Account Based Marketing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 11.94% CAGR |

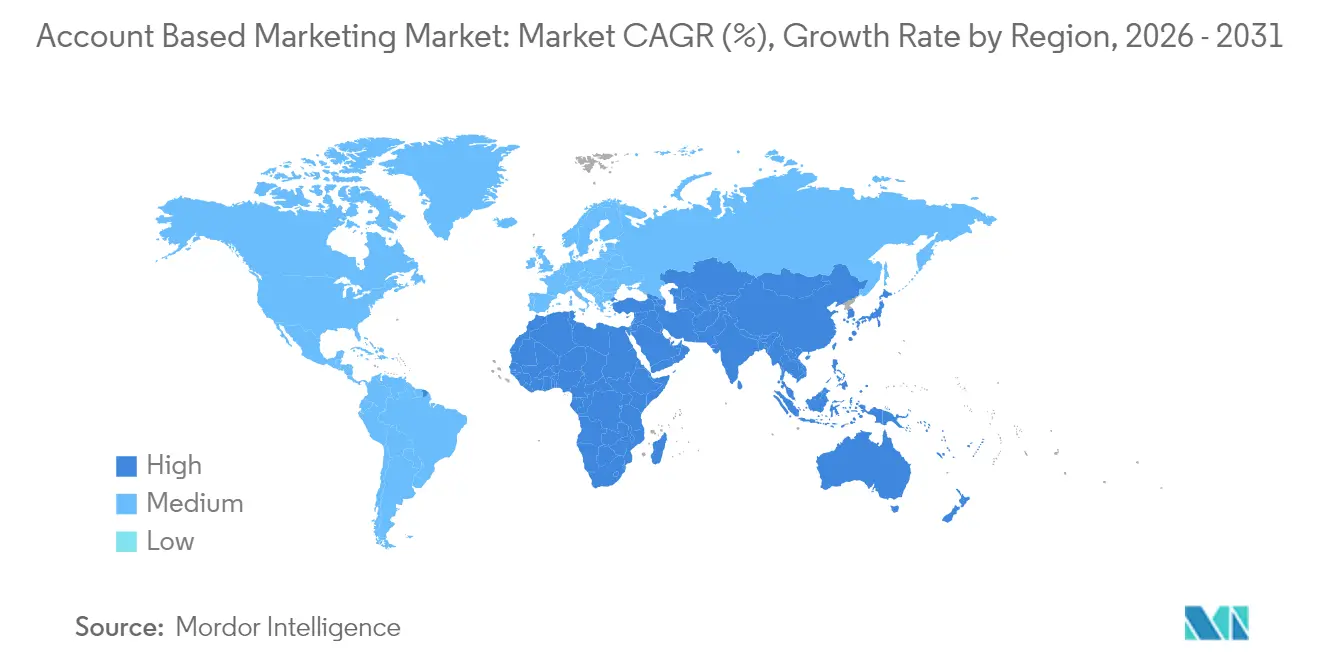

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Account Based Marketing Market Analysis by Mordor Intelligence

The Account-Based Marketing market size is expected to grow from USD 1.03 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 2.02 billion by 2031 at 11.94% CAGR over 2026-2031. This acceleration reflects the shift from broad lead generation to highly personalized engagement, as first-party data strategies, AI-driven intent analytics, and programmatic advertising converge to improve precision targeting. Cloud-native ABM platforms now orchestrate data from customer data platforms (CDPs), CRM systems, and ad exchanges in real time, enabling marketers to identify buying-group signals, shorten sales cycles, and raise conversion rates. Google’s scheduled 2025 phase-out of third-party cookies is reinforcing these trends by making privacy-compliant, first-party data-centric approaches indispensable. Vendors are answering with cookieless ID graphs, IP-based targeting, and hashed-email matching, while CMOs simultaneously reallocate larger budget portions to measurable, revenue-linked programs. The Account-Based Marketing market therefore sits at the crossroads of data privacy regulation, AI innovation, and B2B revenue accountability.

Key Report Takeaways

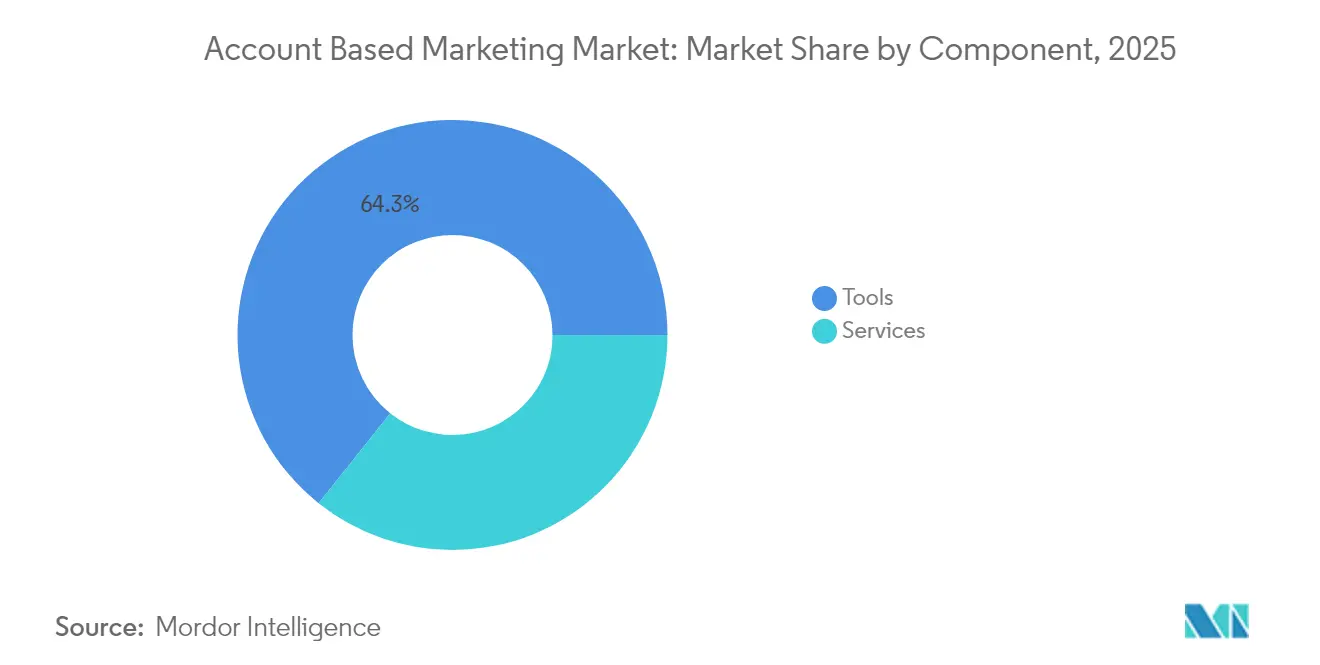

- By component, the Tools segment led with 64.30% of Account-Based Marketing market share in 2025; Services is projected to record a 14.02% CAGR through 2031.

- By deployment model, cloud solutions held 71.40% of the Account-Based Marketing market size in 2025 and are expected to expand at a 13.21% CAGR.

- By end-user industry, IT and Telecommunications accounted for a 25.60% share of the Account-Based Marketing market size in 2025, while Healthcare & Life Sciences is advancing at a 14.62% CAGR.

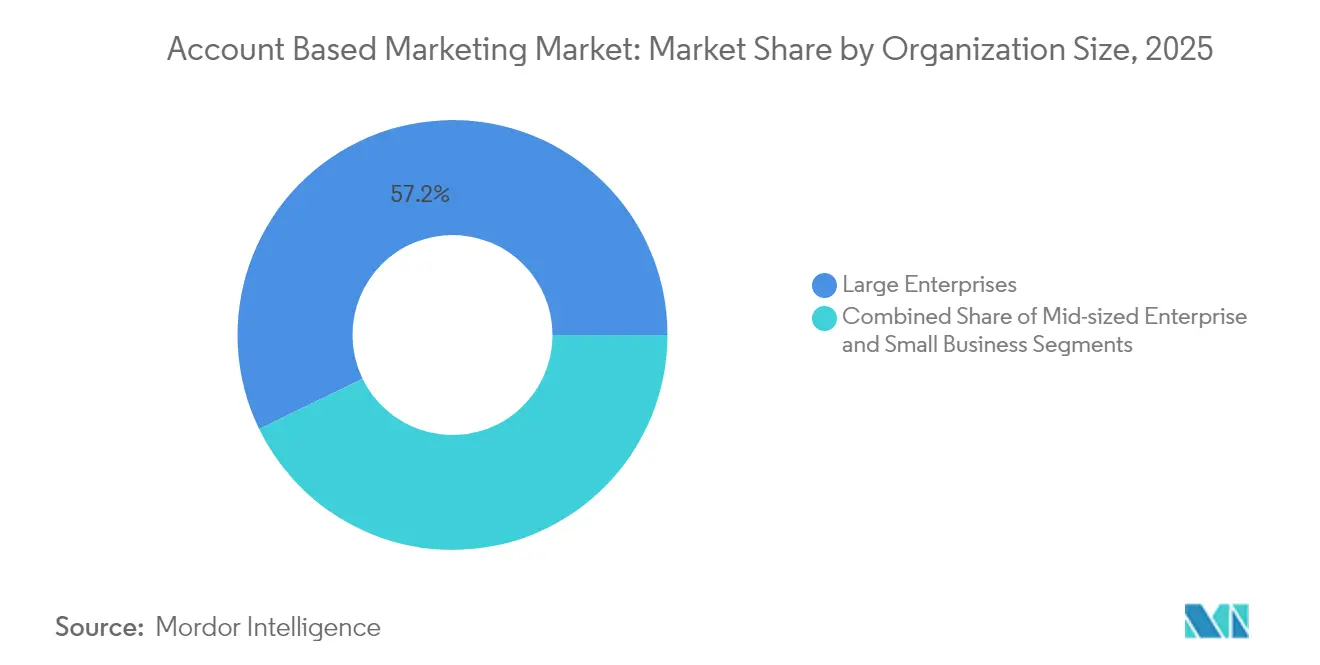

- By organization size, Large Enterprises captured 57.20% of the Account-Based Marketing market share in 2025; Mid-sized Enterprises show the fastest growth at 14.25% CAGR.

- By channel, Display Advertising commanded 29.50% of spending in 2025, whereas Social Media is rising at a 15.38% CAGR.

- By geography, North America represented 40.60% of the Account-Based Marketing market size in 2025; Asia-Pacific is poised for 14.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Account Based Marketing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Intent-Data Partnerships Accelerating ABM Platform Effectiveness | +2.5% | Global, with stronger impact in North America | Medium term (2-4 years) |

| Rapid Uptake of Programmatic ABM in Asia-Pacific Tech Start-Ups | +1.8% | Asia-Pacific, with spillover to global tech hubs | Short term (≤ 2 years) |

| Convergence of Customer Data Platforms (CDPs) with ABM Suites in North America | +1.5% | North America, with gradual adoption in Europe | Medium term (2-4 years) |

| Industry-specific Playbooks Driving ABM Adoption in BFSI & Healthcare | +1.2% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Declining Third-Party Cookie Support Elevating ABM Demand for First-Party Data | +2.1% | Global, with initial impact in North America and Europe | Short term (≤ 2 years) |

| Shift Toward Revenue-Based Metrics Among CMOs Boosting ABM Budgets | +1.4% | Global, with stronger impact in enterprise segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Intent-Data Partnerships Accelerating ABM Platform Effectiveness

Marketers are integrating third-party intent feeds with proprietary first-party data to rank accounts by in-market probability, resulting in sharper audience segmentation and higher win rates. More than nine in ten B2B teams embed purchase-signal data into their scoring models, and reported ROI lifts approach double traditional programs. ABM suites increasingly embed native connectors to feed intent events directly into orchestration engines, enabling same-day activation. Large software vendors are further enriching signals with conversational intelligence that captures qualitative buying context. Because these capabilities shorten sales cycles and increase average deal sizes, they are forecast to add 2.5 percentage points to overall CAGR.

Rapid Uptake of Programmatic ABM in Asia-Pacific Tech Start-Ups

Mobile-first startups across Singapore, India, and Australia are shifting ad spend into programmatic ABM that automatically matches creative, bid, and channel to each intent-rich account. Regional use cases show click-through lifts exceeding 50% and cost-per-opportunity declines of more than 30%. Localized partner ecosystems—DSPs, data providers, and ABM managed-service agencies - are lowering entry barriers, catalyzing broader adoption. The momentum is reinforced by investor pressure on startups to demonstrate efficient growth, turning programmatic ABM into a core acquisition lever. The resulting contribution to the Account-Based Marketing market growth is estimated at 1.8 percentage points over the next two years.

Convergence of Customer Data Platforms with ABM Suites in North America

Enterprises are welding CDPs to ABM engines so that behavioral, transactional, and firmographic attributes stream into unified profiles accessible to sales and marketing teams. Oracle’s CDP-driven marketing suite reports engagement lifts around 20% after enabling real-time journey triggers tailored to buying-group roles. [1]Oracle Corporation, “Oracle Marketing and Sales Unification Suite,” oracle.com Unified identity resolution allows marketers to cut waste from duplicative outreach and shift budgets to high-intent micro-segments. As integration templates from major vendors simplify deployments, North American adoption is accelerating, adding 1.5 percentage points to forecast CAGR.

Declining Third-Party Cookie Support Elevating ABM Demand for First-Party Data

Google’s looming Chrome policy change is forcing B2B advertisers to replace cookie-based retargeting with privacy-safe alternatives. ABM vendors now ship cookieless ID graphs that map hashed business emails, domain signals, and IP ranges to account profiles. Early adopters report stable match rates and impression quality despite cookie loss, while compliance teams welcome reduced regulatory exposure. This shift is driving an incremental 2.1 percentage-point lift in growth as budgets reallocate from broad display to account-centric programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brand-Side Talent Gap in Multi-Touch Attribution Analytics | -0.8% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| High Subscription Costs Limiting Penetration in Emerging Markets | -0.6% | Asia-Pacific, Latin America, Middle East & Africa | Short term (≤ 2 years) |

| Data-Privacy Compliance Complexity (GDPR, LGPD, CCPA) | -0.5% | Global, with strongest impact in Europe | Medium term (2-4 years) |

| CRM–ABM Integration Challenges for Legacy On-Premise Installations | -0.4% | Global, with concentration in enterprise segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Brand-Side Talent Gap in Multi-Touch Attribution Analytics

Enterprises struggle to find analysts who can stitch online and offline touchpoints into reliable influence models, limiting confidence in ABM ROI calculations. Forty-plus percent of in-house teams admit capability gaps, which delay optimization cycles and constrain budget expansion. Outsourcing to agencies raises costs and slows insight turnaround times. Emerging markets feel the pinch most acutely, as experienced talent commands premium salaries in competitive labor pools. Until training pipelines widen, this shortfall is expected to shave 0.8 percentage points off CAGR.

High Subscription Costs Limiting Penetration in Emerging Markets

Comprehensive ABM suites often start near USD 400 per month and scale into five-figure annual contracts once advanced features and higher target-account volumes are unlocked. Such pricing challenges mid-market firms in price-sensitive economies, especially where marketing technology budgets hover at low single-digit shares of revenue. Although modular offerings and region-specific vendors are appearing, cost remains the primary obstacle to mass deployment, dampening overall growth by 0.6 percentage points in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Tools in Value Creation

Tools retained 64.30% of the Account-Based Marketing market share in 2025, supplying AI-powered account selection, multi-channel orchestration, and pipeline analytics. Yet the Services component is entering a higher-velocity phase, delivering a 14.02% CAGR through 2031 as companies enlist strategic advisory, content development, and managed-campaign support. The transition from technology acquisition to execution excellence fuels this surge because organizations recognize that orchestration rigor, sales alignment, and analytics maturity—not software alone—unlock revenue impact. Services providers now package vertical playbooks, attribution consulting, and first-party data architecture, positioning themselves as indispensable transformation partners.

The Account-Based Marketing market consequently relies on a symbiosis: platforms furnish scalable infrastructure, while service specialists de-risk adoption and accelerate time to value. As privacy shifts compel deeper data engineering, demand for service-led CDP integrations and compliance audits intensifies. This dual-track dynamic is set to continue, with Services capturing incremental share, particularly among industries lacking ABM expertise.

By Deployment Model: Cloud Dominance Accelerates Integration

Cloud solutions owned 71.40% of the Account-Based Marketing market size in 2025 and advanced at 13.21% CAGR as buyers favor elastic compute, rapid feature releases, and frictionless API connections. SaaS models streamline data ingestion from CRMs, analytics suites, and ad platforms, letting marketers stand up pilots in weeks rather than quarters. Vendors such as Demandbase and 6sense now offer turnkey connectors to CDPs, marketing automation, and intent feeds, lowering integration hurdles.

On-premise deployments persist in highly regulated sectors such as financial services, where strict data-residency rules apply. Even there, hybrid architectures - local data stores paired with cloud-based orchestration layers—are gaining ground as encryption, zero-trust frameworks, and audit trails assuage security teams. Consequently, cloud’s perceived risk has fallen, and its benefits - continuous innovation, lower capex, and easier AI adoption - are widening the deployment gap.

By End-User Industry: Healthcare Accelerates While IT Leads

IT and Telecommunications maintained a 25.60% slice of the Account-Based Marketing market in 2025 by leveraging deep technographic data and purchasing committees familiar with digital collaboration. Complex enterprise sales cycles and competitive product landscapes sustain IT’s reliance on ABM to focus resources on best-fit, high-lifetime-value accounts. Meanwhile, Healthcare & Life Sciences expands at a 14.62% CAGR as pharmaceutical, medical-device, and health-technology vendors adopt account-centric tactics to reach multidisciplinary hospital and research stakeholders. Tailored playbooks that navigate compliance and clinical governance have lowered barriers to entry for ABM in these settings.

Banking, Financial Services, and Insurance stands as the second-largest industry cohort, applying ABM to guide digital-transformation deal flow and sustainable-finance offerings. Retail and E-commerce, and Manufacturing show accelerating uptake as B2B commerce platforms demand personalized buyer journeys. Collectively, these dynamics confirm that the Account-Based Marketing market has progressed from early-stage technology niches into a cross-industry growth engine.

By Organization Size: Mid-Market Adoption Accelerates Platform Evolution

Large Enterprises controlled 57.20% of the Account-Based Marketing market in 2025, pairing sophisticated data estates with multi-tier ABM strategies that span one-to-one, one-to-few, and one-to-many motions. Their budgets facilitate advanced intent sources, content personalization studios, and sales-enablement integrations. Yet Mid-sized Enterprises are the fastest climbers with a 14.25% CAGR as vendors simplify onboarding, embed best-practice playbooks, and price platforms on tiered account volumes. Lightweight orchestration features, templated reporting, and self-service analytics now allow marketing teams of limited headcount to launch ABM programs within weeks.

This democratization is steering product roadmaps toward modular capabilities that scale with organizational maturity. At the same time, Enterprises press vendors for even deeper AI predictions, custom data-lake connectors, and governing-body compliance modules. The divergent needs spur specialized product editions, reinforcing the segment-specific focus throughout the Account-Based Marketing market.

By Channel: Social Media Disrupts Display Advertising Dominance

Display Advertising kept 29.50% of ABM channel outlays in 2025 due to its breadth and mature targeting taxonomies. However, Social Media bills are climbing fastest at 15.38% CAGR as platforms like LinkedIn refine professional identity graphs that map job titles, skills, and buying responsibilities. Sponsored InMail, matched-audience retargeting, and conversation ads now deliver direct dialogue with buying committees, generating acceptance rates that often exceed 15% for strategic connection requests.

Email remains a workhorse channel because it binds nurturing workflows to CRM opportunity stages, while personalized website experiences surface differentiated value propositions to recognized visitors. Event-driven interactions—virtual roundtables, webinars, and targeted field events—continue to close late-stage opportunities by convening cross-functional stakeholders. Effective ABM programs, therefore, orchestrate sequences across paid, owned, and earned channels, relying on AI to determine optimal touchpoints and progression triggers.

Geography Analysis

North America held 40.60% of the Account-Based Marketing market size in 2025 on the strength of an advanced martech landscape, early adopter technology firms, and a concentration of ABM platform headquarters. United States enterprises pioneer CDP-ABM convergence, cookieless identity innovation, and AI-driven predictive scoring, establishing use-case blueprints for global peers. Data-privacy legislation such as California’s CCPA and sector-specific rules add complexity, yet they also spur investments in compliant data architectures, further entrenching ABM as the privacy-ready alternative to broad-target display.

Asia-Pacific is the fastest-growing territory, charting a 14.55% CAGR to 2031. Singapore, Japan, Australia, and India headline adoption, each adapting ABM to local buyer behaviors and regulatory environments. Startups capitalize on programmatic ABM to counter resource constraints and compete against multinational incumbents. Regional ad-spend reports reveal double-digit gains in mobile and social commerce, aligning perfectly with intent-driven, account-focused tactics that thrive on granular first-party engagement data. Europe ranks second by revenue share, propelled by the United Kingdom, Germany, and France, where GDPR compliance frameworks are embedded into platform feature sets. Strict lawful-basis requirements elevate the value of first-party data and authenticated audiences, positioning ABM suites that automate consent management for competitive advantage. South America and the Middle East & Africa are smaller but growing niches; Brazil and the United Arab Emirates lead regional pilots, aided by localized language support and flexible usage-based pricing. Global diffusion shows the Account-Based Marketing market transitioning from an Anglo-American paradigm to a genuinely worldwide discipline.

Competitive Landscape

The Account-Based Marketing market displays moderate concentration at the enterprise tier. Demandbase, 6sense, and Terminus collectively hold meaningful shares, leveraging proprietary intent data, orchestration engines, and AI models to serve complex global accounts. Consolidation continues: DemandScience’s November 2024 merger with Terminus joined comprehensive data assets with multichannel engagement orchestration, creating a suite capable of cradle-to-grave account nurturing. [3]MarTech, “DemandScience and Terminus Merge to Build End-to-End ABM Platform,” martech.org Mid-market and SMB layers remain fragmented, with RollWorks, HubSpot, and Influ2 competing on ease of use, rapid deployment, and pricing transparency.

Competitive differentiation now centers on three axes: depth of AI-powered insights, breadth of native data partnerships, and vertical-specific playbooks. Vendors integrate intent data providers, conversational intelligence, and ad exchanges into unified dashboards, promising faster pipeline acceleration. Disruptors like Valasys Media use behavioral AI scoring to identify micro-signals and report triple-digit engagement lifts, challenging incumbents on predictive accuracy. Meanwhile, established marketing-cloud providers bundle ABM modules into larger customer-experience suites, seeking stickier platform lock-in.

Despite intensified rivalry, white-space opportunities persist in emerging-market localization, industry-specific compliance modules, and low-touch “ABM lite” products for small businesses. Suppliers that seamlessly link marketing and revenue-operations analytics, prove attribution, and respect global privacy statutes stand to consolidate leadership as budgets migrate from traditional broad-reach tactics to account-centric orchestration.

Account Based Marketing Industry Leaders

Terminus Software, Inc.

Engagio Inc.

6sense Insights, Inc.

Uberflip

Adobe Inc. (Marketo)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Valasys Media introduced its VAIS intent-based ABM platform, reporting 40% higher first-touch conversions and 3× engagement for pilot clients.

- April 2025: UserGems compared 15 intent-data providers, stressing their growing ABM role.

- March 2025: Cognism published an enterprise ABM blueprint covering 1:many, 1:few, and 1:1 models.

- February 2025: Demandbase released a guide profiling 40 ABM tools, underscoring ecosystem expansion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the account-based marketing market as the total annual revenue earned worldwide from dedicated ABM software platforms and their paid support, integration, and advisory services that enable B2B sellers to identify, engage, and expand high-value target accounts. Revenues are tracked regardless of deployment (cloud or on-premise) and across every end-user industry and organization size.

Scope Exclusions: Generic CRM suites or ad-tech tools that lack account-level targeting functions are deliberately left outside the model.

Segmentation Overview

- By Component

- Tools

- Services

- By Deployment Model

- On-premise

- Cloud

- By End-user Industry

- Retail and E-commerce

- BFSI

- IT and Telecommunications

- Government

- Travel and Tourism

- Healthcare and Life Sciences

- Other End-user Industries

- By Organization Size

- Large Enterprises

- Mid-sized Enterprises

- Small Businesses

- By Channel

- Display Advertising

- Social Media

- Website/Personalization

- Events and Webinars

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews with ABM platform product heads, channel partners, and senior demand-generation managers across North America, Europe, and fast-growing Asia Pacific. These conversations validate spend ratios, reveal emerging buyer cohorts, and clarify assumed adoption curves that secondary sources cannot capture alone.

Desk Research

We first map the demand pool through reliable public datasets such as the Interactive Advertising Bureau's digital ad outlays, U.S. Census Service Annual Survey service receipts, Eurostat ICT spending, and IDC marketing-technology trackers. These figures are blended with insights drawn from trade bodies like the B2B Marketing Exchange, patent filings on AI-driven segmentation, and customs codes for marketing software shipments.

Next, we sample company filings, investor presentations, and product pricing sheets of listed ABM vendors, and then mine D&B Hoovers for private-firm billings, while Dow Jones Factiva feeds us real-time expansion news. Government procurement portals and tender databases flag fresh enterprise rollouts, giving early evidence of adoption waves.

The sources listed illustrate our desk research pool and are not exhaustive.

Market-Sizing & Forecasting

A top-down build begins with global B2B marketing-tech budgets, which are then filtered through verified ABM penetration rates by organization size and geography. Results are cross-checked with selective bottom-up vendor revenue roll-ups and sampled average selling price multiplied by active seat counts. Key variables like average ABM spend per target account, cloud subscription pricing trends, CRM penetration, and regional digital-ads cost per mille drive our multivariate regression forecast that projects value growth through 2030. Any bottom-up data gaps are bridged by weighted averages from primary interviews before final calibration.

Data Validation & Update Cycle

Model outputs undergo variance checks against external spending indices, peer benchmarks, and historical trend lines. Senior analysts review anomalies, and numbers are refreshed each year, with interim updates triggered by material events so clients receive the latest vetted view.

Why Mordor's Account-Based Marketing Baseline Earns Trust

Published ABM estimates often diverge because firms pick varied scopes, differing base years, and unaligned refresh cadences, creating confusion for decision-makers.

Disparity mainly stems from whether services revenue is folded in, how fast currency effects are adjusted, and the frequency with which new platform launches are captured. Mordor's disciplined scope, yearly model rebuild, and dual validation steps reduce those gaps, delivering a balanced picture users can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.03 B (2025) | Mordor Intelligence | - |

| USD 1.41 B (2024) | Global Consultancy A | Bundles programmatic media spend and uses older refresh cadence |

| USD 1.22 B (2024) | Industry Association B | Drops managed-services revenue and applies constant currency |

| USD 1.07 B (2023) | Research Publisher C | Relies on vendor survey sample without filing validation |

The comparison shows that, by selecting the right scope and validating with both market budgets and vendor filings, Mordor delivers a transparent, repeatable baseline that sits between overly aggressive and overly conservative counts, giving stakeholders dependable numbers for planning.

Key Questions Answered in the Report

How fast is the Account-Based Marketing market expected to grow?

The market is forecast to climb from USD 1.15 billion in 2026 to USD 2.02 billion by 2031, delivering a 11.94% CAGR over 2026-2031.

Which region is expanding most quickly in the Account-Based Marketing market?

Asia-Pacific leads with a projected 14.55% CAGR through 2031 as tech-savvy startups and enterprises accelerate programmatic ABM adoption.

What components of the Account-Based Marketing market are growing faster—tools or services?

Tools still dominate at 64.30% share, but Services are expanding faster at a 14.02% CAGR because companies need strategic guidance and execution support.

Why is cloud deployment preferred for ABM platforms?

Cloud solutions account for 71.40% of current spend because they enable rapid integration, continuous feature updates, and scalable processing of real-time intent data.

Which industry vertical is currently the fastest-growing ABM adopter?

Healthcare & Life Sciences is rising at a 14.62% CAGR as vendors target complex, multi-stakeholder hospital procurement processes with account-centric engagement.

Page last updated on: