Digital Signatures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

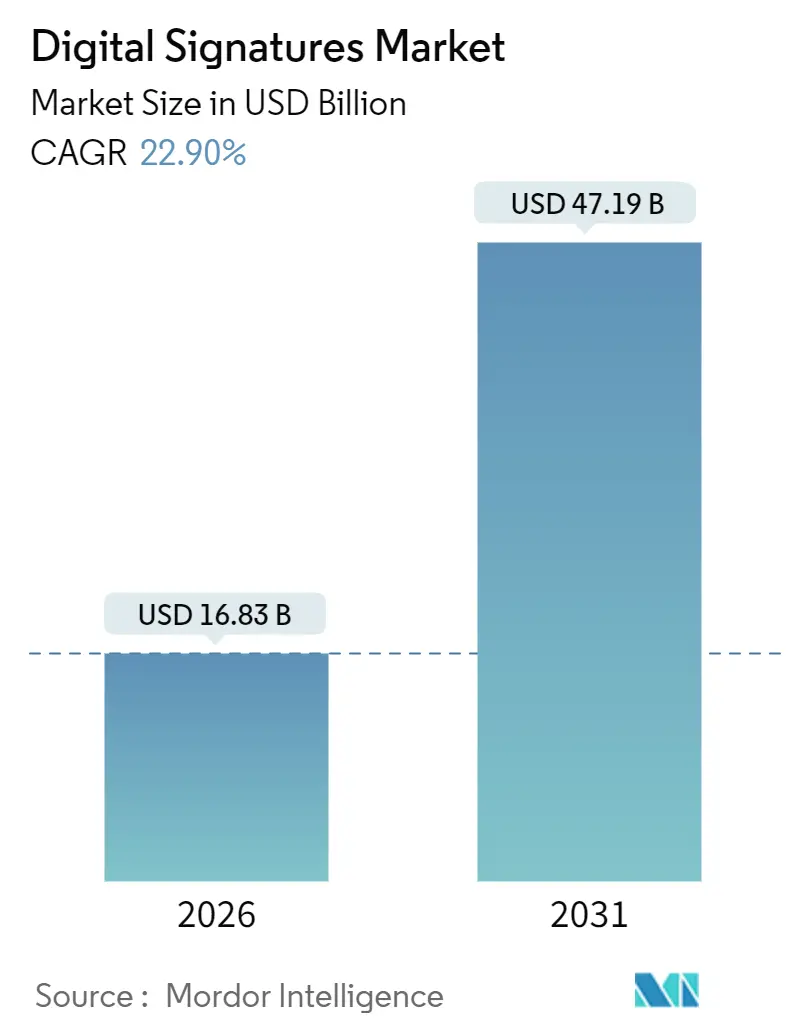

| Market Size (2026) | USD 16.83 Billion |

| Market Size (2031) | USD 47.19 Billion |

| Growth Rate (2026 - 2031) | 22.90% CAGR |

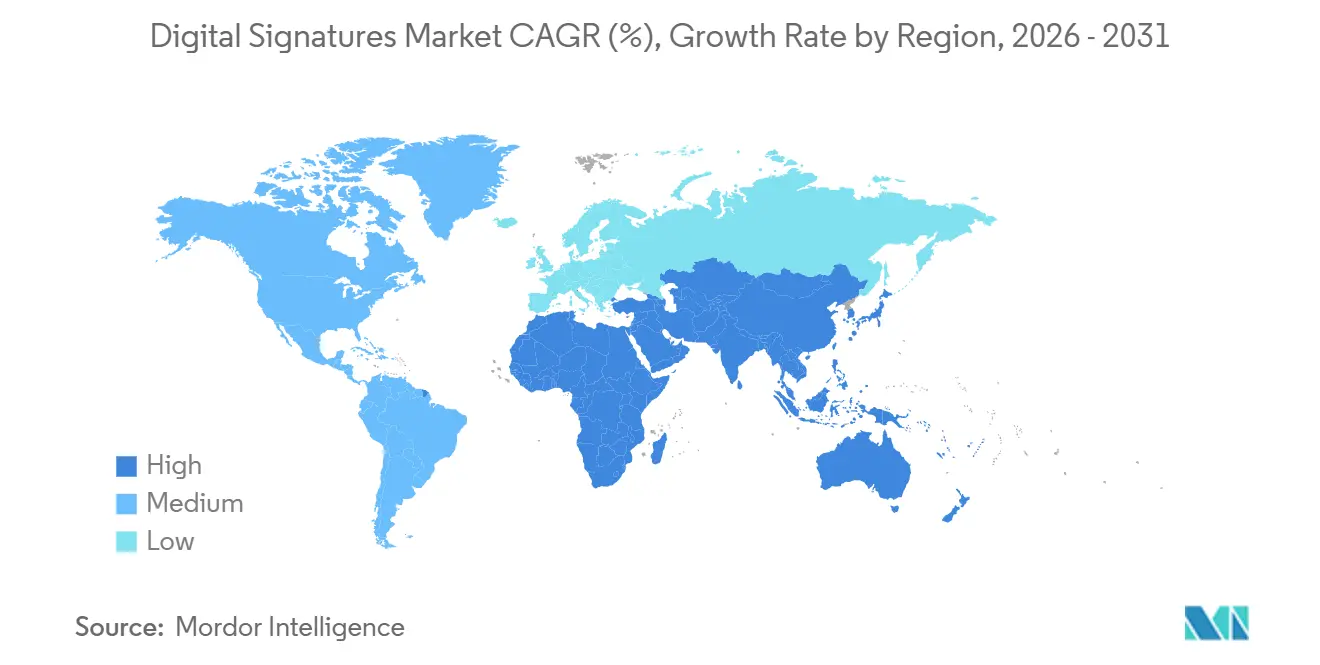

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Signatures Market Analysis by Mordor Intelligence

The digital signatures market size is USD 16.83 billion in 2026 and is forecast to reach USD 47.19 billion by 2031, expanding at a 22.90% CAGR during 2026-2031. This rapid expansion reflects enterprises moving from ink to cryptography as governments tighten compliance rules and software vendors bake signing functions into everyday applications, creating seamless user experiences that boost transaction throughput. Demand for cloud-delivered workflows is accelerating because CIOs want API-first platforms that plug directly into Microsoft 365 and Salesforce, while post-quantum cryptography (PQC) timelines are prompting upgrades of certificate stacks and hardware security modules. Price competition is intensifying as productivity-suite vendors bundle signatures at marginal cost, yet specialist providers still win regulated deals that demand high assurance and auditability. ESG programs are also driving adoption, with multinational corporations linking executive pay to reductions in paper usage, reinforcing the trajectory of the digital signatures market.

Key Report Takeaways

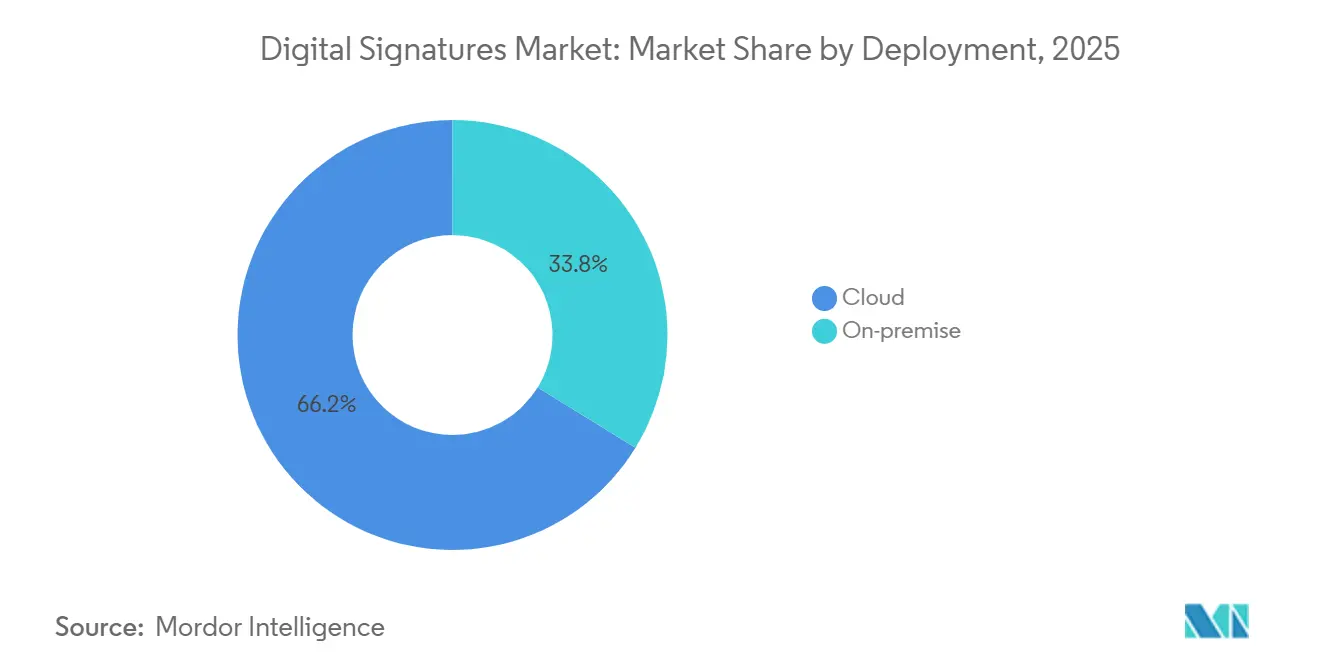

- By deployment, cloud captured 66.22% of the digital signatures market share in 2025, and the segment is projected to advance at a 25.66% CAGR through 2031.

- By offering, software accounted for 78.44% of the digital signatures market size in 2025, while services are the fastest-growing component at a 24.76% CAGR to 2031.

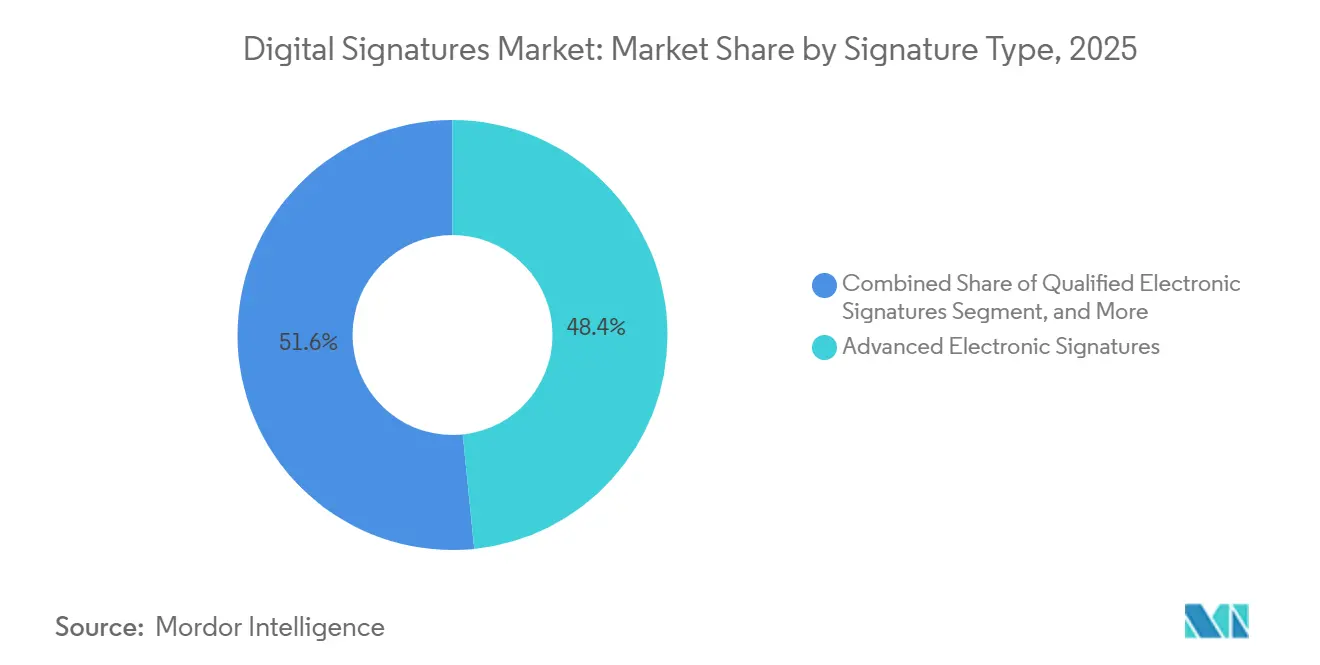

- By signature type, advanced electronic signatures led with 48.38% revenue share in 2025, whereas qualified signatures are on track for a 23.84% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance held 29.76% revenue share in 2025, and healthcare is expected to expand at a 24.12% CAGR to 2031.

- By geography, North America dominated with 40.12% share of the digital signatures market in 2025, but Asia Pacific is the fastest-growing region at a 23.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Signatures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Compliance Mandates for Qualified E-Signatures in EU (eIDAS 2.0) | +5.2% | Europe, with spillover to Middle East and Africa aligning with EU adequacy frameworks | Medium term (2-4 years) |

| Mega-Scale Digitisation Programmes in Asia Pacific Public Sector Workflows | +4.8% | Asia Pacific core (India, Singapore, Australia), expanding to Southeast Asia | Short term (≤ 2 years) |

| Embedded E-Signature APIs in Enterprise SaaS Suites (Microsoft 365, Salesforce) | +4.1% | Global, with highest penetration in North America and Europe | Short term (≤ 2 years) |

| Renewal Cycle Toward Post-Quantum Cryptography Certificate Stacks | +3.3% | Global, led by defense and financial institutions in North America and Europe | Long term (≥ 4 years) |

| ESG-Linked Push for Paperless Transactions and Scope-3 Carbon Reduction | +2.9% | Global, concentrated in North America and Europe with multinational headquarters | Medium term (2-4 years) |

| Digital Signatures Embedded in IoT Device Firmware Updates | +2.7% | Global, with early adoption in automotive hubs (Germany, Japan, United States) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Compliance Mandates For Qualified E-Signatures In EU (eIDAS 2.0)

The phased rollout of eIDAS 2.0 is forcing enterprises to adopt qualified electronic signatures that carry the same legal weight as handwritten ink across all EU jurisdictions. Implementing Regulation 2025/1569 spells out cryptographic algorithms and audit requirements, prompting a surge in qualified certificate issuance that climbed 340% year-over-year in H1 2025.[1]European Commission, “Commission Implementing Regulation (EU) 2025/1569,” eur-lex.europa.eu Notaries, land registries, and government procurement portals are aligning on the new specifications, compressing timelines for legacy certificate authorities to modernize or exit. The regulation’s extraterritorial pull is visible in Dubai International Financial Centre, which amended its Electronic Transactions Law to mirror eIDAS requirements, signaling a broader harmonization trend that stimulates the digital signatures market.

Mega-Scale Digitization Programs In Asia Pacific Public-Sector Workflows

India processed 1.2 billion Aadhaar-authenticated signatures in 2024 under its eSign framework, a 68% jump that spilled into banking and vehicle registration use cases.[2]Ministry of Electronics and Information Technology, “eSign Annual Report 2024-25,” meity.gov.in Singapore’s Sign with Singpass had reached 95% adoption across agencies by mid-2025, cutting approval cycles for public housing from five days to less than two hours. Australia’s Digital Identity system, live since November 2024, is projected to save AUD 11.4 billion (USD 7.6 billion) over 10 years. These programs establish national trust infrastructures that private firms can tap, accelerating network effects and raising the floor for the digital signatures market.

Embedded E-Signature APIs In Enterprise SaaS Suites

Microsoft added native signing to Word, Outlook, and SharePoint in October 2024, capturing 18% of the North American mid-market within nine months. Salesforce reports that 63% of new Sales Cloud tenants activate pre-built signature connectors inside 30 days, trimming implementation from 12 weeks to five. Standalone vendors face price compression as customers treat signatures as a checkbox feature bundled into existing subscriptions. However, API volumes are surging. Adobe logged a 110% jump in API-originated signature requests in 2025, cementing cloud as the default delivery model for the digital signatures market.

Renewal Cycle Toward Post-Quantum Cryptography Certificate Stacks

NIST finalized PQC standards FIPS 204 and FIPS 205 in August 2024, starting a global migration to lattice- and hash-based algorithms. The National Security Agency requires national security systems to complete the shift by 2030, and enterprises are dual-signing with RSA-2048 plus ML-DSA to remain future proof. DigiCert launched hybrid certificates in January 2025, while Thales plans to embed ML-DSA in Luna HSMs by Q4 2025. The capex burden is sizable. Thales estimates 40% of installed HSMs need replacement, yet vendors able to automate algorithm agility gain a competitive edge, lifting long-run growth for the digital signatures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Country-Specific Data-Localisation Rules Hindering Cross-Border Validity | -3.1% | Asia Pacific (China, India, Vietnam), Russia, Brazil | Medium term (2-4 years) |

| Fragmented Global Trust-Service Accreditation Regimes | -2.4% | Global, with highest friction between EU, United States, and Asia Pacific | Long term (≥ 4 years) |

| UX Gaps for Biometric Signatures on Low-Bandwidth Mobile Networks | -1.8% | Africa, South Asia, rural Latin America | Short term (≤ 2 years) |

| High Cost of HSM-Backed Qualified Signatures for SMBs | -1.6% | Global, concentrated in Europe where eIDAS 2.0 mandates qualified signatures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Country-Specific Data-Localization Rules Hindering Cross-Border Validity

China’s 2024 Cybersecurity Law revision forces all signature keys and logs to stay onshore, blocking multinational clouds from offering unified services across Asia Pacific.[3]Cyberspace Administration of China, “Regulations on Cryptographic Key Management for Cloud Services,” cac.gov.cn India mandates domestic certificates for any document addressed to government entities, fragmenting workflows for firms signing both public and private contracts. Brazil’s LGPD raises uncertainty around whether keys constitute sensitive data, pushing firms to host separate signature stacks for subsidiaries. These overlapping rules inflate compliance costs and slow adoption among mid-market firms, moderating the global CAGR of the digital signatures market.

Fragmented Global Trust-Service Accreditation Regimes

European qualified trust service lists do not automatically honor WebTrust-audited U.S. certificate authorities, forcing parallel audits that can exceed USD 300,000 per market. The CA/Browser Forum’s tighter domain checks, updated in March 2025, clash with some national ID schemes, requiring vendors to maintain region-specific certificate profiles. Cross-border transactions like bills of lading still stall when one party’s certificate is not recognized in the destination port, adding legal risk and slowing full digitization of international trade. Until mutual recognition progresses, this restraint weighs on long-range expansion of the digital signatures market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Architectures Dominate Infrastructure Choices

Cloud deployments accounted for 66.22% of the digital signatures market share in 2025, and the segment is projected to grow at a 25.66% CAGR to 2031 as firms favor multi-tenant platforms that keep per-signature costs below USD 0.10. Microsoft’s decision to include signatures at no extra charge for Microsoft 365 E5 subscribers accelerated migration and reduced vendor sprawl. The digital signatures market size attributable to cloud workflows is expanding fastest in regulated industries that now accept ISO/IEC 27001-certified outsourcing.

While on-premise remains important for air-gapped defense networks, hybrid models are emerging. Hospitals hold patient keys on-site yet route vendor contracts through cloud-based orchestrators, compressing turnaround from days to hours. Edge deployments, where IoT gateways validate firmware signatures offline, are gaining traction among offshore energy operators. These nuanced patterns underscore why the digital signatures market retains diversity even as cloud dominates overall growth.

By Offering: Services Surge As Implementation Complexity Rises

Software still captured 78.44% of the 2025 digital signatures market size, but services are expanding at a 24.76% CAGR as firms confront legacy integrations. Managed PKI, compliance consulting, and user-training bundles address gaps that pure software cannot. OneSpan’s professional-services revenue jumped 32% year-over-year, reflecting this pivot.

Hardware spends remain steady because qualified signatures require tamper-resistant modules, yet commoditized USB tokens serve advanced-signature workflows at sub-USD 20 price points. Training and change-management programs reduce help-desk load for qualified signature rollouts, supporting outcome-based engagement models. As enterprises demand turnkey solutions rather than licenses, the services segment will outpace software in contribution to overall digital signatures market growth.

By Signature Type: Advanced Signatures Balance Usability And Legal Weight

Advanced electronic signatures held 48.38% revenue share in 2025, offering enterprises cryptographic assurance without the accredited infrastructure overhead that qualified signatures demand. Courts are tightening evidentiary standards, nudging firms to abandon basic click-wrap methods for any contract above materiality thresholds. The digital signatures market size for qualified signatures is on track to expand at a 23.84% CAGR as EU rules harmonize certificate profiles, lowering integration friction.

Qualified signatures are rising fastest in real-estate and public-procurement workflows, such as Spain’s decree that mandates qualified certificates for property transfers above EUR 300,000 (USD 320,000). Biometric signatures are emerging as a niche, provided capture devices align with ISO/IEC 19794 standards. Vendors that streamline access to qualified or biometric options inside a unified interface will capture incremental wallet share, enhancing stickiness in the digital signatures market.

By End-User Industry: Healthcare Outpaces Traditional Leaders

Banking, financial services, and insurance owned 29.76% revenue in 2025, reinforcing its historical role as the largest vertical user base. Yet healthcare is the fastest-growing vertical, expanding at a 24.12% CAGR through 2031 as telemedicine, electronic health records, and FDA 21 CFR Part 11 requirements meet. Hospitals are embedding signatures directly into patient portals, cutting consent turnaround from hours to minutes.

Government agencies are moving rapidly under digitization mandates, while logistics, real estate, and legal services continue rising adoption curves. IoT firmware signing for automotive and industrial equipment introduces a fresh, high-margin niche. These vertical motions illustrate how diverse pain points converge to propel the broader digital signatures market.

Geography Analysis

North America accounted for 40.12% of the digital signatures market in 2025, buoyed by the mature ESIGN Act and concentration of major vendors. Canadian lenders report that 84% of mortgage applications used electronic signatures in 2025, while Mexico’s 2024 code amendment has pushed notarial acts online. Court enforcement certainty and abundant vendor choice sustain robust transaction volumes across fintech, healthcare, and real estate.

Asia Pacific is the fastest-growing region with a 23.22% CAGR to 2031. India’s eSign handled 76% of vehicle transfers through digital signatures in 2025, extending reach beyond banking. Singapore’s near-universal government adoption and Australia’s national digital identity scheme prove public-sector leadership can jump-start private demand. China’s tight data-localization rules slow foreign cloud vendors but foster domestic champions that satisfy local residency mandates. Japan’s 2024 legal update unlocked export-documentation digitization, lifting usage among manufacturers.

Europe shows complex dynamics. eIDAS 2.0 mandates pan-EU recognition of qualified signatures, and Germany alone issued 2.3 million certificates in 2025. The United Kingdom, outside the EU, recognizes electronic bills of lading under its 2024 regulations, spurring trade-finance digitization. France reduced accredited trust providers to 12 under stricter 2025 audit rules, consolidating share among larger players. Smaller regions such as the Middle East and Africa benefit from EU-aligned frameworks, and Brazil’s ICP-Brasil underpins qualified tax filings across South America. Together these regional trends underscore the global breadth of the digital signatures market.

Regulatory Landscape

Digital signatures sit at the intersection of electronic transaction law, identity assurance, and cryptographic standards. In the European Union, the shift toward the European Digital Identity (EUDI) framework tightens interoperability and assurance requirements: Regulation (EU) 2024/1183 sets a December 2026 deadline for Member States to provide EUDI Wallets, while Commission Implementing Regulation (EU) 2026/248 (February 2026) establishes standard formats for advanced electronic signatures and seals recognized by public sector bodies, replacing earlier rules and reducing cross-border validation friction.

Outside the EU, the United States continues to rely on the ESIGN Act (15 USC 7001) as the federal baseline for legal validity of electronic records and signatures, with state-level frameworks largely harmonized through UETA adoption. New York remains an outlier without UETA, and ongoing 2026 modernization efforts referenced by the New York City Bar Association highlight how residual state-by-state differences can complicate nationwide contracting policies for enterprises that need consistent signature enforceability and audit practices.

Value Chain Analysis

The digital signatures value chain starts with standards and trust frameworks (e.g., NIST and ETSI guidance) that define acceptable algorithms, identity proofing, and signature formats, then flows through certificate authorities and Qualified Trust Service Providers (QTSPs) that issue and manage certificates, timestamping, and validation services. Platform vendors package these capabilities into signing software, APIs, and workflow tooling, often integrating with enterprise productivity and line-of-business systems, while hardware providers supply HSMs and secure elements used for high-assurance and regulated use cases.

Downstream, relying parties include banks, government agencies, healthcare providers, and logistics operators that validate signatures within business workflows and retain evidence for audit and litigation readiness. Near-term bottlenecks concentrate around re-certification and interoperability alignment for eIDAS 2.0 and EUDI Wallet programs, highlighted by the EU move to standardized formats under Implementing Regulation (EU) 2026/248 and the broader push for quantum-safe guidance (e.g., ETSI TR 104 239-1 published in March 2026 and NIST IR 8610 finalized in May 2026), which influences procurement cycles for certificate stacks, HSM refresh, and validation services.

Competitive Landscape

DocuSign, Adobe, Microsoft, OneSpan, and Thales controlled roughly 58% of the digital signatures market in 2025, yet competitive intensity is rising as enterprise-SaaS platforms embed signing at marginal cost. Microsoft leverages its 400 million-user base to capture mid-market accounts without separate procurement. Adobe focuses on AI-driven content summarization and workflow triggers that elevate document intelligence. DocuSign launched Maestro Agentic AI to auto-extract signers, shrinking configuration time by 70%.

Regional specialists thrive by navigating data-localization rules and trust-service accreditation hurdles. India’s eMudhra, Brazil’s CertiSign, and the Nordic region’s Signicat secure public-sector contracts by operating domestic data centers and complying with local cryptography guidelines. PKI specialists like DigiCert and Entrust penetrate IoT firmware signing, where automotive cybersecurity demands high-assurance, low-latency verification. Patent filings for PQC, blockchain audit trails, and biometrics climbed 210% in 2024-2025, showing that technology differentiation remains vital.

Market structure is drifting toward bifurcation: premium qualified trust-service providers charge for high assurance, while commodity advanced-signature vendors compete on user experience and integrations. Vendors that master algorithm agility, identity federation, and AI-based fraud detection will capture disproportionate value as the digital signatures market scales internationally.

Digital Signatures Industry Leaders

DocuSign Inc.

Adobe Inc. (Adobe Sign)

OneSpan Inc.

Thales Group (SafeNet)

Entrust Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The EU-wide EUDI Wallet rollout creates a large, time-bound integration and compliance window for signature providers, trust service providers, and identity vendors. Implementing Regulation (EU) 2026/248 (February 2026) sets recognized formats for advanced electronic signatures and seals for public sector use, while Implementing Regulation (EU) 2026/798 (April 2026) specifies remote onboarding requirements for high-assurance wallet use cases; together, these measures increase demand for wallet-ready signature issuance, validation services, and orchestration layers that connect QTSPs with relying-party applications. ETSI publishing an initial set of EUDI Wallet ecosystem specifications in June 2026 further underpins vendor opportunities in interoperability testing, conformity assessment support, and managed trust services.

Platform-level commoditization also opens whitespace in differentiated, high-assurance workflows rather than basic signing. Google beginning a rollout of a native Signatures app for Android via a June 2026 Google Play system update reinforces the trend toward OS-level and suite-level signing as a utility, pushing independent providers to compete through regulated-grade identity verification, auditability, and deep workflow automation. In parallel, visible moves toward quantum-resistant certificate security, such as Google announcing Merkle Tree Certificates for Chrome in February 2026, raise customer requirements for algorithm agility and long-term cryptographic resilience, strengthening demand for upgrade services around PKI operations, HSM-backed key protection, and validation policy management.

Recent Industry Developments

- June 2026: DocuSign released a Slack app to bring agreement intelligence and agentic contract workflows into Slack-based collaboration. The launch extends signature and agreement automation into daily workstreams, strengthening stickiness through workflow context and reducing the need to switch between contract tools and collaboration apps.

- May 2026: DocuSign announced a partnership with ID.me to integrate identity verification into online agreements. Adding higher-assurance identity proofing supports regulated and higher-risk transactions where signer verification is as critical as document integrity, helping signature workflows meet stricter compliance and fraud-prevention requirements.

- October 2024: Microsoft added native signing capabilities across Word, Outlook, and SharePoint. This embedded approach pushed digital signing closer to a default productivity feature, intensifying price pressure on standalone vendors while expanding the overall volume of digitally executed documents through existing enterprise licenses.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market counts the yearly revenues earned from certificate-based digital signature software, related signing infrastructure, and managed signing services that make an electronic record verifiable and tamper-evident across common document and workflow use cases.

Scope exclusions: We exclude basic e-sign tools that do not use certificate-backed cryptography, and standalone biometric signature verification that is sold as a separate product.

Segmentation Overview

- By Deployment

- On-Premise

- Cloud

- By Offering

- Software

- Hardware

- Services

- By Signature Type

- Basic Electronic Signatures

- Advanced Electronic Signatures

- Qualified Electronic Signatures

- By End-User Industry

- BFSI

- Government

- Healthcare

- Oil and Gas

- Military and Defense

- Logistics and Transportation

- Other End-User Industries (Research and Education, Real Estate, Manufacturing, Legal, IT and Telecom)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the hard boundaries for what is and is not a digital signature, then to collect external indicators that explain adoption by country and by industry. We referenced public sources such as NIST publications, ENISA guidance, US SEC filing and disclosure trends, US Census Bureau business statistics, and European Commission updates tied to eIDAS, which helped us map the policy and trust-services environment.

For the commercial side, we reviewed company filings, audited annual reports, investor presentations, and product documentation to understand how vendors package signing, certificate, and identity steps into paid plans. In a few cases, paid subscriptions for company financials and intelligence, news and financials, patent databases, and global contracts and tenders were used to cross-check product focus and deal-activity signals. The sources listed here are illustrative only, and many other references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what buyers actually pay for and what is bundled, because pricing and packaging can shift quickly in this market. We spoke with a mix of solution providers, channel and integration partners, and enterprise and public-sector users across APAC, EMEA, and the Americas, so assumptions on adoption, renewal behavior, and regulated-use demand could be checked and tightened against firsthand procurement and implementation experience.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 48% |

| Mid tier: 52% | Functional/Unit leaders: 25% | EMEA: 32% |

| Smaller Players: 19% | Managers: 59% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing started from a top-down demand build that ties digital signature spending to the pool of formal document workflows that require identity assurance and integrity, then applies regional weighting based on regulation intensity and enterprise digitization. Once that demand pool was set, we used selective bottom-up approximations such as sampled vendor revenue disclosures, channel feedback on average contract values, and sanity checks on active customer counts to adjust totals where the first pass looked stretched.

Inputs that mattered most were indicators like enterprise cloud adoption and remote-work persistence, the pace of eIDAS-style trust-service rollouts, public-sector digital document programs, regulated signing requirements in sectors like finance and healthcare, and the observed shift from one-time license fees to subscriptions. Forecasting was done using scenario analysis supported by a small set of shared drivers, because adoption is influenced by regulation timing, procurement cycles, and pricing resets that do not move in a straight line. Where direct revenue splits were not available, gaps were handled by using product-mix cues from documentation and interviews, and then applying conservative ranges that were later narrowed through re-contacts.

Data Validation & Update Cycle

Outputs were checked through multiple passes so the final number matches real-world signals and does not rely on a single assumption. We compared regional totals against independent indicators such as public trust-service activity, e-government digitization efforts, and the direction of enterprise security spending, then reviewed outliers that implied unrealistic price or volume jumps.

Before sign-off, the model is reviewed by another analyst, and any large variance against interview feedback triggers a follow-up call to confirm the driver behind the change. The report is refreshed annually, and material events like regulatory changes, major pricing shifts, or step-changes in cloud adoption are monitored for interim revisions. Right before delivery, a fresh review pass is completed so clients receive the most current view.

Mordor Intelligence's Digital Signatures Market Size Compared With Other Published Estimates

Published market numbers for digital signatures can look far apart because the definition line is drawn differently, and timing and currency treatment also vary by publisher. Differences show up most when adjacent tools are counted as digital signatures even if they do not rely on certificate-backed cryptography, or when services like identity proofing are fully blended into the same bucket.

Evidence from certificate-backed signing requirements in regulated workflows, plus cross-checks using deal activity and vendor revenue cues, is what keeps the Mordor Intelligence estimate anchored to paid digital signature capability rather than broad e-sign usage. In practice, gaps usually come from whether hardware security modules and managed signing are included, how subscription expansion is modeled through ASP progression, and how often assumptions are refreshed when packaging changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.83 B (2026) | |

| Global Consultancy A | USD 9.85 B (2025) | Uses an earlier base year and appears to frame the market closer to software and platform revenues, with less clarity on inclusion of signing infrastructure and managed signing services, which can compress the total. |

| Industry Research Group B | USD 6.90 B (2025) | Leans toward a narrower revenue scope around digital signature solutions, and the 2025 cut can miss recent subscription re-pricing and the expanded use of certificate-based signing in government and regulated industries. |

Looking across the three figures, the spread is mostly explained by scope boundaries and year selection rather than disagreement on the growth direction. When the counted revenue base includes infrastructure and managed signing, and when subscription packaging changes are reflected close to the measurement year, the resulting market size becomes easier to reconcile with observed demand signals and repeatable checks.

Key Questions Answered in the Report

What is the projected value of the digital signatures market in 2031?

It is expected to reach USD 47.19 billion, expanding at a 22.90% CAGR during 2026-2031.

Which deployment model is growing fastest within digital signing?

Cloud workflows lead, with a 25.66% CAGR forecast through 2031.

Why is healthcare adoption accelerating?

Telemedicine consent, EHR integrations, and FDA Part 11 compliance drive a 24.12% CAGR to 2031.

How are post-quantum requirements affecting adoption?

NIST PQC standards push vendors to dual-sign certificates, creating upgrade demand for HSMs and software stacks.

Which region shows the highest growth potential?

Asia Pacific posts a 23.22% CAGR through 2031 due to large-scale public-sector digitization programs.

Page last updated on: