Smoke Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

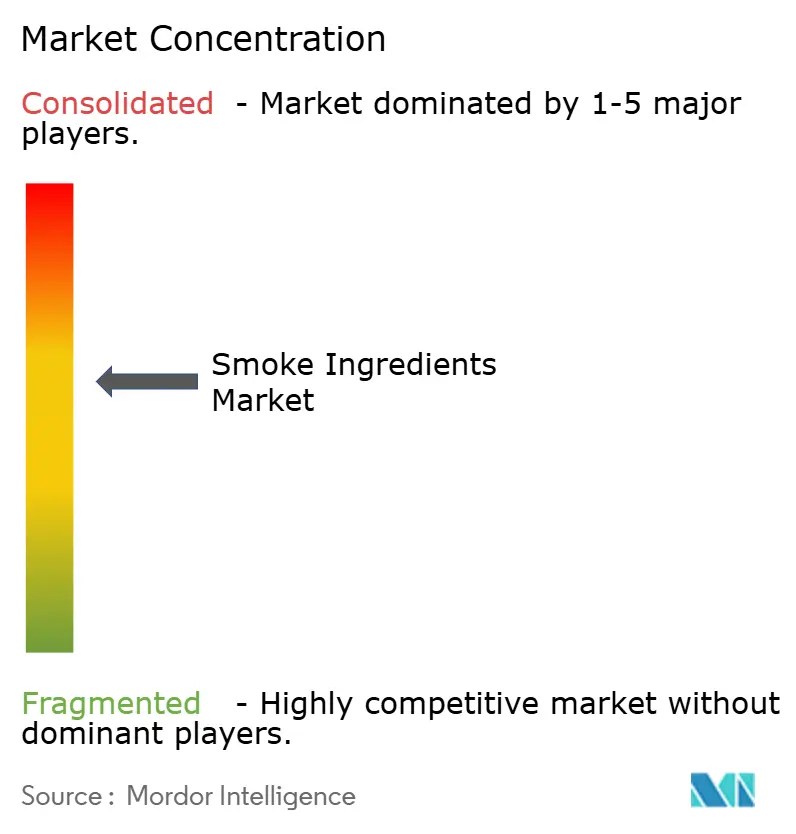

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smoke Ingredients Market Analysis by Mordor Intelligence

Smoke ingredients market size in 2026 is estimated at USD 1.54 billion, growing from 2025 value of USD 1.46 billion with 2031 projections showing USD 2.02 billion, growing at 5.55% CAGR over 2026-2031. Demand is rising as food manufacturers try to recreate the depth of traditional barbecue profiles across snacks, sauces, and plant-based proteins, encouraging steady product launches that showcase wood-specific flavor signatures. Regulatory changes are equally pivotal: Europe’s 2024 withdrawal of eight smoke flavorings is prompting reformulation efforts, while more permissive frameworks in the Asia Pacific support the swift commercialization of novel solutions. Technology investments in low-temperature spray drying and multi-stage purification are reducing thermal degradation of volatiles, yielding cleaner labels and lowering energy costs by more than 30% for leading processors. Parallel growth in plant-based meat analogues is spurring tailored smoke ingredients that mitigate beany or grassy off-notes while providing Maillard-like depth, opening premium pricing territory for suppliers with application-specific expertise.

Key Report Takeaways

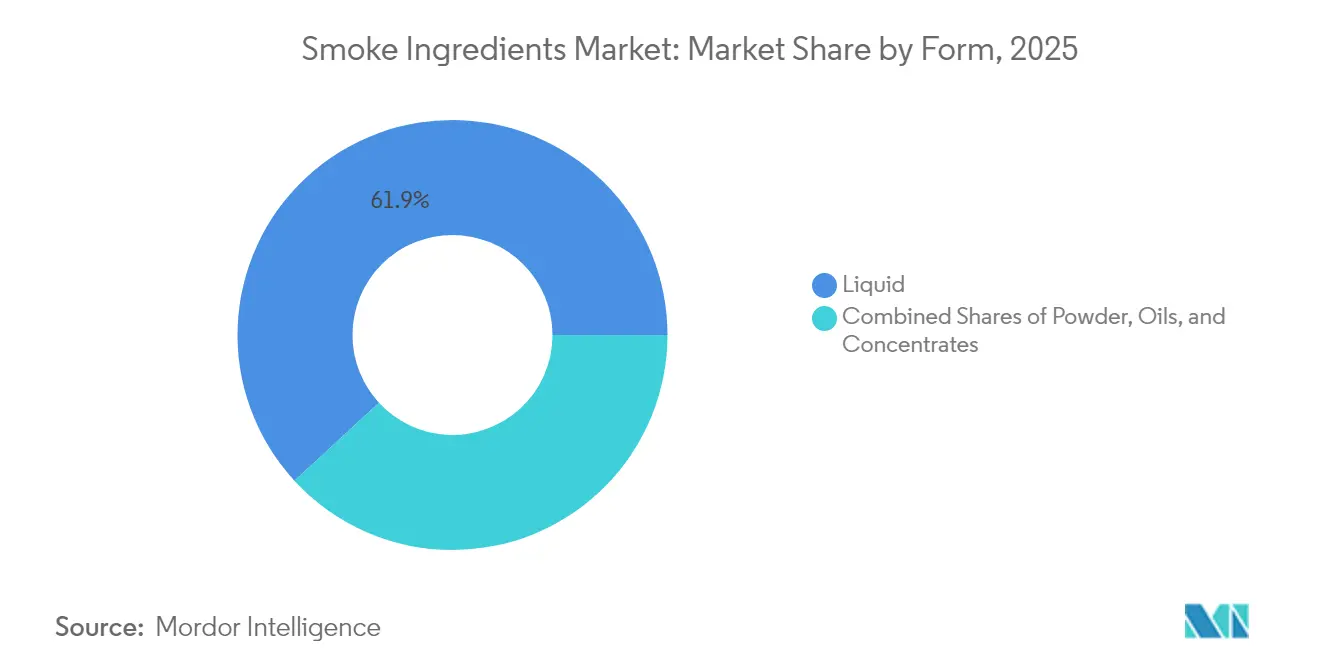

- By form, liquid captured 61.85 % of the smoke ingredients market share in 2025, and powder formats are advancing at a 6.46 % CAGR through 2031.

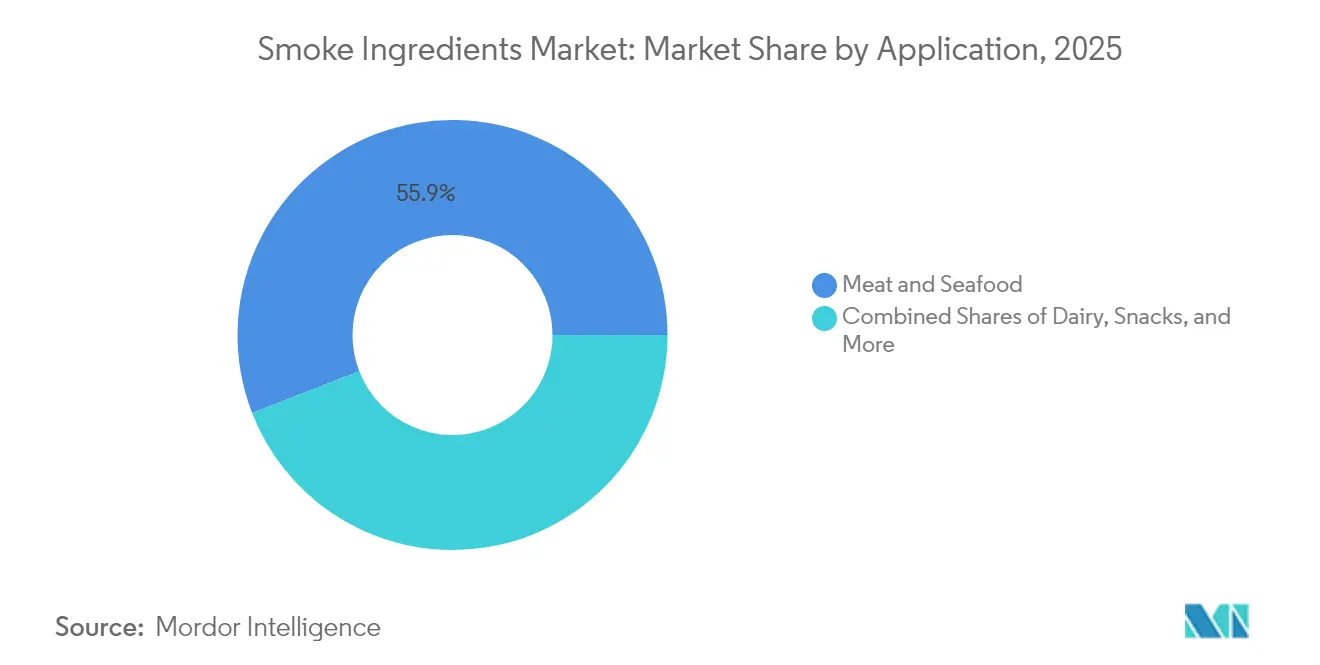

- By application, meat and seafood held a 55.90 % share of the smoke ingredients market size in 2025, while sauces, marinades, and condiments are projected to rise at a 6.76 % CAGR to 2031.

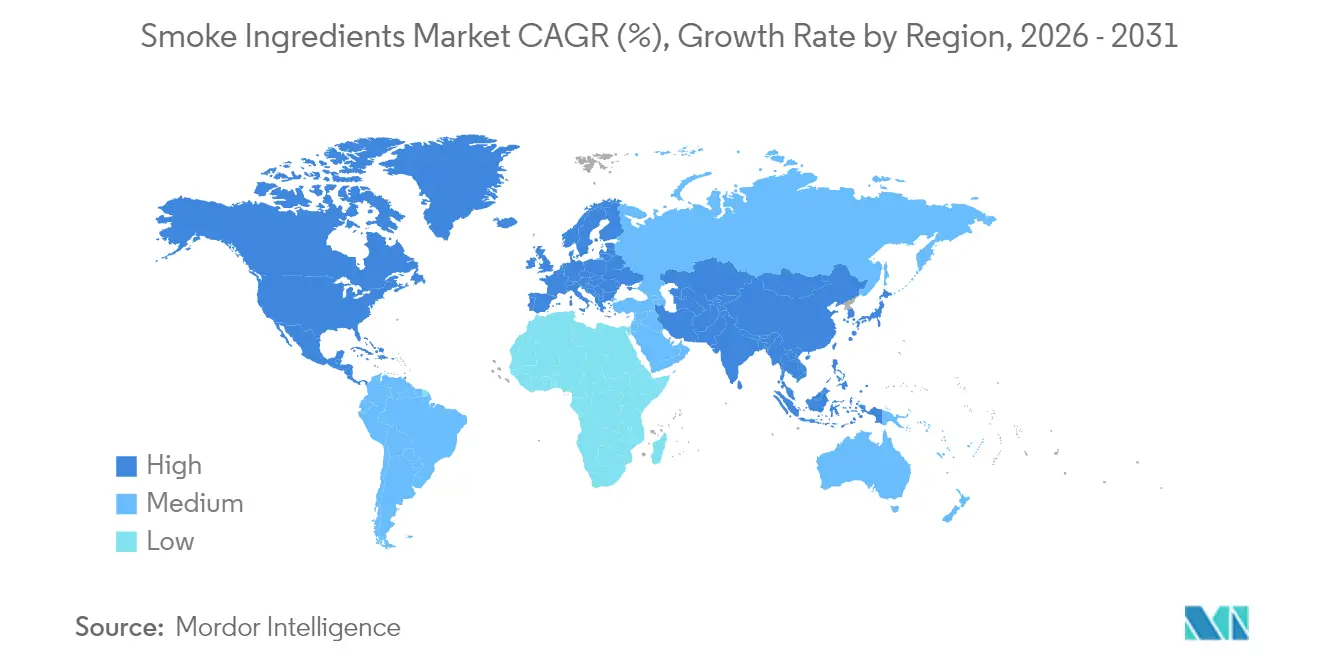

- By geography, North America led with 37.10 % market share in 2025, whereas the Asia Pacific is expected to expand at a 7.14 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smoke Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for authentic smoky flavors | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Innovation in smoking techniques and flavor extraction | +0.9% | Global, led by North America and Europe R&D centers | Long term (≥ 4 years) |

| Shift towards clean-label and natural smoke ingredients | +1.1% | Europe and North America primary, expanding to APAC | Medium term (2-4 years) |

| Growth of plant-based meat analogues needing smoke notes | +0.8% | North America and Europe core, emerging in APAC | Long term (≥ 4 years) |

| Expansion of plant-based and vegan meat alternatives incorporating smoke ingredients | +0.7% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Rising demand for processed and ready-to-eat foods | +1.0% | APAC leading, global expansion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Authentic Smoky Flavors

Consumer demand for authentic smoky flavors is driving significant changes in product development across various food categories, expanding well beyond traditional barbecue applications to include premium snacks, gourmet sauces, and even desserts. This trend highlights a broader shift toward experiential eating, where consumers seek intricate flavor profiles that reflect specific cooking techniques and regional culinary traditions. According to Kerry's 2025 Taste Charts, mesquite and hickory are emerging as key smoke flavors for BBQ sauces, with recommendations for fusion pairings that combine smoky notes with regional spices like garam masala or adobo. The growing sophistication of consumer palates is pushing manufacturers to move past generic "smoke flavor" and adopt wood-specific profiles that provide distinct sensory experiences. This premiumization trend creates opportunities for suppliers offering unique smoke ingredients derived from specific hardwood sources, while presenting challenges for cost-focused competitors relying on standardized formulations.

Innovation in Smoking Techniques and Flavor Extraction

Technological advancements are transforming flavor control and safety in smoke generation and flavor extraction. Besmoke's patented 3-stage PureTech™ Process claims to deliver the "cleanest, safest smoke and grill flavor profiles" using controlled smoking chambers capable of processing over 1,000,000 kg of food ingredients. Similarly, FluidAir's PolarDry electrostatic system, an advanced spray drying technology, operates at temperatures below 90°C. This innovation preserves volatile compounds that typically degrade during conventional processing, enabling manufacturers to maintain consistent flavor intensity while meeting clean-label requirements. Additionally, the integration of digital twin technology with AI-driven spray drying systems is reducing energy consumption by over 30% and enhancing product quality consistency. These advancements provide a competitive edge for suppliers leveraging modern technologies.

Shift Towards Clean-Label and Natural Smoke Ingredients

European markets, influenced by regulatory demands and shifting consumer preferences, are leading the clean-label trend, transitioning from synthetic smoke flavors to naturally-derived alternatives. In January 2025, Sensient Flavors & Extracts introduced SmokeLess Smoke™, a solution designed for manufacturers seeking smoke flavor without traditional smoking methods. The European market's strong emphasis on natural ingredients is opening opportunities for suppliers to provide smoke extracts from specific woods, with a focus on transparent sourcing and processing. Roland Berger's analysis reveals a 7-8% annual growth in natural ingredients, fueled by increasing consumer health awareness and regulatory requirements. This trend is particularly evident in the Asia Pacific and GCC regions, where consumers are favoring natural smoke extracts from woods like hickory and applewood over conventional liquid smoke. Additionally, the European Food Safety Authority's (EFSA) rigorous assessment standards are encouraging manufacturers to adopt naturally-derived alternatives that comply with enhanced safety regulations.

Growth of Plant-Based Meat Analogues Needing Smoke Notes

Plant-based protein manufacturers are refining their methods to replicate traditional meat flavors, with smoke ingredients serving as a key component in creating authentic sensory profiles. Recent research on high-moisture meat analogues emphasizes the complexity of achieving meat-like texture and flavor, highlighting the critical role of smoke ingredients in masking off-notes and delivering familiar taste experiences. This process involves more than just flavor addition; it requires developing complex interactions between smoke compounds and plant proteins to replicate the Maillard reaction products found in cooked meat. Besmoke's PureMami KOKU range addresses this challenge by providing umami and kokumi functionalities derived from smoke volatiles. This solution enables up to a 60% reduction in salt while enhancing meat-like characteristics. The growing technical demands of plant-based applications are driving innovations in encapsulation technologies and controlled-release systems, ensuring consistent smoke flavor intensity throughout the cooking process. As this segment grows, suppliers capable of delivering tailored formulations for specific plant protein matrices are capitalizing on premium pricing opportunities.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter food safety and labeling regulations impacting approval | -0.8% | Europe primary, expanding globally | Short term (≤ 2 years) |

| Health concerns over carcinogenic perception of smoked foods | -0.6% | Global, strongest in developed markets | Medium term (2-4 years) |

| Hardwood supply volatility from forestry & climate policies | -0.5% | Global, concentrated in major forestry regions | Long term (≥ 4 years) |

| Competition from alternative flavour technologies | -0.4% | Global, technology-driven markets leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Food Safety and Labeling Regulations Impacting Approval

Suppliers of smoke ingredients are encountering increasing compliance challenges and market access difficulties due to stricter regulations in major markets. The European Commission's approval of member states' decision to withdraw authorization for 8 smoke flavorings, effective July 2024, highlights a stronger focus on safety assessments, as noted by Food Compliance International[1]Food Compliance International, “Member States endorse withdrawal of smoke flavorings,” foodcomplianceinternational.com. The European Food Safety Authority (EFSA) has revised its methodology, requiring comprehensive chemical composition analyses and genotoxicity evaluations. Importantly, the presence of any genotoxic component in a mixture deems it entirely unacceptable. These regulatory changes are driving manufacturers to make substantial investments in product reformulation and safety testing while facing uncertainties in product approvals. Transition periods vary significantly: traditionally smoked products have until July 2029, whereas other applications must comply by July 2026, adding complexity to inventory management. In the US, the FDA's strengthened post-market assessments for food additives, including the planned revocation of erythrosine (Red No. 3) in January 2025, reflect a similar regulatory tightening. These evolving regulations tend to favor larger companies with strong R&D capabilities, creating obstacles for smaller, specialized suppliers.

Health Concerns Over Carcinogenic Perception of Smoked Foods

Health-conscious consumers are growing increasingly cautious about the potential risks associated with smoked foods, posing challenges for the market. Although liquid smoke contains fewer polycyclic aromatic hydrocarbons (PAHs) than traditional smoking methods, the association of these methods with PAH formation has intensified scrutiny. Furthermore, the European Food Safety Authority (EFSA) has identified certain smoke flavorings, such as furan-2(5H)-one and catechol, as genotoxic substances, stating that no concentration level is safe. These health concerns are driving the demand for "smokeless smoke" alternatives, which offer the desired flavor without combustion byproducts. However, the challenge lies not only in developing these products but also in educating consumers and marketing them effectively. Manufacturers must carefully balance delivering authentic smoke flavor with promoting health-conscious options. Additionally, the cautious regulatory stance of health authorities is reinforcing consumer concerns, particularly in premium segments where health considerations play a significant role in purchasing decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominance Faces Powder Innovation

In 2025, liquid smoke ingredients accounted for a significant 61.85% market share, highlighting their established role in traditional smoking applications and their easy adaptability to food processing systems. Meanwhile, powder formats are witnessing rapid growth, with a 6.46% CAGR projected through 2031. This growth is driven by advancements in spray drying technology and the benefits of clean-label positioning. The expansion of the powder segment reflects manufacturers' preference for ingredients offering extended shelf life, lower shipping costs, and easier handling in dry blend formulations.

Advancements in spray drying, such as PolarDry's electrostatic technology, are enhancing the capabilities of powder smoke ingredients. This method processes at temperatures below 90°C, preserving volatile compounds. Although oil and concentrates represent the smallest segment, they cater to specialized applications requiring intense flavor delivery or specific solubility properties. Form segmentation is increasingly guided by application-specific needs rather than cost alone, with liquid formats retaining advantages in large-scale food processing and powders gaining popularity in convenience foods and seasoning applications. Regulatory factors are influencing form choices, as powder formats often enable cleaner label declarations and simpler ingredient statements compared to liquid formulations that may require stabilizers and preservatives.

By Application: Sauces Drive Growth Beyond Traditional Meat

In 2025, the meat and seafood segment holds a dominant 55.90% market share. However, sauces, marinades, and condiments are emerging as the fastest-growing applications, with a projected 6.76% CAGR through 2031. This growth highlights the premiumization of condiment categories and the expanding use of smoke flavors in various culinary applications beyond traditional proteins. Additionally, plant-based meat alternatives are rapidly gaining traction, requiring specialized smoke formulations to mask off-notes and deliver authentic meat-like flavors.

The dairy and bakery sectors are witnessing steady growth as manufacturers incorporate smoke ingredients to differentiate flavors in premium product lines. In the snacks segment, consumer demand for bold and experiential flavors drives the use of smoke ingredients to stand out in competitive markets. Beverages, particularly craft spirits and specialty non-alcoholic drinks, are adopting smoke flavors to create complex flavor profiles. According to the UNESDA data from 2024, annual consumption of non-alcoholic beverages in the United Kingdom was 15,496.9 million liters. However, this diversification introduces technical challenges, such as ingredient compatibility and processing conditions, which favor suppliers with strong expertise and customization capabilities. Kerry's expansion into personal care ingredient distribution through its LBB Specialties partnership underscores the potential for smoke-derived compounds in non-food applications.

Geography Analysis

In 2025, North America commands a 37.10% market share, underscoring its rich barbecue heritage and advanced food processing capabilities. Yet, the region grapples with regulatory challenges and a shift towards health-conscious consumer trends. North America boasts established supply chains for hardwood feedstocks and cutting-edge flavor extraction technologies. Notably, Kerry is amplifying its Cedar Rapids facility to boost production. However, the FDA's intensified scrutiny on food additives and its broader chemical oversight injects regulatory ambiguity, potentially curbing growth in contrast to more lenient markets. Highlighting its commitment to safety and innovation, the USDA has updated its safe ingredients list for meat, poultry, and egg products.

Asia Pacific is on a growth trajectory, boasting a 7.14% CAGR through 2031, fueled by swift urbanization, a burgeoning middle class, and a rising appetite for processed foods. Thailand's ready-to-eat sector exemplifies this growth, with domestic consumption set to rise 3-4% annually and exports by 5-6%. This surge amplifies the demand for smoke ingredients in instant noodles and ready meals. Clean-label trends are gaining traction, with consumers gravitating towards natural smoke extracts from woods like hickory and applewood, steering away from traditional liquid smoke. Moreover, Asia Pacific's regulatory landscape is more lenient than Europe's, facilitating quicker product launches for innovative smoke solutions.

Europe grapples with stringent regulations, especially after EFSA revoked authorization for 8 smoke flavorings. Yet, this scenario opens doors for suppliers who can navigate the heightened safety standards and offer naturally-derived alternatives. Transition periods—extending to July 2029 for traditionally smoked products and July 2026 for others—are spurring reformulation efforts, granting a competitive edge to compliant companies. Despite these hurdles, European consumers are willing to pay a premium for certified natural ingredients and transparent sourcing. Meanwhile, the UK's move to drop renewal requirements for smoke flavorings could spark competitive shifts within the European landscape.

Competitive Landscape

The smoke ingredients market is moderately consolidated. This landscape allows room for both large-scale efficiency maneuvers and niche innovation strategies. Major players are optimizing their portfolios through strategic divestitures. For instance, IFF divested its Savory Solutions Group for a hefty USD 900 million and its Flavor Specialty Ingredients segment for USD 220 million, redirecting its focus to core growth areas. On another front, consolidation is gaining momentum through targeted acquisitions.

Kerry made headlines with its USD 853 million acquisition of Niacet, bolstering its food preservation capabilities. Meanwhile, NovaTaste's acquisition of McClancy Foods & Flavors marks its strategic entry into the US QSR foodservice segment. Technology differentiation is becoming a pivotal competitive edge. Companies are channeling investments into proprietary processing methods and clean-label formulations, navigating both regulatory challenges and evolving consumer preferences.

Notably, patent activity in smoking device technologies underscores a wave of innovation in delivery systems and filtration methods, potentially reshaping ingredient formulation requirements. The competitive arena increasingly rewards firms that can offer regulatory-compliant, naturally-derived solutions without compromising on cost across varied application segments. Promising opportunities lie in plant-based applications demanding specialized formulations, expanding into the Asia Pacific market, and pioneering "smokeless smoke" alternatives that promise authentic flavor sans traditional combustion byproducts.

Smoke Ingredients Industry Leaders

Kerry Group

Azelis Holdings

International Flavors & Fragrances, Inc.

Essentia Protein Solutions

Sensient Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: French plant extract manufacturer Plantex introduced Smok’EXTRACT, an innovative natural smoke flavouring designed as a safe and aromatic alternative to traditional smoke flavourings containing harmful polycyclic aromatic hydrocarbons (PAHs).

- June 2024: I.T.S has launched a range of ‘smoke-free’ natural smoke flavorings as a compliant alternative for food and beverage manufacturers. These new natural flavors allow producers to legally incorporate smoky aromas without the need for complex on-pack labelling declarations, facilitating clean-label appeal.

- January 2023: Azelis Holdings acquired Smoky Light B.V., an ingredients distributor in the BENELUX region. For the food and nutrition industries, Smoky Light B.V. provides smoke, grill, cooking flavors, browning agents, and additives. With this acquisition, Azelis aims to increase its market share in the Benelux region as well as throughout Europe, the Middle East, and Africa for smoke ingredients.

Global Smoke Ingredients Market Report Scope

Smoke ingredients are food elements added to foods to flavor meat or vegetables. They are generally made by condensing the smoke from wood without any food additives. The smoke ingredients market is segmented by foam, application, and geography. Based on foam the market is segmented into liquid, powder, and other foams. On the basis of application market is segmented into dairy, bakery and confectionery, meat and seafood, and snacks and sauces. Further, the market is segmented by geography into North America, Europe, Asia-Pacific, South America, Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of the value (in USD million).

| Liquid |

| Powder |

| Oil & Concentrates |

| Meat & Seafood |

| Plant-based Meat Alternatives |

| Dairy Products |

| Bakery & Confectionery |

| Snacks |

| Sauces, Marinades & Condiments |

| Beverages |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | Japan |

| India | |

| China | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Liquid | |

| Powder | ||

| Oil & Concentrates | ||

| By Application | Meat & Seafood | |

| Plant-based Meat Alternatives | ||

| Dairy Products | ||

| Bakery & Confectionery | ||

| Snacks | ||

| Sauces, Marinades & Condiments | ||

| Beverages | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | Japan | |

| India | ||

| China | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the smoke ingredients market in 2026?

The smoke ingredients market size is USD 1.54 billion in 2026 and is forecast to reach USD 2.02 billion by 2031.

Which region shows the fastest growth for smoke flavor demand?

Asia Pacific is projected to advance at a 7.14 % CAGR through 2031, driven by urbanization and processed food uptake.

What application segment is gaining share most quickly?

Sauces, marinades, and condiments are expanding at a 6.76 % CAGR as brands premiumize everyday condiments with smoky notes.

Why are powders outperforming liquids in some categories?

Low-temperature spray drying yields cleaner labels, longer shelf life, and lower freight costs, supporting a 6.46 % CAGR for powders.

Page last updated on: