Heart Health Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

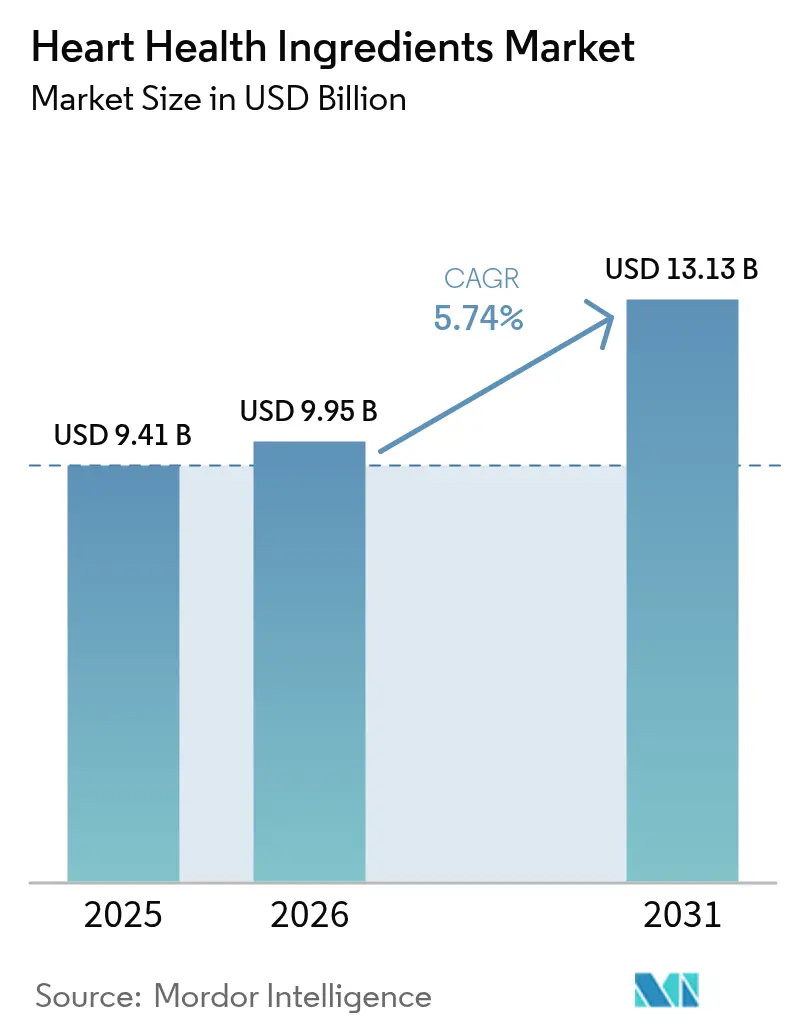

| Market Size (2026) | USD 9.95 Billion |

| Market Size (2031) | USD 13.13 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

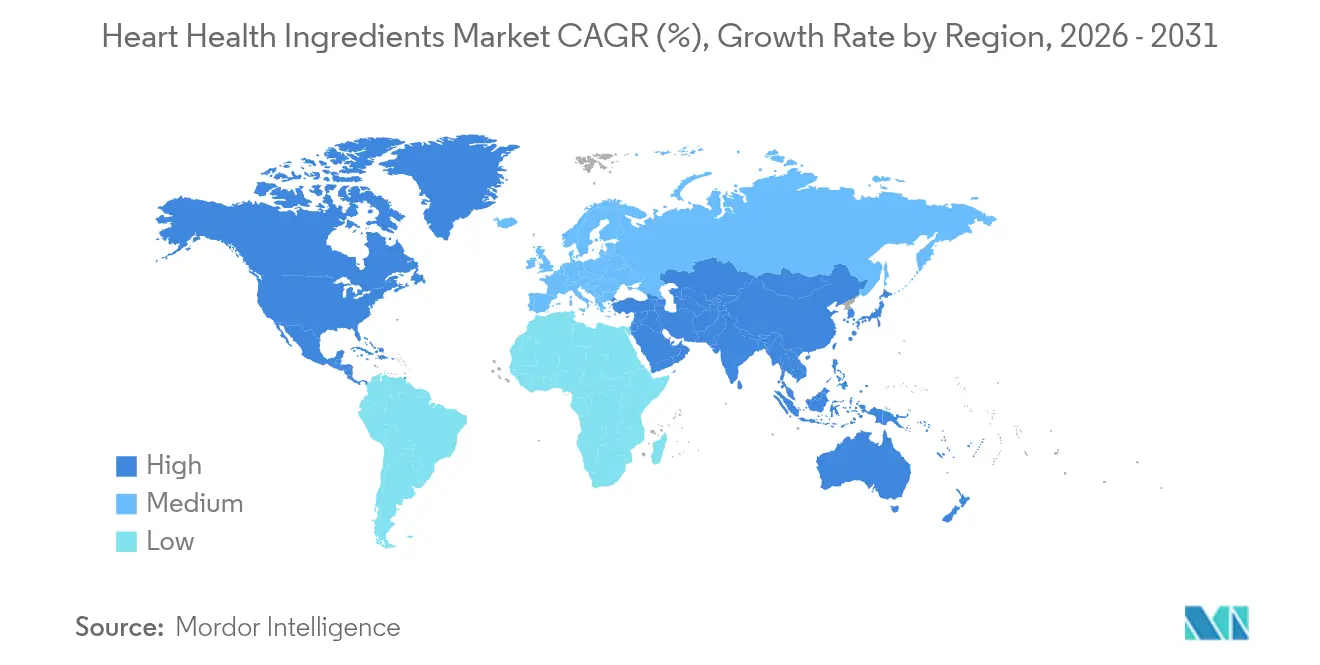

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Heart Health Ingredients Market Analysis by Mordor Intelligence

The Heart Health Ingredients Market size was valued at USD 9.41 billion in 2025 and estimated to grow from USD 9.95 billion in 2026 to reach USD 13.13 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). The market expansion is primarily attributed to demographic transitions, enhanced regulatory frameworks, and technological advancements in ingredient development and processing. According to the American Heart Association's comprehensive analysis, cardiovascular disease is expected to affect 61% of United States adults by 2050, with projected healthcare costs approaching USD 1.8 trillion. This substantial disease burden has intensified the focus on preventive nutrition solutions, particularly heart health ingredients, across the pharmaceutical and nutraceutical industries. The market growth is further propelled by the rising adoption of functional foods and dietary supplements, and the growing aging population worldwide. Additionally, the development of innovative ingredient formulations and increased research and development investments in heart-healthy compounds contribute to market expansion.

Key Report Takeaways

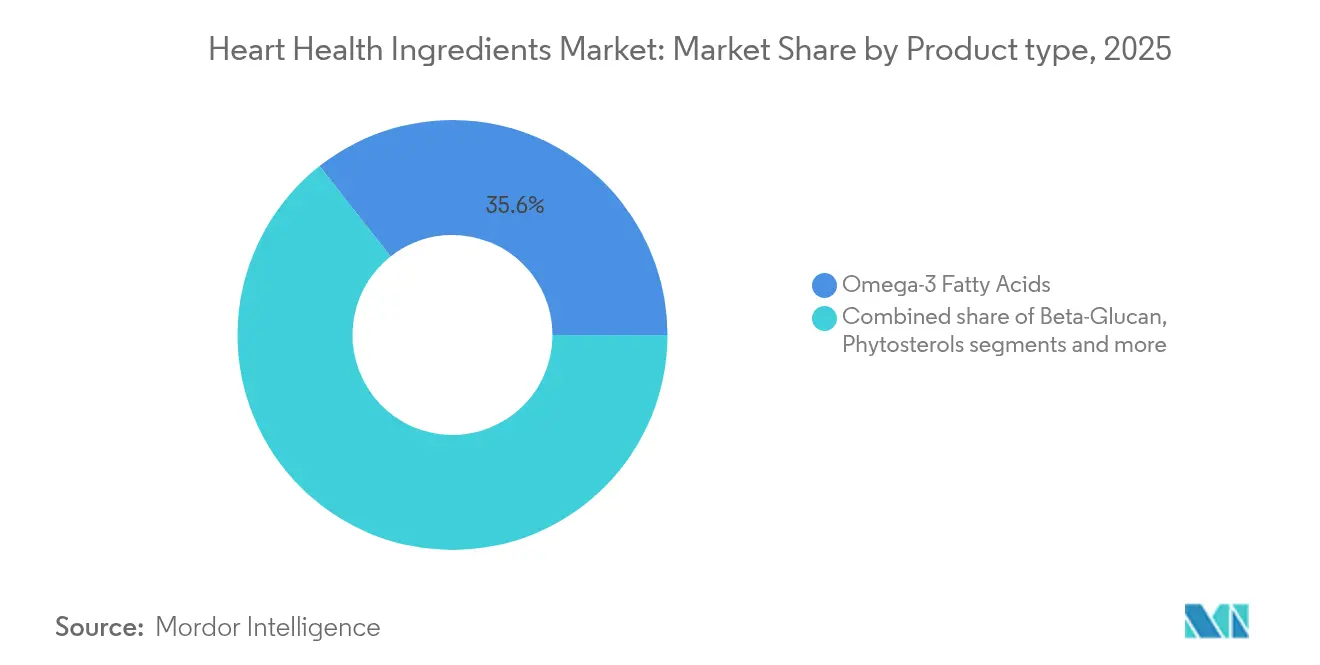

- By ingredient type, Omega-3 fatty acids held 35.62% of the heart health ingredients market share in 2025, while Coenzyme Q10 is projected to expand at a 6.86% CAGR to 2031.

- By source, plant-based inputs led with 55.94% revenue share in 2025; algae-derived alternatives are forecast to rise at a 7.03% CAGR through 2031.

- By form, powder formulations accounted for 60.35% of the heart health ingredients market size in 2025, whereas liquids are growing at a 7.44% CAGR to 2031.

- By application, dietary supplements captured 50.68% share of the heart health ingredients market size in 2025, and functional food and beverages are set to expand at a 6.77% CAGR by 2031.

- By geography, North America held 37.98% revenue in 2025; Asia-Pacific is advancing at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heart Health Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular diseases globally | +1.2% | Global, with highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Increasing aging population and associated heart health concerns | +1.0% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Growing consumer awareness about preventive healthcare | +0.8% | North America and the European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of heart health ingredients in everyday food products | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government initiatives promoting heart health awareness | +0.5% | North America, the European Union, with emerging programs in Asia-Pacific | Short term (≤ 2 years) |

| Increased focus on personalized nutrition | +0.4% | North America and the European Union primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of cardiovascular diseases globally

Cardiovascular diseases (CVDs) represent a significant global health challenge, driving substantial growth in the heart health ingredients market. These diseases, which include coronary artery disease, stroke, and hypertension, are the primary cause of mortality worldwide. The prevalence of CVDs has increased due to sedentary lifestyles, unhealthy dietary habits, tobacco use, and rising rates of obesity and diabetes. As consumers become more aware of these health risks, they increasingly seek heart-healthy products, including functional foods, dietary supplements, and nutraceuticals. These products contain beneficial ingredients, including omega-3 fatty acids, phytosterols, fiber (beta-glucan), and antioxidants such as polyphenols, which help manage cholesterol levels, blood pressure, and overall cardiovascular health. The World Health Organization (WHO) data illustrates the magnitude of this health crisis, with cardiovascular diseases causing approximately 338,000 deaths in Germany, 222,700 in Italy, and 161,200 in Poland as of 2023 [1]Source: World Health Organization (WHO), "Deaths by sex and age group for a selected country or area and year", www.who.int. These statistics, even from countries with sophisticated healthcare systems, have prompted governments and health organizations worldwide to emphasize the importance of preventive healthcare measures.

Increasing aging population and associated heart health concerns

The aging global population drives the demand for heart health ingredients as older adults face higher cardiovascular risks and seek preventive healthcare solutions. Key factors influencing this trend include increased life expectancy, lower birth rates, and medical advancements. In 2023, Japan reported the highest proportion of people aged 65 years or above at 30% of its population, followed by Italy at 24%, according to World Bank data [2]Source: World Bank, "Population ages 65 and above (% of total population)", www.worldbank.org. The older demographic demonstrates higher supplement consumption and increased investment in preventive health measures, creating a strong market for evidence-based heart health ingredients. This age group also shows greater engagement with regular health screenings and preventive care protocols. Population forecasts indicate similar aging patterns across developed markets, with the 65+ age group expected to double by 2050 in many regions due to improved healthcare infrastructure and lower mortality rates.

Growing consumer awareness about preventive healthcare

The global heart health ingredients market is primarily driven by increasing consumer awareness of preventive healthcare. With cardiovascular diseases remaining the leading cause of death and rising healthcare costs, consumers are transitioning from reactive treatment approaches to preventive health strategies. This transformation stems from improved access to health information, enhanced nutritional education, and a broader societal emphasis on wellness and longevity. Government and public health organizations worldwide strengthen this preventive approach through policy initiatives and educational programs. The United States Food and Drug Administration (FDA) and international health ministries provide dietary guidelines recommending omega-3 fatty acids, whole grains, fruits, vegetables, and lean proteins, while approving specific health claims for heart health ingredients on product labels. Additionally, organizations like the CDC Foundation implement targeted campaigns, such as "Live to the Beat," which focuses on cardiovascular disease prevention among Black adults, and support the Million Hearts initiative to reduce heart attacks and strokes nationwide.

Integration of heart health ingredients in everyday food products

The incorporation of heart health ingredients into mainstream food and beverage products has expanded beyond traditional supplement formats, increasing market accessibility and regular consumption. Food manufacturers integrate these ingredients to comply with regulations and meet consumer health preferences. For instance, beta-glucan fortification in everyday foods offers opportunities to enhance dietary fiber intake. The fortification of plant-based beverages with omega-3 fatty acids addresses nutritional requirements while aligning with sustainability preferences, especially among vegetarian and vegan consumers. Regulatory frameworks support this integration through approved health claims for soluble fiber and plant sterols, providing market advantages for compliant products. Advancements in encapsulation and delivery systems improve ingredient stability and bioavailability across various food matrices, enabling broader product development opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from conventional pharmaceutical products | -0.8% | Global, strongest in developed markets with established pharma presence | Long term (≥ 4 years) |

| Stringent regulatory requirements for ingredient approval and health claims | -0.6% | The European Union and North America primarily, expanding globally | Medium term (2-4 years) |

| Limited Consumer Awareness in Developing Regions | -0.4% | Asia-Pacific emerging markets, Latin America, Africa | Medium term (2-4 years) |

| Side Effects and Safety Concerns | -0.3% | Global, heightened in regulated markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from conventional pharmaceutical products

Healthcare providers and consumers prefer drug therapies over nutritional interventions for managing cardiovascular risks. Medical professionals choose proven cardiovascular medications with clear dosing protocols, especially for high-risk patients who need immediate treatment. Bayer's KERENDIA (finerenone), approved by the FDA in 2025 for heart failure treatment, reduced cardiovascular death and heart failure events by 16%, showing how pharmaceuticals compete with nutritional approaches. Insurance companies cover pharmaceutical treatments more readily than nutritional supplements, which creates cost barriers for consumers interested in heart health ingredients. Drugs must undergo extensive Phase III trials, while supplements need only observational studies and smaller clinical trials. However, increasing focus on preventive healthcare and high cardiovascular treatment costs creates opportunities for heart health ingredients to serve as complementary therapies rather than primary treatments.

Stringent regulatory requirements for ingredient approval and health claims

Regulatory complexity affects market entry and innovation as manufacturers must comply with evolving approval processes and health claim requirements across global markets. The European Food Safety Authority's (EFSA) updated guidance for novel food applications, effective February 2025, implements stricter requirements for microorganism-related foods, production processes, and toxicological assessments. The Food and Drug Administration (FDA) has increased scrutiny of heart health supplements, issuing warning letters to companies making unauthorized disease claims about cholesterol and blood pressure management. EFSA's evaluation of red yeast rice monacolins exemplifies ongoing safety assessments that affect ingredient availability and market access. Small manufacturers face higher compliance costs, which create barriers to innovation and market entry while benefiting established companies with regulatory expertise. The differences in regulatory standards between regions affect global product development and marketing strategies, necessitating region-specific formulations and claims documentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Omega-3 Dominance Drives Innovation

Omega-3 fatty acids hold a dominant 35.62% market share in 2025, supported by strong consumer awareness and extensive clinical research validating their cardiovascular benefits. Coenzyme Q10 shows the highest growth potential with a projected CAGR of 6.86% through 2031, supported by research in heart failure treatment and cellular energy production. Beta-glucan maintains consistent market growth, supported by Food and Drug Administration (FDA) approved health claims for LDL cholesterol reduction . Phytosterols benefit from regulatory support, with approved coronary heart disease risk reduction claims in the United States and European Union.

Protein ingredients, including plant and dairy sources, show increasing demand among older consumers for their dual benefits in muscle maintenance and cardiovascular health. Technological developments in bioavailability enhancement and delivery systems are improving product effectiveness and user compliance. For instance, in October 2024, DSM-Firmenich launched Life's DHA B54-0100, an omega-3 formulation containing 545 mg of DHA per gram, enabling reduced capsule sizes to address consumption challenges in omega-3 supplementation.

By Source: Plant-Based Leadership Meets Algae Innovation

Plant-based sources hold a 55.94% market share in 2025, as consumers increasingly prefer sustainable and familiar ingredient origins. Algae-based alternatives show significant growth potential with a projected 7.03% CAGR through 2031. Animal-based sources experience declining preference due to sustainability concerns and dietary restrictions, though they remain important for applications requiring specific bioavailability profiles. Marine-derived ingredients show varied performance, with traditional fish oil facing sustainability challenges while algae cultivation emerges as an environmentally sustainable alternative.

The transition to algae-based sources marks a significant change in omega-3 production, addressing sustainability and quality requirements. Schizochytrium cultivation produces high DHA concentrations in controlled environments, eliminating risks of marine biotoxins and heavy metal contamination. Plant-based ingredient development continues to expand, with Tiger nut oil receiving European Food Safety Authority (EFSA) approval for its oleic acid content and cardiovascular benefits.

By Form: Powder Convenience Versus Liquid Bioavailability

Powder formulations dominate the global heart health ingredients market, holding a 60.35% market share in 2025. This dominance stems from their manufacturing efficiency, extended shelf stability, and consumer acceptance across functional foods and supplements. Powders provide versatility in product development, enabling integration into beverages, meal replacements, and sachet-based supplements. The advancement of technologies like liquisolid systems addresses solubility challenges for fat-soluble heart health compounds, including Coenzyme Q10 and omega-3 fatty acids. These systems convert poorly soluble liquids into dry, free-flowing powders, improving dissolution rates and therapeutic efficacy for enhanced bioavailability and consistent cardiovascular benefits.

Liquid formulations represent the fastest-growing segment, with a projected CAGR of 7.44% through 2031. This growth reflects increasing demand for fast-acting, easily absorbed formats, particularly among seniors and health-conscious consumers seeking immediate benefits from heart-healthy ingredients such as omega-3s and botanical extracts. Liquids offer enhanced bioavailability and faster onset of action, making them suitable for functional beverages, emulsions, and concentrated shots.

By Application: Supplements Lead While Functional Foods Accelerate

Dietary supplements dominate the global heart health ingredients market with a 50.68% market share in 2025. This leadership position stems from established consumer purchasing patterns and clinical marketing efforts over decades. The segment's success is attributed to clear labeling, precise dosing, and extended shelf-life, making it particularly appealing to older adults and individuals managing conditions like high cholesterol or hypertension. The regulatory environment in numerous countries supports this dominance by allowing structure/function claims for cardiovascular wellness without requiring pharmaceutical-level approvals. These factors establish supplements as the market's foundation, characterized by strong consumer loyalty and accessible product development opportunities.

Functional foods and beverages demonstrate significant growth potential, with a projected CAGR of 6.77% through 2031. Manufacturers are integrating heart health ingredients into common food items, including fortified cereals, dairy products, juices, and snack bars. This integration reflects the growing consumer preference for incorporating health management into daily nutrition. The pharmaceutical segment maintains steady growth through prescription and over-the-counter (OTC) formulations for heart failure, hypertension, and hyperlipidemia. These medical applications utilize ingredients such as CoQ10, niacin, and EPA/DHA, adhering to stringent quality and efficacy standards.

Geography Analysis

North America holds 37.98% market share in 2025, supported by clear regulations, robust healthcare systems, and high public awareness of cardiovascular health risks. Companies like Cargill and Archer Daniels Midland Company utilize the region's manufacturing capabilities and regulatory expertise for global distribution. However, market maturity and increased regulatory oversight limit growth opportunities beyond traditional supplement markets.

Asia-Pacific registers the highest growth rate at 7.08% CAGR through 2031, driven by increasing cardiovascular disease incidence and growing middle-class healthcare expenditure. Regional health challenges, including air pollution, changing dietary patterns, and high hypertension rates, increase ingredient demand across multiple applications. The region expands manufacturing capacity through strategic partnerships, while regulatory alignment efforts improve market access for global suppliers.

Europe maintains consistent growth, supported by strict regulations that boost consumer trust in heart health ingredients while restricting unproven products. The region's aging population and comprehensive healthcare systems promote preventive nutrition adoption, especially in Nordic countries with developed functional food markets. Post-Brexit regulatory differences require manufacturers to comply with separate European Union and United Kingdom frameworks. Additionally, the European Union Deforestation Regulation (EUDR) influences ingredient sourcing practices across the food and supplement sectors.

Regulatory Landscape

Heart health ingredients are shaped by health-claim and labeling regimes that define ingredient-specific eligibility thresholds and constrain cardiovascular risk positioning. In the United States, FDA-authorized health claims for coronary heart disease risk reduction include prescriptive daily intake criteria for qualifying ingredients, such as plant sterol/stanol esters under 21 CFR 101.83, which influences formulation choices and the label language used for functional foods and dietary supplements.

In Europe, the policy direction has tightened around safety and claim substantiation for certain bioactives. Regulation (EU) 2024/2041 (July 2024) revoked an authorized health claim related to monacolin K from red yeast rice due to safety concerns, affecting product availability and reformulation decisions. Separately, EFSA guidance updates for novel food applications effective February 2025 increased documentation and assessment requirements, notably for microorganism-related foods and processes. In the United States, the criteria for the voluntary use of the implied nutrient content claim "healthy" were updated in 2025, raising the compliance bar for heart-health positioned foods that rely on front-of-pack and nutrient-content messaging.

Value Chain Analysis

The value chain runs from raw material production (marine, algae, and plant inputs) to ingredient processing and purification (omega-3 concentration, beta-glucan extraction, and phytosterol/stanol isolation). It then extends into formulation and stabilization, including encapsulation, emulsions, and powder systems, before flowing into downstream dietary supplements and functional food and beverage products. Large ingredient suppliers and blenders provide standardized actives, while brand owners and contract manufacturers convert them into consumer formats, with labeling and health-claim compliance, such as FDA plant sterol ester claim thresholds in 21 CFR 101.83 and EU plant sterol/stanol use conditions in Regulation (EC) No 983/2009 and Regulation (EU) No 686/2014, acting as practical handoffs that shape specifications, QC, and documentation.

Risk and cost points concentrate in global logistics and single-site dependencies for certain nutrition inputs. Red Sea shipping diversions have been ongoing since late 2023, lengthening transit times and tightening container availability, which complicates inventory planning for imported bioactives and specialty oils. In parallel, BASF declared force majeure on vitamin A, vitamin E, and carotenoids following an August 2024 incident at its Ludwigshafen site, with restoration timelines extending into 2025. This has reinforced the need for alternative sourcing, safety stocks, and regionally diversified processing for heart-health adjacent fortification systems.

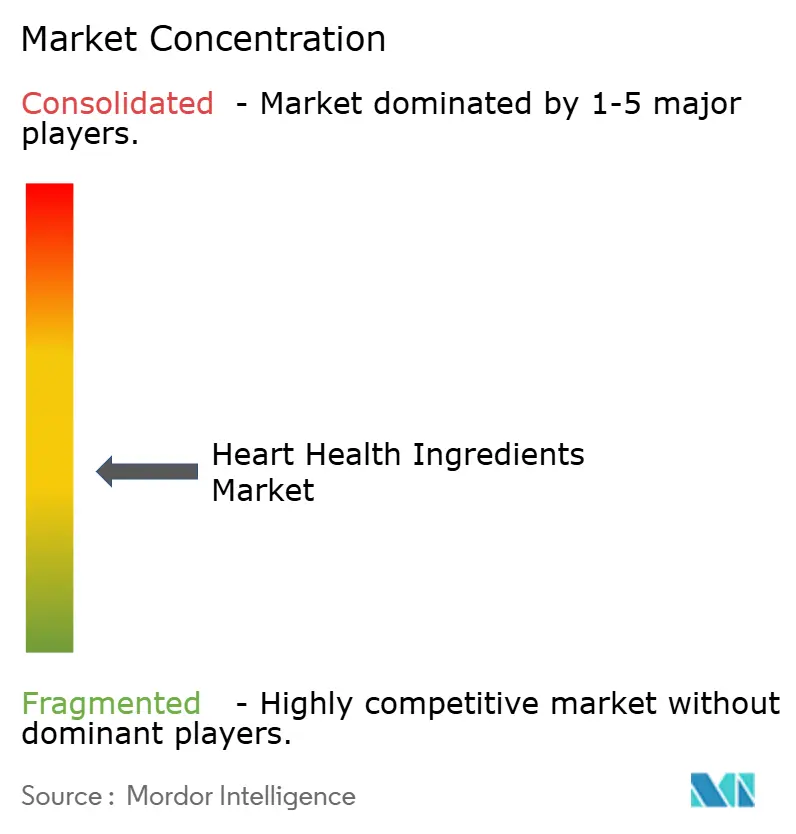

Competitive Landscape

The food ingredients market displays moderate fragmentation, with established suppliers holding market leadership through integrated operations, regulatory compliance, and technological advancement. Key companies, including Cargill Incorporated, DSM-Firmenich AG, Archer Daniels Midland Company, BASF, and Kerry Group, maintain their competitive position through global manufacturing networks and research investments. Industry consolidation continues, as demonstrated by Tate & Lyle's USD 1.8 billion acquisition of CP Kelco in November 2024, strengthening its position in specialty food solutions and natural ingredients portfolios.

Companies focus on technology-driven differentiation through investments in artificial intelligence for nutrition solutions, delivery systems, and sustainable production methods. The market participants prioritize bioavailability enhancement, sustainable sourcing practices, and application-specific formulations to meet consumer preferences and regulatory requirements. Significant market opportunities exist in personalized nutrition platforms, algae-based ingredient production, and expansion into emerging markets with developing regulatory frameworks.

Specialized companies target niche market segments through innovative extraction methods, new ingredient sources, and focused application development. These organizations face challenges in scaling production capabilities and managing regulatory compliance across global markets. The competitive environment continues to evolve as companies adapt to regulatory changes and market demands while maintaining operational efficiency and product development initiatives.

Heart Health Ingredients Industry Leaders

-

Cargill, Incorporated

-

DSM-Firmenich AG

-

Archer Daniels Midland Company

-

BASF SE

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A central opportunity lies at the intersection of clinically supported actives and region-specific claim permissions, enabling differentiated heart-health positioning in everyday foods. FSANZ approval in April 2026 of a new heart health claim for isolated soy protein, tied to daily consumption of 20-25 g, gives manufacturers in Australia and New Zealand a concrete pathway to translate protein fortification into cholesterol-related messaging without relying on supplement-only formats.

Suppliers also have room to build portfolios around biomarker-focused evidence and branded ingredients that can be applied across multiple categories. In June 2026, Gnosis by Lesaffre reported two-year clinical results showing that its MenaQ7 vitamin K2 (MK-7) slowed coronary artery calcification progression by 29%, supporting premium positioning for vitamin K2 in cardiovascular wellness stacks. Product platforms that place bioactives into familiar carriers are also broadening in-market, including New Zealand functional dairy positioning (for example, Four Leaves Co. activity in 2026), which expands routes to consumption beyond capsules and softgels while keeping claims and sensory constraints in view.

Recent Industry Developments

- April 2026: IFF secured the first heart health claim for isolated soy protein in Australia and New Zealand following FSANZ approval, enabling qualifying foods to link daily soy protein intake to heart-health related benefits. The decision creates a new, regulator-backed route for mainstream food and beverage brands to build cardiovascular positioning around protein fortification, not only around oils and fibers.

- September 2025: BASF and Louis Dreyfus Company completed the transaction for BASF’s Food and Health Performance Ingredients business, transferring a portfolio that includes plant sterols, CLA, and omega-3 oils. The completed sale reorganizes supply relationships for formulators and brand owners that source these actives, and it reinforces portfolio specialization among large ingredient players.

- July 2024: DSM-Firmenich divested its marine lipids omega-3 fish oil business, including the MEG-3 brand and facilities in Peru and Canada, to KD Pharma Group. The deal consolidated omega-3 manufacturing assets under a specialist producer, influencing capacity access, quality systems, and long-term supply contracting for EPA/DHA ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the sales value of ingredients formulated and marketed for heart health benefits, and then used in dietary supplements and functional food and beverage products across major regions.

Scope exclusions: Finished branded supplement products and finished foods are excluded, and only the ingredient value at the point of ingredient sale is counted.

Segmentation Overview

-

By Type

- Omega-3 Fatty Acids

- Beta-Glucan

- Phytosterols

- Protein

- Coenzyme Q10

- Others

-

By Source

- Plant-based

- Animal-based

- Algae-based

- Others

-

Form

- Powder

- Liquid

- Others

-

By Application

- Dietary Supplements

- Functional Food and Beverage

- Pharmaceuticals

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the ingredient universe used for heart health claims, then aligning it with how ingredients are traded and consumed in supplements and functional foods. Public references used for this include the NIH Office of Dietary Supplements fact sheets, the USDA FoodData Central ingredient and nutrient references, the FDA dietary supplement and labeling guidance pages, and EU-level food information and health-claim resources, which help keep ingredient definitions and claim boundaries consistent.

To convert these references into a usable market model, we also review company annual reports, investor presentations, and product technical sheets that indicate application mix and typical use rates. In parallel, we use paid subscriptions for company financials and intelligence, news and financials, and patent databases to track capacity additions, formulation activity, and category innovation signals over time. These sources are illustrative only, and other public and paid references were also used to collect, cross-check, and clarify inputs.

Primary Interviews and Surveys

Primary work is used to test what was built from published information, especially around real-world inclusion boundaries, pricing movement, and application splits by region. We spoke with ingredient suppliers, contract manufacturers, and downstream buyers in supplements and functional food and beverage, and respondent feedback was used to tighten assumptions where desk sources remained broad across omega-3s, phytosterols, beta-glucan, and soy protein.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 43% |

| Mid tier: 43% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 21% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

Our core sizing uses a top-down build where demand is reconstructed from nutrition and functional-food consumption pools, and then filtered through ingredient penetration and typical inclusion rates for heart health positioning. To keep totals grounded, the output is cross-checked with selective bottom-up approximations, including sampled supplier revenue splits, channel checks on ingredient shipments, and ASP times volume sanity checks for major ingredient families.

Key inputs treated as market fingerprints include supplement and functional food launch intensity for heart health positioning, regional usage preference for omega-3 and plant sterols, application split between dietary supplements and functional food and beverage, typical dosage or inclusion-rate ranges by ingredient form (powder versus liquid), and observed price movement for commodity-linked inputs. When a bottom-up view could not be cleanly built for smaller ingredient types, we filled gaps using proxy adoption rates from adjacent categories, and validated those proxies using interview feedback.

For forecasting, scenario analysis is applied around adoption speed and price progression, since these two variables tend to move differently by region and by ingredient source (plant-based, animal-based, and algae-based). The final forecast path is kept practical by anchoring assumptions to what interviewees expect in procurement behavior, regulatory comfort, and formulation trends over the 2026 to 2031 window.

Data Validation & Update Cycle

Validation is done through multiple passes, where model totals are compared against independent signals such as trade movement for relevant inputs, capacity and expansion announcements, and observed application growth in supplements and functional foods. If the variance is unusually wide for a region or key ingredient type, we revisit penetration and pricing assumptions and, when needed, re-contact sources to confirm what changed.

Before sign-off, the work is reviewed by another analyst to check math consistency, year-on-year movement, and whether assumptions match the stated scope. Reports are refreshed annually, with interim updates triggered when material events occur, such as regulatory shifts, major capacity additions, or sharp input price changes. Right before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's Heart Health Ingredients Market Size Compared Against Other Published Estimates

Published market sizes for heart health ingredients often differ, and that usually comes from how each publisher draws the boundary between ingredient value and finished product value, plus how they handle claim-based positioning across supplements and functional foods. Differences also show up when sources assume different adoption speeds for omega-3s, phytosterols, beta-glucan, and soy protein, which can quickly change the totals.

Price checks by ingredient form (powder versus liquid) and application mix validation from buyer and supplier interviews are used to keep Mordor Intelligence focused on an ingredient-only revenue pool rather than a broader nutraceutical spend estimate. Other estimates can drift when currency conversion timing is handled differently, when the base year is not aligned to the same market cycle, or when forecasts are presented as an aggressive scenario without re-checking penetration assumptions at the regional level.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.95 B (2026) | |

| Global Publisher A | USD 20.14 B (2025) | The figure appears to reflect a broader definition that blends ingredient value with wider heart health nutrition and delivery-format spending, which can pull finished-product economics into what is labeled as ingredients. |

| Industry Publisher B | USD 18.62 B (2024) | The scope is presented with very broad ingredient and function groupings, and the link between heart health claims and counted revenues is less explicit, which can over-allocate demand from general health ingredients into this category. |

Looking across the three numbers, much of the spread is explained by whether the count stays at ingredient revenues used for heart health positioning, or expands into wider nutraceutical and wellness spending buckets. With clear inclusion rules, practical pricing and adoption inputs, and repeatable cross-checks, the model lands at a balanced estimate that can be re-tested as the market evolves.

Key Questions Answered in the Report

What is the current valuation of the heart health ingredients market?

The market is worth USD 9.95 billion in 2026 and is projected to reach USD 13.13 billion by 2031, expanding at a 5.74% CAGR.

Which ingredient type leads the heart health ingredients market?

Omega-3 fatty acids lead with 35.62% market share in 2025 owing to extensive clinical evidence and strong consumer trust.

Which region is the fastest growing for heart health ingredients?

Asia-Pacific is forecast to grow at a 7.08% CAGR through 2031, driven by escalating cardiovascular disease prevalence and rising disposable income.

Why are algae-based omega-3 sources gaining popularity?

Algae cultivation offers high DHA purity, avoids marine contaminants, and aligns with sustainability goals, driving a 7.03% CAGR for algae-sourced ingredients.

Page last updated on: