South Africa Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

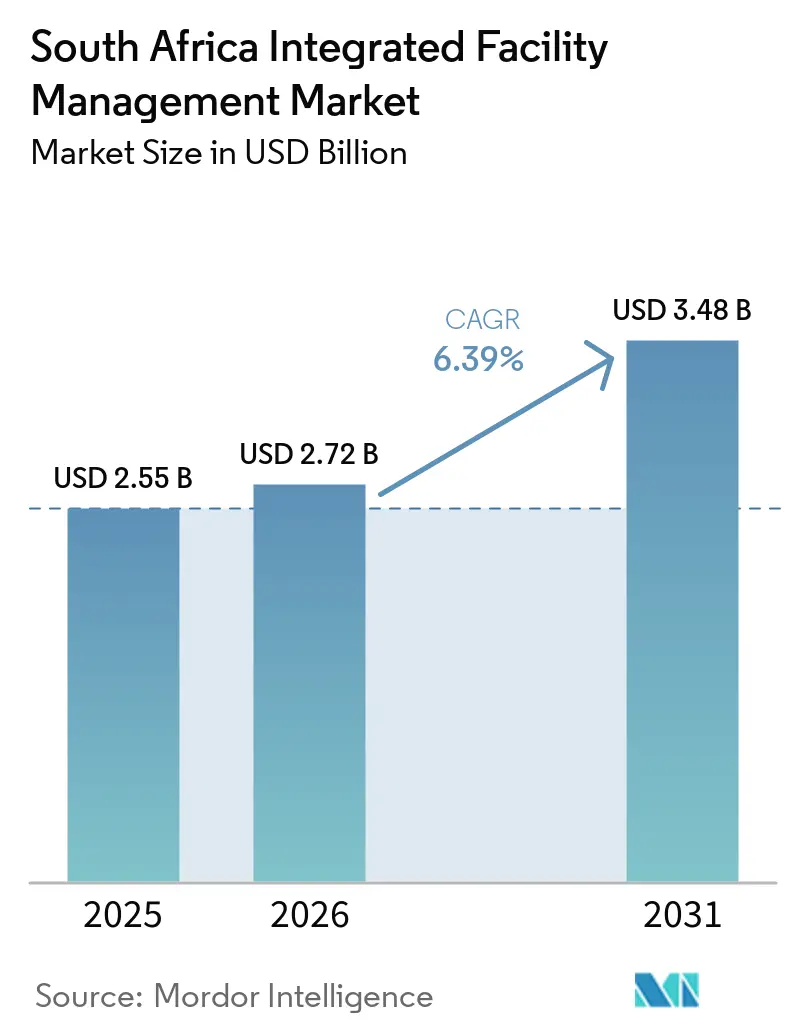

| Base Year Market Size (2025) | USD 2.55 Billion |

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.48 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

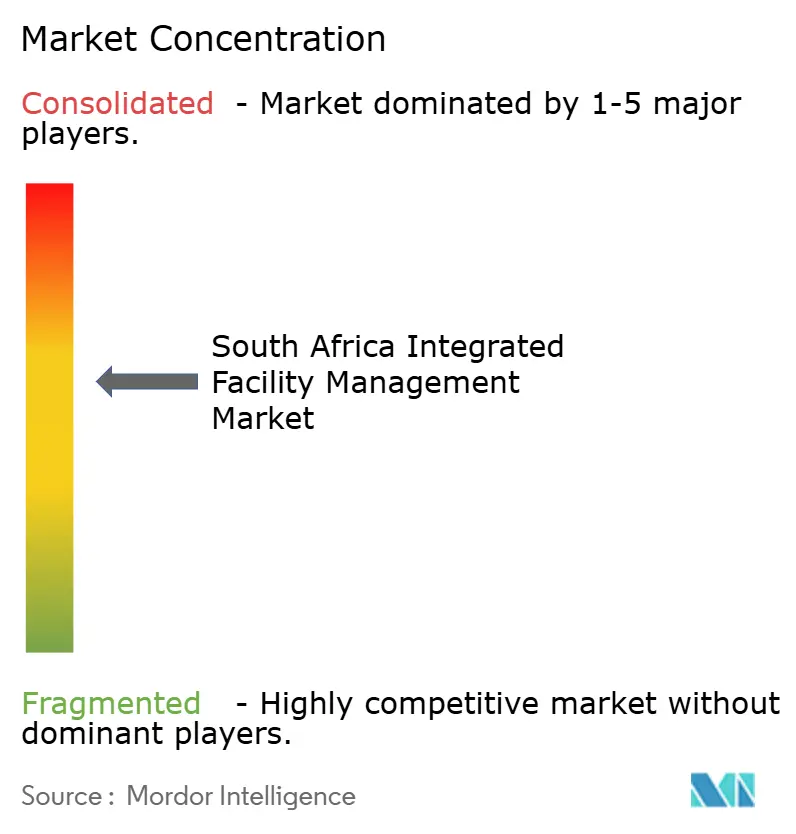

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Integrated Facility Management Market Analysis by Mordor Intelligence

The South Africa integrated facility management market size was valued at USD 2.55 billion in 2025 and estimated to grow from USD 2.72 billion in 2026 to reach USD 3.48 billion by 2031, at a CAGR of 6.39% during the forecast period (2026-2031). The South Africa integrated facility management market is supported by a large installed base of commercial, public, industrial, and institutional assets that need longer-term operations, upkeep, and compliance management. Public infrastructure spending above ZAR 1 trillion (USD 55 billion) across fiscal years 2025 to 2028 and the expansion of Infrastructure South Africa’s Strategic Integrated Projects pipeline from ZAR 340 billion (USD 18.9 billion), in 2020 to more than ZAR 1.3 trillion (USD 72.2 billion by 2025), are widening the pool of assets that can move into outsourced facility management over time. Energy compliance rules, digital work-order systems, and stronger expectations around asset uptime are pushing contracts away from basic service bundles and toward broader performance-based scopes in the South Africa integrated facility management market. Competition remains moderate to high because scale operators have national reach and deeper technical capabilities, while smaller firms still compete in narrower soft-service packages. Demand opportunities are becoming more visible in public healthcare, mining-linked facilities, and energy-managed buildings, where clients increasingly want one operator to handle compliance, maintenance, utilities, and site support under a single contract.

Key Report Takeaways

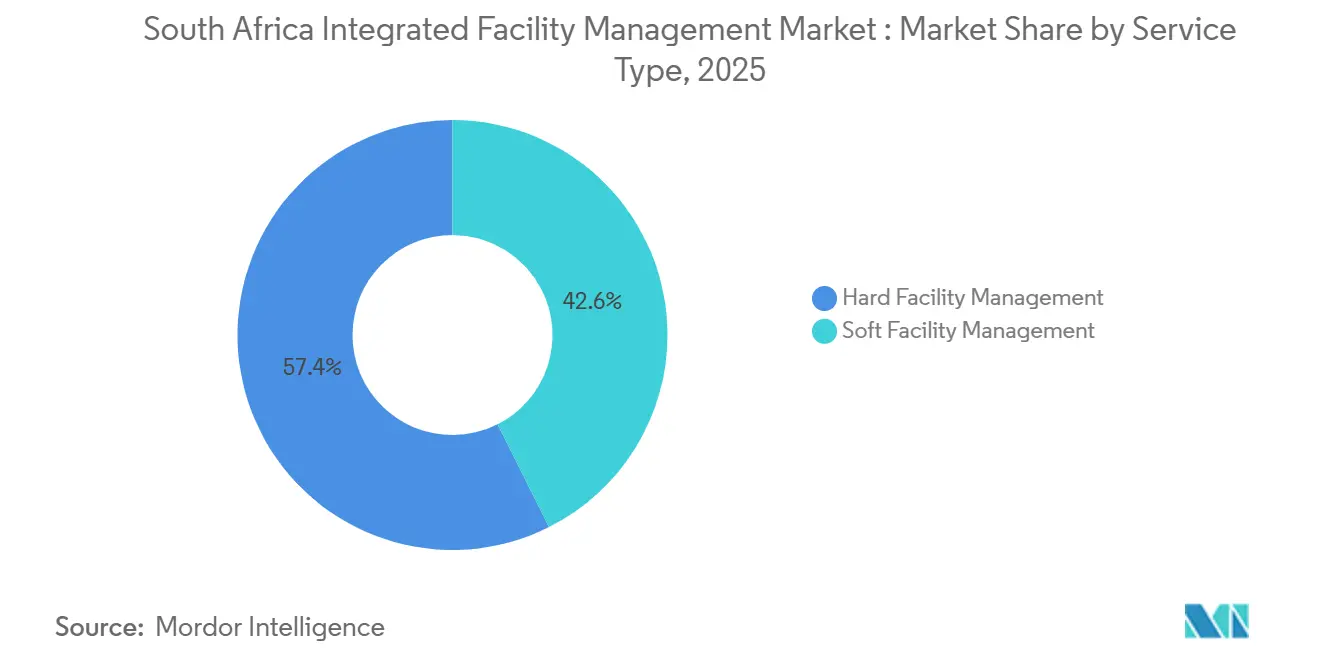

- By service type, soft facility management held 57.41% revenue share of the South Africa integrated facility management market size in 2025, while Hard FM is projected to record the fastest CAGR of 6.97% through 2031.

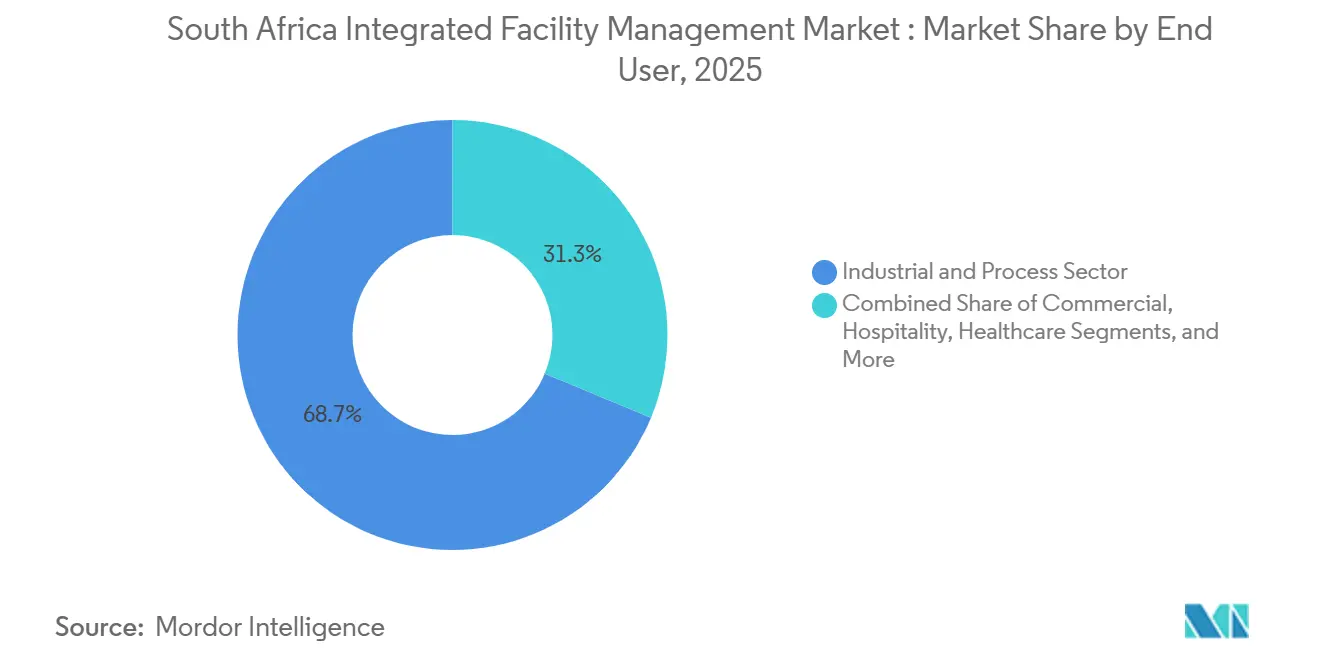

- By end user, industrial and process sector held 31.29% revenue share of the South Africa integrated facility management market size in 2025, while Commercial is projected to grow at 7.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Infrastructure Pipeline Boosting FM Demand | +1.8% | National, concentration in Gauteng, Limpopo, Western Cape | Medium term (2-4 years) |

| Corporate Flight To Quality, Driving Outsourcing Of Non-Core Functions | +1.5% | National, early gains in Johannesburg CBD, Sandton, Cape Town Century City | Medium term (2-4 years) |

| Mandatory Energy-Efficiency Standards For Buildings | +1.2% | National, compliance pressure highest for government-owned buildings 1,000 m² and above | Medium term (2-4 years) |

| Digital Work-Order Management And IoT Adoption | +0.8% | National, advanced deployment in Gauteng and Western Cape commercial precincts | Long term (≥ 4 years) |

| Mining Sector's Shift Toward Predictive Maintenance | +0.6% | Northern Cape, Limpopo, North West, Mpumalanga mining corridors | Long term (≥ 4 years) |

| Growth Of Integrated PPP Hospital Projects | +0.5% | National, active projects in Limpopo, Western Cape, Gauteng, KwaZulu-Natal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Pipeline Boosting FM Demand

South Africa’s infrastructure rollout is creating a larger stock of operational assets that will need maintenance, utilities management, cleaning, security, and compliance support once projects move from construction into service. The Presidency stated in May 2025 that Infrastructure South Africa’s project preparation fund supported 34 projects in fiscal 2024/25, with an estimated capital value of ZAR 259 billion (USD 14.4 billion), and that the wider strategic project pipeline had expanded sharply by 2025.[1]Cyril Ramaphosa, “Address by President Cyril Ramaphosa at the 2025 Sustainable Infrastructure Development Symposium South Africa,” The Presidency, thepresidency.gov.za The same update showed that 250 procurement-ready projects valued at more than ZAR 238 billion (USD 13.2 billion), were active across roads, energy, water, and social infrastructure, which points to a broader future base for outsourced asset management and site services. This matters for the South Africa IFM market because concession-style and public-private delivery models usually extend the service need well beyond commissioning. As that pipeline matures, the South Africa integrated facility management market should see more long-duration contracts tied to asset preservation, uptime, and regulatory reporting rather than short-term site-level service orders.

Corporate Flight to Quality, Driving Outsourcing of Non-Core Functions

The South Africa integrated facility management market is also benefiting from a broader shift among occupiers that want fewer vendors and clearer accountability for building operations. Corporates are under pressure to manage office utilization, service quality, and cost control at the same time, and that is making single-service contracts less practical in larger portfolios. Hybrid workplace patterns have made cleaning cycles, HVAC scheduling, security deployment, and workspace support less predictable, which favors bundled service models with centralized oversight. This shift is strongest in premium office nodes and multi-site portfolios where tenants want one operating standard across all properties. The result is a steadier move in the South Africa IFM market toward integrated contracts that link technical services and soft services under one performance framework.

Mandatory Energy-Efficiency Standards for Buildings

Mandatory compliance rules are turning energy management into a core part of facility management rather than an optional add-on. Under South Africa’s Energy Performance Certificate framework, privately owned buildings of 2,000 m² and above and government-owned buildings of 1,000 m² and above had to display an EPC by December 7, 2025, and non-compliance can draw fines up to ZAR 5 million (USD 278,000) or imprisonment for up to 5 years.[2]City of Cape Town, “Energy Efficiency at Home, Understanding SANS 10400-XA 2021 Compliance,” City of Cape Town, capetown.gov.za SANEDI’s register-based compliance process is pushing owners to track building use, operating performance, and reporting quality more closely than before. The 2021 edition of SANS 10400-XA also reinforces stricter expectations around energy use in buildings, which raises the technical responsibility carried by FM teams across HVAC, lighting, and envelope-related performance. Bidvest Facilities Management’s Tier 1 ESCo registration in 2024 shows how leading operators are building dedicated energy-management capability to capture this work in the South Africa IFM market.

Digital Work-Order Management and IoT Adoption

Digital operating systems are changing how service delivery is planned, measured, and priced across the South Africa integrated facility management market. MRI Software reported in 2026 that AI-enabled IoT integration in South African FM settings can deliver a 30% improvement in operational efficiency, a 35% reduction in maintenance costs, and a 20% reduction in energy use through automated building controls.[3]MRI Software, “MRI Agora IoT Hub - Smart Buildings,” MRI Software, mrisoftware.com Peritus Business Solutions also shows that IoT-enabled CMMS tools can trigger digital work orders automatically once sensor thresholds are breached, which reduces manual follow-up and supports more predictable maintenance cycles. This is important because digital records give clients a clearer audit trail on response times, asset condition, and uptime outcomes. That operating visibility is helping the South Africa IFM market move toward contracts that reward measured performance instead of simple time-and-materials billing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Load-Shedding Increasing Operating Costs | -1.5% | National, highest impact in industrial provinces, Mpumalanga, Gauteng, North West | Short term (≤ 2 years) |

| Skills Shortage In Certified HVAC And MEP Technicians | -1.2% | National, acute in secondary cities and mining provinces | Long term (≥ 4 years) |

| Delayed Government Payments To FM Contractors | -0.8% | National, concentrated in public healthcare and education segments | Medium term (2-4 years) |

| Low Margins Driving Informal Competition | -0.5% | National, particularly evident in Gauteng soft FM sub-contracts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Load-Shedding Increasing Operating Costs

Power reliability improved sharply, but the cost structure created during the crisis is still weighing on operators in the South Africa integrated facility management market. Eskom reported that FY2025 delivered 352 load-shedding-free days and that FY2026 year to date had only 4 days of interruptions by November 2025. Even with that improvement, Eskom spent ZAR 33.4 billion (USD 1.85 billion), on diesel for open-cycle gas turbines in FY2024, and FY2026 year to date had already reached ZAR 6.07 billion (USD 337 million), against a budget of ZAR 8.05 billion (USD 447 million).[4]Theresa Magubane, “Eskom Provides Update on Diesel Usage and System Performance,” Eskom, eskom.co.za FM operators still carry generator upkeep, diesel handling, compliance checks, and backup power coordination in many commercial, healthcare, and industrial sites because those requirements do not disappear as quickly as grid conditions improve. This keeps margin pressure elevated in the South Africa integrated facility management market, especially where contracts were signed during the worst phase of the power crisis and still include costly standby obligations.

Skills Shortage in Certified HVAC and MEP Technicians

The shortage of qualified technical labor remains a harder long-term limit on service quality than headline demand conditions suggest. Hard FM scopes need certified technicians for HVAC, electrical, plumbing, and mechanical systems, and that requirement is most difficult to meet in secondary cities and mining provinces where specialist labor pools are thinner. Industry reporting in late 2024 showed that legacy HVAC&R trade tests had been phased out by June 30, 2024, while the replacement External Integrated Summative Assessment under the QCTO framework was still difficult for new apprentices to access in practice. That transition gap slows technician entry at the same time that energy compliance and more advanced building systems are raising the technical bar for operators. For the South Africa IFM market, the result is wage pressure, higher dependence on subcontractors, and slower scaling in hard FM packages where certified staff cannot be replaced by general service labor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Gains Ground On A Soft Facility Management Base

Soft facility management held 57.41% of the South Africa integrated facility management market share in 2025, which reflected steady demand for cleaning, catering, office support, and security across large commercial and institutional properties. These services remain the most common entry point for long-term client relationships because they are required daily and can be standardized across broad property networks. That installed base gives national operators a way to expand from routine services into broader account management and technical support over time. Even so, the South Africa integrated facility management market is shifting gradually toward more complex work as compliance, asset efficiency, and uptime expectations become more central to procurement decisions.

Hard facility management is the faster-moving part of this market and is projected to expand at 6.97% CAGR through 2031. Building owners now need stronger support around HVAC, MEP systems, fire protection, utilities, and preventive maintenance, especially where operating standards are tied to energy reporting and asset condition. The EPC regime administered through SANEDI adds to that shift by turning building performance into an ongoing operating issue rather than a one-time design concern. Bidvest Facilities Management’s Tier 1 ESCo registration and Tsebo’s management of 1.4 GW of client electricity across 6,000 sites show how leading firms in the South Africa integrated facility management industry are broadening their technical capability so they can capture a larger share of integrated contracts.

By End User: Industrial Spend Leads While Commercial Demand Rises Fast

The industrial and process sector accounted for 31.29% of the South Africa integrated facility management market size in 2025, making it the largest end-user base. That position reflects the country’s broad mining, energy, and manufacturing footprint, where facilities are often spread across remote sites and require tighter maintenance discipline than standard office portfolios. In mining, downtime costs are high and service environments are demanding, so clients place more value on support, technical supervision, and scheduled preventive work. Komatsu’s use of Prognostics and Health Monitoring services in South African mining operations reflects the wider move toward predictive maintenance models that support this demand pattern.

The Commercial segment is projected to expand at a 7.11% CAGR through 2031, which makes it the fastest-growing end-user category in the South Africa integrated facility management market. Office portfolios may be using space differently than before, but service delivery has become more complex because occupancy, cleaning schedules, HVAC loads, and security needs now shift more often within the same building. That makes centralized vendor management and integrated service reporting more valuable to BFSI, IT, telecom, retail, and warehouse occupiers. The South Africa integrated facility management industry is also seeing more opportunity from healthcare and public infrastructure, where the New Development Bank’s USD 200 million approval for Limpopo Central Hospital points to a growing future need for long-duration non-clinical FM support.

Geography Analysis

Gauteng remains the primary demand center in the South Africa integrated facility management market because it concentrates the country’s largest cluster of corporate headquarters, government departments, data centers, and major commercial assets. Johannesburg and Pretoria support large integrated contracts that combine routine services with maintenance, utilities oversight, compliance management, and multi-site coordination. Gauteng also tends to adopt digital FM tools earlier than other provinces because premium assets place more value on uptime reporting and centralized operating control. MRI Software’s 2026 guidance on smart-building integration in South Africa supports that pattern, with measured gains in efficiency, maintenance cost reduction, and energy performance when IoT systems are used at building level. This keeps Gauteng at the center of higher-specification work in the South Africa integrated facility management market, especially for clients that want performance evidence and stronger data visibility.

The Western Cape and KwaZulu-Natal form the next demand tier, but their growth drivers are not identical. In the Western Cape, stronger focus on energy performance and net-zero building operations is pushing FM scopes toward compliance tracking, monitoring, and energy management. The City of Cape Town’s Energy Strategy 2050 commits all new buildings to net-zero carbon in operation by 2030, which raises the value of technically capable operators that can manage performance over the life of the asset. KwaZulu-Natal, by contrast, benefits more from Durban’s logistics and industrial footprint, where site support, maintenance reliability, and service continuity remain central procurement priorities.

Limpopo, Mpumalanga, and the Northern Cape are smaller in corporate office volume, but they matter disproportionately for industrial FM in the South Africa integrated facility management market. Their importance comes from mining-linked assets and more remote operating environments where predictive maintenance and field service responsiveness can carry higher value than basic soft-service scale. Komatsu’s PHM offering in South Africa supports the case for more condition-based service activity in mining regions, where asset failure can disrupt production and site operations. The New Development Bank’s approval of financing for Limpopo Central Hospital, which was 43% complete and ahead of schedule at approval, also points to a wider future FM role for public assets in provinces that historically carried less contract volume.

Competitive Landscape

The South Africa integrated facility management market has a moderately concentrated structure at the national scale. Tsebo Solutions Group and Bidvest Facilities Management form the leading domestic tier, with Tsebo managing 25.5 million m² across 6,000 sites and processing 32,000 client utility bills that cover 1.4 GW of electricity, while Bidvest FM oversees more than 28,000 buildings across 23 million m² through 12 regional offices and 34 satellite sites. Below that level, the South Africa integrated facility management market fragments quickly into mid-sized providers, specialist operators, and single-service subcontractors. This creates a split structure where large integrated contracts favor firms with national reach and technical breadth, while smaller soft-service packages remain much more priced.

Strategic positioning is increasingly shaped by capability building rather than simple footprint expansion. Tsebo’s April 2026 acquisition of Flick Pest Control broadened its workplace services platform and added a specialist line that can be bundled into larger integrated contracts. Bidvest FM’s Tier 1 ESCo registration in 2024 strengthened its position in energy-management work, which is becoming more important as compliance and building efficiency move deeper into procurement criteria. Bidvest FM’s status as the first FM company in South Africa to have its SANS 1752 self-declaration verified by SAFMA also gives it a standards-based advantage in tenders that value documented service quality. Global affiliates such as CBRE, JLL, ISS A/S, and Cushman & Wakefield Excellerate remain relevant in the South Africa integrated facility management market because multinational occupiers often prefer common reporting systems, workplace analytics, and international account structures across several countries.

The strongest near-term white space lies in technical hard FM for healthcare, mining, and energy-managed buildings, where informal operators struggle to meet compliance and uptime expectations. A second opening sits in digital FM services for mid-sized commercial landlords that need better occupancy-based scheduling and energy reporting without full enterprise platform complexity. Procurement quality also improves when actual service providers are separated from property owners and internal facility teams, which is why Atterbury Property, Liberty Two Degrees, and SPAR’s internal FM function are not meaningful competitive references, while Sodexo South Africa, OCS Group South Africa, and Khuthala Environmental Services are more relevant names to track in supplier mapping. Tsebo’s FY2024 sustainability reporting, including ZAR 1.1 billion (USD 61 million), in local-to-local procurement spend and support for 8,911 small business initiatives, shows that B-BBEE-aligned supply chains are becoming part of competitive differentiation in the South Africa integrated facility management market.

South Africa Integrated Facility Management Industry Leaders

Tsebo Solutions Group

Bidvest Facilities Management (Pty) Ltd

Servest Group (Pty) Ltd

Broll Facilities Management (Pty) Ltd

Cushman & Wakefield Excellerate (Pty) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Tsebo Solutions Group announced the acquisition of Flick Pest Control and its regional subsidiaries to strengthen its national integrated workplace management platform. The acquisition extends Tsebo's bundled service offering into specialist pest control across corporate, healthcare, education, mining, and event-space client sites, expanding its scope ahead of hospital PPP and industrial FM contract competitions.

- June 2025: The South African Treasury allocated R1 trillion over three years for infrastructure projects, releasing construction pipelines valued at R313.5 billion that will require downstream FM and IFM services once operational creating a significant forward contract opportunity for service providers

- September 2025: Fidelity Services Group has acquired a majority stake in SSG Holdings, strengthening South Africa’s integrated security and facilities management sector. The deal expands Fidelity’s national footprint, workforce, and service capabilities, reinforcing its position as a leading South African-owned risk solutions provider.

- September 2025: MSC Education Holdings has launched Project WON Hundred, an 18-month facilities management learnership aimed at developing South Africa’s next generation of FM leaders. Backed by Services SETA and SAFMA, the initiative equips unemployed graduates with accredited training, workplace experience, and career opportunities across the country’s growing facilities management sector.

South Africa Integrated Facility Management Market Report Scope

The South Africa Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD)

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User, Value | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of the South Africa integrated facility management market?

The South Africa integrated facility management market stood at USD 2.72 billion in 2026 and is projected to reach USD 3.48 billion by 2031 at a 6.39% CAGR.

Which service type leads demand in South Africa?

Soft FM led in 2025 with a 57.41% share because cleaning, catering, office support, and security remain the broadest outsourced needs across corporate and institutional sites.

Which service type is growing faster through 2031?

Hard FM is growing faster, with a 6.97% CAGR through 2031, supported by energy compliance, MEP demand, and stronger focus on preventive maintenance.

Which end-user group contributes the most spending?

The Industrial and Process Sector was the largest end-user in 2025 with a 31.29% share, supported by mining, energy, and manufacturing facilities that need more intensive operational support.

Why is commercial demand rising so quickly?

Commercial demand is projected to grow at 7.11% CAGR because hybrid occupancy patterns have made HVAC, cleaning, security, and site support more complex across multi-site portfolios.

Which province is the main demand center for facility management services?

Gauteng remains the main demand center because it has the highest concentration of headquarters, government buildings, data centers, and large commercial assets, which support recurring integrated contracts.

Page last updated on: