Single Sign-On Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

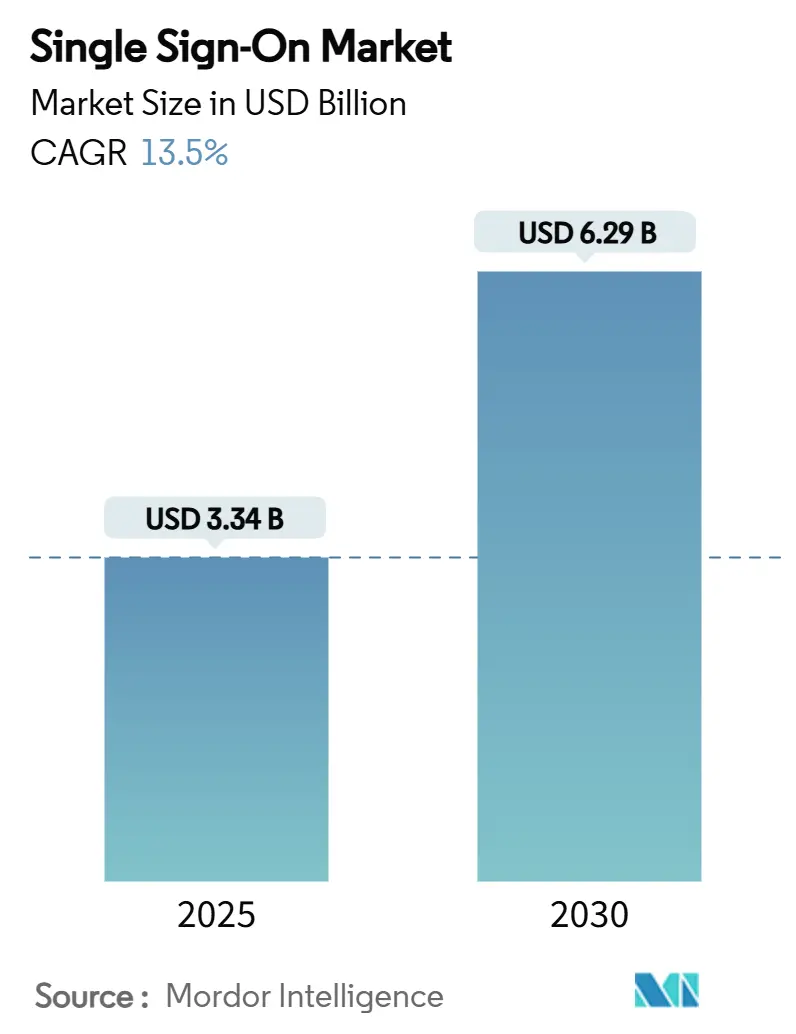

| Market Size (2025) | USD 3.34 Billion |

| Market Size (2030) | USD 6.29 Billion |

| Growth Rate (2025 - 2030) | 13.50% CAGR |

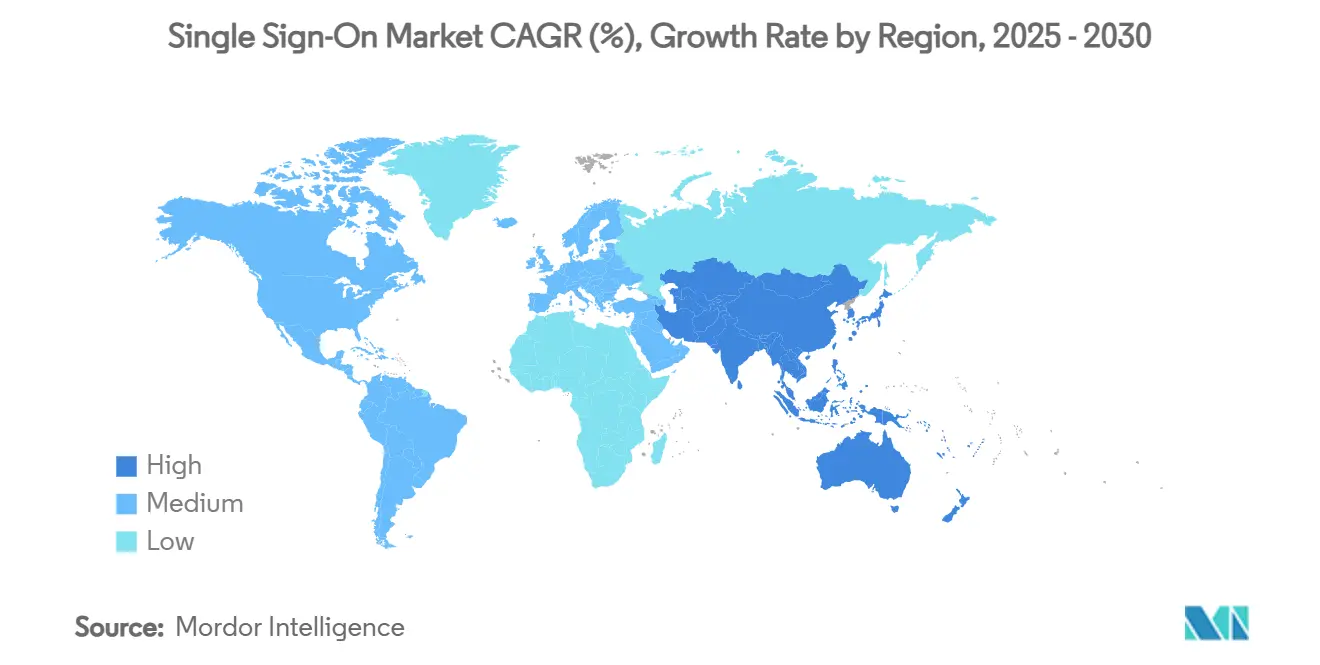

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single Sign-On Market Analysis by Mordor Intelligence

The Single Sign-On Market size is estimated at USD 3.34 billion in 2025, and is expected to reach USD 6.29 billion by 2030, at a CAGR of 13.5% during the forecast period (2025-2030). This robust trajectory mirrors the ongoing digital transformation of enterprises, the surge in distributed workforces, and the resulting need for simplified yet secure authentication. Widespread SaaS adoption, rising cyber-risk awareness, and rapid cloud migration collectively propel spending, while passwordless initiatives and zero-trust frameworks sharpen competitive differentiation. In addition, consolidation plays—such as JumpCloud’s Stack Identity purchase—are reshaping value propositions as vendors race to embed AI-driven analytics, threat detection, and governance at scale.

Key Report Takeaways

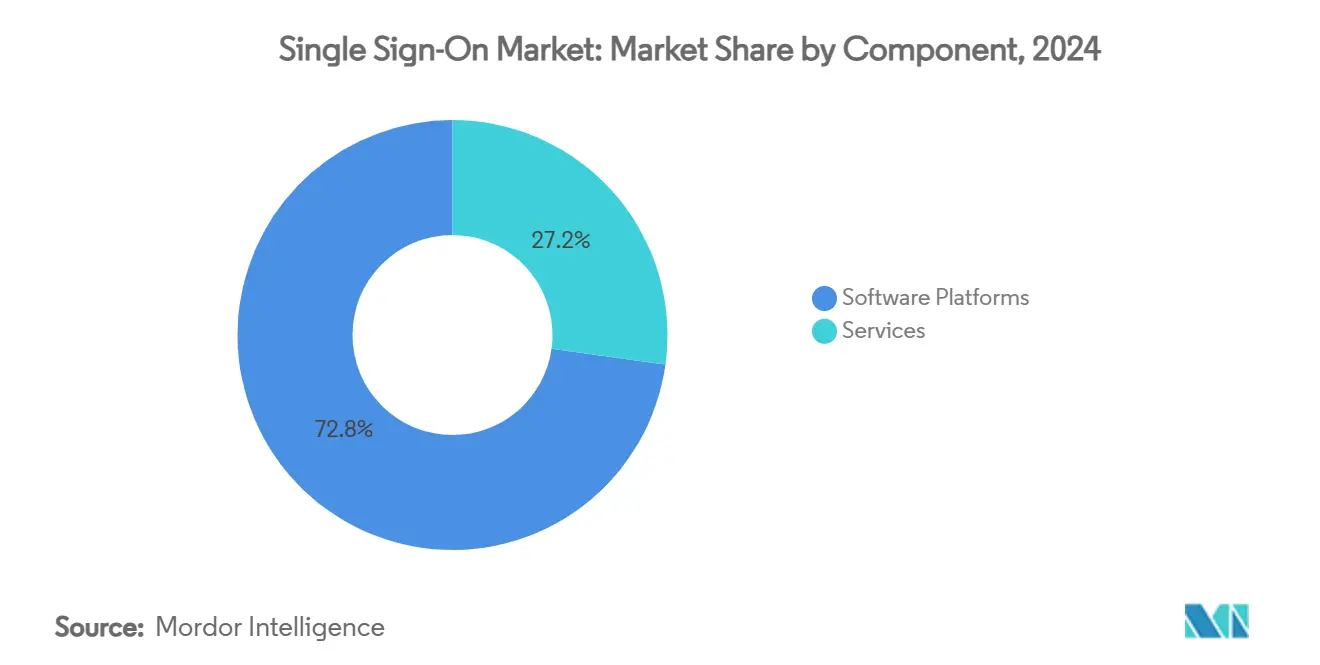

- By component, software platforms led with 72.8% revenue share of the single sign-on market size in 2024, whereas services are projected to advance at a 15.8% CAGR to 2030.

- By deployment mode, cloud captured 67.7% of the single sign-on market share in 2024, and its segment is expanding at a 14.7% CAGR through 2030.

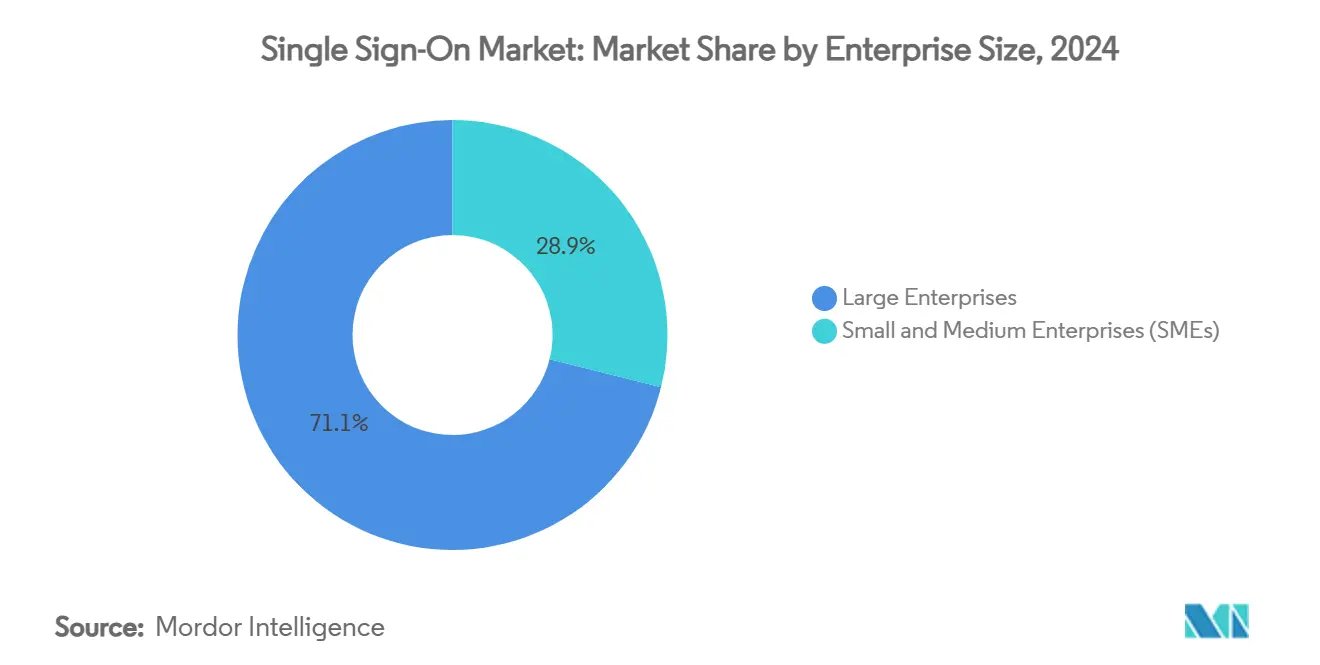

- By enterprise size, large enterprises accounted for 71.1% of the single sign-on market size in 2024, yet SMEs record the steepest growth at 15.6% CAGR to 2030.

- By SSO type, federated and web-based solutions commanded a 50.5% share of the single sign-on market size in 2024; Windows-integrated SSO posts the fastest 15.2% CAGR through 2030.

- By industry vertical, IT and telecom held 30.3% revenue share of the single sign-on market size in 2024, while BFSI is forecast to widen at a 15% CAGR between 2025–2030.

- By geography, North America dominated with 38.2% of single sign-on market share in 2024; Asia-Pacific is accelerating at a 15.1% CAGR toward 2030.

- Microsoft, Okta, and Ping Identity collectively controlled 34% of 2024 revenues, reflecting moderate concentration in a landscape still open to cloud-native disruptors.

Global Single Sign-On Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding SaaS adoption among distributed workforces | +2.5% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Mandatory zero-trust security in regulated sectors | +1.8% | Global BFSI and healthcare | Long term (≥4 years) |

| Migration from VPN to SASE architectures | +1.2% | North America and APAC core | Medium term (2-4 years) |

| Surge in passwordless initiatives (FIDO2, passkeys) | +1.5% | Tech-forward enterprises worldwide | Short term (≤2 years) |

| Embedded SSO in vertical SaaS marketplaces | +1.0% | North America, Europe, APAC expansion | Medium term (2-4 years) |

| Edge-native SSO for IoT and OT device fleets | +0.8% | Manufacturing hubs worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Exploding SaaS Adoption Among Distributed Workforces

The average enterprise now manages about 130 SaaS applications, up from fewer than 50 in 2020, forcing IT teams to mitigate password fatigue and shadow-IT risks. Employees lose 12.2 minutes each day juggling credentials, while help-desk tickets for resets remain a top cost center. Centralized authentication via single sign-on market platforms alleviates friction, as evidenced by AIA Group’s 60% decline in reset incidents after rolling out Okta across APAC. [1]Okta, “AIA Group,” OKTA.COM Heightened hybrid-work penetration—75% of businesses host networks primarily in the cloud—further cements the driver.

Mandatory Zero-Trust Security Frameworks in Regulated Sectors

Regulators frame identity as the new perimeter. SOX, NYDFS, GDPR, HIPAA, and the EU Digital Markets Act oblige audit-ready access controls, leading 39% of APAC organizations to implement zero-trust baselines. Centralized logs, real-time analytics, and continuous verification built into single sign-on market suites shorten audit preparations by 40% for healthcare providers. [2]Microsoft Tech Community, “Upcoming Changes to Windows Single Sign-On,” TECHCOMMUNITY.MICROSOFT.COM Vendors consequently embed consent flows, risk-based policies, and automated attestation to pass regulatory scrutiny.

Migration from Legacy VPN to SASE Architectures

Traditional VPNs falter under cloud traffic loads and granular access demands. SASE unifies networking and security at the edge, making identity the enforcement point. Organizations report 35% faster application response and 50% leaner network stacks when single sign-on market authentication is natively integrated. Manufacturers deploy edge-native SSO to secure OT assets without exposing production lines, blending human and machine identities under one policy plane.

Surge in Passwordless Initiatives (FIDO2, Passkeys)

Passkey rollouts cut credential-based breach vectors by 99.9% and trim help-desk volumes by 60% at early adopters. User satisfaction rises to 85%, doubling legacy login scores. Microsoft’s 2025 Entra roadmap hardwires passkey support, signaling mainstream enterprise adoption and reshaping vendor product maps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Audit-grade breach reporting escalates compliance cost | -1.2% | Regulated sectors worldwide | Short term (≤2 years) |

| Vendor lock-in fears across hyperscaler stacks | -0.9% | Global enterprises | Medium term (2-4 years) |

| Fragmented open-source forks hamper interoperability | -0.7% | Multi-vendor deployments | Long term (≥4 years) |

| Talent shortage in identity engineering and DevSecOps | -1.1% | North America, Europe, global impact | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Audit-Grade Breach Reporting Requirements Inflate Compliance Cost

GDPR fines of up to EUR 20 million or 4% of revenue, coupled with CCPA and state mandates, oblige businesses to capture immutable, high-granularity logs. Financial institutions juggling seven overlapping frameworks allocate as much as 25% of SSO budgets to compliance tooling and expertise. Data-residency rules add architectural complexity, often slowing multi-cloud rollouts.

Talent Shortage in Identity Engineering and DevSecOps

Roughly 700,000 U.S. cybersecurity roles remain unfilled; identity specialists command 40% salary premiums. Scarcity elongates deployment cycles and pushes organizations toward managed SSO services, raising long-run vendor dependencies and Total Cost of Ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Drive Market Value

Software suites represented 72.8% of 2024 revenues, anchoring the single sign-on market through integrated policy engines, governance workflows, and AI-powered risk analytics. The services segment, although smaller, is enjoying a 15.8% CAGR on the back of consultative deployments, managed identity orchestration, and compliance reporting. Vendors monetize recurring subscriptions and upsell adjacent modules—privileged access, lifecycle governance, and API security—embedding themselves deeper into enterprise architectures.

Enterprises gravitate to consolidated stacks to reduce vendor sprawl and administrative overhead. Cloud-native platforms further differentiate through DevOps automation, RESTful APIs, and no-code connectors that accelerate time-to-value. Vertical SaaS ecosystems increasingly bundle built-in SSO, redirecting value toward platform providers and fortifying customer lock-in. MSSPs likewise package white-label SSO to court mid-market firms constrained by talent gaps.

By Deployment Mode: Cloud Dominance Accelerates

Cloud implementations accounted for 67.7% of 2024 spending and will expand at a 14.7% CAGR as perimeter-less network models prevail. The single sign-on market size linked to cloud deployments benefits from elastic scalability, AI analytics, and pay-as-you-grow economics. On-premise instances linger in highly regulated or latency-sensitive environments; nonetheless, hybrid overlays fast-track modernization without breaching data-sovereignty obligations. Microsoft Entra’s automated anomaly detection exemplifies the AI-as-a-service edge that cloud SSO platforms wield. [3]Microsoft Entra Blog, “ID Governance Licensing for Business Guests,” MICROSOFT.COM

Edge computing further accentuates cloud demand because centrally defined policies must extend to branch devices and IoT gateways. Hence, vendors offer lightweight agents and distributed policy caches that sync with cloud controllers, maintaining resilience during connectivity disruptions.

By Enterprise Size: SME Growth Momentum Builds

Large enterprises owned 71.1% of 2024 revenues owing to complex app estates and sizable cybersecurity budgets. Yet SMEs represent the single sign-on market’s fastest-expanding cohort, clocking 15.6% CAGR. Low-code setup wizards, transparent pricing, and open-source forks such as Keycloak erode the historical “SSO tax,” unlocking security parity for smaller firms. Government grants and cyber-insurance incentives accelerate adoption, while MSSPs curate out-of-the-box policies that square affordability with compliance.

By SSO Type: Federated Solutions Lead Innovation

Federated and web-based protocols retained 50.5% of 2024 revenue, underpinned by SAML, OAuth, and OpenID Connect ubiquity across SaaS and mobile ecosystems. The segment’s open-standards ethos eases multi-cloud onboarding, propelling steady renewals.

Windows-integrated SSO, though a smaller slice, enjoys 15.2% CAGR as organizations harmonize Azure Active Directory (now Entra ID) with on-device biometrics and passkeys. The single sign-on market size attached to legacy SSO shrinks as hybrid bridges funnel users toward cloud platforms, but niche requirements in mainframe-heavy industries sustain maintenance contracts.

By Industry Vertical: BFSI Drives Fastest Adoption

IT and telecom held a 30.3% share in 2024, serving as technology bellwethers that test-drive new authentication paradigms. Within BFSI, soaring fintech integrations, Open Banking APIs, and stringent audit rules turbo-charge a 15% CAGR, marking the vertical as the prime revenue-growth engine.

Healthcare organizations reduce audit prep by 40% through centralized credentialing, while retail chains fuse online carts with in-store point-of-sale via customer SSO for frictionless omnichannel journeys.

Geography Analysis

North America controlled 38.2% of 2024 revenue, leveraging early cloud adoption, stringent regulatory regimes, and proximity to leading vendors. Yet the region’s cybersecurity labor crunch propels uptake of managed SSO services. Asia-Pacific posts a 15.1% CAGR, fueled by government digital-economy targets, e-commerce booms, and South-East Asian banking reforms. AIA Group’s cross-country rollout underscores a large-scale appetite for unified identity across multilingual user bases. [4]Okta, “AIA Group,” OKTA.COM Moreover, the single sign-on market size in APAC benefits from manufacturing-driven IoT growth, demanding edge-aware authentication.

Europe balances privacy imperatives—GDPR, the Digital Markets Act—with digital-sovereignty ambitions, encouraging domestic and open-source alternatives that satisfy data-residency clauses. Cross-border identity federation remains a persistent pain point, steering demand toward providers offering multi-tenant, regional cloud hosting. The Middle East and Africa trail in absolute spending but notch double-digit gains, especially within Gulf Cooperation Council smart-city and e-government programs seeking citizen SSO portals.

Competitive Landscape

The arena is moderately concentrated yet dynamic. Microsoft, Okta, and Ping Identity held roughly 34% combined share in 2024 as platform breadth, global channel networks, and deep R&D wells sustain leadership. Consolidation heats up: JumpCloud bought Stack Identity to infuse real-time threat detection, and Silverfort aligned with Rezonate to mesh adaptive MFA with identity threat analytics. Legacy vendors face backlash over the “SSO tax,” opening footholds for open-source and value-priced challengers that tout fee transparency.

Advanced analytics, machine learning, and passwordless authentication form the next competitive frontier. Microsoft’s 2025 passkey roadmap and Okta’s cross-platform device assurance illustrate how rapid feature cycles influence enterprise evaluations. Edge IoT and OT authentication remain white-space territory, where specialists like CyberArk and ForgeRock craft lightweight agents for constrained devices. Pricing pressure intensifies as hyperscalers bundle identity into broader cloud stacks, nudging independent vendors to differentiate on autonomy, multi-cloud neutrality, and deep compliance tooling.

Single Sign-On Industry Leaders

Okta, Inc.

Microsoft Corporation

Ping Identity Holding Corp.

ForgeRock, Inc.

OneLogin, Inc. (One Identity LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Varonis posted Q1 2025 SaaS revenue of USD 88.6 million, reflecting elevated cloud-security demand.

- January 2025: Microsoft detailed Entra passkey expansion and zero-trust blueprints to harden enterprise identity.

- January 2025: ServiceNow released the Xanadu update, adding granular permissions workflows for authentication estates.

- December 2024: Microsoft’s 2024 annual report highlighted the Secure Future Initiative’s priority status across cloud and identity lines.

Global Single Sign-On Market Report Scope

| Software Platforms |

| Services |

| Cloud |

| On-premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Federated and Web-based SSO |

| Enterprise/Legacy SSO |

| Windows Integrated SSO |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Public Sector |

| Education |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software Platforms | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By SSO Type | Federated and Web-based SSO | ||

| Enterprise/Legacy SSO | |||

| Windows Integrated SSO | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Public Sector | |||

| Education | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current single sign-on market size and growth outlook?

The single sign-on market size is USD 3.34 billion in 2025 and is projected to reach USD 6.29 billion by 2030, registering a 13.5% CAGR.

Which deployment mode is gaining the most traction?

Cloud deployments hold 67.7% revenue share and are expanding at 14.7% CAGR as organizations shift to cloud-first identity frameworks.

Why are SMEs embracing SSO more rapidly than before?

Lower cost cloud subscriptions, no-code setup, and government cyber incentives enable SMEs to overcome the historical “SSO tax” and adopt enterprise-grade security.

How are passwordless methods changing the SSO landscape?

Passkeys and FIDO2 eliminate credential-based breach vectors, cutting help-desk tickets by 60% and improving user satisfaction to 85%.

Which region will grow fastest through 2030?

Asia-Pacific leads with a 15.1% CAGR, driven by large-scale digitalization projects, regulatory mandates, and manufacturing-centric IoT rollouts.

Who are the key vendors in the single sign-on industry?

Microsoft, Okta, and Ping Identity remain front-runners, with challengers such as JumpCloud, ForgeRock, and open-source Keycloak expanding share through specializations and cost transparency.

Page last updated on: