Lipstick Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

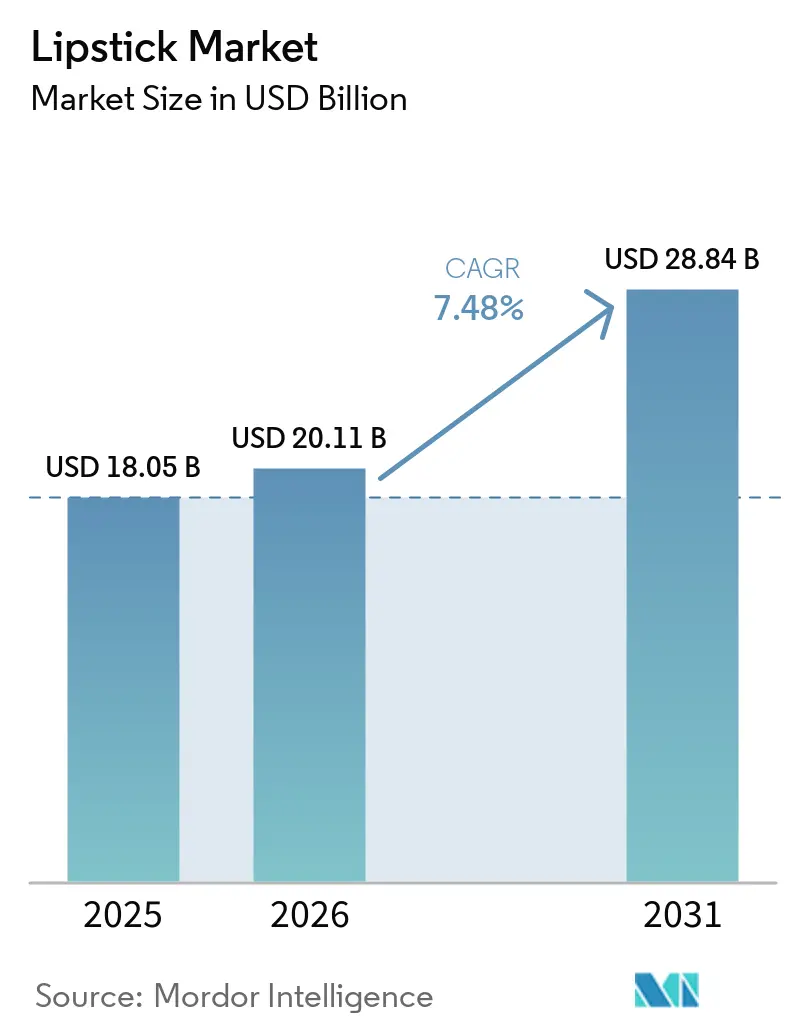

| Market Size (2026) | USD 20.11 Billion |

| Market Size (2031) | USD 28.84 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

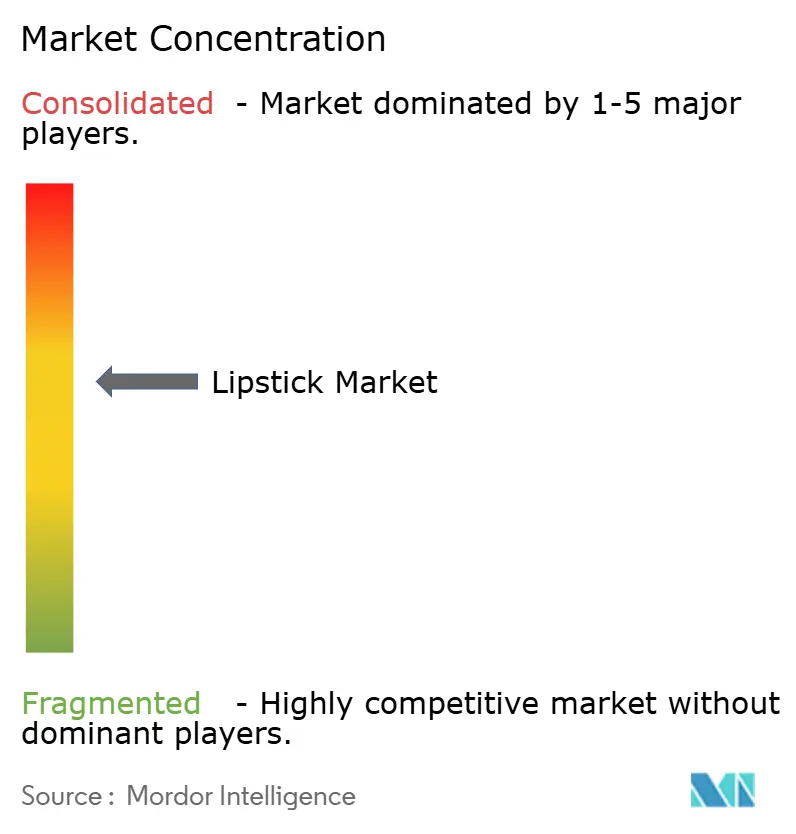

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lipstick Market Analysis by Mordor Intelligence

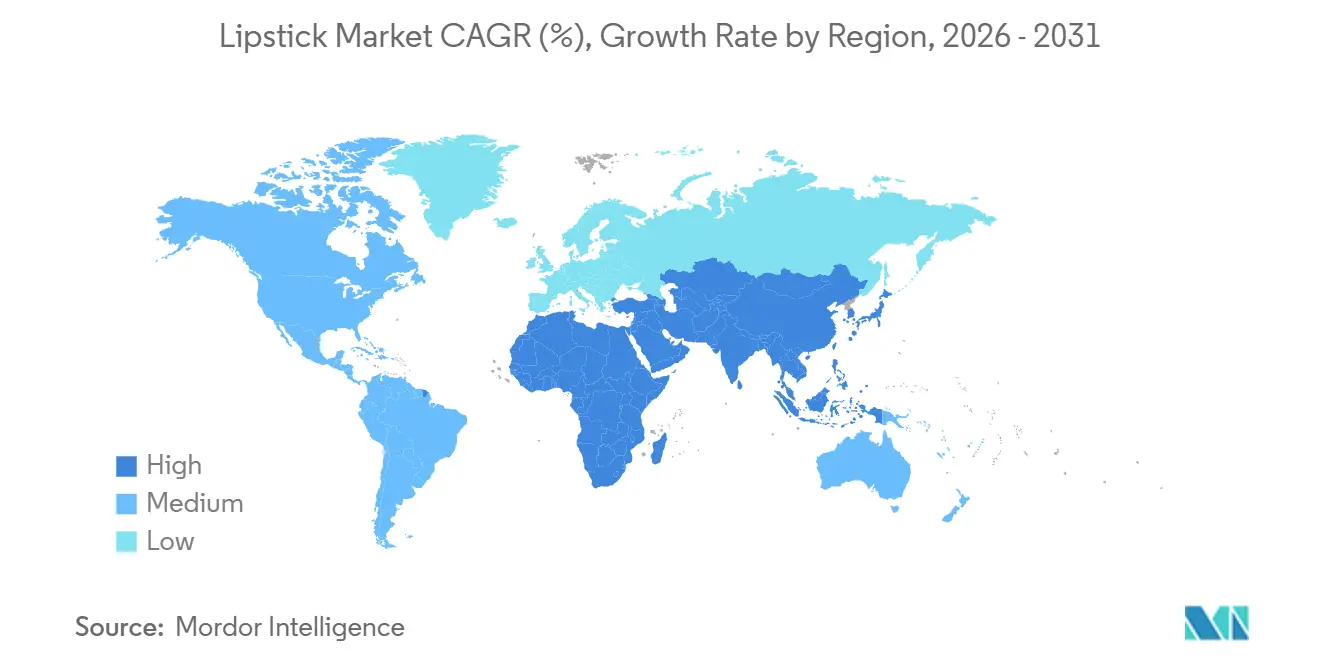

The lipstick market was valued at USD 18.05 billion in 2025, and is expected to reach USD 20.11 billion in 2026, and is projected to grow to USD 28.84 billion by 2031, registering a CAGR of 7.48% during the forecast period. This growth is attributed to factors such as the acceleration of digital commerce, increasing demand for clean formulations, and a shift from mass-market products to premium, influencer-endorsed offerings. The Asia-Pacific region accounted for 34.40% of the revenue in 2025 and is expected to experience the fastest regional growth, with a CAGR of 8.01% through 2031. This growth is driven by increasing per-capita beauty expenditures in India and China, the expansion of K-beauty exports into Latin America, and the rise of live-commerce platforms that integrate entertainment with instant purchasing options.

Key Report Takeaways

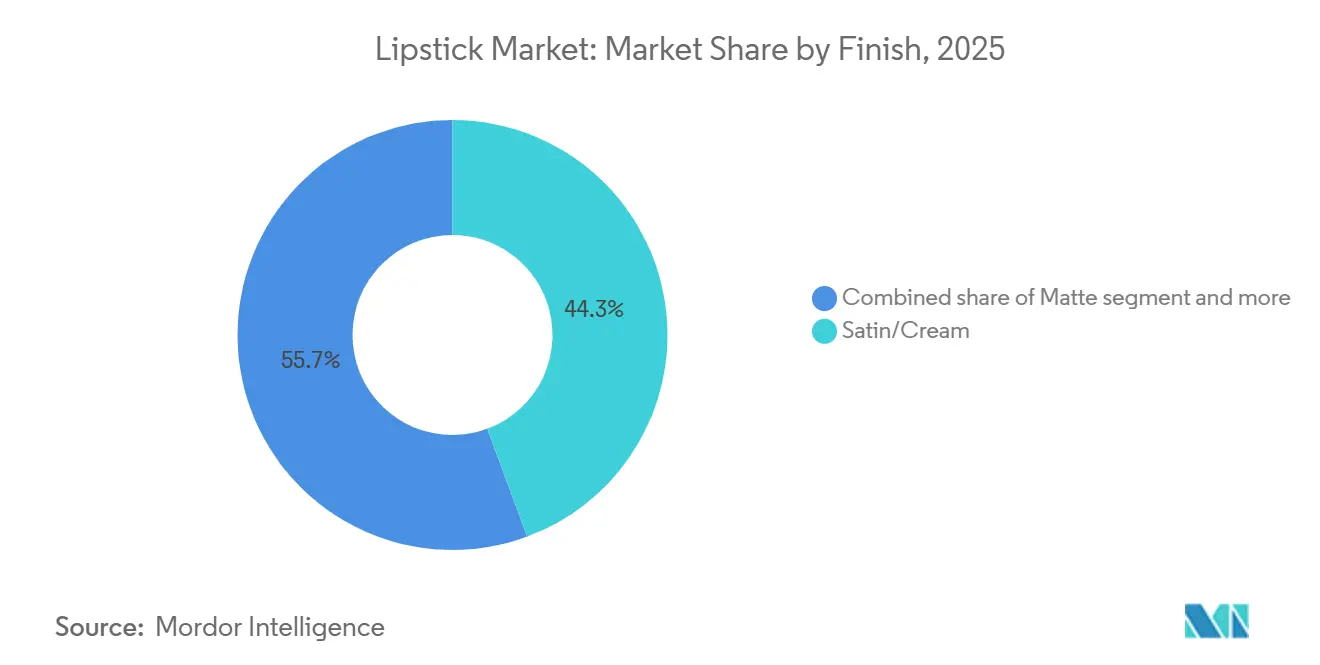

- By finish, satin/cream led with 44.34% of the 2025 lipstick market share and matte is poised to grow fastest at a 7.59% CAGR through 2031.

- By form, stick products commanded 59.18% of the lipstick market size in 2025, while liquid formats are forecast to expand at 7.81% CAGR.

- By price range, mass held 62.19% of 2025 revenue; premium and luxury are expected to expand at 8.28% CAGR.

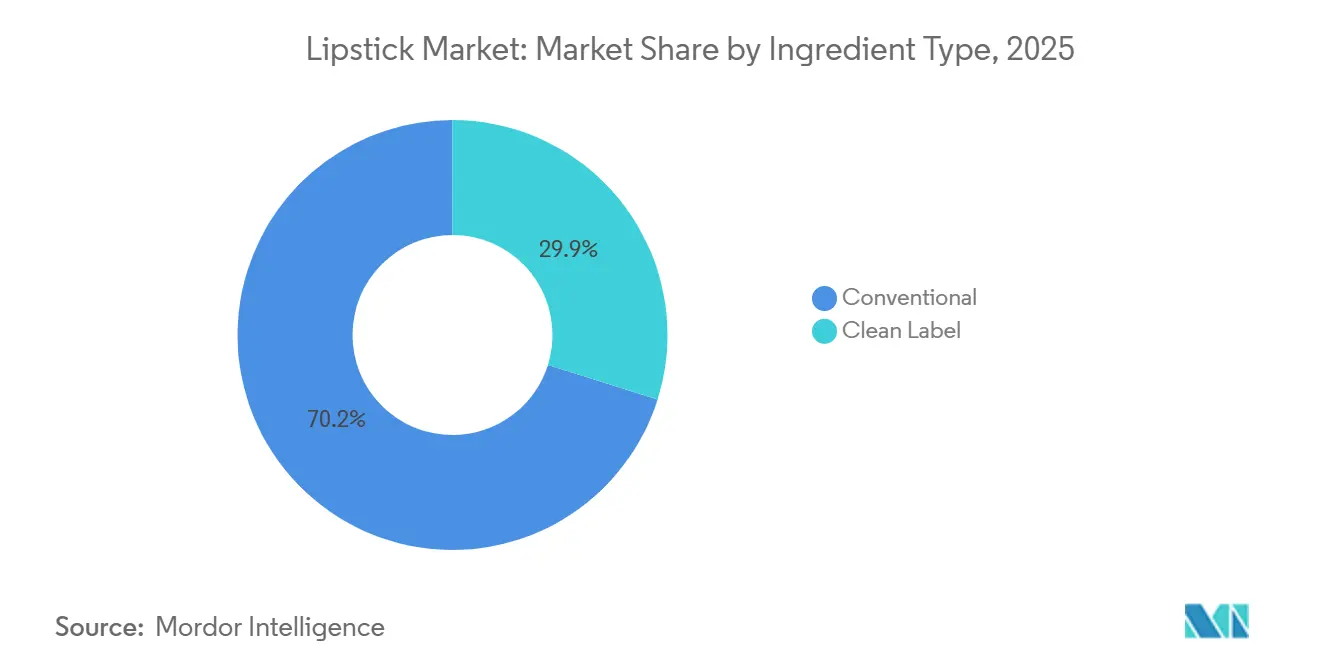

- By ingredient type, conventional captured 70.15% share in 2025; clean label alternatives are predicted to rise at a 8.67% CAGR.

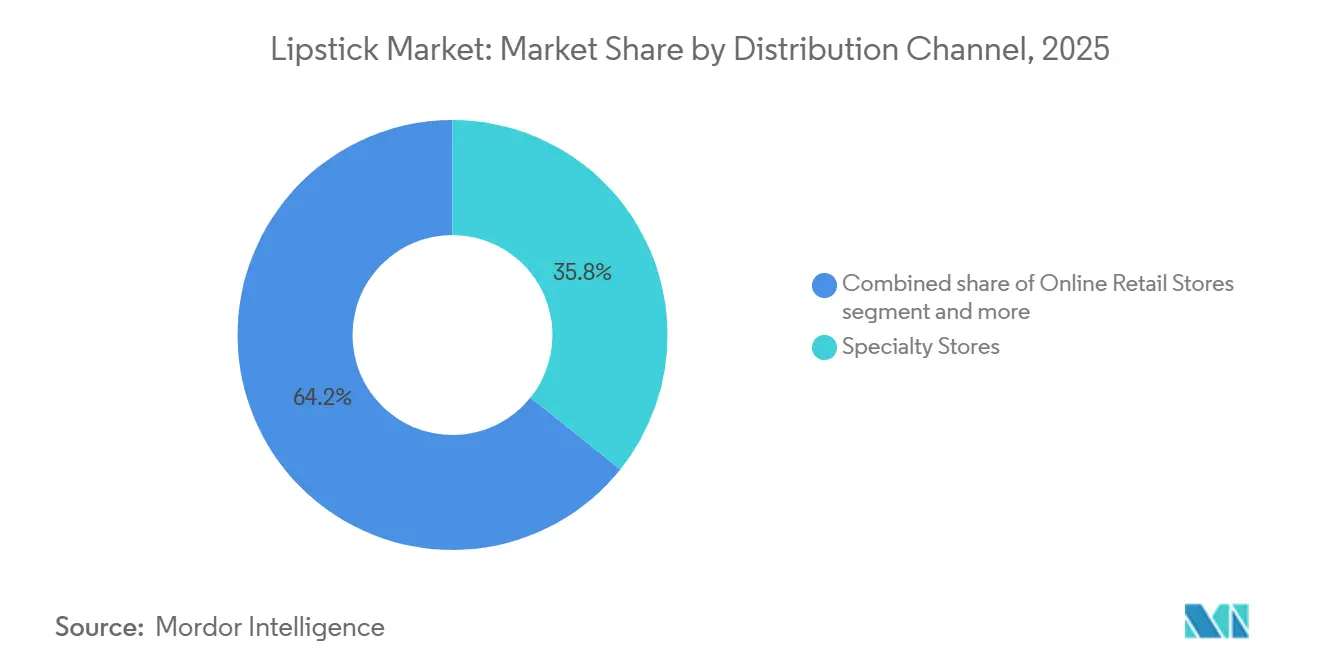

- By distribution, specialty stores accounted for 35.76% of sales in 2025, yet online retail is set to grow fastest at 9.07% CAGR.

- By geography, Asia-Pacific secured 34.40% of the 2025 lipstick market share and is forecast to register the fastest regional CAGR of 8.01% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lipstick Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising beauty consciousness and personal grooming | +1.2% | Global, with a stronger impact in Asia-Pacific and South America | Medium term (2-4 years) |

| Product innovation and texture Diversification | +1.5% | Global, led by North America and Europe, research and development centers | Long term (≥ 4 years) |

| Demand for natural, vegan, and sustainable products | +1.8% | North America and European Union regulatory-driven, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Influence of social media and beauty influencers and celebrity brands | +2.1% | Global, with peak impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Premiumization and aspirational consumption | +0.9% | Global, with the highest impact in North America and emerging markets | Medium term (2-4 years) |

| Innovative, sustainable packaging enhancing user experience and brand appeal | +1.1% | North America and European Union technology-driven, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising beauty consciousness and personal grooming

The post-pandemic recovery in makeup consumption highlights the "lipstick effect," a consumer behavior trend where individuals opt for affordable luxury items during periods of economic uncertainty. This phenomenon occurs as consumers shift their spending from high-end luxury goods to more accessible indulgences, particularly cosmetics. For instance, John Lewis reported a 14% rise in lip product sales, with these items emerging as status symbols akin to luxury accessories. The trend is also broadening its reach, with male consumers, especially in China, increasingly purchasing cosmetics. Lip products have become entry-level items for makeup experimentation, signifying a broader movement toward self-expression and personal branding. This pattern is particularly pronounced in emerging markets, where rising disposable incomes are driving higher expenditure on beauty products.

Product innovation and texture Diversification

Recent advancements in lipstick formulation technology address consumer concerns by combining color cosmetics with skincare benefits. Shiseido's "Automatic Veil Technology" enhances product durability by enabling lipstick films to self-repair minor damage caused by regular use. This technology incorporates specialized polymers that respond to mechanical stress, redistributing the product to maintain an even layer on the lips, potentially extending the product's lifespan. Similarly, Global Bioenergies has introduced plant-based isododecane, offering a sustainable alternative to petroleum-derived ingredients while maintaining performance standards. This plant-based isododecane is produced through a fermentation process using renewable resources, resulting in a molecularly identical substitute for conventional petroleum-based components. Additionally, consumer demand for extended-wear products continues to drive growth in the long-lasting cosmetics market. These innovations are significant as companies strive to replace synthetic waxes with plant-based alternatives.

Demand for natural, vegan, and sustainable products

The regulatory environment for cosmetics is undergoing significant changes, with seven states, including California, Colorado, and Washington, introducing PFAS restrictions that necessitate product reformulation between 2025 and 2030. These regulations pose operational challenges for manufacturers, who must balance maintaining product performance with meeting diverse jurisdictional requirements. At the federal level, the FDA's Modernization of Cosmetics Regulation Act (MoCRA) requires PFAS safety assessments in cosmetics by December 2025[1]Source: U.S. Food & Drug Administration, “Modernization of Cosmetics Regulation Act (MoCRA),” fda.gov. Consumer preferences are also shifting in line with these regulatory developments. According to Shopify's 2024 beauty e-commerce trends report, 69% of consumers show increased interest in sustainable practices. The industry is responding with technological advancements, such as L'Oréal's partnership with IBM to create AI-powered formulation tools for sustainable ingredients, aligning with their objective to source 95% of ingredients from renewable sources by 2030.

Influence of social media and beauty influencers and celebrity brands

Social media platforms have significantly influenced lipstick marketing and consumer discovery patterns. Platforms like TikTok and Instagram facilitate rapid product launches, enabling brands to achieve substantial reach within weeks. In South Korea in 2024, Instagram was among the most popular social media platforms, with approximately 45.8% of population indicating it as their most frequently used platform[2]KISDI STAT, stat.kisdi.re.kr. Research from Bryant University shows that 86% of beauty brands utilize influencer marketing, as Gen Z consumers prioritize authenticity and relatability over traditional celebrity endorsements. This trend also impacts product development, as seen with Florasis, which became a top seller on Amazon Japan by offering collections inspired by local cultural aesthetics. Celebrity-founded brands, such as Hailey Bieber's Rhode, are reshaping market dynamics by employing innovative marketing strategies, including branded phone cases, to create comprehensive lifestyle experiences around lip products. Additionally, TikTok Shop's social commerce capabilities are expected to boost the beauty market share for digital-native channels. Traditional brands are adapting to this digital transformation, with M·A·C reporting a 200% increase in customer engagement through Perfect Corp's virtual try-on technology integrated with social media platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns around PFAS and heavy-metal pigments | -0.8% | North America and European Union regulatory-driven, expanding globally | Medium term (2-4 years) |

| Increasing availability of counterfeit products | -0.6% | Global, with highest impact in Asia-Pacific and online channels | Short term (≤ 2 years) |

| Regulatory challenges | -0.7% | North America and European Union leading, with spillover to other regions | Medium term (2-4 years) |

| Sustainability and environmental issues | -0.5% | Global, with stronger pressure in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns around PFAS and heavy-metal pigments

Regulatory actions targeting per- and polyfluoroalkyl substances (PFAS) in cosmetics are causing notable market disruptions and increasing reformulation costs across various regions. In May 2025, the FDA rejected 89 batches of imported cosmetics, with 50 batches classified as "unapproved new drugs" due to ingredient safety classification issues. New Zealand's Environmental Protection Authority has announced a PFAS ban in cosmetics, set to take effect in December 2026[3]Source: Environmental Protection Authority, "EPA bans ‘forever chemicals’ in cosmetic products," epa.govt.nz. Similarly, the European Union's evaluation of PFAS restrictions under REACH, following France's implementation of a ban in January 2026, has introduced diverse compliance requirements impacting global supply chain operations. Companies are now required to invest in alternative formulation technologies while addressing performance challenges, such as developing plant-based substitutes for synthetic waxes that preserve product quality. These regulatory changes are creating market uncertainty and increasing development costs, particularly for smaller brands with limited research and development capabilities to meet varying regulatory demands.

Increasing availability of counterfeit products

The rise of counterfeit lipstick products through e-commerce channels presents significant challenges to brand integrity and consumer safety. According to U.S. Customs and Border Protection, 31% of counterfeit goods intercepted in fiscal year 2023 were beauty products. Recent enforcement efforts highlight the scale of the issue, with Cincinnati CBP seizing 318 shipments worth USD 1.23 million in a single operation targeting illegal cosmetic imports from China, South Korea, and Hong Kong. Criminal cases, such as the prosecution of Rebecca Fadanelli for smuggling counterfeit Botox and dermal fillers, emphasize the health risks posed by unregulated cosmetic products. The planned closure of the "de minimis loophole" for low-value shipments, through an executive order set for April 2025, is expected to strengthen customs enforcement. However, the rapid expansion of social commerce platforms introduces new avenues for counterfeit product distribution, necessitating ongoing monitoring and adaptive enforcement strategies. This situation not only threatens the market share of legitimate brands but also poses consumer safety risks that could erode trust in the overall lipstick market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Finish: Matte Formulations Drive Innovation

The satin/cream finish lipsticks accounted for a dominant market share of 44.34% in 2025, while the matte lipstick segment is projected to grow at a CAGR of 7.59% during 2026-2031. The growth of the matte lipstick segment is driven by increasing demand for long-lasting, transfer-resistant products that align with consumer preferences. Advances in formulation technology have contributed to this growth by addressing traditional comfort challenges. Manufacturers are introducing hybrid formulations that combine the matte finish with improved wearability and moisturizing properties.

Satin finish lipsticks continue to be popular due to their versatility and appeal across various age groups. These lipsticks offer a balanced combination of color intensity and comfortable wear without feeling heavy on the lips. Their formulation ensures easy application and long-lasting results, making them suitable for both professional settings and casual occasions. The moderate sheen of satin finishes provides a natural-looking appearance while maintaining vibrant color throughout the day. The "Others" category, which includes glossy, metallic, and specialty finishes, presents emerging opportunities for differentiation. Brands are exploring innovative textures and effects, leveraging the visual-first culture of social media to attract consumers.

By Form: Liquid Formats Surge on Application Innovation

Stick formats maintained a dominance with a 59.18% market share in 2025, while the liquid lipstick segment is expected to grow at a CAGR of 7.81% during 2026-2031. This growth is driven by innovations in applicator technology and the influence of viral social media trends showcasing dramatic color transformations. Liquid formulations offer superior color intensity and longevity compared to traditional stick formats, appealing to consumers seeking professional-quality results and extended wear. Market growth reflects advancements in liquid lipstick formulations that address issues such as drying, flaking, and uneven application through improved chemical compositions and applicator designs.

Stick formats continue to dominate the market due to their convenience, portability, and ease of application, particularly for consumers requiring quick touch-ups and on-the-go solutions. Crayon formats attract younger consumers looking for user-friendly products, while palette formats cater to professional makeup artists and enthusiasts who prioritize color customization and blending options. The market reflects a division between traditional formats emphasizing convenience and innovative liquid formulations focusing on performance. Companies are increasingly offering hybrid products that combine features from multiple formats to appeal to a broader consumer base.

By Price Range: Premium Segment Accelerates Growth

The mass products segment accounted for a 62.19% market share in 2025, while the premium and luxury segments are projected to grow at a CAGR of 8.28% during 2026-2031. This growth is attributed to effective premiumization strategies, including celebrity collaborations, specialized formulations, and enhanced packaging designs. The expansion of the premium segment is driven by consumers' increasing willingness to invest in high-quality products that deliver superior performance, unique aesthetics, and brand prestige. This trend is particularly prominent among younger demographics, who perceive beauty purchases as a means of self-expression and social signaling. For instance, Estée Lauder's collaboration with Indian designer Sabyasachi Mukherjee, featuring 10 lipstick shades in ornate packaging with 24K gold accents, highlights how premium brands are creating culturally relevant luxury experiences that justify higher price points.

Mass market products continue to dominate due to their accessible pricing and widespread distribution, serving as entry points for new consumers and providing reliable options for established users. The segment's resilience underscores the democratization of beauty, where effective formulations and appealing aesthetics are increasingly accessible across various price points. However, the faster growth of the premium segment indicates that successful brands must adopt portfolio strategies that capture the shift toward higher-priced products while maintaining mass market appeal. For example, brands like Too Faced have achieved success, such as securing the #1 position in the U.S. lip plumping category, through strategic positioning and placement in platforms like the Amazon Premium Beauty store.

By Ingredient Type: Clean Label Transformation

Conventional ingredients accounted for a 70.15% market share in 2025, while clean label formulations are projected to grow at a CAGR of 8.67% during 2026-2031. This growth is driven by regulatory requirements and increasing consumer demand for transparent cosmetic formulations. The shift toward clean labels highlights consumer health awareness, environmental concerns, and the need for regulatory compliance. Companies are increasingly investing in bio-based alternatives that deliver performance comparable to traditional synthetic ingredients. For instance, L'Oréal's collaboration with IBM on AI-powered sustainable formulation tools demonstrates how technology supports the transition to clean ingredients while maintaining product efficacy.

Conventional formulations continue to dominate the market due to their proven performance, established supply chains, and cost advantages, particularly in price-sensitive mass market segments where premium ingredient adoption is limited. However, the regulatory environment is evolving rapidly, with restrictions on PFAS in multiple states and the FDA's MoCRA requirements creating compliance challenges that favor clean label alternatives. This transformation is generating opportunities for ingredient suppliers and contract manufacturers capable of developing cost-effective natural alternatives.

By Distribution Channel: Digital Commerce Reshapes Retail

Specialty stores held the largest market share at 35.76% in 2025, while online retail stores are projected to grow at a CAGR of 9.07% during 2026-2031. This growth reflects the ongoing digital transformation of beauty retail and shifts in consumer shopping behaviors, accelerated by adaptations during the pandemic. The expansion of online retail is supported by advancements in digital experiences, such as augmented reality try-on tools, personalized recommendations, and social commerce integration, which address traditional challenges associated with purchasing cosmetics online.

Specialty stores maintain their market leadership by offering curated product selections, professional consultations, and retail environments that enable product testing. Hypermarkets, supermarkets, drug stores, and pharmacies provide convenience and accessibility for mass-market products and routine purchases. The evolving retail landscape highlights the importance of omnichannel strategies that integrate online and offline platforms. For example, John Lewis's augmented reality (AR) lipstick try-on feature bridges digital and physical shopping experiences, demonstrating the effectiveness of such approaches.

Geography Analysis

Asia-Pacific dominated the global lipstick market with a 34.40% share in 2025 and is projected to experience the fastest regional growth at a CAGR of 8.01% from 2026 to 2031. This growth is attributed to the expanding middle-class population, rising disposable incomes, and cultural shifts toward beauty consciousness in key markets such as China, India, and Japan. The region's growth is further supported by the success of local brands, exemplified by Chinese brand Florasis, which achieved top-seller status on Amazon Japan through culturally-inspired collections. This highlights the potential for regional brands to achieve cross-border success. Additionally, the region's digital-first consumer behavior is transforming distribution channels, with social commerce and livestream selling gaining significant traction in markets like China and South Korea.

North America and Europe are characterized as mature markets with established infrastructure and sophisticated consumer preferences. Growth in these regions is driven by trends such as premiumization, the adoption of clean beauty products, and advancements in retail technology. However, these markets face significant regulatory pressures related to ingredient safety. For instance, PFAS restrictions in the United States and European Union REACH evaluations are creating compliance challenges, favoring larger brands with robust research and development capabilities to navigate these regulatory landscapes.

The Middle East and Africa lipstic market is experiencing growth driven by social reforms that empower women and foster new consumption patterns. The region's unique climate conditions are encouraging the development of specialized formulations designed to withstand extreme weather, creating opportunities for brands that can meet these specific performance requirements. South America presents significant growth potential in the beauty market. Regional companies such as Natura and O Boticário maintain strong domestic market positions, while international brands are expanding their presence through digital platforms and strategic partnerships. Growth in this region is fueled by improved e-commerce infrastructure and increased social media usage, which facilitate brand discovery and influence purchasing behavior, particularly among younger consumers.

Competitive Landscape

The lipstick market is moderately consolidated. This indicates a balanced environment where established multinational corporations coexist with emerging disruptors and regional players. Prominent beauty conglomerates such as L'Oréal, Estée Lauder, and Coty hold significant market positions, supported by extensive brand portfolios, global distribution networks, and substantial investments in research and development. The competitive landscape is evolving with increased technology integration. For instance, companies like Perfect Corp have enabled brands to achieve up to a 200% increase in customer engagement through AI-powered virtual try-on tools, reshaping online shopping behaviors.

Opportunities in the market are emerging at the intersection of sustainability and technology. Companies offering environmentally friendly formulations with high performance are gaining market share from established manufacturers. Additionally, the regulatory environment is favoring companies with strong compliance capabilities and reformulation expertise. Restrictions on PFAS and other safety requirements provide a competitive edge to brands with robust research and development resources and regulatory affairs capabilities.

Celebrity and influencer-founded brands are disrupting traditional marketing strategies by fostering authentic connections with younger consumers. In response, established companies are pursuing strategic partnerships and acquisitions to integrate digital-native capabilities. The competitive landscape is increasingly shaped by the ability to merge online and offline experiences. Successful brands are adopting omnichannel strategies that incorporate augmented reality, personalized recommendations, and social commerce to deliver differentiated customer experiences, driving both engagement and conversion.

Lipstick Industry Leaders

-

L’Oréal Group

-

Estée Lauder Companies

-

Coty Inc.

-

LVMH

-

Revlon Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dior Beauty introduced a limited-edition Rouge Dior lipstick collection to celebrate Lunar New Year 2026. The collection features couture-inspired cases adorned with Christian Dior’s lucky star motif and gold accents, along with exclusive satin and velvet-finish shades. It combines long-lasting color performance with Dior’s signature floral lip-care formula, presenting the launch as both a premium lipstick release and a collectible beauty product.

- July 2025: JT launched a limited-edition lip kit in partnership with MAC Cosmetics, showcasing her preferred lip color combination. Priced at USD 52, the collection includes MAC's Lip Pencil in Chestnut, a matte lipstick in Snob (a neutral pink shade), and a clear lip gloss. The kit is packaged in a MAC-branded carrying case for convenient storage.

- October 2024: Celine introduced its first makeup product, a red lipstick featuring a powdery rose fragrance inspired by 1970s perfumes. The scent includes the signature powdery notes from the Celine Haute Parfumerie fragrance collection. The lipstick formula is enriched with squalane for lip conditioning and offers long-lasting wear with a satin finish in a classic red hue.

- September 2024: MAC Cosmetics introduced MACximal, an updated version of its signature satin lipstick. The reformulated product offers enhanced pigmentation, a satin finish, and a hydrating formula designed for a creamy texture and smooth application. MACximal is available in various shades, including Blankety (soft beige-pink), Espresso Yourself (blackened orange), Creme d'Nude (pale peachy beige), Film Noir (deep cool brown), Violet Vapour (electric violet), Tilted Denim (pale dusty blue), and In the Clear, a transparent lip balm providing eight-hour hydration that can also be used as a topcoat.

Global Lipstick Market Report Scope

| Matte |

| Satin/Cream |

| Gloss |

| Others |

| Stick |

| Liquid |

| Crayon |

| Palette |

| Mass |

| Premium and Luxury |

| Conventional |

| Clean Label |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Finish | Matte | |

| Satin/Cream | ||

| Gloss | ||

| Others | ||

| By Form | Stick | |

| Liquid | ||

| Crayon | ||

| Palette | ||

| By Price Range | Mass | |

| Premium and Luxury | ||

| By Ingredient Type | Conventional | |

| Clean Label | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the lipstick market?

The lipstick market is valued at USD 20.11 billion in 2026.

Which finish category is growing fastest through 2031?

Matte finishes are projected to grow at a 7.59% CAGR, the fastest among all finishes.

How quickly will online sales expand?

Online retail is forecast to post a 9.07% CAGR between 2026 and 2031, the highest among all channels.

Which region will account for the largest incremental revenue?

Asia-Pacific is expected to add the most revenue, growing at an 8.01% CAGR to 2031.

Page last updated on: