Facial Cleansers And Toners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

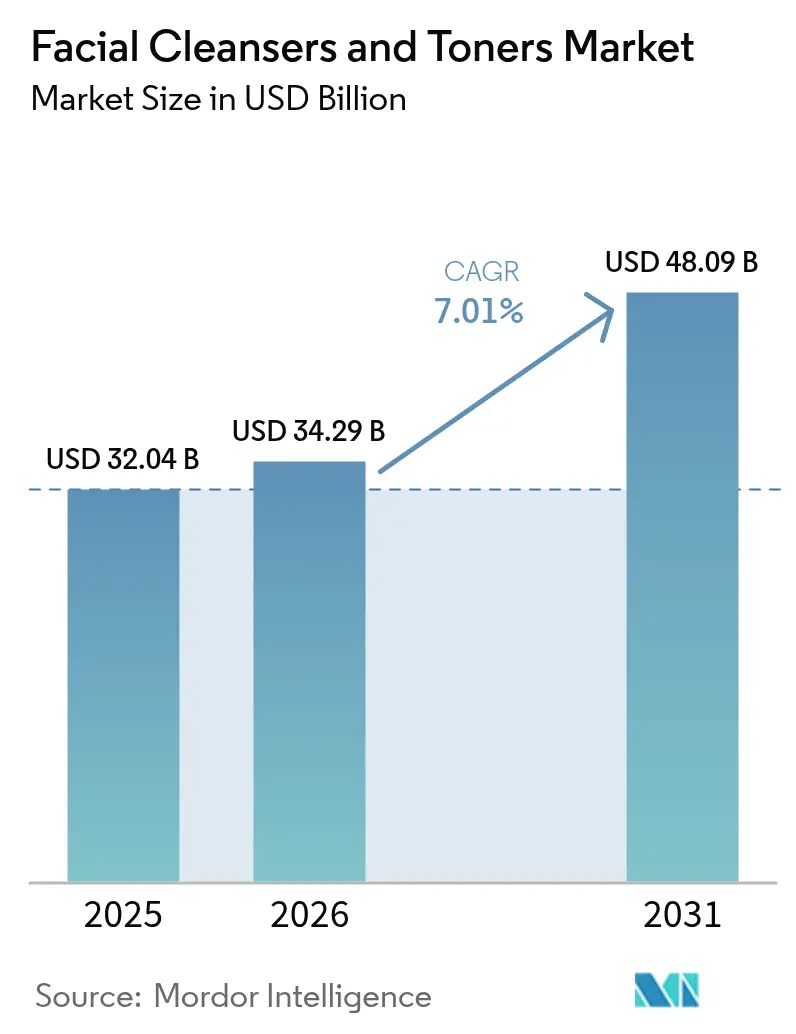

| Market Size (2026) | USD 34.29 Billion |

| Market Size (2031) | USD 48.09 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

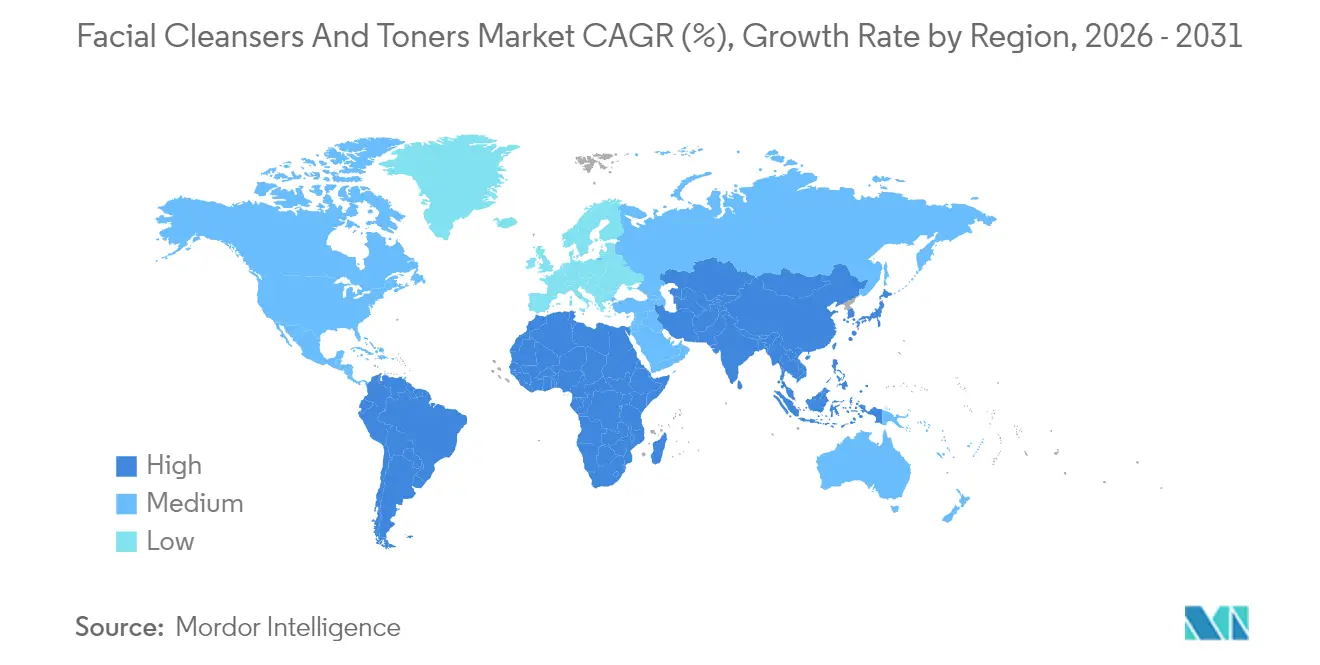

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

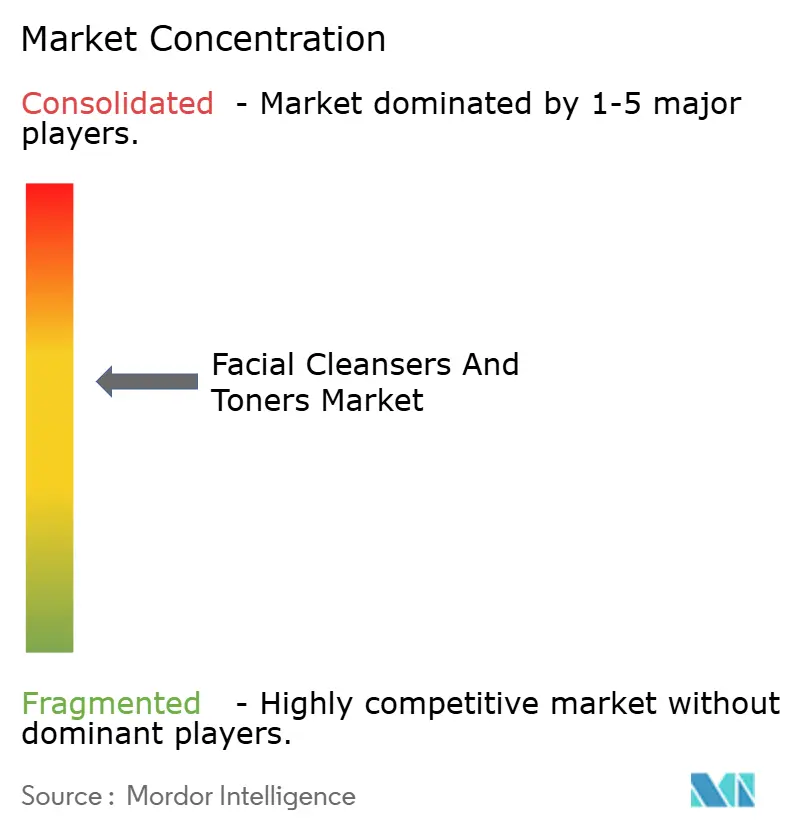

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Facial Cleansers And Toners Market Analysis by Mordor Intelligence

The facial cleansers and toners market size was valued at USD 32.04 billion in 2025 and estimated to grow from USD 34.29 billion in 2026 to reach USD 48.09 billion by 2031, at a CAGR of 7.01% during the forecast period (2026-2031). This growth reflects a shift in skincare habits, with daily cleansing and toning increasingly viewed as essential preventive care rather than optional cosmetic practices, particularly among Gen Z and Millennials. Brands are expanding their offerings to include microbiome-friendly ingredients, refillable packaging, and AI-driven skin diagnostics that enable personalized skincare solutions. Additionally, regulatory requirements for full ingredient transparency are fostering greater consumer trust. The competitive landscape is intensifying as multinational corporations compete with digital-native brands that leverage shorter product development cycles and social commerce trends. The market's long-term growth is supported by strong demand in the Asia-Pacific region, a rise in premium product offerings, and the increasing adoption of direct-to-consumer channels.

Key Report Takeaways

- By product type, cleansers led with 71.62% revenue share in 2025, whereas toners are projected to record the fastest 7.79% CAGR to 2031.

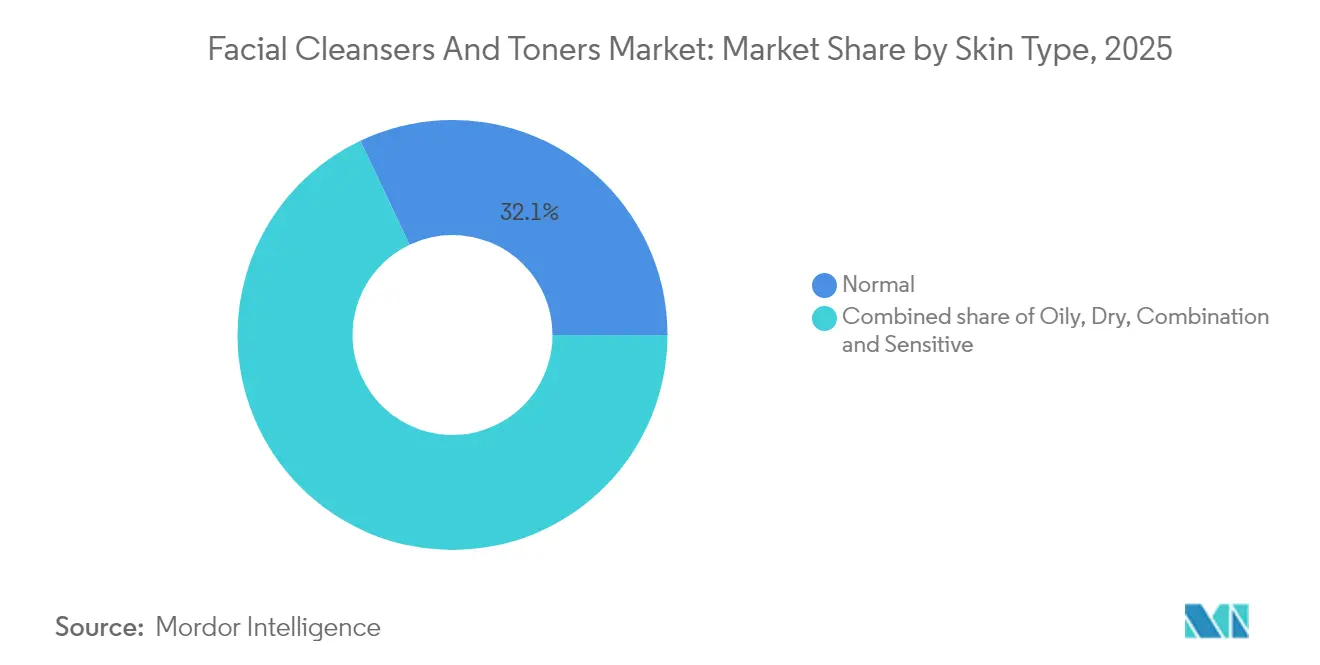

- By skin type, normal-skin formulations accounted for 32.05% of 2025 revenue, while sensitive-skin products are poised to expand at 9.12% CAGR through 2031.

- By price range, the mass tier commanded 62.58% share in 2025; premium lines will advance at a robust 8.96% CAGR to 2031.

- By category, conventional products held 61.88% share in 2025, while natural and organic variants are set to grow at 8.02% CAGR.

- By distribution channel, supermarkets captured 38.74% of 2025 sales, yet online platforms are projected to register an 8.38% CAGR by 2031.

- By geography, Asia-Pacific dominated with 36.12% 2025 revenue and is forecast to progress at a vigorous 9.1% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Facial Cleansers And Toners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness of skincare routines | +1.8% | Global, with strongest uptake in Asia-Pacific and North America | Medium term (2-4 years) |

| Demand for natural and organic formulations | +1.5% | Europe and North America core, expanding to urban Asia-Pacific | Long term (≥ 4 years) |

| Influence of social media and influencers | +1.3% | Global, particularly Gen Z and Millennial cohorts across all regions | Short term (≤ 2 years) |

| Shift toward clean beauty products | +1.2% | North America and EU regulatory-driven, spillover to APAC | Medium term (2-4 years) |

| Increasing male grooming adoption | +0.9% | Asia-Pacific, Middle East, and urban centers in Europe and North America | Long term (≥ 4 years) |

| Popularity of multifunctional products | +0.7% | Global, with early adoption in Asia-Pacific and premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Awareness of Skincare Routines

Dermatological education campaigns and telemedicine consultations have promoted the adoption of multi-step skincare regimens, transforming cleansing and toning from occasional practices into consistent, twice-daily routines. A 2024 study published in the Journal of Cosmetic Dermatology revealed that 68% of participants following a structured facial cleansing routine experienced improved skin barrier function and reduced transepidermal water loss within eight weeks, supporting the clinical benefits of routine skincare[1]Journal of Cosmetic Dermatology. "Adherence to Facial Cleansing Routine and Skin Barrier Function.", onlinelibrary.wiley.com. This evidence-based approach has enabled brands to position cleansers and toners as tools for preventive dermatology rather than mere cosmetic products. Social media platforms have further reinforced this trend, with TikTok's #SkinTok hashtag featuring dermatologists and aestheticians sharing tutorials that clarify ingredient lists and application methods. The growing professionalization of skincare discussions has enhanced consumer knowledge, prompting brands to prioritize clinical trials and transparent labeling to address increased consumer scrutiny.

Demand for Natural and Organic Formulations

Regulatory frameworks are speeding up the shift to clean beauty. The EU Cosmetics Regulation (EC) No 1223/2009 has banned over 1,600 substances and will require allergen disclosure for 26 fragrance compounds starting in 2024[2]European Commission. "Cosmetics Legislation - Growth.", ec.europa.eu. These regulations have encouraged brands to reformulate their products using plant-based surfactants like coco-glucoside and decyl glucoside, which meet biodegradability standards under ISO 16128 guidelines for natural and organic cosmetic ingredients. COSMOS-certified products, which must contain at least 95% natural-origin ingredients, saw growth in European retail markets in 2024, showing that consumers are willing to pay more for certified products. Transparency in ingredients has become a significant competitive advantage. For example, brands like L'Oréal's La Roche-Posay now share detailed information about ingredient sourcing and environmental impact on their product pages. This meets consumer expectations for traceability, covering not just organic certification but also carbon footprint and water usage data.

Influence of Social Media and Influencers

Influencer partnerships have made the journey from awareness to purchase much faster. A 2024 survey showed that most Gen Z consumers found their current facial cleanser through TikTok or Instagram content. This change has made product discovery more accessible, helping smaller brands gain attention without large advertising budgets. For example, Korean brand ANUA's Heartleaf Pore Control Cleansing Oil received over 500 million TikTok views in 2024, leading to its availability in Ulta Beauty's 1,300 U.S. stores. The influencer economy has also increased awareness about product ingredients, with creators explaining formulation science and questioning marketing claims. This has raised expectations for product performance. As a result, brands now spend 25-35% of their marketing budgets on micro-influencers with dermatology expertise, as their authenticity and knowledge are more effective in driving sales than celebrity endorsements.

Shift Toward Clean Beauty Products

The clean beauty movement has grown to focus on overall sustainability, moving beyond just avoiding certain ingredients. This includes efforts like refillable packaging and carbon-neutral manufacturing. In 2024, Unilever's Dove launched a refillable facial cleanser system that cuts plastic use by 60% per unit, supporting its goal to reduce virgin plastic consumption by half by 2025. Regulatory changes are also advancing. California's Safer Cosmetics Act now requires brands to disclose fragrance ingredients and phthalates. Meanwhile, the European Union's proposed Ecodesign for Sustainable Products Regulation will enforce recyclability and repairability standards for cosmetic packaging by 2026. These regulations are transforming supply chains, with brands adopting post-consumer recycled (PCR) resin and aluminum packaging to meet both legal requirements and consumer demands for environmentally friendly products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory compliances | -0.8% | Global, with highest friction in EU, North America, and China | Long term (≥ 4 years) |

| Rise of counterfeit products | -0.6% | Emerging markets in Asia-Pacific, Middle East, Africa, and Latin America | Medium term (2-4 years) |

| Potential skin irritation and allergic reactions | -0.4% | Global, with heightened awareness in North America and Europe | Short term (≤ 2 years) |

| Consumer skepticism and lack of awareness | -0.3% | Emerging markets and rural areas across all geographies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Regulatory Compliances

Differences in regulations across regions create significant cost challenges for brands. In the United States, the FDA offers voluntary cosmetic registration, while the European Union requires mandatory safety assessments under Regulation (EC) No 1223/2009. In China, changing rules on animal-testing exemptions for imported ordinary cosmetics add further complexity. The EU's 2024 amendments to the Cosmetics Regulation set stricter limits on butylated hydroxytoluene (BHT) at 0.001% in leave-on products and expanded the list of banned nanomaterials. These changes have forced the reformulation of over 200 SKUs in major portfolios. For small and mid-sized brands, compliance costs for toxicological assessments and stability testing can range from USD 50,000 to 100,000 per SKU, creating high barriers to entry. This often benefits multinational companies with dedicated regulatory teams, consolidating their market share. Additionally, regional differences in clean beauty standards add to the complexity. For example, California's Safer Cosmetics Act bans 24 ingredients, while the EU prohibits over 1,600. As a result, brands must create region-specific formulations, increasing inventory complexity and reducing economies of scale.

Rise of Counterfeit Products

Counterfeit facial cleansers present serious health risks, as tests have revealed harmful substances like undeclared corticosteroids, mercury, and bacterial contamination in seized products. In October 2024, Interpol's Operation Pangea XVI confiscated over 1 million counterfeit cosmetic items across 120 countries. These included facial cleansers falsely marketed as premium brands but manufactured in unregulated facilities. In the United States, Customs and Border Protection seized counterfeit cosmetics worth USD 4.2 million during fiscal year 2024, with facial skincare products accounting for 18% of the total[3]U.S. Customs and Border Protection. "Trade Enforcement Statistics FY2024.", cbp.gov. To combat counterfeiting, brands are adopting blockchain-based authentication systems and holographic packaging. However, these measures increase per-unit costs by 5-8%, which affects price-sensitive consumers. The widespread availability of counterfeit products harms consumer trust and lowers their willingness to pay premium prices, especially in regions like Southeast Asia and the Middle East, where enforcement systems are less developed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cleansers Dominate, Toners Accelerate with Active Formulations

Cleansers held 71.62% of the 2025 market share, driven by their broad appeal across different skin types and price ranges. Their dominance highlights their importance as the first step in skincare routines, with dermatologists recommending cleansing twice daily to remove dirt, oil, and makeup that can harm the skin barrier. Oil-based cleansers and micellar waters have become increasingly popular, with products like Bioderma's Sensibio H2O Micellar Water standing out in European pharmacies for its gentle formula that maintains the skin's natural pH. Gel cleansers remain the most popular sub-segment due to their foaming action and perceived ability to deeply clean the skin. However, cream and balm cleansers are gaining attention as more consumers focus on hydration during cleansing. Kenvue's Neutrogena Hydro Boost Gel Cleanser, launched in 2024 with hyaluronic acid, reflects the growing demand for products that clean effectively without causing dryness, addressing common concerns about tightness after cleansing.

The toners market is expected to grow at a CAGR of 7.79% from 2026 to 2031, supported by new formulations that include active ingredients like polyhydroxy acids (PHAs), niacinamide, and fermented extracts. These ingredients provide benefits such as exfoliation, brightening, and hydration. The Korean beauty industry has led this shift, with brands like COSRX and Isntree introducing essence-toners that combine the benefits of toners and serums. These products have gained a strong following, especially on platforms like Reddit's SkincareAddiction forum, which has over 2 million members. In 2024, L'Oréal's La Roche-Posay launched the Effaclar Clarifying Lotion Micro-Exfoliant, featuring lipo-hydroxy acid (LHA) for gentle exfoliation. This product targets acne-prone consumers looking for effective over-the-counter solutions. Additionally, the "7-skin method," where multiple layers of hydrating toner are applied to improve moisture retention, has become popular. Originating in Asia, this trend has spread to Western markets, boosting toner usage and increasing per-capita consumption.

By Skin Type: Normal Skin Leads, Sensitive Formulations Surge on Barrier-Repair Focus

Normal skin products accounted for 32.05% of 2025 revenue, highlighting their broad demographic appeal and suitability as entry-level options for consumers new to structured skincare routines. These products focus on maintaining balance, avoiding aggressive active ingredients or heavy emollients that could disrupt skin homeostasis. They often feature minimalist ingredient lists, incorporating gentle surfactants such as cocamidopropyl betaine and hydrating agents like glycerin. An example is Unilever's Simple Kind to Skin Refreshing Facial Wash, which leads the UK market with a formula free from dyes, artificial perfumes, and harsh irritants.

Sensitive skin products are projected to grow at a 9.12% CAGR through 2031, driven by an increasing prevalence of conditions such as contact dermatitis and rosacea, often linked to environmental stressors and over-exfoliation from popular skincare trends. Brands are addressing these concerns with hypoallergenic formulations that undergo rigorous patch testing and exclude the 26 allergens required for disclosure under EU regulations, such as linalool and limonene found in natural fragrances. Galderma's Cetaphil Gentle Skin Cleanser, reformulated in 2024 with niacinamide and glycerin, earned the National Eczema Association Seal of Acceptance, confirming its suitability for sensitive and compromised skin barriers. Additionally, the "skinimalism" trend, where consumers with reactive skin simplify routines to 3-4 essential products, has increased the demand for gentle cleansers and soothing toners that minimize the risk of inflammation.

By Category: Conventional Leads, Natural/Organic Accelerates on Certification Demand

Conventional products held 61.88% of the 2025 market share, supported by well-established supply chains, extensive clinical testing, and consumer trust in synthetic ingredients like salicylic acid and retinol, which deliver reliable results. These products often use preservatives such as phenoxyethanol and parabens to extend shelf life and prevent microbial growth, addressing safety concerns linked to some natural alternatives with shorter stability. Shiseido's Senka Perfect Whip, a leading product in Japan with over 100 million units sold since its launch, demonstrates the strength of this category. Its rich foam texture and affordable price appeal to Asian consumers who prefer high-foaming cleansers. Conventional brands are also focusing on sustainable packaging and carbon-neutral manufacturing to address environmental concerns. These efforts allow them to improve sustainability without changing their core formulations, ensuring product effectiveness remains intact.

Natural and organic products are expected to grow at a CAGR of 8.02% through 2031, driven by certifications like COSMOS, Ecocert, and USDA Organic, which validate ingredient sourcing and manufacturing practices. In 2024, Natura & Co's Avon launched the Distillery collection, featuring cleansers made with upcycled botanicals and 95% natural-origin ingredients, targeting European consumers who value circular economy principles. However, this segment faces challenges as natural surfactants like decyl glucoside produce less foam compared to synthetic ones. To address this, brands are educating consumers that foam is not necessary for effective cleansing. For example, Weleda's Gentle Cleansing Milk, launched in 2024 with organic almond oil, includes packaging messages explaining that low-foam formulas are gentler on the skin barrier. The natural and organic category is also benefiting from ingredient innovations, such as fermented extracts like galactomyces and bifida, which offer probiotic benefits and attract consumers looking for microbiome-friendly skincare options.

By Distribution Channel: Supermarkets Lead, Online Surges on Personalization Tools

Supermarkets and hypermarkets made up 38.74% of the 2025 distribution, benefiting from high customer traffic, impulse buying, and the convenience of offering a wide range of household and personal care products in one place. Retailers like Walmart and Carrefour dedicate ample shelf space to facial cleansers and toners, often using promotional displays and buy-one-get-one offers to boost sales of mass-market brands. These stores also provide in-store testers and beauty advisors for personalized recommendations. However, the COVID-19 pandemic has reduced the availability of testers, leading to a shift toward sealed packaging and QR codes that connect to virtual try-on tools.

Online retail is expected to grow at a CAGR of 8.38% from 2026 to 2031, driven by direct-to-consumer models that help brands earn higher margins, collect customer data, and use AI-powered skin diagnostics to offer personalized product suggestions. Glossier's digital-first strategy, which generated over 70% of its 2024 revenue through its website, shows how this channel can build customer engagement through user-generated content and social commerce features. E-commerce platforms are also investing in augmented reality tools. For example, L'Oréal's ModiFace technology, available on Amazon and brand websites, lets customers see AI-generated before-and-after skincare results. This has helped reduce return rates and improve sales conversions.

By Price Range: Mass Segment Dominates, Premium Grows on Clinical Validation

Mass-market products held 62.58% of the market share in 2025, driven by their affordability and availability through supermarkets, drugstores, and e-commerce platforms. These brands rely on strong recognition and dermatologist endorsements. For example, CeraVe leads U.S. drugstore facial cleansers with its "developed with dermatologists" positioning and ceramide-based formulations priced under USD 15. Mass brands benefit from economies of scale, enabling investments in clinical testing and celebrity endorsements to boost value without raising prices. Procter & Gamble's Olay Regenerist line, priced at USD 20-30, competes with prestige brands by offering peptides and niacinamide at concentrations similar to luxury products, proving efficacy is not limited to premium tiers.

Premium products are expected to grow at a 8.96% CAGR from 2026 to 2031, driven by consumers seeking high-quality ingredients, sustainable packaging, and personalized formulations priced between USD 40 and USD 150. In 2024, Clinique launched its Smart Clinical Repair Wrinkle Correcting Serum Cleanser at USD 55, combining cleansing with anti-aging peptides for consumers treating skincare as preventive healthcare. The rise of clean luxury also supports this segment, with brands like Coty's Orveda offering bio-fermented ingredients and refillable glass packaging in cleansers priced above USD 100, appealing to eco-conscious high-net-worth buyers. Medical-grade skincare, sold through dermatology clinics, further drives premiumization as brands like SkinCeuticals and SkinMedica use clinical data and professional endorsements to justify higher prices and build trust.

Geography Analysis

Asia-Pacific held 36.12% of the market share in 2025 and is expected to grow at a 9.1% CAGR through 2031. Growth is driven by K-beauty and J-beauty trends focusing on gentle, hydrating ingredients and multi-step routines. South Korea's cosmetics exports reached USD 9.8 billion in 2024, with facial cleansers and toners making up 22% of shipments, showcasing its global impact on skincare. In China, regulatory changes by the NMPA in 2024 reduced time-to-market for imported ordinary cosmetics from 18 months to 6 months, allowing Western brands to launch globally. India's skincare market is growing due to rising incomes and urbanization, with Tier 2 and Tier 3 cities boosting sales through platforms like Nykaa and Amazon. Japan's aging population is driving demand for anti-aging products with collagen and hyaluronic acid. Southeast Asia, led by Indonesia and Thailand, is seeing rapid growth in halal-certified products catering to Muslim consumers.

North America and Europe hold a significant market share, with growth supported by premiumization and clean beauty regulations. In the US, the FDA's 2024 MoCRA law requires facility registration and adverse event reporting, raising safety standards. In Europe, the Green Deal and Circular Economy Action Plan are pushing investments in refillable packaging and biodegradable products. Beiersdorf's Nivea, for example, aims to use 50% recycled plastic in packaging by 2025. Canada's updated Cosmetic Ingredient Hotlist in 2024 banned more phthalates and microplastics, aligning with EU standards and simplifying compliance for brands. Post-Brexit, UK and EU regulatory systems remain mostly aligned, though brands must navigate both REACH systems.

South America, the Middle East, and Africa are high-growth regions, with Brazil, Saudi Arabia, and South Africa as key hubs. Brazil's 2024 ANVISA updates aligned cosmetic regulations with Mercosur standards, easing trade. In the Middle East, rising female workforce participation and economic diversification, including Saudi Arabia's Vision 2030, are boosting local beauty manufacturing. Halal certification is critical, with brands like Wardah and Iba gaining market share through certifications from bodies like IFANCA. In Sub-Saharan Africa, challenges like poor logistics and counterfeit products persist, but mobile commerce is expanding access. For instance, Unilever's partnership with M-Pesa in Kenya enables rural consumers to buy facial cleansers via mobile wallets, bypassing traditional retail barriers.

Competitive Landscape

The facial cleansers and toners market is moderately consolidated, featuring a mix of multinational skincare companies and strong regional brands that shape the competitive landscape. Established players leverage extensive Research and Development capabilities, diverse product portfolios, and endorsements from dermatologists to maintain visibility across both premium and mass-market segments. Key players in the market include the Procter & Gamble Company, L'Oréal S.A., Unilever PLC, Kenvue Inc., and The Estée Lauder Companies Inc. Their market dominance is further supported by broad retail partnerships and robust digital marketing strategies, ensuring consistent consumer engagement.

Technology adoption is playing a critical role in enhancing competitive differentiation. Brands are increasingly utilizing AI-driven skin diagnostics, blockchain-based product authentication, and augmented reality try-on tools to improve consumer engagement and minimize return rates. For instance, Shiseido's Optune system, launched in 2024, employs IoT sensors to measure skin moisture levels and environmental conditions. Based on this data, the system dispenses customized cleanser and moisturizer formulations through a connected device, creating a subscription-based model that fosters recurring revenue and strengthens customer loyalty.

Emerging disruptors, such as Glossier and independent Korean brands, are leveraging community-driven product development. By gathering feedback through social media and iterating formulations based on user input, these brands are able to compress innovation cycles and build strong brand loyalty that extends beyond traditional advertising methods. Additionally, compliance with ISO 22716 (Good Manufacturing Practices for Cosmetics) and ISO 16128 (Guidelines on Technical Definitions and Criteria for Natural and Organic Cosmetic Ingredients) has become a baseline requirement for market entry. Retailers increasingly demand third-party certifications to mitigate liability risks and align with consumer expectations for safety and sustainability.

Facial Cleansers And Toners Industry Leaders

-

The Procter & Gamble Company

-

L'Oréal S.A.

-

Unilever PLC

-

Kenvue Inc

-

The Estée Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Garnier Men has expanded its product line with the launch of its new AcnoFight Gentle Cleanser. According to the brand, the new product is a soap-free, alcohol-free, and paraben-free formula that delivers powerful results without compromising on gentleness.

- June 2025: Kao Corporation launched two new products under the Curél brand, which specializes in skincare for dry, sensitive skin. The products are the Curél Intensive Moisture Care Carbonated Foam Serum and Curél Intensive Moisture Care Carbonated Foam Gel Cleanser.

- February 2025: Indagare, one of the leading skin care brand, has expanded its product line with the launch of its new natural botanical cleanser suitable for all skin types and concerns.

- May 2024: Amorepacific’s Hanyul line entered the United States exclusively through Sephora, highlighting Korean botanicals such as yuja and artemisia in toner formulations.

Global Facial Cleansers And Toners Market Report Scope

The global facial cleansers and toners market is segmented by product type into facial toners and by distribution channel into supermarkets/hypermarkets, specialist retailers, convenience stores, online channels, and other distribution channels. The segmentation by geography provides insights into the key trends in the top markets for this category.

| Cleansers |

| Toners |

| Normal |

| Oily |

| Dry |

| Combination |

| Sensitive |

| Mass |

| Premium |

| Conventional |

| Natural/Organic |

| Supermarkets/Hypermarkets |

| Specialist Stores |

| Online Retail Stores |

| Convenience Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Cleansers | |

| Toners | ||

| Skin Type | Normal | |

| Oily | ||

| Dry | ||

| Combination | ||

| Sensitive | ||

| Price Range | Mass | |

| Premium | ||

| Category | Conventional | |

| Natural/Organic | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Specialist Stores | ||

| Online Retail Stores | ||

| Convenience Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the facial cleansers and toners market in 2026?

The facial cleanser and toner market size reaches USD 34.29 billion in 2026, with projections pointing to USD 48.09 billion by 2031.

Which region leads sales of facial cleansers and toners?

Asia-Pacific holds the largest share at 36.12% in 2025 and is forecast to keep expanding at a 9.1% CAGR.

What segment is growing fastest within product types?

Toners are the fastest-growing product type, advancing at an 7.79% CAGR through 2031 as brands pack them with treatment-grade actives.

Why are premium cleansers gaining traction?

Affluent consumers look for clinically validated ingredients, refillable packaging, and personalized routines, fueling a 8.96% CAGR for premium lines.

Page last updated on: