Australia Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2024 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

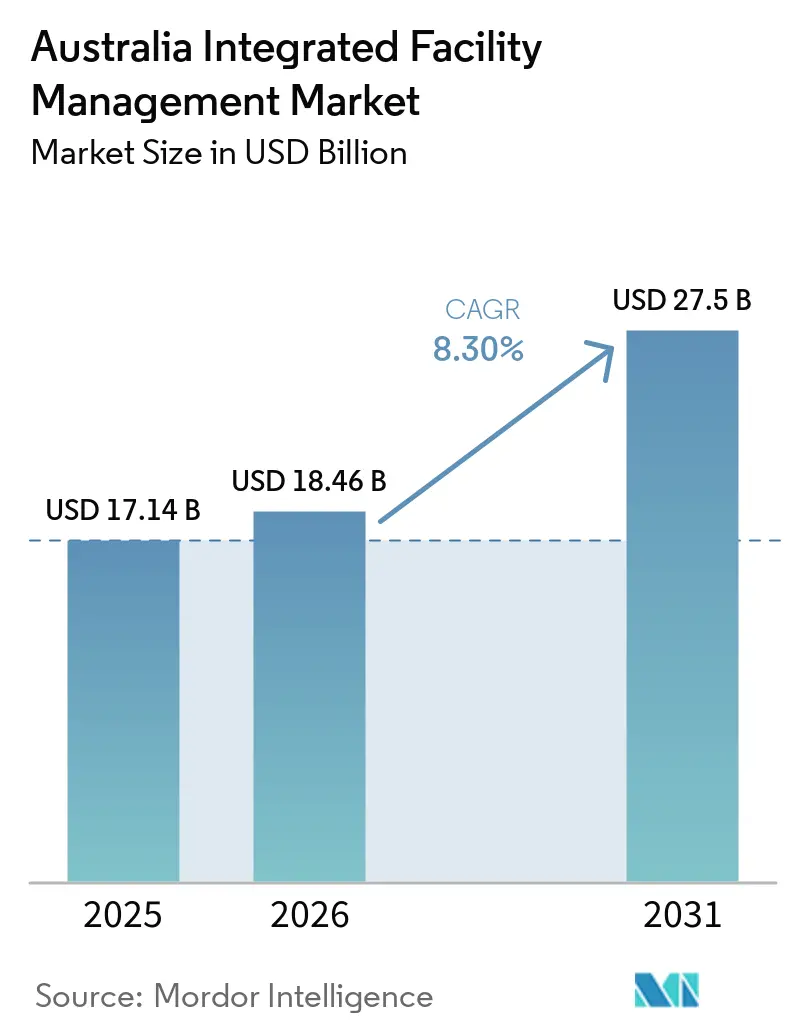

| Base Year Market Size (2025) | USD 17.14 Billion |

| Market Size (2026) | USD 18.46 Billion |

| Market Size (2031) | USD 27.5 Billion |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

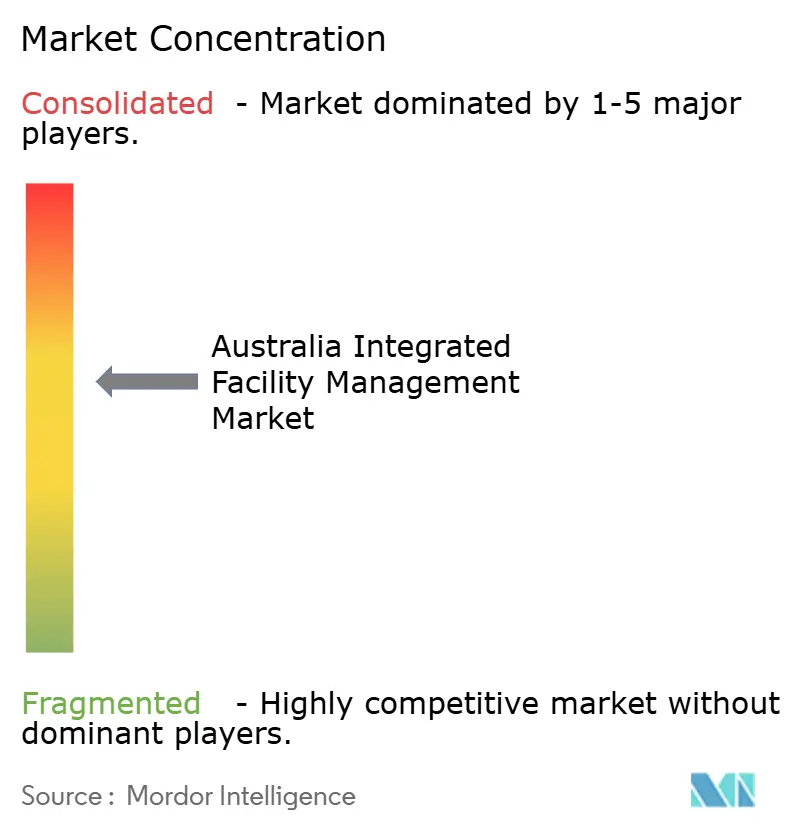

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Integrated Facility Management Market Analysis by Mordor Intelligence

The Australia Integrated Facility Management Market size was valued at USD 17.14 billion in 2025 and is estimated to grow from USD 18.46 billion in 2026 to reach USD 27.5 billion by 2031, at a CAGR of 8.30% during the forecast period (2026-2031).

The Australia integrated facility management (IFM) market is being lifted by a clear shift away from reactive maintenance and toward lifecycle asset stewardship, as owners now want one provider that can manage compliance, energy performance, and decarbonization tasks together. Mandatory climate reporting for large Australian entities from 2025 has shortened outsourcing decisions because property owners need operating partners that can support Scope 1 and Scope 2 management alongside routine building services. Public-private partnership awards are also adding larger and more complex portfolios that favor integrated delivery over fragmented subcontracting. Australia IFM market remains moderately concentrated, with global operators holding many government and institutional contracts while domestic specialists and PropTech-led challengers compete through speed, flexibility, and technology use. Skills shortages among MEP technicians and trade workers, together with a fragmented supplier base, are still pressuring margins, which is why digital maintenance tools, workforce augmentation, and vendor consolidation are becoming more important across the forecast period.

Key Report Takeaways

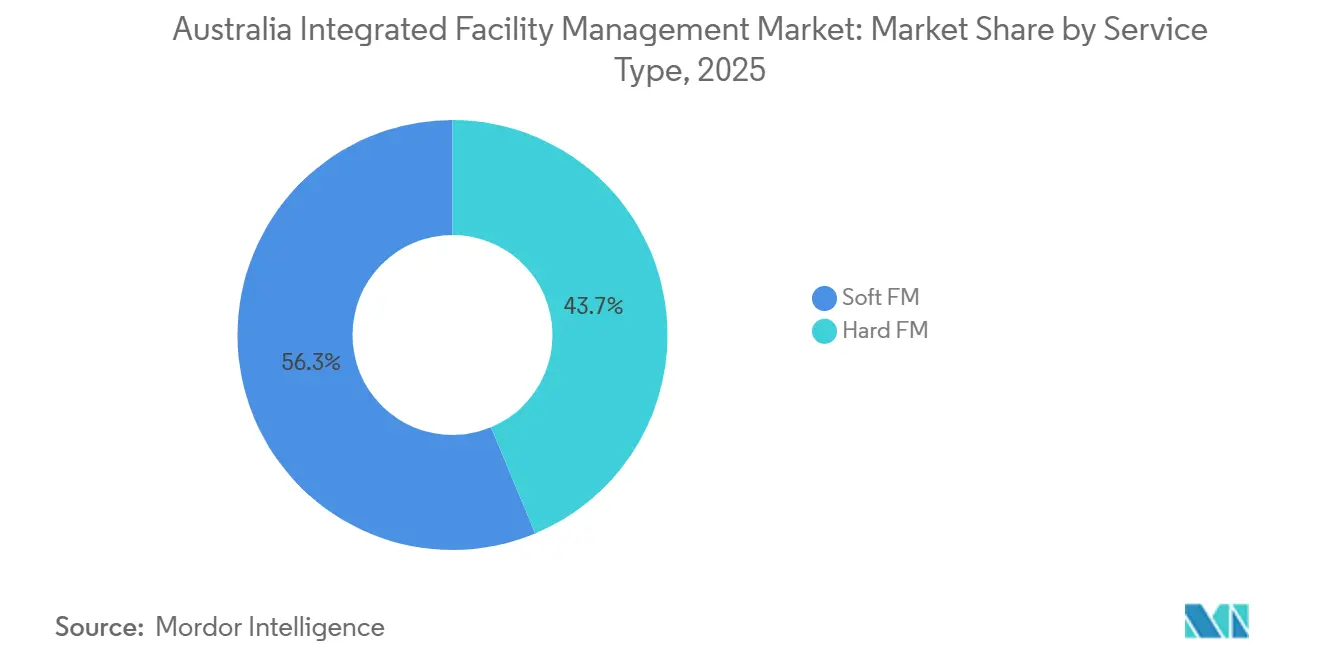

- By Service Type, Soft Facility Management accounted for 56.29% share of Australia Integrated Facility Management market size in 2025, while Hard Facility Management is projected to expand at an 8.24% CAGR through 2031.

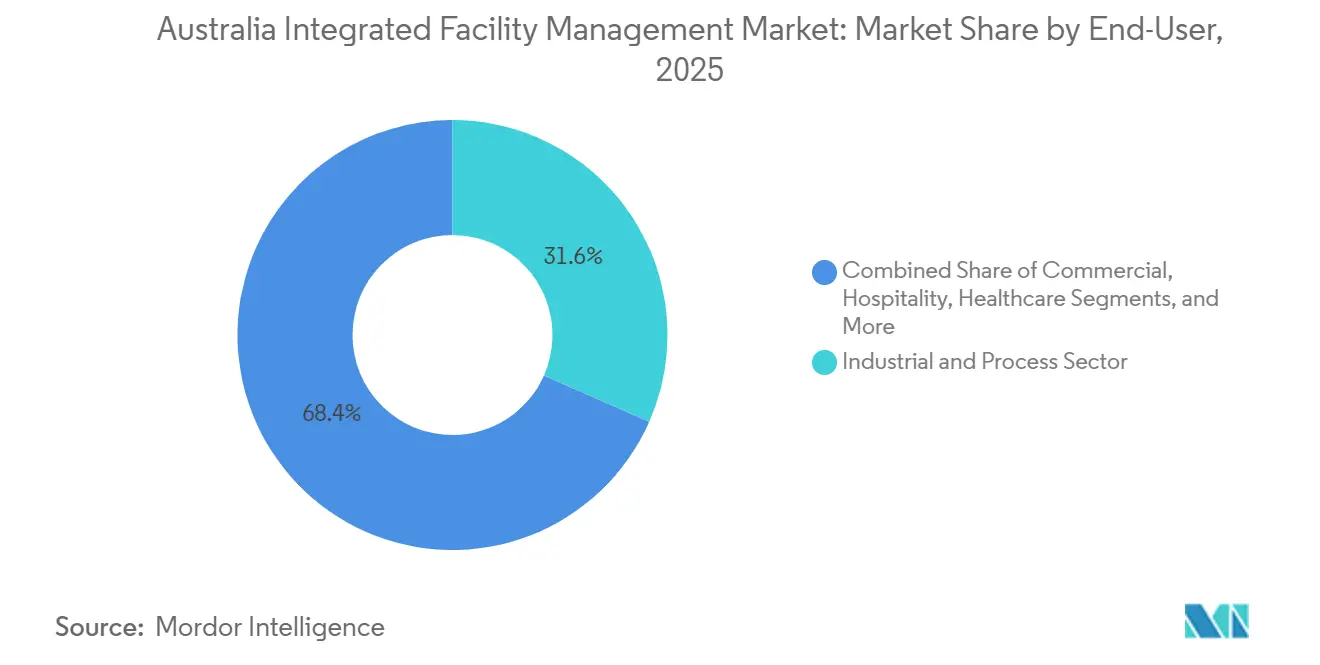

- By End-User, the Industrial and Process Sector held 31.62% of the Australia integrated facility management (IFM) market share in 2025, while Commercial end-users are forecast to grow at an 8.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Green-Building Certifications in Corporate Real Estate | +2.0% | National, concentrated gains in Sydney, Melbourne, Brisbane CBDs | Short term (≤2 years) |

| Government Mandates for Energy-Efficient Public Infrastructure | +1.8% | National, early gains in ACT, NSW, and Victoria | Short term (≤2 years) |

| Expansion of Data Centers Requiring Specialized IFM | +1.5% | National, concentrated in NSW and Victoria | Medium term (2-4 years) |

| Labor Shortage Driving Outsourcing of Non-Core Functions | +1.2% | National, more pronounced in regional and remote areas | Short term (≤2 years) |

| Rise of PropTech and IoT-Enabled Predictive Maintenance | +0.9% | National | Medium term (2-4 years) |

| Corporate Net-Zero Carbon Commitments by 2030 | +0.7% | National, early adoption in major corporate and financial hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated Green-Building Certifications In Corporate Real Estate

The Australia integrated facility management market is gaining from the way green-building certification has moved from a branding tool into a practical filter in leasing, operations, and procurement decisions. NABERS reported that certified ratings nearly doubled in FY2025, with a 120% increase from FY2024, while the Green Building Council of Australia said FY2024-25 delivered almost 2,000 Green Star certifications, the strongest year in the scheme’s history.[1]NABERS, “NABERS Annual Report FY2025,” NABERS, nabers.gov.au From May 1, 2026, all new building projects in Australia must register under Green Star Buildings v1.1, which brings all-electric construction and embodied-carbon reporting into the baseline expectation for new assets.[2]Green Building Council of Australia, “Green Star Buildings v1.1,” Green Building Council of Australia, new.gbca.org.au This matters for operating contracts because maintaining a 5.5-star NABERS Energy rating requires regular HVAC tuning, sub-metered energy tracking, and steady compliance reporting rather than occasional maintenance visits. Green Star-rated assets have also been associated with a 10% premium in net face rents and 2.7% lower vacancy than unrated peers, which gives landlords a direct financial reason to retain integrated service providers that can protect certified performance over time. As a result, the Australia integrated facility management (IFM) market is seeing stronger demand for bundled contracts that combine technical maintenance, energy oversight, and reporting support within one operating model.

Government Mandates for Energy-Efficient Public Infrastructure

The Australia integrated facility management market is also being reshaped by public policy because federal and state mandates now favour providers that can show measurable outcomes on energy use and emissions. The Australian Government’s Net Zero in Government Operations Strategy has required prioritizing all-electric infrastructure for government office leasing since July 2024, and for purchase and construction since July 2026.[3]Department of Climate Change, Energy, the Environment and Water, “Government Buildings,” Australian Government, dcceew.gov.au Treasury and the Department of Climate Change, Energy, the Environment, and Water stated in the Built Environment Sector Plan that commercial buildings produced 9 MtCO2-e of direct Scope 1 emissions in 2024, which underscores the need to keep operational performance under closer scrutiny.[4]Treasury and Department of Climate Change, Energy, the Environment and Water, “Built Environment Sector Plan,” Australian Government, treasury.gov.au That policy setting is changing contract design in the Australia IFM market, because fees are increasingly linked to rating retention, carbon milestones, and energy intensity benchmarks rather than only routine service outputs. It also broadens the FM provider's scope of work, since maintaining a mandatory NABERS threshold often requires BMS calibration, refrigerant compliance management, and tenant-side data collection across the building. The result is a steady move toward longer, more integrated, and more performance-based agreements across public portfolios.

Expansion Of Data Centers Requiring Specialized IFM

The Australia integrated facility management market is developing a more specialized layer of demand through the rapid expansion of data centers, where uptime, thermal stability, and security controls are far stricter than in standard office assets. The Australian Energy Market Operator estimated that data centers currently account for around 4 TWh of electricity use on the National Electricity Market, or close to 2% of grid demand, and this is projected to rise to around 12 TWh by 2029 to 2030. That growth brings a different service profile because operators need constant environmental monitoring, advanced cooling support, energy optimization, and physical security compliance over a 24/7 operating cycle. The barrier to entry is also becoming higher, as NABERS policy settings require at least a 5-star rating for data centers serving government operations, which ties technical maintenance directly to compliance outcomes. Providers that can field dedicated critical-environment teams therefore have a stronger position in this part of the Australia integrated facility management (IFM) market than generalists that still rely on conventional commercial building skill sets. This is one reason commercial demand is moving up faster, even though the broader installed base remains weighted toward older property categories.

Labor Shortage Driving Outsourcing of Non-Core Functions

The Australia integrated facility management market is also benefiting from labour constraints because persistent shortages are pushing occupiers to outsource facility functions that are difficult to staff internally. Jobs and Skills Australia continued to identify shortage pressure across a large share of skilled occupations, which supports the view that building services teams remain hard to replace in many parts of the country. The Australian Bureau of Statistics reported 337,900 job vacancies in February 2026, with construction and administrative support activities still showing tight supply conditions. In practical terms, large IFM providers can move technicians across accounts, carry training costs over a broader revenue base, and absorb wage escalation more effectively than most in-house teams. That is especially important in industrial sites, healthcare campuses, and remote operations, where regulatory maintenance cannot simply be delayed until staffing improves. The result is higher demand in the Australia iIFM market for multi-year contracts that replace ad hoc subcontracting with broader outsourced delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Supplier Base Inflating Contract Management Costs | -1.8% | National | Short term (≤2 years) and medium term (2-4 years) |

| Skills Gap in MEP Technicians for Smart Buildings | -1.2% | National, acute in regional and remote areas | Medium term (2-4 years) |

| Inflationary Pressure on Cleaning and Catering Inputs | -0.9% | National | Short term (≤2 years) |

| Slow Standardization of Digital FM Platforms Across States | -0.5% | National, with variation across jurisdictions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented Supplier Base Inflating Contract Management Costs

The Australia integrated facility management market still carries a sizable coordination burden because many portfolios depend on large webs of specialized subcontractors spread across several states. That model increases approval steps, insurance checks, documentation work, and service-quality tracking, which raises contract administration costs for both the buyer and the prime contractor. It also creates uneven execution when one provider handles cleaning, another covers technical maintenance, and several more manage local trades, landscaping, waste, and compliance tasks. The ACCC’s December 2024 civil cartel proceedings against Spotless Facility Services and Ventia Australia on Defence estate maintenance contracts highlighted how procurement risk can rise when high-value submarkets rely on a narrow pool of suppliers. Administrative friction of this kind slows the move to fully integrated delivery in the Australia integrated facility management (IFM) market, even when customers clearly prefer single-accountability models. Until vendor consolidation moves further, this restraint is likely to keep pressuring margins and back-office costs.

Skills Gap in MEP Technicians for Smart Buildings

The Australia integrated facility management market is also being held back by a shortage of technicians who can work across mechanical systems, digital controls, and sustainability reporting within the same asset. Modern MEP roles now involve BMS interpretation, IoT-connected asset checks, energy optimization support, and evidence gathering for NABERS-related reporting, which is a wider brief than many traditional trade pathways were designed to support. Vacancy pressure remains high in the broader labour market, and that keeps recruitment cycles long while wage expectations continue to rise for experienced technical staff. The pressure is strongest in regional and remote portfolios, where travel demands and smaller labour pools make response times harder to maintain. Providers are trying to offset this through remote monitoring, automated scheduling, and semi-autonomous maintenance tools, yet adoption is still uneven across the Australia IFM market. This leaves operators with a difficult balance between protecting service quality and protecting contract margins, especially in smart-building environments where compliance failure can carry immediate consequences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Pulls Ahead on Compliance and Connectivity

Soft Facility Management (FM) held 56.29% of the Australia integrated facility management (IFM) market share in 2025, and it remained the largest service line because cleaning, office support, catering, and security demand was spread across commercial offices, healthcare campuses, government buildings, and Defence estates. That scale matters in the Australia integrated facility management market because high-frequency services create regular renewal points, stable site presence, and close operational relationships with occupiers. The segment also covers many site-specific needs, from specialist cleaning at university and healthcare facilities to catering and support logistics at remote industrial and mining locations, which makes switching providers more disruptive than it may first appear. Buyers therefore tend to stay with vendors that already understand local service rules, reporting lines, and compliance routines across multi-site portfolios. This helps explain why Soft FM continues to anchor overall contract volumes even as more technical work receives greater strategic attention.

Hard Facility Management (FM) is projected to grow at an 8.24% CAGR through 2031, the fastest pace among service categories, because electrification, energy compliance, and data-center requirements are shifting more value toward technical maintenance and asset management. In the Australia integrated facility management industry, this part of the service mix now carries stronger pricing support because customers increasingly need MEP and HVAC teams that can keep systems efficient, compliant, and digitally visible over the life of the asset. Asset Management and MEP and HVAC Services are also supported by proposals in the National Construction Code 2025 Public Comment Draft, which include photovoltaic systems, heat-pump-ready infrastructure, and variable-speed fan requirements in commercial buildings. Fire Systems and Safety adds another protected niche, because accreditation and state-level compliance rules limit the available labour pool and reduce price sensitivity for qualified providers. Other Soft FM services such as waste management and landscaping are also changing, as sustainable procurement expectations in contracts above AUD 7.5 million, or USD 4.8 million, are pushing environmental criteria deeper into routine service scopes. The Australia IFM market therefore still depends on Soft FM for breadth, but margin expansion and technology-led differentiation are moving more clearly toward Hard FM.

By End-User: Industrial Leads on Volume, Commercial Accelerates on Technology

The Industrial and Process Sector held 31.62% of the Australia integrated facility management market share in 2025, making it the largest end-user group because remote assets, camp management, and process-area maintenance are difficult to replicate with in-house teams. This is a defining feature of the Australia integrated facility management (IFM) market, since energy, resources, and manufacturing sites often require integrated delivery across accommodation, catering, technical maintenance, and site-support services within a single contract. Sodexo’s five-year Santos contract, awarded in March 2025, covered 25 camps, 3,500 rooms, and average daily occupancy of 2,000 residents across Queensland, South Australia, and Western Australia, which shows the scale available in industrial outsourcing models. Contract size in this segment is usually supported by distance, workforce rotation, and compliance needs, all of which raise the value of a provider that can manage both living environments and operational assets. These conditions have kept industrial demand broad and durable, even while newer white-collar property categories receive more attention in market discussions.

Commercial end-users are forecast to grow at an 8.16% CAGR through 2031, making them the fastest-moving customer base as data-center construction and premium office refurbishment continue to lift technical service intensity. In the Australia integrated facility management industry, this growth is tied to smart-building infrastructure, high-density cooling systems, occupancy analytics, and energy performance obligations that require constant oversight rather than periodic maintenance. Institutional and public infrastructure also remain central to the Australia IFM market because whole-of-government property arrangements, Defence transformation programs, and transport public-private partnerships generate long contracts with dependable renewal profiles. Healthcare is following the same direction, and ISS extended its Canberra Health Services contract in December 2024 to include the AUD 640 million, or USD 420 million, Critical Services Building within scope. Hospitality has a more mixed outlook because hybrid work still limits some CBD food-service volumes, while other end-user groups such as multi-house residential, entertainment, and sports venues should gain relevance as Brisbane 2032 infrastructure moves closer to delivery.

Geography Analysis

The Australia integrated facility management market is a single-country market, but demand is not evenly spread because federal government and Defence portfolios still shape a large share of contracted national activity. The Department of Defence’s Base Services Transformation program showed this clearly, with Ventia securing two packages valued at AUD 2.7 billion, or USD 1.72 billion, in September 2025, while JLL won a six-year national Defence Estate Works Programme contract in February 2026. This concentration gives the Australia IFM market a national backbone that is more policy-led than in many other service sectors. It also makes contract capability in compliance, reporting, mobilization, and remote portfolio coordination more important than simple local scale. New South Wales remains the commercial anchor because Sydney combines premium office towers, dense government-leased space, and a growing data-center footprint that demands integrated hard and soft services at the same time.

NSW policy settings also matter beyond the state itself because government office requirements now call for a minimum 5-star NABERS Energy rating, and that pushes performance-based FM specifications deeper into lease structures. Victoria has become the most active state for new infrastructure-linked demand, helped by electrification priorities in the Built Environment Sector Plan and a strong pipeline of transport, health, and digital infrastructure projects. AirTrunk’s MEL2 hyperscale campus announcement, with more than 354 MW of capacity and over AUD 5 billion, or USD 3.18 billion, in planned investment, adds another large critical-environment requirement to the state’s FM workload. That combination keeps Victoria central to growth in technical maintenance, compliance services, and uptime-sensitive operating models.

Queensland and Western Australia add high-value demand through energy and mining operations, where remote workforce support and asset lifecycle services continue to favour outsourced delivery. South Australia is also emerging as a more important Defence maintenance corridor within the Australia integrated facility management market because federal contracts are increasing the concentration of specialist work there. ISS signed a six-year integrated facility services agreement with the Australian Department of Defence in September 2025, covering 85 Defence locations in South Australia and Western Australia from 2026 onward. As a result, geography in the Australia integrated facility management (IFM) market is less about broad regional fragmentation and more about the interaction between policy-heavy public estates, major metropolitan commercial assets, and remote industrial operations.

Competitive Landscape

The Australia integrated facility management market is moderately concentrated, with a small group of large operators, including Ventia Services Group, CBRE Group, ISS, Cushman and Wakefield, JLL, Sodexo, BGIS, and Compass Group, holding much of the government and institutional revenue pool. At the same time, the Australia integrated facility management market still has a long tail of domestic specialists and niche providers that compete on response time, local relationships, and targeted technical capability. This creates a competitive structure where scale matters in large tenders, but specialist execution still matters in regional work, defense-linked assets, and complex technical environments. The most consistent themes across the leading firms are technology integration, ESG credentials, and the ability to meet indigenous and social-enterprise procurement expectations in public bids. In practice, that means customers are now testing not only labour coverage and price, but also digital reporting quality, asset visibility, and the provider’s ability to support sustainability outcomes over the full contract term.

Recent contract activity shows how the leaders are defending their position in the Australia integrated facility management market through digital accountability and broader operating scope. Ventia said its September 2025 Base Services Transformation packages embedded digital and operational innovations aimed at better transparency and stronger environmental management, which shows how outcome tracking is becoming contractual rather than optional. JLL’s February 2026 reappointment under the whole-of-Australian-government property services arrangements points to the same shift, since net-zero alignment and end-to-end portfolio capability are now closely linked in federal property work. BGIS’s April 2026 general facilities management award for Sydney Airport, which included a 24/7 FM Hub across terminal, car park, airside, and landside assets, is another example of scale being reinforced through integrated operating models.

There is still clear room in the Australia integrated facility management market for expansion into mid-market commercial portfolios, lower-penetration residential and multi-house assets, and specialized data-center environments where only a few providers can operate at hyperscale standards. PropTech-native challengers are using autonomous maintenance tools, AI scheduling, and connected CMMS platforms to challenge the traditional labour-heavy model and win attention during tenders. Governance has also moved higher up the agenda after the ACCC’s civil cartel proceedings against Spotless and Ventia, because buyers now pay closer attention to compliance discipline and subcontractor controls. This is why merger and acquisition interest is building around regional specialists, digital maintenance platforms, and operators with strong public-sector client relationships, even though the Australia integrated facility management market still remains far from highly consolidated.

Australia Integrated Facility Management Industry Leaders

CBRE Group, Inc.

ISS Facility Services Australia Ltd

Jones Lang LaSalle Incorporated

Ventia Services Group Limited

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BGIS was awarded the General Facilities Management Services contract for Sydney Airport, covering T1 International, T2 Domestic, T3 Domestic, associated car parks, and all airside and landside spaces, including a dedicated 24/7 FM Hub. The win positioned BGIS as a leading aviation FM provider in Australia.

- February 2026: JLL was reappointed as a Property Service Provider under the Whole of Australian Government Property Services Coordinated Procurement Arrangements for a five-year term, covering end-to-end property and portfolio management for 28 Federal Government entities with a Net Zero in Government Operations alignment mandate.

- February 2026: JLL secured a six-year contract for national programme services under the Defence Estate Works Programme, building on an 11-year relationship and management of 1,510 projects valued at USD 2.41 billion since 2014.

- January 2026: BGIS was awarded the Real Estate and Facilities Management Services Contract for the Victorian Government’s Department of Government Services, effective January 7, 2026, covering 291 properties including offices, heritage buildings, courts, and police stations.

Australia Integrated Facility Management Market Report Scope

The Australia Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current outlook for the Australia integrated facility management market?

The Australia integrated facility management market stood at USD 18.46 billion in 2026 and is forecast to reach USD 27.50 billion by 2031 at an 8.3% CAGR.

Which service type currently leads demand in Australia?

Soft FM led in 2025 with a 56.29% share, supported by large cleaning, catering, security, and office-support requirements across commercial, healthcare, government, and Defence assets.

Which service type is growing the fastest through 2031?

Hard FM is projected to grow at an 8.24% CAGR through 2031, helped by electrification, energy performance compliance, and rising MEP and HVAC demand from data centers and modern buildings.

Which end-user group contributes the most revenue?

The Industrial and Process Sector was the largest end-user in 2025 with a 31.62% share, reflecting the size of remote operations, camp management, and process-facility maintenance needs.

Why are commercial occupiers becoming more important in Australia?

Commercial demand is forecast to grow at an 8.16% CAGR through 2031 as hyperscale data-center projects and premium office refurbishments require continuous technical and energy-related oversight.

What is the main operating challenge for providers in this space?

The biggest near-term issue is the shortage of MEP technicians and trade workers, which increases wage pressure, slows response times, and makes digital tools and remote monitoring more valuable.

Page last updated on: