Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.26 Billion |

| Market Size (2031) | USD 8.02 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sortation Systems Market Analysis by Mordor Intelligence

The sortation systems market size is expected to grow from USD 5.96 billion in 2025 to USD 6.26 billion in 2026 and is forecast to reach USD 8.02 billion by 2031 at 5.08% CAGR over 2026-2031. Moderate but steady expansion shows the field is transitioning from novel automation toward core infrastructure. Cross-belt equipment is also the fastest-expanding sorter platform, confirming a shift from premium niche toward de-facto standard. The convergence of dominant position and accelerated expansion signals cross-belt technology's evolution from premium solution to industry standard, driven by its superior handling of diverse package geometries and weights. E-commerce and omnichannel operators dominate demand, illustrating that parcel automation remains in a long runway. Hardware continues to account for majority of sales, yet the shift toward software-centric value creation reflects industry recognition that competitive differentiation increasingly depends on algorithmic efficiency rather than mechanical speed alone. Geographically, APAC leads highest share in 2024, fuelled by Chinese cross-border e-commerce and Indian automation investments exemplified by Daifuku’s 2025 plant launch

Key Report Takeaways

- By sorter type, cross-belt technology led with 37.60% of sortation systems market share in 2025 and is expanding at 7.52% CAGR through 2031.

- By end-user, e-commerce and omnichannel retail held 40.70% revenue in 2025; airports represent the fastest-growing institutional segment at 6.66% CAGR through 2031.

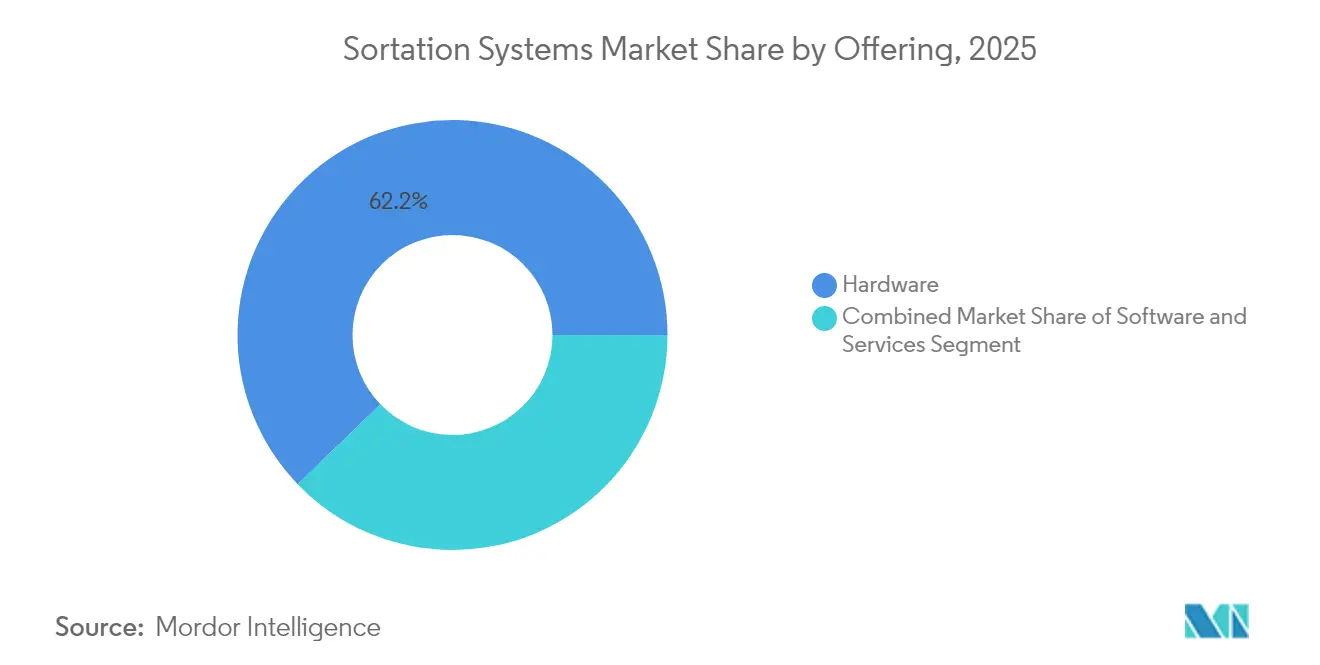

- By offering, hardware commanded 62.20% share of the sortation systems market size in 2025, while software is climbing at 7.01% CAGR to 2031.

- By throughput, high-speed installations (10,000-25,000 pph) represented 45.60% of 2025 deployments; ultra-high-speed solutions are growing 6.31% annually.

- By region, APAC held 35.90% revenue in 2025, and the region is accelerating at 8.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sortation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel surge | +1.8% | Global with APAC volume leadership | Medium term (2-4 years) |

| Labor-cost escalation and scarcity | +1.2% | North America and EU core; spreading in APAC | Short term (≤ 2 years) |

| SKU proliferation demanding accuracy | +0.9% | Global high-density e-commerce zones | Long term (≥ 4 years) |

| Airport baggage-handling upgrades | +0.7% | Global hub modernisation focus | Medium term (2-4 years) |

| AI-vision powered dynamic sorters | +0.6% | North America and EU early adoption | Long term (≥ 4 years) |

| Sustainability-driven energy savings | +0.4% | EU regulatory leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce parcel surge

Parcel growth reshapes capacity planning. United States annual parcel flow is forecast to hit 28 billion by 2028, a 5% yearly increase. Chinese cross-border sellers accelerate digitalisation and employ generative AI to improve demand forecasting, allowing facilities to move from reactive peaks to predictive load balancing.[1]FreightWaves, "Study: US annual parcel shipping volumes to grow 5% through 2028.", freightwaves.comSorters that self-adjust to volume spikes and shift routing rules on the fly now underpin peak-season resilience.

Labor-cost escalation & scarcity

Warehouse payroll inflation and technician shortages compress deployment timelines. A 63% majority of operators cite skilled labour gaps as the top obstacle, while 770,000 supply-chain technician vacancies are expected by mid-decade.[2]DC Velocity, "Getting around the warehouse tech labor crunch.", dcvelocity.com Procurement criteria now weigh remote diagnostics and simplified maintenance as heavily as nominal throughput.

SKU proliferation demands accuracy

Rising product variety turns accuracy into customer retention metric. Advanced vision suites now recognise more than 30 material types and orientations, delivering 99.9% order fulfilment precision. Machine-learning models refine settings continuously, important for pharmaceuticals and food lines that mandate strict handling scripts.

Airport baggage-handling upgrades

Airports consolidate legacy layouts into single, high-speed networks to trim transfer times and energy usage. Seattle-Tacoma’s 8,200-bag per hour rebuild and Salt Lake City’s 3,540-bag energy-efficient project illustrate integrated overhauls superseding piecemeal add-ons. Baggage projects often specify cross-belt or tilt-tray modules fitted with RFID and permanent-magnet drives to cut idle power draw.

AI-vision powered dynamic sorters

Vision sensors linked to deep-learning cores adapt routing rules in milliseconds, allowing belt speeds to vary by parcel type and destination. Early adopters in North America and Europe report 20-30% productivity up-lifts due to reduced manual exception handling.[3]Siemens Logistics, “Siemens Logistics Newsroom,” siemens-logistics.com

Sustainability-driven energy savings

EU environmental directives drive operators to audit energy usage and cut emissions. Conveyors using regenerative braking and variable-frequency drives lower energy draw by 15-20%, creating a measurable compliance benefit. [4]MDPI Sustainability, "An Evaluation of the Environmental Impact of Logistics Activities: A Case Study of a Logistics Centre.", mdpi.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and ROI uncertainty | -1.1% | Global, mid-market adopters most affected | Short term (≤ 2 years) |

| Skilled-technician shortage | -0.8% | North America and EU acute; emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capex & ROI uncertainty

Full-scale sorters require multimillion-dollar outlays plus facility remodelling. Operators demanding 18-24-month payback often delay adoption, favouring modular add-ons that can stretch ROI but impair long-term efficiency. Quantifying soft returns such as reduced churn and customer loyalty remains challenging.

Skilled-technician shortage

Advanced equipment cuts unplanned downtime by up to 90% when predictive maintenance is active, yet many plants cannot recruit the specialised staff needed to run these programmes. Vendors now offer subscription maintenance and cloud analytics, but dependence on stable connectivity introduces new risk vectors during peak events.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sorter Type: Cross-belt adaptability cements leadership

Cross-belt units generated 37.60% revenue in 2025 and are set to rise 7.52% annually, giving the sorter class the largest and fastest path within the sortation systems market. Facilities prefer its capability to handle irregular packages without speed loss. Tilt-tray and sliding-shoe equipment stay relevant where either fragile goods or uniform cartons dominate. Narrow-belt installations persist in legacy buildings with limited floor plates. Pop-up wheel and diverter systems continue to fade as operators pursue higher flexibility and uptime.

The sortation systems market size for cross-belt platforms is projected to exceed USD 3.15 billion by 2031, reflecting entrenched migration from niche to mainstream. Meanwhile, sliding-shoe products hold a mid-single-digit sortation systems market share and show low-single-digit expansion as they retain fit in apparel and parcel hubs demanding gentle flow control.

By End-User Industry: E-commerce strength endures

E-commerce and omnichannel retailers captured 40.70% of 2025 turnover and are increasing 7.18% annually. Post-and-parcel operators remain the second-largest cohort, yet margin pressure converts automation into a cost-containment lever rather than growth catalyst. Airports contribute stable, project-based opportunities as hubs modernise baggage loops. Food, beverage and pharma lines embrace high-accuracy sorting to honour compliance, fuelling adoption of sensor-laden cross-belt and high-speed tray units.

By 2031, the e-commerce segment is expected to command more than USD 3.27 billion of the sortation systems market size. Airport programmes, though lumpy, could achieve mid-single-digit CAGR on the back of combined passenger and cargo investments.

By Offering: Software ascends in value hierarchy

Hardware still delivers 62.20% 2025 revenue, but software modules grow 7.01% annually as warehouses seek real-time orchestration. Platforms like Hai Robotics’ HaiQ process 10,000 concurrent events and integrate with WMS, enabling predictive order release and dynamic batching. Services covering system design, maintenance and continuous improvement hold the fastest momentum, reflecting buyer preference to outsource specialist know-how.

The sortation systems market share held by software could reach 41.35% by 2031 as analytics and machine learning drive headline efficiency gains. Hardware differentiation will likely pivot toward energy-management and modularity while leaving optimisation logic to cloud-native stacks.

By Throughput Rate: Ultra high-speed accelerates

High-speed lines (10,000-25,000 pph) account for 45.60% deployments, aligning with typical parcel-centre volumes. Ultra high-speed (>25,000 pph) is climbing at 6.31% CAGR, driven by consolidation of fulfillment hubs and peak-season burst requirements. New Zealand Post’s Auckland hub now processes more than 30,000 parcels hourly, underscoring the business case for top-tier capacity.

Medium-speed machines retain relevance in regional facilities, while low-speed systems shift toward specialist applications such as fragile goods kitting. Investment appetite is trending toward scalable architectures capable of toggling between high and ultra-high throughput via software throttling rather than mechanical change-outs.

Geography Analysis

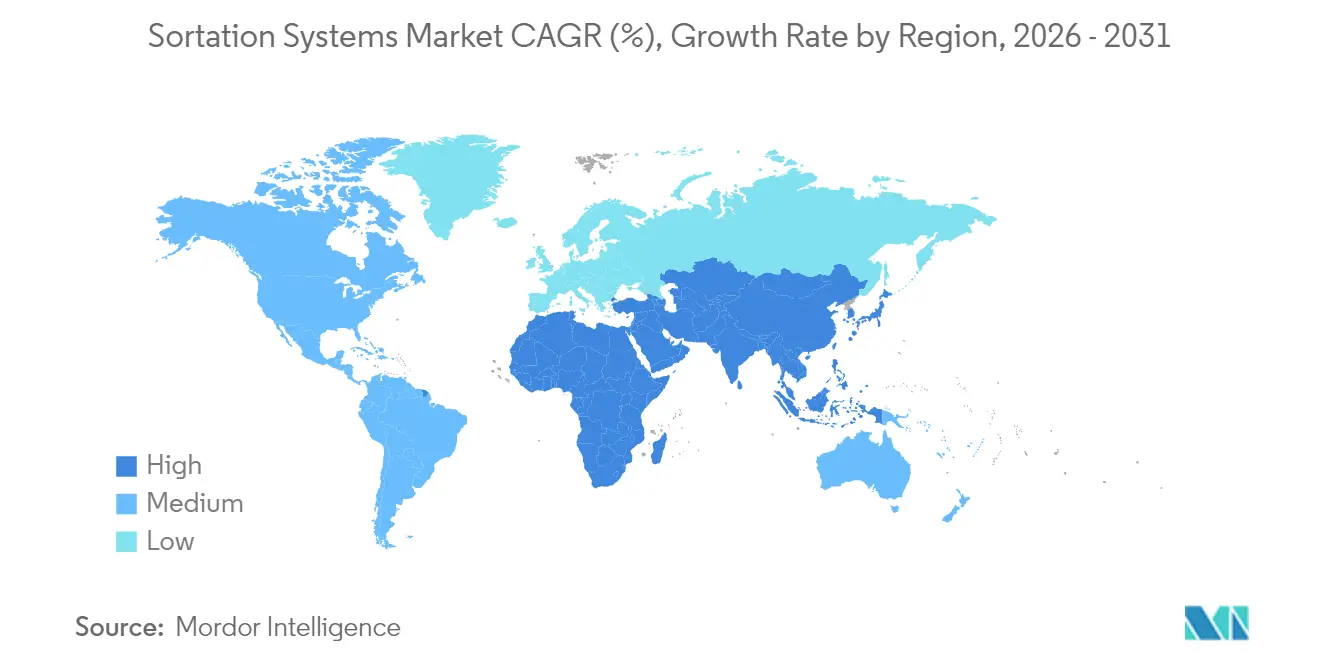

APAC dominated the sortation systems market with 35.90% 2025 share and is expanding at 8.25% CAGR. China’s logistics sector uses AI to lift collection efficiency 30% and delivery 35%, spurring further adoption of intelligent sorters. India’s automation drive is illustrated by Daifuku’s 2025 manufacturing complex designed to localise production and lower lead times. Southeast Asian e-commerce growth also channels investment into flexible sorting in urban micro-fulfilment nodes.

North America remains a core revenue pillar through airport baggage rebuilds and ongoing parcel-centre upgrades. Growth moderates to a mid-4% rate as many first-wave facilities are already automated, causing spend to pivot towards retrofits, software, and sustainability upgrades. Europe balances green mandates with performance. Operators favour energy-efficient motors and recyclable belt materials to align with EU circularity targets.

Middle East and Africa present nascent but rising demand as Gulf airports invest in hub capability and African e-commerce leapfrogs conventional retail. South America exhibits selective uptake in metropolitan corridors where parcel volumes and labour inflation justify capital outlays. Policymakers in Brazil and Chile have signalled intent to streamline customs processes, indirectly supporting sorter adoption in export-oriented logistics parks.

Regulatory Landscape

Sortation systems placed on the EU market are increasingly shaped by Regulation (EU) 2023/1230 (Machinery Regulation), which replaces the Machinery Directive 2006/42/EC and applies in full from January 20, 2027. The regulation strengthens obligations around safety-by-design, documentation, and conformity assessment, and it increases scrutiny on changes made after installation. As a result, operators and integrators are pushed to treat major retrofits and control-system upgrades with the same rigor as new equipment placement.

Alongside binding regulation, voluntary standards are tightening expectations for automated intralogistics and robotics used around sorters. ISO 10218-2:2025 updates safety requirements for industrial robot applications and integration, which is relevant where robotic induction, singulation, or transfer modules are coupled to sortation lines. In 2026, new specifications such as BSI PAS 4000:2026 for digitalized data communication in cargo-handling facilities and IEC PAS 63277:2026 for robotics-related protocols further anchor interoperability and safety practices that buyers increasingly reference in procurement and acceptance testing.

Value Chain Analysis

The value chain begins with component and sub-system suppliers for drives, motors, sensors, controls, and machine vision. OEMs and system integrators then design sorter mechanics (cross-belt, tilt-tray, shoe, and modular transfer elements) and deliver site engineering, software configuration, and commissioning. Software and controls layers (routing logic, diagnostics, and WMS/WCS integration) have become a primary value capture point as operators demand dynamic rule changes, event processing at scale, and remote support to offset technician scarcity.

Downstream, deployment and lifecycle services (installation, preventive maintenance, spares, and upgrades) shape total cost and uptime, particularly in parcel hubs and airport baggage environments where failures can cascade into network delays. Recent industry moves show how the chain is being reshaped by localization, modular platforms, and capability expansion: Daifuku opened a manufacturing plant in India in 2025 to reduce regional lead times, and Vanderlande expanded its airport and cargo sortation footprint through the Siemens Logistics acquisition completed in 2024. Product direction also reflects the shift toward smarter, modular architectures, such as Vanderlande introducing its SPOX line sorter with predictive maintenance and health reporting to reduce wear and improve maintainability.

Competitive Landscape

The sector shows moderate concentration. Vanderlande, Honeywell Intelligrated, Siemens Logistics, Daifuku and Beumer remain top-tier. Vanderlande’s EUR 300 million (USD 325 million) takeover of Siemens Logistics in 2024, and its ownership by Toyota Industries, highlight a tilt toward scale and full-suite capability. Large peers are coupling hardware depth with AI optimisation layers, while smaller entrants push modular, software-first propositions.

Technological advantage centres on predictive maintenance and machine-vision routing. Siemens Logistics systems can decode damaged bag tags in seconds, cutting delays 75%. Amazon’s patented container-chute design enabling 2,100 units per hour for 45kg items underlines how in-house innovations still shape competitive benchmarks. Patent filings cluster around vision, sensor fusion and motor efficiency.

Price competition remains present but secondary to lifecycle value. Vendor lock-in risks and cybersecurity have come to the foreground, prompting operators to request open APIs and third-party service rights. The emergence of subscription-based RaaS (Robotics-as-a-Service) models may reshape revenue recognition and balance-sheet optics over the next five years.

Sortation Systems Industry Leaders

-

Daifuku Co. Ltd

-

Interroll Holding AG

-

Viastore Systems Gmbh

-

Bastian Solutions Inc.

-

Dematic Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are opening where large operators are investing in new or upgraded automated hubs and explicitly tying capacity to advanced sortation and material handling. In 2026, SingPost unveiled a S$30 million automated parcel sortation hub in Tampines to raise parcel processing capacity from 100,000 to 300,000 parcels per day, signaling demand for high-throughput, intelligent sorting in dense urban networks. Similar investment-led whitespace exists in integrated logistics parks and fulfillment networks that combine storage automation with downstream sorting, as shown by Maersk opening its World Gateway II facility in Singapore (2026) with ASRS and robotic handling, and by Maersk announcing a USD 100 million fulfillment center in Hopedale, Massachusetts designed around advanced conveyor and sortation capability.

A second opportunity area involves modular and distributed sortation architectures that support phased deployment and reconfiguration within constrained footprints, consistent with the market shift toward software-centric differentiation. Operators facing capex scrutiny and 18-24 month payback targets are increasingly receptive to modular add-ons, decentralized transfer robots, and tightly integrated vision and controls that reduce exception handling while preserving belt-speed performance. The growing emphasis on interoperability and data models (for example, BSI PAS 4000:2026) also creates room for vendors and integrators that can package open interfaces, cybersecurity-aware remote diagnostics, and multi-vendor orchestration into service contracts rather than one-time hardware projects.

Recent Industry Developments

- June 2026: Daifuku Intralogistics America launched the AutoRoll+ S motorized roller conveyor for distribution center material flow applications. The launch supports Daifuku’s conveyor and line-level handling portfolio that commonly interfaces with sortation systems, strengthening uptime and making maintenance easier in high-throughput operations.

- April 2026: Daifuku Co., Ltd. resolved to acquire Eisenmann GmbH, with the share transfer planned for July 2026. The deal expands Daifuku’s European industrial systems footprint and service coverage, reinforcing its ability to deliver large, integrated automation programs that can bundle sortation, conveying, and adjacent manufacturing or handling processes for global customers.

- November 2024: Vanderlande completed its acquisition of Siemens Logistics for about EUR 300 million (USD 325 million). The transaction deepened Vanderlande’s airport baggage and cargo capabilities, consolidating a larger installed base where high-speed sortation technologies and lifecycle services are central to modernization projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the sortation systems market covers newly installed automated equipment that identifies items and diverts them to preset destinations inside logistics and industrial facilities, including warehouses, distribution centers, parcel hubs, and airports.

Scope exclusions: We exclude conveyors or material handling lines that only transport items and do not perform destination-specific divert or sorting actions.

Segmentation Overview

-

By Sorter Type

- Cross-belt Sorters

- Tilt-tray Sorters

- Sliding-shoe Sorters

- Narrow-belt Sorters

- Push-tray / Split-tray Sorters

- Pop-up Wheel & Diverter Sorters

-

By End-user Industry

- Post & Parcel Operators

- E-commerce & Omnichannel Retail

- Airports (Baggage Handling)

- Food & Beverages

- Pharmaceuticals & Healthcare

- 3PL & Contract Logistics

- Automotive & Industrial Manufacturing

-

By Offering

- Hardware

- Software

- Services (Installation, MRO)

-

By Throughput Rate

- Low-speed (<3k)

- Medium-speed (3k-10k)

- High-speed (10k-25k)

- Ultra High-speed (>25k)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

-

APAC

- China

- Japan

- India

- South Korea

- Australia & New Zealand

- Southeast Asia

- Rest of APAC

-

Middle East & Africa

- GCC (ex-Saudi)

- Saudi Arabia

- Turkey

- South Africa

- Israel

- Rest of Middle East & Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public baselines that explain demand for high-throughput handling, including logistics output, e-commerce activity, and air cargo flows. Sources used included US Census Bureau data, the US Bureau of Labor Statistics, World Bank indicators, UN Comtrade trade statistics, and International Air Transport Association releases for air freight and baggage trends.

We also reviewed manufacturer product literature, public case studies, press releases, annual reports, and investor presentations to understand typical system configurations, capacity ranges, and buying triggers. In a few cases, we relied on paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records to confirm supply-side activity and cross-check pricing direction. These desk research sources are not exhaustive, and we used additional public and paid references to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with system OEMs, component suppliers, integrators, and end users such as parcel hubs, retail fulfillment operators, and airport logistics teams. We used these inputs to verify what gets counted as a sortation system, pressure-test throughput and utilization assumptions, and align regional adoption patterns across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 40% |

| Mid tier: 42% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 19% | Managers: 54% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where logistics and parcel throughput growth, signals tied to warehouse automation spend, and airport and air cargo expansion plans were used to reconstruct the addressable demand pool for new sortation installations. We then corroborated the totals through selective bottom-up checks, using sampled project counts, channel conversations, and a volume-by-typical-ASP approximation for common sorter formats to adjust totals when the model drifted from what the field was seeing.

Key inputs (illustrative) included parcel volume growth and delivery speed expectations, distribution center additions and retrofits, labor availability and wage pressure that shifts ROI math, typical sorter throughput bands (pieces per hour), and lead times for commissioning. Forecasts were developed using scenario analysis, where base, faster adoption, and slower capex cases were tied to macro indicators and then refined using primary feedback on backlog visibility and pricing behavior. When segment-level data was missing in a country, we filled gaps using proxy ratios from comparable markets, and then rechecked the output against known installation intensity and trade flow signals.

Data Validation & Update Cycle

Validation is done through multiple checks that look for outliers in growth, pricing, and regional mix, then we confirm whether the drivers still make practical sense for facility operators. The model outputs are compared against independent signals such as trade flows for key equipment categories, disclosed order momentum, and reported automation investment themes, which are then reviewed in an analyst-to-analyst sign-off step.

The report is refreshed annually, and interim updates are triggered when material events shift demand, such as large policy changes affecting logistics, major airport capex cycles, or abrupt macro slowdowns. Before delivery, a final analyst pass is completed so clients receive the most current view that can still be traced back to clear inputs and repeatable steps.

Mordor Intelligence's Sortation Systems Market Size Versus Other Published Estimates

Published market values for sortation systems do not always match, even when they use similar labels, because the counted equipment, timing, and pricing assumptions can differ. In practice, the biggest gaps usually come from how firms treat automation scope, whether services are included, and how fast ASPs are assumed to move over the forecast.

Order activity signals and installation-only boundaries are the checks that keep Mordor Intelligence focused on newly installed systems (and not broader material handling lines or multi-year service bundles), which is a common place where totals get inflated. Another driver is the year and currency timing used for conversion, since capex cycles and large projects can make one year look unusually strong or weak when the base year differs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.26 B (2026) | |

| Global Consultancy A | USD 7.31 B (2025) | Uses a different base year and commonly includes software and service elements alongside equipment, which can lift totals versus an installation-focused equipment scope. |

| Industry Research Desk B | USD 9.30 B (2024) | Covers automated sortation more broadly and can fold adjacent automation or wider material handling definitions into the count, and it also reflects an earlier pricing and demand cycle year. |

The comparison shows that most of the spread is explained by scope boundaries and timing, not by a disagreement that demand is rising. By keeping the count centered on new system installations and cross-checking growth with throughput and capex signals, the estimate remains easier to audit and repeat when users update assumptions.

Key Questions Answered in the Report

What is the projected value of the sortation systems market by 2031?

The market is forecast to reach USD 8.02 billion by 2031, expanding at a 5.08% CAGR.

Which sorter technology commands the largest share today?

Cross-belt systems hold 37.60% 2025 revenue and are also the fastest-growing platform at a 7.52% CAGR.

Why is software gaining importance in sortation projects?

Software enables real-time optimisation and predictive routing, driving a 7.01% CAGR that outpaces hardware growth.

Which region offers the highest growth opportunity for suppliers?

APAC combines 35.90% current share with an 8.25% CAGR due to Chinese and Indian logistics investments.

How is airline baggage handling influencing sorter demand?

Global hub upgrades, such as Seattle-Tacoma and Salt Lake City, require high-speed, RFID-enabled cross-belt solutions to cut transfer times and energy use.

What strategic moves signal consolidation in the sector?

Vanderlande’s EUR 300 million purchase of Siemens Logistics and Toyota Industries’ ownership illustrate a pivot toward integrated, full-suite service capability.

Page last updated on: