hit first in these periods because they lack the sourcing reach and balance-sheet strength of the leading integrated groups.

Water Stress And Utility-Cost Volatility

Water stress is another clear restraint on the Moroccan containerboard market, as paper and board manufacturing depends on stable process water for pulping, pressing, and cooling. Morocco entered late 2025 under severe water pressure, and the country also accelerated wastewater reuse plans as part of a broader response to scarcity. That helped frame water efficiency as an operating requirement rather than a sustainability side issue for containerboard mills and converters. Facilities that do not invest in recirculation loops, lower-intensity process systems, and tighter utility management are more exposed to cost volatility and to local operating restrictions in drought-stressed catchments. This matters most in agricultural and industrial zones where packaging demand is growing, because the same regions are also under strain from competing water needs across farming, households, and manufacturing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled-Fiber Dominance Tested By Quality Premiums

Recycled fibers commanded a 60.48% share of the Moroccan containerboard market in 2025, reflecting the long-standing build-out of old corrugated containerboard capacity around Kenitra and nearby conversion corridors. That lead remained tied to the cost advantage of recycled board in domestic distribution, industrial secondary packaging, and large-volume brown-box applications where appearance and burst strength are not the first buying criteria. Even so, the Morocco containerboard market is seeing a gradual mix shift toward virgin-fiber grades in applications where export durability, print quality, and food-contact documentation matter more. Virgin fibers are the fastest-growing material segment from 2026 to 2031, with a CAGR of 3.16%, supported by automotive packaging needs around Tanger Med and by export accounts seeking stronger traceability and more consistent performance.

The change in material demand is not a simple move away from recycled board; it is a move toward more differentiated substrates within the Moroccan containerboard industry. Buyers increasingly want documented recycled-content percentages, chain-of-custody support, and stable print surfaces, which gives integrated mills an advantage when specifications become stricter. International Paper said its Kenitra site recycles around 90,000 tons of recovered paper annually, underscoring the central role of local fiber recovery in the material balance of the Moroccan containerboard market. The same site also holds ISO 50001 energy management certification, which demonstrates the operating discipline now expected from larger producers serving demanding customers. Recycled grades should therefore keep their volume lead through 2031, while virgin-fiber kraft products are likely to take a larger share of value growth.

By Product Type: Kraftliners Gaining Ground In High-Value Channels

Testliners held a 41.64% share of the Moroccan containerboard market by product type in 2025, consistent with a supply base built around cost-efficient agricultural, retail, and industrial boxes. Flutings remained the structural companion grade for a wide range of corrugated formats and continued to serve conversion plants in Agadir, Casablanca, and Tangier. Kraftliners are the fastest-growing product type from 2026 to 2031, with a CAGR of 3.24%, and that growth reflects demand from automotive suppliers, pharmaceutical packaging needs, and premium fresh-produce exports that require stronger, cleaner-performing board. This mix shift shows that the Morocco containerboard market is no longer defined only by high-volume commodity grades.

The product upgrade is most visible in contracts that require humidity resistance, better surface quality, or documented food-safety compliance. Smurfit WestRock’s Rabat facility achieved BRCGS AA+ packaging safety certification in 2025, signaling that internationally recognized safety systems are becoming a baseline requirement in food-contact corrugated rather than a niche extra. The company also presented AgroLife, AquaStop, and Goliath packaging solutions for produce exporters, showing how product development is moving toward application-specific corrugated formats rather than generic board substitution. Testliners should continue to defend their place in domestic consumer goods and lower-margin industrial uses, where recycled content and price remain central to purchasing decisions. Still, Kraftliner is likely to gain faster in value terms than in tonnage, which will keep lifting the average quality mix of the Moroccan containerboard market.

By End-User Industry: Food And Beverage Anchors Demand But Consumer Goods Accelerates

Food and beverage retained the leading position in 2025 with a 38.77% share of the Moroccan containerboard market, supported by domestic processed food flows and a large fresh produce export base that depends on corrugated trays and boxes. That segment remains the clearest volume anchor because food distribution creates repeat packaging demand across growing, packing, warehousing, and shipment. Consumer goods are the fastest-growing end-user segment from 2026 to 2031 with a CAGR of 3.31%, as formal retail channels expand and more shipments move through parcel-ready formats. This shift shows that the Moroccan containerboard market is gaining support from both everyday retail distribution and export agriculture.

Industrial demand also plays an important role, as the Tanger Med platform has become a major and growing source of packaging for automotive and supplier networks. The platform hosted more than 120 automotive operators with combined investments exceeding USD 4 billion, providing the Moroccan containerboard market with a meaningful industrial packaging base beyond food and fast-moving consumer goods. Online buyer penetration rose from 15.1% of the population in 2019 to 24.9% in 2024, adding 3.7 million online shoppers, and the e-commerce economy exceeded MAD 22 billion (USD 2.35 billion) in 2023. Other end-user categories, including pharmaceuticals, chemicals, and ceramics, provide a stable demand floor even when seasonal agricultural volumes fluctuate. As retail, export compliance, and industrial supply chains become more formal, the Moroccan containerboard market should continue to shift toward converters that can meet delivery, documentation, and print requirements simultaneously.

Geography Analysis

The Morocco containerboard market is concentrated across 3 main geographic clusters that closely reflect the country’s industrial and agricultural map. The Atlantic corridor from Kenitra through Casablanca to Mohammedia remained the core production and conversion belt in 2025, with the largest concentration of recycled-fiber mills and corrugated converters. Casablanca continued to serve as the main center for the consumption of consumer goods, pharmaceuticals, and general industrial packaging because it remained Morocco’s commercial and logistics hub. Kenitra benefited from established recovered-paper collection links to Greater Casablanca and from automotive-related packaging demand tied to nearby manufacturing activity. The corridor’s scale is also visible in plant-level operations, with International Paper stating that its Kenitra mill recycles around 90,000 tons of recovered paper annually and serves containerboard demand across Morocco.

The northern Tangier corridor presents a different demand profile in the Moroccan containerboard market, driven more by industrial and transit packaging than by agricultural boxes. Tanger Med’s automotive platform hosted more than 120 operators and had attracted more than USD 4 billion in investment, supporting a steady demand for technical corrugated packaging and just-in-time box supply. The third expansion of Tanger Automotive City in September 2025 added 140 hectares and more than 70 developed lots, further increasing the packaging demand base in the zone. Broad-Ocean Motor also confirmed a MAD 1.245 billion (USD 125.8 million) facility in Tanger Automotive City, which reinforced the long-term industrial packaging outlook for the northern Morocco containerboard market.

The southern Souss-Massa corridor around Agadir remained the center of fresh produce export packaging in the Moroccan containerboard market and was also the area most exposed to seasonality and weather conditions. Demand is tied to packinghouse schedules, the produce mix, and the need for trays and boxes that can handle moisture, support traceability, and comply with export requirements. CMCP-International Paper’s expansion of its Ait Melloul facility near Agadir showed how closely conversion capacity is being placed near produce-export activity in the south. The interior Meknes-Fes area is emerging as a supporting node, and Morocco’s use of Tanger Med and AfCFTA routes is gradually widening the addressable reach of the Morocco containerboard market beyond domestic consumption alone.

Competitive Landscape

The Morocco containerboard market remained concentrated at the integrated production level in 2025, even as competition remained intense among smaller regional converters serving commodity box grades. CMCP-International Paper and GPC Papier et Carton continued to shape the market through their control of core papermaking and corrugated conversion assets, while more than a dozen smaller converters competed mainly on price, speed, and local customer relationships. That structure means the Morocco containerboard market is concentrated in manufacturing capacity, but less concentrated in day-to-day bidding for standard box formats. The biggest competitive gap now lies in certification, print capability, fiber sourcing, and the ability to serve national accounts across multiple end markets. Smaller firms can still win regional business, but they face growing pressure when buyers ask for food-safety systems, traceability, or more complex printed packaging.

A major strategic move came in January 2025, when International Paper completed its acquisition of DS Smith, creating a broader global packaging platform with combined 2024 net sales of USD 18.6 billion. That deal strengthens CMCP-International Paper's position in the Moroccan containerboard market through greater procurement leverage, broader technical resources, and stronger access to EMEA packaging know-how. International Paper also increased investment in Morocco to support demand for corrugated packaging, reinforcing its local customer ties in both agricultural and industrial channels. On the domestic side, GPC has been expanding capacity and upgrading printing capabilities, indicating that competition in the Moroccan containerboard market is moving away from pure volume toward technical differentiation.

Smurfit Westrock Morocco has taken a different route by focusing on design-led selling, food-contact corrugated, and premium accounts in FMCG, pharmaceuticals, and export agriculture. That position matters because the Moroccan containerboard market is starting to reward converters that can combine compliance, speed, and product development in a single offer. Another strategic signal came in May 2026, when Boxon Group established local industrial packaging manufacturing and supply operations in Morocco to serve standard and customized corrugated demand closer to customer sites. The move suggests that specialist European packaging suppliers now see Morocco as large enough and capable enough to support local manufacturing rather than export-only service models. As a result, the Moroccan containerboard market is likely to remain led by a small group of strong integrated players, while new specialist entries increase pressure in selected higher-value niches.

Morocco Containerboard Industry Leaders

International Paper Company

GPC Papier et Carton

Smurfit Westrock Morocco

AMG PACKAGING

Fineprod

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Boxon Group (Sweden) established local industrial packaging manufacturing and supply operations in Morocco, enabling delivery of both standard and customized corrugated solutions produced domestically. The move, announced via the company's official press release, is designed to reduce lead times for automotive and agricultural industrial accounts and responds to growing regional sourcing requirements from European clients investing in Morocco.

- October 2025: Broad-Ocean Motor (China) confirmed the establishment of a MAD 1.245 billion (USD 125.8 million) electric and hybrid engine manufacturing facility at Tanger Automotive City through subsidiaries SHedrive Industrial Morocco and SHedrive Trading Morocco. While primarily an automotive investment, this confirms sustained growth in Tanger Med's industrial packaging demand through 2027 and beyond, per Tanger Med Special Agency's official announcement.

- September 2025: Tanger Med Special Agency delivered the third expansion of Tanger Automotive City, spanning 140 hectares with a MAD 300 million (USD 30.3 million) infrastructure investment, providing over 70 developed industrial lots. This expansion directly adds industrial packaging demand from new Tier 1 and Tier 2 automotive suppliers entering the ecosystem, per Tanger Med Special Agency's official announcement.

- January 2025: International Paper completed its acquisition of DS Smith plc, creating a global leader in sustainable packaging with combined 2024 net sales of USD 18.6 billion, as disclosed in International Paper's January 31, 2025, SEC 8-K filing. The combined entity strengthens CMCP-International Paper's position in Morocco through access to DS Smith's EMEA papermaking assets, technology, and sustainability frameworks.

Morocco Containerboard Market Report Scope

The Morocco Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Morocco Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Morocco containerboard market and what is the outlook to 2031?

The Morocco containerboard market was valued at USD 121.91 million in 2025, reached USD 133.81 million in 2026, and is projected to reach USD 154.01 million by 2031 at a 2.85% CAGR.

Which material type leads demand in Morocco?

Recycled fibers led in 2025 with a 60.48% share, supported by the country's established recovered-paper and corrugated conversion base.

Which product type is growing the fastest in Morocco's containerboard space?

Kraftliners are projected to record the fastest growth at a 3.24% CAGR through 2031 because export and industrial users need stronger and more durable board grades.

Which end-user group drives the largest share of demand?

Food and beverage led with a 38.77% share in 2025, reflecting the importance of domestic food distribution and fresh produce export packaging.

Why is Tanger Med important for corrugated packaging demand?

Tanger Med anchors automotive and industrial nearshoring, which raises demand for heavier-duty, specification-driven corrugated packaging used in parts movement and export logistics.

What are the main risks affecting future growth in Morocco?

The main risks are uneven recovered-fiber availability, periodic import dependence for OCC, and water stress that can raise operating costs for mills and converters.

Page last updated on: