E-Signature Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

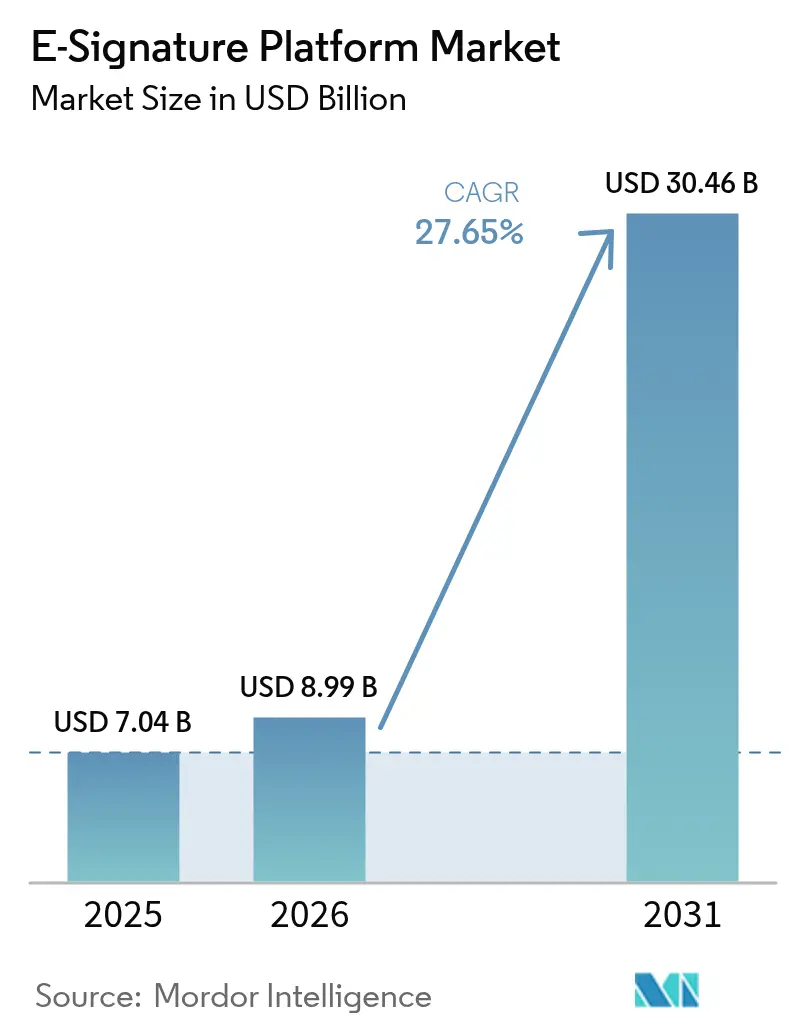

| Market Size (2026) | USD 8.99 Billion |

| Market Size (2031) | USD 30.46 Billion |

| Growth Rate (2026 - 2031) | 27.65% CAGR |

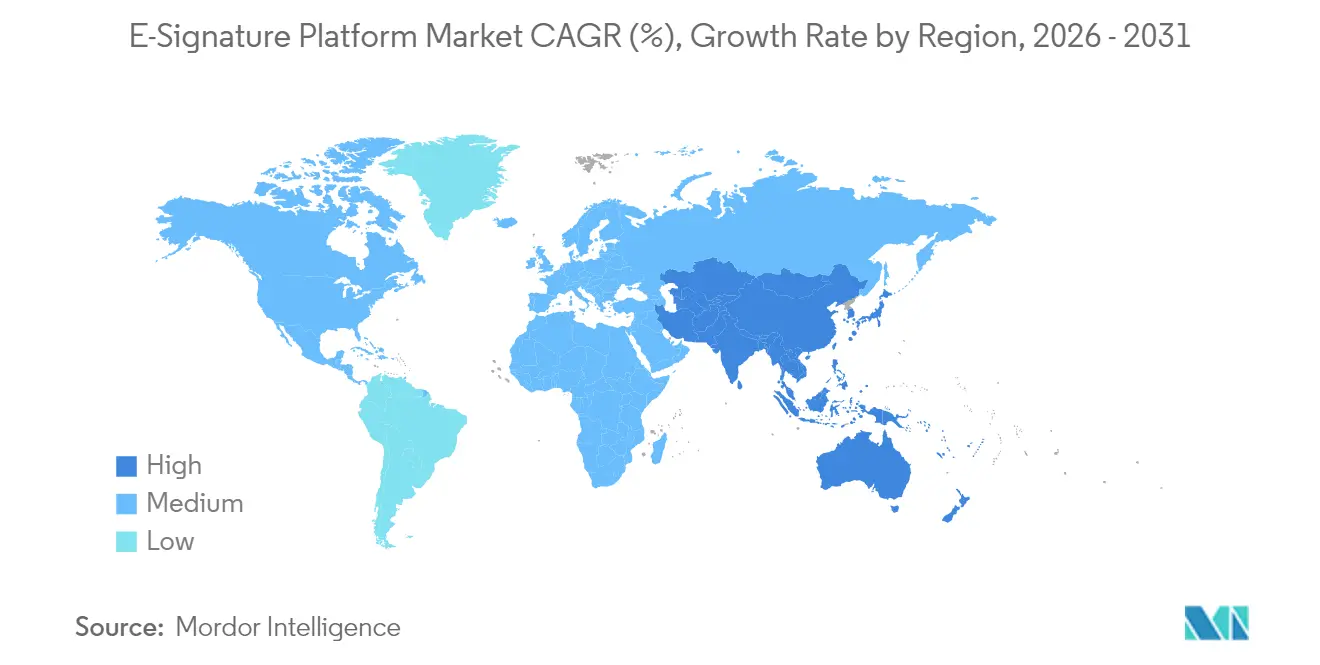

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-Signature Platform Market Analysis by Mordor Intelligence

E-Signature platform market size in 2026 is estimated at USD 8.99 billion, growing from 2025 value of USD 7.04 billion with 2031 projections showing USD 30.46 billion, growing at 27.65% CAGR over 2026-2031. Strong demand for agreement-intelligent ecosystems, harmonized regulations such as eIDAS 2.0 and an expanding pool of cloud-native integrations continue to accelerate global adoption. Vendors that embed AI-powered risk analysis and quantum-safe encryption into their offerings win enterprise preference, while SMEs flock to subscription packages that remove infrastructure overhead. Regulatory mandates in North America and Asia Pacific, coupled with ESG-driven paperless goals, anchor multi-region growth opportunities. Competitive intensity rises as platform providers move upstream into contract lifecycle management and downstream into vertical SaaS, pushing incumbents toward selective M&A and developer-centric partner programs.

Key Report Takeaways

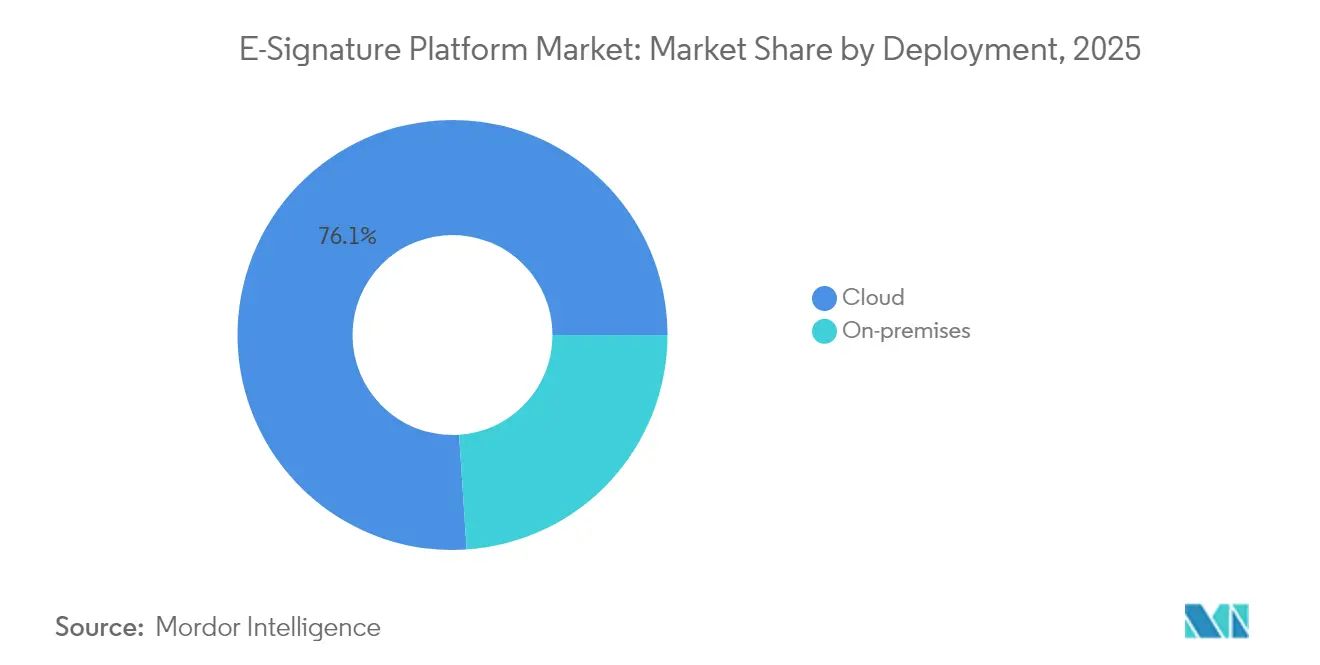

- By deployment, cloud infrastructure led with 76.05% of E-Signature platform market share in 2025; on-premises and hybrid models lag but cloud is expanding at a 29.10% CAGR through 2031.

- By organization size, large enterprises accounted for 62.10% of the E-Signature platform market size in 2025, while SMEs are growing the fastest at 28.75% CAGR to 2031.

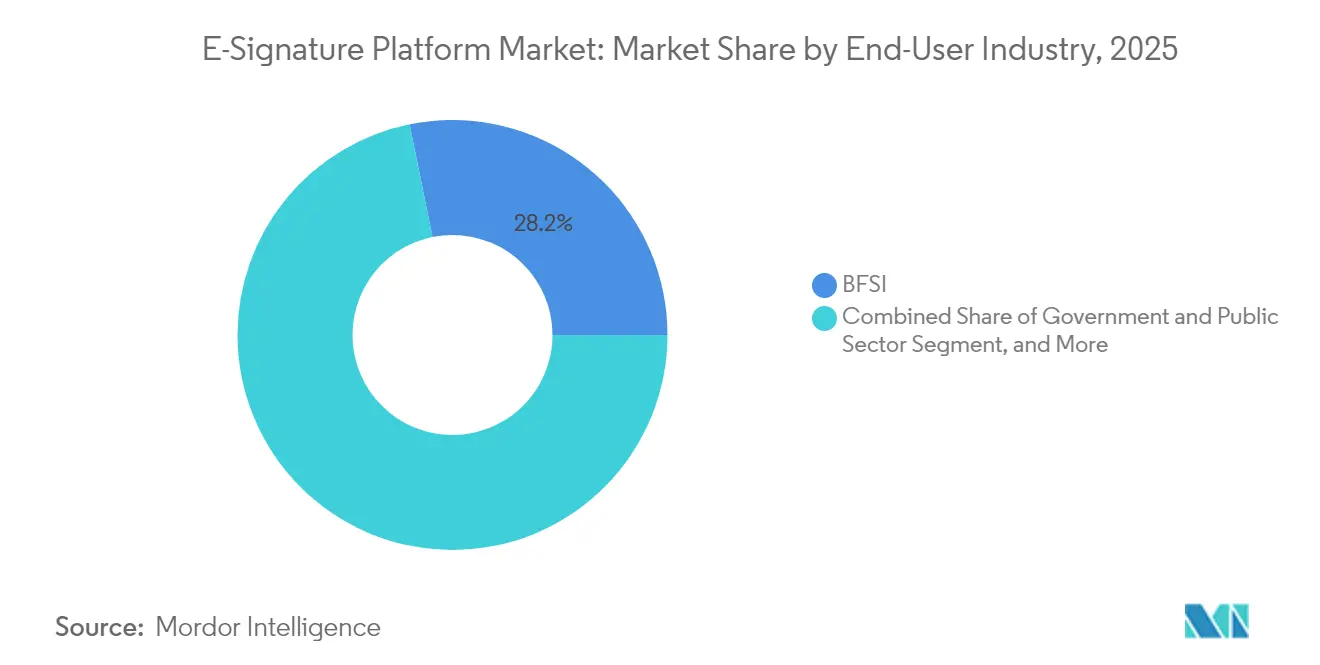

- By end-user industry, healthcare and life sciences is advancing at a 28.05% CAGR through 2031 in the E-Signature platform market, outpacing all other sectors. Whereas BFSI retained 28.20% share in 2025.

- By authentication level, qualified electronic signatures are the fastest riser at 28.60% CAGR in the E-Signature platform market, whereas simple electronic signatures retained 48.10% share in 2025.

- By geography, North America held 37.20% revenue in 2025 in the E-Signature platform market; Asia Pacific is projected to register a 28.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-Signature Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote work and distributed deal-making | +6.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cloud-first adoption among SMEs | +5.4% | Global, strongest in Asia Pacific and South America | Short term (≤ 2 years) |

| Global regulatory backing (eIDAS 2.0, UETA, etc.) | +7.2% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Embedded signature APIs in vertical SaaS | +4.9% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Quantum-resistant crypto roadmaps | +2.1% | Global, led by government and enterprise sectors | Long term (≥ 4 years) |

| ESG-driven paperless mandates | +3.8% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Remote Work and Distributed Deal-Making

Hybrid work models now dominate white-collar employment, forcing organizations to finalize agreements across locations and time zones without physical presence. Modern platforms therefore support real-time co-authoring, multi-stakeholder routing and AI-enabled clause risk surfacing inside collaboration suites such as Microsoft 365.[1]Erika Sperekas, “AI-Powered Agreement Insights With Microsoft 365 Copilot,” DOCUSIGN.COM Government agencies also leverage these capabilities to satisfy procurement audit requirements while accelerating award cycles. As a result, signatures shift from a final checkpoint to the orchestration layer for complex, many-party decision flows. Vendors that integrate seamlessly with email, video conferencing and content repositories reduce context switching and shorten revenue recognition timelines.

Cloud-First Adoption Among SMEs

SMEs increasingly bypass on-premises infrastructure by choosing SaaS packages that embed signatures into accounting, CRM, and HR tools. OECD research shows U.S. small-firm usage of advanced digital solutions jumped from 45% in 2020 to 69% in 2024. Pay-as-you-go pricing, mobile-native experiences, and sector-specific templates widen accessibility, evidenced by Signeasy’s NPS above 70 and App Store recognition.[2]Sunil Patro, “Signeasy 2024: Milestones and Vision,” SIGNEASY.COMVendors capturing this cohort emphasize simplified onboarding, marketplace connectors, and transparent usage tiers, enabling SMEs to scale transaction volumes without IT intervention.

Global Regulatory Backing (eIDAS 2.0, UETA, etc.)

Unified legal frameworks remove cross-border uncertainty and elevate electronic signatures to equal footing with wet ink. Under eIDAS 2.0, a qualified signature issued in one EU state is enforceable in all 27, while U.S. agencies must embed signatures in citizen-facing services within 180 days of the M-23-22 memo. Singapore and Japan have enacted similar mandates, triggering platform upgrades that integrate national identity schemes and tamper-evident audit trails. Enterprises consequently standardize on solutions covering multiple jurisdictions, lowering expansion friction and compliance overhead.

Embedded Signature APIs in Vertical SaaS

Industry-specific software increasingly bundles signature APIs to deliver frictionless user journeys. Salesforce’s AgentExchange allows AI agents to generate, route and archive contracts end-to-end within CRM records. Healthcare EHR vendors now include e-consent modules that preserve HIPAA compliance without external redirects. Platforms with robust SDKs, white-label options and granular permissioning become default infrastructure for vertical providers, expanding total addressable transactions beyond standalone tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-breach and fraud concerns | -4.2% | Global, particularly acute in financial services | Short term (≤ 2 years) |

| Cross-border legal fragmentation | -3.1% | Global, most complex in emerging markets | Medium term (2-4 years) |

| High QES transaction fees | -2.8% | Europe and regulated industries globally | Medium term (2-4 years) |

| Energy scrutiny of blockchain stamping | -1.5% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Breach and Fraud Concerns

Phishing campaigns that mimic legitimate signature requests undermine user trust, compelling enterprises to introduce multi-factor authentication and out-of-band verification that slow workflows. Breaches at well-known providers generate sector-wide caution, particularly in finance and healthcare where penalties for data loss remain severe. Platforms respond by layering machine-learning fraud detection, device fingerprinting and detailed signer analytics, while user-awareness training becomes a staple of onboarding packages. Balancing security with frictionless user experience remains an immediate industry challenge.

Cross-Border Legal Fragmentation

Despite headline harmonization, nuanced differences persist across jurisdictions regarding identity proofing, certificate hierarchy and evidentiary requirements. Multinationals often must operate multiple tenant instances or secure country-specific approvals, adding cost and governance complexity. In emerging markets, evolving statutes and limited case law raise enforceability questions, delaying large-scale rollouts. Vendors with in-house legal teams and adaptive policy engines can turn this hurdle into a competitive differentiator, but smaller entrants face steep compliance burdens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Infrastructure Drives Market Evolution

Cloud deployment held 76.05% of the E-Signature platform market share in 2025 and is projected to expand at a 29.10% CAGR through 2031. Consumption-based pricing and instant scalability make cloud the default choice for enterprises seeking AI-powered search, continuous security patching and low-latency global access. The E-Signature platform market size linked to on-premises models remains relevant for defense, healthcare and public-sector workloads that must retain sensitive data within sovereign boundaries. Even here, hybrid strategies emerge: document storage stays local while orchestration logic runs in cloud regions certified under FedRAMP or ISO 27001. Vendors differentiate by offering regionally isolated data centers and zero-knowledge encryption, satisfying both agility and sovereignty requirements.

SMEs benefit disproportionately, leveraging cloud dashboards that consolidate templates, signer status and analytics into a single pane of glass. Service providers push automated backup, uptime SLAs and API usage meters, reducing back-office strain. Conversely, cost predictability raises scrutiny among high-transaction enterprises; advanced tiering options and reserved-volume discounts therefore surface in long-term contracts. As integrations proliferate across CRM, ERP and vertical SaaS, cloud platforms positioned as central trust fabrics stand to capture incremental value per agreement.

By Organization Size: SME Adoption Accelerates Digital Transformation

Large enterprises provided 62.10% of 2025 revenue, reflecting complex contract portfolios, multi-language templates and stringent audit requirements. They adopt end-to-end agreement clouds that integrate with SAP, Oracle and ServiceNow workflows, enabling version control, AI clause comparison and risk dashboards. Yet transaction growth is fastest among SMEs, which post a 28.75% CAGR through 2031 as they leapfrog legacy processes. Easy setup, pre-built connectors to QuickBooks and HubSpot, and mobile-optimized signer journeys remove barriers once faced by resource-constrained firms.

For SMEs, templates covering NDAs, purchase orders and HR forms reduce legal spend and accelerate cash flow. Platform providers that bundle identity verification credits and offer community support forums capture loyalty. Meanwhile, large enterprises negotiate enterprise-wide licenses, custom SLA metrics and localized data residency addenda, creating high-margin accounts. Across both cohorts, embedded analytics reveal cycle-time bottlenecks, empowering managers to benchmark performance and justify further automation investment.

By End-User Industry: Healthcare Leads Digital Transformation

Healthcare and life sciences is slated to contribute the highest incremental revenue, growing at 28.05% CAGR as telehealth, e-consent and decentralized clinical trials demand HIPAA-compliant workflows. The E-Signature platform market size tied to healthcare agreements is projected to surge as hospitals digitize admission packets, pharmacies capture remote prescriptions and labs automate test authorizations. Platforms winning in this arena bundle tamper-evident audit trails, FHIR API connectors and granular access controls for multi-disciplinary care teams.

BFSI remains a core vertical, automating mortgage closings, policy renewals, and wealth management onboarding under strict KYC mandates. Government agencies accelerate procurement and citizen-service digitization, guided by federal memos that call for digital-first interactions. Manufacturing and automotive firms attach signatures to quality certificates and supply-chain documents, while real-estate portals embed them into remote closing portals. Each sector influences product road-maps: healthcare prioritizes secure patient identity matching, whereas BFSI concentrates on sanctions screening and transaction-level fraud analytics.

By Authentication Level: Security Requirements Drive QES Growth

Simple electronic signatures captured 48.10% share in 2025, maintaining appeal for internal approvals and low-risk agreements. However, qualified electronic signatures record the fastest 28.60% CAGR, buoyed by transactions requiring non-repudiation, loan disbursements, cross-border mergers, and government grants. The E-Signature platform market size for QES solutions accelerates further as EU regulators enforce remote identification prerequisites and notarization equivalence. Vendors respond with one-click upgrade paths: the same interface prompts users to step up from SES to AES or QES based on risk scoring.

Advanced electronic signatures fill the middle ground, often selected by SaaS providers that need elevated assurance without hardware tokens. Platforms offering flexible policy engines enable administrators to bind risk rules to signer geography, document type, and deal value, ensuring the right assurance level without maintaining multiple tools. Post-quantum algorithms, already piloted in qualified certificates, future-proof high-value archives against cryptographic obsolescence.

Geography Analysis

North America generated 37.20% of 2025 revenue, propelled by U.S. federal mandates that every agency deliver digital-first citizen services incorporating electronic signatures within 180 days. The Office of Management and Budget’s directive drives volume spikes in defense, health and treasury departments, while Canadian authorities mirror policies to speed benefit administration. High cloud maturity and clear case law make procurement straightforward, enabling vendors to upsell AI add-ons and industry modules.

Asia-Pacific posts the highest 28.55% CAGR through 2031, as Singapore’s 2025 authentication requirement, Japan’s AI-contract alliances and India’s Aadhaar-based e-KYC fuels rapid onboarding. SMEs across Southeast Asia adopt mobile-first bundles that cater to multilingual staff and require minimal bandwidth. Chinese and South Korean enterprises invest in quantum-safe trials, seeking long-term compliance with anticipated cybersecurity statutes. Regulatory fragmentation persists, but regional governments increasingly reference international standards, reducing contract-enforcement ambiguity.

Europe leverages eIDAS 2.0 to harmonize recognition, stimulating cross-border B2B trade and public-sector implementations. Data-sovereignty concerns shape vendor selection, with buyers demanding EU-hosted environments and GDPR-compliant processing. Latin America gains momentum after Zucchetti’s USD 32 million acquisition of Brazil-based D4Sign, signaling investor confidence and ushering in localized payment integrations. The Middle East and Africa trail in absolute spend yet display strong green-field potential where government digitization and fintech growth intersect with mobile penetration.

Competitive Landscape

Top Companies in E-Signature Platform Market

The E-Signature platform market shows moderate concentration: the top five players collectively hold roughly 60% of global revenue. DocuSign extends beyond signatures into AI clause extraction, releasing its Intelligent Agreement Management upgrade and Copilot integration for Microsoft 365. Adobe Responds with tighter Creative Cloud and Acrobat synergies, while Microsoft scales SharePoint eSignature to additional regions.[3]Amcdonnell, “SharePoint eSignature Product Updates,” MICROSOFT.COM

Strategic acquisitions reshape regional footprints. Visma’s USD 21.4 million purchase of Penneo enlarges Nordic KYC and audit capabilities.[4]Visma Newsroom, “Visma’s Offer for Penneo,” VISMA.COM Zucchetti’s take-over of D4Sign secures a Latin American customer base that exceeds 35,000 companies. Such deals underscore a pivot toward vertical integration, bundling invoices, identity verification and compliance reporting into a unified stack.

Emerging challengers prioritize industry-specific depth: LegalOn collaborates with DocuSign to pair AI contract review with signing workflows in Japan. Signeasy targets SMEs with mobile-first simplicity, leveraging App Store accolades to bolster brand trust. Quantum-resistant pilots, open API ecosystems and consumption-based pricing remain differentiators as procurement teams weigh total-cost-of-ownership against long-term security assurances.

E-Signature Platform Industry Leaders

DocuSign Inc.

Zoho Corporation Pvt. Ltd

Adobe Inc.

PandaDoc Inc.

SignEasy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Salesforce launched AgentExchange, enabling autonomous AI agents to complete contract workflows in partnership with DocuSign.

- January 2025: Visma finalized its acquisition of Penneo for approximately USD 21.4 million, deepening Nordic digital-signing capabilities.

- November 2024: Zucchetti acquired Brazil’s D4Sign for USD 32 million, expanding its Latin American presence.

- November 2024: LegalOn and DocuSign announced a fully integrated offering for the Japanese market.

Global E-Signature Platform Market Report Scope

An electronic signature solution is designed to support various business needs. It is an electronic sound, symbol, or process attached to, or associated with, a contract or other record and adopted by a person with the intent to sign a record. It is a digital form of a wet ink signature that is legally binding and secure, but it does not incorporate any encryption standards. E-signature can be less secure and less authentic than a digital signature, but it still has legal validity and enforceability.

The e-signature platform market is segmented by deployment (on-premise, cloud), organization size (small and medium enterprise, large enterprise), end-user industry (BFSI, government and defense, healthcare, oil and gas, IT and telecom, logistics and transportation, other end-user industries), and geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Italy, Rest of Europe), Asia-Pacific (China, Japan, South Korea, Rest of Asia-Pacific), Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Cloud |

| On-premises |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| IT and Telecom |

| Logistics and Transportation |

| Manufacturing and Automotive |

| Real Estate and Construction |

| Other End-User Industries |

| Simple Electronic Signature (SES) |

| Advanced Electronic Signature (AES) |

| Qualified Electronic Signature (QES) |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment | Cloud | ||

| On-premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | BFSI | ||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Logistics and Transportation | |||

| Manufacturing and Automotive | |||

| Real Estate and Construction | |||

| Other End-User Industries | |||

| By Authentication Level | Simple Electronic Signature (SES) | ||

| Advanced Electronic Signature (AES) | |||

| Qualified Electronic Signature (QES) | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What growth rate is predicted for the E-Signature platform market through 2031?

The market is projected to expand at a 27.65% CAGR, rising from USD 7.04 billion in 2025 to USD 30.46 billion by 2031.

Which deployment model currently dominates global adoption?

Cloud deployment held 76.05% share in 2025 and continues to grow fastest due to low infrastructure overhead and rapid scalability.

Why is healthcare the fastest-growing vertical for e-signatures?

HIPAA compliance, telemedicine workflows and decentralized clinical trials are driving a 28.05% CAGR for healthcare and life sciences.

What regions present the strongest near-term expansion potential?

Asia Pacific leads with a 28.55% CAGR, supported by Singapore’s 2025 authentication mandate and Japan’s AI-contract alliances.

How are vendors addressing post-quantum security threats?

Leading platforms pilot ML-DSA certificates aligned with NIST FIPS 204, ensuring long-term validity against quantum decryption risks.

Page last updated on: