Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

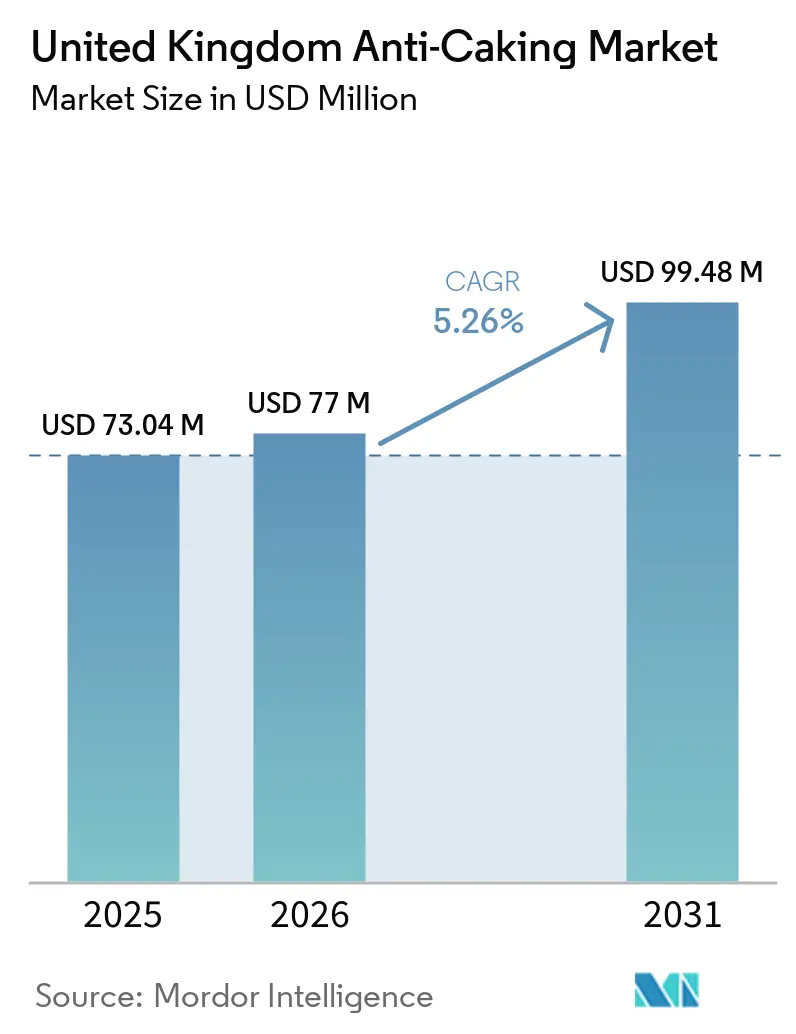

| Base Year Market Size (2025) | USD 73.04 Million |

| Market Size (2026) | USD 77 Million |

| Market Size (2031) | USD 99.48 Million |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

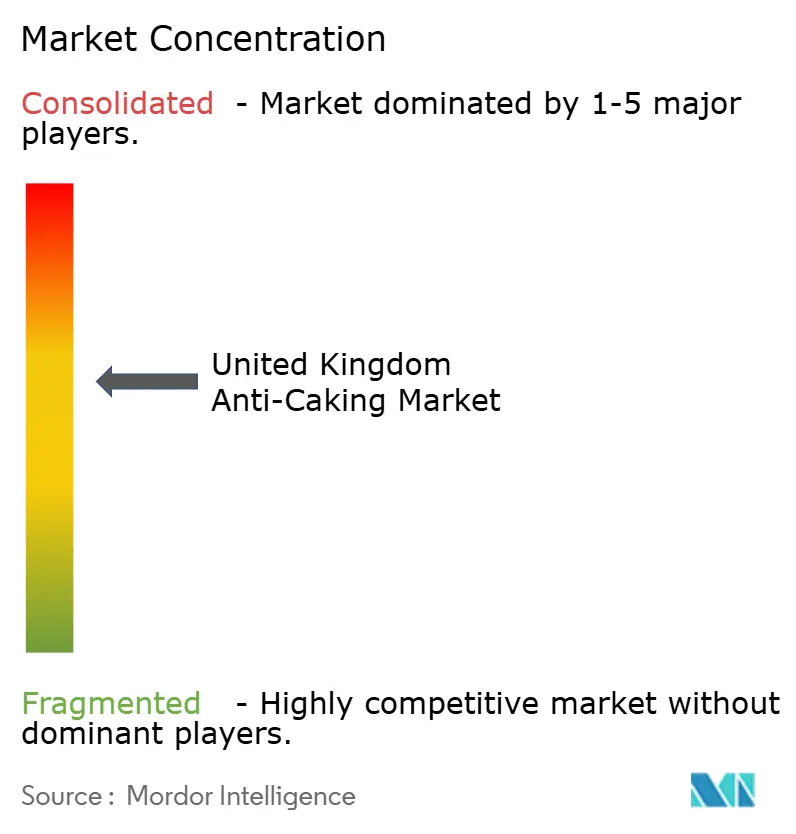

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Anti-Caking Market Analysis by Mordor Intelligence

The United Kingdom anti-caking agents market size is expected to increase from USD 73.04 million in 2025 to reach USD 77 million in 2026 and is forecast to reach USD 99.48 million by 2031 at a CAGR of 5.26% over 2026-2031. The United Kingdom anti-caking agents market is supported by the country’s food and drink manufacturing base, which remained the largest manufacturing sector in the United Kingdom in 2025 and continued to process large volumes of dairy powders, seasoning blends, bakery mixes, and other dry ingredients that need stable flow properties. The United Kingdom anti-caking agents market is also being shaped by the post-Brexit regulatory framework, where the Food Standards Agency continues to enforce the retained additives regime while suppliers monitor divergence from ongoing EU changes and manage separate documentation needs across the devolved administrations. Demand in the United Kingdom anti-caking agents market follows 2 clear paths: large food and feed processors drive steady volume use, while pharmaceutical and nutraceutical manufacturers create demand for tighter particle control and higher specification grades.

Key Report Takeaways

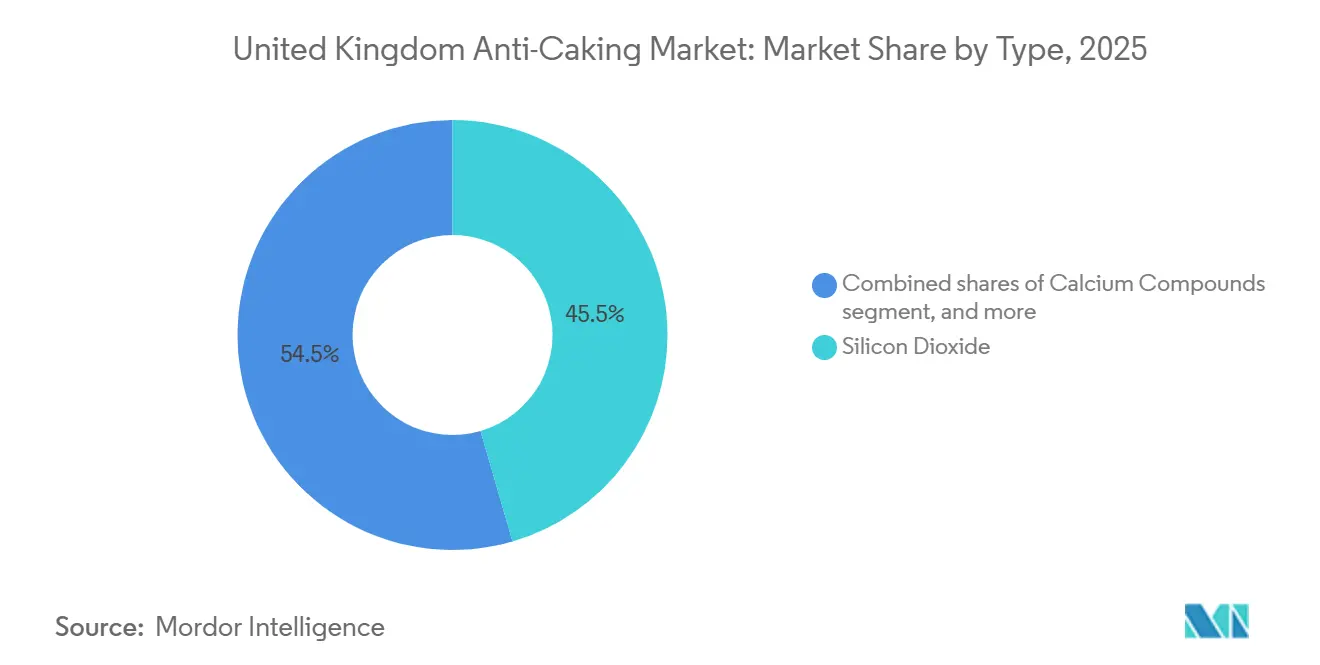

- By type, Silicon Dioxide held 45.5% of the United Kingdom anti-caking agents market in 2025, while Microcrystalline Cellulose is projected to record the fastest growth at a 6.52% CAGR through 2031.

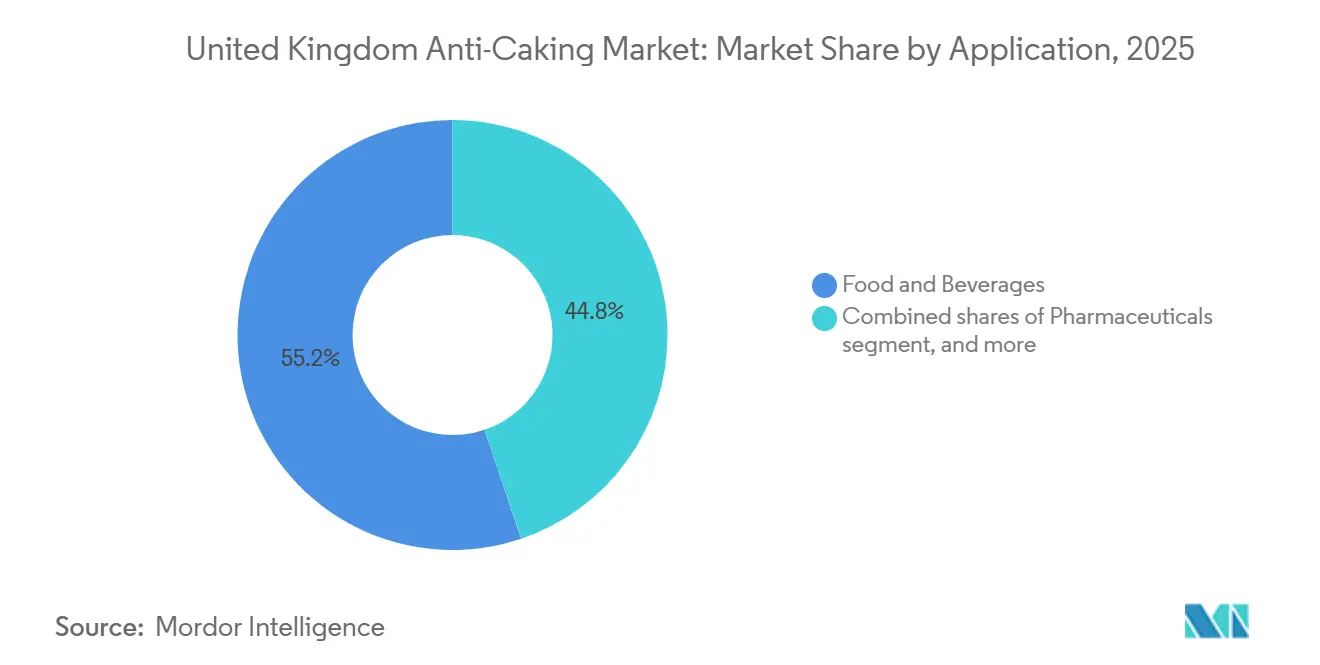

- By application, Food and Beverages accounted for 55.2% of the United Kingdom anti-caking agents market in 2025, while Pharmaceuticals is forecast to expand at a 7.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Anti-Caking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for shelf-stable powdered food formats | +1.1% | United Kingdom-wide, with strongest concentration in North England and Midlands food processing hubs | Medium term (2-4 years) |

| United Kingdom clean label reformulation is accelerating silicon dioxide and mineral-based substitution | +0.9% | England and Wales, especially among branded food and health supplement manufacturers | Medium term (2-4 years) |

| Growth in specialty feed premixes is increasing flow-aid usage | +0.8% | United Kingdom-wide, with spillover into Northern Ireland dairy farming and Scottish aquaculture premix demand | Long term (≥ 4 years) |

| Food safety and anti-clumping compliance are raising specification-driven demand | +0.7% | United Kingdom-wide under the retained additives framework enforced by the Food Standards Agency | Short term (≤ 2 years) |

| Micro dosing and precision blending are increasing the demand for high-performance anti-caking systems | +0.7% | England and Scotland pharmaceutical and contract manufacturing belts | Long term (≥ 4 years) |

| Powdered nutraceuticals and functional foods are expanding downstream consumption | +0.6% | United Kingdom-wide, with stronger premium supplement demand in London and South England | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for shelf-stable powdered food formats

The United Kingdom anti-caking agents market is benefiting from stronger investment in shelf-stable and low-moisture product formats, including powdered soups, seasoning blends, meal-kit bases, spray-dried dairy inputs, and fortified beverage mixes. These formats help manufacturers reduce cold-chain dependence and simplify handling, which matters in a cost-sensitive operating environment. In 2025, the Food & Drink Federation stated that 65% of United Kingdom food and drink manufacturers were prioritizing domestic sales growth while operating under elevated cost pressure, which supports continued interest in dry and efficient product formats[1]Source: Food & Drink Federation, “State of the Food & Drink Industry Report Q1 2025,” Food & Drink Federation, fdf.org.uk. This shift is also bringing the UK anti-caking agents market into categories that were previously less dependent on flow aids, such as plant protein powders, functional instant drinks, and nutrient-fortified dry blends. Silicon dioxide continues to benefit because it performs reliably across spray-dried and dry-blended systems and fits a wide range of existing production setups. As a result, anti-caking selection is increasingly being made earlier in product design, which gives approved suppliers a stronger position in future formulation pipelines.

United Kingdom clean label reformulation is accelerating silicon dioxide and mineral-based substitution

The United Kingdom anti-caking agents market is being influenced by a clean-label push that makes food manufacturers review every additive declaration more closely, even though the retained United Kingdom version of Regulation (EC) No 1333/2008 has not yet created a major shift in approved anti-caking categories. In October 2024, the European Food Safety Authority (EFSA) re-evaluation of silicon dioxide confirmed that E551 did not raise safety concerns for any population group at current exposure levels, which supports its continued use in relevant formulations[2]Source: European Food Safety Authority, “Re-Evaluation of Silicon Dioxide (E551) as a Food Additive for All Population Groups,” EFSA Journal via PubMed, pubmed.ncbi.nlm.nih.gov. At the same time, cleaner ingredient language is encouraging manufacturers to consider plant-derived flow agents and cellulose-based options where label presentation matters more. Campden BRI noted in 2024 that additives used to support clean-label positioning still need to meet the relevant regulatory requirements, which limits the speed at which novel alternatives can move into regular use in the United Kingdom. This is helping Microcrystalline Cellulose gain attention because it aligns better with consumer-friendly naming in some supplement formats while still offering functional value.

Growth in specialty feed premixes is increasing flow-aid usage

The United Kingdom anti-caking agents market has a stable demand base in animal feed because specialty premixes use amino acids, vitamins, minerals, and phytogenic inputs that need strong flow control during storage, transport, and dosing. Moisture-sensitive premix ingredients are especially dependent on hydrophobic silica and related high-performance grades when humidity conditions change across warehouses and farm distribution points. Evonik’s SIPERNAT portfolio and its feed-related product documentation show how suppliers are positioning specific silica grades for anti-caking, carrier, and flow-aid roles in premix systems, with Feed Additive and preMIxture Quality System (FAMI-QS) certification remaining an important qualifier in this channel. As livestock nutrition becomes more precise and premix formulas become more complex, the value of reliable particle flow rises because nutrient segregation can directly affect formulation quality. The United Kingdom anti-caking agents market is therefore seeing feed premixes move from a basic mineral input segment toward a more specification-driven part of demand.

Powdered nutraceuticals and functional foods are expanding downstream consumption

The United Kingdom anti-caking agents market is seeing stronger downstream demand from powdered nutraceuticals and functional foods, including protein powders, collagen blends, vitamin mixes, and dry beverage bases. These products often use hygroscopic ingredient systems, which makes moisture control and free-flow performance important for both packaging and end-user consistency. A growing number of United Kingdom supplement producers are also using pharmaceutical-style blending and tableting standards, which narrows the gap between food-grade and pharma-grade anti-caking specifications. This has increased interest in dual-specification grades that can meet food additive rules while also fitting pharmacopoeial quality expectations and advanced processing needs. The United Kingdom anti-caking agents market benefits from that shift because higher-specification grades tend to support longer supply agreements and closer formulation partnerships. It also reduces the number of suppliers that can compete effectively in this channel, since documentation, purity, and functionality all need to hold up under stricter customer review.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight ingredient approval and labeling requirements limit reformulation flexibility | -0.5% | United Kingdom-wide, with differing enforcement pathways across England, Scotland, Wales, and Northern Ireland | Short term (≤ 2 years) |

| Volatile feedstock costs for specialty silica and mineral input pressure margins | -0.4% | Global cost pressure, with Europe Middle East and Africa supply chains exposed to energy-intensive silica production | Medium term (2-4 years) |

| Functional trade-offs in low-sodium and clean-label formulations reduce substitute options | -0.3% | United Kingdom-wide, with stronger exposure in bakery and seasoning reformulation work | Medium term (2-4 years) |

| The dependence on certain specialty grades increases supply risk and leads to longer lead times | -0.3% | Global supply concentration, with United Kingdom importers managing United Kingdom REACH and documentation requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight ingredient approval and labeling requirements limit reformulation flexibility

The United Kingdom anti-caking agents market still faces a real constraint from the current food additive approval framework, especially for suppliers that want to introduce reformulated or next-generation grades. Under the retained additives regime enforced by the Food Standards Agency, approved anti-caking agents need to meet category-specific use conditions, while suppliers that serve Northern Ireland also need to handle an additional layer of alignment with the EU framework. In 2025, the Food Standards Agency said it planned to modernize the food regulatory system, which reflects clear recognition that the current process can be slow for regulated product approvals[3]Source: Food Standards Agency, “Approved Additives and E Numbers,” Food Standards Agency, food.gov.uk. That leaves established materials such as silicon dioxide and several calcium-based compounds in a stronger commercial position, while new plant-derived alternatives face a longer route to regular adoption. The United Kingdom anti-caking agents market also carries added administrative complexity because national suppliers must work across different enforcement settings in the devolved administrations. This does not stop reformulation, but it does slow the pace at which new anti-caking concepts can move from trial stage to scaled use.

Volatile feedstock costs for specialty silica and mineral input pressure margins

The United Kingdom anti-caking agents market remains exposed to cost pressure because precipitated and fumed silica production depends on energy-intensive processes that are sensitive to swings in natural gas and electricity costs. The Food & Drink Federation reported that United Kingdom food manufacturers projected an average cost increase of 4.8% in the year to March 2026, and 41% of manufacturers had scaled back investment, which limited room for premium ingredient spending. Similar cost exposure also affects calcium carbonate and sodium-based materials because mining, calcination, and related processing activities all carry their own energy burden. In addition, the highest-performance pharmaceutical-style silica grades are produced by a limited number of global suppliers, which keeps pricing firm even when downstream demand softens. The United Kingdom anti-caking agents market, therefore, does not benefit much from short-term cost relief when specialty grade availability remains tight. This gives established producers more leverage in price discussions with food, feed, and pharmaceutical buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silicon Dioxide Anchors Volume Demand

Silicon Dioxide held 45.5% of the United Kingdom anti-caking agents market share in 2025, reflecting long-standing approval status, dependable performance in moisture-sensitive powders, and broad use across food, feed, and nutraceutical applications. Its position remains strong because United Kingdom manufacturers can use a familiar grade with clear regulatory standing and a long record in spray-dried, blended, and tableted products. The 2024 European Food Safety Authority's scientific opinion added further confidence by confirming that silicon dioxide did not raise safety concerns at current use levels, which helps maintain continuity in formulation planning. Calcium Compounds and Sodium Compounds formed the next volume tiers in the United Kingdom anti-caking agents industry, mainly in bakery, dairy, and powder, where lower-cost mineral performance is often sufficient.

Microcrystalline Cellulose is projected to be the fastest-growing type in the United Kingdom anti-caking agents market at a 6.52% CAGR through 2031. Its growth is tied to a broader move from a mainly pharmaceutical excipient role toward wider use in food supplements and nutraceutical powders, where label presentation and multifunctionality both matter. In several supplement formats, Microcrystalline Cellulose can avoid the same label perception issues that apply to more familiar E-number ingredients, which strengthens its appeal in reformulation work. The United Kingdom anti-caking agents industry is therefore giving more room to co-processed and performance-designed excipients, especially where food and pharmaceutical processing standards begin to overlap. Pharmacopoeial alignment also supports this shift because customers in tablet and nutraceutical production want materials that can meet stricter quality expectations without adding multiple separate inputs.

By Application: Food Leads Market Value, Pharmaceuticals Accelerates

Food and Beverages accounted for 55.2% share of the United Kingdom anti-caking agents market size in 2025, supported by the scale of powdered food processing across seasoning blends, dried soups, bakery mixes, spray-dried dairy products, infant nutrition, and functional food ingredients. This application remained the largest because anti-caking agents are central to maintaining powder consistency, handling stability, and acceptable shelf life across large production volumes. The Food & Drink Federation continued to identify food and drink as the United Kingdom’s largest manufacturing sector in 2025, which explains why food processing remained the main consumption base for anti-caking materials. The United Kingdom anti-caking agents market, therefore, continued to draw most of its value from food systems, even as other applications became more specification-driven.

Pharmaceuticals is forecast to be the fastest-growing application in the United Kingdom anti-caking agents market at a 7.01% CAGR through 2031. Growth is being supported by solid dosage manufacturing, direct-compression processes, and higher demand for inputs that improve both flow and tablet compressibility in one step. Customer requirements are tighter in this channel because purity, particle size, and functional consistency all carry greater importance in supplier qualification. JRS Pharma’s PROSOLV SMCC (Microcrystalline Cellulose) is one example of how anti-caking properties are being built into advanced excipient systems rather than supplied only as stand-alone flow aids. This gives the United Kingdom anti-caking agents market a stronger high-value growth lane, even though overall pharmaceutical volumes remain below food processing volumes.

Competitive Landscape

The United Kingdom anti-caking agents market remains moderately consolidated, with global specialty chemical companies holding a strong position in the volume silica segment while food ingredient suppliers and pharmaceutical excipient producers compete more actively in application-specific niches. Evonik, Cabot, Nouryon, and BASF formed the main backbone of silica supply in the United Kingdom anti-caking agents market because precipitated and fumed silica remain central to many anti-caking formulations. Imerys held a differentiated place through its mineral platform, especially where calcium carbonate-based solutions align with cost and performance needs. This meant the United Kingdom anti-caking agents market was not controlled by a single supplier group, but it still favored companies with scale, technical service, and established grade portfolios. It also meant that commodity volume and high-value specification business followed different competitive rules.

In the United Kingdom anti-caking agents market, supplier advantage increasingly depends on the ability to support several customer requirements at the same time, including additive approval, feed certification, purity standards, and processing performance. Evonik’s June 2026International Sustainability and Carbon Certification (ISCC) Plus certification for its precipitated silica site in Turkey and the start of ULTRASIL eCO production showed how silica producers are connecting sustainability credentials to broader portfolio relevance across customer industries. Nouryon’s nearly 50% expansion of Levasil colloidal silica capacity at its Green Bay site in 2024 showed continued investment in high-performance silica supply, even though that capacity sits outside the United Kingdom. In 2026, Nouryon also moved ahead with expansion of Levasil production in Guangzhou, which reinforced the broader pattern of capacity support for premium silica applications. These moves matter to the United Kingdom anti-caking agents market because buyers in food, feed, and pharmaceuticals want stable access to proven grades rather than exposure to narrow supply pools.

Another competitive line in the United Kingdom anti-caking agents market is formulation technology, especially in products that need both flow control and processing efficiency. JRS Pharma’s PROSOLV SMCC range shows how co-processed excipients can combine MCC and silicon dioxide in a single system, which helps reduce direct substitution risk for suppliers that compete beyond standard mineral grades. Entry barriers remain meaningful because food additive approval, United Kingdom Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) obligations, customer quality audits, and channel-specific documentation all favor suppliers that already have established files and regulatory discipline. The United Kingdom anti-caking agents market therefore remains open to focused challengers, but those challengers are more likely to succeed in narrow high-specification spaces than in the broad silica volume base.

United Kingdom Anti-Caking Industry Leaders

BASF SE

Evonik Industries AG

Cabot Corporation

Nouryon

Imerys

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Evonik obtained ISCC Plus certification for its precipitated silica plant in Adapazarı, Turkey, the first ISCC Plus-certified silica site in the EMEA region, and commenced commercial production of ULTRASIL eCO, its circular silica based on recognised mass balance standards. enhances Evonik’s value proposition to United Kingdom customers seeking lower‑footprint additives without changing existing formulations.

- February 2025: Nouryon's announced an initiative to double the production capacity of Kromasil chromatography media in Sweden, enhancing its role in the high-purity silica market for pharmaceutical separations, particularly for peptide-based drugs such as GLP-1 agonists. This expansion also bolsters the broader high-purity silica value chain, which includes applications in excipient and flow-aid functions (e.g., colloidal and precipitated silica used as glidants and anti-caking agents in solid dosage forms) in markets like the United Kingdom.

- October 2024: Evonik AG announced that the European Food Safety Authority's (EFSA) scientific opinion confirmed silicon dioxide (E551) as safe for all population groups, including infants under 16 weeks. The company highlighted the continued role of its SIPERNAT and AEROSIL product ranges as approved, fully compliant food anti-caking agents, reassuring United Kingdom food manufacturers that silica‑based systems remain compliant, with only tighter purity specs expected.

United Kingdom Anti-Caking Market Report Scope

An anti-caking agent is a substance added in small quantities to powdered or granulated materials to prevent clumping and ensure free flow during processing, packaging, and usage. These additives function by either absorbing excess moisture or coating particle surfaces, thereby reducing particle-to-particle adhesion in products such as foods, animal feeds, fertilizers, and other powdered materials. The United Kingdom's anti-caking market is segmented by type into silicon dioxide, calcium compounds, sodium compounds, magnesium compounds, and others; and by application into food and beverage, personal care and cosmetics, animal feed, and others. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Silicon Dioxide |

| Calcium Compounds |

| Sodium Compounds |

| Magnesium Compounds |

| Microcrystalline Cellulose |

| Others |

By Application

| Food and Beverages |

| Animal Feed |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Other Applications |

| By Type | Silicon Dioxide |

| Calcium Compounds | |

| Sodium Compounds | |

| Magnesium Compounds | |

| Microcrystalline Cellulose | |

| Others | |

| By Application | Food and Beverages |

| Animal Feed | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Other Applications |

Key Questions Answered in the Report

What is the current United Kingdom Anti Caking Market size?

The United Kingdom anti-caking agents' market is estimated at USD 77 million in 2026 and is forecast to reach USD 99.5 million by 2031 at a 5.3% CAGR.

Which anti-caking type leads demand in the United Kingdom?

Silicon Dioxide led with 45.5% share in 2025 because of broad approval status, strong functional performance, and wide use across food, feed, and nutraceutical powders.

Which end-use area is growing the fastest in the United Kingdom anti-caking agents space?

Pharmaceuticals is projected to grow the fastest at a 7.01% CAGR through 2031 as manufacturers use more advanced excipients that improve both powder flow and tablet performance.

What is the main competitive advantage for suppliers in this space?

Suppliers with approved grades, strong documentation, feed or pharma credentials, and application support are in the best position because customers increasingly want more than a basic mineral input.

Page last updated on: