Passwordless Authentication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

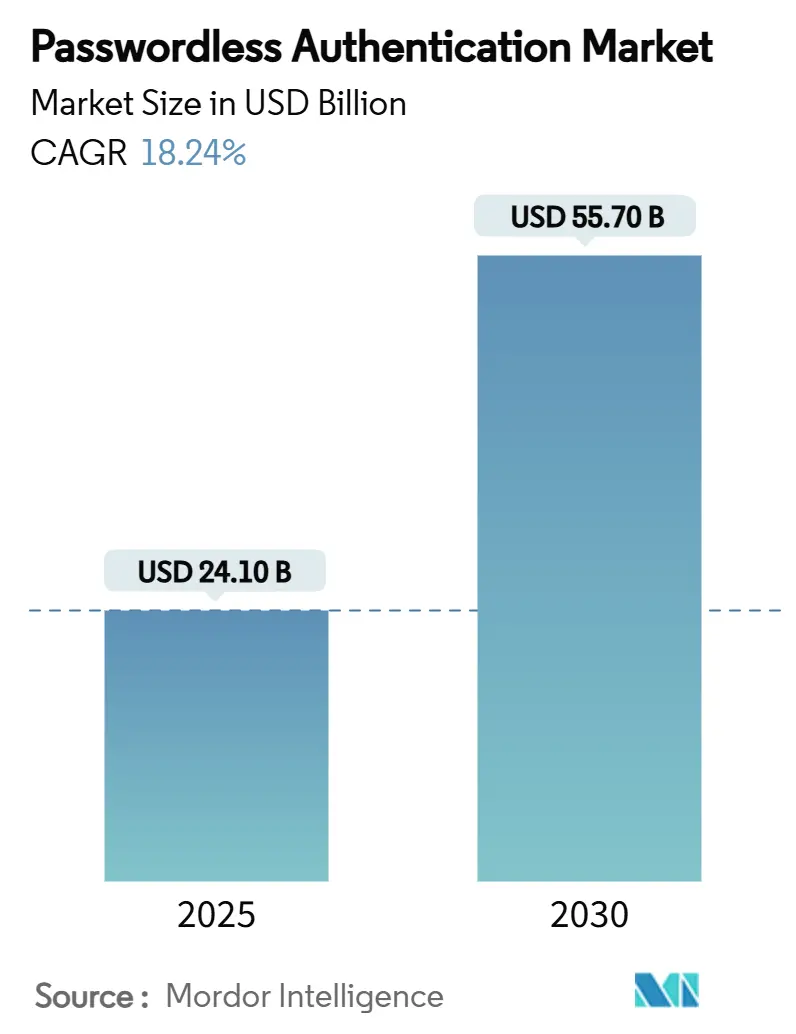

| Market Size (2025) | USD 24.10 Billion |

| Market Size (2030) | USD 55.70 Billion |

| Growth Rate (2025 - 2030) | 18.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passwordless Authentication Market Analysis by Mordor Intelligence

The Passwordless Authentication Market size is estimated at USD 24.10 billion in 2025, and is expected to reach USD 55.70 billion by 2030, at a CAGR of 18.24% during the forecast period (2025-2030). Regulatory pressure from the EU’s eIDAS 2.0 digital-wallet mandate, the U.S. federal executive order on phishing-resistant MFA, and Japan’s national digital ID roadmap pushes enterprises to replace vulnerable passwords with cryptographic credentials, making the passwordless authentication market the de facto security layer for zero-trust architectures. Software platforms still dominate value creation, yet enterprises increasingly pay for implementation expertise, signaling that project success hinges more on services than on licenses. FIDO-aligned passkeys backed by Apple, Google, and Microsoft accelerate from the consumer tier into workplace authentication, while hybrid deployment models emerge as the preferred design for organizations balancing data residency with operational agility. Competitive stakes rise as cloud hyperscalers embed passwordless authentication features natively, forcing pure-play vendors to differentiate on integration depth, hardware complementarity, and vertical specialization.

Key Report Takeaways

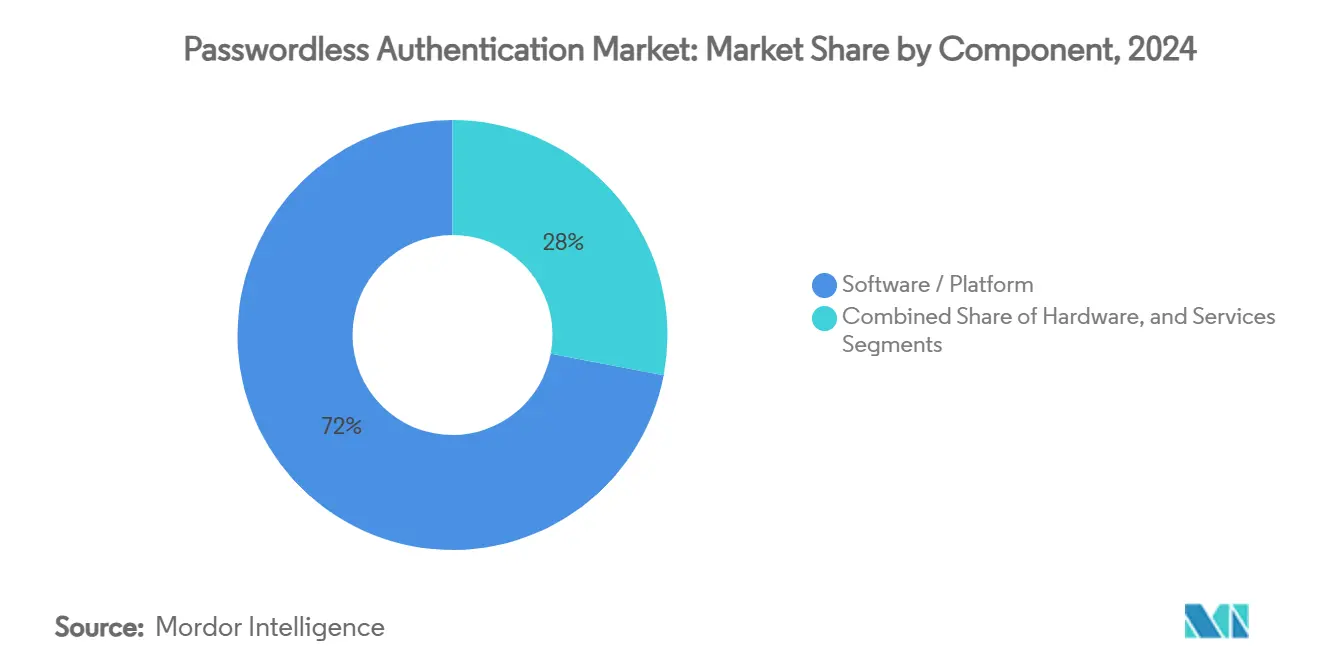

- By component, software platforms commanded 72% of the passwordless authentication market share in 2024, while the services segment is projected to expand at a 19.44% CAGR through 2030.

- By authentication method, biometrics led with 49.5% share in 2024; passkeys are on track for a 19.75% CAGR to 2030 - the fastest among all methods.

- By deployment mode, cloud accounted for 57.3% of the passwordless authentication market size in 2024, but hybrid deployments are set to grow at a 21.44% CAGR through 2030.

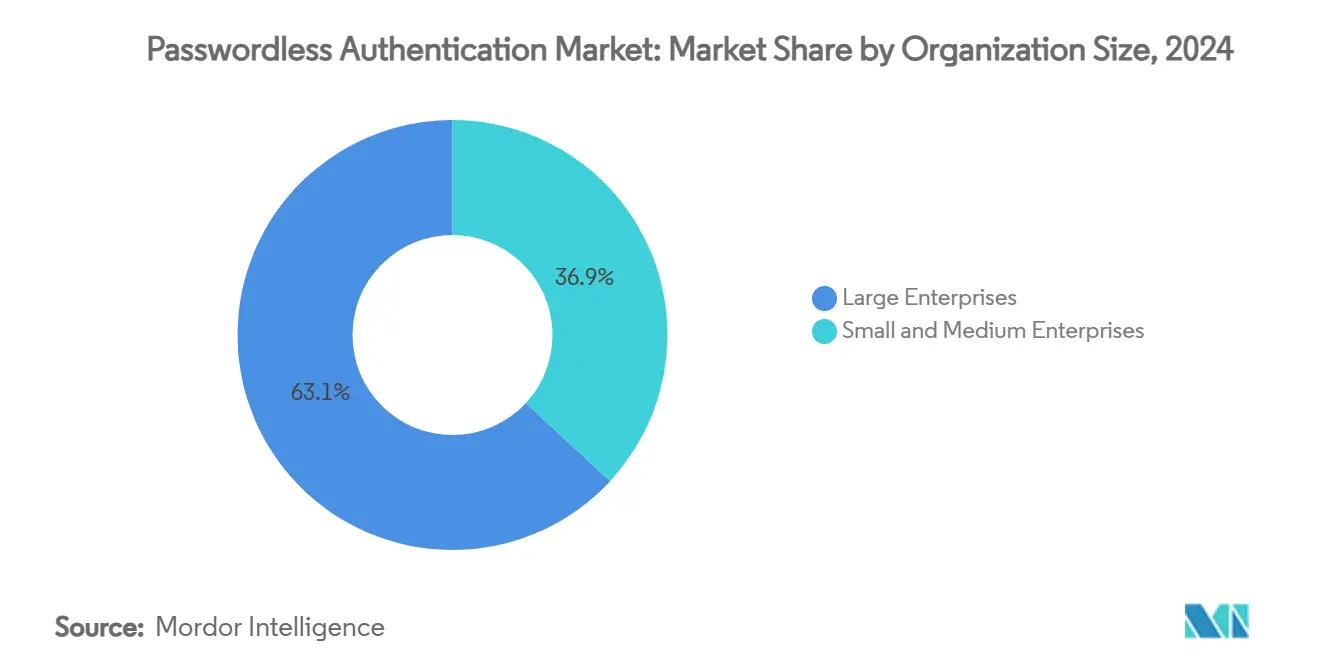

- By organization size, large enterprises held 63.1% spending in 2024, whereas SMEs will post a 20.34% CAGR to 2030 as simplified cloud offerings lower entry barriers.

- By end-user industry, financial services led at 28.4% revenue share in 2024; retail & e-commerce will record the steepest 19.54% CAGR through 2030 as customer-experience investment intensifies.

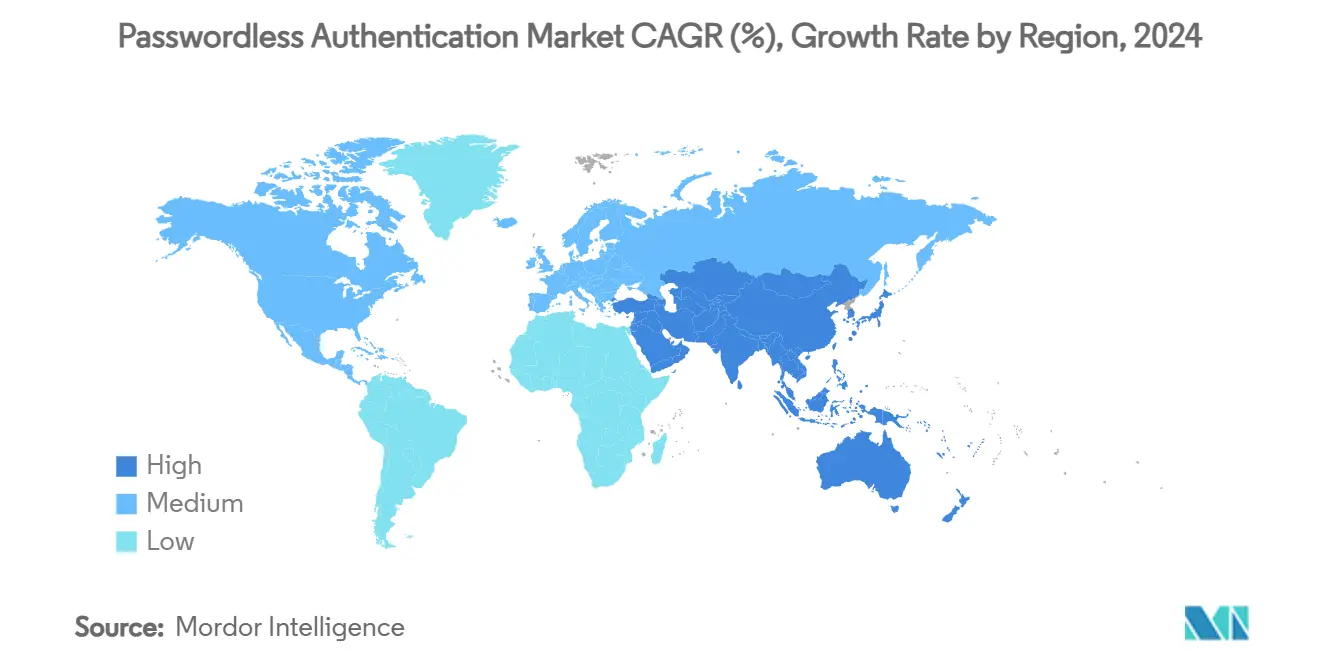

- By geography, North America represented 38.6% revenue in 2024; Asia–Pacific is projected to grow at 21.14% CAGR, driven by Japan, India, and Singapore’s digital-ID programs.

Global Passwordless Authentication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing MFA-driven compliance mandates | +3.20% | EU, North America | Medium term (2-4 years) |

| Proliferation of mobile biometrics & smartphones | +3.10% | APAC, Global | Short term (≤2 years) |

| Surge in credential-stuffing & phishing attacks | +2.80% | Financial hubs, Global | Short term (≤2 years) |

| Help-desk cost savings & UX improvement | +2.60% | North America, EU | Medium term (2-4 years) |

| Zero-trust + machine-ID convergence | +2.40% | Global enterprises | Long term (≥4 years) |

| Passkeys’ spread across consumer-IoT ecosystems | +1.90% | APAC, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing MFA-Driven Compliance Mandates

Governments now mandate phishing-resistant authentication across sectors. eIDAS 2.0 obliges all EU states to issue digital identity wallets by 2026, while the U.S. federal executive order requires agencies to adopt FIDO-compliant MFA[1] European Commission, “European Digital Identity Wallet | Shaping Europe’s Digital Future,” digital-strategy.ec.europa.eu . Financial regulators in New York and Singapore impose similar rules on privileged accounts, pushing banks to replace passwords with cryptographic keys. Aviation follow-through is visible as the TSA scales credential-screening tech to hundreds of airports[2] Security Info Watch Staff, “TSA Speeds Millions Through Airports Using Identity Verification Technology,” securityinfowatch.com . This rulemaking converts security posture gaps into board-level budget items, ensuring the passwordless authentication market receives recurring funding cycles. Beyond finance, HIPAA enforcement in healthcare drives hospitals to protect patient records with passkeys, widening demand across regulated verticals.

Proliferation of Mobile Biometrics & Smartphones

Smart-device saturation, surpassing 6.8 billion handsets, sets a ready hardware base for biometric sign-in. Apple Face ID and Android BiometricPrompt APIs package FIDO2 support, giving enterprises a turnkey path to consumer-grade usability[3] Mastercard Editorial Team, “What Is a Passkey? Here’s Your 101 on Passwordless Login,” mastercard.com . BYOD norms extend the same convenience to remote employees, lowering resistance to new log-on flows. Vendors bake adaptive risk scoring into mobile SDKs so fraudulent anomalies trigger step-up checks, mitigating deepfake threats. For APAC, where mobile predominates over PC, local banks deploy voice and selfie verification straight into super-apps, shortening onboarding time from minutes to seconds. The resulting network effect ramps market penetration without incremental hardware spending.

Surge in Credential-Stuffing & Phishing Attacks

Credential-stuffing volumes have jumped 200% year-over-year, and phishing kits now automate MFA fatigue attacks[4] David Birch, “British Airways Trial End-To-End Hands-Free Travel With Biometrics,” forbes.com . Each breach averages USD 4.5 million in losses, making password risk a measurable financial liability. Boards consequently treat passwordless rollouts as a loss-avoidance investment with a multiyear payback measurable in reduced cyber-insurance premiums. Gartner predicts that by 2026, 70% of identity-related incidents will stem from legacy password stores, further cornering CISOs into adopting passkeys for privileged-user flows and machine-to-machine API calls.

Passkeys’ Expansion Across Consumer-IoT Ecosystems

Smart-home platforms and automotive OEMs are pairing car-entry or device-pairing flows with passkeys, familiarizing consumers with credential-less sign-in. As users grow comfortable approving prompts on their phones, employers ride that learned behavior to roll out workplace passkeys with minimal training overhead. Standards bodies such as the FIDO Alliance endorse roaming-credential use across multiple devices, smoothing cross-platform adoption and reinforcing market growth over the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High migration & integration cost | -1.80% | Global, particularly SME markets | Short term (≤ 2 years) |

| Legacy application incompatibilities | -1.20% | North America & EU enterprise legacy systems | Medium term (2-4 years) |

| Data-localization rules limiting cloud auth | -0.90% | EU, China, Russia, with spillover to MEA | Medium term (2-4 years) |

| Deepfake-driven biometric spoofing risks | -0.70% | Global, concentrated in high-security sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Migration & Integration Cost

Full passwordless rollouts demand directory upgrades, FIDO server clusters, and UEM policy revamps that price small firms out of the market. Total project spend ranges from USD 0.5 million for mid-caps to USD 5 million for large multinationals, with professional services fees often triple software costs[6] 1Kosmos Research Team, “The Truth About Passwordless IAM Authentication,” 1kosmos.com . Off-the-shelf cloud offerings temper this capex, but privacy rules in some jurisdictions require on-premise attestation servers, sustaining high entry hurdles through at least 2026. Vendors have responded with phased licensing that unlocks passkey support in smaller user packs, slowly easing the restraint.

Legacy Application Incompatibilities

Mainframe and client-server apps built before WebAuthn lack hooks for public-key credentials, obliging enterprises to deploy costly proxies or rewrite code altogether[7] European Commission, “Entry Into Force of Digital Identity Regulation,” digital-strategy.ec.europa.eu . Banks bearing decades of COBOL back-ends face multiyear migration windows, causing hybrid authentication states to persist. Over time, gateway vendors are layering FIDO translation services that map passkeys to legacy SAML assertions, but until completion, integration drag shaves roughly 1.2 percentage points off the CAGR forecast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Implementation Expertise Demand

Services revenue accounted for only 28% in 2024, yet it is forecast to outpace every other component at 19.44% CAGR because enterprises realize that expertise, not software alone, unlocks ROI. Consulting partners integrate passkeys with privileged-access vaults, automate certificate life-cycle management, and deliver user-adoption campaigns that lift login-success rates above 98%. The passwordless authentication market thus shifts value from perpetual software licenses toward recurring advisory engagements and managed services subscriptions.

Software platforms still command 72% spending as identity suites from Okta and Microsoft anchor enterprise security stacks, but pricing is gravitating toward consumption-based models. Hardware tokens such as YubiKeys protect air-gapped networks and regulated sectors subject to FIPS compliance, ensuring a continued niche. Implementation services bundle these elements, reducing time-to-value and mitigating the integration restraint outlined earlier.

By Authentication Method: Passkeys Emerge as Velocity Leader

Biometrics captured a 49.5% share in 2024 on the back of ubiquitous sensors in modern phones. Their primacy underscores user preference for “look-or-touch” convenience over OTP codes. Nevertheless, passkeys are the rising star with a 19.75% CAGR, thanks to cross-platform sync that avoids hardware purchase friction. The passwordless authentication market size for passkeys is projected to exceed USD 18 billion by 2030 if the growth trajectory persists, anchoring the method as the ecosystem’s de facto standard.

Token-based FIDO2 keys retain relevance for admins and developers needing offline recovery, while push-notification MFA lingers as a stepping-stone for lagging enterprises. PKI-backed smartcards dominate defense and nuclear facilities, highlighting that method diversity will remain. Vendors increasingly bundle multiple modalities so administrators can align assurance levels with contextual risk at runtime.

By Deployment Mode: Hybrid Models Accelerate Enterprise Adoption

Cloud deployment delivered 57.3% of 2024 revenue because SaaS eliminates server upkeep and accelerates patching cadence. Yet privacy legislation plus data-residency clauses in Germany and India spur organizations to keep signing keys on-premise while consuming cloud orchestration. As a result, hybrid deployments are tracking a robust 21.44% CAGR, converting into the architecture of choice for regulated global enterprises. The passwordless authentication market share for hybrid models could surpass 40% well before 2030 if the current adoption pace holds.

Pure on-premise footprints persist in defense and highly classified R&D, but vendors now ship containerized FIDO servers that slot into Kubernetes clusters, narrowing functional gaps with SaaS. Meanwhile, cloud-first startups skip hybrid complexity, illustrating how organization maturity shapes deployment paths.

By Organization Size: SME Adoption Accelerates Through Simplified Solutions

Large enterprises accounted for 63.1% of 2024 spend as they possess the teams and budgets for enterprise-wide identity transformations. Their early uptake crowdsourced best practices later used by SaaS vendors to pre-configure templates and shrink deployment timelines for smaller customers. Consequently, SMEs are predicted to grow at a 20.34% CAGR, elevating their contribution to the overall passwordless authentication market size.

Ease-of-use improvements, subscription-tier pricing, and workflow automation remove the steep learning curve. Managed service providers (MSPs) package passwordless authentication as a bundle alongside endpoint management for less than the cost of one full-time admin, encouraging take-up across retail franchises, law firms, and regional banks.

By End-User Industry: Retail Velocity Driven by Customer Experience Optimization

SI (Banking, Financial Services, and Insurance) led adoption at 28.4% market share in 2024 because regulatory fines make two-factor evasion untenable. Their outsized share will persist, but retail and e-commerce are now the fastest movers, advancing at a 19.54% CAGR as frictionless checkout links directly to conversion rates. The passwordless authentication market size for retail applications is expected to triple by 2030 if current payment-fraud trends continue.

Healthcare leans on passkeys to satisfy HIPAA while easing clinician workload, and government agencies deploy biometric portals to support citizen services. Manufacturing unites workforce and machine identities, using passkeys inside OT zones to streamline shift changes without compromising safety protocols.

Geography Analysis

North America retained a 38.6% share in 2024 on the strength of federal mandates and deep cybersecurity budgets. U.S. agencies such as the USDA already issue FIDO tokens to 40,000 staff, creating lighthouse references that private industry emulates[8] Security Info Watch Staff, “TSA Speeds Millions Through Airports Using Identity Verification Technology,” securityinfowatch.com . Yet Asia–Pacific’s 21.14% CAGR positions it as the next billion-dollar increment for the passwordless authentication market.

Japan’s Mercari surpassed 10 million passkey users inside a single marketplace app, while India’s Aadhaar-linked e-KYC workflows enable fintechs to open accounts in under two minutes. Singapore’s Smart Nation drive embeds face-verification kiosks across government offices, showcasing public-private synergy that accelerates consumer trust. Europe remains policy-rich, funding EUR 46 million pilot projects for cross-border digital wallets under eIDAS 2.0[9] European Commission, “European Digital Identity Wallet | Shaping Europe’s Digital Future,” digital-strategy.ec.europa.eu . Latin America and the Middle East trail but gain momentum through financial-inclusion programs and energy-sector modernization, respectively.

North America’s leadership rests on early regulatory action and public-sector exemplars that de-risk vendor selection for private buyers. High breach-remediation costs coupled with cyber-insurance clauses that reward phishing-resistant MFA keep adoption budgets intact. U.S. cloud providers further cement dominance by bundling passkey APIs into developer toolchains, ensuring continuous reinforcement of the regional ecosystem.

Asia–Pacific presents the highest runway owing to massive mobile-internet penetration and proactive government backing. Japanese enterprises transition from physical badges to phone-based passkeys; Indian banks fold FIDO authentication into UPI payments to curb OTP fraud. The region’s youth-skewed demographics favor biometric sign-in, translating cultural comfort into enterprise acceptance at scale.

Europe’s growth hinges on harmonized regulation. eIDAS 2.0 unlocks cross-border service portability, compelling multinational banks and insurers to standardize on FIDO2 credentials across subsidiaries. Germany’s BSI endorses passkeys for critical infrastructure staff, while French public services embed biometric login into healthcare portals. Privacy concerns shape vendor roadmaps toward on-premise key storage and open-source attestation libraries.

Competitive Landscape

The passwordless authentication market is moderately fragmented. Platform suites from Microsoft, Okta, and Ping Identity bundle SSO, governance, and passkey orchestration in one license, leveraging existing account footprints for upsell. Specialized players such as HYPR, Yubico, and 1Kosmos carve niches in high-assurance or hardware-centric deployments, partnering with integrators to win regulated verticals. Traditional MFA vendors retrofit WebAuthn, avoiding irrelevance, while cloud hyperscalers expose passkey APIs free of charge to fortify stickiness.

Strategic patterns tilt toward consolidation. Consensys’ acquisition of Web3Auth extended MetaMask into passwordless territory, signaling blockchain wallets’ convergence with enterprise identity. ColorTokens’ purchase of PureID added FIDO validators to its zero-trust mesh, illustrating horizontal security-platform expansion. Technology differentiation revolves around phishing-resistant UX, AI-powered risk signals, and silicon-rooted keys. Vendors able to prove fast-track integrations with legacy HR and VPN stacks secure larger total-contract values.

Channel alliances rise in importance: 1Kosmos’ USD 194.5 million Login.gov award via Carahsoft demonstrates that public-sector contract vehicles can swing market share rapidly. Hardware providers strike bundling deals with endpoint-management suites to widen reach beyond security admins. The race now centers on embedding passwordless capabilities into every digital touchpoint, from developer command lines to consumer e-commerce carts.

Passwordless Authentication Industry Leaders

Microsoft Corporation

Okta Inc.

Cisco Systems, Inc. (Duo Security)

Ping Identity Holding Corp.

Thales Group (Gemalto)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The FIDO Alliance celebrated World Passkey Day, showcasing new government case studies to spur wider standard adoption; vendors leveraged the event to unveil SDK upgrades that shorten implementation sprints.

- June 2025: British Airways extended hands-free biometric travel trials across additional routes, signaling transportation’s shift to frictionless identity to reclaim passenger throughput.

- May 2025: The European Commission launched the EU Digital Identity Wallet framework with EUR 46 million pilot funding, anchoring regulatory certainty that compels vendors to localize passkey storage.

- March 2025: NEC deployed facial-recognition passkeys to 20,000 employees, validating large-scale enterprise rollouts and seeding regional reference wins.

- January 2025: 1Kosmos secured a USD 194.5 million Login.gov contract via Carahsoft, accelerating federal market capture and strengthening public-sector credibility.

Global Passwordless Authentication Market Report Scope

| Hardware |

| Software / Platform |

| Services |

| Biometrics |

| Token-Based / FIDO2 Security Keys |

| OTP-less Push Notification |

| PKI / Certificate-Based |

| Magic-Link Email |

| Passkeys |

| On-Premises |

| Cloud |

| Hybrid |

| Small & Medium Enterprises |

| Large Enterprises |

| BFSI |

| IT & Telecom |

| Healthcare |

| Government & Defense |

| Retail & E-commerce |

| Education |

| Manufacturing |

| Others (Transport, Energy, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Qatar | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software / Platform | |||

| Services | |||

| By Authentication Method | Biometrics | ||

| Token-Based / FIDO2 Security Keys | |||

| OTP-less Push Notification | |||

| PKI / Certificate-Based | |||

| Magic-Link Email | |||

| Passkeys | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Small & Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | BFSI | ||

| IT & Telecom | |||

| Healthcare | |||

| Government & Defense | |||

| Retail & E-commerce | |||

| Education | |||

| Manufacturing | |||

| Others (Transport, Energy, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Israel | |||

| Qatar | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected CAGR for the passwordless authentication market from 2025 to 2030?

The market is forecast to rise at an 18.24% CAGR over the period, growing from USD 24.1 billion in 2025 to USD 55.7 billion in 2030.

Which component segment is expanding the fastest in passwordless authentication deployments?

Professional services are advancing at a 19.44% CAGR as enterprises seek integration expertise and change-management support.

Why are passkeys gaining momentum compared with other authentication methods?

Passkeys follow FIDO standards and sync across Apple, Google, and Microsoft ecosystems, driving a 19.75% CAGR that outpaces biometrics, tokens, and OTP-less push notifications.

What primary regulatory mandate is accelerating passwordless adoption in Europe?

The EU eIDAS 2.0 framework requires member states to issue digital identity wallets by 2026, making phishing-resistant authentication a legal necessity.

How do passwordless solutions improve operational efficiency for enterprises?

Eliminating password resets removes 20–30% of help-desk tickets, cutting support costs while boosting employee productivity and user satisfaction.

Page last updated on: