Facial Serum Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

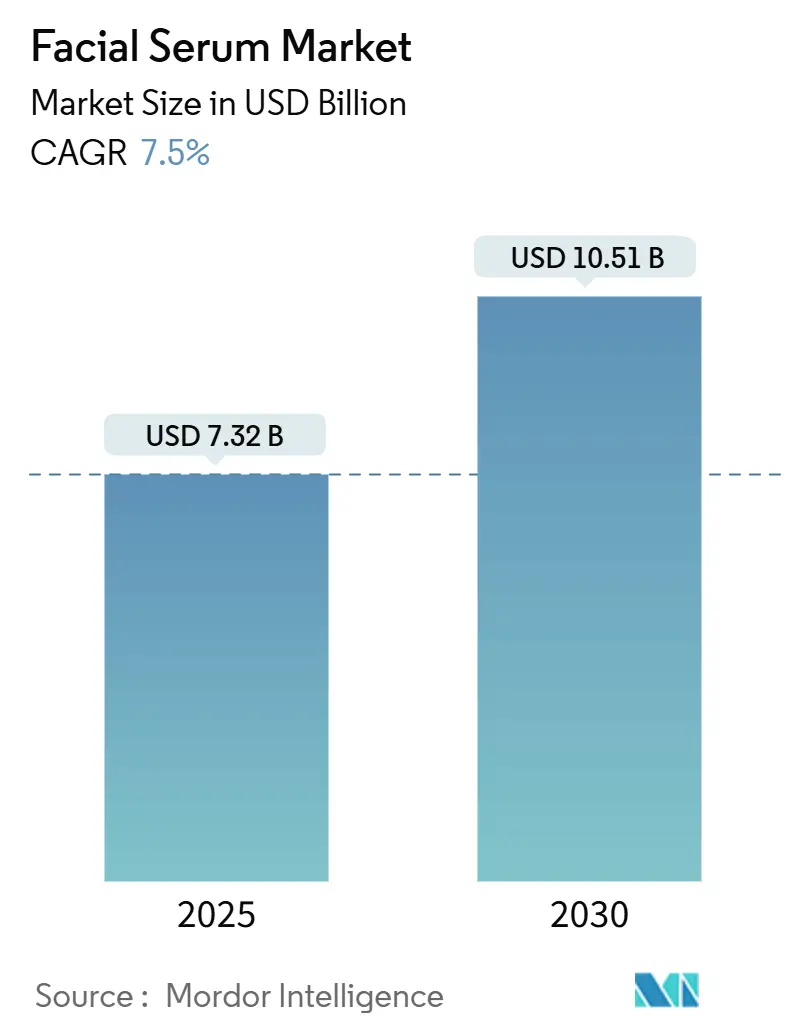

| Market Size (2025) | USD 7.32 Billion |

| Market Size (2030) | USD 10.51 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Facial Serum Market Analysis by Mordor Intelligence

The Facial Serum Market size is estimated at USD 7.32 billion in 2025, and is expected to reach USD 10.51 billion by 2030, at a CAGR of 7.5% during the forecast period (2025-2030).

The market expansion reflects demographic changes, technological advancements, and consumer preferences that have established facial serums as a premium skincare category. The market's strength lies in addressing multiple skin concerns, from anti-aging to specific skin conditions, while capitalizing on the global trend toward premium beauty products. Recent regulatory changes, including the U.S. Food and Drug Administration's Modernization of Cosmetics Regulation Act (MoCRA), which mandates cosmetic facility registration and product listing since July 2024, are influencing market dynamics.[1]Source: U.S. Food and Drug Administration, “Cosmetics Facility Registration and Product Listing Under MoCRA,” fda.gov.

Key Report Takeaways

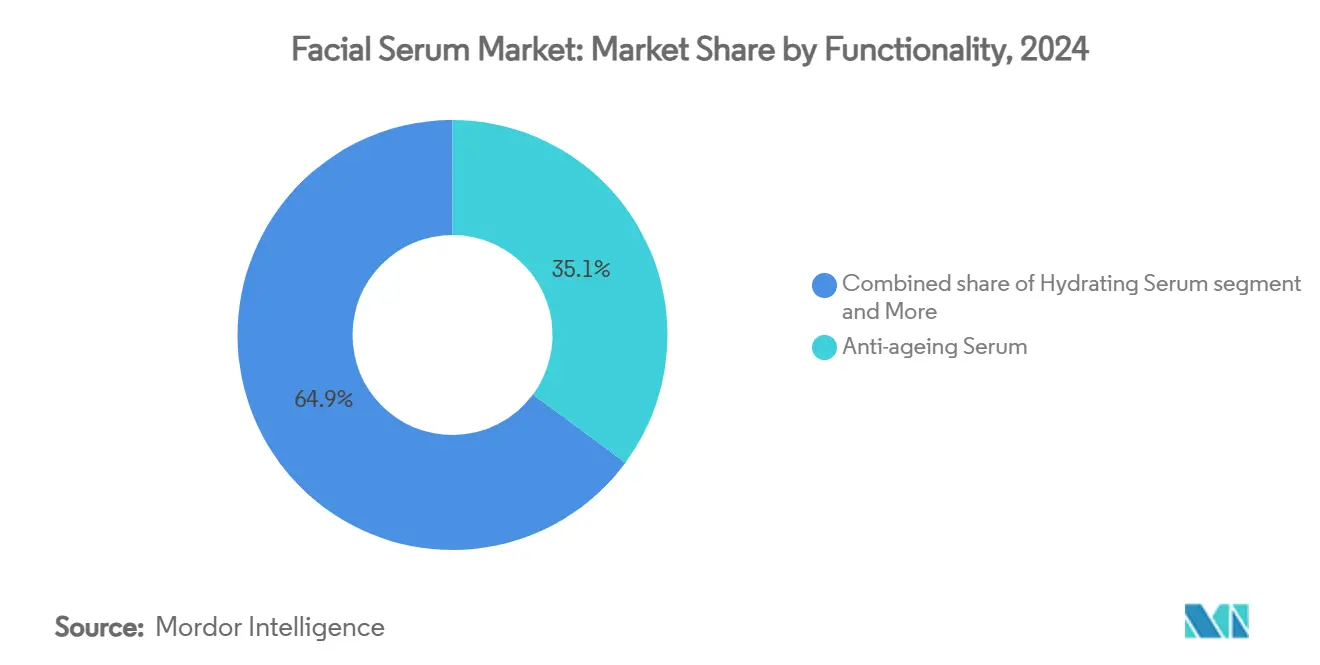

- By functionality, anti-aging serums led with a 35.12% facial serum market share in 2024, while acne-fighting serums are projected to grow at an 8.22% CAGR between 2025-2030.

- By form, water-based products commanded 60.26% of the facial serum market in 2024; oil-based variants are advancing at an 8.76% CAGR through 2030.

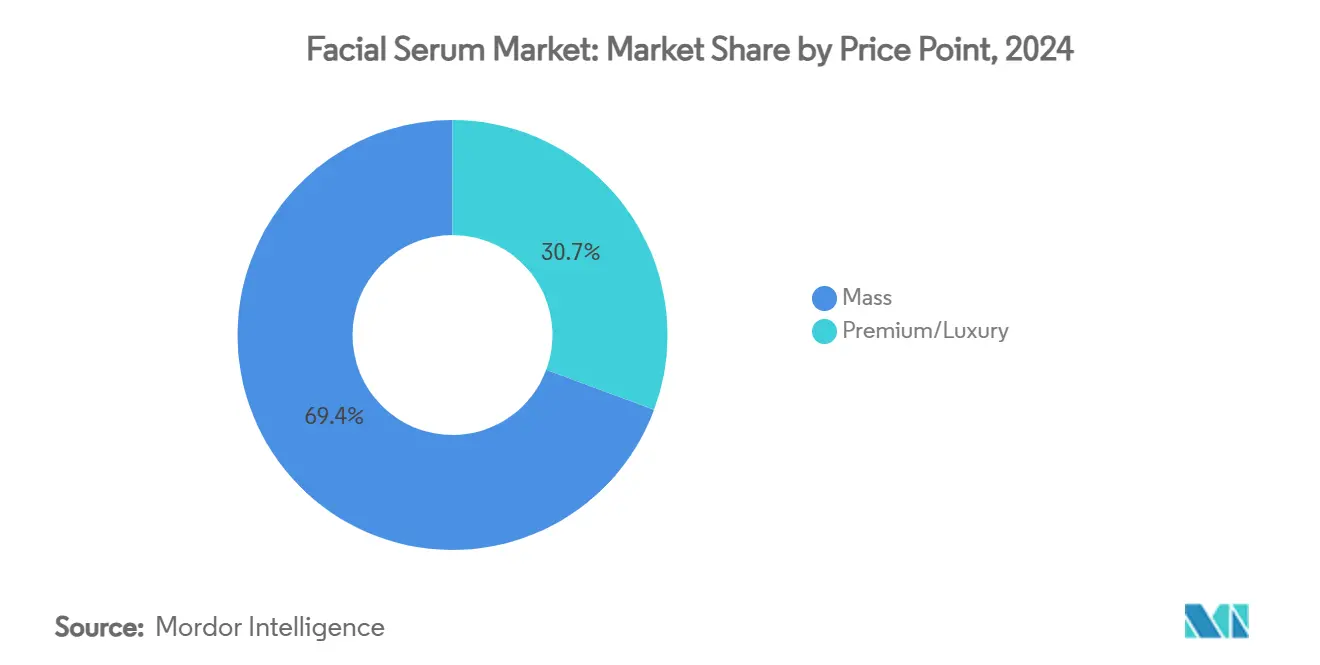

- By price point, the mass segment accounted for 69.35% of 2024 revenue, whereas the premium/luxury segment is forecast to expand at a 9.04% CAGR to 2030.

- By distribution channel, health and beauty stores accounted for 36.47% of sales in 2024, while online retail is projected to grow at a CAGR of 9.12% during the forecast period.

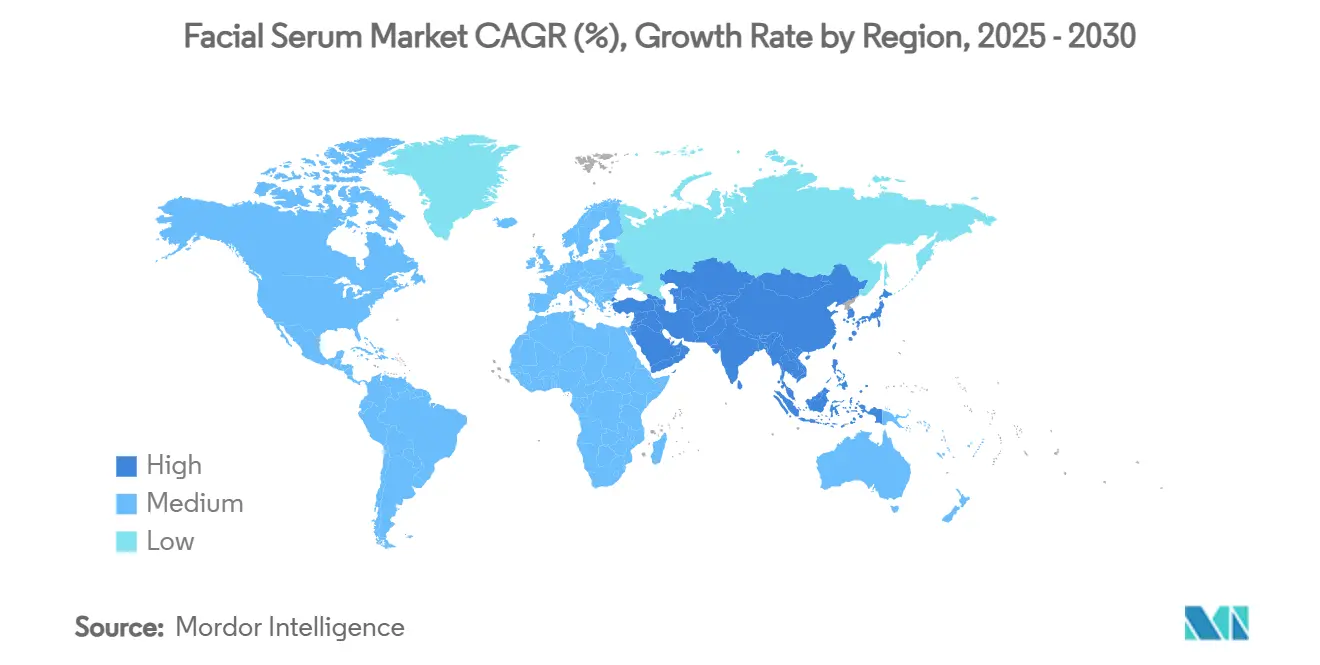

- By geography, the Asia-Pacific region accounted for 35.28% of the market revenue in 2024, while the Middle East and Africa region is expected to grow at the highest CAGR of 8.65% during the forecast period 2025-2030.

Global Facial Serum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for anti-aging solutions | +1.8% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Influence of K-beauty and J-beauty trends | +1.2% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising consumer preference for clean, natural, organic, vegan formulations | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rise of personalized skincare | +1.0% | North America and Europe, early adoption in urban Asia-Pacific | Long term (≥ 4 years) |

| Demand for multifunctional and targeted solutions | +1.3% | Global | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +0.9% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for anti-aging solutions

The anti-aging serum segment dominates the market due to demographic changes, with the global population aged 60 and above expected to reach 2.1 billion by 2050[2]Source: World Health Organization, “Ageing and health,” who.int. The segment's market share growth stems from aging populations and increased preventive skincare adoption among younger consumers, particularly millennials. Advancements in peptide technology, specifically OS-01 peptide formulations, have demonstrated improved skin barrier function and reduced inflammation markers in 12-week clinical trials. These scientifically validated results enable premium pricing strategies, maintaining segment profitability despite market competition. The combination of aging demographics and growing preventive skincare trends continues to drive segment expansion.

Influence of K-beauty and J-beauty trends

Korean and Japanese beauty practices have transformed global skincare routines, making facial serums essential rather than supplementary products. Their influence has expanded into ingredient development, as Korean research has advanced the use of fermented botanicals and peptide complexes in skincare formulations. These ingredients undergo extensive fermentation processes that break down compounds into smaller, more easily absorbed molecules. Shiseido's identification of OBP2A protein expression in human skin, which responds to French white lily flower extract, demonstrates the scientific contributions of Japanese beauty research. The study revealed that this protein plays a crucial role in maintaining skin barrier function and moisture retention. Companies that combine Asian beauty principles with scientific research gain market advantages through product differentiation and enhanced efficacy claims supported by clinical studies.

Rising consumer preference for clean, natural, organic, vegan formulations

The U.S. Food and Drug Administration's enhanced oversight under MoCRA enables natural formulation companies to differentiate their products through quality standards, aligning with growing consumer demand for clean beauty products. This movement extends beyond ingredient selection to include sustainable packaging and responsible manufacturing practices. Companies using fermented bioactives demonstrate improved product stability and effectiveness compared to traditional extraction methods. Consumers demonstrate a willingness to pay higher prices for clean formulations based on shared values, providing competitive advantages for established clean beauty brands. The market's growth in the Asia-Pacific regions creates opportunities to blend traditional herbal knowledge with modern formulation techniques. This integration allows companies to maintain premium pricing while developing customer loyalty through value-driven positioning.

Demand for multifunctional and targeted solutions

The increasing complexity in serum formulations aligns with consumer demand for products that target multiple skin concerns at once, reflecting both modern lifestyle needs and growing skincare awareness. Research shows that multifunctional formulations containing Palmitoyl Tripeptide-38, Hydrolyzed Hyaluronic Acid, and Bakuchiol deliver measurable results, with clinical studies documenting a 23.82% increase in skin moisture along with improvements in elasticity and brightness[3]Source: Scientific Research Publishing Inc., “A Face Serum Containing Palmitoyl Tripeptide-38, Hydrolyzed Hyaluronic Acid, Bakuchiol and a Polyherbal and Vitamin Blend Improves Skin Quality,” scirp.org. This development benefits companies with strong research capabilities and regulatory knowledge, as these complex formulations require thorough safety and stability testing. The market has evolved toward pharmaceutical-grade effectiveness, particularly with peptide-based alternatives to injectables, where compounds like Argireline and SYN-Ake produce Botox-like effects through neurotransmitter inhibition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing limiting penetration in emerging markets | -1.1% | South America, Middle East and Africa, parts of Asia-Pacific | Medium term (2-4 years) |

| Rise of counterfeit and imitation products | -0.8% | Global, concentrated in online channels | Short term (≤ 2 years) |

| Regulatory caps on active-ingredient concentration, labelling, and claims | -0.6% | Global, varying by jurisdiction | Long term (≥ 4 years) |

| Concerns over product safety and allergic reactions | -0.7% | Global, heightened in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium pricing limiting penetration in emerging markets

Price sensitivity in emerging markets affects facial serum adoption rates. Consumers in these markets often prioritize essential products over premium skincare items due to limited disposable income. This creates a need for brands to develop market-specific formulations and pricing strategies that balance product effectiveness with affordability. Local competitors use their lower cost structures to offer functional alternatives by utilizing regional ingredients and streamlined production processes, requiring international brands to demonstrate premium value through ingredient quality and clinical validation. Pricing strategies face additional complexity from currency fluctuations and import duties, especially for brands using imported active ingredients, as these factors directly impact production costs and final retail prices.

Rise of counterfeit and imitation products

The European Union cosmetics industry faces annual losses of EUR 3 billion due to counterfeit products, resulting in approximately 32,000 job losses[4]Source: European Union Intellectual Property Office, “Economic impact of counterfeiting in the clothing, cosmetics, and toy sectors in the EU,” euipo.europa.eu. The Modernization of Cosmetic Regulation Act (MoCRA) has strengthened U.S. Food and Drug Administration enforcement capabilities through enhanced registration requirements, with 589,762 active cosmetic product listings recorded in the U.S. Food and Drug Administration database as of January 2025. The elimination of the de minimis loophole for low-value shipments has improved coordination between the FDA and Customs and Border Protection to intercept non-compliant products. Companies are responding by implementing robust supply chain security measures, consumer education programs, and intellectual property protection strategies to safeguard market integrity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: Anti-Aging Dominance Drives Innovation

Anti-aging serums hold the largest market share at 35.12% in 2024, due to demographic changes such as an aging population and increased life expectancy. The growing adoption of preventive skincare across different age groups is driven by rising awareness of early skin maintenance, increased disposable income, and the influence of social media beauty trends. Young consumers are starting anti-aging routines earlier, while older consumers seek advanced formulations, contributing to the segment's dominance.

The acne treatment serum segment is expected to grow at a CAGR of 8.22% through 2030. This growth is driven by increasing consumer preference for targeted skincare solutions, rising awareness of specialized treatments, and advancements in serum formulations. The segment benefits from the growing demand for non-prescription acne solutions, particularly among young adults and teenagers. Additionally, the rise in disposable income and expanding urban populations contribute to the increased adoption of premium acne treatment products.

By Form: Water-Based Formulations Lead Market Evolution

Water-based serums hold a dominant 60.26% market share in 2024, as consumers favor their lightweight texture and ability to layer with other skincare products. Oil-based formulations demonstrate stronger growth potential with an 8.76% CAGR through 2030, as users increasingly value their skin barrier-strengthening properties. This market distribution indicates consumers' growing understanding of formulation types and their specific benefits in skincare routines. Oil-based serums align with clean beauty preferences, offering natural alternatives to synthetic ingredients. The gel-based segment introduces innovative hybrid formulations that combine the benefits of both water and oil-based delivery systems.

Advanced formulation technologies create enhanced texture profiles and delivery systems, including encapsulated active ingredients and time-release mechanisms. The growth of personalized skincare increases demand for adaptable formulations that respond to individual skin needs and environmental conditions. Regional climate differences influence consumer preferences, with water-based formulas performing well in humid areas and oil-based variants showing strength in dry climates. Improved packaging solutions, particularly airless systems, enhance product stability and user experience across all formulation types.

By Price Point: Premium Segment Outpaces Mass Market

The mass market segment holds 69.35% market share in 2024, driven by broad consumer accessibility. The premium/luxury segment demonstrates stronger growth at 9.04% CAGR through 2030, as consumers show increased willingness to invest in products with higher perceived efficacy and brand value. This market division creates two distinct strategic approaches: mass market brands prioritize value and accessibility, while premium brands focus on ingredient innovation and clinical validation.

Premium brands leverage ingredient transparency and clinical testing to justify higher price points, with consumers demonstrating acceptance of increased costs for products with documented efficacy and safety. Direct-to-consumer distribution models enable premium positioning without traditional retail margins, reshaping competition in the luxury segment. During economic uncertainty, premium brands maintain stability as consumers prioritize quality in skincare purchases. The integration of wellness and beauty trends provides opportunities for premium brands to market facial serums as health investments.

By Distribution Channel: Digital Transformation Accelerates

Health and beauty stores hold a 36.47% market share in 2024, offering product sampling opportunities and expert consultation services. Online retail stores demonstrate the highest growth rate at 9.12% CAGR through 2030, benefiting from convenience and broader product assortments. This shift in distribution channels reflects evolving consumer preferences, especially among younger consumers who rely on digital research and customer reviews rather than traditional retail experiences. Hypermarkets/supermarkets function as discovery points for mass market products.

Brands implement omnichannel strategies to provide consistent experiences across all customer touchpoints. They invest in virtual try-on capabilities and personalized product recommendations to replicate in-store consultation services online. Social commerce facilitates influencer-based sales, particularly for facial serums where product education and application demonstrations influence purchasing decisions. Subscription-based models generate recurring revenue streams while fostering customer loyalty through customized product selection.

Geography Analysis

Asia-Pacific holds 35.28% market share in 2024, supported by cultural emphasis on skincare routines and increasing disposable incomes. The Middle East and Africa show the highest growth rate at 8.65% CAGR through 2030. The Asia-Pacific region's strong position comes from established beauty practices in South Korea and Japan, where multi-step skincare routines have made facial serums essential products. China's large consumer base and expanding middle class drive continuous demand growth, while Southeast Asian markets grow through K-beauty influence and urbanization. India's beauty market expansion, supported by its young population and increased digital commerce use, adds to regional growth.

North America demonstrates stable market growth through new product adoption and preference for premium offerings. The Modernization of Cosmetic Regulations Act (MoCRA) provides competitive benefits to established companies with strong compliance systems. Consumers in this region show readiness to invest in scientifically proven formulations, encouraging continued product development by major companies. Canada and Mexico offer growth potential through online cross-border sales and growing middle-class consumers seeking quality skincare products.

Europe shows advanced consumer preferences for clean beauty products and sustainable packaging, creating market opportunities for environmentally conscious brands that maintain product effectiveness. The region's strict regulations on cosmetic safety and marketing claims benefit companies with strong scientific backing and regulatory knowledge. Brexit continues to influence supply chain operations and market strategies, while Eastern European markets show growth potential due to improving living standards and increased beauty awareness. The Middle East and Africa's growth reflects increasing urbanization, higher disposable incomes, and growing beauty consciousness, particularly among younger consumers seeking premium products.

Competitive Landscape

The facial serum market exhibits moderate concentration with a score of 6 out of 10, enabling both established giants and emerging disruptors to capture value through differentiated positioning strategies. Major players like L'Oréal, Estée Lauder, and Shiseido leverage extensive R&D capabilities and global distribution networks to maintain market leadership, while emerging brands like DECIEM (The Ordinary) and Drunk Elephant disrupt traditional pricing models through direct-to-consumer strategies and ingredient transparency.

Strategic patterns reveal increasing investment in peptide technology and personalized formulations, with brands seeking to differentiate through scientific validation and clinical efficacy rather than marketing claims alone. Technology adoption drives competitive differentiation, with companies investing in AI-enhanced formulation development and personalized skincare solutions that adapt to individual skin conditions and environmental factors.

White-space opportunities exist in underserved demographics and emerging markets, where local brands can leverage cultural understanding and cost advantages to compete effectively against international players. The rise of clean beauty and sustainable packaging creates entry opportunities for brands that authentically integrate environmental values with product efficacy, while regulatory compliance requirements favor companies with robust quality systems and scientific expertise.

Facial Serum Industry Leaders

Unilever PLC

L'oreal SA

Estee Lauder Companies Inc.

Johnson & Johnson Services LLC

Procter & Gamble Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Aptar Beauty and Clarins introduced the ninth generation of their Double Serum product. The design incorporates two chambers containing lipidic and hydric serums that dispense simultaneously. The packaging comprises 94% recyclable materials and incorporates 24% recycled content.

- July 2025: Sacred Rituel launched Sacred Serum, an organic face oil with broad-spectrum SPF 10 that has received MADE SAFE certification. The serum contains plant-based, cold-pressed botanicals including raspberry seed,

- June 2025: Shiseido held a pop-up event at Herald Square Plaza in New York City to launch its new Ultimune Power Infusing Serum, which is available exclusively at Macy's. The serum, developed from 30 years of skin immunity research, aims to decelerate the skin aging process.

- April 2025: TruSkin has launched its SPF 30 Mineral Sunscreen Facial Serum. The product combines botanical ingredients to hydrate and firm the skin while providing sun protection in a lightweight, non-whitening formula.

Global Facial Serum Market Report Scope

| Hydrating Serum |

| Anti-ageing Serum |

| Brightening/Lightening Serum |

| Acne Fighting Serum |

| Exfoliating Serum |

| Others |

| Oil-based |

| Water-based |

| Others |

| Mass |

| Premium/Luxury |

| Hypermarkets/Supermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Functionality | Hydrating Serum | |

| Anti-ageing Serum | ||

| Brightening/Lightening Serum | ||

| Acne Fighting Serum | ||

| Exfoliating Serum | ||

| Others | ||

| By Form | Oil-based | |

| Water-based | ||

| Others | ||

| By Price Point | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the facial serum market?

The facial serum market size is valued at USD 7.32 billion in 2025 and is projected to reach USD 10.51 billion by 2030.

Which functionality segment holds the largest revenue share?

Anti-aging serums command the top position with 35.12% of 2024 sales, reflecting strong demand across age groups.

Which region is expanding the fastest?

The Middle East and Africa region is expected to record the highest CAGR at 8.65% from 2025-2030, driven by rising urban incomes and beauty awareness.

Why are oil-based serums growing faster than water-based variants?

Oil-based formulas gain momentum due to barrier-repair narratives, clean-beauty trends, and consumer education on the role of lipophilic carriers in locking moisture.

Page last updated on: