Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

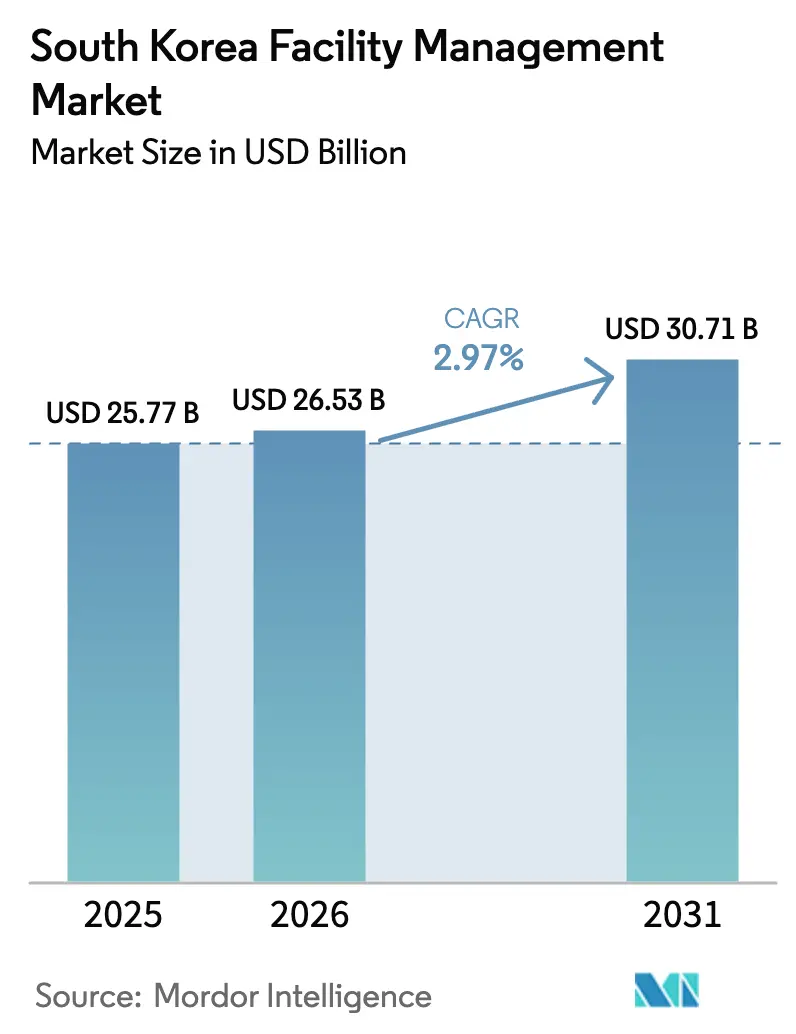

| Base Year Market Size (2025) | USD 25.77 Billion |

| Market Size (2026) | USD 26.53 Billion |

| Market Size (2031) | USD 30.71 Billion |

| Growth Rate (2026 - 2031) | 2.97% CAGR |

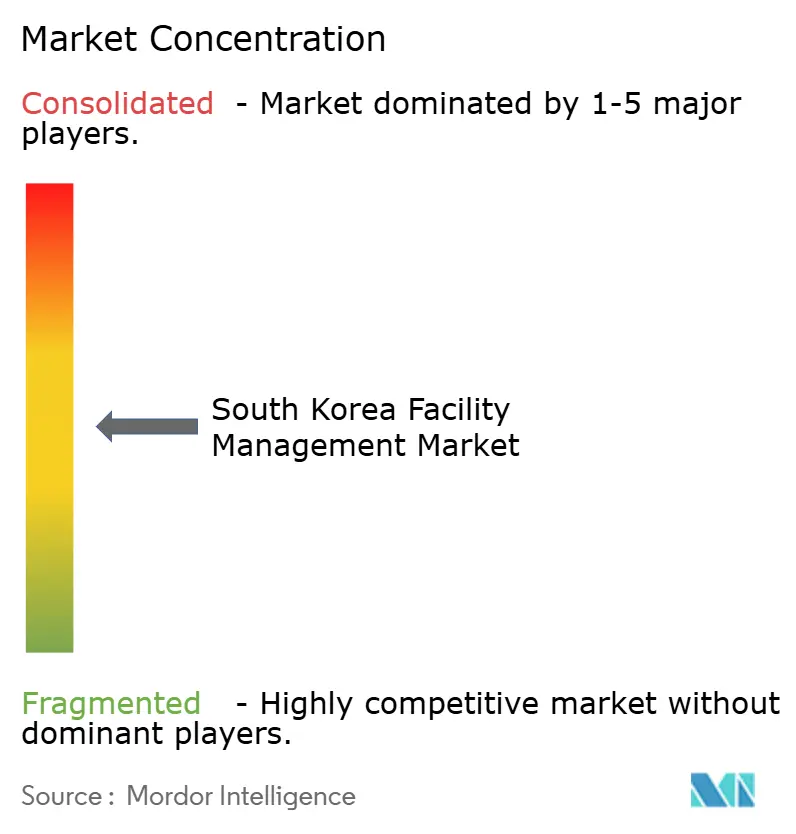

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Facility Management Market Analysis by Mordor Intelligence

The South Korea facility management market size was valued at USD 25.77 billion in 2025 and estimated to grow from USD 26.53 billion in 2026 to reach USD 30.71 billion by 2031, at a CAGR of 2.97% during the forecast period (2026-2031). This growth is being underpinned by hyperscale data-center construction, stringent safety regulations, and rising demand for energy-efficient building operations. Outsourced, technology-enabled service models are gaining momentum as corporations focus on core competencies and delegate increasingly complex building tasks to specialist providers. Steady urbanization in the Seoul Capital Area and government incentives for zero-energy buildings are expanding the addressable base for professional facility services. Meanwhile, risk-transfer motives linked to the Serious Accidents Punishment Act (SAPA) and emerging ESG disclosure mandates are accelerating the shift toward certified, compliance-oriented partners.

Key Report Takeaways

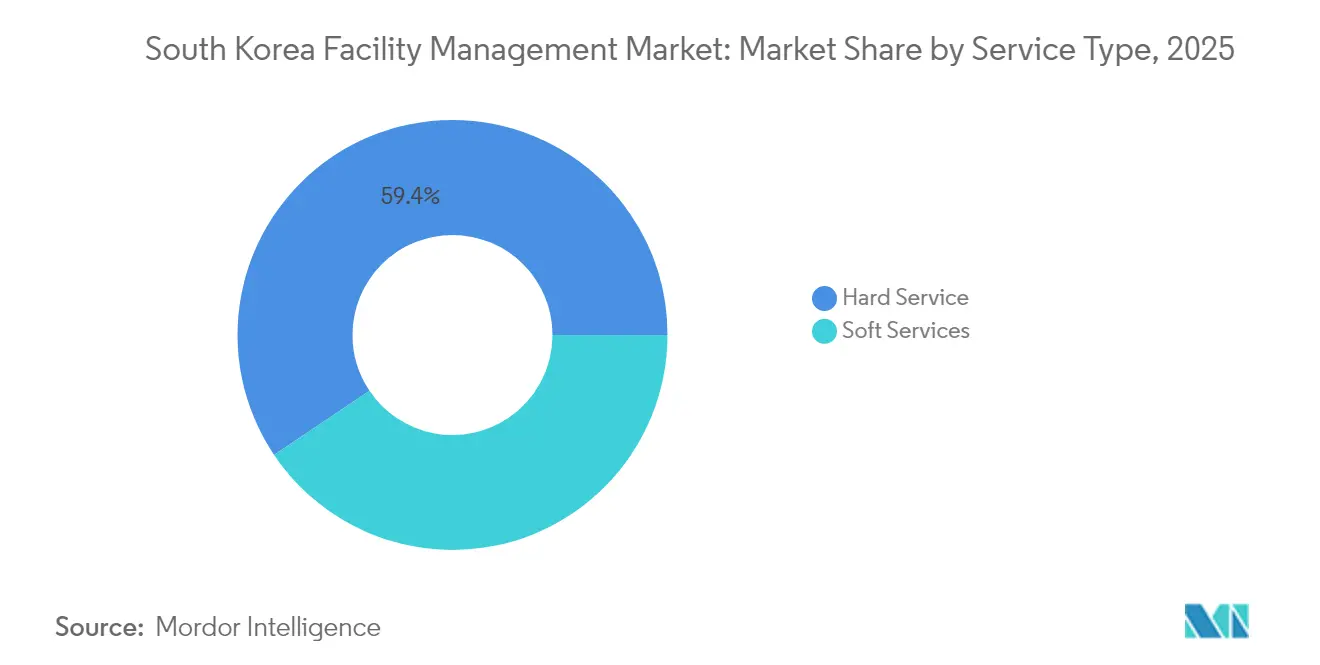

- By service type, hard services dominated with 59.42% South Korea facility management market share in 2025, while soft services are advancing at a 4.41% CAGR through 2031.

- By offering type, outsourced services captured 62.10% of the South Korea facility management market size in 2025 and are expanding at a 4.82% CAGR over the same horizon.

- By end-user industry, the commercial segment led with 42.02% revenue share in 2025, whereas institutional and public infrastructure facilities are forecast to grow at 6.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technology-led integrated FM | +1.2% | National; Seoul Capital Area focus | Medium term (2-4 years) |

| ESG compliance mandates | +0.8% | National; early uptake by large listed firms | Long term (≥ 4 years) |

| Urbanization of metropolitan corridors | +0.6% | Seoul, Busan, Daegu | Long term (≥ 4 years) |

| Labour-standards enforcement | +0.4% | Nationwide; highest in manufacturing clusters | Short term (≤ 2 years) |

| Hyperscale and AI data-center expansion | +0.7% | Gyeonggi, Ulsan, Jeollanam-do | Medium term (2-4 years) |

| Zero-energy building (ZEB) incentives | +0.3% | Nationwide; aging stock concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technology-led Integrated FM Drives Market Transformation

IoT-enabled sensors, AI analytics, and building-management platforms are converging to deliver predictive maintenance that cuts facility downtime by 15-20% while shrinking energy bills by close to one-quarter. [1] Hanwha Systems, “Smart Building Solution,” hanwhasystems.comKorean service providers embed cloud-based diagnostics in elevators, HVAC units, and security networks, enabling real-time fault isolation in dense urban complexes. Labour shortages and rising wage costs are pushing owners to automate inspection routines, sustaining investment in building-automation software even during economic slowdowns. Indoor 5G roll-outs promise faster device-to-device communication, allowing high-bandwidth data streams from smart cameras and environmental sensors to feed central dashboards. Integrated FM contracts built around guaranteed uptime and energy-saving metrics command premium pricing and foster deeper, multi-year alliances with occupiers.

ESG Compliance Mandates Reshape Service Delivery Models

From 2026, listed firms with assets above KRW 2 trillion must publish ESG reports in line with IFRS Sustainability Standards, expanding to all listed companies by 2030. The Korea Sustainability Standards Board has specified carbon-reduction and energy-performance indicators that facility managers must monitor, audit, and improve. Building owners therefore bundle metering, waste-management, and environmental data analytics into FM contracts to prove year-on-year progress. Outcome-based agreements—where providers are remunerated for delivering specific carbon-emission cuts—are gaining traction, particularly among conglomerates seeking to future-proof regulatory disclosures. The shift is steering investment toward smart meters, renewable-ready electrical infrastructure, and LEED/G-SEED certification advisory services, positioning FM partners as guardians of corporate sustainability credentials.

Urbanization Accelerates Demand for Sophisticated FM Services

High-density corridors now hold 46.1% of South Korea’s population and generate 46.2% of its GDP, concentrating facility needs in vertical office towers, mixed-use retail hubs, and co-living complexes. With land finite and rental rates climbing, owners prioritise occupant experience, pushing FM providers to integrate concierge, space-scheduling, and indoor-air-quality optimisation into everyday operations. Living SOC programmes deliver new community centres, libraries, and sports halls in provincial cities, creating fresh institutional FM demand. Urban regeneration projects funded by the National Housing and Urban Fund require adaptive-reuse strategies and tight coordination between heritage preservation and modern safety codes. Case evidence from Gangnam shows integrated FM adoption lifting tenant-retention rates by one-fifth and enabling landlords to charge rent premiums above neighbouring mono-use assets.

Labour Standards Enforcement Creates Compliance Opportunities

The Serious Accidents Punishment Act (SAPA) makes corporate executives criminally liable for fatal incidents, elevating safety management to board-level priority. Workplace accidents spiked to 136,796 cases in 2023, intensifying scrutiny on risk assessments and contractor oversight. Specialist FM partners supply certified safety officers, maintain digital permit-to-work logs, and automate chemical-handling documentation, helping manufacturers reduce incident frequency and avoid reputational damage. Outsourced safety programmes have shown capability to lower workplace injuries by over 40% and to trim compliance administration costs by roughly one-third, according to aggregated case studies in heavy industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic pressures on construction | -0.5% | Nationwide; strongest in SME segments | Short term (≤ 2 years) |

| Technical-skills shortage | -0.3% | Nationwide; acute in IoT and energy disciplines | Medium term (2-4 years) |

| Volatile electricity tariffs | -0.4% | Nationwide; acute for energy-intensive assets | Short term (≤ 2 years) |

| Short-term, price-driven contracts | -0.2% | Nationwide; prevalent in public procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Pressures Constrain Service Expansion

Construction revenues slid 6.7% to USD 166 billion in 2023 as tighter monetary policy cooled new-build pipelines, prompting building owners to defer non-essential upgrades. [2]U.S. International Trade Administration, “South Korea – Construction Services,” trade.gov Steel and cement prices surged 35% and 28% respectively in 2024, squeezing capex budgets and steering demand toward minimal-scope maintenance contracts. Facility management teams now pitch demonstrable ROI via energy-cost reductions, deferred capex through asset-life extension, and stricter safety compliance as antidotes to owners’ budget caution.

Workforce Skills Gap Limits Service Quality Advancement

Aging technicians and a preference among graduates for large-firm employment have left mid-sized FM contractors understaffed in advanced controls, cybersecurity, and sustainability analytics. Only 26.1% of certified fire engineers are currently engaged in value-engineering proposals, highlighting under-utilisation of hard-won expertise. [3]Korean Society of Hazard Mitigation, “Applying Value Engineering in the Fire Brigade,” j-kosham.or.kr Project delays lengthen by 20% and labour costs inflate by around 15% when specialist skills are scarce, curbing adoption of smart-building upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Dominate Despite Soft Services Growth Acceleration

Hard services accounted for 59.42% of the South Korea facility management market in 2025 and remain indispensable because mechanical, electrical, and plumbing systems must meet strict uptime and safety codes. Asset-management revenues are rising as 72.3% of national water infrastructure is forecast to reach obsolescence by 2035, amplifying the need for proactive maintenance. Compliance with SAPA has also boosted demand for certified life-safety inspections. Integrated hard-service contracts have delivered 30% downtime reductions and 25% energy savings compared with siloed outsourcing models.

Soft services, though smaller, are projected to outpace hard services at 4.41% CAGR to 2031. Robotic cleaning, AI-driven security analytics, and premium workplace amenities are reshaping expectations among technology tenants in Seoul’s Grade-A offices. Hybrid-work footprints compel continuous re-planning of desk allocation and conference areas, fostering growth in space-optimisation advisory. As ingredient prices climbed 18% in 2024, catering providers introduced menu-engineering software and dynamic pricing to safeguard margins while maintaining employee-experience standards.

By Offering Type: Outsourcing Acceleration Reshapes Service Delivery

Outsourced arrangements represented 62.10% of the South Korea facility management market size in 2025 and will expand at 4.82% CAGR through 2031 as corporations concentrate on core digital-transformation initiatives. Bundled and integrated FM models reduce vendor-management complexity, shifting risk to providers that possess multi-disciplinary talent pools. Comparative studies show enterprises trimming indirect costs by 25% when they migrate from fragmented in-house teams to single-provider frameworks.

In-house operations, still holding 37.90% share, persist in defence, critical-infrastructure, and select public-sector domains where security sovereignty is paramount. Yet these owners bear 25% higher hidden costs related to technology upgrades and compliance administration, prompting a gradual move toward hybrid models. Bulk purchasing of cleaning supplies and maintenance consumables through outsourced providers mitigates material-cost inflation of more than 28% in 2024, strengthening the outsourcing value proposition.

By End-user Industry: Commercial Leadership Challenged by Institutional Growth

The commercial segment led with 42.02% South Korea facility management market share in 2025, anchored by Seoul’s role as a regional headquarters hub and its surging inventory of data-rich office campuses. Demand is especially strong for uptime-orientated services covering building-management systems, cybersecurity overlays, and flexible workspace re-configuration.

Institutional and public infrastructure facilities are slated for the fastest expansion at 6.32% CAGR through 2031 as Living SOC policies channel capital into community centres, hospitals, and transport interchanges. Hospitals that adopt dedicated healthcare-FM protocols have cut infection-control failures by one-fifth and shaved 15% off biomedical-equipment maintenance costs. Industrial complexes and semiconductor fabs seek FM partners with hazardous-materials stewardship and clean-room certification, while hospitality operators rely on cost-efficient linen and housekeeping solutions amid rising tourism traffic.

Geography Analysis

The Seoul Capital Area commands the largest slice of the South Korea facility management market due to its high-rise skyline, dense data-center footprint, and concentration of headquarters buildings. Integrated FM contracts in the city’s central business district achieve 35% higher client-retention rates and secure 20% premium pricing compared with other regions, illustrating the value placed on technical sophistication and rapid response times.

Gyeonggi Province and adjacent corridors are emerging as the fastest-growing markets as hyperscale data-center clusters, logistics hubs, and satellite R&D campuses proliferate. Providers that deploy regionally distributed technician teams capture economies of proximity while mitigating Seoul’s 15% higher average labour costs. Ulsan and Jeollanam-do, newly earmarked for multigigawatt AI data-center complexes, present greenfield opportunities for critical-environment FM specialists equipped to deliver 99.99% uptime guarantees.

Beyond the metropolitan ring, provincial cities benefit from Living SOC infrastructure infusions and green-growth incentives. Tourism-focused coastal zones require guest-experience-centric FM packages for resorts and convention centres. Rural renewables installations create niches in asset-integrity monitoring, though the scarcity of local engineers obliges providers to invest in mobile service units and remote-diagnostics platforms to match metropolitan service benchmarks.

Competitive Landscape

South Korea’s facility-management arena is moderately fragmented. No single firm holds more than 10% national revenue, pushing providers to differentiate through technology investment and sector specialisation. Domestic champions such as S&I Corporation leverage deep regulatory familiarity and have secured landmark data-center mandates, underscoring the premium attached to mission-critical expertise. Global multinationals complement their scale advantage with proprietary CAFM software, yet must tailor workflows to Korea’s stringent labour and safety codes.

Technology is rapidly redefining competitive boundaries. Firms integrating AI-driven analytics into core workflows routinely demonstrate 15-point margin advantages over peers reliant on manual inspection logs. Outcome-based contracts tied to ESG metrics reward agile providers that can quantify carbon reductions and safety improvements in real time. Sector specialists—serving semiconductor clean rooms, pharmaceutical labs, or renewable-energy parks—command price premiums upwards of 40% owing to scarce technical know-how.

Looking ahead, competitive intensity is set to rise as mid-tier contractors form alliances with proptech start-ups to bridge the digital-skills gap. Meanwhile, foreign entrants eye provincial growth corridors opened by mega-data-center investments. The ability to align with SAPA compliance, deliver validated sustainability data, and scale technician pools swiftly will determine share gains during the forecast window.

South Korea Facility Management Industry Leaders

Samkoo Inc Co., Ltd

Hyundai GBFMS

CBRE Group, Inc.

Sodexo Oy

Savills Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SK Group and Amazon Web Services confirmed a USD 4 billion joint venture to construct a 103-MW AI data center in Ulsan, creating significant demand for critical-environment FM solutions.

- February 2025: Stock Farm Road gained government clearance for a USD 35 billion, 3-GW data-center project in Jeollanam-do, projected to open in 2028.

- February 2025: SK Ecoplant agreed to divest waste-treatment units worth USD 1.4 billion, reallocating capital toward semiconductor-infrastructure FM services.

- July 2024: S&I Corporation won the operation contract for Seoul’s Gasan DCI Data Center, reinforcing its data-center management credentials.

South Korea Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through its responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The market for integrated facility management service (IFM), along with single and bundled services, is included in the outsourced FM services segment.

The South Korea facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail andWarehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail andWarehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the South Korea facility management market?

The market was valued at USD 26.53 billion in 2026 and is forecast to climb to USD 30.71 billion by 2031 at a 2.97% CAGR.

Which service type leads revenue generation?

Hard services—covering MEP, fire safety, and asset management—held 59.42% market share in 2025, driven by strict compliance requirements.

Why are outsourced facility-management models expanding quickly?

Outsourcing captured 62.10% market share in 2025 and is growing at 4.82% CAGR because companies are transferring regulatory risk and technical complexity to specialised providers.

How do ESG mandates influence facility-management demand?

Starting in 2026, large listed firms must report building-performance metrics, pushing them to hire FM partners that can deliver verifiable energy and carbon reductions.

What impact will hyperscale data-center construction have on service providers?

New AI and cloud campuses require 99.99% uptime, precision cooling, and fortified security, creating high-margin opportunities for critical-environment FM specialists.

Which geographic regions offer the fastest growth prospects?

Gyeonggi Province, Ulsan, and Jeollanam-do are poised for rapid expansion owing to large data-center investments and government infrastructure programmes.

Page last updated on: