Saudi Arabia Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

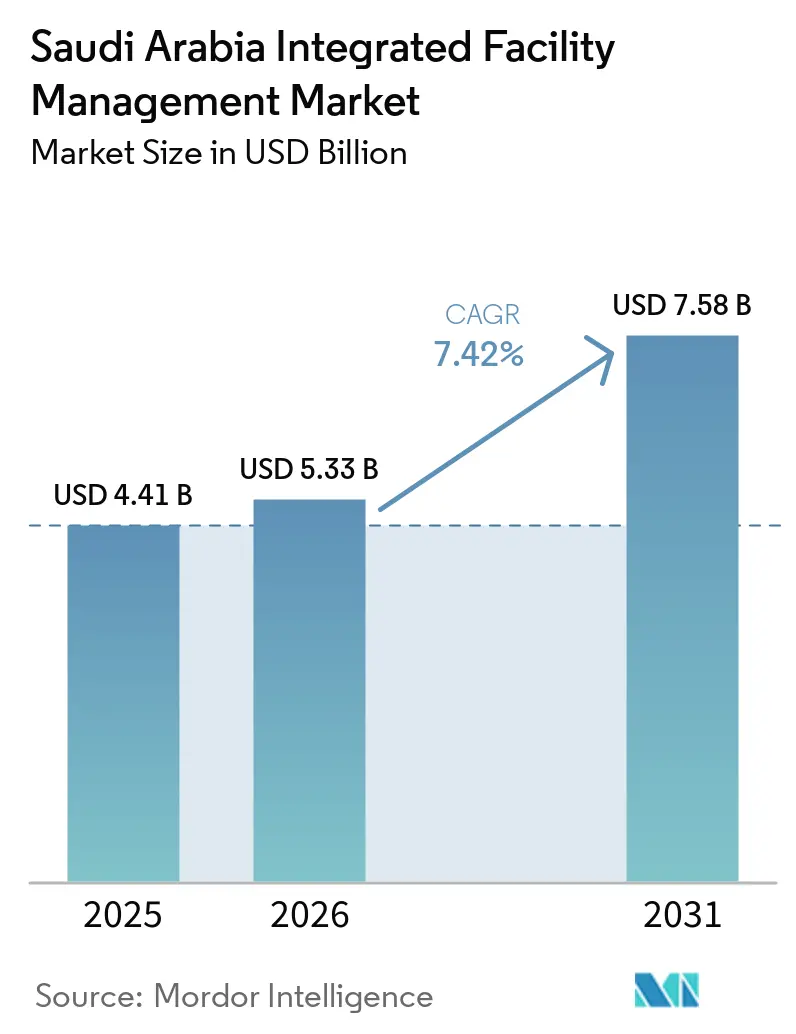

| Base Year Market Size (2025) | USD 4.41 Billion |

| Market Size (2026) | USD 5.33 Billion |

| Market Size (2031) | USD 7.58 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

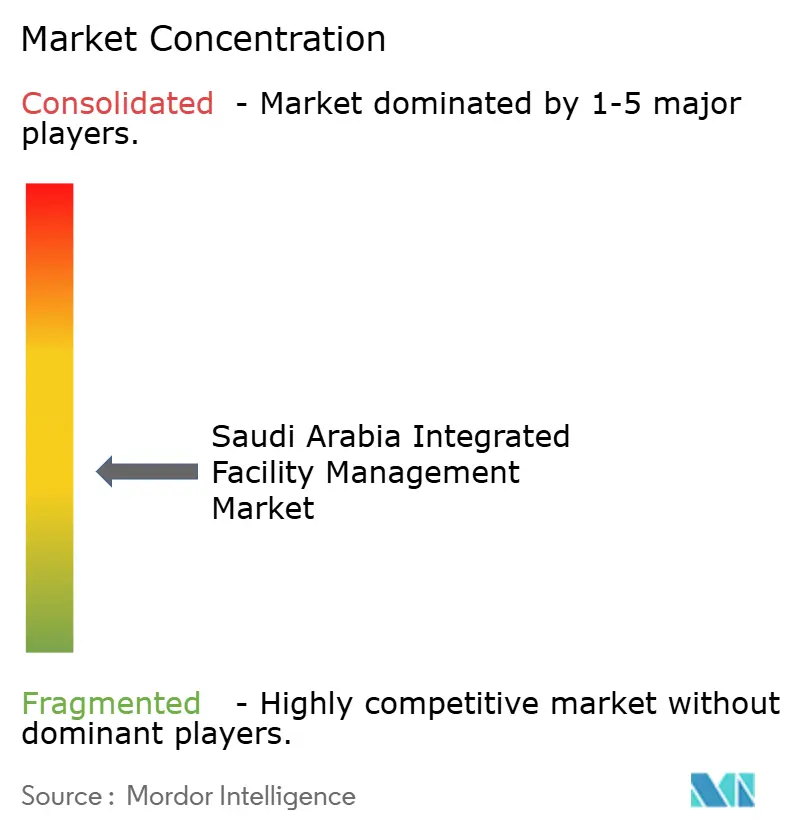

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Integrated Facility Management Market Analysis by Mordor Intelligence

The Saudi Arabia integrated facility management market size was valued at USD 4.41 billion in 2025 and is estimated to grow from USD 5.33 billion in 2026 to reach USD 7.58 billion by 2031, at a CAGR of 7.42% during the forecast period 2026-2031. The Saudi Arabia integrated facility management (IFM) market is being shaped by Vision 2030, which continues to add large commercial, industrial, tourism, and public assets that need coordinated operations, maintenance, and lifecycle management across long contract periods. The Saudi Arabia (KSA) IFM market is also moving away from stand-alone service delivery because new assets require digital systems, up-time accountability, and measurable energy performance at the operating stage. Contract structures in the Saudi Arabia IFM market are becoming more output-based, and long-duration agreements now place greater value on technical capability, service integration, and sustainability performance than on labor scale alone. Cost pressure remains relevant because smart FM platforms require upfront investment and localization requirements are tightening the labor base for technical roles. Even so, the KSA integrated facility management market continues to offer room for providers that can combine compliance, engineering depth, digital maintenance, and energy management in a single delivery model.

Key Report Takeaways

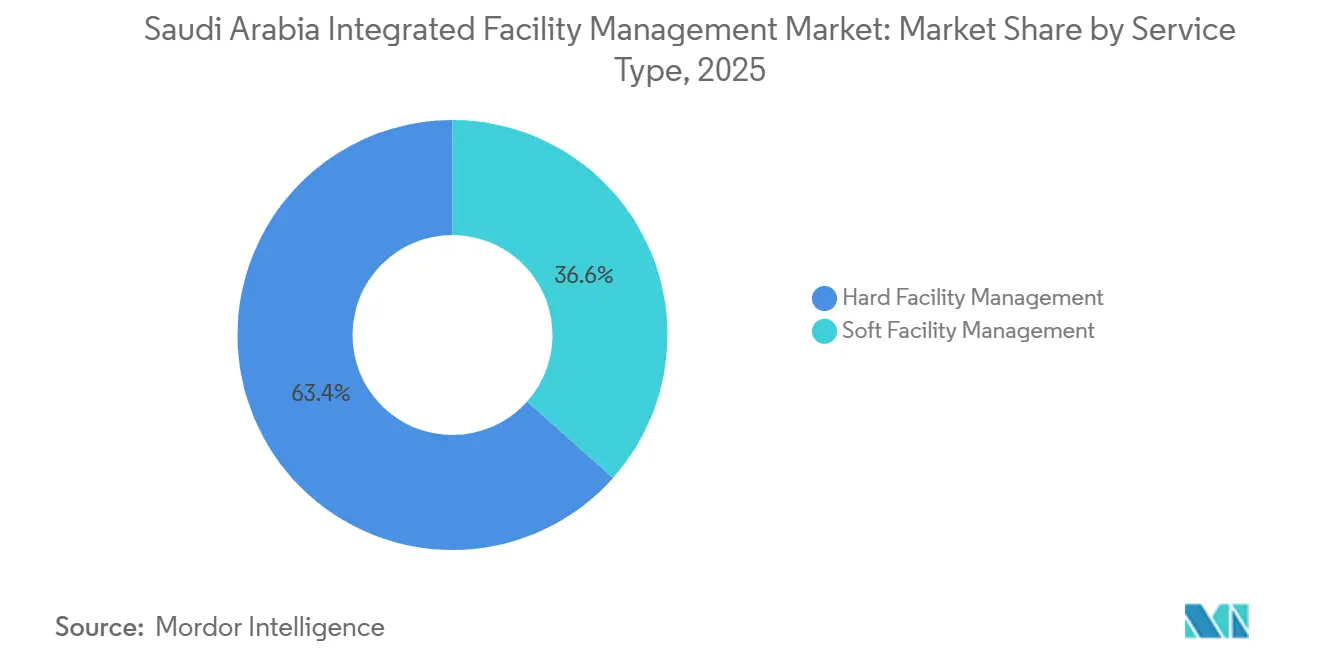

- By service type, soft facility management led with 63.41% revenue share of the Saudi Arabia integrated facility management market size in 2025, and hard facility management is forecast to expand at 8.29% CAGR through 2031.

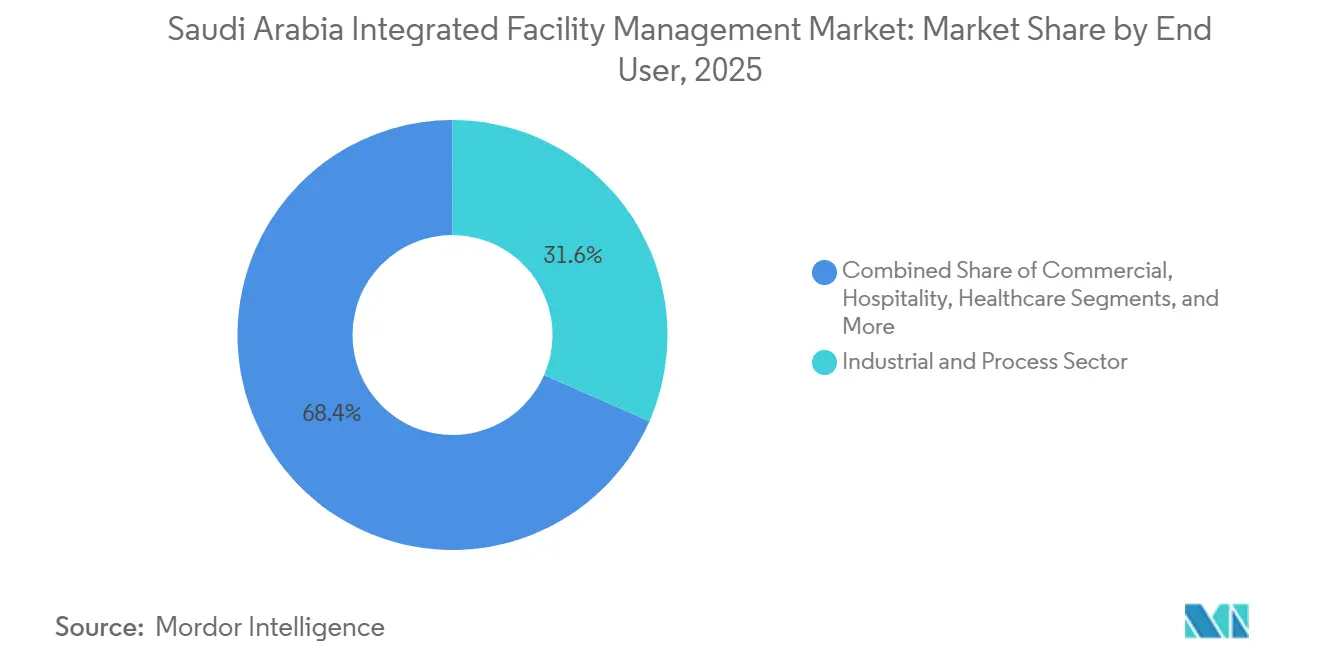

- By end-user industry, the Industrial and Process Sector held 31.56% revenue share of the Saudi Arabia integrated facility management (IFM) market size in 2025, and Commercial is forecast to grow at 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Giga-Projects Under Vision 2030 | +2.1% | National, with concentration in Riyadh, Western Region, including NEOM and Red Sea Global, and Eastern Province | Medium term (2-4 years) |

| Growing Demand For Technology-Enabled Predictive Maintenance | +1.3% | National, with early adopter concentration in Riyadh, Eastern Province industrial sites, and NEOM | Medium term (2-4 years) |

| Increasing Outsourcing Preference To Reduce Operating Costs | +1.0% | National, strongest in Commercial and Healthcare end-user segments | Short term (≤ 2 years) |

| Emphasis On Energy Efficiency And Sustainability Compliance | +0.8% | National, priority in Government and Commercial buildings in Riyadh and Jeddah | Medium term (2-4 years) |

| Rapid Growth Of Smart Buildings And IoT Deployment | +0.6% | National, concentrated in Riyadh, NEOM, and newly commissioned giga-project assets | Long term (≥ 4 years) |

| Facilities Management Consolidation For Single-Contract Accountability | +0.5% | National, highest traction in Healthcare, Institutional, and large Commercial portfolios | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Giga-Projects Under Vision 2030

The Saudi Arabia integrated facility management market is strongly tied to the Kingdom's giga-project pipeline because these projects are creating large volumes of complex built space that need integrated support after commissioning. Public Investment Fund assets under management stood at USD 0.94 trillion in 2024, and the official target remains USD 2.67 trillion by 2030, which shows the scale of future real asset creation behind demand for integrated services.[1]Saudi Vision 2030, “Vision 2030 Annual Report 2024,” Vision 2030, vision2030.gov.sa NEOM, Diriyah, Qiddiya, and Red Sea Global are not ordinary real estate additions because they are being designed around smart infrastructure, sustainability goals, and long operating lives. That changes the service mix in the Saudi Arabia integrated facility management market because owners need providers that can handle engineering systems, occupant services, compliance, and data visibility under one contract. It also raises the qualification bar because asset owners increasingly expect digital twin readiness, connected maintenance workflows, and performance reporting from the first day of operations. As more of these projects move from construction into operation, the KSA integrated facility management market is likely to see stronger demand for bundled contracts rather than isolated service packages.

Growing Demand for Technology-Enabled Predictive Maintenance

Predictive maintenance is becoming a normal requirement in the Saudi Arabia integrated facility management (IFM) market because downtime risk is rising across premium commercial, industrial, and hospitality assets. AI-driven fault detection and diagnostics at King Abdullah Financial District delivered a 30-45% reduction in unplanned downtime, and that level of performance is raising expectations for future Hard FM contracts.[2]IFMA Journal, “January 2026 Issue,” IFMA Journal, ifma.org A 2024 peer-reviewed study of 313 FM professionals in Saudi Arabia found that AI adoption had reached 40%, and 60% of respondents expected wider integration within 2 years. The value is not limited to convenience because predictive tools help providers reduce breakdowns, manage labor more efficiently, and protect service continuity in critical environments. In industrial settings, the same operating logic supports asset reliability, maintenance planning, and cost control across energy, process, and infrastructure sites. Providers that can connect IoT sensors, CAFM platforms, and measurable uptime targets are therefore improving their position in the Saudi Arabia IFM market.

Increasing Outsourcing Preference to Reduce Operating Costs

The Saudi Arabia integrated facility management market is also benefiting from a steady move away from in-house service delivery and toward outsourced integrated contracts. Asset owners are finding it harder to manage complex systems internally because modern portfolios now combine HVAC controls, access management, energy reporting, fire safety, and workplace support in a single operating environment. This is especially true in commercial and healthcare settings, where uptime, compliance, and user experience need specialist skills that internal teams often do not maintain at scale. The shift is changing contract design because buyers increasingly want one accountable party across multiple services instead of several small vendors working in parallel. That structure reduces coordination gaps and gives owners clearer service responsibility at site level. It also supports the KSA integrated facility management market by favoring providers that can absorb operational risk and offer lifecycle-based service commitments instead of short-term labor supply.

Emphasis on Energy Efficiency and Sustainability Compliance

Energy performance has become a core driver in the Saudi Arabia integrated facility management (IFM) market because buildings consume nearly 50% of the country's electricity, and HVAC alone can account for up to 70% of building-level consumption. Under the Saudi Green Initiative, all new public buildings are expected to meet at least LEED Gold or Mostadam 3-Pearl standards by 2030, which pushes FM providers into a more direct role in operational performance after handover. The Saudi Energy Efficiency Center is enforcing minimum performance standards across building systems, and the Sustainable Building Program has already assessed more than 70 projects covering over 50 million m² of built space.[3]Sustainability, “January 2026 Research On Energy Use In Buildings,” Sustainability, mdpi.com As a result, energy, water, and carbon metrics are moving into routine service agreements instead of sitting outside FM contracts. This is important for the KSA IFM market because sustainability capability is now linked to tender qualification, contract renewal, and premium pricing. Providers that cannot show documented efficiency outcomes are facing a weaker position in new procurement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Investment In Smart FM Technologies | -1.5% | National, most acute for mid-size FM operators lacking capital for CAFM and IoT deployment | Medium term (2-4 years) |

| Shortage Of Certified Skilled FM Workforce | -1.1% | National, most severe for MEP and HVAC technical roles in Eastern Province and NEOM corridors | Short term (≤ 2 years) |

| Complex And Evolving Regulatory Compliance Requirements | -0.8% | National, with highest burden in Healthcare, Institutional, and government-linked contracts | Medium term (2-4 years) |

| Price Competition Leading To Margin Pressure | -0.5% | National, most pronounced in commodity Soft FM services such as cleaning and security | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Investment in Smart FM Technologies

The largest near-term restraint in the Saudi Arabia integrated facility management market is the capital needed to deploy smart operating systems at scale. In the 2024 Saudi FM study, 50% of professionals identified high implementation cost as the main barrier to adoption, and the challenge received an average severity score of 4.5 out of 5. CAFM platforms, IoT sensors, digital twins, and AI-based diagnostics all require spending before providers can even compete for the most advanced contracts. That creates a practical threshold because smaller operators often struggle to fund the technology stack now expected by owners of premium and technically advanced facilities. The burden rises further when providers must align digital systems with labor monitoring and energy reporting requirements across the Saudi operating environment. For that reason, the KSA integrated facility management market is becoming more difficult for undercapitalized firms to access at the top end.

Shortage of Certified Skilled FM Workforce

The Saudi Arabia integrated facility management (IFM) market also faces a clear labor constraint because asset complexity is rising faster than the supply of certified technical staff. Only 30% of FM professionals in Saudi Arabia were Saudi nationals in 2025, while localization rules now cover 269 professions and can require quotas of up to 70% for specific roles.[4]Ministry of Human Resources and Social Development, “Labor Market And Localization Framework,” MHRSD, hrsd.gov.sa The pressure is most visible in MEP, HVAC, BIM-capable engineering, and other specialized functions where training pipelines are still developing. EFSIM onboarded more than 800 professionals in H1 2025 and expanded its workforce to 8,500 employees, which shows both the intensity of labor demand and the scale of training needed to support growth. Leading operators are responding through training partnerships and internal academies, but workforce development still takes time and creates a lag between contract demand and delivery capacity. Until that gap narrows, the Saudi Arabia IFM market will continue to face execution pressure in technically demanding accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Gains Momentum as Asset Complexity Rises

Soft facility management held 63.41% of the Saudi Arabia integrated facility management market share in 2025, which reflected the labor-heavy role of cleaning, catering, security, and office support across hospitality, healthcare, aviation, and public assets. Cleaning and catering continue to drive high service volumes because expanding occupied space creates daily demand across large portfolios. Security and office support are also changing in quality terms because access control, CCTV monitoring, and visitor management software are increasingly being bundled into site contracts instead of sitting outside the service package. Other Soft FM activities, including waste management, pest control, and landscaping, are rising with the continued buildout of residential communities and mixed-use developments. ROSHN's planned communities exceed 200 million m² of residential space, which supports long-run demand for repetitive and site-based soft services across growing neighborhoods. The Saudi Arabia integrated facility management market therefore still depends on Soft FM for contract volume, workforce intensity, and broad geographic coverage.

Hard facility management in the Saudi Arabia integrated facility management market size is projected to expand at 8.29% CAGR through 2031, making it the fastest-growing service category in the forecast period. This growth is linked to the commissioning of more technically sophisticated assets that need MEP support, HVAC optimization, fire and life safety management, and asset lifecycle monitoring. Cooling systems consume a major share of power in Saudi buildings, and deployed AI-enabled HVAC optimization case studies in Riyadh towers have shown energy savings of 27-40%, which makes engineering-led service models more valuable. Fire systems and safety have also moved higher in the service mix because licensing and inspection expectations are becoming more formalized in new and refurbished assets. Asset management is gaining strategic importance as long-term contracts push more responsibility for equipment condition, replacement planning, and failure prevention onto FM providers, which is changing the technical center of the Saudi Arabia integrated facility management industry.

By End-User Industry: Industrial Scale Anchors Demand While Commercial Growth Quickens

The Industrial and Process segment accounted for 31.56% share of the Saudi Arabia integrated facility management market size in 2025, which made it the largest end-user base in the report period. This position reflects sustained demand from upstream energy sites, petrochemical facilities, logistics infrastructure, and large industrial corridors in the Eastern Province and emerging development zones. ENGIE Solutions' facility management appointment for the International Maritime Industries project in Ras Al-Khair covers 12 million sq.m., more than 500 buildings, and a workforce above 23,500, which shows the scale and integration level common in industrial contracts. Vision 2030 data showed that more than 12,000 factories were operational in the Kingdom in 2024, and NEOM's Oxagon is targeting 4,000 digitally transformed factories by 2035, both of which support future demand for safety, maintenance, utilities, and process-support services. Healthcare also adds stable underlying demand because hospitals and clinical sites need reliable cleaning, technical maintenance, compliance support, and patient-sensitive operating standards.

Commercial end users are forecast to grow at 8.12% CAGR through 2031, which makes this the fastest-expanding end-user segment in the Saudi Arabia integrated facility management (IFM) market. Private sector GDP contribution reached 47% in Q3 2024, and the increase in business registrations is widening the base of offices, mixed-use assets, retail sites, warehouses, and telecom-linked facilities that need outsourced support. Within commercial accounts, BFSI and IT and telecom users are asking for tighter digital oversight because connected building systems create new service interfaces between physical operations and security risk management. Hospitality is also scaling quickly, with 475,900 hotel rooms added through 2024 and a further pipeline connected to western tourism corridors and destination projects, which supports strong demand for Soft FM and energy-aware Hard FM services. Institutional and public infrastructure demand remains meaningful because education, transport, airports, rail, and government facilities continue to add complex assets that need integrated operations across broad service scopes, which keeps the Saudi Arabia integrated facility management industry balanced between stable public demand and faster-growing private demand.

Geography Analysis

Riyadh remains the largest operating center in the Saudi Arabia integrated facility management market because it combines the country's deepest concentration of government assets, corporate offices, commercial districts, and large entertainment developments. The city continues to add managed space through projects such as King Salman Park, Sports Boulevard, and Diriyah Gate, each of which increases the need for integrated site operations and lifecycle support. Riyadh also benefits from the Regional Headquarters program, under which 517 international companies had established offices in the capital by 2024, reinforcing demand for corporate FM services such as office support, energy management, access control, and workplace operations. This concentration makes Riyadh the most important contract cluster for providers that want a strong presence in premium commercial and public sector portfolios. It also gives leading operators a base from which to scale into surrounding regions and multi-city accounts.

The Western Region is the fastest-rising geographic cluster in the Saudi Arabia integrated facility management (IFM) market because tourism, hospitality, and destination-led infrastructure are expanding rapidly from Jeddah and Makkah toward Red Sea developments and new resort corridors. Tourism investment reached USD 3.95 billion through Q3 2024, and international tourist arrivals stood at 29.7 million in 2024, which confirms the speed at which new visitor-facing assets are being added. Red Sea Global has already opened 5 resorts and developed the region's first carbon-neutral airport, which means FM contracts in this cluster are closely tied to premium guest service and sustainability outcomes. These projects demand more than routine maintenance because operators are expected to manage energy, waste, housekeeping, transport support, and environmental performance in a single service environment. That mix gives the Western Region a distinct profile within the KSA IFM market.

The Eastern Province remains the most technically demanding region in the Saudi Arabia IFM market because it is anchored by oil and gas infrastructure, petrochemical operations, industrial cities, and specialized maritime assets. Hard FM carries greater weight here because industrial users place high value on asset reliability, utilities performance, process safety support, and preventive maintenance. The International Maritime Industries development in Ras Al-Khair reflects this pattern, with ENGIE Solutions managing a wide operating scope across industrial, residential, and workforce-linked infrastructure. Regulatory oversight also tends to feel stricter in this region because the criticality of industrial assets leaves less room for service failure, documentation gaps, or delayed maintenance cycles. As a result, the Eastern Province acts as a proving ground for the higher-end technical capabilities that increasingly define the KSA integrated facility management market.

Competitive Landscape

The Saudi Arabia integrated facility management market shows a moderately fragmented structure at the broad level, but competition is tightening around providers that can deliver integrated, measurable, and technology-supported contracts across large portfolios. Saudi national operators such as Initial Saudi Group, AlMajal AlArabi Group, Musanadah Facilities Management, and Zamil Operations and Maintenance compete from a position of local reach, government familiarity, and compliance with localization expectations. International firms including CBRE, JLL, Sodexo, ENGIE Solutions, and ISS compete in engineering depth, digital systems, and the ability to standardize service delivery across demanding client environments. This has created a two-tier pattern in the Saudi Arabia integrated facility management market where scale alone is no longer enough, and contract wins increasingly depend on documented outcomes. Providers that can combine CAFM, IoT-based monitoring, sustainability reporting, and strong mobilization capability are better placed to move up the value chain.

Several strategic moves show how companies are repositioning inside the Saudi Arabia integrated facility management market. JLL appointed a dedicated Head of Property and Facilities Management Consultancy for MENA in March 2025, which signaled stronger focus on advisory-led FM relationships and AI-enabled service optimization in the region. Shalfa Facilities Management signed a SAR 52.1 million (USD 14.07 million) contract in January 2026 with the National Water Company for integrated FM services in the Southern Sector, which shows that local listed players are expanding through government-linked accounts. EFSIM also secured more than SAR 750 million USD 202.5 million) in H1 2025 contract awards across infrastructure, healthcare, education, government services, hospitality, and sports, showing that digitally capable regional providers are winning broader and more diversified portfolios. These moves reinforce that contract depth, financing capacity, and delivery systems matter more than a basic labor model.

White-space opportunities remain visible in healthcare, education, platform-led service delivery, and sustainability-linked FM packages. Healthcare and education demand is already meaningful, yet both segments still offer room for deeper outsourcing and more performance-based integrated contracts across technical and soft service scopes. Smaller operators may also find space in platform-led models where they provide managed CAFM or specialist energy services without matching the full capital base of the largest integrators. Sustainability-linked delivery is another opening because clients increasingly want support that combines compliance, energy performance, and operational reporting in one service arrangement. The Saudi Arabia integrated facility management market is therefore not closed to new growth, but the strongest opportunities now sit in capability-led niches rather than in undifferentiated labor supply.

Saudi Arabia Integrated Facility Management Industry Leaders

Initial Saudi Group

Muheel Services

Almajal G4S

ENGIE Solutions

Zamil Operations and Maintenance Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nemetschek Group signed a strategic MoU with the Saudi Facility Management Association (SFMA) to accelerate smart and sustainable integrated facility management across Saudi Arabia. The partnership focuses on digital twins, AI-driven operations, workforce development, and data-enabled FM delivery aligned with Vision 2030. The agreement highlights how Saudi Arabia’s IFM market is increasingly shifting toward technology-led, lifecycle-based service models and digitally integrated asset management.

- November 2025: Shalfa Facilities Management signed a SAR 52.1 million (USD 13.9 million), 36-month contract with the National Water Company to provide integrated FM services for NWC buildings in Saudi Arabia's Southern Sector, with financial impact expected in H2 2026.

- December 2025: JLL and the Public Investment Fund (PIF) announced that JLL acquired a significant stake in FMTECH, a national integrated facilities management company launched by PIF in 2023. The transaction strengthened Saudi Arabia’s IFM sector by combining JLL’s digital FM platforms and operational expertise with FMTECH’s local delivery scale, supporting technology-enabled, long-term integrated service models aligned with Vision 2030.

- August 2025: EFSIM secured over SAR 750 million (USD 200 million) in new contract awards during H1 2025 across infrastructure, healthcare, education, government services, hospitality, and sports sectors, onboarding 800+ professionals and expanding operations into the Southern region of Saudi Arabia.

Saudi Arabia Integrated Facility Management Market Report Scope

The Saudi Arabia Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of Saudi Arabia integrated facility management demand?

The Saudi Arabia integrated facility management market size stood at USD 4.41 billion in 2025 and is estimated at USD 5.33 billion in 2026, with projected value reaching USD 7.58 billion by 2031.

What is driving growth in Saudi Arabia facility management services?

Growth is being supported by Vision 2030 projects, rising outsourcing of complex building operations, stronger energy compliance needs, and wider use of predictive maintenance tools.

Which service type leads demand in Saudi Arabia?

Soft facility management led in 2025 with 63.41% revenue share because cleaning, catering, security, and workplace support remain essential across hospitality, healthcare, and public assets.

Which service type is growing the fastest through 2031?

Hard facility management is forecast to grow at 8.29% CAGR through 2031 as technically advanced assets require stronger MEP, HVAC, fire safety, and lifecycle asset management support.

Which end-user group contributes the most revenue?

The Industrial and Process Sector held the largest share at 31.56% in 2025, supported by upstream energy facilities, industrial corridors, and large maritime and manufacturing assets.

Where are the strongest geographic opportunities located?

Riyadh remains the largest contract center, the Western Region is the fastest-rising tourism and hospitality cluster, and the Eastern Province offers the most technically demanding industrial opportunities.

Page last updated on: