Single Factor Authentication System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

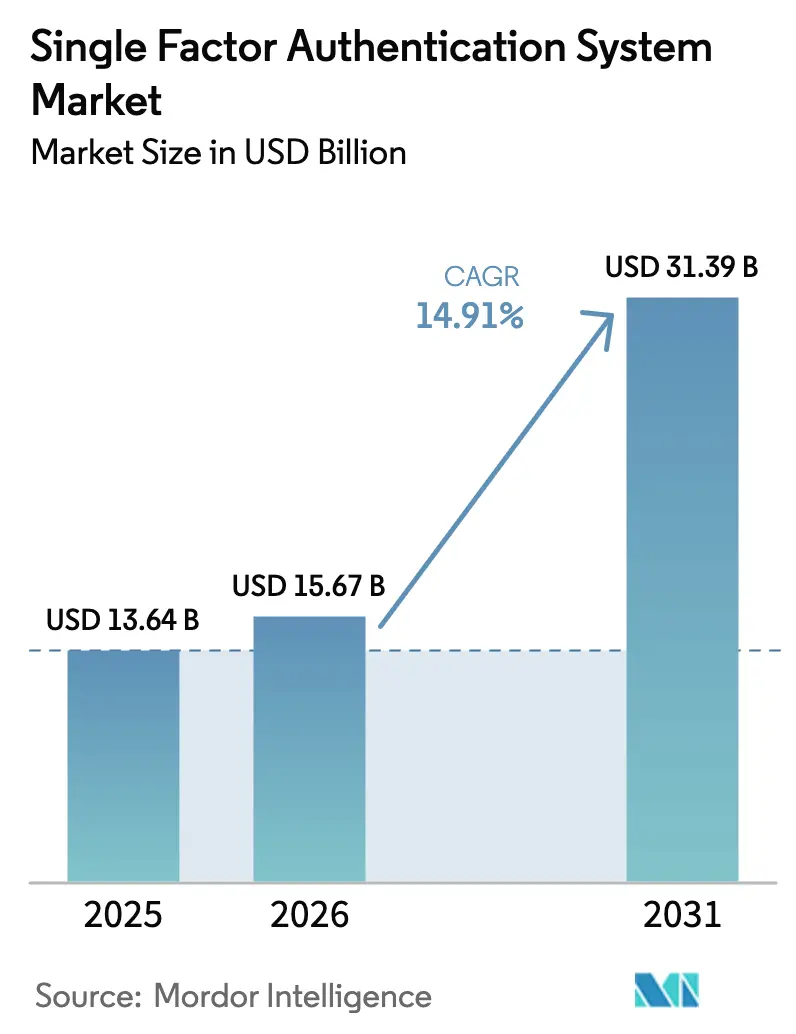

| Market Size (2026) | USD 15.67 Billion |

| Market Size (2031) | USD 31.39 Billion |

| Growth Rate (2026 - 2031) | 14.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

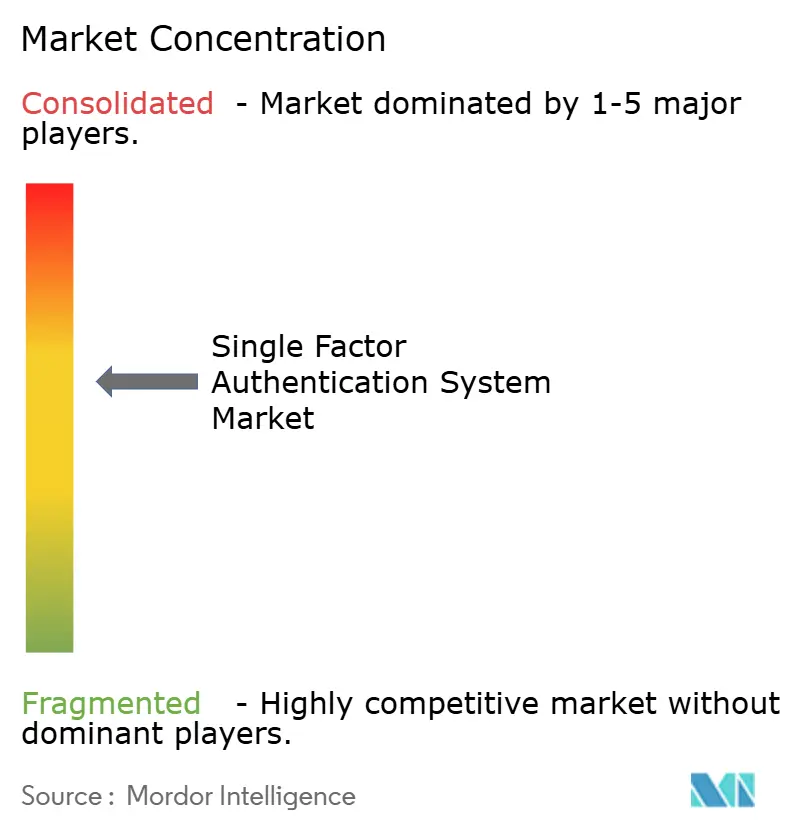

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single Factor Authentication System Market Analysis by Mordor Intelligence

Single factor authentication system market size in 2026 is estimated at USD 15.67 billion, growing from 2025 value of USD 13.64 billion with 2031 projections showing USD 31.39 billion, growing at 14.91% CAGR over 2026-2031. Growth stems from enterprises replacing passwords with biometric scans, hardware keys, and other phishing-resistant single-factor options while cloud identity platforms embed passwordless journeys by default. Regulatory bodies across major economies now accept sophisticated single-factor techniques as compliant when assurance levels are met, thereby unlocking demand among banks, telecom companies, and government portals. Hardware token vendors benefit from the rise in credential-phishing incidents, yet software providers still command a larger volume by integrating on-device biometrics into SaaS workflows. The competitive field increasingly rewards vendors capable of unifying verification, authentication, and risk analytics into one seamless experience, prompting acquisitions that bundle identity proofing with single-factor sign-in.

Key Report Takeaways

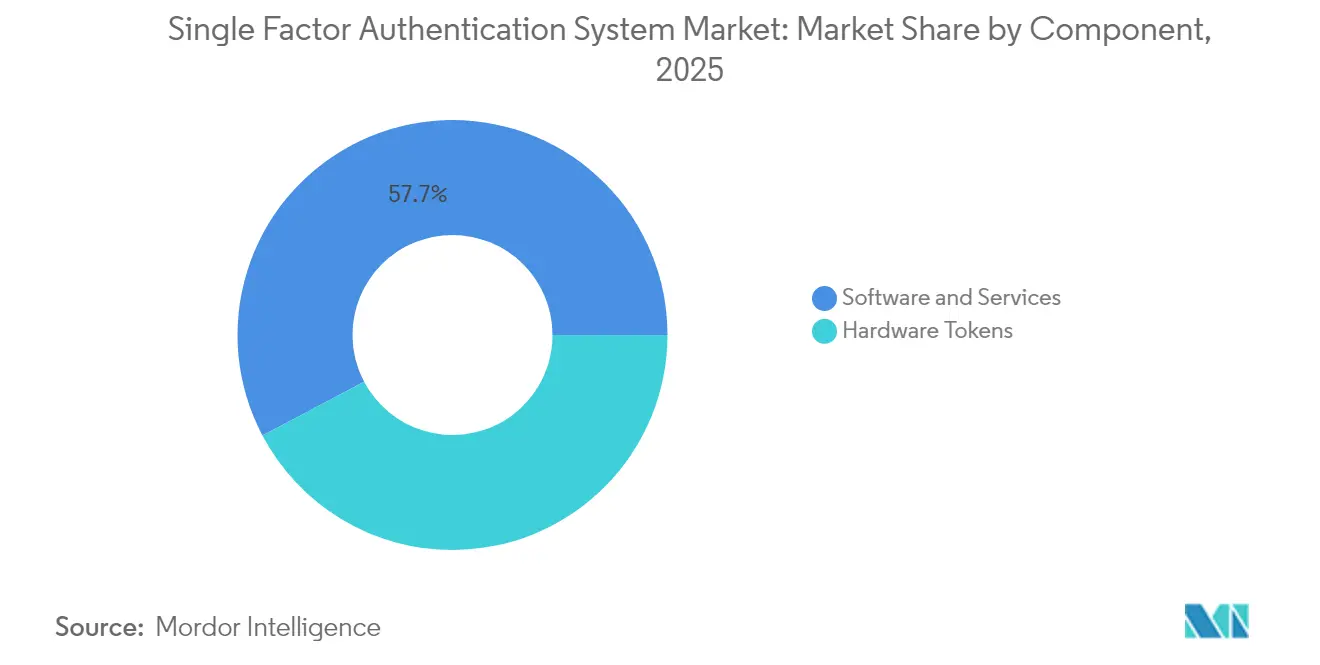

- By component, Software and Services led with 57.74% of single-factor authentication system market share in 2025; Hardware Tokens are poised to expand at a 16.08% CAGR through 2031.

- By authentication method, SMS/Email OTP captured 43.38% revenue share of the single-factor authentication system market size in 2025, while Hardware Security Key solutions are projected to grow at 16.87% CAGR to 2031.

- By deployment model, the Cloud accounted for 59.14% of the 2025 single-factor authentication system market size and is expected to advance at a 15.86% CAGR through 2031.

- By end-user industry, Banking, Financial Services, and Insurance held 30.07% of the single-factor authentication system market in 2025; IT and Telecommunications are expected to record the highest forecast CAGR at 17.52% through 2031.

- By geography, North America dominated the single-factor authentication system market with a 36.23% share in 2025, whereas the Asia Pacific is projected to register the fastest growth, at a 17.33% CAGR, from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single Factor Authentication System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in credential phishing attacks on SaaS workloads | +3.2% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Expansion of digital banking and fintech ecosystems | +2.8% | Asia Pacific core, spill-over to Latin America and Africa | Medium term (2-4 years) |

| Regulatory mandates for strong customer authentication | +2.1% | Europe, Asia Pacific | Long term (≥ 4 years) |

| Shift to passwordless user journeys by major cloud IAM suites | +2.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising adoption of FIDO2-based hardware security keys | +1.9% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Telco-grade SIM authentication opening single-factor paths for IoT devices | +1.4% | Global, early in Asia Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Credential Phishing Attacks on SaaS Workloads

Microsoft’s 2024 telemetry indicates that adversary-in-the-middle campaigns against cloud sign-ins have tripled year over year, driving boards to reevaluate their minimum authentication baselines.[1]Microsoft Corporation, “Security Blog: Identity and Access Management Trends 2024,” microsoft.com Enterprises now view single-factor approaches through the lens of phishing resistance, rather than the number of factors, elevating hardware keys and device-bound biometrics. Security teams find that properly enforced FIDO2 keys eliminate token replay, leading to accelerated budgets for hardware rollouts within privileged access groups. Cloud identity suites respond by embedding WebAuthn flows, providing administrators with turnkey options that replace passwords without requiring additional steps. As a result, the single-factor authentication system market is experiencing immediate tailwinds from breach-avoidance spending, particularly among North American SaaS heavyweights.

Expansion of Digital Banking and Fintech Ecosystems

Fintech adoption in Southeast Asia and Latin America continues to outpace the development of secure authentication infrastructure, prompting regulators to endorse biometric single-factor solutions that satisfy the strong customer authentication criteria when the inherent requirements are met.[2]European Central Bank, “Digital Finance Report 2024,” ecb.europa.eu Mobile-first banks leverage device-native face and fingerprint sensors to streamline onboarding, cutting conversion friction and broadening financial inclusion. Government-sponsored digital identity frameworks, such as India’s Aadhaar and Australia’s Digital Identity Act 2024, incorporate single-factor protocols that can be upgraded to risk-based flows when anomalies arise. Venture-backed neobanks view seamless biometrics as a market differentiator, amplifying equipment orders for embedded secure elements. These intersecting drivers position Asia Pacific to post the strongest volume gains over the forecast period, reinforcing its role as the fastest-growing region for the single-factor authentication system market.

Regulatory Mandates for Strong Customer Authentication

NIST’s second public draft of SP 800-63-4 clarifies that assurance hinges on authenticator strength and binding, not on multi-factor presence, thereby legitimizing advanced single-factor deployments for AAL1 use cases. European regulators share this stance by permitting biometric or possession-based authenticators when they are cryptographically tied to the user, an interpretation that is already shaping PSD2 audits. Healthcare portals, patient e-records, and public benefits services leverage the guidance to simplify sign-in flows, raising usage rates while remaining compliant. Vendors that align product roadmaps with these frameworks secure pre-approved status in procurement cycles, driving subscription expansion across the public sector and regulated industries. The net effect is a long-tail uplift in the single-factor authentication system market as compliance budgets reallocate toward passwordless upgrades.

Shift to Passwordless User Journeys by Major Cloud IAM Suites

Okta’s 2025 Secure Sign-in Trends Report shows that 61% of IT leaders plan to roll out passwordless production within a year, with many classifying passkeys and biometrics as enhanced single-factor methods rather than as multi-factor add-ons. Cloud IAM vendors offer inline risk analytics that escalate to step-up verification only when anomaly scores spike, enabling single-factor journeys for 90% of legitimate traffic. Enterprises favor this model because it pairs lower abandonment rates with proven cryptographic assurance. The strategy also reduces SMS gateway fees, satisfying CFO mandates to trim operational spend. As platform ecosystems from Microsoft, Google, and Amazon Web Services make passkeys universally available, the single-factor authentication system market benefits from bundled licensing agreements that accelerate customer conversion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| User fatigue and friction from legacy OTP methods | −1.8% | Global, consumer-facing applications | Short term (≤ 2 years) |

| Cost of secure element chips amid semiconductor volatility | −1.5% | Global supply chain, hardware token segment | Medium term (2-4 years) |

| SMS termination fees and A2P messaging fraud losses | −1.2% | Global, higher in expensive SMS regions | Short term (≤ 2 years) |

| Emerging deep-fake spoofing techniques against voice OTP | −0.9% | Global, early in voice-OTP markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

User Fatigue and Friction from Legacy OTP Methods

The FIDO Alliance’s 2024 barometer reveals that 56% of consumers abandon digital services when confronted with cumbersome OTP flows, tarnishing perceptions of the broader single-factor authentication category.[3]FIDO Alliance, “Online Authentication Barometer 2024,” fidoalliance.org Brands reliant on SMS OTP face conversion drops and SIM swap incidents, eroding trust and revenue. This resistance slows migration from passwords because decision-makers conflate legacy OTP with all single-factor approaches. Vendors must invest heavily in user education campaigns and intuitive UX design to overcome entrenched perceptions, consuming marketing budgets that could otherwise be allocated to R&D. Until modern single-factor methods outnumber OTP implementations in the wild, friction-induced churn will temper the near-term expansion of the single-factor authentication system market.

Cost of Secure Element Chips Amid Semiconductor Volatility

Secure element pricing rose 35% between 2022 and 2024, with lead times exceeding a year for niche authentication processors. Enterprises deploying tens of thousands of hardware keys for workforce identity management struggle with higher capital expenditures and longer ROI calculations. Vendors sometimes strip non-essential features to meet price points, reducing durability or cryptographic agility. These constraints funnel buyers toward software alternatives, although certain compliance regimes still mandate physical tokens. If supply bottlenecks persist, the hardware token growth curve could flatten, shaving points off the aggregate CAGR of the single-factor authentication system market despite robust underlying demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Meets Hardware Innovation

Software and Services maintained a 57.74% single-factor authentication system market share in 2025 by capitalizing on enterprises’ existing cloud subscriptions and DevOps tooling. Vendors deliver turnkey APIs, SDKs, and orchestration dashboards that enable administrators to embed passkeys or biometrics into SaaS portfolios without re-architecting their identity stores. The segment also enjoys steady annuity revenue from per-user SaaS pricing, which aligns with enterprises’ shift from CapEx to OpEx budgeting. Yet the model faces security limitations when adversaries exploit cookie replay or session hijacking. Consequently, hardware tokens driven by FIDO2 and supported by an 89% year-over-year increase in new certifications are projected to grow at a faster rate of 16.08% CAGR, signaling that high-assurance use cases now justify higher unit costs.

In practice, many enterprises run tiered architectures that reserve hardware keys for privileged workloads while relying on device-bound biometrics for general staff. This hybrid stance underscores a broader evolution in which both segments grow in tandem, drawing incremental value from distinct risk profiles. Microsoft’s Azure AD integration with YubiKey and Google’s Titan series exemplify the convergence, as each provider embeds firmware attestation with cloud-side analytics. The single-factor authentication system market, therefore, rewards portfolio breadth: vendors able to supply both software orchestration and certified hardware widen their average contract value and reduce account churn. As economies of scale improve semiconductor supply, per-unit prices will normalize, enabling hardware tokens to nibble further into software’s share without negating its growth.

By Authentication Method: Legacy Persistence Versus Future-Ready Innovation

SMS/Email OTP accounted for a 43.38% share of the single-factor authentication system market size in 2025, largely due to its universal device compatibility and minimal coding effort. E-commerce merchants continue to favor OTP when speed to market outweighs the risk of breach liability, especially in regions with slow regulatory enforcement. Nevertheless, policy headwinds loom: the European Banking Authority discouraged the use of SMS OTP for payments in late 2024, and several U.S. agencies flagged it as inadequate for citizen portals, foreshadowing a decline in usage. Enterprises also confront escalating A2P message fees and termination fraud, which erode cost advantages and squeeze margins.

Hardware Security Key authentication represents the fastest growing segment, posting a 16.87% CAGR as CISOs earmark budgets for phishing-proof authenticators that bind cryptographic secrets to physical devices. Yubico reports customers see a 99.9% drop in account takeovers post-deployment, a statistic that resonates with CFOs underwriting cybersecurity insurance premiums. Biometric single-factor methods strike a middle ground by embedding inherence directly into mobile apps, thereby sidestepping distribution costs tied to hardware. Together, hardware keys and biometrics create a future-ready cohort that is poised to surpass OTP within the decade, reshaping the single-factor authentication system market toward cryptographically anchored factors.

By Deployment Model: Cloud Supremacy Drives Market Evolution

Cloud held 59.14% of the single-factor authentication system market share in 2025 as enterprises offloaded identity expertise to managed service providers. Platform vendors leverage threat telemetry across millions of tenants, enabling machine-learning-based anomaly detection that on-premise teams struggle to replicate. Microsoft’s 2024 Identity Report notes a 73% decrease in incidents among organizations that rely on cloud-managed authentication. Subscription models also lower entry barriers for mid-market firms that cannot afford dedicated security staff. Consequently, cloud deployments are expected to enjoy a 15.86% CAGR through 2031.

On-premise and hybrid footprints persist where legislation dictates data residency or where air-gapped networks protect critical infrastructure. Even in those verticals, administrators are increasingly connecting local credential stores to cloud-based risk engines, further reinforcing the cloud's influence. Vendors pitch “bring your own HSM” options that allow customers to host keys on-premises while still utilizing cloud orchestration. This architectural flexibility enables parallel growth across deployment models, while the cloud retains its lead position due to economies of scale and continuous control updates, solidifying its role as the substrate of the single-factor authentication system market.

By End-User Industry: Financial Services Leadership Faces Technology Sector Challenge

Banking, Financial Services, and Insurance controlled 30.07% of the single-factor authentication system market in 2025 as PSD2, GLBA, and FFIEC requirements made robust authentication a non-negotiable cost of doing business. Financial institutions allocate premium budgets to biometric sign-ons and hardware keys that safeguard high-value transactions and client trust. The sector’s conservative risk posture results in lengthy purchase cycles, but contract values are large. Pressure intensifies as open banking APIs proliferate, obligating banks to secure machine-to-machine sessions alongside human users within the same authentication mesh.

Conversely, the IT and Telecommunications sector registers the fastest 17.52% CAGR, reflecting its dual identity as both technology producer and high-value target. Telcos adopt SIM-based authentication for IoT, while hyperscalers protect root console access with hardware tokens. Telecom operators in the Asia Pacific are applying mobile-network-level attestation that combines possession with SIM cryptography, an approach gaining attention in 5G core deployments. This convergence of network and application identities exemplifies why technology firms accelerate the adoption curve, gradually narrowing the share gap with banks in the single-factor authentication system market.

Geography Analysis

North America captured 36.23% of 2025 revenue for the single-factor authentication system market, leveraging strong cybersecurity awareness, early vendor ecosystems, and regulatory momentum such as CISA’s zero-trust directives. Multinational enterprises headquartered in the United States often roll out passwordless pilots domestically before expanding globally, thereby reinforcing their home-market share. Platform giants embed passkey APIs into operating systems and browsers, easing developer adoption and speeding consumer familiarity. Federal agencies, meanwhile, are accelerating FIDO2 procurement frameworks that ripple into state and municipal levels, thereby broadening public-sector opportunities.

The Asia Pacific region logs the highest 17.33% CAGR, driven by mobile-centric economies and government-sponsored digital identity schemes. Singapore’s scheduled OTP sunset and Australia’s Digital ID Act 2024 compel service providers to offer biometric or hardware key sign-ins that meet updated assurance measures. India and China drive transaction volumes through massive real-time payment rails, testing authentication scalability at a continental scale. Favorable demographics, including young, smartphone-savvy populations, and shorten learning curves, allowing fintechs to bypass legacy OTP and move directly to passkeys. These dynamics establish Asia Pacific as the bellwether region for next-generation single-factor adoption patterns.

Europe occupies a middle ground marked by strong privacy regulations and mature payment security mandates. The GDPR constrains biometric data processing, prompting vendors to develop privacy-preserving techniques, such as on-device liveness checks and unlinkable templates. Simultaneously, PSD2 enforces strong customer authentication, inadvertently encouraging banks to adopt FIDO2 keys that meet inherence or possession criteria without exposing sensitive data. Nordic countries demonstrate high trust in government e-ID systems, while Southern Europe makes incremental gains through EU-funded digital transition grants. The patchwork of local data-residency laws creates opportunities for regional cloud providers, ensuring competitive diversity within the European segment of the single-factor authentication system market.

Competitive Landscape

The single-factor authentication system market remains moderately fragmented. Legacy identity providers, such as Thales and RSA Security, retain large installed bases, providing them with opportunities to cross-sell into passwordless upgrades. Okta and Microsoft extend cloud IAM suites with first-party passkey orchestration, embedding single-factor capabilities deep into enterprise SaaS stacks. Specialized hardware vendors, such as Yubico and HID Global, differentiate themselves through certified secure elements, FIPS compliance, and supply-chain transparency. Biometric pure-plays, notably Bio-Key International, pitch multimodal scanners tailored to healthcare and government desks.

Strategic positioning increasingly hinges on platform completeness. Entrust’s 2024 acquisition of Onfido merges AI-driven ID verification with hardware-assured sign-in, satisfying regulators who expect validated identity proofing before credential issuance. CyberArk’s USD 1.54 billion purchase of Venafi adds machine identity management, extending beyond human authentication.[4]Chris French, “CyberArk Acquires Venafi for USD 1.54 B,” scmedia.com These deals illustrate a shift toward holistic identity security platforms that span the lifecycle, from onboarding to de-provisioning, across both people and machines.

Market entry barriers remain moderate. Open standards like WebAuthn lower integration friction, inviting new SaaS entrants to position niche offerings. Yet sustained success demands scale economies for credential telemetry and threat research, assets typically held by established firms. Consequently, consolidation is likely to continue, lifting the combined top-five share while still leaving room for innovation. The market’s moderate fragmentation aligns with a concentration score of 6, reflecting that the top five providers hold slightly more than 60% of aggregate revenue.

Single Factor Authentication System Industry Leaders

Thales SA

RSA Security LLC

Okta Inc.

Entrust Corporation

OneSpan Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Okta’s 2025 Secure Sign-in Trends Report found that 61% of organizations expect to roll out passwordless logins within a year, indicating that biometrics and hardware keys are becoming the default method of sign-in, rather than a backup solution.

- January 2025: RSA Security released its 2025 ID IQ Report, indicating that 61% of enterprises intend to implement passkeys within 12 months, with 66% of respondents classifying identity-related breaches as severe events.

- October 2024: FIDO Alliance launched Passkey Central to accelerate enterprise deployments by providing ROI calculators and UX templates.

- August 2024: NIST issued the second public draft of SP 800-63-4, introducing guidance on syncable authenticators and passkeys for federal agencies.

Global Single Factor Authentication System Market Report Scope

| Hardware Tokens |

| Software and Services |

| Password / Knowledge-based |

| SMS / Email OTP |

| Biometric Single-Factor |

| Hardware Security Key |

| On-Premise |

| Cloud |

| Banking, Financial Services and Insurance |

| Healthcare |

| Government and Public Sector |

| Retail and E-commerce |

| IT and Telecommunications |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware Tokens | |

| Software and Services | ||

| By Authentication Method | Password / Knowledge-based | |

| SMS / Email OTP | ||

| Biometric Single-Factor | ||

| Hardware Security Key | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| Healthcare | ||

| Government and Public Sector | ||

| Retail and E-commerce | ||

| IT and Telecommunications | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What revenue figure does the single factor authentication system market reach by 2031?

It is forecast to reach USD 31.39 billion by 2031, up from USD 15.67 billion in 2026.

Which component segment grows fastest through 2031?

Hardware Tokens post the highest 16.08% CAGR due to demand for phishing-resistant authentication.

Why is Asia Pacific the fastest-growing region?

Government digital ID programs and rapid fintech expansion lift the region at a 17.33% CAGR.

Which authentication method offers the strongest security?

FIDO2-compliant Hardware Security Keys provide hardware-rooted cryptography that blocks phishing.

How do regulations influence single-factor adoption?

Updated guidance from NIST and PSD2 allow biometric or hardware single-factor solutions when assurance goals are met, spurring compliant deployments.

Page last updated on: