Japan Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

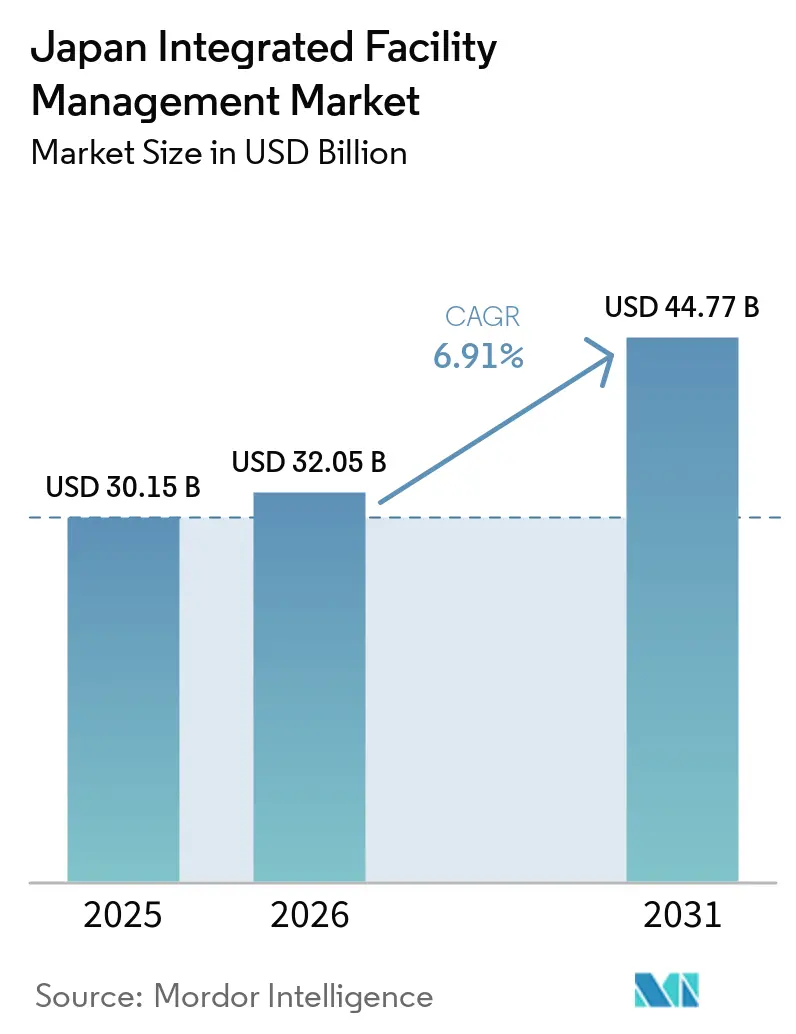

| Base Year Market Size (2025) | USD 30.15 Billion |

| Market Size (2026) | USD 32.05 Billion |

| Market Size (2031) | USD 44.77 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

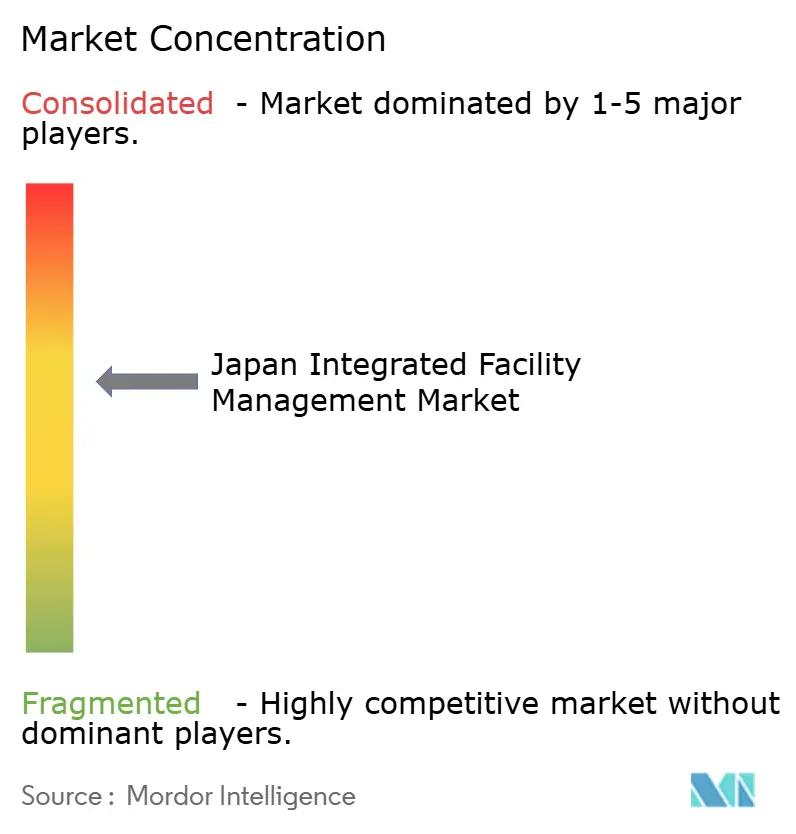

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Integrated Facility Management Market Analysis by Mordor Intelligence

The Japan Integrated Facility Management Market size is expected to increase from USD 30.15 billion in 2025 to USD 32.05 billion in 2026 and reach USD 44.77 billion by 2031, growing at a CAGR of 6.91% over 2026-2031.

The Japan integrated facility management (IFM) market is moving toward consolidated contracts as corporate and institutional clients try to reduce vendor overlap, improve accountability, and gain clearer visibility on asset performance across large property portfolios. Demand is also being lifted by aging commercial buildings that need coordinated maintenance, retrofit planning, and regulatory compliance under one operating structure rather than through separate vendors. Another strong tailwind comes from the expansion of hyperscale data center capacity, which raises the need for highly specialized service delivery across cooling, electrical systems, uptime monitoring, and safety management. Competitive advantage in the Japan IFM market is shifting toward firms that can pair service integration with digital tools such as predictive maintenance, connected work order systems, and robotic support in labour-intensive workflows. At the same time, providers that keep relying on conventional staffing models face rising pressure as clients increasingly prefer uptime commitments, energy reporting, and outcome-based performance standards over simple headcount-based contracting.

Key Report Takeaways

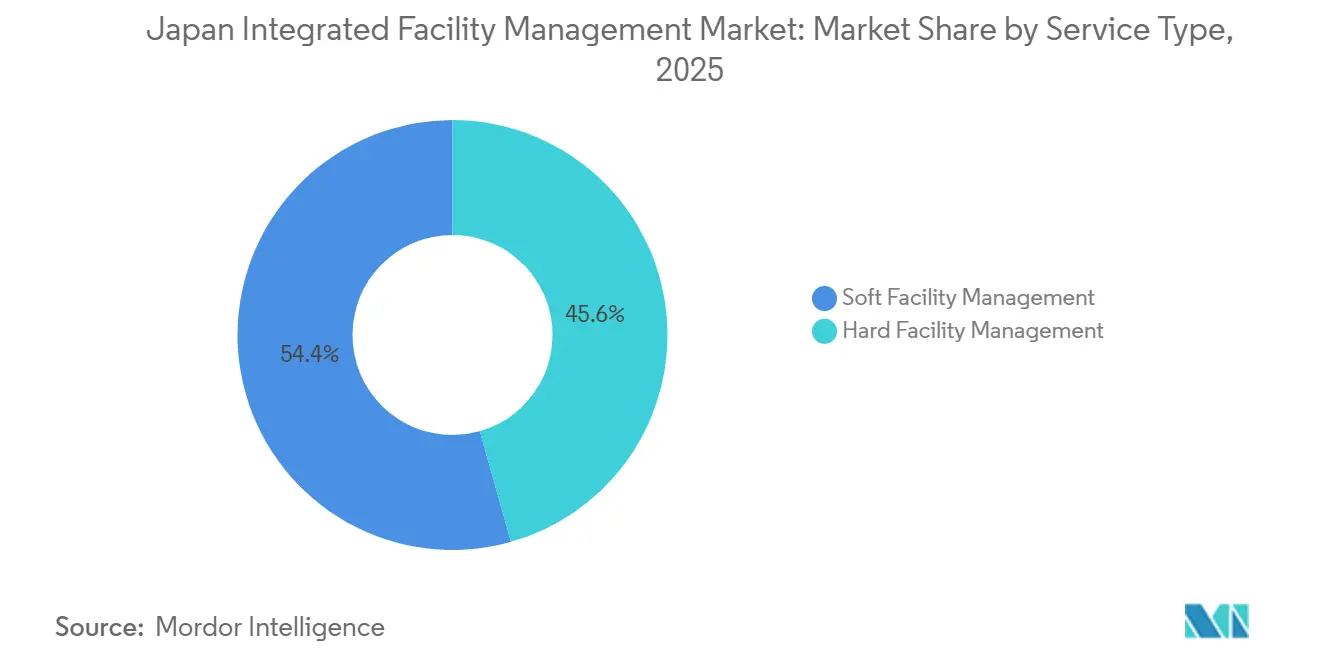

- By service type, soft facility management held 54.4% revenue share of the Japan integrated facility management market in 2025, while Hard Facility Management is projected to expand at a 7.7% CAGR through 2031.

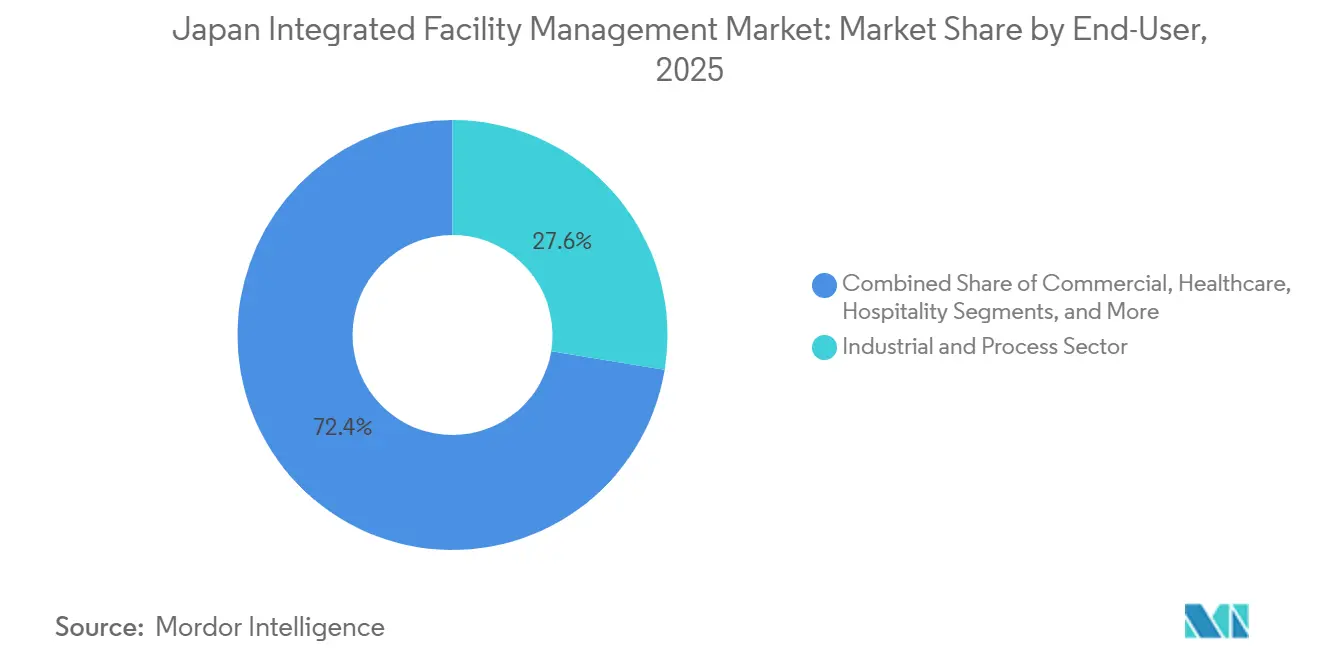

- By end-user, the industrial and process Sector accounted for 27.6% share of the Japan integrated facility management (IFM) market in 2025, while the commercial sector is forecast to grow at a 7.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Aging Infrastructure, Citing Outsourcing Demand | +1.5% | National, concentrated in Tokyo, Osaka, and Nagoya metropolitan areas | Medium-term (2-4 years) |

| Accuracy of Demand of the Predictive Maintenance | +1.3% | National, with early adoption concentrated in Tokyo and Osaka industrial corridors | Short-term (≤2 years) |

| Government Energy/Corporate FM Service Needs for Improving Integrated Services | +1.0% | National, with pronounced uptake in government-contracted buildings and large corporate campuses | Medium-term (2-4 years) |

| Local Technology/Managed Services Growing Rapidly | +0.8% | National, led by Tokyo metropolitan area with expansion to Osaka and Fukuoka | Short-term (≤2 years) |

| Expansion of Data Centers Resulting in FM Specialization | +0.7% | Tokyo (capacity-constrained), Osaka, Hokkaido, and Kyushu expansion corridors | Medium-term (2-4 years) |

| Rising Healthcare and Institutional Facility Requirements Amid Japan's Aging Demographics | +0.5% | National, with highest concentration in metropolitan areas and secondary cities with expanding senior care infrastructure | Long-term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Aging Infrastructure Driving Outsourcing Demand

Aging commercial buildings are creating a long-duration outsourcing base for the Japan integrated facility management market because older assets need more coordinated upkeep and stricter maintenance planning. Seismic reinforcement, MEP upgrades, fire safety work, and sanitation obligations are harder to manage when handled by disconnected vendors, especially in large, occupied properties that cannot tolerate service disruptions.[1]Ministry of Land, Infrastructure, Transport and Tourism, “MLIT Policy and Building Regulation Information,” MLIT, mlit.go.jp Asset owners are therefore moving toward integrated providers that can handle multiple technical scopes within a single contract and maintain documentation aligned with statutory requirements. This shift also improves contract stickiness because clients place value on single-point accountability, lifecycle visibility, and fewer operational handoffs across the building portfolio. In practice, the aging stock in Tokyo, Osaka, and Nagoya is supporting a wider role for providers that can combine building engineering oversight with scheduled compliance execution. That keeps the Japan integrated facility management (IFM) market tied not only to routine services but also to recurring upgrade cycles across mature urban assets.[2]e-Gov Laws and Regulations, “Japanese Laws and Regulations Database,” e-Gov, e-gov.go.jp

Growing Demand for Predictive Maintenance Accuracy

Predictive maintenance is becoming a practical growth lever in the Japan integrated facility management market because it helps providers shift from scheduled inspections to condition-based intervention. This matters more in Japan because aging building systems, labour scarcity, and the need for technical reliability raise the cost of reactive maintenance failure. NTT Docomo and NTT Facilities began field validation in April 2026 of a conversational AI system that uses Graph RAG and multi-agent processing to let staff query BIM data in natural language across seven NTT Docomo buildings. The model is important because it lowers the training barrier for non-specialist FM personnel while improving access to asset health information in daily operations.[3]NTT Facilities, “Non-Energy Benefits Evaluation Metrics Update for Buildings and Production Facilities,” NTT Facilities, ntt-f.co.jp NTT Data also reported in 2025 that BIM-FM integration at its Mitaka East facility reduced model data size by 98.8% while preserving full asset visibility, supporting broader multi-site deployment on standard hardware. As these tools move from pilot use to contract expectations, the Japan IFM market will keep moving toward pricing based on uptime, prevented failures, and measurable building outcomes rather than labour input alone.

Government Energy and Corporate FM Service Needs Are Improving Integrated Services

Energy and carbon targets are increasing the value of integrated delivery in the Japan integrated facility management (IFM) market because compliance now affects procurement, reporting, and long-term capital planning. Japan’s national decarbonization pathway and building-efficiency rules are pushing both public and private asset owners to more closely align facility services with energy performance and reporting needs. The Building Energy Efficiency Act gives that shift operational weight by tying major projects to performance expectations that cannot be met through fragmented building services alone. NTT Facilities and Deloitte Touche published updated non-energy Benefits metrics in February 2026, showing that retrofit projects in production facilities and government buildings can generate material annual value beyond direct energy savings. That supports broader acceptance of integrated FM programs because the investment case becomes easier to defend when energy, comfort, productivity, and asset performance are assessed together. Corporate occupiers are also placing more weight on providers that can support asset-level carbon accounting and sustainability reporting at renewal points, which improves retention for digitally capable operators in the Japan integrated facility management market.

Local Technology and Managed Services Are Growing Rapidly

The local shift toward managed services and digital delivery is strengthening the Japan IFM market because technology is now tied directly to labour resilience and service consistency. Providers are moving beyond software as a reporting layer and using connected systems to schedule work, monitor assets, and support robotic workflows in areas with limited staffing. AEON Delight’s FY2024 to 2026 medium-term plan set aside JPY 12 billion (USD 75.6 million) of a JPY 20 billion (USD 126.0 million) growth investment pool for digitization, robotics, IoT, and AI, which shows that leading operators are treating digital capability as core operating infrastructure rather than optional improvement spending.[4]AEON Delight, “Integrated Report and FY2024-2026 Medium-Term Plan,” AEON Delight, aeondelight.co.jp That investment direction matters because it supports a transition from specification-based contracts to SLA-based contracts, enabling providers to charge for performance, transparency, and lower interruption risk. Facilio’s 2024 deployment at Takenaka Central Building South also showed that owners are willing to consolidate multiple entities onto one facility platform when the system improves energy monitoring, asset tracking, and workforce coordination from the start. The result is a Japan integrated facility management market where firms that own digital workflows gain an advantage in both pricing power and contract renewal quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor Costs Limiting Competitiveness | -1.5% | National, acutest in Tokyo and Osaka metropolitan areas | Short term (≤2 years) |

| Stringent Building Codes Raising Compliance Costs | -0.9% | National, with highest compliance intensity in seismically active zones and major urban centers | Medium term (2-4 years) |

| Shortage of FM Talent for Niche Services | -0.7% | National, with critical gaps in specialized trades, certified inspectors, and high-voltage technicians | Long term (≥4 years) |

| Outdated Performance Metrics Hindering CAFM Administration | -0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Labor Costs Limiting Future Competitiveness

Labor cost inflation remains the clearest near-term restraint on the Japan integrated facility management market because staffing is still essential across cleaning, security, inspections, and building operations. Wage pressure is difficult to offset when many contracts were designed around traditional labour deployment and low pass-through flexibility. The pressure is more visible in public-sector work, where procurement structures often limit how much cost inflation can be reflected in contract pricing. That weakens the economics of advanced service delivery because providers may hesitate to place higher-skilled teams or digital support layers into contracts that do not compensate for rising execution costs. It also accelerates the push toward robotic cleaning, remote monitoring, and AI-assisted security because automation becomes a hedge against structurally tight labour supply rather than a simple efficiency upgrade. As that divide widens, scale operators with funding and technology will be better placed than cost-reactive providers to defend margins in the Japan integrated facility management (IFM) market.

Stringent Building Codes Increasing Compliance Costs

Japan’s building service environment is shaped by several overlapping legal frameworks, and that creates a heavier compliance burden for the Japan IFM market than for simpler outsourced service categories. The Building Standards Act, the Building Sanitation Law, the Fire Services Act, and the Building Energy Efficiency Act all influence how work is documented, certified, inspected, and delivered across building types. This raises administrative overhead and increases the need for certified labour, especially in hard FM, where work often touches safety systems, engineering controls, or renovation-linked performance standards. The burden is particularly challenging for smaller operators because compliance effort rises even when contract size is limited. As a result, technically demanding contracts are becoming more concentrated among firms with stronger technical benches, better process control, and enough balance sheet capacity to absorb front-loaded compliance work. That makes regulation a growth support for scale leaders but a cost barrier for a wider part of the Japan integrated facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Holds the Revenue Base While Hard FM Gains Technical Momentum

Soft Facility Management (FM) held 54.4% of the Japan integrated facility management market share in 2025, while Hard FM is projected to grow at a 7.7% CAGR through 2031. Hard FM is expanding faster because clients are giving more weight to building integrity, lifecycle planning, and the coordination of engineering-heavy scopes under one accountable provider. Demand is strongest where aging assets, retrofit requirements, and performance-led maintenance need a deeper technical operating model than basic scheduled servicing. NTT Data’s work at the Mitaka East facility showed that BIM-FM integration can preserve full asset visibility while cutting model data size by 98.8%, which supports broader hard service deployment across large portfolios without a heavy system burden. NTT Facilities and NTT Docomo are also testing conversational AI for building information access, which can reduce the friction of using BIM data in day-to-day FM work and improve the quality of technician responses.

Soft Facility Management remains the foundational volume layer of the Japan IFM market because cleaning, catering, waste management, front-of-house support, and related recurring services are tied to daily building continuity. Even when occupiers tighten budgets, these functions are difficult to defer for long because they directly affect hygiene, occupant experience, and baseline compliance. The segment also fits integrated contracts well because soft services are often the first bundle clients consolidate before they expand into more technical scopes. That creates a practical entry route for providers that want to deepen account coverage over time and turn recurring site presence into larger managed service relationships. In that sense, Soft FM continues to anchor the Japan integrated facility management industry even as Hard FM becomes the faster-growing part of the service mix.

By End-User: Industrial and Manufacturing Leads on Scale While Commercial Advances on Quality of Integration

Industrial and Process Sector accounted for 27.6% of the Japan IFM market size in 2025, while the Commercial segment is expected to grow at a 7.6% CAGR through 2031. Industrial sites lead because automotive plants, electronics facilities, semiconductor operations, and EV battery projects require round-the-clock technical reliability that is difficult to support through fragmented vendor structures. These environments depend on specialized electrical maintenance, precision HVAC control, fire safety management, waste handling, and documented operating procedures that support stronger contract pricing for qualified providers. The supplier pool is naturally narrower in this part of the Japan integrated facility management market, since delivery quality depends on engineering depth and compliance discipline as much as labour availability. That is why industrial contracts remain important for scale operators that want defensible positions in technically demanding accounts.

The Commercial segment is growing faster because office portfolios, telecom facilities, retail sites, travel hubs, and business campuses are moving toward integrated, digitally visible service models. Corporate occupiers are also consolidating into higher-specification buildings where energy monitoring, asset reporting, and service coordination matter more than simple low-cost outsourcing. Facilio’s 2024 deployment at Takenaka Central Building South, which brought seven group companies onto one connected facility platform, reflects this demand for unified digital control at the building level. Other end-user groups still matter to the Japan integrated facility management industry because healthcare and pharmaceutical sites bring strong compliance depth, hospitality creates recurring soft-service volume, and real estate and transportation assets are tied to logistics and occupancy trends. AEON Delight’s expansion of comprehensive contracts into areas such as nationwide accommodation operators and Nagasaki Stadium City also shows that large providers are broadening their account mix rather than relying on one vertical alone.

Geography Analysis

Tokyo and Osaka remain the core demand centers in the Japan IFM market because both cities combine large commercial inventories, major corporate occupiers, and early adoption of digital building systems. Tokyo stands out for aging office stock, dense institutional assets, and a high concentration of clients that prefer consolidated contracts with stronger reporting and lifecycle visibility. It is also the main area where digital-first facility workflows are likely to scale fastest because many large occupiers already use connected building tools, structured vendor governance, and multi-site operating models. Osaka is equally important because it combines a large urban property base with new data center activity that raises the technical bar for integrated service delivery. Nagoya remains relevant because its metropolitan economy links large industrial operations with commercial real estate that benefits from coordinated maintenance, engineering support, and compliance-led building services.

Osaka’s role will likely deepen through 2031 because new capacity in data infrastructure and commercial assets supports more specialized contract demand than standard labour-based FM can handle. Hokkaido and Kyushu are becoming more visible in the geographic profile of the Japan IFM market because data center and industrial expansion corridors are spreading outside the largest traditional metropolitan areas. Fukuoka also appears in the technology rollout pattern as digital managed services expand beyond Tokyo into other urban centers. This broadens the addressable footprint for providers that can standardize operations across multiple regions without losing technical control.

At the national level, the Japan integrated facility management market is shaped by a common regulatory environment that supports integrated delivery where compliance, sanitation, fire safety, and energy performance need to be managed together. That national structure favours providers with consistent process design, strong documentation, and scalable technical oversight across cities and asset types. Regional differences therefore matter less in basic service categories and more in how quickly each area adopts digital tools, specialist hard services, and outcome-based contract models. Tokyo and Osaka are setting the pace, but the wider Japan integrated facility management (IFM) market is gaining depth as industrial corridors, logistics nodes, and new digital infrastructure projects create demand in adjacent prefectures. Over time, geography in this market will be defined less by simple service volume and more by the spread of complex assets that require integrated accountability, data-led maintenance, and energy-aware operations.

Competitive Landscape

The Japan integrated facility management market shows moderate concentration because a relatively small group of scale operators handles many of the more complex multi-site contracts, while a much larger pool of mid-tier and regional firms remains active in single-service and basic bundled work. Domestic groups still hold clear advantages in compliance familiarity, labour network depth, and long-standing relationships with Japanese clients. Global operators, including ISS Facility Services, Compass Group, and Globeship Sodexo, compete most effectively where multinational occupiers want standardized service models and recognized international operating credentials. Even so, the real dividing line in the Japan iIFM market is no longer just service breadth. It is increasingly defined by who owns the digital tools, data architecture, and workflow systems needed to support outcome-based delivery at scale.

AEON Delight is a strong example of this shift because its FY2024 to 2026 plan committed JPY 20 billion (USD 126.0 million) to growth investments, including JPY 12 billion (USD 75.6 million) for digitization, robotics, IoT, and AI. That move signals a deliberate effort to price contracts around service performance and operating reliability rather than labour input alone. NEC Facilities pursued a different route in March 2026 through its alliance with Ugo Inc., using a Robotics-as-a-Service model to deploy autonomous inspection robots without requiring client capital spending. Both approaches point to the same market direction, which is lower dependence on manual execution and stronger differentiation through technology-enabled service assurance.

Facilio’s 2024 rollout at Takenaka Central Building South showed that SaaS-native platforms can win in a conservative operating environment when they reduce integration time and improve building visibility across multiple entities. Japan Kanzai Holdings also responded with its own digital transformation platform in July 2025, underlining that incumbents are not leaving the software layer to new entrants. NTT Facilities adds another competitive dimension because its AI-based BIM query work with NTT Docomo suggests that proprietary building-data architecture may become a contract differentiator in the Japan integrated facility management market, especially where non-specialist staff must manage complex assets efficiently. This means the market is likely to stay moderately concentrated, but the winners within that structure will be the firms that combine compliance strength with repeatable digital execution. Providers that cannot make that transition may still keep smaller accounts, but they will face weaker pricing, lower renewal quality, and less access to technically demanding work in the Japan integrated facility management (IFM) market.

Japan Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Compass Group PLC

ISS A/S

Sodexo S.A.

Jones Lang LaSalle Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NTT Global Data Centers announced plans to double its global capacity to 4 gigawatts within two years, including a new Osaka site, driven by AI workload and cloud migration demand. Over 70% of the expansion projects are already under contract, creating substantial sustained demand for specialized power, cooling, and critical-systems FM services across hyperscale infrastructure in Japan.

- March 2026: NEC Facilities and ugo Inc. formed a strategic alliance to deploy "ugo mini" autonomous mobile robots across NEC Facilities' integrated FM portfolio for facility surveillance, environmental sensing, and routine equipment inspections. The arrangement operates under a Robotics-as-a-Service model, enabling property-level robotic coverage without client capital investment and directly countering the FM sector's deepening labour shortage.

- February 2026: NTT Facilities, in collaboration with Deloitte Touche, published updated non-energy Benefits evaluation metrics covering production facilities, training centers, and government buildings. For a government facility of approximately 36,000 sqm, the total annual benefit reached approximately JPY 259 million (USD 1.63 million), with non-energy Benefits accounting for approximately JPY 221 million (USD 1.39 million), reducing the investment recovery period to approximately one-seventh compared with energy-cost-only analysis and materially improving the financial case for integrated FM-led retrofit programs.

- February 2026: NTT Urban Development deployed Asilla AI security surveillance and human flow analytics across four major office properties, including Urbannet Nagoya Nexta and Shinagawa Season Terrace, integrating 24/7 anomaly detection with occupancy data to optimize cleaning and security scheduling.

Japan Integrated Facility Management Market Report Scope

The Japan Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of Japan integrated facility management in 2026?

The sector stands at USD 32.05 billion in 2026 and is expected to reach USD 44.77 billion by 2031 at a 6.9% CAGR.

Which service category leads revenue in Japan?

Soft FM leads revenue with a 54.4% share in 2025, supported by recurring demand across cleaning, catering, waste management, and related building services.

Which service category is growing the fastest through 2031?

Hard FM is the fastest-growing service area, with a projected 7.7% CAGR through 2031 because clients need stronger support for engineering systems, upgrades, and compliance-heavy maintenance.

Which end-user group contributes the most demand?

Industrial & Manufacturing led with a 27.6% share in 2025 because Japanese plants and advanced production sites require continuous, technical FM support.

Why is the commercial segment expanding quickly?

Commercial demand is rising at a 7.6% CAGR through 2031 as occupiers shift into better-quality buildings and prefer integrated contracts with stronger reporting, energy visibility, and digital control.

What is changing competition among FM providers in Japan?

Competition is moving away from simple service breadth and toward technology ownership, especially in predictive maintenance, connected platforms, robotics, and outcome-based contract delivery.

Page last updated on: