US Electric Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 24.35 Billion |

| Market Size (2026) | USD 25.67 Billion |

| Market Size (2031) | USD 33.39 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

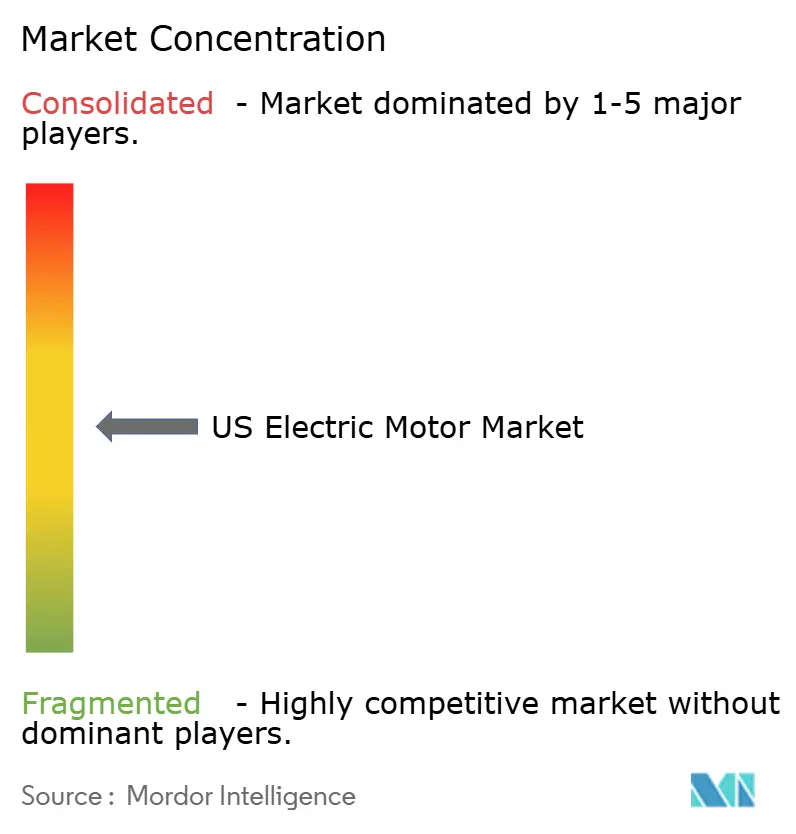

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Electric Motor Market Analysis by Mordor Intelligence

The US electric motor market size was valued at USD 24.35 billion in 2025 and estimated to grow from USD 25.67 billion in 2026 to reach USD 33.39 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). Growth rested on federal clean-energy incentives that improved project economics, a wave of manufacturing reshoring that reduced logistics risk, and steady electrification across automotive, industrial, and defense sectors. Automakers increased demand for high-power-density traction motors, while building owners accelerated HVAC retrofits to comply with efficiency mandates. Industrial plants modernized drive systems to meet Industry 4.0 connectivity standards, and Department of Defense programs added niche volumes for tactical electric platforms. Copper, semiconductor, and labor constraints remained the main cost headwinds.

Key Report Takeaways

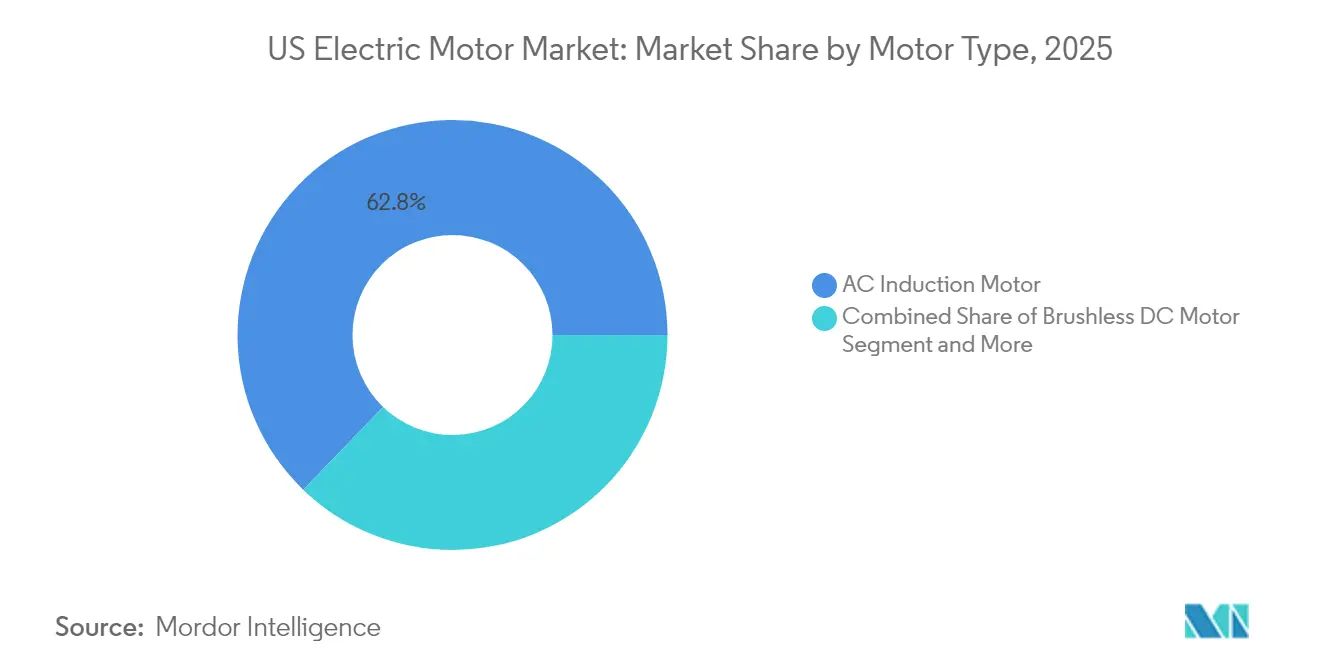

- By motor type, AC induction motors led with 62.78% of the US electric motor market share in 2025, whereas permanent-magnet synchronous motors are forecast to grow at an 10.96% CAGR through 2031.

- By power output, fractional horsepower units (<1 HP) accounted for 53.85% share of the US electric motor market size in 2025, while medium-voltage motors (250-3,000 HP) are expanding at a 9.98% CAGR to 2031.

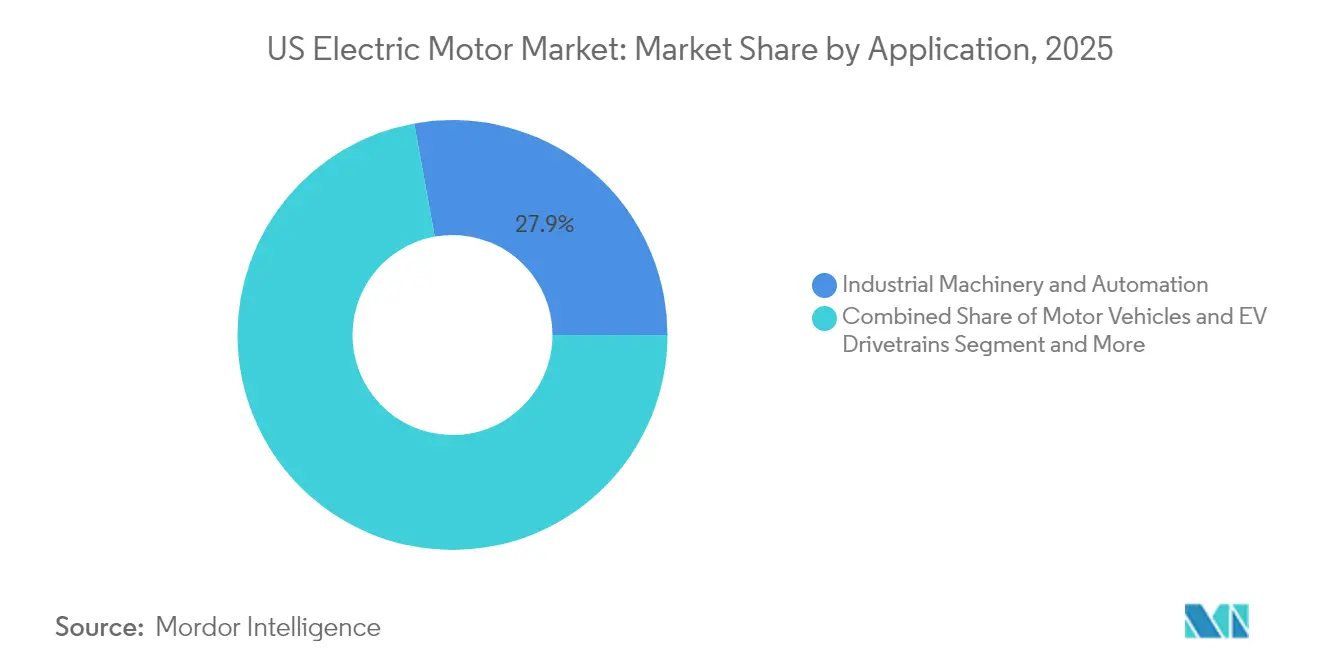

- By application, industrial machinery and automation held 27.85% revenue share in 2025; EV drivetrains represent the fastest-growing application with a 16.92% CAGR to 2031.

- By technology, conventional induction designs maintained a 71.92% share in 2025, and axial-flux innovations are advancing at a 14.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Electric Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV manufacturing surge | +1.8% | National; hubs in Michigan, Ohio, Tennessee | Medium term (2-4 years) |

| Industrial automation and IIoT retrofits | +1.2% | National; early gains in Texas, California, North Carolina | Long term (≥ 4 years) |

| HVAC efficiency upgrades in commercial real estate | +0.9% | National; accelerated in California, New York, and Massachusetts | Short term (≤ 2 years) |

| Federal clean-energy tax incentives (IRA) | +0.7% | National | Medium term (2-4 years) |

| Axial-flux and SynRM tech enabling reshoring | +0.4% | National; hubs in Alabama, Wisconsin, Ohio | Long term (≥ 4 years) |

| DoD vehicle electrification programs | +0.3% | National, near major military installations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV manufacturing surge

Passenger BEVs captured one quarter of new-vehicle sales in 2025, and domestic automakers responded by scaling motor production footprints in Michigan, Ohio, and Tennessee. Automakers specified traction motors that deliver three times the power density of legacy units, prompting a pivot toward permanent-magnet synchronous and axial-flux topologies. General Motors filed axial-flux patents targeting sub-compact EVs, while Schaeffler invested USD 230 million in Ohio to build e-axles that integrate motors and power electronics. Localized component sourcing reduced exposure to foreign rare-earth supply risk and shortened logistics lead times. As platform volumes rose, cost parity with imported units improved, strengthening the US electric motor market.

Industrial automation and IIoT retrofits

Modernization programs replaced legacy drives with intelligent systems that embed sensors and edge computing. Rockwell Automation documented predictive maintenance rollouts that cut unplanned downtime 55% and trimmed energy use 18%[1]Rockwell Automation Staff, “8 Key Industrial Automation Trends in 2025,” rockwellautomation.com. The retrofit cycle gained urgency because motor-driven equipment consumed about 53% of industrial electricity, making efficiency an immediate cost lever. Variable-frequency drives became default specifications, and demand for premium-efficiency IE5 motors increased despite higher upfront prices. Industrial hubs in Texas and North Carolina emerged as early adopters, reflecting dense manufacturing footprints and supportive state incentives.

HVAC efficiency upgrades in commercial real estate

Building owners raced to comply with state and city climate rules that mandate lower greenhouse-gas intensity. California utilities offered rebates that shortened retrofit paybacks to less than three years. Case studies such as Wells Fargo’s retrofit of switched-reluctance motors demonstrated 70% HVAC energy savings. IE5 motors paired with integrated drives reported 10% energy reduction versus IE3 equivalents. The American Innovation and Manufacturing Act accelerated refrigerant transitions, and variable refrigerant flow systems lifted demand for electronically commutated motors able to modulate speed precisely.

Federal clean-energy tax incentives

The Inflation Reduction Act offered credits up to USD 40,000 for qualified commercial clean vehicles and extended manufacturing credits to facilities producing high-efficiency electrical equipment. ArcelorMittal secured USD 280.5 million in credits to fund a USD 1.2 billion electrical steel plant in Alabama, tightening domestic supply loops for motor laminations. Credit certainty improved board-level confidence for capital expenditure, and incremental demand rippled into motor OEM order books. State programs layered additional rebates, further enhancing project economics for fleet operators and industrial retrofits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and rare-earth price volatility | -0.8% | Global; acute cost impact on US manufacturers | Short term (≤ 2 years) |

| Semiconductor shortages for drive electronics | -0.6% | National; high-tech regions | Medium term (2-4 years) |

| Compliance cost of ultra-premium tiers | -0.3% | National | Long term (≥ 4 years) |

| Skilled motor-winding labor gap | -0.4% | National; traditional manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper and rare-earth price volatility

Copper averaged USD 8,800-9,500 per ton in 2025 and faced a projected 70% increase by 2050 as electrification raised structural demand. Rare-earth export policies tightened permanent-magnet supply, exposing motor OEMs to price spikes and delivery risk. Firms responded by hedging, redesigning rotors to use ferrite materials, and expanding recovery of metals from end-of-life products. ZF’s 220 kW separately-excited design illustrated a path to eliminate magnets while preserving performance. Smaller domestic manufacturers without scale or long-term contracts bore the highest cost pressure, which diluted margins and slowed capacity expansions.

Semiconductor shortages for drive electronics

Lead times for motor control chips lengthened from 12 to 26 weeks in 2024 as automotive and consumer electronics absorbed fab capacity. Variable-frequency drive lines were hit hardest because they rely on power management ICs fabricated at mature nodes still in short supply. GlobalFoundries and other foundries ramped US hiring but flagged skilled workforce shortages despite CHIPS Act incentives. OEMs revised PCB layouts to accept multiple controller options, yet performance compromises persisted. Extended inventory holding raised working-capital needs and forced some distributors to allocate units to strategic customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: AC induction leadership persists while PMSM gains scale.

AC induction units retained 62.78% share in 2025, giving the segment the largest slice of the US electric motor market. The design’s rugged construction and mature supply base kept pricing competitive, so adopters in pulp and paper or water utilities continued to favor it for constant-speed pumps and compressors. However, permanent-magnet synchronous motors expanded at an 10.96% CAGR through 2031 because EV traction and high-precision automation prioritized power density and efficiency. PMSMs remove rotor I²R losses, permitting compact housings that meet stringent vehicle packaging envelopes. Brushless DC solutions addressed servo applications that demand fine speed control, whereas hermetic motors stayed relevant in sealed refrigeration circuits. Research into synchronous reluctance designs, including ribless rotor prototypes that raised torque by 22.1%, signalled future competitive pressure for magnet-based machines.

The US electric motor market size for PMSMs is estimated to rise from USD 6.5 billion in 2025 to roughly USD 12.12 billion by 2031, underpinning broader drivetrain electrification. Automakers’ shift to axial-flux variants combated rare-earth risk and shaved curb weight. Conversely, induction products continued to dominate harsh environments because they tolerate voltage spikes and harmonics that damage magnet rotors. OEM roadmaps suggested a gradual portfolio mix shift rather than a rapid displacement. Motor-rewind service revenues supported the legacy installed base, ensuring aftermarket cash flows for large industrial suppliers.

By Power Output: Medium-voltage motors accelerate amid plant upgrades

Fractional horsepower products represented 53.85% of shipments in 2025 and spanned domestic appliances, small pumps, and office equipment, cementing a broad but price-sensitive foundation for the US electric motor market. Rising minimum-efficiency standards nudged appliance makers toward electronically commutated variants that delivered 65-75% electrical efficiency compared with 30% for shaded-pole units. Nonetheless, the headline growth story emerged in the 250-3,000 HP band, where medium-voltage motors are forecast to compound at 9.98% through 2031. Mining, metals, and large water infrastructure owners replaced multiple smaller drives with one high-capacity synchronous reluctance machine, cutting lifecycle maintenance costs.

The US electric motor market size for medium-voltage systems was valued near USD 5.9 billion in 2025 and is projected to top USD 10.44 billion by 2031. Policy support under the Infrastructure Investment and Jobs Act financed water-treatment and grid projects that specify premium-efficiency MV drives. Users highlighted reduced cable losses and improved power-factor correction. Integral horsepower motors ≥ 1 HP remained workhorses in conveyors and fan arrays, especially when bundled with smart drives featuring condition-monitoring analytics. Service organizations gained revenue by upgrading legacy MV starters to solid-state soft-starters that limit inrush current during ramp-up, extending switchgear life.

By Application: Industrial machinery anchors demand, EV drivetrains outpace

Industrial machinery and automation held 27.85% revenue share in 2025, representing the single largest end-use pool within the US electric motor market. Investment cycles at chemical plants, food processors, and semiconductor fabs kept replacement volumes steady. Predictive maintenance platforms such as Regal Rexnord’s Perceptiv captured vibration and thermal signatures, cutting downtime events by more than half. In contrast, EV drivetrains logged a 16.92% CAGR due to federal fleet electrification incentives and consumer adoption momentum. Each battery-electric light vehicle required two to three traction motors plus auxiliary pumps, swelling total unit demand.

HVAC and refrigeration formed a highly regulated niche that leveraged IE5 motors to satisfy emerging refrigerant and building code mandates. Aerospace and defense embraced high power-density solutions such as H3X’s 8-12 kW/kg machines for electric aircraft prototype programs h3x.tech. Household appliances matured but added incremental volume from smart-home integrations that relied on brushless DC drives for silent operation. The US electric motor market share attributed to EV drivetrains is predicted to climb toward 14.75% by 2031, narrowing the gap with industrial machinery as automakers completely new assembly capacity.

By Technology: Conventional induction steadies, axial-flux innovation scales

Conventional induction architecture still captured 71.92% share in 2025 because of entrenched manufacturing capacity and cost leadership. OEMs offered premium-grade induction frames certified to NEMA Premium efficiency levels, extending relevance in regulated markets. However, axial-flux designs grew at a 14.32% CAGR and promised triple power density, making them attractive for high-end passenger cars and compact HVAC blowers. Mercedes-Benz confirmed AMG models would employ axial-flux rotors that trimmed weight and improved transient response.

The US electric motor market size attributed to axial-flux solutions was under USD 800 million in 2025 but could surpass USD 2.08 billion by 2031. Infinitum’s PCB-stator topology cut core losses and simplified manufacturing. Synchronous reluctance adoption widened in motion-control lines that need precise torque without magnet costs, and switched reluctance gained prominence in harsh-environment pumps because it tolerated elevated temperatures without demagnetization. Patent filings for Halbach-array variants hinted at future breakthroughs for space or desert duty, where magnetic field shaping boosts thrust without added mass.

Geography Analysis

Demand mapped closely to regional industrial strengths. The Great Lakes corridor anchored by Michigan and Ohio attracted more than USD 4 billion in announced EV motor and component investments between 2024 and 2025. The region benefited from skilled labor and union-negotiated training programs that addressed winding and assembly bottlenecks. Tennessee and Alabama added electrical steel and e-axle plants, reinforcing a vertically integrated supply chain that tightened regional content for automakers.

Western states led adoption in building electrification. California’s Title 24 energy code pushed premium-efficiency motor sales for HVAC and water pumping, while data-center growth in Arizona and Nevada pushed high-reliability fan demand. Texas became a production hotspot after Linear Labs announced a 500,000-square-foot facility in Fort Worth backed by USD 68.9 million in incentives. Renewable project developers in the Southwest ordered yaw and pitch motors for onshore wind farms and tracking drives for large solar arrays.

The Northeast saw a retrofit wave triggered by New York City Local Law 97, which penalized inefficient buildings beginning 2027. Co-op boards installed heat-pump systems powered by permanent-magnet motors to avoid fines. Defense spending concentrated in Virginia, Maryland, and California drove procurement of rugged motor-generator sets for naval vessels and tactical hybrid vehicles. Across all regions, Infrastructure Investment and Jobs Act funds were earmarked for water and transit projects that specify NEMA Premium motors, thereby standardizing high-efficiency demand nationwide.

Competitive Landscape

Competition remained moderate, with top five suppliers accounting for roughly 45-50% of revenue. Global multinationals such as ABB, Siemens, and Nidec leveraged broad portfolios spanning motors, drives, and digital platforms to cross-sell integrated solutions. ABB committed USD 120 million to expand low-voltage capacity in Tennessee and Mississippi, creating 250 jobs and shortening lead times for North American customers. Siemens divested its Innomotics unit to KPS Capital for USD 3.9 billion, creating an independent player focused solely on large drives and motor systems.

Emerging technology firms exploited the white-space created by rare-earth risk and efficiency mandates. Infinitum commercialized an axial-flux HVAC motor with a printed-circuit-board stator, while Linear Labs targeted EV two-wheelers. Turntide Technologies inked partnerships with FridgeWize to retrofit supermarket refrigeration cases using switched-reluctance drives that eliminate magnets. Patent activity rose around Halbach-array configurations, and Boeing’s filings indicated cross-industry interest in high-field architectures for extreme environments.

Service capability and supply-chain resilience differentiated vendors. Hitachi’s purchase of Joliet Electric Motors bolstered repair capacity for large motors in energy markets, embedding recurring revenue alongside equipment sales. Companies with co-located winding, laminations, and drive electronics escaped port congestion delays that lingered into 2025. Conversely, smaller regionals reliant on imported stator stacks struggled to ensure delivery, prompting some OEMs to consolidate procurement with larger partners.

US Electric Motor Industry Leaders

-

ABB Ltd.

-

Ametek Inc.

-

Johnson Electric Holdings Limited

-

Schneider Electric

-

Oriental Motor USA Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unusual Machines agreed to acquire Rotor Lab for USD 7 million in stock to gain small-form-factor propulsion motors for unmanned aerial systems.

- March 2025: ArcelorMittal started construction of a USD 1.2 billion electrical steel plant in Alabama, slated for 150,000 t annual output.

- March 2025: ABB announced a USD 120 million capacity expansion across Tennessee and Mississippi for low-voltage products.

- February 2025: GE Vernova outlined a USD 600 million US manufacturing program through 2027 covering gas turbines and electrification R&D.

US Electric Motor Market Report Scope

Electric motors, devices that transform electrical energy into mechanical energy, find applications in diverse industries and household appliances. Notably, they boast greater energy efficiency than internal combustion engines (ICEs). The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrive at using top-down and bottom-up approaches.

The US Electric Motor market is segmented by motor type (AC Motor, DC Motor and Hermetic Motor), by power output (Integral HP Output and Fractional HP Output), and by application (Industrial Machinery, Motor Vehicles, HVAC Equipment, Aerospace & Transportation, Household Appliances and Other Applications). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| AC Induction Motor |

| Brushless DC Motor |

| Permanent-Magnet Synchronous Motor |

| Hermetic Motor |

| Stepper and Other Specialty Motors |

| Fractional Horsepower (<1 HP) |

| Integral Horsepower (?1 HP) |

| Medium Voltage (250�3000 HP) |

| Industrial Machinery and Automation |

| Motor Vehicles and EV Drivetrains |

| HVAC and Refrigeration |

| Aerospace, Defense and Transportation |

| Household and Consumer Appliances |

| Conventional Induction |

| Axial-Flux |

| Synchronous Reluctance |

| Switched Reluctance |

| By Motor Type | AC Induction Motor |

| Brushless DC Motor | |

| Permanent-Magnet Synchronous Motor | |

| Hermetic Motor | |

| Stepper and Other Specialty Motors | |

| By Power Output | Fractional Horsepower (<1 HP) |

| Integral Horsepower (?1 HP) | |

| Medium Voltage (250�3000 HP) | |

| By Application | Industrial Machinery and Automation |

| Motor Vehicles and EV Drivetrains | |

| HVAC and Refrigeration | |

| Aerospace, Defense and Transportation | |

| Household and Consumer Appliances | |

| By Technology | Conventional Induction |

| Axial-Flux | |

| Synchronous Reluctance | |

| Switched Reluctance |

Key Questions Answered in the Report

What is the current value of the US electric motor market?

The market was valued at USD 25.67 billion in 2026 and is forecast to reach USD 33.39 billion by 2031.

Which motor type holds the largest share today?

AC induction motors led with 62.78% of the US electric motor market share in 2025.

Why are axial-flux motors drawing attention?

They deliver up to three times the power density of radial designs, making them ideal for compact EV and HVAC applications.

How are federal incentives influencing demand?

Inflation Reduction Act credits reduce upfront costs for fleet electrification and fund domestic manufacturing capacity, adding roughly 0.7 percentage point to the forecast CAGR.

What is the biggest supply-chain challenge facing motor OEMs?

Volatile copper and rare-earth prices are squeezing margins and pushing companies toward magnet-free designs.

Which application segment is growing fastest through 2031?

EV drivetrains are projected to expand at a 16.92% CAGR, outpacing all other end-use categories.

Page last updated on: