South America Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

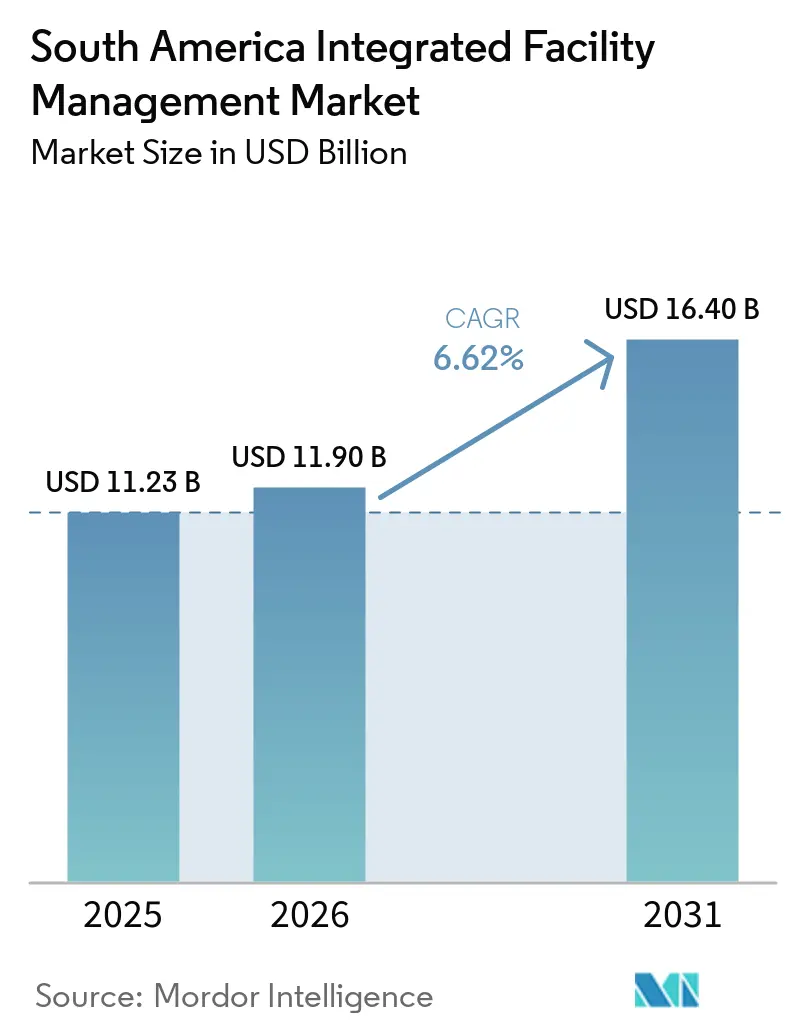

| Base Year Market Size (2025) | USD 11.23 Billion |

| Market Size (2026) | USD 11.90 Billion |

| Market Size (2031) | USD 16.40 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Integrated Facility Management Market Analysis by Mordor Intelligence

The South America integrated facility management market size was valued at USD 11.23 billion in 2025 and estimated to grow from USD 11.90 billion in 2026 to reach USD 16.40 billion by 2031, at a CAGR of 6.62% during the forecast period 2026-2031. The South America integrated facility management market (IFM) is moving away from fragmented single-service outsourcing and toward unified contracts that combine hard and soft services under one operating model. That shift is still uneven across the region, which leaves substantial room for expansion outside tier-1 cities where outsourcing penetration remains low and service delivery is still handled by multiple local vendors. Demand is being shaped more by industrial corridors, mining assets, logistics sites, and energy campuses than by traditional office portfolios alone, which gives the South America (SA) integrated facility management (IFM) market a different operating profile from more mature regions. Competitive success in 2026 depends less on service breadth alone and more on digital depth, especially in IoT dashboards, CMMS integration, predictive maintenance workflows, and remote asset visibility. Currency instability and the shortage of technicians who can manage both plant systems and digital platforms continue to slow adoption, but those same conditions favor providers that can scale modular and remotely managed delivery models.

Key Report Takeaways

- By service type, soft facility management services (soft FM) led with 64.21% share of the South America integrated facility management market in 2025, while hard facility management (hard FM) is projected to record the fastest growth at a CAGR of 7.43% through 2031.

- By end user, the industrial and process sector held the largest share at 32.34% of the South America IFM market in 2025, while the commercial segment is expected to expand at a CAGR of 6.91% during 2026-2031.

- By geography, Brazil accounted for 40.45% of regional demand of the South America integrated facility management market in 2025, while Argentina is forecast to register the highest CAGR at 7.60% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Smart-Building Platforms | +1.6% | Brazil, Chile, Argentina, especially tier-1 cities | Short term (≤ 2 years) |

| Growing Emphasis on Energy-Efficient Facilities | +1.3% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Post-Pandemic Hybrid Work Models Demanding Flexible IFM | +1.0% | Brazil, especially São Paulo and Rio de Janeiro, and Chile, especially Santiago and Valparaíso | Short term (≤ 2 years) |

| Rising Private-Equity Investments in FM Service Vendors | +0.8% | Brazil, with spillover into Argentina and Chile | Medium term (2-4 years) |

| Accelerated Digital Twin Deployments for Asset Optimization | +0.6% | Brazil, especially São Paulo data centers, and Chile, especially energy assets | Long term (≥ 4 years) |

| Government-Backed Infrastructure Modernization Programs | +0.5% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption Of Smart-Building Platforms

Smart-building adoption remains the strongest near-term demand trigger for integrated contracts because operators are increasingly connecting occupancy, HVAC, lighting, and access systems to daily service delivery decisions rather than relying on fixed maintenance calendars. Brazil’s EPE reported that HVAC and lighting represented a significant portion of electricity consumption in commercial and public buildings, which gives owners a clear cost reason to connect building systems with performance-led FM models. Aureside also reported that a substantial number of new commercial constructions in Brazil already include some level of automation, which means the installed base available for platform-linked IFM contracts is expanding even before retrofit demand is considered. The larger opportunity still sits in older commercial stock, where legacy point solutions need replacement or integration before a true single management layer becomes practical, and that backlog supports a multi-year contract pipeline for the SA integrated facility management market. Technical standards and energy-labeling programs in Brazil are also pushing owners toward more structured building management approaches, which broadens the service scope for providers that can manage MEP systems and digital controls together. Providers that already operate with integrated dashboards and remote visibility tools are therefore in a better position to convert automation spending into long-term recurring contracts across the South America IFM market.

Growing Emphasis On Energy-Efficient Facilities

Energy efficiency is no longer being treated only as a sustainability objective, because clients are now placing consumption targets, monitoring routines, and operating penalties directly into service agreements. The IEA stated in 2025 that building sensors and monitoring software can reduce commercial energy consumption by up to 30%, which gives procurement teams a concrete basis for using integrated FM contracts to justify technology spending.[1]International Energy Agency, “Buildings - Tracking Clean Energy Progress,” IEA, iea.org That change matters in South America because energy performance had often remained outside the core scope of outsourced facility services, especially in lease structures where owners and occupiers split responsibility. As those responsibilities move into the service contract, FM providers can add measurable value without owning the asset itself, and that is expanding the commercial case for the South America integrated facility management market. GBC Brasil also noted that ESG metrics and technical standards such as ABNT and ASHRAE are becoming part of day-to-day facilities governance, which raises the need for credentialed vendors that can manage energy, indoor environment, and compliance outcomes in one operating structure. The result is a steadier shift from labor-led contracts toward contracts where energy performance becomes part of the value proposition in the South America integrated facility management market.

Post-Pandemic Hybrid Work Models Demanding Flexible IFM

Hybrid work is changing how corporate facilities are used in the region, and that is forcing service delivery to align with actual occupancy rather than fixed staffing assumptions. Cleaning, catering, meeting support, access control, and environmental monitoring now need to respond to uneven demand across days and locations, which makes static service models less efficient than they were before. DeskFlex entered Brazil in March 2026 and described a local base of approximately 201,000 corporate offices where many organizations still lacked workplace tools for managing hybrid operations, which shows how much digital workplace infrastructure remains to be deployed.[2]DeskFlex, “Accessible Workplace Management Software DeskFlex Launches in Brazil, Expands into LATAM,” DeskFlex, deskflex.com For FM providers, this shift does not simply reduce service demand, because it also creates a higher-value layer around occupancy analytics, flexible scheduling, smart booking, and service orchestration. The commercial segment therefore becomes more attractive when providers can connect workplace software with on-site execution rather than treating office support as a stand-alone labor contract. This is one reason the South America integrated facility management market is beginning to separate digitally capable vendors from providers that still depend on headcount-led pricing and fixed routines.

Rising Private-Equity Investments in FM Service Vendors

Private-equity funding is helping change market structure by giving mid-tier providers access to technology, acquisition capital, and broader service capabilities more quickly than organic growth would allow. The IFC and GPCA announced a USD 125 million commitment to Advent LatAm Private Equity Fund VIII in late 2025, targeting sectors that overlap with outsourced services and operational infrastructure across the region.[3]Global Private Capital Association and International Finance Corporation, “IFC to Invest USD125m in Advent LatAm PE Fund VIII and Co-Investment Vehicle,” GPCA, globalprivatecapital.org In Brazil, Grupo GPS completed 3 acquisitions in 2025, raised its employee base to more than 185,000, and delivered 17% year-over-year revenue growth in FY2025, which shows how capital-backed scaling is already reshaping competitive capability in the sector.[4]Grupo GPS Participações e Empreendimentos S.A., “Earnings Release 4Q25,” Grupo GPS, api.mziq.com The effect is larger than added scale alone, because newly capitalized operators can fund enterprise CMMS tools, sensor layers, reporting systems, and specialized teams that previously sat outside their reach. That closes part of the historical technology gap between local operators and multinational firms, and it raises the minimum performance level expected by large clients across the South America IFM market. Providers that remain outside the consolidation cycle face a higher risk of losing anchor contracts to better-funded rivals that can bundle technology, compliance, and multi-site delivery at more competitive prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Multidisciplinary Technicians | -0.8% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Fragmented Local Vendor Landscape Limiting Standardization | -0.6% | Regional, with concentration in Brazil and the rest of South America | Long term (≥ 4 years) |

| Currency Volatility Inflating Service Contract Costs | -0.5% | Argentina most acute, Brazil moderate, Chile limited | Short term (≤ 2 years) |

| Low End-User Awareness Outside Tier-1 Cities | -0.3% | Rest of South America, plus secondary cities in Brazil and Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Skilled Multidisciplinary Technicians

The regional labor constraint is not simply a shortage of maintenance workers, because the real gap lies in technicians who can handle MEP systems, digital controls, monitoring tools, and compliance requirements in the same role. GBC Brasil stated in February 2026 that the facility manager role had shifted from reactive operations toward data-led strategic governance, and it linked that change to rising use of ABNT, ASHRAE, and CRI-204 standards in daily practice. That shift increases the training burden for providers because clients now expect technical staff to interpret building data, support audits, and manage performance systems rather than only execute physical maintenance tasks. The problem is more acute outside the largest urban centers, where the available labor pool is smaller and recruitment for multi-site contracts takes longer. This slows the rollout of integrated models in secondary markets and raises the cost of ramping complex accounts even when demand is present. In practice, the talent gap gives a structural advantage to vendors that can combine centralized expertise, remote support, and field execution in one delivery model.

Fragmented Local Vendor Landscape Limiting Standardization

The regional vendor base remains highly fragmented, which makes it harder for large occupiers and asset owners to secure consistent service quality across multiple countries or states. In 2025, JLL completed a multi-country facilities integration program for Schneider Electric across 6 South American countries, and the project stood out precisely because it brought unified processes, Corrigo software, and real-time performance dashboards into an operating environment that is usually managed through separate local arrangements. Domestic operators often maintain strong local relationships, but many still lack the capital, systems, or technical depth needed to support genuinely integrated cross-border portfolios at enterprise scale. The result is that clients in São Paulo, Buenos Aires, Santiago, and secondary cities may still rely on different vendors for cleaning, maintenance, catering, and workplace support even when they prefer one reporting line. That weakens the core value proposition of integrated FM, because cost pooling, SLA consistency, and data transparency are harder to achieve when delivery remains split across multiple contractors. The SA integrated facility management market will continue to face this restraint until consolidation, platform adoption, and multi-country operating discipline advance more evenly across the supplier base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Holds The Volume Base While Hard FM Gains From Technical Demand

Soft Facility Management services held 64.21% of the South America integrated facility management market share in 2025, which confirms that cleaning, catering, office support, and security remained the main outsourcing entry points for most client organizations. Cleaning services continue to form the broadest adoption base because they are easier to contract out than highly technical functions, especially for small and medium-sized firms taking their first step away from in-house operations. That gives soft FM a large installed base across industrial parks, commercial buildings, hospitals, and education sites, particularly in Brazil where outsourcing has matured further than in many neighboring countries. The category also benefits from its direct link to day-to-day occupancy, employee experience, and site presentation, which keeps renewal rates relatively resilient even when budgets tighten. For that reason, soft FM still anchors the operating scale of the South America integrated facility management market even as clients become more selective about service design.

The soft facility management mix is also changing in ways that matter for the South America IFM industry, because clients increasingly expect flexible staffing, usage-based scheduling, and digitally supported service visibility rather than fixed routines alone. Demand-led cleaning and attendance-linked workplace support are becoming more relevant in offices and mixed-use sites where occupancy changes materially by day and by zone. Catering is evolving as well, with Sodexo Brazil expanding autonomous micromarket formats across corporate, hospital, school, and factory environments in 2025, which shows how food-related services are moving toward convenience-led models that fit hybrid work and extended shift operations. Security and office support are following a similar path, where clients want better control, reporting, and adaptability across multiple locations. This means soft FM is likely to remain the largest service layer in the South America integrated facility management market, even though its growth profile is increasingly shaped by technology and contract design rather than labor scale alone.

Hard Facility Management is projected to expand at a CAGR of 7.43% through 2031, making it the fastest-growing part of the SA integrated facility management market size as clients spend more on asset uptime, compliance, and technical reliability. MEP and HVAC services sit at the center of that demand because downtime in healthcare facilities, data centers, industrial sites, and mining assets carries direct operating and safety consequences. Fire systems and safety compliance are also becoming more visible in procurement, and the 2025 edition updates to NFPA 72 are being referenced as a performance benchmark by engineers and multinational occupiers that expect common standards across geographies. That matters in South America because many international tenants want the same maintenance discipline from regional service providers that they require in North America or Europe. As a result, hard FM proposals that combine engineering depth, compliance capability, and monitoring tools are gaining more weight in competitive bids.

The hard FM opportunity is widening further because asset management is moving beyond preventive maintenance into longer-term planning supported by software and remote data. Telefónica is deploying AI-powered digital twins for cooling optimization at its São Paulo data centers and estimated potential energy reductions of 15% to 20%, which gives a practical example of how technical FM is moving into continuous optimization rather than reactive repair. Leadec also reported strong performance in the Americas in FY2025 and highlighted Green Factory Solutions revenue of EUR 140 million (USD 158 million) from energy management, battery storage, photovoltaic, and smart factory maintenance activities that align closely with hard FM demand. These examples show that the South America integrated facility management industry is assigning greater value to technical service lines that improve reliability, energy use, and life-cycle outcomes. Hard FM therefore has the strongest forward momentum even though soft FM continues to hold the larger revenue base in the South America integrated facility management market.

By End User: Industrial and Process Assets Lead Current Demand While Commercial Sites Show The Fastest Growth

The industrial and process sector held 32.34% of regional demand in 2025, making it the largest end-user group in the South America integrated facility management market because large manufacturing, mining, logistics, and processing assets require broader technical and support coverage than most office sites. These contracts tend to carry higher value per site because they combine maintenance, cleaning, compliance, catering, safety support, and utilities management under stricter uptime expectations. Brazil remains central to that demand because its industrial footprint, mining activity, and multinational operating presence create a deeper base for structured outsourced services than most other countries in the region. Leadec reported outstanding Americas performance in FY2025 and pointed directly to Brazil as a strong contributor, with its Green Factory Solutions business showing how industrial clients are tying facility services to energy, storage, and smart production goals. The industrial and process segment therefore continues to provide the most stable revenue foundation for providers that operate across the South America integrated facility management market.

Mining is especially important within this end-user base because remote locations, labor logistics, food services, accommodation support, and technical maintenance all need to be coordinated within a single operating framework. Sodexo resumed full operations at Antamina in Peru in February 2026 under a contract serving approximately 6,500 daily users across 2 remote camps, which highlights how large mining sites can function as integrated service ecosystems rather than simple maintenance accounts. That kind of scope suits providers with strong hard FM depth and large-scale soft FM capabilities, which is why industrial and extractive environments remain key gateways for multinational operators entering the region. The South America integrated facility management industry also benefits from the fact that industrial clients usually have more mature procurement standards and clearer performance expectations than smaller commercial occupiers. That maturity supports longer contracts, deeper technical scope, and wider adoption of digitally enabled operating models.

The commercial segment is forecast to grow at a CAGR of 6.91% through 2031, making it the fastest-expanding end-user category in the South America integrated facility management market as offices shift toward hybrid occupancy and flexible workplace operations. Demand in this segment is moving away from fixed labor allocation and toward occupancy-linked cleaning, desk booking support, access control, air-quality monitoring, and service scheduling that can change by building and by day. DeskFlex described Brazil as a market with approximately 201,000 corporate offices when it launched locally in 2026, which underlines how much office infrastructure remains open to software-enabled service coordination. That transition expands the role of FM vendors that can connect workplace platforms with operational response on-site. It also makes the commercial segment more attractive to firms with digital capability even when total floor space usage becomes less predictable.

Healthcare, hospitality, and public infrastructure are adding to that momentum by widening the addressable client base beyond standard office portfolios. Cushman and Wakefield stated in late 2025 that it had expanded actively into hospital and data center facilities in Brazil, and by early 2026 it launched a Virtual Technician Program that used wearable technology to support audits, thermographic inspections, and maintenance from centralized specialists. Hospitality is also recovering as tourism and event activity normalize, which supports service demand in resort, convention, and mixed-use assets. Public infrastructure is becoming more relevant as transport, water, health, and civic assets move from construction into operations, even though the pace differs by country and procurement structure. Together, these trends broaden the customer mix of the South America integrated facility management market and reduce dependence on any single end-user profile.

Geography Analysis

Brazil held 40.45% of regional demand in 2025, which gave it the largest position in the South America integrated facility management market share because it combines the region’s deepest industrial base, the densest stock of grade-A commercial assets, and the highest outsourcing maturity. São Paulo remains the center of that demand, but the national opportunity extends across healthcare, agribusiness, energy, logistics, and technology facilities where large occupiers expect more structured service delivery. JLL completed a South America-wide facilities integration project for Schneider Electric in 2025, while Cushman and Wakefield and Grupo GPS also expanded their operational reach across more specialized client environments in Brazil during the same period. Sustainability frameworks also carry more weight in Brazil than in most neighboring markets, and GBC Brasil noted in 2026 that ESG metrics and technical standards had become part of the operating baseline for facility leadership. That combination of scale, client maturity, and technology adoption keeps Brazil as the anchor geography of the South America integrated facility management market.

Argentina is expected to record the fastest expansion at a CAGR of 7.60% through 2031, which makes it the most dynamic national opportunity within the South America integrated facility management market size despite a difficult macroeconomic backdrop. The growth case rests on a large base of commercial and industrial assets where formal outsourcing penetration is still low, which leaves room for providers to convert fragmented service arrangements into integrated contracts. Buenos Aires Province announced a 2026-2027 infrastructure plan worth ARS 1.91 trillion (USD 1.29 billion} across 20 priority projects in water, roads, and energy, and that creates a clearer pipeline for public-asset operations over the near term. Mercado Libre also announced a USD 115 million logistics center in Escobar in 2026 with capacity to process up to 130,000 products daily, which shows how private investment is expanding the asset base that needs structured facility services. Currency instability remains the main operational risk because multi-year local-currency contracts can erode provider margins, but the underlying outsourcing runway still supports faster growth than in several larger but more mature sub-markets.

Chile represents the most formalized IFM sub-market after Brazil, and its opportunity is shaped by stronger regulatory enforcement, mining demand, and a public-asset pipeline that favors technically structured service models. Chile’s Ministry of Public Works presented a 30-year National Infrastructure Plan in 2025 with more than 22,662 projects worth USD 357 billion, while the 2026 roadworks budget added near-term visibility for public-asset management demand. The incoming administration also prioritized USD 28 billion in infrastructure projects for 2026-2030, including hospital and highway assets that are likely to require more organized FM support once operational. The rest of South America, especially Peru, Colombia, and Ecuador, remains a more mixed opportunity set, but contract wins such as Sodexo’s Antamina engagement in Peru show that resource-sector and remote-site demand can still provide meaningful entry points for the South America integrated facility management market.

Competitive Landscape

The South America integrated facility management market remains moderately fragmented, with large multinational firms competing for institutional and multinational accounts while domestic groups maintain strong positions in Brazil’s mid-market, industrial, and energy-linked portfolios. ISS A/S, Sodexo S.A., Compass Group PLC, CBRE Group Inc., and Jones Lang LaSalle Inc. continue to hold an advantage in global account management, reporting systems, and standardized operating frameworks across multiple countries. Domestic providers such as Grupo GPS, Grupo Verzani and Sandrini S/A, Manserv Facilities, Brasanitas Serviços Integrados, and Engie’s Brazil operations remain important because they combine local labor reach with practical knowledge of contract execution in complex site environments. This balance keeps competition active across both large and mid-sized accounts, especially where clients need national coverage but not always full cross-border integration. It also means the South America integrated facility management market continues to reward vendors that can localize delivery without losing control of process, compliance, and reporting.

Technology has become the clearest point of separation among leading providers in 2026 because contract decisions increasingly depend on visibility, response speed, and performance data rather than labor scale alone. Cushman and Wakefield launched its Virtual Technician Program in Brazil in February 2026, using wearable devices to connect field staff with remote specialists during audits, inspections, and maintenance work across hospitals, data centers, and distributed sites. Leadec reported that its Leadec.os platform was supporting more than 2,400 daily users across 16 countries, which gives it a stronger base for IIoT-enabled service optimization in industrial environments, including Brazil. JLL’s Schneider Electric engagement across 6 South American countries also showed how clients are placing value on common software, unified workflows, and real-time dashboards when they want regional consistency. New software-led entrants such as DeskFlex add another pressure point because workplace technology providers can become strategic partners to local operators and change how value is captured in the South America IFM market.

Capital-backed expansion is also raising the competitive threshold because acquisition-driven growth now gives local operators faster access to adjacent services and operational scale. Grupo GPS completed multiple acquisitions in 2025 and entered 2026 with more than 185,000 employees, which strengthened its position across occupational health, retail support, and labor-linked services around its facilities base. Sodexo also signaled in 2026 that M&A would be a core growth route in Brazil, which reinforces the view that scale and consolidation will remain active themes in the region. At the same time, ISS extended a major global IFM relationship in 2026 that included cleaning, catering, technical, engineering, and workplace services, showing that multinational account structures continue to support broader regional delivery models. The competitive picture therefore remains open, but the firms most likely to gain share are those that combine digital operating depth, multi-site execution discipline, and enough capital to keep closing capability gaps.

South America Integrated Facility Management Industry Leaders

ISS A/S

Sodexo S.A.

Compass Group PLC

ABM Industries Inc.

CBRE Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ISS A/S extended a global IFM contract with a large multinational client at an annual value exceeding DKK 700 million (USD 100 million) for a 2-year period effective from Q3 2027, covering cleaning, catering, technical and building maintenance, engineering, and workplace experience services globally, including South America operations.

- February 2026: Cushman and Wakefield launched its Virtual Technician Program in Brazil, deploying wearable-device technology to connect field technicians with remote specialists in real time for FM audits, thermographic inspections, and maintenance at data centers, hospitals, and multi-site operations. The company's FM business in Brazil had grown approximately 70% in the 2-year period preceding the launch.

- February 2026: Sodexo resumed full operations at Antamina, one of South America's largest mining complexes in Peru, under a new food, hospitality, and recreational facilities management contract serving approximately 6,500 daily users across 2 remote camps, requiring recruitment of approximately 1,100 employees from local communities.

- January 2026: Buenos Aires Province unveiled its 2026-2027 infrastructure investment plan covering ARS 1.91 trillion (USD 1.29 billion) across 20 priority projects in water supply, roads, and energy, substantially expanding the addressable market for public-sector IFM across Argentina's largest provincial infrastructure portfolio.

- January 2026: Grupo Verzani and Sandrini announced continued geographic expansion across 24 Brazilian states and the Federal District, maintaining a workforce of 71,000+ employees and serving more than 1,400 clients, with plans for continuous investment in digital technology and team specialization.

South America Integrated Facility Management Market Report Scope

The South America Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels),Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)), and Geography (Brazil, Argentina, Chile, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial (BFSI, IT and telecom, retail and warehouses) |

| Hospitality (eateries, restaurants and large-scale hotels) |

| Institutional and Public Infrastructure (government, education, airports, railways) |

| Healthcare (public and private facilities) |

| Industrial and Process Sector (manufacturing, energy, mining) |

| Other End-User Industries (multi-house residential, entertainment, sports and leisure) |

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial (BFSI, IT and telecom, retail and warehouses) | |

| Hospitality (eateries, restaurants and large-scale hotels) | ||

| Institutional and Public Infrastructure (government, education, airports, railways) | ||

| Healthcare (public and private facilities) | ||

| Industrial and Process Sector (manufacturing, energy, mining) | ||

| Other End-User Industries (multi-house residential, entertainment, sports and leisure) | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size outlook for the South America integrated facility management market?

The South America integrated facility management market was valued at USD 11.23 billion in 2025, reached USD 11.90 billion in 2026, and is forecast to reach USD 16.40 billion by 2031 at a CAGR of 6.62%.

Which service category leads demand in South America integrated facility management?

Soft FM led with 64.21% share in 2025 because cleaning, catering, office support, and security still form the first outsourcing step for many organizations.

Which service category is growing the fastest in South America integrated facility management?

Hard FM is projected to grow at a CAGR of 7.43% through 2031 as clients place more weight on MEP reliability, HVAC performance, safety systems, and technical compliance.

Which end-user group creates the largest revenue opportunity in the region?

The industrial and process sector led with 32.34% share in 2025, supported by manufacturing, mining, logistics, and remote-site operations that require broader integrated service coverage.

Which country offers the strongest near-term growth opportunity?

Argentina is expected to post the fastest CAGR at 7.60% through 2031 because outsourcing penetration is still low and new logistics and infrastructure assets are expanding the service base.

What is shaping competition among IFM providers in South America?

Competition is being shaped by digital platform depth, remote technical support, multi-site execution, and acquisition-led capability expansion rather than service breadth alone.

Page last updated on: