Hair Dryer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

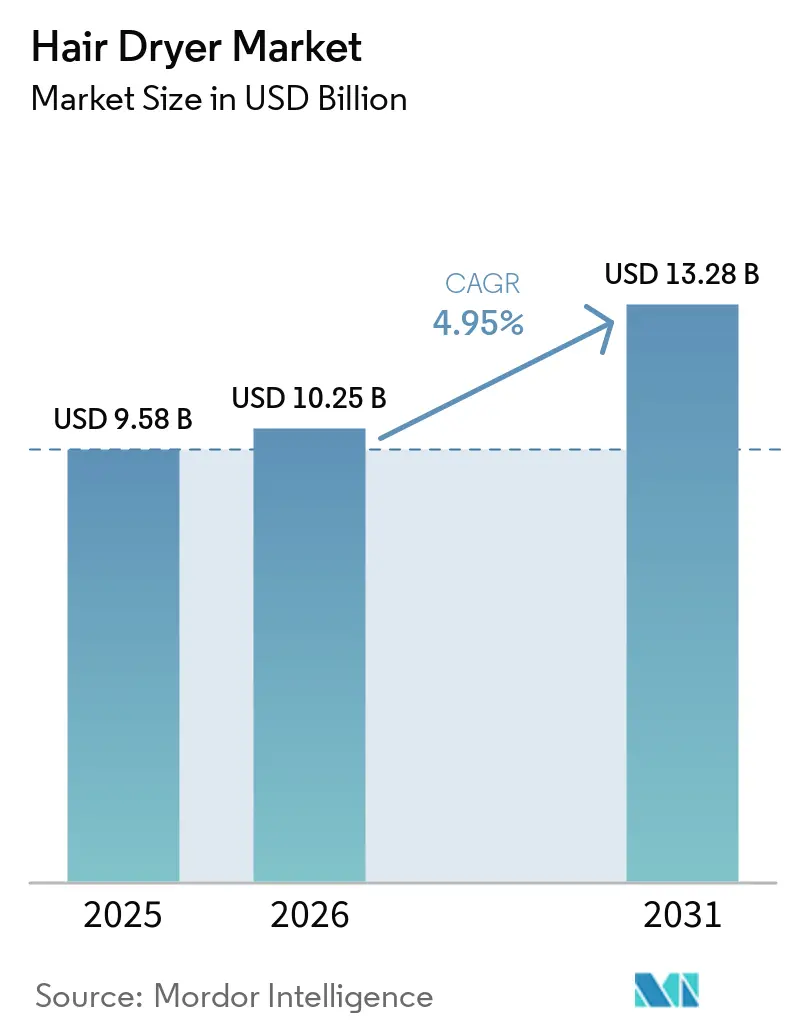

| Market Size (2026) | USD 10.25 Billion |

| Market Size (2031) | USD 13.28 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hair Dryer Market Analysis by Mordor Intelligence

The hair dryer market size is expected to increase from USD 9.58 billion in 2025 to USD 10.25 billion in 2026 and reach USD 13.28 billion by 2031, growing at a CAGR of 4.95% over 2026-2031. The shift in consumer preferences toward premium features is driving demand in the hair dryer market for advanced technologies, such as sensor-driven temperature controls and app-based personalization, which offer greater value compared to traditional wattage upgrades. In the hair dryer market, the Asia-Pacific region, rising disposable incomes, and the adoption of urban lifestyles are fueling demand for salon-quality styling solutions for home use. Additionally, advancements in lithium-ion battery technology in the hair dryer industry are accelerating the adoption of cordless hair dryers, while energy-efficient brushless motors are addressing the European Union's increasingly stringent eco-design regulations. Furthermore, in the hair dryer market, the rise in counterfeit product seizures and product recalls has heightened the emphasis on trusted brands that can ensure safety and compliance with regulatory standards.

Key Report Takeaways

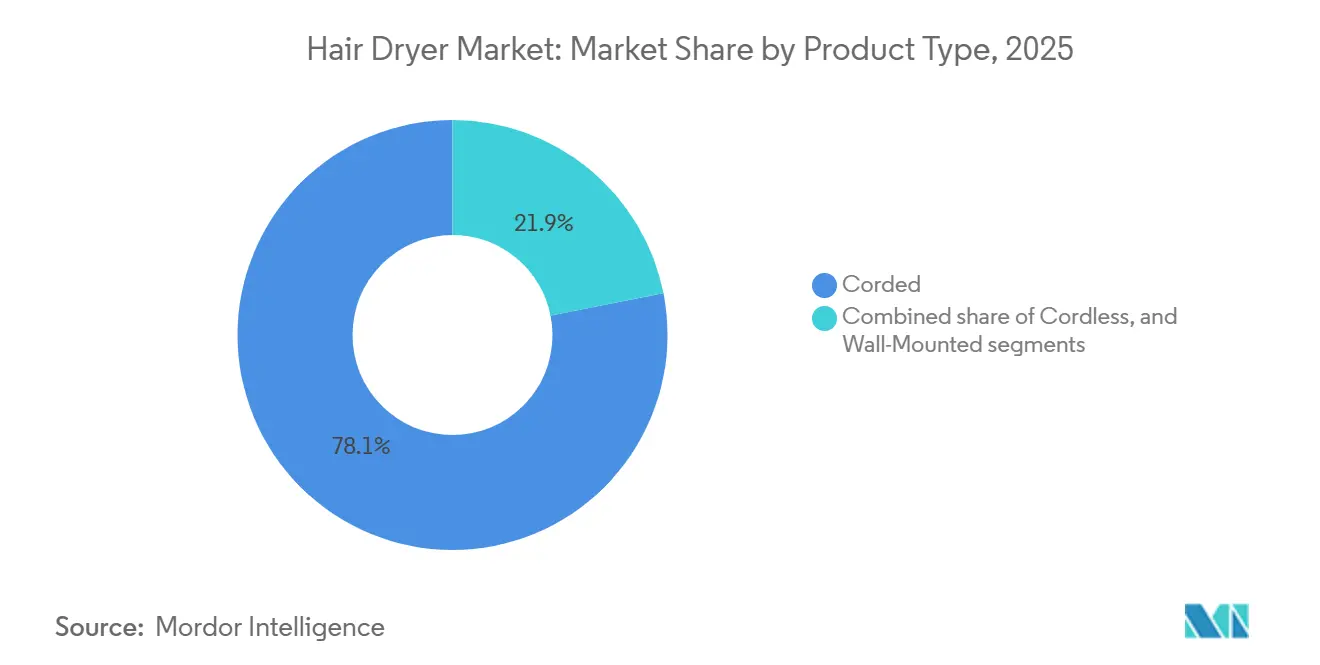

- By product type, corded units led the hair dryer market with 78.11% revenue share in 2025, whereas cordless models are projected to post a 6.12% CAGR through 2031.

- By application, individual households accounted for 65.81% of the hair dryer market size in 2025, while professional salons are forecast to expand at a 6.68% CAGR over 2026-2031.

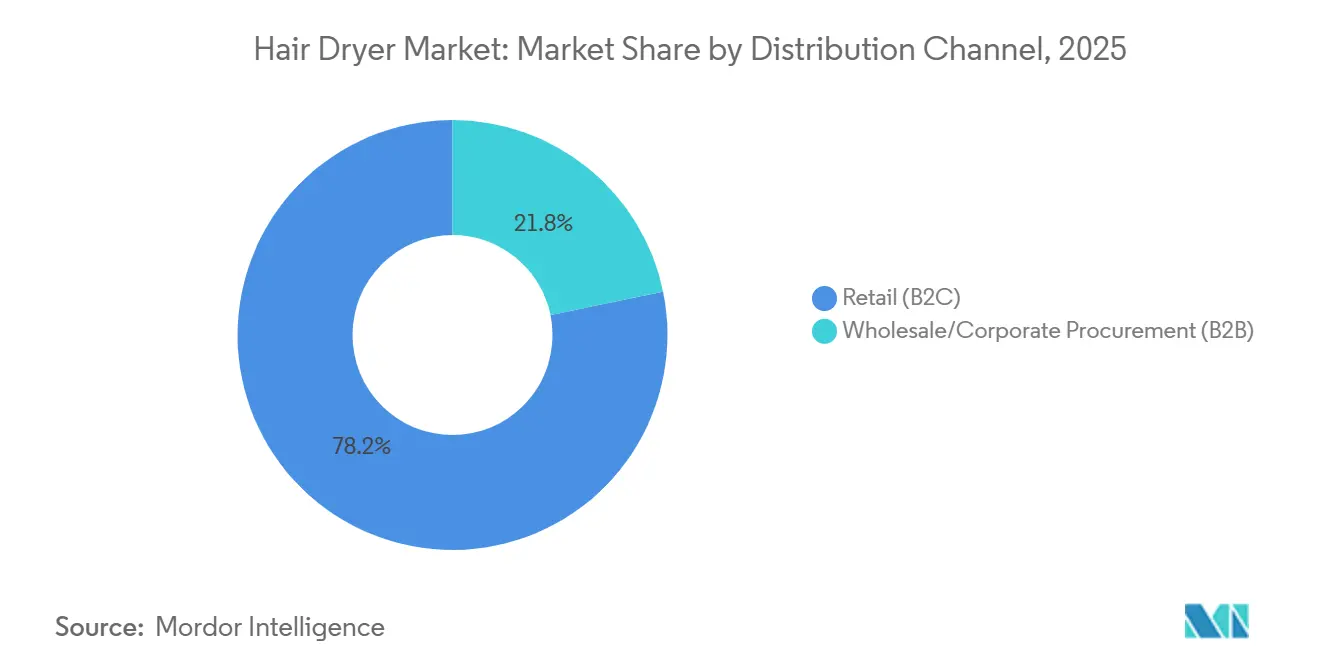

- By distribution channel, retail captured 78.22% of the hair dryer market size in 2025 and is expected to grow at a 7.08% CAGR through 2031.

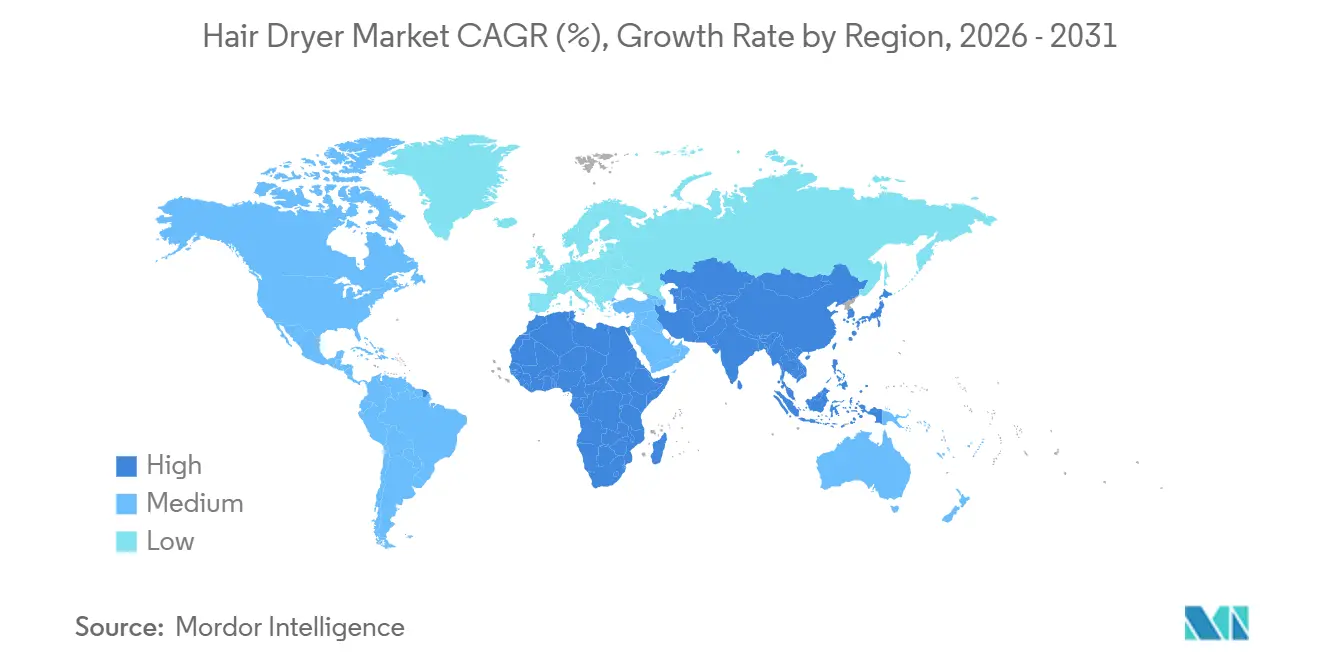

- By geography, Asia-Pacific contributed 38.59% revenue share in 2025 and is set to advance at a 5.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Dryer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart And Customizable Features In Hair Dryers | +0.8% | Global, with early adoption in North America, Europe, and urban Asia-Pacific (China, Japan, South Korea) | Medium term (2–4 years) |

| Rapid Innovation In Hair Dryer Technology | +0.9% | Global, led by Japan, South Korea, and Western Europe; spillover to emerging APAC markets | Long term (≥4 years) |

| Social Media And Influencer Endorsements | +0.6% | Global, particularly North America, Europe, and urban Asia-Pacific; strong penetration in India and Southeast Asia | Short term (≤2 years) |

| Professional And Salon-Grade Product Adoption At Home | +0.7% | North America, Europe, and APAC core (China, India, Japan, Australia); emerging in Middle East | Medium term (2–4 years) |

| Product Differentiation And Brand Competition | +0.5% | Global, with intense rivalry in North America, Europe, and China | Long term (≥4 years) |

| Focus On Hair Health And Damage Prevention | +0.6% | Global, with premium-segment concentration in North America, Europe, Japan, and Australia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Smart and Customizable Features in Hair Dryers

Sensor-driven thermal management and app connectivity are redefining consumer expectations in the hair dryer market, particularly among millennial and Gen-Z buyers who prioritize personalized styling routines. Dreame's 2026 Pilot model integrates AI-powered sensors that detect hair moisture levels and adjust heat output in real time, while Tineco's MODA ONE employs iLoop proximity sensors to modulate airflow based on distance from the scalp. Dyson's Supersonic r, launched in March 2025, uses RFID chips embedded in magnetic attachments to automatically configure temperature and speed profiles, eliminating manual adjustments and reducing user error that can cause heat damage. These features in the hair dryer market command price premiums of 40% to 60% over conventional models, yet adoption accelerates as consumers recognize long-term hair-health benefits and reduced styling time. The shift in the hair dryer industry mirrors broader smart-home integration trends, with manufacturers exploring voice-assistant compatibility and cloud-based styling recommendations derived from aggregated usage data.

Rapid Innovation in Hair Dryer Technology

In the hair dryer market, brushless DC motors operating at 150,000 RPM and ceramic heating elements incorporating carbon-nanotube additives represent the current frontier in thermal efficiency and durability. Philips India's BLDC 8000 Series, released in June 2025, consumes 50% less energy than legacy 2,300-watt AC-motor units while maintaining equivalent drying speed, addressing both cost-of-ownership and environmental concerns. L'Oréal's January 2024 investment in Zuvi via its BOLD venture fund enabled co-development of the AirLight Pro, which employs infrared LightCare technology and 150-plus patents to reduce energy consumption by 31% compared to conventional dryers. A February 2026 study published in Molecules demonstrated that thermoresponsive organic silicon-modified keratin coatings can prevent heat-induced protein denaturation, suggesting that material science will increasingly complement electrical engineering in next-generation product design. Patent filings in the hair dryer industry for thermal-control methods and CNT-based heating elements surged in 2024 and 2025, indicating sustained R&D investment by incumbents and challengers alike.

Social Media and Influencer Endorsements

In the hair dryer market, TikTok and Instagram have become primary discovery channels, with viral product demonstrations generating measurable sales uplift within 48 to 72 hours of posting. Dyson's Corrale campaign achieved over 1 million impressions and a 17.25% engagement rate, while T3 Micro's Aire IQ launch generated USD 10.5 million in earned media value and 22 million earned impressions, including two viral TikTok videos that each surpassed 5 million views. The Revlon One-Step accumulated 42.4 million TikTok views, and Dyson's Airwrap reached 3.6 billion views, demonstrating that influencer-driven content can eclipse traditional advertising in reach and conversion efficiency. Brands in the hair dryer market increasingly structure launch timelines around influencer partnerships, seeding products with micro-influencers (10,000 to 100,000 followers) 4 to 6 weeks before retail availability to build anticipation and user-generated content libraries. This dynamic favors agile brands that can iterate packaging, messaging, and feature sets based on real-time social feedback, compressing product-development cycles and enabling rapid pivots when initial positioning underperforms.

Professional and Salon-Grade Product Adoption at Home

In the hair dryer market, salon professionals' endorsement of specific models, often driven by ergonomic design, motor longevity, and consistent thermal output, creates a halo effect that influences household buyers seeking to replicate salon results. Panasonic's November 2025 ELMISTA Beautifying Hair Dryer, developed jointly with Milbon for salon-exclusive distribution in Japan, atomizes beauty serums during drying to repair damaged hair, effectively merging treatment and styling in a single appliance. Dyson's Supersonic, initially marketed to professional stylists, transitioned to consumer channels and now commands a USD 400 to USD 600 retail price, demonstrating that pro-grade positioning can sustain premium pricing in household segments. Salons' procurement cycles, typically replacing equipment every 18 to 24 months due to heavy daily use, also drive volume demand for brushless-motor units rated for 10,000-plus hours of operation, as seen in Valera's Hotello BLDC model deployed in high-traffic hospitality environments. This cross-pollination between professional and consumer segments accelerates technology diffusion and elevates baseline performance expectations across price tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Products Flooding Distribution Channels | -0.4% | Global, with acute issues in Asia-Pacific (China, India, Southeast Asia), Middle East, and online marketplaces | Short term (≤2 years) |

| Product Recalls And Quality Assurance Challenges | -0.3% | Global, particularly North America (CPSC jurisdiction) and Europe (CE compliance) | Short term (≤2 years) |

| Safety Concerns And Risk Of Hair Or Skin Damage | -0.3% | Global, with heightened regulatory focus in North America, Europe, and Australia | Medium term (2–4 years) |

| Environmental Concerns Over Energy Consumption And E-Waste | -0.2% | Europe (WEEE, Ecodesign), North America (DOE), and Asia-Pacific (China, Japan environmental mandates) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Flooding Distribution Channels

In the hair dryer market, fake units that replicate premium-brand aesthetics but omit safety features and performance technologies erode brand equity and expose consumers to electrocution and fire hazards. U.S. Customs and Border Protection seized 60 counterfeit hair dryers from China in 2024, while Thailand customs confiscated over 30,000 unsafe units in March 2026 following a child electrocution incident that prompted nationwide enforcement sweeps[1]Source: U.S. Customs and Border Protection, “CBP Seizes Unsafe Hair Dryers,” cbp.gov. The UK's Port of Felixstowe intercepted 500 counterfeit Dyson dryers in 2025, with testing revealing substandard wiring and missing thermal cutoffs that posed electric shock and fire risks[2]Source: Office for Product Safety and Standards, “Safety Alert: Counterfeit Hair Styling Devices,” gov.uk. Online marketplaces in the hair dryer industry amplify the problem: the CPSC issued warnings in 2025 for hair dryers sold on DHGate.com and Wish.com that lacked immersion-protection devices, yet these platforms' decentralized seller networks complicate enforcement. Legitimate manufacturers invest in holographic labels, QR-code authentication, and blockchain-based provenance tracking, but counterfeiters rapidly adapt, creating an arms race that diverts R&D resources and increases cost of goods sold by an estimated 3% to 5% for premium brands.

Product Recalls and Quality-Assurance Challenges

The hair dryer market witnessed multiple recalls issued by the CPSC in 2025 and 2026, totaling over 57,000 units, primarily due to missing immersion-protection devices that violate UL 859 standards for household electric personal grooming appliances. McLee Creations recalled 740 units in February 2025, Legend Brands recalled 500 units in March 2025, Empower Brands/Remington recalled 56,300 units in June 2025, and AliExpress recalled 80 units in January 2026, all citing electrocution hazards when devices contact water. These incidents in the hair dryer industry highlight supply-chain fragmentation, where third-party manufacturers in China and Southeast Asia may lack familiarity with North American and European safety standards, particularly IEC 60335-2-23 for household and similar electrical appliances. Indonesia mandated SNI IEC 60335-2-23:2010 compliance in October 2025, requiring importers and domestic manufacturers to obtain certification before sale, which temporarily disrupted distribution as non-compliant inventory was withdrawn[3]Source: Indonesia Ministry of Trade, “SNI Certification,” kemendag.go.id. Recalls damage retailer relationships, trigger class-action litigation, and necessitate costly reverse-logistics operations, with estimated per-unit recall costs ranging from USD 15 to USD 30 when factoring in legal fees, customer refunds, and brand-reputation remediation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cordless Units Challenge Corded Dominance

In 2025, corded dryers led the global hair dryer market with 78.11% of the share, reflecting consumer preference for unlimited runtime and consistent power. However, cordless models in the hair dryer market are set to grow at a 6.12% CAGR through 2031, driven by advancements in lithium-ion battery energy density and increasing demand for portability. Zuvi's Halo Cordless, priced at USD 499, features a 44-watt-hour battery with 27 minutes of runtime and a 90% recharge in 19 minutes, showcasing how premium cordless models can rival high-end corded units when battery performance meets professional standards. Volo's cordless model, operating at 600 watts compared to the typical 1,800-watt corded unit, targets travelers and multi-user households. Retailing at AUD 500 to AUD 600 (approximately USD 330 to USD 395), it appeals to those prioritizing convenience over airflow. Wall-mounted dryers, common in hospitality and healthcare, maintain a stable niche. Valera's Hotello BLDC model, rated at 1,500 watts with IP34 splash protection and a 10,000-hour brushless motor, is ideal for high-traffic areas requiring theft-resistant installation and low maintenance.

Corded units in the hair dryer industry benefit from established supply chains, lower material costs, and consumer familiarity but face challenges from energy-efficiency mandates and the inconvenience of tethered operation in small bathrooms. Cordless adoption is rising in Asia-Pacific urban centers, where compact living spaces and frequent travel drive demand for portable appliances. Battery technology remains a key factor. Current lithium-ion cells, delivering 150 to 200 watt-hours per kilogram, limit runtime to 20–30 minutes at full power. However, solid-state batteries under development by automotive and consumer-electronics firms could exceed 300 watt-hours per kilogram by 2028, enabling 45–60 minutes of operation and addressing a major drawback of cordless models. Wall-mounted units, though a smaller segment, remain resilient in commercial settings due to their durability and vandal-resistant design. DERBAL's luxury wall-mounted model, with a 21,000 RPM DC motor and 50,000-hour service life, has been installed in over 800 rooms at Mandarin Oriental Doha, requiring only two replacements and highlighting its cost-efficiency in institutional use.

By Application/End User: Professional Segment Drives Premium Adoption

In 2025, individual households in the hair dryer market accounted for 65.81% of end-use demand. From 2025 to 2031, professional salons in the hair dryer market and barber shops are expected to grow at a 6.68% CAGR, driven by stylists upgrading to brushless-motor units with 150,000 RPM and extended service intervals from 12 to 24 months. Panasonic's ELMISTA Beautifying Hair Dryer, launched in November 2025 and co-developed with Milbon for Japanese salons, atomizes beauty serums during use, combining treatment and styling to enable salons to offer premium-priced services. Dyson's Supersonic, initially targeted at professional stylists, transitioned to consumer markets, retailing at USD 400 to USD 600. This demonstrates how pro-grade products can sustain premium pricing in household markets, with salon endorsements enhancing credibility. Commercial buyers, such as hotels, hospitals, and gyms, prioritize durability and energy efficiency. Valera's Hotello BLDC, with a 1,500-watt brushless motor and IP34 splash protection, meets these needs and has reduced maintenance calls by 92% in luxury venues like Six Senses Fiji.

Household buyers increasingly seek salon-quality results, influenced by social media tutorials and the high cost of salon visits. Philips India's BLDC 8000 Series, priced at INR 19,995 (around USD 240), addresses this demand by delivering 200 million ions and using 50% less energy than older models, offering both performance and cost savings. Professional salons, with 18 to 24-month procurement cycles due to heavy use, prefer units rated for over 10,000 hours of operation, emphasizing motor longevity and consistent thermal output over aesthetics. Commercial buyers, valuing energy efficiency and low maintenance, show higher price tolerance. DERBAL's luxury wall-mounted model, consuming 40% less energy than AC-motor units and offering a 50,000-hour motor life, has been adopted by high-traffic venues like the Ritz-Carlton and Emirates First Class Lounge Dubai, justifying its premium pricing.

By Distribution Channel: Retail B2C Maintains Omnichannel Leadership

In 2025, retail channels in the hair dryer market accounted for 78.22% of distribution and are projected to grow at a 7.08% CAGR through 2031, driven by online platforms enabling direct-to-consumer launches, influencer-led discoveries, and quick customer feedback integration. L'Oréal's November 2024 launch of the AirLight Pro via Ulta's e-commerce platform and 1,385 stores highlights how omnichannel strategies speed up market entry for co-developed innovations, allowing brands to test messaging and pricing digitally before full retail rollout. Specialty beauty retailers like Sephora, Ulta, and Nordstrom provide curated platforms where in-store demos and trained staff enhance credibility for premium-priced products. For example, Panasonic Australia's November 2024 launch of the EH-NA0J at AUD 499 (around USD 330) used these channels to promote its nanoe MOISTURE+ technology, distinguishing it from cheaper alternatives. Supermarkets and hypermarkets remain relevant for budget products driven by impulse buys and brand familiarity, but are growing more slowly as consumers shift online for price comparisons and niche brands.

Wholesale and B2B procurement in the hair dryer industry, comprising the rest of the distribution, serves commercial buyers like hotels, salons, and hospitals, focusing on bulk pricing, extended warranties, and technical support. Europages, a B2B directory, lists 187 suppliers offering 91 hair dryer products across Europe, with minimum order quantities of 500 to 5,000 units and prices ranging from USD 15 to USD 30, reflecting the commoditized nature of mid-tier commercial models. Hangzhou-based Creade targeted hotel and hospitality buyers in the Middle East and Asia-Pacific through trade shows in Dubai (December 2024), Singapore (October 2025), and Riyadh (2025). However, online retail growth brings challenges like counterfeit listings on Amazon and AliExpress, which harm brand equity, and higher return rates for online purchases (15%-20%) compared to physical retail (5%-8%), increasing reverse-logistics costs and inventory write-offs. Dyson's direct-to-consumer strategy, offering best-price guarantees and extended trial periods, aims to recover margins lost to third-party retailers while building direct customer relationships for subscription services and accessory upsells.

Geography Analysis

In the hair dryer market, Asia-Pacific, contributing 38.59% of global revenue in 2025, is projected to grow at a 5.58% CAGR through 2031, driven by rising incomes, urbanization, and increased adoption of premium salon-grade devices at home. Philips India launched the BLDC 8000 Series in June 2025 at INR 19,995 (around USD 240), offering 200 million ions and 50% energy savings over older 2,300-watt models, aligning with the premiumization trend. China remains a manufacturing hub in the hair dryer industry, with Guangzhou Fenghe operating a 12,000-square-meter facility employing over 100 workers and exporting to 60+ countries, while Foshan Hanyi has a 100,000-unit annual capacity. Panasonic Malaysia's May 2024 launch of the nanocare EH-NA0J, delivering 18 times more moisture than earlier nanoe models, highlights how Japanese and South Korean manufacturers use proprietary patents to compete against lower-cost Chinese brands. Indonesia's October 2025 enforcement of SNI IEC 60335-2-23:2010 compliance disrupted distribution temporarily but raised safety standards by requiring certification for all importers and manufacturers.

Demand in the hair dryer market across North America and Europe, is driven by replacements and feature upgrades rather than first-time purchases. L'Oréal's November 2024 launch of the AirLight Pro via Ulta's e-commerce platform and 1,385 stores demonstrates how omnichannel strategies accelerate market entry. The EU's WEEE Directive 2012/19/EU mandates a 65% collection target for small appliances, while the UK's updated WEEE Regulations 2013 (2025) increase compliance costs but create opportunities for brands adopting circular-economy principles. In 2025 and 2026, the CPSC recalled over 57,000 units due to missing immersion-protection devices, reflecting strict regulations favoring brands with strong quality assurance. Dyson's direct-to-consumer strategy in North America, offering best-price guarantees and extended trials, aims to recover margins lost to third-party retailers while fostering customer relationships for subscriptions and accessory sales.

In the hair dryer market, South America, the Middle East, and Africa, though smaller markets, are growing, with hospitality and commercial procurement leading adoption before household penetration. Created targeted Middle Eastern hospitality buyers at trade shows in Dubai (December 2024) and Riyadh (2025). Brazil's Kenby Hotelaria supplies 1,600 to 1,800-watt models to hotels, reflecting demand for durable, energy-efficient units. Panasonic's May 2025 launch of the EH-NA9N and EH-NA7M models with nanoe and mineral-ion technology in the Middle East and Africa highlights the region's potential, driven by rising incomes and westernized beauty standards. Thailand's March 2026 crackdown on counterfeit and unsafe dryers, following a child electrocution incident, underscores stricter enforcement in emerging markets, addressing long-standing safety concerns.

Competitive Landscape

Five key players dominate the hair dryer market, Dyson, Panasonic, Philips, Conair, and Spectrum Brands (Remington), leveraging their brand equity, patent portfolios, and extensive distribution networks. However, the mid-tier and budget segments remain fragmented, with Chinese manufacturers capitalizing on cost-efficient production and rapid SKU iterations. Henkel's March 2026 acquisition of OLAPLEX for USD 1.4 billion highlights a growing trend where beauty-care leaders view hair-appliance portfolios as strategic complements to treatment products. This development could reshape competitive dynamics by integrating formulation expertise with hardware R&D, as reported by Reuters. Similarly, Coty's USD 511 million acquisition of GHD and Helen of Troy's January 2020 purchase of Drybar for USD 255 million, both supported by private equity, reflect a focus on consolidating premium lifestyle brands with loyal customer bases and strong international growth potential.

L'Oréal's January 2024 investment in Zuvi, through its BOLD venture fund, exemplifies another approach. Their collaboration on the AirLight Pro, featuring infrared LightCare technology and over 150 patents, demonstrates how industry leaders are using corporate venture capital to access disruptive technologies and accelerate product development timelines. White-space opportunities include cordless models with extended runtimes of 45 to 60 minutes, enabled by the solid-state batteries currently under development. Additionally, appliances integrating hair-health diagnostics—using spectroscopy or moisture sensors- present opportunities for subscription revenue streams through consumable serums and personalized treatment recommendations. Emerging disruptors like Zuvi, Dreame, and Tineco differentiate themselves from legacy brands by focusing on sensor-driven automation and app connectivity.

Meanwhile, Chinese manufacturers such as Xiaomi (MIJIA) and Laifen employ aggressive pricing strategies and rapid feature iterations to capture market share in the Asia-Pacific region and online channels. A rise in patent filings for thermal-control methods and CNT-based heating elements in 2024 and 2025 indicates sustained R&D efforts by both established players and challengers. However, the absence of a dominant standards body, similar to the Bluetooth SIG or Wi-Fi Alliance, limits interoperability, often locking consumers into proprietary ecosystems when purchasing smart-connected models. VGR's July 2025 announcement of a 35% capacity expansion, including new automated assembly lines and advanced blade-production machinery, highlights the scaling efforts of mid-tier suppliers. These suppliers are addressing rising global demand while maintaining international quality standards.

Hair Dryer Industry Leaders

Remington (Spectrum Brands Holdings Inc.)

Conair Corp.

Dyson

Philips (Koninklijke Philips N.V.)

Panasonic Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dyson launched the Airwrap Coanda 2x in South Korea, featuring the most powerful motor in the company's history and AI-based temperature control sensors, priced at 879,000 won (USD 608) to expand premium market presence despite economic headwinds and competitive pressure from cost-effective alternatives.

- March 2025: Dyson released the Supersonic r hair dryer to general consumers in the United States and Europe, previously available only to professional stylists, featuring 30% size reduction and 20% weight decrease compared to its predecessor while maintaining professional-grade performance capabilities.

- September 2024: L'Oréal announced plans to double its Brazilian revenue by 2027, emphasizing hair care products and digital sales expansion in response to the Brazilian beauty market's 12.7% growth, with social media influencers playing crucial roles in product visibility and consumer engagement.

- August 2024: Panasonic launched high-tech blow dryers in Southeast Asia featuring moisture-balancing technology, competing with Dyson and Chinese brands through social media influencer partnerships and climate-adapted product specifications designed for tropical conditions.

Global Hair Dryer Market Report Scope

| Corded |

| Cordless |

| Wall-Mounted |

| Individual/Household |

| Professional (Salon And Barber Shops) |

| Commercial (Hotel/Institutional) |

| Wholesale/Corporate Procurement (B2B) | |

| Retail (B2C) | Supermarkets And Hypermarkets |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Corded | |

| Cordless | ||

| Wall-Mounted | ||

| By Application/End User | Individual/Household | |

| Professional (Salon And Barber Shops) | ||

| Commercial (Hotel/Institutional) | ||

| By Distribution Channel | Wholesale/Corporate Procurement (B2B) | |

| Retail (B2C) | Supermarkets And Hypermarkets | |

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for hair dryers be by 2031?

The hair dryer market size is forecast to reach USD 13.28 billion by 2031, reflecting a 4.95% CAGR from 2026 to 2031.

Which region contributes the most revenue today?

Asia-Pacific generated 38.59% of global sales in 2025 and is projected to retain leadership thanks to rising disposable income and premiumization.

Which product segment is growing fastest?

Cordless models are expected to post the highest growth, expanding at a 6.12% CAGR as battery energy density improves and portability gains priority.

What are the main regulatory risks that brands face?

Counterfeit products, safety recalls tied to missing immersion-protection devices, and upcoming EU energy-efficiency mandates are the chief compliance challenges.

Page last updated on: