Market Overview

| Study Period | 2020 - 2031 |

|---|---|

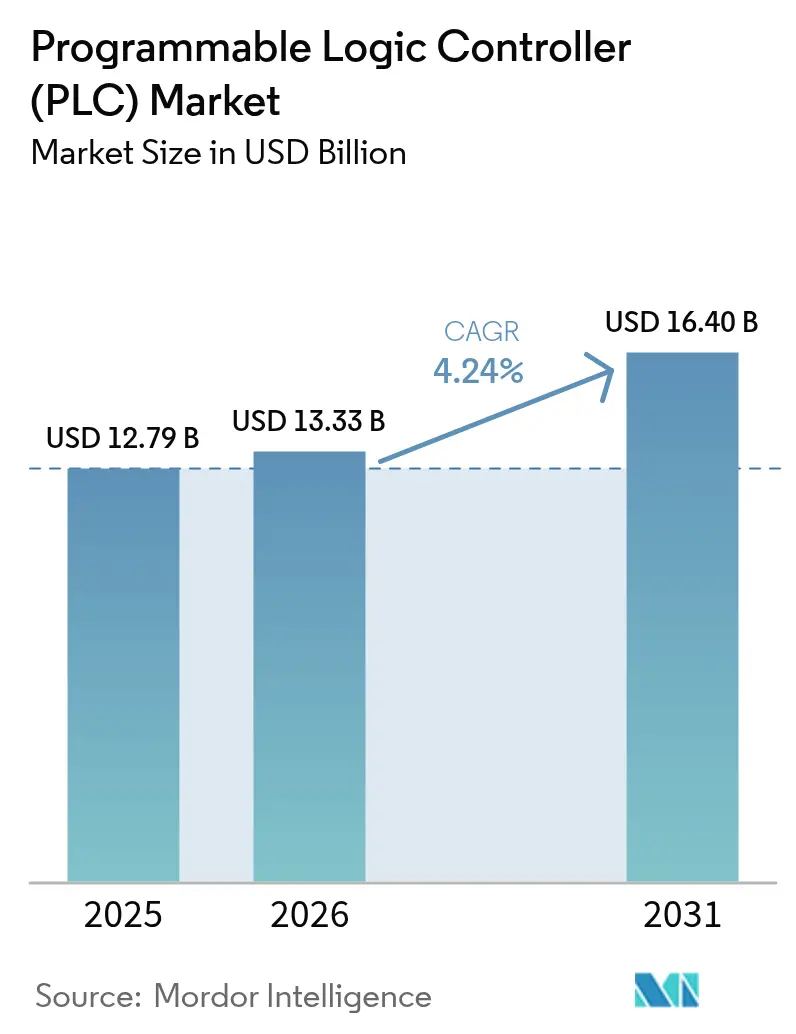

| Market Size (2026) | USD 13.33 Billion |

| Market Size (2031) | USD 16.4 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

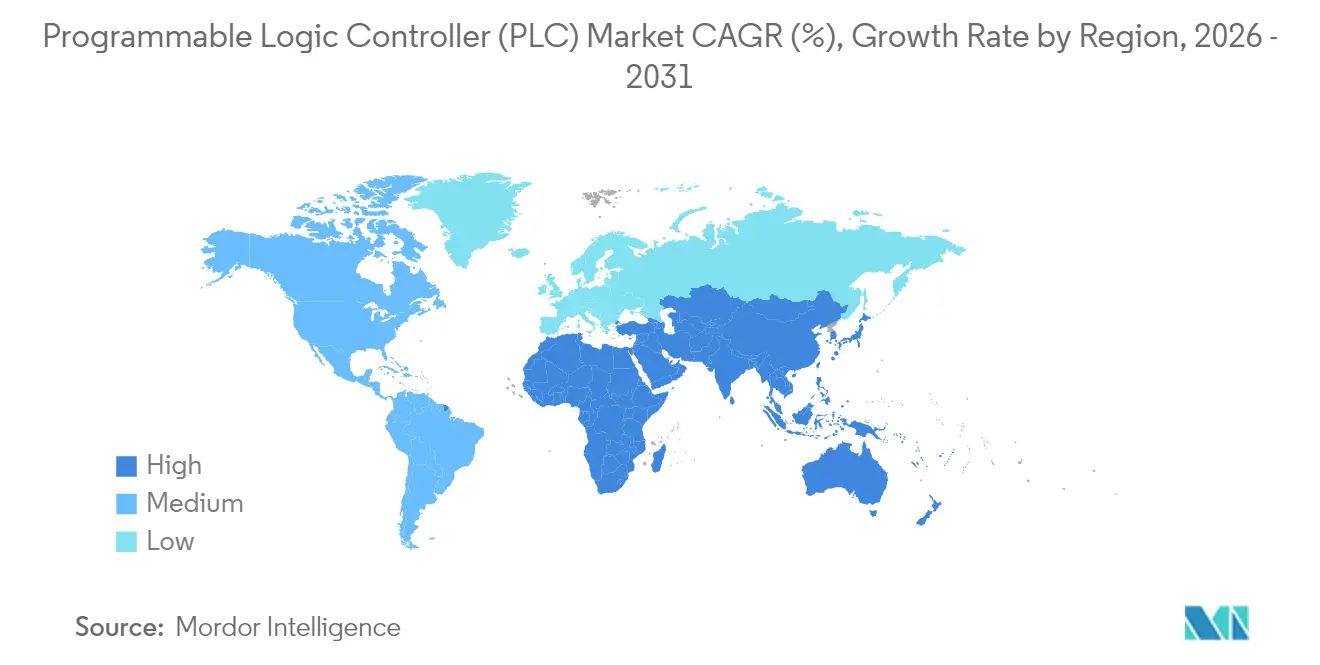

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players-Market-ML.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Programmable Logic Controller (PLC) Market Analysis by Mordor Intelligence

The Programmable Logic Controller Market size is expected to grow from USD 12.79 billion in 2025 to USD 13.33 billion in 2026 and is forecast to reach USD 16.4 billion by 2031 at 4.24% CAGR over 2026-2031.

Steady expansion reflects ongoing modernization of factory floors, rising cybersecurity-driven reshoring, and the gradual shift from fixed hardware to software-defined automation. The Asia-Pacific region leads in both scale and momentum, as subsidy-backed capacity additions in China and India boost baseline demand for compact controllers. Modular architectures remain the cornerstone of large plants; yet, virtualized solutions are gaining market share as users seek flexible deployments on standard industrial PCs. Utilities, automotive electrification, and grid-edge projects anchor near-term purchases, while predictive-maintenance initiatives extend the revenue stream toward services. Supply-chain dual-sourcing and stronger cybersecurity mandates raise switching costs, allowing established brands to protect pricing even as component shortages ease.

Key Report Takeaways

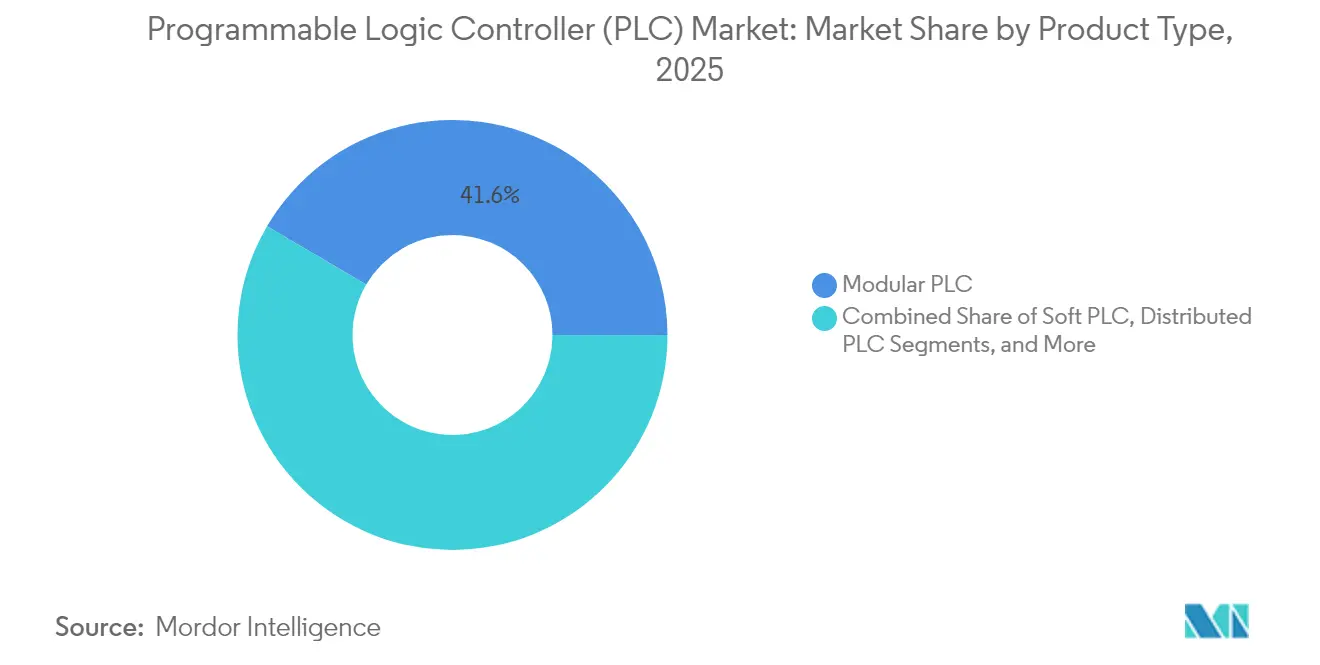

- By product type, modular systems captured 41.56% of the programmable logic controller market share in 2025, whereas soft PLC solutions are expected to grow at a 7.22% CAGR through 2031.

- By component, hardware and software together accounted for 84.67% of the programmable logic controller market size in 2025; however, services are expected to represent the fastest trajectory, growing at an 7.76% CAGR toward 2031.

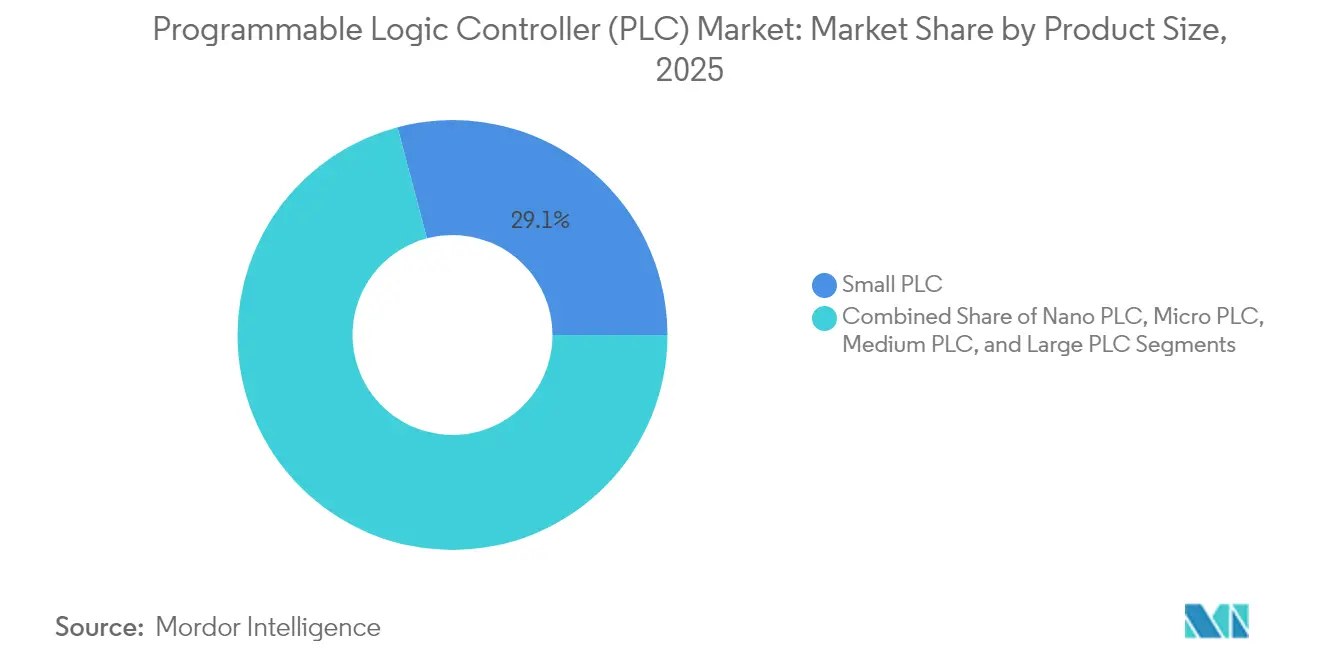

- By product size, nano PLCs are expected to expand at an 8.11% CAGR, outpacing small PLCs, which held a 29.12% share of the programmable logic controller market size in 2025.

- By end-user, energy and utilities led with a 31.25% share in 2025, while automotive manufacturing is forecast to accelerate at a 8.64% CAGR to 2031.

- By geography, the Asia-Pacific region commanded 35.10% of the revenue in 2025 and is projected to maintain a 6.12% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Programmable Logic Controller (PLC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Industry 4.0 adoption in manufacturing | +1.2% | Global with Asia-Pacific and Europe leading | Medium term (2-4 years) |

| Growing demand for compact automation among SMEs | +0.8% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| IIoT and cloud integration enabling predictive maintenance | +1.0% | North America and EU expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift to software-defined PLC workstations | +0.7% | Global with early adoption in developed markets | Medium term (2-4 years) |

| Adoption of open industrial protocols (OPC-UA over TSN) | +0.5% | Europe and North America | Long term (≥ 4 years) |

| Cybersecurity-driven domestic sourcing mandates | +0.3% | North America, EU, select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Industry 4.0 Adoption in Manufacturing

Factories digitalize to boost productivity, and PLCs act as the local data hubs that connect machines with enterprise software. The German Federal Ministry for Economic Affairs reported a jump to 78% Industry 4.0 adoption in 2024, up from 65% in 2023, underscoring the momentum behind controller upgrades. Subsidies in China and India further lower the cost of automation for small producers, while Audi’s virtual PLC rollout cut commissioning time by 23% and improved real-time optimization, validating the transition toward software-centric control. Rising ISO 9001 traceability requirements obligate manufacturers to replace legacy hardware with modern controllers that support granular data logging and seamless ERP integration. Across discrete and process industries, demand concentrates on PLCs with built-in edge analytics that shorten feedback loops without compromising cybersecurity protocols.

IIoT and Cloud Integration Enabling Predictive Maintenance

Edge-ready PLCs analyze vibration, temperature, and power metrics locally, sending only refined insights to cloud dashboards for fleetwide health monitoring. Schneider Electric’s EcoStruxure platform exemplifies the hybrid model, fusing on-premise logic with cloud algorithms for continuous optimization.[1]Schneider Electric, “EcoStruxure Platform Overview,” SE.COM 5G connectivity and digital-twin software now coordinate distributed PLC nodes in real time, supporting autonomous process adjustments that curb unplanned downtime. Utilities and metals plants that deploy predictive maintenance report sharper OEE gains and lower spare-parts inventories, validating the investment case despite residual cybersecurity concerns.

Growing Demand for Compact Automation Among SMEs

The European Commission earmarked EUR 1.3 billion (USD 1.4 billion) for SME digitalization in 2024, slashing payback periods for first-time PLC adopters. Affordable compact controllers integrate I/O, networking, and HMI functions in a single chassis, minimizing engineering labor for firms that lack in-house automation teams. Plug-and-play modules with IEC 61131-3 compliant programming lower learning curves, and industry associations note a 45% annual rise in SME automation in developing markets during 2024. As wage inflation erodes the labor-cost advantage, small factories view compact PLCs as essential to remain competitive and to meet stricter quality benchmarks imposed by global buyers.

Shift to Software-Defined PLC Workstations

Virtual controllers that run on industrial PCs are detaching logic from proprietary hardware, allowing users to scale compute power with off-the-shelf processors. Beckhoff, Siemens, and ABB now offer hypervisor-based solutions that consolidate multiple control tasks on a single server, shrinking cabinet footprints and spares inventories. Fast changeovers in automotive and electronics plants drive demand for drag-and-drop engineering environments that enable code tweaks to deploy in minutes. Simulation first, deploy later workflows cut risk and commissioning costs, though they demand rugged cybersecurity layers to shield virtualized assets from network intrusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capital cost for small manufacturers | -0.9% | Global, particularly in developing markets | Medium term (2-4 years) |

| Escalating cybersecurity threats to connected PLCs | -0.6% | Global with higher impact in critical infrastructure | Short term (≤ 2 years) |

| Substitution risk from industrial PCs and soft-PLCs | -0.4% | Developed markets | Long term (≥ 4 years) |

| Semiconductor supply volatility inflating lead times | -0.7% | Global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Cost for Small Manufacturers

Average project outlays of USD 15,000–50,000 still deter many micro-scale firms, especially when integration, training, and downtime are counted. Limited cash reserves often lead to over-specification because novice buyers adopt a one-size-fits-all mindset to mitigate perceived risk. Financing schemes and vendor leasing ease pressure, but cannot fully offset conservative investment cultures. Subscription-based virtual PLCs promise lower entry points, yet nascent offerings leave adoption uneven, particularly in regions where internet reliability lags.

Escalating Cybersecurity Threats to Connected PLCs

The Cybersecurity and Infrastructure Security Agency logged a 34% surge in industrial-control incidents during 2024, with PLCs at the center of 28% of recorded events.[2]Cybersecurity and Infrastructure Security Agency, “ICS Incident Response Report 2024,” CISA.GOV Attackers exploit increased connectivity to ransom production data or manipulate process parameters in critical plants. Hardening a new PLC installation adds 15–25% to project spend once network segmentation, intrusion detection, and compliance audits are included. Energy and water operators must also demonstrate security-by-design under the EU Cyber Resilience Act, lifting procurement thresholds and elongating qualification cycles for smaller suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Modular Systems Drive Flexibility Demands

Modular configurations dominated with 41.56% programmable logic controller market share in 2025, reflecting their ability to expand I/O and compute power alongside plant upgrades. The architecture lets engineers add motion, safety, or AI cards without forklift replacements, supporting mixed-model lines in automotive and consumer electronics. Soft PLCs, though still niche, are advancing at a 7.22% CAGR as hypervisors deliver deterministic performance and vendors embed hardened kernels.

Across both discrete and process industries, demand centers on controllers that host edge analytics for anomaly detection at the machine level. Compact PLCs retain appeal for stand-alone machines, while distributed PLCs serve large refineries and power stations that favor fault-tolerant, geographically separated nodes. As OPC-UA over TSN matures, users expect seamless interoperability, further commoditizing hardware and shifting differentiation to software toolchains and support ecosystems.

By Component: Services Transformation Accelerates Value Creation

Hardware and software together held 84.67% of the programmable logic controller market size in 2025, yet service revenue is expanding at 7.76% CAGR as users pivot from CapEx to OpEx models. Integration complexity climbs with each layer of IIoT connectivity, elevating demand for vendor-led consulting and application engineering.

Predictive maintenance packages bundle remote monitoring, firmware management, and AI-driven diagnostics, creating sticky multi-year contracts. Vendors also ramp training academies in emerging economies to close the skills gap and lock in brand familiarity. Cloud-hosted support portals lower travel costs, while augmented-reality guides shorten onsite repair cycles, reinforcing service pull even in hardware-centric replacement projects.

By Product Size: Miniaturization Enables IoT Integration

Small PLCs accounted for 29.12% of the programmable logic controller market size in 2025, serving mainstream machining centers and packaging lines. Nano PLCs, however, post an 8.11% CAGR as sensors and actuators proliferate across smart-factory cells that demand footprint-constrained control.

Battery-backed nano modules with Wi-Fi or 5G radios slip into rotating or remote equipment where cabling is impractical. Meanwhile, micro and medium systems fill the gap between I/O density and cost, often chosen for batch processes in the food, beverage, and pharmaceutical industries. Vendors now offer modular nano chassis that scale from eight to 64 I/O points, ensuring growth paths without upfront overspend.

By End-User Industry: Automotive Digitalization Drives Growth Acceleration

Energy and utilities led with a 31.25% share as grid modernization and renewable tie-ins mandate reliable, deterministic logic that withstands harsh substations. Automotive lines, chasing 8.64% CAGR, leverage PLCs for battery-cell assembly, torque-controlled fastening, and end-of-line test rigs.

Chemical and petrochemical players rely on SIL-rated controllers for safety interlocks, while food processors integrate recipe management and allergen tracking. Water and wastewater sites adopt rugged PLCs with conformal coating to survive high humidity and corrosive atmospheres, and pharmaceuticals rely on 21 CFR Part 11 audit trails woven into controller firmware. Across sectors, IT-OT convergence accelerates as enterprise MES and ERP suites query live PLC data for real-time KPI dashboards.

Geography Analysis

Asia-Pacific’s manufacturing resurgence underpins both scale and speed, with 35.10% revenue in 2025 and 6.12% CAGR to 2031. China’s post-pandemic stimulus subsidized controller upgrades in automotive and electronics, while India’s industrial corridor builds encourage first-time PLC rollouts. Japan’s Quality-4.0 initiatives keep demand high for deterministic, nano-second-level controllers used in electronics placement machines. South Korean shipyards and fabs specify redundant PLC clusters for mission-critical uptime, anchoring high-margin orders.

Europe’s sustainability push frames controller purchases around energy management and circular-economy compliance. The EU Cyber Resilience Act of 2024 obliges OEMs to certify security-by-design, boosting demand for products with encrypted communications and built-in anomaly detection. German automakers pilot software-defined PLC sandboxes, while France and Italy automate aerospace composites lines with fail-safe logic.

North American users prioritize secure supply chains and domestic semiconductor content. The Infrastructure Investment and Jobs Act funds substation refurbishments that incorporate modern controllers for load-balancing and fault isolation. Mexico’s nearshore boom ramps automotive harness production, requiring swift deployment of compact PLCs. Canada’s mining and lumber sectors favor rugged gear with extended temperature ratings. Overall, regional buyers weigh cybersecurity credentials and on-shore repair support heavily in tender scoring.

Regulatory Landscape

Cybersecurity and product-assurance rules are tightening for connected industrial automation, increasing qualification requirements for PLC hardware, firmware, and engineering toolchains. In the European Union, the Cyber Resilience Act (Regulation (EU) 2024/2847) formalized horizontal cybersecurity obligations for products with digital elements, with key compliance infrastructure milestones in 2026 (for example, Chapter IV provisions on notifying conformity assessment bodies applying from 11 June 2026, and Article 14 reporting obligations applying from 11 September 2026). Separately, enforcement aligned to the EN IEC 62443-4-2:2026 cybersecurity requirements for industrial control devices was cited as commencing on 18 April 2026, pushing vendors and OEMs to document secure development lifecycle controls, vulnerability handling, and device security capabilities as part of purchasing and acceptance.

Standards updates also affect functional compliance and portability of PLC applications. IEC 61131-3:2025 (Edition 4) was published in May 2025, advancing programming requirements (including removal of Instruction List and additions such as UTF-8 string support), and local adoptions continued in 2026 (for example, MEST EN IEC 61131-3:2026 published on 1 June 2026 as an identical adoption of the international standard). In China, GB/T 47234-2026 was issued on 27 February 2026 for intelligent control systems, with an implementation date of 1 September 2026, adding national requirements that suppliers address through product documentation, testing, and localized conformity planning.

Value Chain Analysis

The PLC value chain starts with industrial-grade electronic inputs (MCUs, FPGAs, memory, power management ICs, connectors, and ruggedized passives) and embedded software components (real-time operating environments, IEC 61131-3 runtimes, communication stacks such as PROFINET/EtherNet/IP, and security libraries). These inputs feed into OEM design, assembly, and validation, followed by distribution through direct sales and channel partners, and then system integration where panels, networks, sensors/actuators, HMI/SCADA, and safety systems are engineered into end-user lines. Major PLC suppliers active across the chain include Siemens, Rockwell Automation, Schneider Electric, Mitsubishi Electric, ABB, Omron, Beckhoff, Delta Electronics, Emerson, and Honeywell, with value shifting from CPUs and I/O toward engineering software, connectivity, and lifecycle services.

Downstream, automation distributors, panel builders, and controls integrators bridge vendor platforms and plant-specific requirements, often bundling PLCs with drives, robots, vision, and data platforms. Supply constraints and transition management remain practical chokepoints: post-2024 recovery has been uneven, and end-of-life transitions for legacy platforms can create pockets of scarcity. High-specification fail-safe controllers can also stay constrained due to concentrated demand in critical infrastructure programs. Trade policies and tariff volatility add friction to procurement and encourage dual-sourcing and regionalized assembly, while interoperable architectures (including virtualized and software-defined control) increase the importance of certified toolchains, cybersecurity patching, and long-term support contracts in delivered value.

Competitive Landscape

The top five suppliers command roughly 60% of global revenue, signaling a moderately concentrated field.[5]IEEE Industrial Electronics Society, “Industrial Control Systems Security Report 2024,” IEEE-IES.ORG Siemens, Schneider Electric, and ABB defend their shares through complete portfolios, global service reach, and patent depth. They bundle controllers with SCADA, drives, and lifecycle services, locking customers into integrated ecosystems. Patent activity rose 23% in 2024, focused on AI inference at the edge and wireless TSN communication.

Mid-tier challengers promote open-source firmware and subscription pricing, targeting customers wary of vendor lock-in. Virtual PLC pioneers leverage hypervisor isolation to promise deterministic performance on standard PCs, reducing hardware spend and cabinet space. Hardware margins compress as software adds the primary value, prompting incumbents to launch cloud-native engineering suites and open developer marketplaces.

Persistent semiconductor supply shocks push buyers toward dual sourcing, benefitting regional assemblers with short lead times. Cybersecurity hardening further distinguishes premium offerings, with ISO 27001-certified remote-management portals emerging as key differentiators. In end markets like EV batteries and green hydrogen, tailored libraries and safety-certified function blocks provide entry barriers that slow commoditization.

Programmable Logic Controller (PLC) Industry Leaders

ABB Ltd

Mitsubishi Electric Corporation

Schneider Electric SE

Rockwell Automation Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Software-defined automation is creating whitespace around virtualized PLC runtimes, cloud-connected engineering, and hybrid deployments that reduce cabinet footprint while preserving deterministic control. Enterprise users are operationalizing these patterns through named platforms already common in PLC estates, including Schneider Electric EcoStruxure, and through vendor toolchains from Siemens, ABB, and Beckhoff. At the same time, cybersecurity pressure is pushing procurement toward controllers with stronger secure-by-design features and faster patch cadences. The 2024 surge in industrial-control incidents recorded by CISA (34% increase, with PLCs implicated in a significant share of events) reinforces demand for hardened PLC platforms, secure remote access, and managed services that combine firmware governance with continuous monitoring.

Electrification and capacity buildouts in high-throughput manufacturing also support controller upgrade cycles, because new facilities and expansions embed higher levels of automation, traceability, and energy management from day one. In 2026, large semiconductor and electronics manufacturing investment announcements and capacity moves (for example, Intel expanding its Leixlip, Ireland campus and Infineon opening the Smart Power Fab in Dresden) point to continued capital spending in industries that deploy dense automation, motion, and process controls. This environment favors PLC suppliers and integrators that can deliver standardized architectures across sites, provide validated libraries for regulated industries (such as 21 CFR Part 11-aligned audit trails in pharmaceuticals), and offer service-led modernization paths that convert large installed bases to secure, interoperable, software-centric control stacks.

Recent Industry Developments

- July 2026: ABB expanded its partnership with Nvidia to integrate digital models of electrical power products into the Omniverse DSX platform for data center design. The move tightens ABBs digital-twin workflows that depend on reliable control and power infrastructure, linking automation and electrification engineering data more closely to simulation-led commissioning.

- June 2026: Schneider Electric launched Industrial Automation Modernization as a Service, combining EcoStruxure Automation Expert with HPE SimpliVity hybrid cloud infrastructure. Packaging modernization as a service supports software-defined automation programs where PLC logic and orchestration are deployed with standardized compute, accelerating multi-site upgrades and adding recurring services content.

- May 2026: ABB released firmware v2.4.1-R3 for AC500 V2 series PLCs to mitigate critical vulnerabilities flagged for industrial control environments. The update highlights the growing role of vulnerability response and secure lifecycle management as purchase criteria for connected PLC deployments in critical infrastructure and manufacturing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the programmable logic controller (PLC) market is defined as revenues generated from PLC hardware, embedded and related software, and associated services used to automate industrial and infrastructure processes across end users.

Scope exclusions: We exclude broader automation layers such as SCADA, DCS, industrial PCs, sensors, actuators, and networking gear unless they are bundled and priced as part of a PLC offering.

Segmentation Overview

- By Product Type

- Compact PLC

- Modular PLC

- Distributed PLC

- Soft PLC

- Other Products

- By Component

- Hardware and Software

- Services

- Installation and Integration

- Training and Support

- Maintenance

- By Product Size

- Nano PLC

- Micro PLC

- Small PLC

- Medium PLC

- Large PLC

- By End-user Industry

- Automotive

- Food and Beverage

- Chemical and Petrochemical

- Oil and Gas

- Energy and Utilities

- Water and Wastewater Treatment

- Pharmaceutical

- Pulp and Paper

- Metals and Mining

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the PLC value chain and to build the starting ranges for demand and pricing. We referenced public, non-paywalled sources such as US Census Bureau manufacturing data, Eurostat production indicators, UN Comtrade trade flows for electrical control equipment proxies, International Federation of Robotics updates, and standards or technical notes from bodies such as IEC. These inputs helped us anchor where automation spending is rising, and where industrial output cycles might create short-term swings.

We also reviewed company filings, annual reports, investor presentations, product catalogs, distributor listings, and reputable press coverage to understand product positioning and typical replacement cycles. In a few places, paid subscriptions for company financials and news were used to cross-check revenue splits and corporate actions that can impact reported PLC sales. The desk sources listed here are illustrative only, and many other public and paid sources were also reviewed for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually counted as PLC spend in customer budgets and channel invoices, and on pressure-testing price and mix assumptions for compact, modular, and software-based PLC deployments. We spoke with a spread of participants across manufacturing and process industries, including OEM and system integration voices, distributors, and plant-level automation teams, and then we balanced viewpoints across APAC, EMEA, and the Americas so regional adoption patterns were not overgeneralized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 19% | APAC: 48% |

| Mid tier: 55% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 20% | Managers: 41% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where top-down demand pools were first reconstructed from industrial production trends, automation investment signals, and installed base replacement behavior, and then checked with selective supplier and channel roll-ups. In practice, we start by estimating PLC attach and refresh rates across key automation-heavy industries, which is then converted into value using typical price bands and mix by PLC class.

A few market fingerprints were used as core inputs, including manufacturing output indexes by region, new plant and expansion activity in discrete and process industries, automation retrofit intensity, typical I/O density by application (which influences compact versus modular mix), and service attach rates for integration, support, and maintenance. Pricing assumptions were kept realistic by separating entry-level compact units from higher-value modular deployments and by reflecting year-to-year price movements through interview feedback and public product positioning.

For forecasting, scenario analysis was applied around industrial cycle strength, capex pacing, and substitution between PLC and adjacent control architectures, and then a simple regression check was used to make sure the forecast direction matched macro and factory-automation signals. Where bottom-up data had gaps, we used conservative proxies, such as sampling representative product lines and scaling by region and end-user exposure, before the totals were reconciled back to the demand pool view.

Data Validation & Update Cycle

Validation is handled through multiple checks so the final number is not driven by one dataset or one assumption. We compare outputs against independent signals such as industrial automation spending commentary, trade and production movements, and the implied PLC replacement burden from installed base estimates, and any large variance triggers a deeper review.

Before sign-off, the model is re-checked for outliers in regional splits, price progression, and service shares, and then a separate analyst review is completed to confirm that definitions and boundaries stayed consistent across years. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp industrial slowdowns, major regulatory shifts, or supply disruptions. Right before delivery, the latest public updates are re-screened so clients receive the most current view.

Mordor Intelligence's Programmable Logic Controller Plc Market Size Compared With Other Published Estimates

Published market sizes for PLCs can vary even when they use the same label, because the underlying scope and counting rules are not always aligned. The biggest differences usually come from what is treated as PLC revenue versus adjacent automation equipment, how services are handled, and whether the model is built from demand indicators or from supplier disclosures.

By tracking end-user automation spend signals and refreshing product mix and service attach assumptions, Mordor Intelligence keeps the PLC total tied to hardware, related software, and services that are sold as part of PLC deployments, rather than folding in broader control systems by default. Some estimates also apply faster ASP escalation or more aggressive retrofit assumptions during the forecast build, which can lift the starting year if the same logic is back-applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.33 B (2026) | |

| Trade Journal A | USD 13.98 B (2025) | Uses a broader PLC definition that can treat selected automation components as PLC-related spend, and it reports a 2025 base year that may reflect different currency timing and price assumptions. |

| Regional Consultancy B | USD 11.70 B (2025) | Leans on a narrower unit and component scope and emphasizes conservative replacement pacing, which tends to reduce the value captured from higher-spec modular systems and services. |

The spread in the table mainly comes down to boundary choices and how pricing and service revenue are applied in the base year. When scope is kept consistent and assumptions are cross-checked against adoption and replacement signals, the resulting market size becomes easier to audit and repeat year after year.

Key Questions Answered in the Report

What is the current valuation of the programmable logic controller market?

The programmable logic controller market size is USD 13.33 billion in 2026.

How fast is the sector expected to grow?

The market is projected to expand at a 4.24% CAGR through 2031.

Which region leads both revenue and growth?

Asia-Pacific holds 35.10% share and is forecast for a 6.12% CAGR.

Which product category is growing the quickest?

Soft PLC solutions are poised for a 7.22% CAGR between 2026 and 2031.

Why are services gaining momentum?

Manufacturers favor predictable OpEx models, pushing service revenue to an 7.76% CAGR.

What is the main cybersecurity challenge?

Rising industrial-control attacks add 15-25% to project costs due to mandatory hardening and compliance audits.

Page last updated on: