Tokenization Solution Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

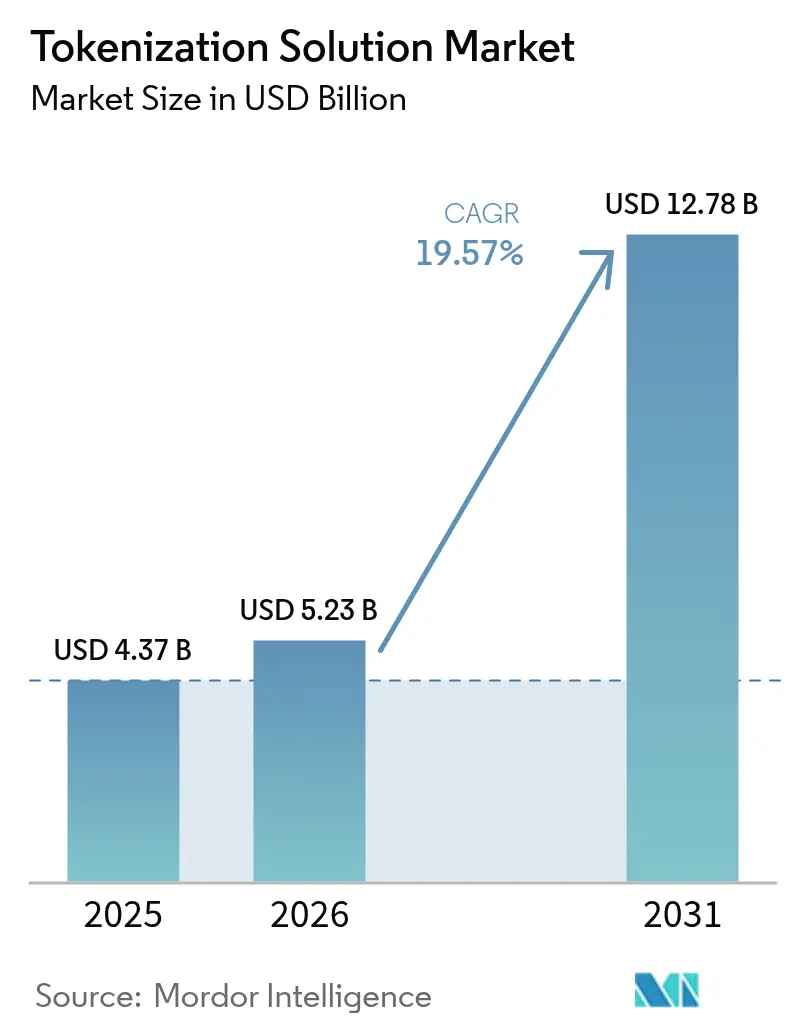

| Market Size (2026) | USD 5.23 Billion |

| Market Size (2031) | USD 12.78 Billion |

| Growth Rate (2026 - 2031) | 19.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tokenization Solution Market Analysis by Mordor Intelligence

The tokenization solution market size is expected to grow from USD 4.37 billion in 2025 to USD 5.23 billion in 2026 and is forecast to reach USD 12.78 billion by 2031 at 19.57% CAGR over 2026-2031. Investment momentum stems from widespread digital-first commerce, stricter payment security mandates, and rapid shifts toward cloud-native infrastructure. Mandatory PCI DSS 4.0 timelines, especially in the United States and Canada, have compelled enterprises to prioritise token vault modernisation or vaultless migration, compressing decision cycles and accelerating deployments. Converging regulatory urgency with the promise of operational agility positions the tokenization solution market as a cornerstone of next-generation payment architecture. At a geographic level, North America accounts for 39% of 2024 revenue, yet Asia Pacific is compounding fastest on the back of mobile wallet ubiquity and government-backed real-time payment rails. Competitive intensity is rising as fintechs pioneer vaultless designs and large processors embed network tokenisation directly into issuer services.

Key Report Takeaways

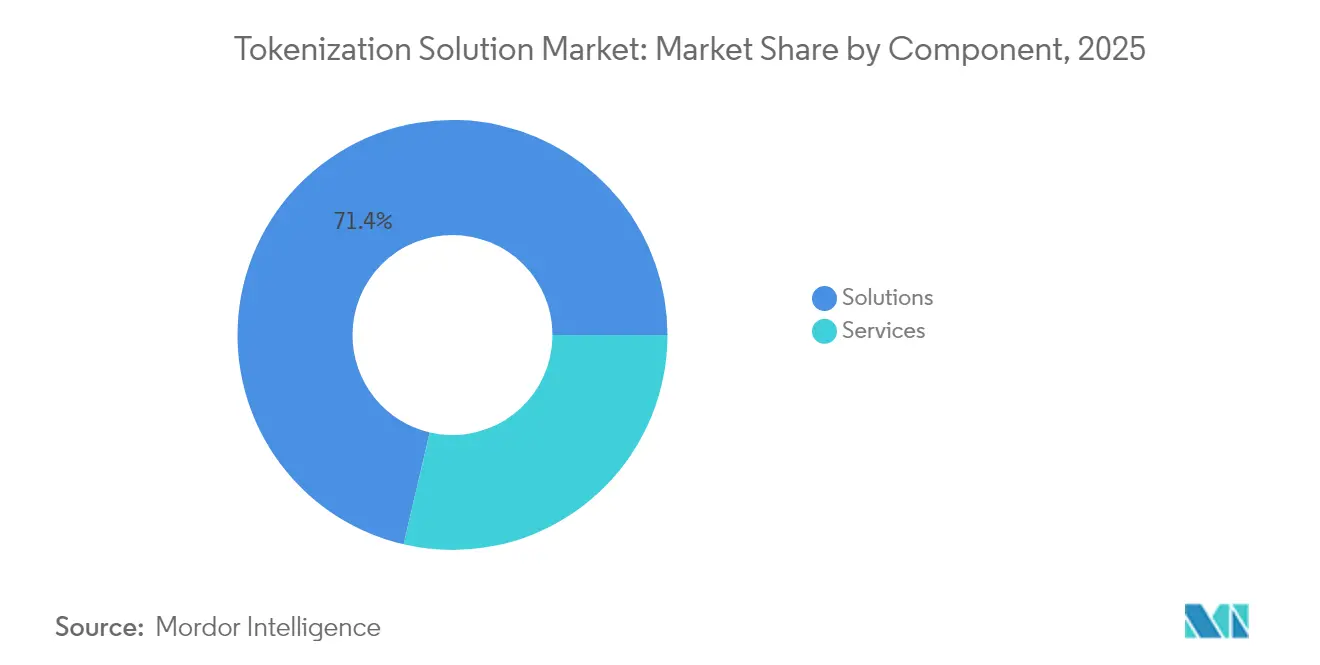

- By component, solutions led with 71.35% revenue share in 2025; services are projected to expand at a 20.35% CAGR to 2031.

- By deployment mode, cloud captured 63.10% of the tokenization solution market share in 2025, while hybrid cloud yields the highest forecast CAGR at 20.90% through 2031.

- By tokenisation technique, vaultless approaches commanded 57.40% share of the tokenization solution market size in 2025 and are poised to grow at 22.70% CAGR.

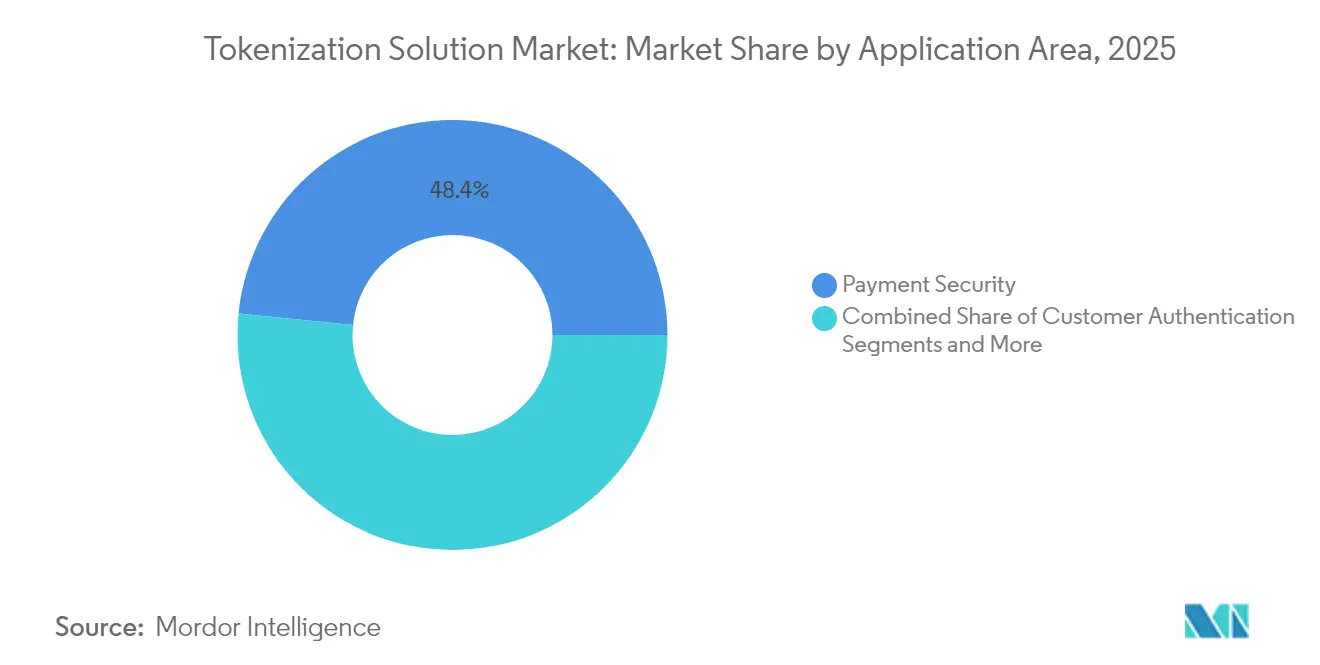

- By application, payment security held 48.40% revenue share in 2025; fraud prevention is tracking the fastest growth at 22.55% CAGR to 2031.

- By end-user, BFSI dominated with 27.70% share in 2025, whereas retail and e-commerce are expected to post a 21.95% CAGR through 2031.

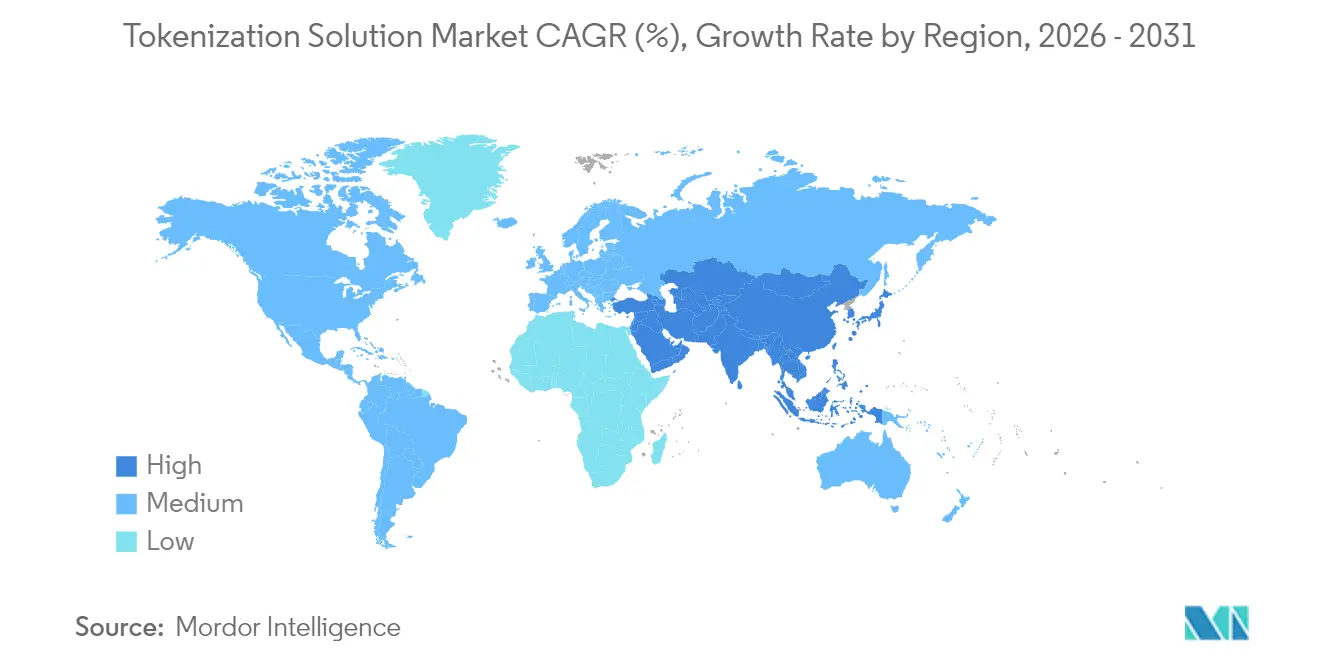

- By geography, North America retained 38.60% share in 2025; Asia Pacific is forecast to deliver a 19.95% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tokenization Solution Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Tokenization Adoption for Contactless & Mobile Wallet Payments in Asia | +3.0% | Asia Pacific, with spillover to MEA | Medium term (2-4 years) |

| Mandatory PCI DSS 4.0 Compliance Deadlines Boosting Tokenization Investments in North America | +2.4% | North America & EU | Short term (≤ 2 years) |

| Rising Fraud Losses in Card-Not-Present Transactions Driving Vaultless Tokenization Uptake in Europe | +2.0% | Europe, with expansion to global markets | Medium term (2-4 years) |

| Expansion of "Buy Now Pay Later" Platforms Demanding Tokenized Credentials Integration | +1.6% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Emergence of Network Tokenization Programs by Card Schemes Accelerating Merchant Enrolment | +1.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Tokenisation Adoption for Contactless & Mobile Wallet Payments in Asia

Mobile payment transactions in Asia Pacific more than doubled year-on-year in early 2024, drawing tokenisation into the region’s core payments stack. Japan’s plan for a joint ASEAN QR network by fiscal 2025, covering 2 million domestic merchants, showcases the scale at which cross-wallet interoperability now depends on network tokens. China’s mobile payment throughput, projected above CNY 1,100 trillion by 2029, relies on tokenised credentials to secure super-app ecosystems. With Japan’s cashless ratio topping 39.3% in 2024, regional policy targets drive merchants toward tokenisation as a precondition for subsidy eligibility. [1]Daiwa Institute of Research, "Current status and outlook for cashless payments", dir.co.jp This network effect compels global processors to deepen Asian partnerships to retain addressable volume.

Mandatory PCI DSS 4.0 Compliance Deadlines Boosting Tokenisation Investments in North America

PCI DSS 4.0 elevates cardholder-data obligations, making tokenisation the quickest path to scope reduction and audit-cost containment. Enterprises that tokenise sensitive fields can quarantine fewer systems under annual assessment, freeing security budgets for proactive threat-hunting and zero-trust initiatives. Continuous-monitoring clauses in the new standard align with real-time analytics embedded in modern token platforms, allowing boards to evidence compliance on demand. Cloud-delivered tokenisation services further compress deployment timelines, accelerating time-to-value for omnichannel retailers and fintech issuers.

Rising Fraud Losses in Card-Not-Present Transactions Driving Vaultless Tokenisation Uptake in Europe

Card-not-present fraud now represents the fastest-growing European loss category. Vaultless tokenisation mitigates this exposure by generating cryptographic tokens without a central vault, eliminating attractive breach targets. Alignment with EMV’s 2024 token standards assures scheme-level interoperability, simplifying acceptance for high-volume e-commerce merchants. Financial institutions report quicker authorisation and lower false declines once vaultless models feed richer behavioural signals into risk engines.

Expansion of BNPL Platforms Demanding Tokenised Credentials Integration

BNPL orchestration multiplies payment endpoints, each liable for token lifecycle management. Marqeta Flex illustrates how embedded tokens allow consumers to select installment plans within a single checkout flow while shielding underlying cards. Mastercard’s roadmap to full e-commerce tokenisation by 2030 underscores BNPL as a strategic vector because serial instalments amplify the surface area for credential compromise.[2]PYMNTS, “Mastercard New Use Cases Prep for Total Ecommerce Tokenization by 2030,” pymnts.comTokens simplify credit decisioning by providing alias data streams compliant with privacy regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps among Proprietary Token Service Providers | -1.0% | Global, with acute impact in multi-vendor environments | Medium term (2-4 years) |

| High Latency Concerns in Token Vault Architectures for High-Frequency Trading Firms | -0.6% | North America & Europe, concentrated in financial hubs | Short term (≤ 2 years) |

| Limited Awareness of Non-Payment Tokenization Use-Cases in Mid-Tier Healthcare Providers | -0.4% | Global, with concentration in emerging markets | Long term (≥ 4 years) |

| Vendor Lock-in Risk Restricting Adoption by Government Agencies | -0.3% | Global, with emphasis on public sector procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Among Proprietary Token Service Providers

Disparate token formats and proprietary APIs hinder multi-rail payment acceptance, elevating integration cost and vendor-lock-in risk. Government agencies mandated to diversify suppliers must often maintain parallel token infrastructures, draining CapEx and complicating governance. Absence of a universal token exchange protocol also impedes cross-border commerce, where mismatched schemes require complex translation gateways that inflate processing fees.

High Latency Concerns in Token Vault Architectures for High-Frequency Trading Firms

Central vault look-ups add 10-50 milliseconds to authorisation loops—unacceptable for algorithmic trading desks that benchmark in microseconds.[3]USPTO, “Patent Application 20170346807 - Tokenization System and Method,” uspto.report Physical distance between trading engines and cloud vaults compounds the lag, while encrypted channel handshakes further erode performance. Although vaultless models remove this bottleneck, migration entails cryptographic re-architecture and stringent change-control, causing firms to delay cut-over pending cost-benefit clarity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale as Enterprises Seek Managed Execution

Solutions accounted for 71.35% of 2025 revenue, testifying to the foundational role of platform software in the tokenization solution market. Professional and managed services are forecast to grow at a 20.35% CAGR, aided by scarce in-house expertise and continuous compliance obligations that favour outsourcing. Enterprises leverage advisory engagements to map data flows and reduce PCI exposure, then transition to ongoing service contracts for token maintenance. Tokenization-as-a-Service frameworks blur the boundary between product and service, lowering entry barriers for mid-market adopters. AI-enabled documentation tools, such as Marqeta Docs AI, further accelerate onboarding by automating code-snippet generation.

The solutions segment remains critical for enterprises demanding extensibility into proprietary payment flows or hybrid on-premise deployments. Feature roadmaps increasingly embed artificial-intelligence analytics that surface fraud patterns within the token stream, turning passive controls into active decision engines. Vendors that pair extensible APIs with compliance attestation are best placed to lock in long-cycle enterprise accounts.

By Deployment Mode: Cloud Dominance Validates Pay-As-You-Go Security

Cloud held 63.10% of 2025 revenue and will sustain leadership with a 20.65% CAGR, reflecting the structural advantage of global point-of-presence coverage and elastic scaling. Integrations with existing identity-and-access-management stacks allow security teams to unify policy enforcement, speeding audits and breach preparation. Edge compute extensions reduce network hops, closing the latency gap that once favoured on-premise deployments. Post-quantum cryptography roadmaps hosted by hyperscalers further tip the balance by de-risking future algorithmic transitions.

On-premise installations persist in industries with strict residency mandates or mainframe dependencies. Hybrid architectures offer a middle path, retaining local key custody while bursting tokenisation workloads to the cloud during seasonal spikes. As zero-trust frameworks mature, even conservative sectors may offload non-core workloads, shrinking the on-premise footprint over the forecast horizon.

By Tokenisation Technique: Vaultless Architectures Migrate From Niche to Mainstream

Vaultless methods owned 57.40% of 2025 revenue and exhibit the strongest growth trajectory at 22.70% CAGR. By generating format-preserving tokens without central storage, vaultless platforms remove a high-value breach target and streamline disaster-recovery planning. Financial-market participants prize the sub-millisecond response times and deterministic scaling. Compliance teams welcome vaultless models because fewer systems fall under sensitive-data classification.

Vaulted approaches endure where legacy integrations and compliance documentation are deeply embedded. Some issuers retain vaults for deterministic token-to-PAN mapping required by back-office dispute processes. Nevertheless, EMVCo’s 2024 specifications reinforce the industry shift toward vaultless schemes, legitimising the approach for issuers previously constrained by scheme rules.

By Application Area: Fraud Prevention Takes Centre Stage

Payment security accounts for 48.40% of 2025 spend, underpinning nearly every card-on-file use case in the tokenization solution market. Fraud prevention and risk management, however, will register a 22.55% CAGR as enterprises weaponise behavioural analytics on tokenised transaction streams. AI engines trained on enriched token metadata deliver adaptive risk scores that minimise false declines without sacrificing protection.

Customer authentication grows steadily as strong-customer-authentication mandates in Europe and Asia integrate tokenised multi-factor challenges. Emerging verticals—health data, IoT telemetry, and digital identity—occupy the “Other” bucket but demonstrate high strategic value as they extend tokenisation beyond payments.

By End-User Industry: Retail & E-Commerce Outpace BFSI

BFSI institutions contributed 27.70% of 2025 turnover, cementing their role as anchor tenants for tokenisation platforms. Yet retail and e-commerce are projected to expand at 21.95% CAGR as omnichannel merchants embed network tokens to stitch together in-app, online, and in-store journeys.

BNPL and embedded-checkout models amplify token volumes because every instalment triggers a new authorisation event, making credential life-cycle automation critical. Telecommunications and IT providers apply tokenisation to subscription billing and API monetisation, while healthcare pilots protect patient identifiers across clinical research data sets.

Geography Analysis

North America generated 38.60% of 2025 revenue for the tokenization solution market, anchored by early cloud adoption and a strict payment-security compliance regime. PCI DSS 4.0 deadlines have compressed upgrade cycles, tipping many late adopters toward managed tokenisation services. Market saturation is approaching in core credit-card verticals, so providers are pivoting to adjacent use cases such as healthcare payments and government disbursements.

Asia Pacific is pacing the field with a 19.95% CAGR through 2031, catalysed by mobile-wallet penetration and public-sector digitalisation funds. Japan’s ASEAN QR project and Alipay+ merchant expansion exemplify how cross-border wallets leverage network tokens for currency-agnostic settlement. China’s super-app ecosystems continue to scale, demanding ultra-high-throughput token engines capable of handling peak shopping festivals. India’s unified payments infrastructure offers fertile ground for tokenisation providers that can tailor to local Aadhaar identity norms.

Europe remains a steady adopter, balancing GDPR constraints with strong fraud-prevention incentives. Vaultless implementations resonate with regulators wary of centralised data stores, while national digital-ID programmes open fresh opportunities for citizen-service tokenisation.Fragmented rule sets still complicate pan-European roll-outs, but scheme-level harmonisation is gradually lowering technical barriers.

Regulatory Landscape

Tokenization deployments in payments continue to be shaped by PCI Security Standards Council requirements. PCI DSS v4.0.1 tightens operational controls around cryptographic key management, including cryptoperiod and key retirement, and reinforces that tokenization can reduce scope without removing PCI obligations for de-tokenization and PAN storage components. For 2026 assessments, organizations are aligning token-vault modernization or vaultless migrations with these controls to limit the in-scope cardholder data environment while meeting continuous-monitoring expectations embedded in the standard.

In Europe, digital identity policy is adding regulatory pull for token-like pseudonymous identifiers and high-assurance onboarding. Regulation (EU) 2024/1183 requires Member States to provide European Digital Identity Wallets (EUDI Wallets) by end-2026, and Commission Implementing Regulation (EU) 2026/798 (April 2026) specifies reference standards for remote user onboarding, aligning wallet ecosystems to common technical requirements. At the international level, IMF policy work in 2026 highlights regulatory priorities around legal certainty, interoperability, and settlement finality for tokenized finance, which reinforces demand for auditability and cross-border governance features in enterprise tokenization platforms.

Value Chain Analysis

The tokenization solution value chain spans (i) standards and trust anchors, (ii) core tokenization platforms, and (iii) distribution and operations. At the upstream layer, payment and security standards (PCI DSS v4.0.1 and PCI SSC tokenization guidance) and identity frameworks (EUDI Wallet Architecture and Reference Framework) define technical and assurance requirements. The midstream platform layer includes tokenization engines (vaulted and vaultless), token lifecycle services, policy and analytics, and cryptographic infrastructure such as cloud HSMs and key management, which are increasingly delivered as managed services to shorten compliance timelines.

Downstream, adoption is routed through payment networks and processors (network tokenization and Click to Pay), issuers and acquirers, and enterprise channels such as retail, BFSI, and government digital identity programs. Implementation partners and managed security providers handle assessment scoping, integration with IAM and fraud stacks, and ongoing operations such as key rotation, device binding, and token requestor governance. Interoperability across proprietary token service providers and integration complexity with legacy cores remain key bottlenecks, pushing buyers toward platforms that offer certified APIs, migration tooling, and cross-scheme token orchestration while balancing lock-in risk.

Competitive Landscape

Competitive intensity is moderate, with legacy processors, cybersecurity specialists, and fintech entrants battling for share. Network-tokenisation “rails” embedded by Visa and Mastercard give incumbents scale advantages, yet vaultless and edge-compute pioneers differentiate on latency and configurable risk scoring. Marqeta’s collaboration with Klarna and Affirm illustrates the strategic shift toward platform partnerships that monetise tokenised data through flexible instalment financing. Thales leverages government digital-ID contracts to anchor cross-vertical expansion, evidenced by the Mauritius national wallet award.

Patent filings covering distributed token orchestration, quantum-safe algorithms, and token auditability underscore the technology arms race. Larger vendors are layering AI-driven observability over token streams, enabling predictive risk mitigation and adaptive credential rotation. The ecosystem’s moderate fragmentation creates room for niche specialists targeting sectors such as healthcare or IoT, but sustained success will hinge on interoperability alliances and compliance certifications.

Tokenization Solution Industry Leaders

-

Thales Group

-

Broadcom Inc. (Symantec Enterprise)

-

Visa Inc.

-

Mastercard Inc.

-

Fiserv Inc. (First Data)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clearer whitespace is emerging for tokenization beyond card data, particularly where enterprises need to use sensitive datasets inside analytics and AI workflows without exposing clear text. In June 2026, Capital One Software work with PwC Research compared tokenization against masking in a structured health survey use case, reporting materially higher predictive accuracy on tokenized data than on masked data. This supports adoption of tokenization at ingestion for governed data lakes and model development, expanding the addressable market for tokenization providers into healthcare and life sciences, customer analytics, and enterprise AI governance programs that require reversible controls, audit trails, and separation of duties.

Payments-led opportunities are also concentrating around network-token scale-up, agentic commerce controls, and identity wallet ecosystems. The move to PCI DSS v4.0.1 requirements for 2026 assessments is driving demand for managed tokenization operations, including continuous control monitoring, key lifecycle management, and segmented architectures. It is also sustaining interest in vaultless designs that reduce latency and concentrate fewer breach targets. In parallel, EU Digital Identity Wallet implementation milestones through end-2026 create integration needs for pseudonymization, high-assurance onboarding, and trust-service interoperability, adding a dedicated enterprise budget line where tokenization vendors can package wallet-facing credential protection, privacy-by-design identifiers, and cross-border verification workflows.

Recent Industry Developments

- July 2026: Thales joined the Visa Digitalization Ready Program (VDRP) in Asia Pacific to accelerate deployments of digital payment solutions and Click to Pay capabilities. The initiative aligns Thales payment tokenization and enablement services more tightly with Visa-led merchant and issuer rollouts, supporting faster regional scaling for network tokenization programs.

- December 2025: Fiserv announced a collaboration with Visa to deploy Visa Trusted Agent Protocol across Fiserv's merchant ecosystem to secure AI-driven agentic transactions. This embeds tokenization and credential controls into emerging agent-led commerce flows, extending token governance requirements beyond traditional card-on-file implementations.

- June 2024: Visa reported it had issued more than 10 billion tokens since 2014 and linked tokenization to measurable incremental e-commerce revenue. The milestone reinforced network-token scale as a competitive differentiator and encouraged merchants and processors to prioritize token adoption to reduce fraud exposure and improve authorization performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the tokenization solution market is defined as revenues earned from software and related services that replace sensitive data (such as payment or customer identifiers) with tokens, so data stays usable but is less exposed during storage and transfer.

Scope exclusions: Hardware security modules, generic encryption-only tools, and pure consulting that does not involve tokenization deployment are excluded.

Segmentation Overview

-

By Component

- Solutions

- Services

-

By Deployment Mode

- On-Premise

- Cloud

-

By Tokenization Technique

- Vaulted Tokenization

- Vaultless Tokenization

-

By Application Area

- Payment Security

- Customer Authentication

- Fraud Prevention and Risk Management

- Compliance and Audit Management

- Others

-

By End-User Industry

- BFSI

- Retail and E-commerce

- IT and Telecommunications

- Healthcare and Life Sciences

- Transportation and Logistics

- Government and Public Sector

- Energy and Utilities

- Media and Entertainment

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Nordics

- Rest of Europe

-

Asia Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia Pacific

-

Middle East and Africa

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by collecting public signals that show how fast digital payments, data protection, and cloud adoption are moving, since these shape tokenization demand. We typically refer to sources such as the National Institute of Standards and Technology (NIST) guidance, PCI Security Standards Council materials, Federal Trade Commission (FTC) consumer protection updates, and International Organization for Standardization (ISO) references, which help anchor definitions and compliance boundaries.

To quantify and cross-check adoption, we also review company annual reports, investor presentations, audited filings, and trusted press coverage on breaches and regulatory actions. A paid subscription for company financials and intelligence is used to speed up screening of relevant revenue lines and business descriptions, and a patent database is selectively checked to understand solution focus areas and activity trends. These desk sources are not exhaustive, and many other public documents and datasets were also consulted to collect, validate, and clarify the final analysis.

Primary Interviews and Surveys

Primary work is used to pressure-test what we saw in desk research and to fill gaps on pricing, typical deployment patterns, and where tokenization is being adopted first. We spoke with a mix of solution providers, system integrators, and end-user teams across BFSI, retail, IT, healthcare, and government, and input was balanced across APAC, EMEA, and the Americas so regional rollups did not get skewed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 49% |

| Mid tier: 53% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 19% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, where the top-down view is formed by reconstructing the addressable spend pool for tokenization from digital transaction growth, regulatory compliance intensity, and cloud migration pace across key industries. Once the demand pool is formed, it is then converted into revenue using practical adoption rates and average contract values that were checked during interviews.

To keep the model grounded, we corroborate totals using selective bottom-up approximations, such as sampled vendor revenue exposure to tokenization, channel checks with implementation partners, and sanity checks using typical annual spend per large enterprise for payment security and data protection programs. When gaps appear (for example, when services revenue is bundled into broader security work), assumptions are adjusted using interview-backed ranges and then applied consistently across regions.

Forecasting leans on scenario analysis supported by a light multivariate regression, where the key drivers include growth in card-not-present transactions, tokenization penetration in payment flows, cloud workload share, pace of compliance-driven upgrades, and observed breach frequency trends. The forward path is finalized only after the assumed driver ranges are aligned with what practitioners said is realistic for budgets, timelines, and deployment complexity.

Data Validation & Update Cycle

Validation happens in steps, starting with internal consistency checks across components (solutions versus services), regions, and end-user adoption patterns, so growth is not accidentally double counted. Outliers are reviewed against independent signals like digital payment growth, security spend direction, and notable regulation changes, and then the model is reworked if a mismatch is persistent.

Before sign-off, the output is reviewed by another analyst who checks key assumptions, currency conversions, and whether the final totals remain traceable to the stated inputs. Reports are refreshed annually, and if a material event occurs (such as a major regulatory shift or a sharp change in breach trends), we re-contact sources and update the model. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Tokenization Solution Market Size Measured Against Other Published Estimates

Published market sizes for tokenization can look different even when the topic sounds similar, because authors do not always count the same revenue streams or use the same timing for the base year. Differences also show up when one study focuses on payment tokenization, while another expands into broader asset tokenization or adds adjacent security categories.

By tracking component-level revenues and refreshing adoption and ASP assumptions with interview checks, Mordor Intelligence keeps the tokenization solution total tied to solutions and services used to tokenize sensitive data, instead of blending in wider digital asset platform activity or unrelated security tools. Currency conversion timing, whether services are fully included, and how aggressively cloud deployments are assumed to ramp can each move the number by a noticeable margin.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.23 B (2026) | |

| Global Consultancy A | USD 5.97 B (2026) | Uses a broader tokenization framing that can extend into asset tokenization platforms and related infrastructure, which inflates the spend pool beyond enterprise data tokenization solutions and services. |

| Industry Publisher B | USD 3.95 B (2025) | Uses an earlier base year and applies more conservative adoption and pricing progression, which lowers the near-term value when compared to a 2026 starting point and updated contract benchmarks. |

The spread in estimates is mainly explained by what is counted inside the market boundary and which year anchors the model. When scope stays limited to tokenization solutions and services, and assumptions are checked against practical adoption and pricing signals, the result becomes easier to trace and repeat for planning discussions.

Key Questions Answered in the Report

What is the projected growth rate of the tokenization solution market to 2031?

The market is forecast to grow at a 19.57% CAGR, advancing from USD 5.23 billion in 2026 to USD 12.78 billion by 2031.

Which region will expand fastest in the tokenization solution market?

Asia Pacific is expected to post the strongest CAGR at 19.95% through 2031, fuelled by surging mobile wallets and supportive government programmes.

Why are vaultless tokenisation techniques gaining traction?

Vaultless designs remove central storage points, cut latency and simplify compliance, which explains their 22.70% CAGR and 57.40% 2025 revenue share.

How does PCI DSS 4.0 influence enterprise spending on tokenisation?

The standard’s enhanced data-protection rules push firms to adopt tokenisation to narrow audit scope and lower compliance expenditures.

What role does tokenisation play in BNPL platforms?

Tokens secure the multiple instalment authorisations inherent in BNPL, enabling seamless consumer experiences while protecting underlying payment credentials.

Which industry vertical beyond BFSI is accelerating its adoption?

Retail and e-commerce are forecast to grow at 21.95% CAGR as omnichannel merchants integrate tokenised checkout, loyalty and embedded finance capabilities.

Page last updated on: