Smart Motors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

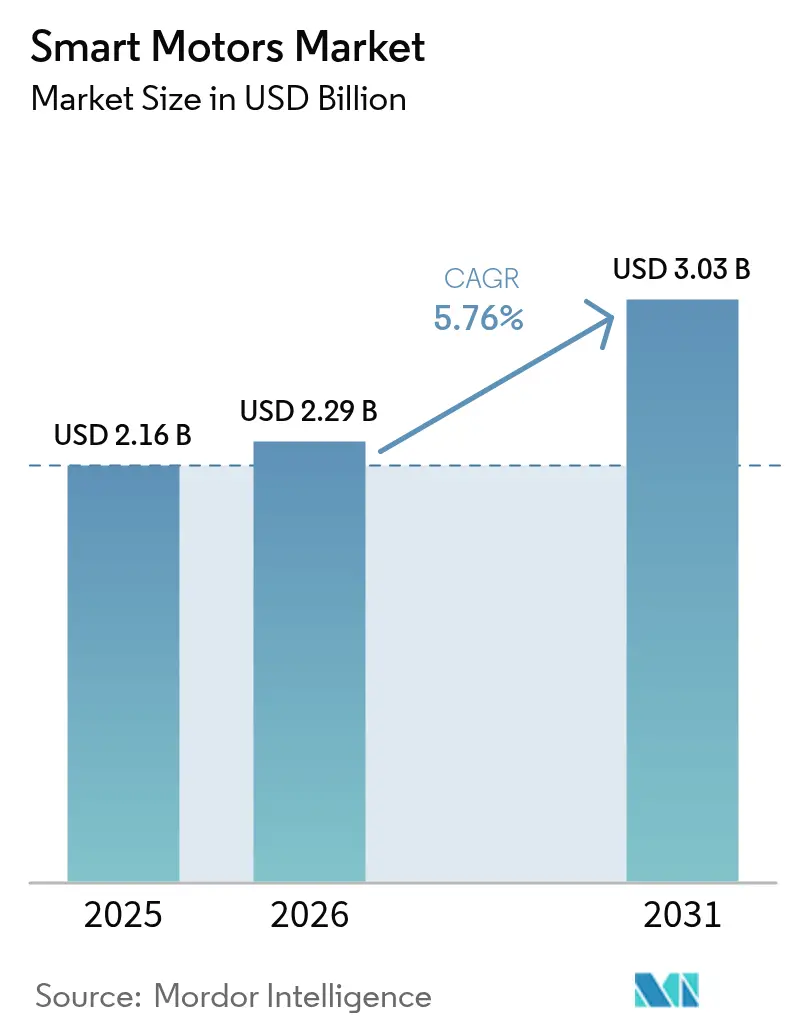

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Motors Market Analysis by Mordor Intelligence

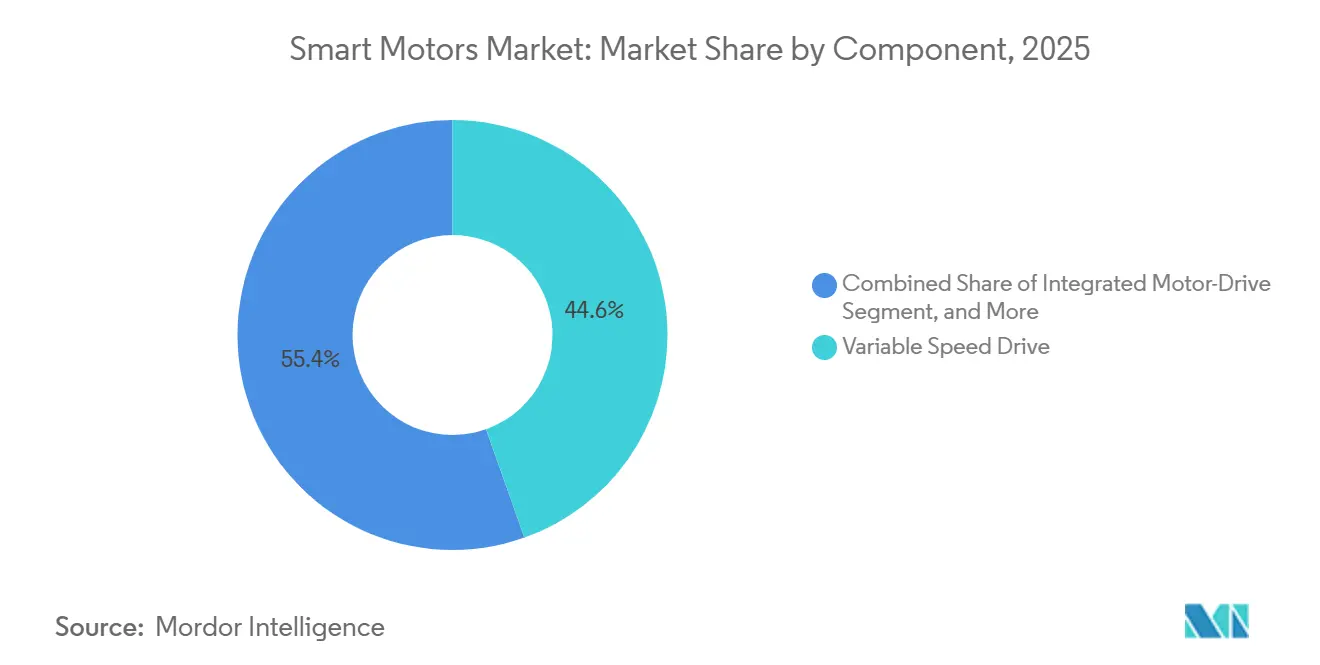

The smart motors market size was valued at USD 2.16 billion in 2025 and estimated to grow from USD 2.29 billion in 2026 to reach USD 3.03 billion by 2031, at a CAGR of 5.76% during the forecast period (2026-2031). This steady climb reflects progressive migration from fixed-speed motors to networked, sensor-rich systems that fine-tune energy use in real time. Variable-speed drives still accounted for 44.56% of 2025 revenue, yet factory-calibrated integrated motor-drive packages are advancing by 6.31% each year as end users seek simpler commissioning and lower lifetime costs. Demand is concentrated in the 1-10 kilowatt band, which accounted for 38.72% of 2025 shipments for pumps, fans, and conveyors, while sub-1 kilowatt designs are outpacing at 6.34% because autonomous mobile robots and smart building actuators require compact, battery-friendly solutions. Regionally, Asia-Pacific accounted for 39.74% of spending in 2025, whereas the Middle East led growth at 6.71% as energy-efficiency mandates accompany large industrial projects.

Key Report Takeaways

- By component, variable-speed drives led with a 44.56% revenue share in 2025, while integrated motor-drive packages are forecast to expand at a 6.31% CAGR through 2031.

- By power rating, the 1-10 kilowatt segment held 38.72% of the smart motors market share in 2025, whereas sub-1 kilowatt units are projected to grow the quickest at 6.34% CAGR to 2031.

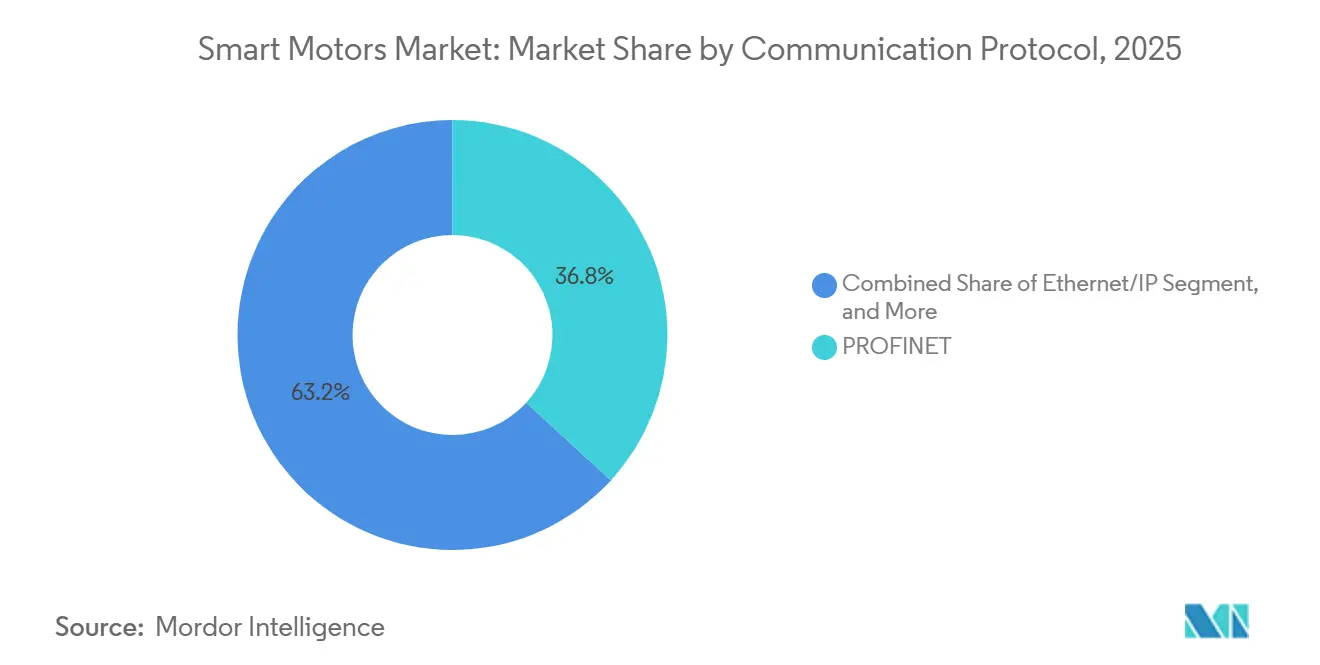

- By communication protocol, PROFINET commanded 36.82% of 2025 installations, and Ethernet/IP is expected to post the fastest 6.51% CAGR over the same horizon.

- By application, industrial uses accounted for 42.79% of the smart motors market share in 2025, but commercial deployments are set to rise at a 6.56% CAGR as data-center and HVAC upgrades accelerate.

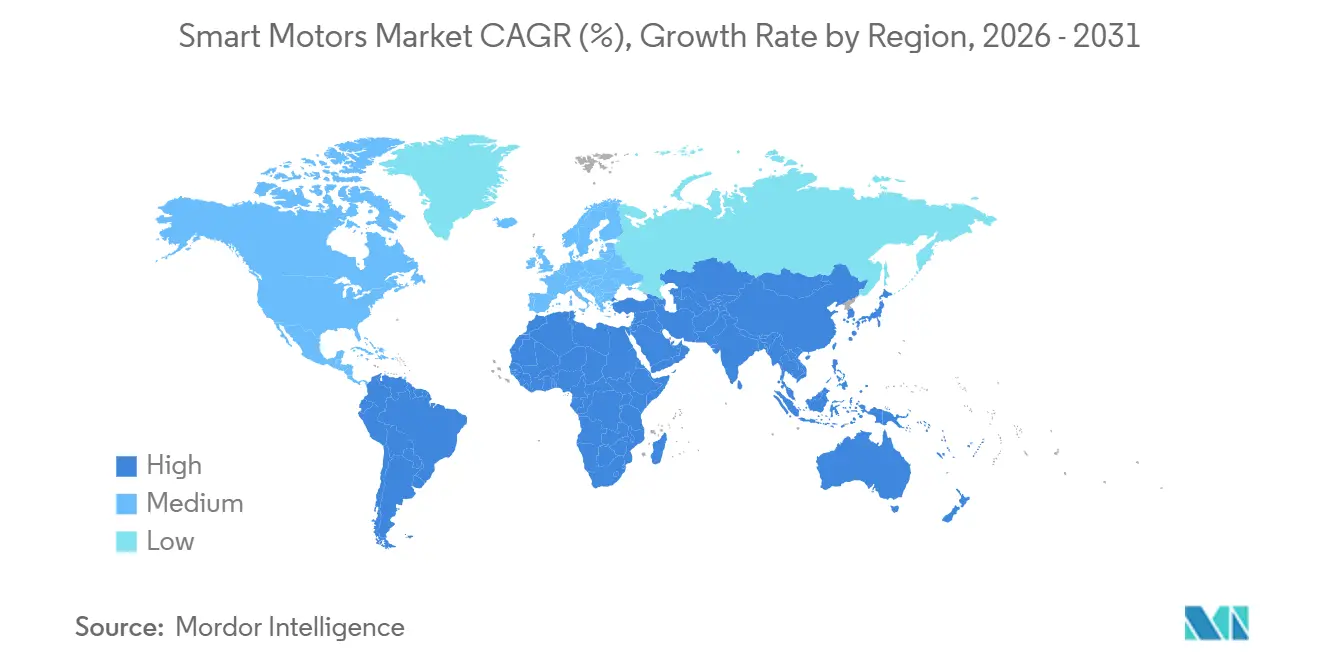

- By geography, Asia-Pacific captured 39.74% of 2025 demand, while the Middle East is on track for the highest 6.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Cost of Integrated Motor-Drive Packages Due to SiC/GaN Power Devices | +1.2% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Mandates on Industrial Energy Efficiency Standards in Europe and China | +1.1% | Europe and China, spillover to ASEAN and Latin America | Short term (≤ 2 years) |

| Convergence of Smart Motor Controls with Edge AI for On-Device Optimization | +0.9% | Global, concentrated in industrial automation hubs | Medium term (2-4 years) |

| Rapid Electrification of HVAC Systems in Commercial Buildings | +0.8% | North America, Europe, and Middle East | Short term (≤ 2 years) |

| Increasing Adoption in Autonomous Mobile Robots and AGVs | +0.7% | Asia-Pacific core, expanding to North America and Europe | Medium term (2-4 years) |

| Rising Deployment in Offshore Wind Turbine Pitch and Yaw Systems | +0.5% | Europe and Asia-Pacific coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Cost of Integrated Motor-Drive Packages Due to SiC/GaN Power Devices

Wide-bandgap silicon carbide and gallium nitride transistors are reducing material costs by nearly one-fifth, enabling suppliers to house the motor, inverter, and feedback sensor in one enclosure without a premium.[1]IEEE Power Electronics Society, “Wide Bandgap Power Devices,” ieee.org Switching frequencies above 100 kHz reduces passive component size by 40%, making integrated units lighter and easier to mount in collaborative robots and electric-vehicle coolant loops. Conduction losses fall by 30-35%, a critical gain for battery-powered mobile robots that must extend runtime between charges. Global wafer output for 200 mm SiC increased in 2025, driving module prices down from USD 85 to USD 62 and making integrated packages feasible for mid-range industrial drives. Adoption is fastest in North America and Europe, while Chinese fabs remain 12-18 months behind in yield and reliability benchmarks.

Mandates on Industrial Energy Efficiency Standards in Europe and China

The European Union extended IE4 requirements to motors below 0.75 kilowatts in July 2025, and China barred IE2 motors from new projects in January 2024, converging global rules around IE3-plus efficiency. A 75-kilowatt IE4 motor with a drive consumes 8-12% less power, recouping the USD 1,800 premium within 18 months at industrial electricity tariffs.[2]International Electrotechnical Commission, “IEC 60034-30-1 Energy Efficiency Standard,” iec.ch Metals, cement, and pulp producers are thus retiring motors ahead of failure, favoring turnkey integrated units that ship with verified efficiency curves. Thailand drafted an IE3 mandate for 2027, and Vietnam is consulting on IE4 targets, signaling spillover across ASEAN. Accelerated replacement cycles underpin rising demand despite macroeconomic headwinds.

Convergence of Smart Motor Controls with Edge AI for On-Device Optimization

Microcontrollers running TinyML models identify bearing wear, insulation degradation, and load imbalance with up to 96% accuracy while eliminating cloud latency. In 2025, Siemens Gamesa equipped 180 offshore turbines with AI-enabled pitch-control drives, reducing unplanned call-outs by 28%.[3]Siemens Gamesa Renewable Energy, “Hollandse Kust Zuid Deployment,” siemensgamesa.com Autonomous mobile robots now adjust torque on the fly based on floor friction and payload, extending battery life by 12-15%. Water-treatment pumps preload speed profiles based on historical demand, reducing inrush energy by more than one-fifth. The cost of adding an AI-ready controller has fallen below USD 15, making predictive maintenance mainstream for mid-range drives.

Rapid Electrification of HVAC Systems in Commercial Buildings

Variable-speed electronically commutated motors deliver airflow in 1% increments, slicing HVAC energy by up to 30% in data centers and office towers. California’s Title 24 and the European Energy Performance directive require demand-controlled ventilation, pushing building owners toward smart motors with BACnet or Modbus interfaces. Microsoft’s Iowa data center achieved a 1.12 PUE in 2025 using liquid-cooling loops regulated by smart pumps that throttle flow to server thermal load. Global heat-pump installations rose 18% in 2025, each unit containing two to four smart compressors and fan motors. Middle East commercial projects are gaining momentum as ISO 50001 certification is now mandatory for new government facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity Vulnerabilities in Networked Motor Systems | -0.6% | Global, acute in critical infrastructure sectors | Short term (≤ 2 years) |

| Fragmented Communication Protocol Ecosystem Limiting Interoperability | -0.5% | Global, severe in multi-vendor brownfield sites | Medium term (2-4 years) |

| Prolonged Supply Chain Constraints for Power Electronics Components | -0.4% | Global, centered on Asia-Pacific fabs | Short term (≤ 2 years) |

| Skills Gap in Condition-Based Maintenance Analytics | -0.3% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Vulnerabilities in Networked Motor Systems

Fourteen firmware flaws exposed in 2025 enabled unauthenticated Modbus-TCP writes that could cause smart drives to turn off emergency stops. Only 38% of 2025 shipments met SL2 of IEC 62443, and fewer than 12% reached SL3, which mandates encryption and role-based access controls. Water utilities and refineries face the greatest risk after a 2024 breach at a European treatment plant via an unpatched PROFINET drive. Hardening steps, network segmentation, signed firmware, and intrusion detection add USD 300-800 per motor and require dual-skilled OT-security engineers, a resource that 64% of operators lack.

Fragmented Communication Protocol Ecosystem Limiting Interoperability

More than 42% of discrete manufacturers ran three or more fieldbus or Ethernet protocols in 2025, forcing gateways to introduce up to 15 ms of latency and complicating time-critical motion. Only 29% of new smart motors shipped with native OPC UA servers, keeping multivendor plants dependent on USD 450-900 external converters. Vendor tool-chain lock-in inflates lifecycle costs by 12-18% when users mix PROFINET, EtherNet/IP, and EtherCAT lines. Until IEEE 802.1 Time-Sensitive Networking reaches scale, interoperability issues will slow the broad convergence of OT and IT networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integrated Units Gain as Commissioning Complexity Drives Consolidation

Integrated motor-drive packages are growing faster than the overall smart motors market, with a 6.31% CAGR, capturing users who value 30-40% shorter installation times and reduced electromagnetic interference troubleshooting. Standalone variable-speed drives still accounted for the largest 44.56% of revenue in 2025 because retrofit projects often only replace the controller, not the motor. Yet integrated designs are penetrating mobile robots and wash-down food lines, where single-housing IP69K units avoid the cost of stainless-steel enclosures.

The shift aligns with distributed control trends; a packaging machine needing 40 servo axes can free an entire cabinet row by mounting integrated drives on each motor shaft. Asia-Pacific retains an appetite for standalone drives, as capital budgets favor incremental upgrades, but China’s subsidy programs are tipping state enterprises in heavy industries toward integrated platforms above 500 kilowatts. Modular architectures persist, allowing operators to replace either the motor or the drive independently after a fault.

By Power Rating: Sub-Kilowatt Segment Accelerates on Robotics and Building Automation

Sub-1 kilowatt motors are advancing 6.34% each year as e-commerce warehouses deploy autonomous mobile robots that carry four to six 0.2-0.5 kilowatt wheel drives per unit. In contrast, the 1-10 kilowatt class retained 38.72% of 2025 revenue and constitutes the backbone of industrial pumps and conveyors. Integrated 0.5-kilowatt packages fell to USD 180-240 per unit in 2025, enabling smart control of applications that once used fixed-speed induction motors.

Above 10 kilowatts, growth trails the market average because oil, gas, and metals plants prioritize ruggedness over energy savings, opting for predictive maintenance upgrades rather than full motor replacement. Building automation adds volume at the low end: a mid-size office may contain 100 variable-air-volume boxes, each with a 0.1-0.3 kilowatt smart actuator. Consequently, the smart motors market size for sub-kilowatt solutions is poised to close the gap with mid-power units over the forecast period.

By Communication Protocol: Ethernet/IP Gains as North America Converges OT and IT Networks

PROFINET anchored 36.82% of 2025 protocol deployments in European auto and pharma plants, but Ethernet/IP is expected to outpace all peers with a 6.51% CAGR to 2031. North American manufacturers migrating from DeviceNet favor Ethernet/IP because it meshes with existing enterprise data infrastructures. Modbus TCP endures in water and building systems for its simplicity, while EtherCAT, POWERLINK, and CC-Link IE split regional and niche share.

A 2025 Cisco survey found that 68% of plants plan to adopt converged Ethernet by 2028, boosting demand for multi-protocol drives that switch between standards via firmware updates. Time-Sensitive Networking features in IEEE 802.1 close deterministic gaps relative to PROFINET, leveling performance between the two. As a result, the smart motors market share held by fieldbus protocols dropped to 17% in 2025, down from 34% in 2020, indicating accelerating Ethernet dominance.

By Application: Commercial Segment Outpaces as Data Centers and HVAC Drive Demand

In 2025, industrial applications dominated shipments, making up 42.79% across sectors like oil, gas, metals, and water. This highlights the continued reliance on industrial operations for key resources and infrastructure. However, commercial projects are projected to grow at a 6.56% CAGR, fueled by the electrification of HVAC systems and the increasing cooling demands of data centers. These trends are driven by the growing need for energy efficiency and sustainability in commercial operations. To achieve PUE targets under 1.2, a typical 10-megawatt data center now incorporates 200-300 smart motors into its air handlers and cooling-tower fans, showcasing the integration of advanced technologies to optimize performance and reduce energy consumption.

Oil and gas operators install variable-frequency drives on electric submersible pumps, extending well life by 8-12%. Mining conveyors use regenerative drives, saving USD 40,000-80,000 in annual energy per kilometer. Municipal water plants, where power costs account for 30-40% of budgets, save USD 15,000-25,000 annually after upgrading high-service pumps. Meanwhile, commercial office retrofits comply with the 2024 International Energy Conservation Code, which mandates variable-speed fans for large air handlers.

Geography Analysis

Asia-Pacific held the highest smart motors market share of 39.74% in 2025, supported by China’s CNY 300 billion (USD 42 billion) energy-efficiency fund that upgraded 1.8 million motors during the year. India’s Production Linked Incentive program for white goods and air conditioners added 1.2 million units of annual capacity in 2025, while Japan and South Korea pushed servo-motor output for robotics and semiconductor fabs. Regional demand is reinforced by local suppliers that tailor integrated motor-drive packages to national standards, shortening approval cycles for government projects. As supply chains diversify away from single-source components, multinational original-equipment manufacturers are co-locating electronics and motor assembly lines in Vietnam, Thailand, and Indonesia to contain logistics risk. Such investments keep the region firmly positioned as the volume anchor of global shipments.

The smart motors market size in the Middle East is projected to expand at a 6.71% CAGR between 2026 and 2031, the fastest worldwide, as Saudi Arabia’s Public Investment Fund channels USD 20 billion into the NEOM industrial city, where IE4 motors and ISO 50001 certification are mandatory. The UAE’s Dubai Electricity and Water Authority introduced time-of-use tariffs that cut off-peak power prices by 18%, persuading factories to retrofit variable-speed drives for compressors, pumps, and fan arrays. Qatar’s USD 13 billion petrochemical expansion specifies explosion-proof smart motors up to 500 kilowatts, while Oman’s desalination projects favor corrosion-resistant integrated units for high-salinity pumps. Collectively, these initiatives convert large-scale infrastructure spending into durable equipment orders.

North America accounted for roughly 24% of 2025 revenue, energized by the Inflation Reduction Act tax credits that reimburse 30% of plant upgrades, including motor replacements in battery, semiconductor, and pharmaceutical facilities. Europe followed with a 22% share, anchored by strict Ecodesign rules and more than 4 gigawatts of annual offshore wind additions that demand pitch- and yaw-control drives. South America and Africa together made up 14% of spending, led by Brazilian mining conveyors and South African water-treatment pumps, both of which benefit from regenerative drive technology that reduces operating costs. Cross-border trade agreements and rising local-content rules are prompting suppliers to license assembly to regional partners, ensuring service coverage and shorter lead times.

Regulatory Landscape

Energy-efficiency regulation remains the main compliance driver for smart motors and associated drives, anchored in IEC efficiency classes and regional implementing rules. The IEC 60034-30-1:2025 update introduced IE5 efficiency class limits for line-operated AC motors, which many national regimes use when setting minimum performance requirements for motors used in industrial and building applications.

In the European Union, Ecodesign requirements for electric motors and variable speed drives under Regulation (EU) 2019/1781 are in formal review that began in December 2024 and is scheduled to conclude in Spring 2027. This timeline keeps OEMs focused on verifiable efficiency documentation for motor-drive systems. In the United States, the Department of Energy published a final rule in January 2025 for energy conservation standards covering Expanded Scope Electric Motors (ESEMs), with mandatory compliance effective January 1, 2029, which raises the importance of designing products that can be certified across broader motor categories. Standards adoption is also being refreshed at the national level, such as the January 2026 publication of BS EN IEC 60034-30-1:2026 by BSI, supporting alignment with the updated international framework for efficiency classification.

Value Chain Analysis

The smart motors value chain starts with upstream materials and components, including electrical steel and copper for stators and rotors, bearings, permanent magnets or magnet-free designs, and power electronics. It then moves into motor manufacturing, drive and control electronics, embedded firmware, and industrial networking components. A key upstream dependency is semiconductors used for control and connectivity, including industrial-grade MCUs, functional-safety ICs, and communication ICs for factory and building protocols. Concentrated sourcing and long lead times for certain industrial IC categories increase the premium on multi-sourcing and platform reuse across motor families.

Midstream, manufacturers integrate the motor, variable-speed drive or inverter, sensors (current, temperature, vibration), and communications into either discrete motor-plus-drive offerings or integrated motor-drive packages that simplify commissioning and maintenance. The downstream chain includes OEMs (HVAC, pumps, compressors, conveyors, robotics and AMR, and process equipment), system integrators, industrial distributors, and aftersales service organizations that provide commissioning, condition monitoring, and cybersecurity hardening for networked assets. Increasing product integration is also visible at the component level, including Toshiba commencing sample shipments (April 2026) of a SmartMCD device that combines a microcontroller and motor driver in a compact package, supporting tighter integration of motor control electronics and smaller form-factor smart motor designs in relevant applications.

Competitive Landscape

The competitive field remains moderately concentrated, with ABB, Siemens, Rockwell Automation, Nidec, and Schneider Electric commanding about 45% of global revenue in 2025. These leaders bundle hardware, firmware, and analytics into subscription contracts that stabilize margins even as component prices fall. Their combined scale allows preferred access to scarce silicon-carbide modules, giving them delivery advantages over smaller rivals during supply constraints.

Mid-tier manufacturers such as WEG, Yaskawa, and Emerson focus on regional strength or niche power bands, often undercutting global brands by 10-15% while meeting local certification needs. Strategic moves underscore this divergence: ABB’s USD 280 million stake in Shanghai Moons’ Electric expanded its sub-5-kilowatt catalog, and Siemens opened a USD 165 million Erlangen plant that automates winding and testing to cut cycle time by 35%. Nidec’s partnership with Microsoft integrates Azure IoT Edge functions into M-FORCE servos, eliminating the need for separate gateways for predictive analytics. Each initiative seeks to lock customers into proprietary ecosystems where switching costs rise over time.

Emerging disruptors cultivate white-space opportunities. Turntide Technologies markets switched-reluctance motors that eliminate rare-earth magnets and cut material costs by up to 40%, appealing to buyers exposed to volatile neodymium prices. Beckhoff and SEW-Eurodrive promote cabinet-free architectures, placing IP69K integrated drives at the machine frame and reclaiming valuable floor space in packaging and food lines. At the high-power end, Moog and Bosch Rexroth court aerospace, defense, and marine users who demand custom-engineered 1-megawatt solutions with 98% efficiency and MIL-STD-810 qualification. With no single player exceeding 20% share, the smart motors arena remains competitive enough for both incremental innovation and radical design alternatives.

Smart Motors Industry Leaders

ABB Ltd

Siemens AG

Schneider Electric SE

Rockwell Automation Inc.

Nidec Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is helping end users meet tightening efficiency requirements and system-level compliance through motor-plus-drive upgrades, especially where legacy fixed-speed installations dominate pumps, fans, and compressors. As IEC 60034-30-1:2025 raises the efficiency benchmark to higher classes, including IE5, demand shifts toward integrated sensing, variable-speed operation, and verified efficiency curves across the combined motor-drive system. This creates room for suppliers that can package hardware with commissioning tools and secure connectivity aligned to industrial security requirements.

Opportunities also track deeper integration of power electronics and digital control into the motor platform, reducing size and assembly complexity while enabling embedded diagnostics. Corporate investments and product programs illustrate this direction: Mercedes-Benz began large-scale production of axial flux motors at its Berlin-Marienfelde site in June 2026 with AI-supported quality control and new production steps, showing broader industrial adoption of highly automated motor manufacturing approaches that can carry over into smart motor production methods. On the drives and module side, Mitsubishi Electric and Semikron Danfoss announced joint development (June 2026) of a new standard power module package for 3-level T-type circuits, which supports more compact and efficient inverter designs that can be incorporated into smart motor drive architectures.

Recent Industry Developments

- May 2026: ABB introduced an IE6 hyper-efficiency magnet-free motor for hazardous areas, certified to ATEX and IECEx requirements. The launch expands high-efficiency options for regulated environments where motor replacements are driven by safety certification and lifecycle energy costs, supporting upgrades in oil and gas, chemicals, and other hazardous-duty settings.

- December 2025: ABB acquired a 60% stake in Shanghai Moons' Electric for USD 280 million to broaden its sub-5 kilowatt portfolio for building automation. This acquisition strengthens ABB's position in high-volume low-power smart motor applications and adds regional breadth in Asia-centric supply and product development.

- January 2024: China barred IE2 motors from new projects, pushing new installations toward higher-efficiency classes. This policy step accelerates replacement and specification upgrades in industrial projects, increasing pull-through for smart motors paired with variable-speed operation and monitoring features.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the smart motors market is defined as revenue generated from motors that combine a motor with electronics and control features, so speed, torque, and status can be monitored or adjusted locally or over a network for end-use operations.

Scope exclusions: We exclude stand-alone sensors, PLCs, and plant software that may connect to motors but are sold as separate automation products.

Segmentation Overview

- By Component

- Variable Speed Drive

- Motor

- Integrated Motor-Drive

- By Power Rating

- Below 1 kW

- 1-10 kW

- Above 10 kW

- By Communication Protocol

- Ethernet/IP

- PROFINET

- Modbus TCP

- Other Communication Protocols

- By Application

- Industrial

- Oil and Gas

- Metal and Mining

- Water and Wastewater

- Food and Beverage

- Chemicals

- Commercial

- HVAC and Building Automation

- Data Centers

- Automotive

- Aerospace and Defense

- Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping where smart motors show up in real demand, mainly industrial automation, building equipment, and selected vehicle and defense uses. To ground the model, we relied on public references such as the US Energy Information Administration (EIA) for industrial energy signals, the International Energy Agency (IEA) for efficiency trends, US Census Bureau trade data for motor and drive related flows, and NEMA or IEC efficiency standards to understand what qualifies as an energy efficient motor and drive combination.

We also reviewed annual reports and investor materials from motor and automation suppliers to capture product mix direction, regional exposure, and typical pricing commentary. In parallel, patents and technical publications were scanned (through a paid patent database subscription) to track where integrated motor-drive designs and connectivity features were being emphasized. The sources listed above are not exhaustive, and many other public and paid references were used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work focused on interviews and structured questionnaires with motor suppliers, drive and automation channel partners, and large users in factories and commercial facilities. Respondent feedback was used to confirm what buyers call a smart motor in practice, how often variable speed drives are bundled versus integrated, and how communication protocols are selected for new installations across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 46% |

| Mid tier: 51% | Functional/Unit leaders: 26% | EMEA: 33% |

| Smaller Players: 21% | Managers: 60% | Americas: 21% |

Market-Sizing & Forecasting

Sizing began with a top-down approach where we reconstruct demand from the installed base of motor-driven equipment and the rising share of variable speed control, and then apply smart motor penetration by application and region. The model was kept practical by using a small set of measurable inputs, including industrial automation spending direction, the share of variable speed drives in motor control, typical power-rating mix (below 1 kW, 1 to 10 kW, and above 10 kW), and the adoption pace of Ethernet-based industrial networks that support connected motor monitoring.

To make sure totals were not drifting, we also ran selective bottom-up checks using sampled average selling prices and estimated unit volumes from supplier and distributor conversations, followed by sanity checks against segment cues such as the reported share of variable speed drives and growth in integrated motor-drive packages. For forecasting, scenario analysis was used because policy and capex cycles can shift quickly, and then yearly growth was adjusted using expert expectations on energy efficiency upgrades, retrofit intensity, and new-build activity by region. Where bottom-up signals were thin in smaller countries, we used proxy ratios from similar industries and then re-checked with local feedback before finalizing.

Data Validation & Update Cycle

Validation was done through triangulation across demand signals, supplier commentary, and macro indicators that should move in the same direction for smart motors. We flagged outliers when a country or application showed growth that did not fit known plant investment cycles, trade movement, or protocol adoption, and those parts were revisited with fresh assumptions and follow-up questions.

Before sign-off, the model goes through a multi-step analyst review where key inputs, unit conversions, and currency timing are rechecked, and sensitivity ranges are tested for the largest drivers. Reports are refreshed annually, and interim updates are made when material events occur, such as large regulatory changes on motor efficiency or sharp shifts in industrial production. Right before delivery, an analyst performs a final pass to ensure the latest public releases and field notes are reflected.

Mordor Intelligence's Smart Motors Market Sizing Compared With Other Published Estimates

Published market sizes for smart motors often do not match because the boundary of what is counted can shift, and the timing of the currency year and base year also varies. We looked at the most common differences that show up when definitions mix smart motors with broader motor control hardware, or when forecasts are stretched across longer horizons.

Evidence like the share of variable speed drives within smart motor value, the split by power rating, and cross-checks from supplier and distributor channel feedback are what keep Mordor Intelligence's estimate tied to the addressable revenue pool for smart motors sold as motor plus embedded control capability (not adjacent automation hardware).

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.16 B (2025) | |

| Industry Publisher A | USD 2.10 B (2025) | The estimate appears to use a wider voltage-led product scope and a longer forecast frame, which can smooth year-to-year pricing and understate near-term mix shifts such as integrated motor-drive uptake. |

| Industry Publisher B | USD 2.45 B (2024) | This figure is anchored to a different base year and leans heavily on automotive end uses described on the page, which can inflate totals if conventional small motors in vehicles are grouped under the smart motor label. |

Overall, the spread is mainly explained by how tightly smart motors are defined, which years are compared, and how pricing and adoption are stepped forward during forecasting. By keeping the demand pool connected to power-rating mix, drive integration, and practical protocol adoption checks, our final number stays traceable to inputs that can be revisited and repeated.

Key Questions Answered in the Report

What is the projected value of the smart motors market by 2031?

It is forecast to reach USD 3.03 billion by 2031, reflecting a 5.76% CAGR from 2026.

Which component segment is expanding the fastest?

Integrated motor-drive packages, growing at a 6.31% CAGR through 2031 as users prefer factory-calibrated units.

Why are sub-1 kilowatt smart motors in high demand?

Autonomous mobile robots and building-automation actuators require compact, efficient drives, pushing this band to a 6.34% CAGR.

Which region shows the highest growth momentum?

The Middle East leads with a 6.71% CAGR, driven by large industrial-city and energy-efficiency projects.

How are energy-efficiency mandates affecting adoption?

European and Chinese IE4 regulations shorten payback periods, prompting early motor replacement and boosting sales of high-efficiency designs.

What major cybersecurity risk impacts smart motor uptake?

Firmware vulnerabilities that allow unauthorized control over networked drives, compelling operators to invest in certified secure devices.

Page last updated on: