United States Anti-Caking Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

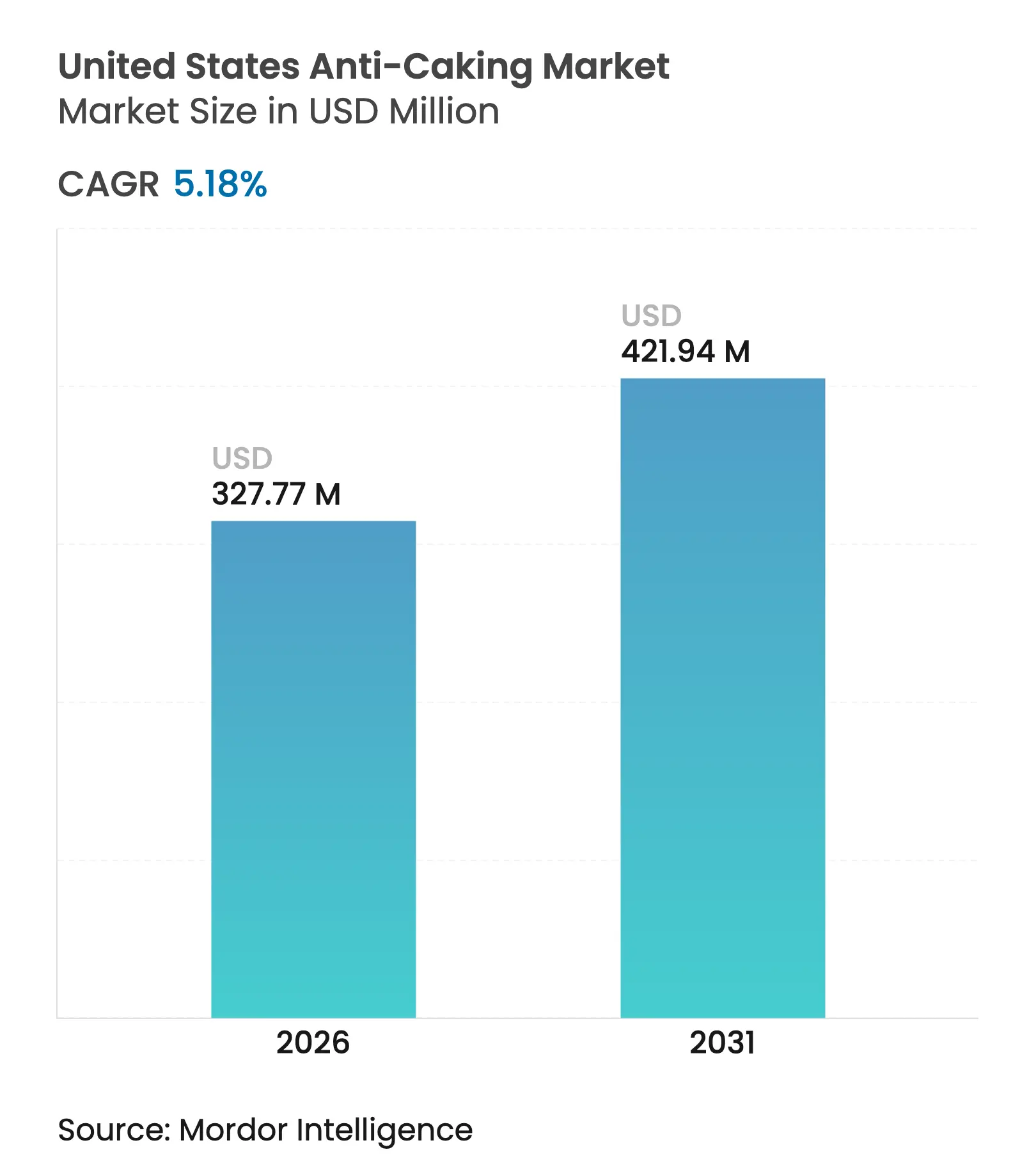

| Market Size (2026) | USD 327.77 Million |

| Market Size (2031) | USD 421.94 Million |

| Growth Rate (2026 - 2031) | 5.18 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United States Anti-Caking Market Analysis by Mordor Intelligence

The United States anti-caking agents market size in 2026 is estimated at USD 327.77 million, growing from 2025 value of USD 311.62 million with 2031 projections showing USD 421.94 million, growing at 5.18% CAGR over 2026-2031. The current trajectory reflects a balanced mix of regulatory certainty, widespread processed-food demand, and a steady shift toward clean-label solutions. Silicon dioxide, calcium silicate, and magnesium silicate remain the foundation of most formulations because the Food and Drug Administration continues to affirm their GRAS status, giving manufacturers confidence to invest in higher-speed packaging and direct-compression equipment. At the same time, retailer ingredient lists and consumer perception have nudged premium brands to experiment with rice hull, bamboo fiber, and organic starch alternatives, creating dual-track procurement strategies for multinationals. Competitive dynamics favor global silica leaders that can supply ultra-pure grades for pharmaceutical and semiconductor uses, yet smaller regional suppliers still wield pricing leverage in food-grade calcium carbonate because proximity lowers freight costs and shortens lead times.

Key Report Takeaways

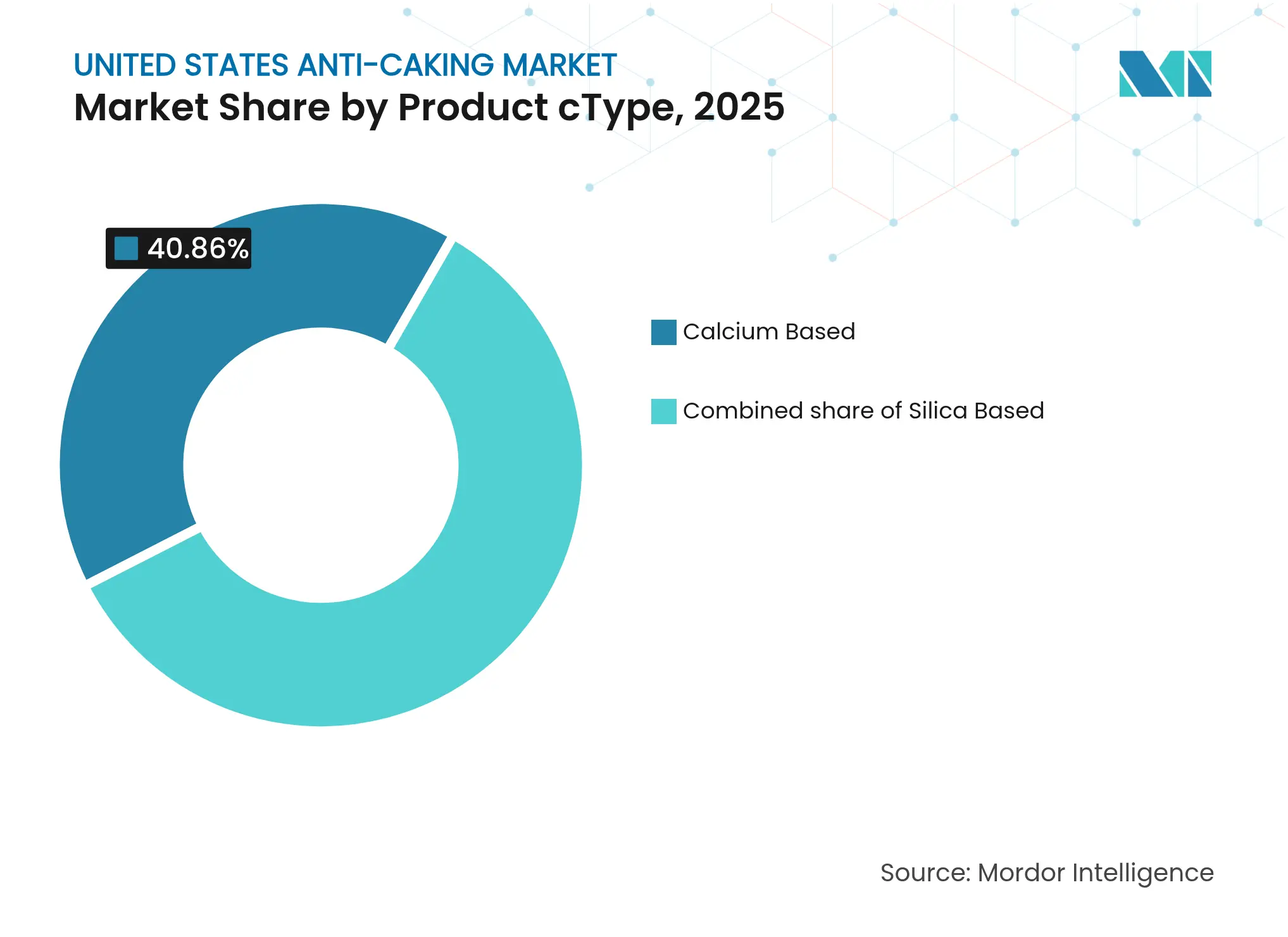

- By product type, calcium-based agents held 40.86% of the United States anti-caking agents market share in 2025 and are forecast to grow at a 4.63% CAGR through 2031.

- By product type, silica-based agents are projected to post the fastest 6.62% CAGR.

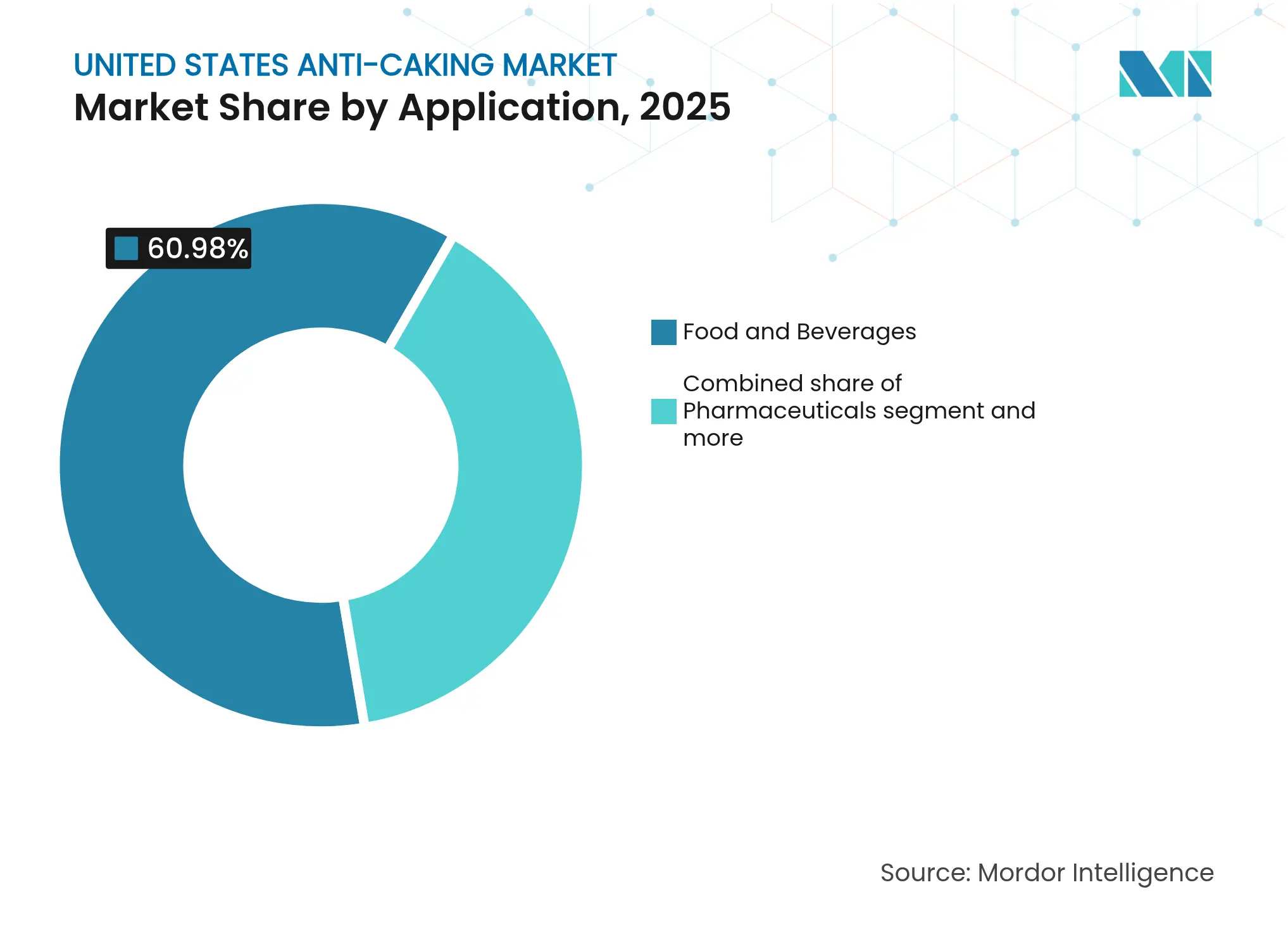

- By application, food and beverages commanded 60.98% of the United States anti-caking agents market share in 2025 and will expand at a 6.55% CAGR during 2026-2031.

- By geography, the Midwest accounted for 39.62% of 2025 demand and is expected to maintain a 4.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Anti-Caking Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Processed foods, spice blends, and instant mix adoption

Processed foods, spice blends, and instant mix adoption

| +1.2% | Midwest hubs (Illinois, Ohio, Wisconsin) | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

Midwest hubs (Illinois, Ohio, Wisconsin)

|

Impact Timeline

:

Medium term (2-4 years)

|

Regulatory certainty for silicon dioxide and cellulosics

Regulatory certainty for silicon dioxide and cellulosics

| +0.8% | National | Long term (≥ 4 years) | |||

Expansion in nutraceutical and OTC pharma manufacturing

Expansion in nutraceutical and OTC pharma manufacturing

| +1.0% | California, New Jersey, North Carolina | Medium term (2-4 years) | |||

High-speed packaging demands in salt, bakery, beverage

mixes

High-speed packaging demands in salt, bakery, beverage

mixes

| +0.9% | National | Short term (≤ 2 years) | |||

Fertilizer anti-caking across varied humidity zones

Fertilizer anti-caking across varied humidity zones

| +0.7% | Midwest and Great Plains | Medium term (2-4 years) | |||

Clean-label rice/bamboo alternatives in supplements

Clean-label rice/bamboo alternatives in supplements

| +0.6% | Coastal urban markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Processed foods, spice blends, and instant mix adoption in the u.s.

Instant soups, seasoning blends, and meal-kit sachets, collectively forming a USD 3.5 billion processed-food subsegment, prioritize moisture blocking to ensure product quality and shelf stability. These powders, designed to sit on shelves for months in 60-75% relative humidity, rely on silicon dioxide (1.5–2%) and calcium silicate (0.5–1%) to remain free-flowing. This prevents a 2–3% moisture pick-up, which would render the product unsaleable by causing clumping and degradation of texture. The USDA's 2024 Food Availability Data System indicates that per capita consumption of dried soups and sauces has stabilized at approximately 2.3 kilograms annually, yet the shift toward premium spice blends, organic turmeric, smoked paprika, and specialty salts commands 40-60% higher retail prices and tolerates proportionally higher anti-caking agent costs[1]Source: United States Department of Agriculture, "Food Availability (Per Capita) Data System", ers.usda.gov. While McCormick adheres to these inclusion rates to maintain product integrity, it is also experimenting with rice concentrate in its organic line to align with Whole Foods’ ingredient policies, which emphasize natural and clean-label components. The stakes are higher for single-serve meal kits, as sachets endure temperature fluctuations during last-mile delivery, which can exacerbate moisture-related issues. In these scenarios, silica grades with hydrophobic surfaces prove superior to hygroscopic calcium salts, offering enhanced performance in maintaining product flowability and quality under challenging conditions.

Regulatory certainty (GRAS) for silicon dioxide and cellulosics

In the U.S., the FDA's GRAS listings for silicon dioxide (21 CFR 172.480) and powdered cellulose (21 CFR 182.90) provide manufacturers with confidence in minimal reformulation risks[2]Source: Food and Drug Administration, "CFR - Code of Federal Regulations Title 21", accessdata.fda.gov. This contrasts with the European Union, where E551 is subject to periodic scrutiny due to evolving regulatory standards and safety evaluations. Cabot's AEROSIL fumed silica, with a surface area of 200–300 m²/g, achieves anti-caking targets at a mere 0.2–0.5% inclusion, solidifying its status as a staple in pharmaceutical excipients. Its high surface area enhances its ability to prevent clumping, ensuring consistent product quality and performance. Meanwhile, organic operators are capitalizing on the benefits of silicon dioxide. Thanks to 7 CFR 205, which permits its use when derived without synthetic solvents, brands like Annie's can uphold their USDA Organic labels while adhering to flow-control specifications. This regulatory allowance enables organic brands to maintain both product integrity and compliance with organic certification standards.

Expansion in nutraceutical and OTC pharma manufacturing (glidants)

In 2024-2025, U.S. nutraceutical contract capacity surged by 15-18%, driven by advancements in manufacturing technologies and increased demand for dietary supplements. In California and New Jersey, tablet presses, now exceeding 10,000 units per hour, have started incorporating colloidal silicon dioxide to enhance production efficiency and tablet quality. Meanwhile, calcium phosphates from Innophos are being utilized as disintegrants, improving tablet dissolution and bioavailability. Although SPI Pharma’s magnesium stearate continues to be the preferred lubricant due to its effectiveness in preventing tablet sticking and ensuring smooth production, IFF’s divestiture to Roquette in 2025 may constrict the domestic supply, potentially impacting manufacturers. In 2024, WHO reaffirmed the 0-3 mg/kg ADI for magnesium stearate, paving the way for elevated supplement dosages and providing manufacturers with greater flexibility in formulation.

High-speed packaging and free-flow needs in salt, bakery, beverage mixes

Manufacturers fill over 120 packs per minute with table salt, baking mixes, and sports-nutrition products, ensuring high-speed production to meet growing consumer demand. In premium iodized salt, calcium silicate, which can absorb 600% of its weight in water, has replaced ferrocyanides. This shift is driven by consumer concerns, as the term “cyanide” is often associated with toxicity, despite its safe usage in regulated amounts. Clumping downtime, which can disrupt production lines, costs manufacturers between USD 500-1,000 per hour. To mitigate these losses, manufacturers invest in hydrophobic silica. This material not only resists Gulf-Coast humidity, a common challenge in humid climates, but also disperses instantly in shaker tests, ensuring product quality and consistency.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Clean-label scrutiny and retailer bans on E-numbers

Clean-label scrutiny and retailer bans on E-numbers

| -0.5% | Whole Foods, Sprouts, Trader Joe’s | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.5%

|

Geographic Relevance

:

Whole Foods, Sprouts, Trader Joe’s

|

Impact Timeline

:

Short term (≤ 2 years)

|

Talc litigation and perception risks

Talc litigation and perception risks

| -0.4% | National | Medium term (2-4 years) | |||

Label avoidance of ferrocyanides in salt

Label avoidance of ferrocyanides in salt

| -0.3% | National | Short term (≤ 2 years) | |||

Dust-exposure safety compliance costs

Dust-exposure safety compliance costs

| -0.3% | Facilities handling fine powders | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Clean-label scrutiny and retailer bans on certain E-numbers

Whole Foods, concerned about the use of silicon dioxide, scrutinizes its suppliers and has pushed for a shift towards rice hull and organic tapioca starch, moving away from roughly 230 synthetic ingredients. Following suit, private labels from Target and Kroger are incentivizing similar reformulations across their mainstream offerings. While natural agents occasionally falter in tropical humidity, drawing customer complaints, a 2024 IFIC survey found that 54% of consumers steer clear of unfamiliar ingredients. This consumer sentiment underscores brands' readiness to absorb higher costs. Meanwhile, ingredient manufacturers like Evonik are pouring resources into educational campaigns, yet they find themselves overshadowed by the marketing clout of "free-from" labels.

Talc litigation and perception risks in personal care/food

Despite being asbestos-free, food-grade talc has been shunned by users, largely due to Johnson & Johnson's staggering USD 8 billion settlements over talc-related issues. In 2024, the FDA's cosmetic tests detected asbestos in certain samples, igniting demands for stricter purity checks, with implications reaching food standards[3]Source: Food and Drug Administration, "Talc", fda.gov. This has raised concerns among food manufacturers about potential regulatory scrutiny and consumer backlash. As a result, formulators of chewing gum and rice coatings have turned to a combination of calcium carbonate and stearic acid. This shift has inflated their formula costs by 20-30%, as no alternative can replicate talc's unique lubricity and whitening properties, which are critical for achieving the desired texture and appearance in these products.

Segment Analysis

By Product Type: Silica Overtakes Calcium in High-Value Niches

In 2025, calcium-based agents dominated the U.S. anti-caking agents market, securing 40.86% of total revenues. Within this segment, calcium silicate stands out in iodized salt applications, where a 0.5–1% inclusion effectively mitigates potassium iodide's hygroscopicity, ensuring a free-flowing product. Tricalcium phosphate not only fortifies calcium in cereal and flour blends, adhering to FDA nutrient regulations, but also prevents caking in bulk commodities. Suppliers such as Mississippi Lime and Omya leverage cost leadership and strategically advantageous freight distribution to maintain their dominance, particularly catering to salt and dairy processors.

Silica-based agents, currently holding a 59.14% market share, are the fastest-growing category, projected to advance at a 6.62% CAGR through 2031. Fumed silica grades, with surface areas of 200–400 m²/g, achieve superior flow at a mere 0.2% loading. This efficiency proves especially economical for high-value nutraceutical tablets and pharmaceutical clusters that prioritize ultra-pure colloidal variants. Meanwhile, in dried soup and beverage mixes, precipitated silica commands a premium over mineral salts, thanks to its compliance with stricter color and heavy-metal specifications. Notably, Evonik's decision to boost capacity by 50% at its Charleston plant by 2026 highlights the accelerating demand for silica, driven by rising purity standards.

Note: Segment shares of all individual segments available upon report purchase

By Application: Food and Beverages Keep the Lead, Pharma Gains Pace

In 2025, the food and beverage sector dominated the U.S. anti-caking agents market, accounting for 60.98% of total revenues. Within this sector, seasonings and condiments took the lead, using 1.5–2% of either silicon dioxide or calcium silicate. This addition prevents clumping in garlic, onion, and paprika powders, which are then distributed through grocery stores and e-commerce platforms. Bakery mixes, on the other hand, utilize mildly alkaline agents like tricalcium phosphate and magnesium carbonate. These agents blend seamlessly with leavening agents, ensuring a consistent flow. Dairy powders, including whey protein concentrate, incorporate 0.5–1% silicon dioxide. This dosage prevents particle bridging in both spray-dryer cyclones and shipping totes. The segment's growth, at a 6.55% CAGR, is driven by rising demand for spice blends, protein powders, and instant soup mixes.

While pharmaceutical applications accounted for only 9% of the 2025 volume, they emerged as the fastest-growing end-use, projected to expand at a 6.79% CAGR through 2031. In New Jersey and North Carolina, direct-compression tablet lines utilize 0.2–0.5% colloidal silica or magnesium stearate. This ensures optimal flowability, allowing presses to achieve an impressive rate of 12,000 units per hour. These high-purity agents are pivotal for efficient production, especially with the increasing volumes of nutraceuticals and generic drugs. While the beauty and personal care sector is moving away from talc in favor of higher-loading kaolin substitutes, the pharmaceutical industry's stringent precision requirements underscore its leadership in growth. Additionally, the "Other" category sees fertilizer conditioning bolstered by low-cost clays and lignosulfonates, ensuring 18-month humidity resistance.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Manufacturing clusters, humidity profiles, and regulatory climates shape regional consumption patterns. In the Midwest, states like Illinois, Ohio, Wisconsin, and Indiana account for 39.62% of the nation's volume. This is largely due to mega-plants operated by Kraft Heinz, Conagra, and General Mills, producing everything from soup mixes to bakery premixes. With Midwestern summers boasting 60-75% relative humidity, these companies are compelled to increase their use of silica and calcium silicate to ensure smooth operations. Meanwhile, California stands at the forefront of clean-label experimentation. Here, supplement giants in Orange County and organic brands in the Sacramento Valley opt for rice hull and bamboo fiber, even at a premium price.

The Southeast has emerged as a hub for pharmaceuticals and over-the-counter products. Notable companies like Patheon, Catalent, and Thermo Fisher are setting the standard, often specifying USP-grade colloidal silica. In North Carolina’s Research Triangle Park, nutraceutical research and development labs are making strides, refining direct-compression blends that can reduce cycle times by 30-40%. Over in the Gulf Coast, fertilizer granulation plants in Texas and Louisiana are applying kaolin-polymer coatings to withstand tropical moisture. This practice bolsters a consistent demand for clay-based anti-caking agents throughout the year.

On the East Coast, New Jersey's pharmaceutical corridor has a high demand for top-tier glidants. Meanwhile, distributor warehouses in Pennsylvania, such as Brenntag, Univar, and IMC, are streamlining just-in-time deliveries for small-batch food producers. In the Pacific Northwest, organic processors, spearheaded by Bob’s Red Mill, are opting for powdered cellulose or rice concentrate to uphold their USDA Organic credentials. States like California and Washington, known for their stringent combustible-dust codes, are witnessing a swift shift towards liquid anti-caking slurries or enclosed transfer systems. This transition, while beneficial, comes with added capital costs, posing a challenge for smaller firms who either have to absorb these expenses or consider exiting the market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

In the U.S. anti-caking agents market, a few players hold significant sway. Global leaders in silica, namely Evonik, Solvay, and Cabot, command a dominant position, controlling over half of the nation's high-purity precipitated and fumed silica capacity. Their edge comes from advanced process technology and proprietary research and development, specifically tailored for sectors like pharmaceuticals, semiconductors, and batteries. In a strategic move, Evonik is reshaping its U.S. operations: planning to close its Waterford, New York facility in mid-2025 and the Havre de Grace, Maryland site in mid-2026, both focusing on shedding lower-margin grades. Simultaneously, the company is amplifying its operations in Charleston and enhancing its semiconductor line in Weston.

Regional players like Minerals Technologies, Mississippi Lime, and Omya leverage their proximity to defend their market share in calcium carbonate. Specialty distributors, including Brenntag, Univar, IMCD, and Azelis, utilize formulation labs to assist smaller clients in transitioning to clean-label alternatives. They often package solutions like rice-hull or bamboo-fiber with added technical support. In a strategic move, J.M. Huber's acquisition of Active Minerals in 2024 not only expanded its clay portfolio but also positioned it to compete with ICL’s polymer-clay coatings in the fertilizer market.

Glidants are witnessing emerging supply risks. IFF's sale of Pharma Solutions to Roquette shifts magnesium stearate and calcium phosphate assets to a player with a European focus. This move raises concerns for U.S. tablet manufacturers about potential delays post the 2025 deal closure. Meanwhile, trademark filings by Innophos hint at a shift towards battery-grade phosphates, which could limit the availability of food-grade calcium phosphates. However, suppliers of natural alternatives grapple with scalability issues: their organic-certified rice-hull production meets less than 5% of the total demand, leading to price fluctuations and batch inconsistencies.

United States Anti-Caking Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Papillon Agricultural Company unveiled DeTerra 365, a top-tier anti-caking agent tailored for dairy and beef cow feed. This product is made from consistently pure calcium montmorillonite clay, which is mined in the United States. It effectively binds moisture in feed, preventing mold growth and the production of harmful mycotoxins, thereby ensuring better feed quality and safety for livestock.

- May 2024: J.M. Huber finalized its acquisition of Active Minerals International, a strategic move to expand its specialty-minerals portfolio. This acquisition added attapulgite and kaolin to its product line, strengthening its position in the specialty minerals market and broadening its offerings for various industrial applications.

Table of Contents for United States Anti-Caking Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1 Processed foods, spice blends, and instant mix adoption in the U.S.

- 4.2.2Regulatory certainty (GRAS) for silicon dioxide and cellulosics

- 4.2.3Expansion in nutraceutical and OTC pharma manufacturing (glidants)

- 4.2.4 High-speed packaging and free-flow needs in salt, bakery, beverage mixes

- 4.2.5Fertilizer anti-caking across longer supply chains and humidity zones

- 4.2.6 Clean-label alternatives (e.g., rice/bamboo-based) in supplements

- 4.3Market Restraints

- 4.3.1Clean-label scrutiny and retailer bans on certain E-numbers

- 4.3.2Talc litigation and perception risks in personal care/food

- 4.3.3Label avoidance and limits on ferrocyanides in salt

- 4.3.4Dust exposure and explosion safety compliance costs

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Porter's Five Forces

- 4.6.1Bargaining Power of Suppliers

- 4.6.2Bargaining Power of Buyers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Silica Based

- 5.1.2Calcium Based

- 5.1.3Magnesium Based

- 5.1.4Others

- 5.2Application

- 5.2.1Food and Beveraegs

- 5.2.1.1Seasoning, Spcies and Condiments

- 5.2.1.2Bakery and Confectionery

- 5.2.1.3Dairy Products

- 5.2.1.4Beverages

- 5.2.1.5Soups and Sauces

- 5.2.1.6Meat and Meat Substitutes

- 5.2.2Beauty and Personal Care

- 5.2.3Animal Feed

- 5.2.4Pharmaceuticals

- 5.2.5Others

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Positioning Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Evonik Industries AG

- 6.4.2Solvay S.A.

- 6.4.3Cabot Corporation

- 6.4.4PQ Corporation

- 6.4.5 Innophos Holdings, Inc.

- 6.4.6Minerals Technologies Inc. (Specialty Minerals Inc.)

- 6.4.7J.M. Huber Corporation

- 6.4.8ICL Group Ltd.

- 6.4.9Arkema-ArrMaz

- 6.4.10 Cargill, Incorporated (Salt)

- 6.4.11 Morton Salt, Inc.

- 6.4.12International Flavors & Fragrances Inc. (IFF)

- 6.4.13 SPI Pharma, Inc.

- 6.4.14 Azelis Americas, LLC

- 6.4.15IMCD US

- 6.4.16Univar Solutions Inc.

- 6.4.17Imerys S.A.

- 6.4.18Peter Greven GmbH & Co. KG

- 6.4.19 Brenntag North America, Inc.

- 6.4.20Graham Partners

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

United States Anti-Caking Market Report Scope

The United States anti-caking market is segmented by type, application, and geography. On the basis of type, the market is segmented into Calcium Compounds, Sodium Compounds, Magnesium Compounds, Others. On the basis of application, the market is segmented into Food and Beverage, Cosmetic and Personal Care, Feed, and Others. The Food and Beverage segment is further segmented under Bakery Products, Dairy Products, Soups & Sauces, Beverages, and Others.