Signature Verification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 8.35 Billion |

| Growth Rate (2026 - 2031) | 19.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Signature Verification Market Analysis by Mordor Intelligence

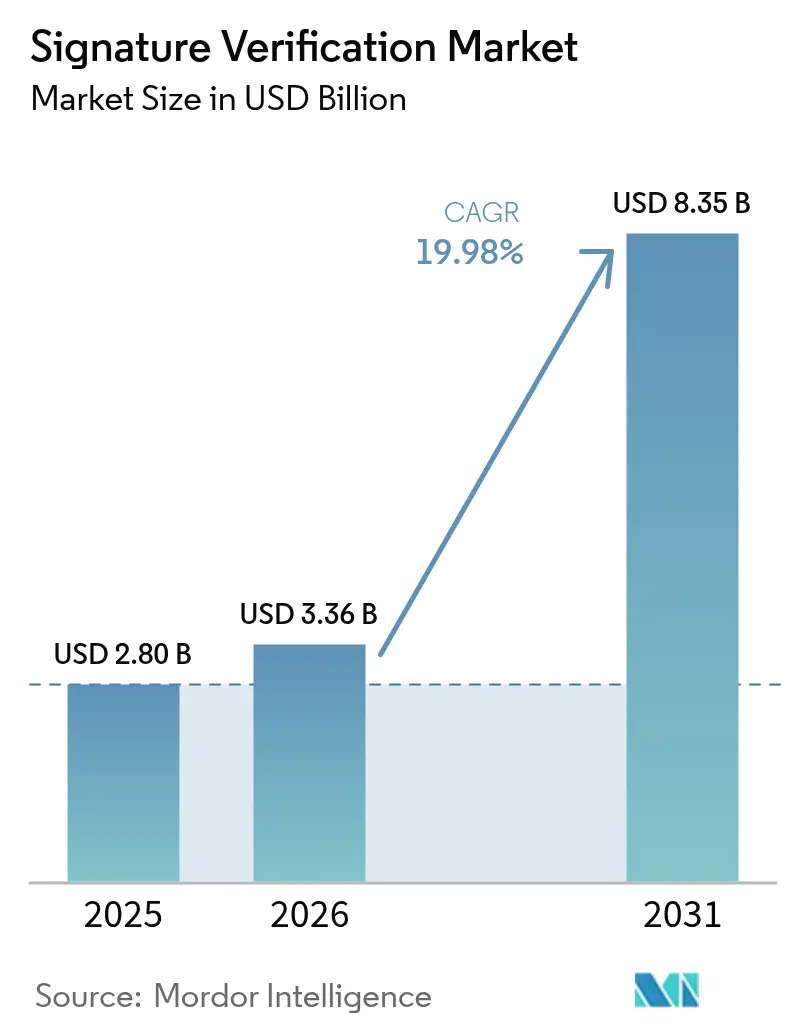

The signature verification market size is expected to grow from USD 2.8 billion in 2025 to USD 3.36 billion in 2026 and is forecast to reach USD 8.35 billion by 2031 at 19.98% CAGR over 2026-2031. Momentum is fueled by eIDAS 2.0 in Europe and 21 CFR Part 11 in the United States, both of which compel regulated sectors to adopt trustworthy digital-signature validation. Rising fraud losses, advances in AI-driven forgery analytics, and rapid cloud migration further elevate demand. Government programs ranging from AI-assisted mail-in ballot processing to Aadhaar-linked wallets expand use-cases and geographic reach. Meanwhile, multimodal authentication and API-first delivery models are reshaping competitive positioning across the signature verification market. [1]U.S. Food and Drug Administration, “21 CFR Part 11—Electronic Records; Electronic Signatures,”

Key Report Takeaways

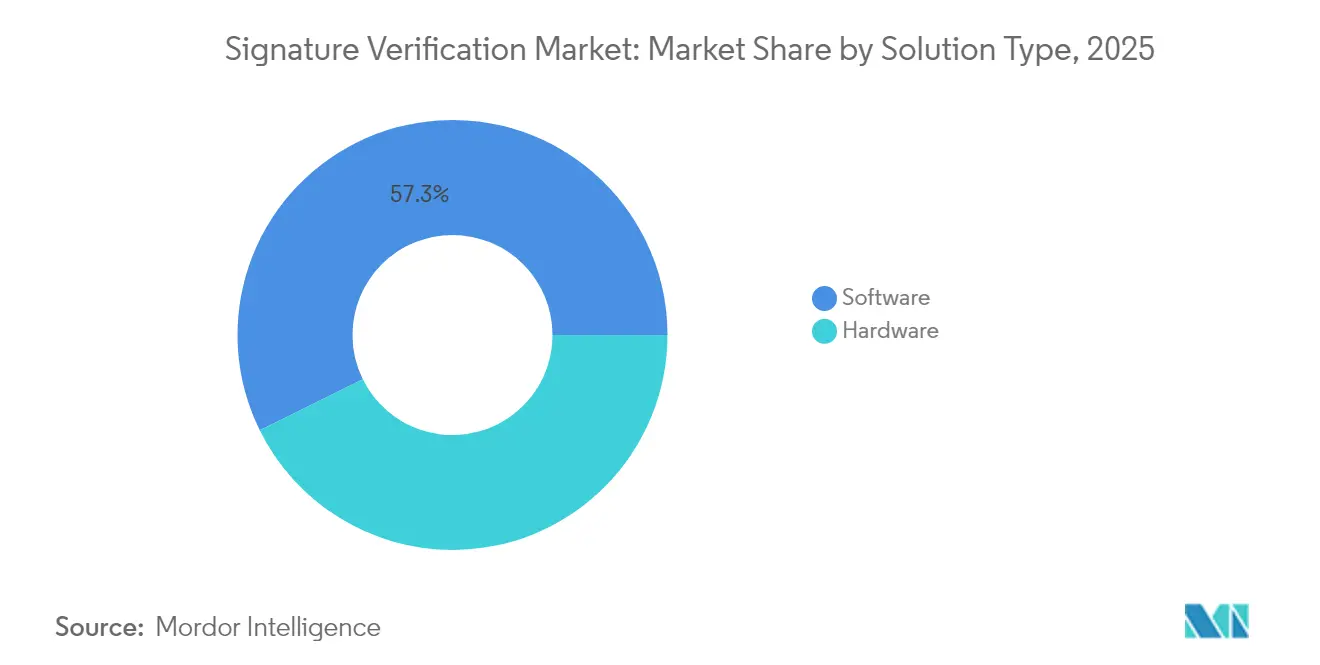

- By solution type, software led with 57.30% revenue share in 2025 while AI-enhanced software is projected to expand at a 22.85% CAGR through 2031.

- By deployment model, on-premise held 53.90% of the signature verification market share in 2025, whereas cloud/SaaS is forecast to accelerate at a 27.05% CAGR to 2031.

- By authentication mode, stand-alone signature verification accounted for a 70.80% share of the signature verification market size in 2025, while multimodal authentication is pacing a 23.10% CAGR through 2031.

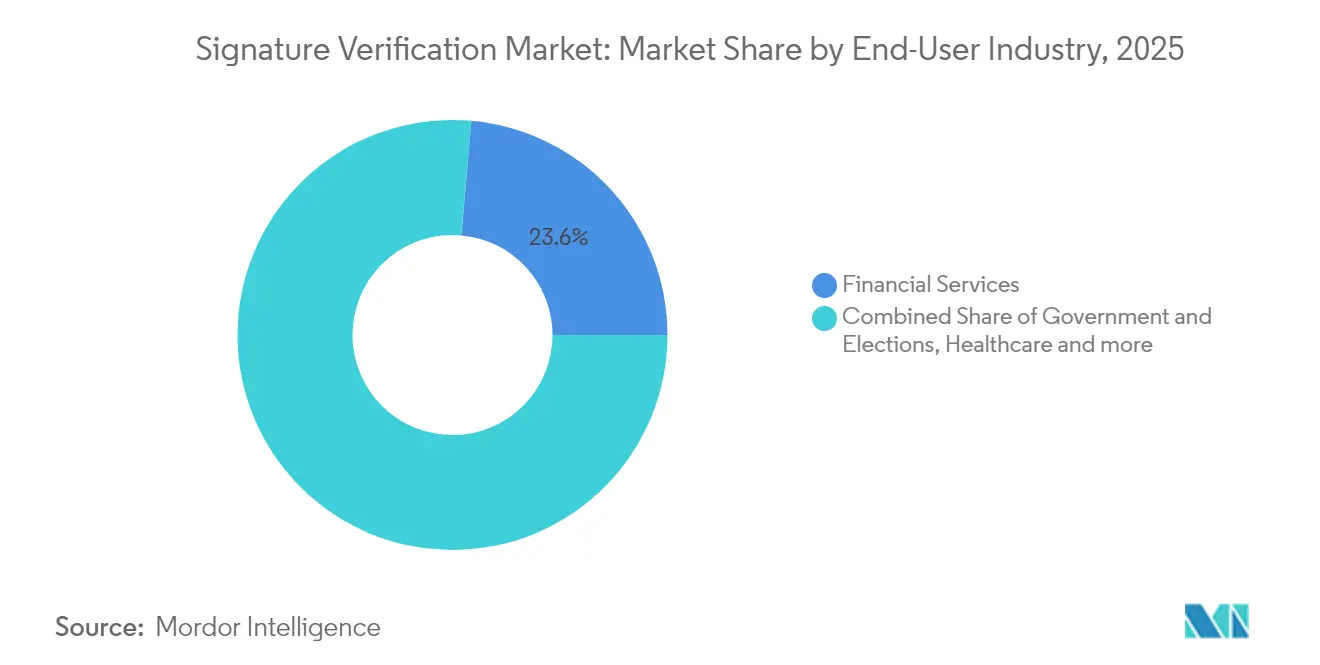

- By end-user industry, financial services captured 23.60% of the 2025 market, yet government and elections is positioned for the fastest 24.55% CAGR to 2031.

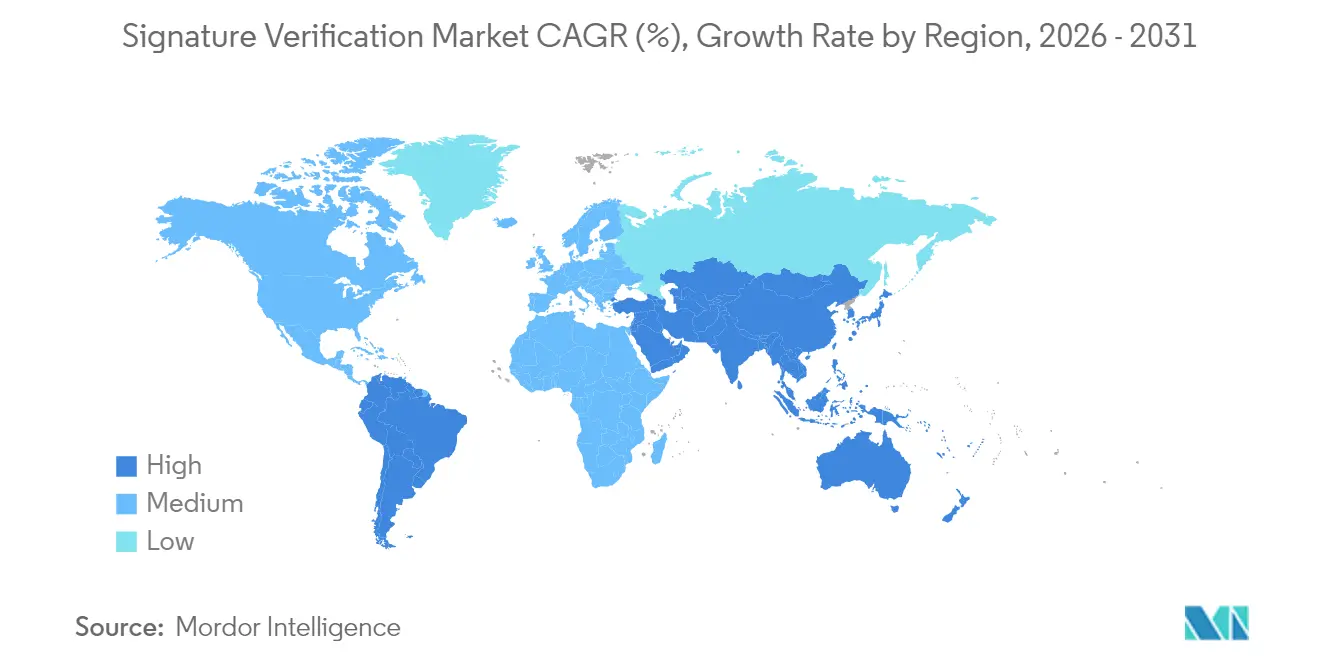

- By geography, North America commanded 33.40% revenue share in 2025; Asia Pacific is projected to deliver the highest regional CAGR of 24.60% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Signature Verification Market Trends and Insights

Drivers Impact Analysis*

| Compliance mandates under eIDAS 2.0 & U.S. CFR Part 11 | +4.2% | Europe & North America | Medium term (2-4 years) |

|---|---|---|---|

| Surge in mail-in ballot signature checks post-2024 elections | +3.8% | North America, with expansion to EU | Short term (≤ 2 years) |

| Fin-crime losses driving AI-based check-fraud analytics | +5.1% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Cloud-native APIs embedded in e-signature suites | +3.9% | Global | Medium term (2-4 years) |

| GenAI forged-signature detection algorithms | +2.7% | Global, early adoption in North America | Long term (≥ 4 years) |

| India's Aadhaar-linked digital signature wallets (UPI 3.0) | +1.3% | Asia Pacific, primarily India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compliance mandates under eIDAS 2.0 & U.S. CFR Part 11

The harmonized push from Brussels and Washington is forcing enterprises to modernize outdated electronic-record systems. eIDAS 2.0 obliges all EU citizens to hold interoperable digital identity wallets by 2026, raising the bar for qualified electronic signatures backed by certified trust service providers. Simultaneously, updated FDA guidance stresses audit trails and risk-based validation, compelling pharmaceutical sponsors to shift toward AI-enabled signature verification platforms. Multinationals consequently seek unified verification architectures that satisfy both regimes, accelerating consolidation around cloud players capable of global policy compliance.

Surge in mail-in ballot signature checks post-2024 elections

Thirty-one U.S. states now require signature verification for absentee ballots, elevating demand for high-throughput systems. North Carolina’s pilot demonstrated that automated platforms processed 1,000 ballots per hour, cutting manual review time by 95%. California subsequently mandated technology-assisted review with manual fail-safes, placing auditability above speed. Vendors able to accommodate multicultural signature variation and age-related changes command premium pricing as election agencies pay for accuracy, adjudication transparency, and regulatory audit features.[2]North Carolina State Board of Elections, “Signature Verification Pilot,” dl.ncsbe.gov

Fin-crime losses driving AI-based check-fraud analytics

Check fraud surged in 2024, with 65% of U.S. organizations reporting attacks. Banks responded by integrating machine-learning engines that flag anomalies in real time. Mitek’s Check Fraud Defender delivers “Day Zero” detection by correlating issuance data, routing numbers, and signature vectors before posting deposits. Parallel efforts at the U.S. Treasury recovered USD 375 million in fraudulent payments, proving the ROI of AI-powered signature analysis. Loss-avoidance incentives thus sustain double-digit software growth even amid budget scrutiny.

Cloud-native APIs embedded in e-signature suites

The market is shifting from stand-alone verification tools toward embedded services residing inside document-workflow platforms. Adobe and DocuSign now expose qualified trust-service integrations that enable real-time checks across devices while honoring data-sovereignty rules. API-first delivery trims deployment cycles and allows smaller firms to access enterprise-grade controls with consumption-based pricing. Recurring subscription revenue, low-friction upgrades, and regional cloud instances strengthen vendor lock-in and accelerate the signature verification market’s pivot to SaaS.

Restraints Impact Analysis*

| Variability across capture devices & legacy silo integration | -2.8% | Global, acute in emerging markets | Medium term (2-4 years) |

|---|---|---|---|

| High FRR in multicultural voter rolls sparks litigation | -1.9% | North America, expanding to diverse democracies | Short term (≤ 2 years) |

| Data-sovereignty limits on cross-border model training | -1.4% | Global, concentrated in EU & China | Long term (≥ 4 years) |

| Patent litigation risk (e.g., MITK vs USAA) | -1.1% | North America, spillover to global markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Variability across capture devices & legacy silo integration

Organizations often rely on a patchwork of signature pads, tablets, and mobile apps, each producing data at different resolutions and sampling rates. Algorithms must compensate for inconsistent pressure curves and timing data, which inflates false-reject rates and raises total cost of ownership. Integrating modern verification with legacy record systems adds complexity, as siloed data prevents holistic fraud analytics. Smaller institutions postpone upgrades because replacing hardware exceeds perceived benefits, restraining near-term adoption despite compelling security gains.

High FRR in multicultural voter rolls sparks litigation

Automated verifiers misclassify legitimate signatures from voters whose scripts differ by language, age, or disability. Litigation has already challenged rejections that disproportionately affect minority communities. California’s emergency rules now demand human review for all machine-flagged ballots and mandate training to recognize signature variability factors. Elevated compliance overhead narrows public-sector budgets and forces vendors to rebalance algorithms toward lower false-reject rates, even at the expense of marginally higher false-accept rates. [3] California Secretary of State, “Signature Verification Emergency Regulations,” sos.ca.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Software Extends its Lead

Software accounted for 57.30% of the 2025 signature verification market, reflecting widespread adoption of cloud-native AI models that deliver real-time fraud detection across web, mobile, and branch channels. Hardware devices such as signature pads remain entrenched in regulated environments, yet their share will continue to erode as remote workflows dominate. The software segment is forecast to post a 22.85% CAGR through 2031, propelled by SDKs that embed verification inside banking, healthcare, and government portals. Vendors are layering behavioral analytics atop static image comparison, thereby reducing manual review rates and shrinking decision latency. Edge-deployable models address locations with intermittent connectivity, broadening appeal to logistics and field-service use-cases. Continuous model retraining also enables vendors to counter emerging attack patterns without customer-side code changes, underscoring software’s structural advantage within the signature verification market.

Hardware, though slower-growing, retains niche relevance where physical custody of wet-ink signatures is non-negotiable. Courts, notaries, and select life-sciences labs still require in-person capture using certified devices that append cryptographic timestamps. Yet procurement cycles in these verticals remain long, capital budgets fixed, and retrofit costs high. As cloud economics shift decision criteria toward operating expenditure, many buyers now phase out devices at end-of-life, migrating to mobile capture plus back-end AI validation. This transition reinforces the ascendancy of software-centric business models and cements provider focus on subscription revenue streams rather than one-time hardware sales.

By Deployment Model: Cloud and SaaS Ascend

On-premises deployments represented 53.90% of the signature verification market size in 2025 as heavily regulated banks, insurers, and life-sciences firms favored local control for audit and latency reasons. However, cloud/SaaS installations are projected to compound at 27.05% annually through 2031, narrowing the installed-base gap on economies of scale and universal API reach. Cloud platforms concentrate model training in centralized environments, leveraging diverse datasets that sharpen accuracy against deepfake threats. Elastic compute provisioning cuts idle infrastructure spending, a critical advantage for election boards that process workloads in intense bursts during peak voting periods.

Regional cloud zones support data-residency mandates under GDPR and eIDAS 2.0 while maintaining uniform policy engines. Hybrid architectures—local storage of signature artefacts combined with cloud-based inference—offer a compliance-friendly bridge for cautious adopters. Providers bolster value propositions with uptime SLAs, automated patching, and seamless feature rollouts that would be cost-prohibitive in isolated data centers. As organizations conclude that operational agility outweighs perceived sovereignty risks, the signature verification market is poised for an accelerated shift toward SaaS subscriptions.

By Authentication Mode: Multimodal Gains Traction

Stand-alone signature checks held 70.80% of total revenue in 2025, underscoring decades of institutional reliance on handwritten authorization. Nevertheless, multimodal authentication—fusing signatures with ID-document scans, selfie liveness, and behavioral biometrics—is set to grow 23.10% annually as deepfake fraudsters erode single-factor defenses. Banks increasingly bundle Mitek’s face biometrics with signature analytics to thwart account takeovers at remote-deposit checkpoints. Healthcare providers likewise pair patient signatures with government-issued ID for consent forms to satisfy HIPAA and reduce liability.

In high-value real-estate closings, simultaneous signature and face capture bolster non-repudiation without extending session times beyond user tolerance thresholds. Adaptive scoring engines calibrate factors dynamically—lowering friction for low-risk transactions while escalating to multimodal checks when anomalies surface. As regulators endorse layered assurance models, vendors that seamlessly orchestrate multiple factors within one interface will seize incremental share across the broader signature verification market.

By End-User Industry: Government Adoption Surges

Financial services contributed 23.60% of market revenue in 2025, anchored by check-fraud detection and account-opening compliance. Banks price verification accuracy directly against loss-prevention savings, fostering predictable demand even as interest-rate cycles fluctuate. Conversely, government and elections emerge as the fastest-expanding vertical, forecast at a 24.55% CAGR through 2031 as jurisdictions embed automation into ballot validation and digital citizen-service portals. State procurement specifications now list API compatibility, explainability logs, and human-review controls as mandatory features, opening a lane for specialized vendors that tailor engines to statutory audit trails.

Healthcare accelerates adoption via e-consent workflows, shortening surgical-prep cycles and reconciling prescription orders in tele-medicine sessions. Logistics players retrofit proof-of-delivery systems with on-device signature capture synced to cloud verification, reducing disputes and chargebacks. Legal and real-estate sectors prize immutable audit trails that protect against contract repudiation, sustaining premium pricing for compliant archives. Together these diverse verticals dilute revenue concentration risk and widen the signature verification market’s total addressable pool.

Geography Analysis

North America accounted for 33.40% of 2025 revenue, supported by mature regulatory regimes and venture-backed innovation ecosystems. States introduced automated ballot-signature systems to enhance electoral integrity after the 2024 cycle, driving rapid upgrades among election boards. Financial institutions also escalated adoption to blunt check-fraud schemes that escalated in sophistication and scale, leveraging AI analytics to detect subtle signature deviations at deposit time. Patent enforcement remains a double-edged sword: USAA’s ongoing licensing victories generate revenue but elevate compliance costs for banks integrating remote-deposit modules. The region’s focus on audit readiness under FDA Part 11 further solidifies demand for specialized platforms that document signature provenance and chain-of-custody.

Asia Pacific is forecast to deliver the highest regional CAGR of 24.60% between 2026 and 2031, anchored by India’s Aadhaar-linked wallets and surging mobile-payment ecosystems. Massive transaction volumes and episodic fraud incidents encourage the Reserve Bank of India to tighten KYC norms, prompting banks to embed multimodal signature verification in onboarding workflows. Japan and South Korea advance finger-vein and behavioural-biometric research, often pairing those technologies with signature analysis for high-trust enterprise login. Local data-sovereignty mandates spur demand for regionally hosted inference clusters, which cloud hyperscale’s provide through in-country availability zones, ensuring that the signature verification market meets stringent residency rules while still leveraging global threat-intelligence feeds.

Europe’s growth narrative revolves around eIDAS 2.0, which formalizes qualified electronic signatures and compels cross-border interoperability throughout the bloc. Certified trust service providers play a pivotal role in issuing digital certificates embedded within signature payloads, raising technical requirements for algorithmic verification. Brexit complicates UK-EU workflows, forcing vendors to maintain dual compliance stacks while promising seamless user experiences. GDPR expectations of privacy-by-design push providers to adopt federated-learning techniques, training models without exporting signature artefacts beyond jurisdictional boundaries. As a result, European buyers weigh algorithmic precision alongside demonstrable privacy safeguards, favouring vendors that deliver both.

Regulatory Landscape

The regulatory environment for signature verification is tightening around explicit technical conformance and auditability across the EU and the United States. In Europe, the eIDAS framework is being operationalized through implementing acts that specify how qualified electronic signatures (QES) and related certificates are validated, including the European Commission Implementing Regulations (EU) 2025/1942, 2025/1943, and 2025/1945 adopted in September 2025, and Implementing Regulation (EU) 2025/1566 adopted in July 2025 that establishes reference standards for identity verification for qualified certificates and electronic attestations of attributes. In April 2026, Implementing Regulation (EU) 2026/798 further anchored technical requirements for remote onboarding to European Digital Identity Wallets, linking conformance to ETSI TS 119 461 (v2.1.1, 2025-02) and reinforcing demand for standardized, provable verification controls.

In the United States, NIST updates are shaping how relying parties strengthen identity proofing and assertion validation against modern fraud. NIST finalized SP 800-63 Revision 4 in July 2025, adding guidance to address threats such as injection attacks and forged media, and followed with NIST IR 8587 in December 2025 to guide protection of identity tokens and assertions from forgery, theft, and misuse. Together, these updates elevate expectations for integrity checks and digital signature verification of identity assertions before granting access to government and other regulated systems, which is steering vendors toward stronger evidence capture, tamper resistance, and traceable validation logs.

Value Chain Analysis

The value chain runs from standards and trust anchors to capture and cryptographic hardware, verification software, and downstream workflow platforms that consume verification decisions. At the foundation are standards bodies and frameworks that define how signatures, attestations, and integrity proofs are formed and validated, including ETSI specifications referenced under eIDAS for qualified trust services, IETF work such as SCITT (RFC 9943) for transparent supply-chain style registries, and GS1 Digital Signatures for item-level and document integrity use cases. Trust service providers, including qualified trust service providers in Europe, and certificate ecosystems supply the root-of-trust artifacts and trust lists that verification engines rely on for long-term validation and cross-border interoperability.

Upstream inputs include signature-capture devices (signature pads, tablets, biometric terminals), secure elements and HSMs for key protection, and document and transaction data streams from banks, government agencies, and enterprises. Midstream, software vendors deliver SDKs and APIs that execute static and dynamic signature verification, add fraud analytics, and integrate with identity proofing and orchestration layers, while specialist verification servers broaden format support across PAdES/XAdES/CAdES and archive-centric long-term validation requirements. Key bottlenecks include interoperability across heterogeneous capture devices, long-term validation for archived agreements, and reconciling centralized trust lists with newer decentralized identity models, which increases integration effort for buyers embedding signature verification into e-signature suites, onboarding flows, and high-throughput public-sector processes.

Competitive Landscape

The signature verification market remains moderately fragmented, with no supplier commanding dominant market share across all verticals and geographies. Established players such as Mitek, Adobe, DocuSign, and Entrust leverage AI portfolios and patent estates to protect margin, while venture-backed challengers pursue cloud-native niches. Horizontal consolidation is accelerating as identity-verification specialists absorb signature-specific assets; Entrust’s purchase of Onfido and Jumio’s USD 150 million capital infusion typify moves to knit document, biometric, and signature analytics into one orchestration layer.

Technology differentiation increasingly hinges on the breadth of data ingested during model training and the speed with which vendors push signature-forgery countermeasures into production. Mitek’s “Day Zero” architecture exemplifies the pivot toward real-time rejection of fraudulent checks before funds hit customer accounts. At the same time, Adobe’s qualified-trust integrations give European customers turnkey compliance with eIDAS 2.0, strengthening its foothold within regulated workflows. Prices trend toward consumption-based tiers, rewarding high-utilization customers with lower per-transaction costs while preserving premium rates for public-sector workloads that demand exhaustive audit trails.

Patent litigation injects both risk and opportunity. USAA’s multimillion-dollar settlements with major U.S. banks validate the economic value of remote-deposit intellectual property, encouraging large incumbents to license rather than litigate. Yet aggressive enforcement can suppress smaller innovators wary of infringement exposure, potentially nudging the market toward licensing consortiums. Providers that pair robust patent portfolios with collaborative open-API ecosystems stand to capture incremental OEM revenue as device manufacturers embed signature verification at the silicon or firmware layer, extending total addressable users well beyond traditional document workflows.

Signature Verification Industry Leaders

Mitek Systems Inc.

DocuSign Inc.

IBM Corporation

Parascript LLC

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven wallet and qualified signature infrastructure in Europe creates whitespace for vendors that can translate standards into turnkey verification services. The EU requirement for member states to provide at least one certified European Digital Identity (EUDI) Wallet by December 2026, alongside implementing rules on validating qualified electronic signatures and seals (for example, Implementing Regulation (EU) 2025/1945 and Implementing Regulation (EU) 2026/248), increases demand for verification modules that support qualified certificate path validation, long-term validation, and explainable audit evidence across borders. This environment favors API-first verification that can be embedded into agreement workflows and public-service portals while fitting within data residency and trust-list constraints.

A second opportunity is crypto-agile signature verification aligned to post-quantum readiness and evolving identity assurance profiles. In April 2026, authID announced integration of NIST-standardized post-quantum algorithms (including ML-DSA and SLH-DSA variants) into its biometric digital signature platform, highlighting buyer interest in modernizing signature integrity controls rather than treating signatures as a static compliance checkbox. At the same time, the shift from stand-alone e-signature tools to broader digital trust platforms is visible in partnership patterns that connect signing with identity verification and credential management, creating openings for signature verification providers that can plug into identity orchestration stacks, support multiple signature formats, and deliver policy-driven verification for regulated and high-value transactions.

Recent Industry Developments

- May 2026: DocuSign and ID.me announced a partnership to integrate ID.me identity verification into DocuSign agreements, targeting higher-assurance transactions aligned with NIST Identity Assurance Level 2 (IAL2). The partnership tightens the coupling of signing workflows with identity proofing, pushing signature verification deeper into end-to-end digital trust stacks for regulated and high-value agreements.

- October 2025: Socure and DocuSign announced a collaboration to bring identity verification and risk signals into the signing experience. This extends signature-centric workflows into identity-informed decisioning, lifting the baseline for fraud controls and increasing the value of verification APIs that can integrate across document, ID, and biometric checks.

- December 2024: Mitek introduced Digital Fraud Defender, positioned as a next-generation defense against deepfakes and emerging digital frauds. The launch points to rising demand for verification solutions that can detect synthetic media and injection-style attacks that undermine remote onboarding and signature-adjacent approvals.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the signature verification market covers tools and services used to confirm whether a signature is genuine, across physical and digital workflows, where the output is a verification decision and a related risk signal.

Scope exclusions: We exclude broader e-signature creation, general identity verification that does not test signatures, and purely manual handwriting review services.

Segmentation Overview

- By Solution Type

- Hardware

- Signature pads and sensors

- Biometric terminals / kiosks

- Software

- Static (offline) verification

- Dynamic (online) verification

- SDK / API platforms

- Hardware

- By Deployment Model

- On-premise

- Cloud / SaaS

- By Authentication Mode

- Stand-alone signature

- Multimodal (signature + doc image / ID / liveness)

- By End-user Industry

- Financial Services

- Government and Elections

- Healthcare

- Transport and Logistics

- Legal and Real-estate

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic structure of demand, adoption, and pricing logic before speaking with market participants. We reviewed public and official references such as NIST publications, the U.S. FDA guidance around 21 CFR Part 11, EU eIDAS related public releases, USPTO patent databases for signature and handwriting analytics, and cybersecurity and digital identity guidance from government portals.

Along with these, we used company annual reports, product documentation, developer notes, investor presentations, and credible press coverage to understand where signature verification is being deployed, and how delivery models are shifting between on-premise and cloud. A paid subscription for company financials and intelligence, plus a paid patent database, was used selectively to confirm revenue exposure cues and technology focus areas. The desk sources listed here are illustrative, and many other public references were also used for data collection, cross-checks, and clarifying assumptions.

Primary Interviews and Surveys

Primary work was used to test what we built from desk findings, especially deployment patterns, buyer decision criteria, and how vendors price verification features across volumes and risk tiers. We spoke with supply-side and demand-side experts across Americas, EMEA, and APAC to ensure regional compliance needs and document workflow maturity were properly reflected in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 14% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

The core sizing started with a top-down build where we reconstructed the addressable demand pool using adoption of digital document workflows, regulated electronic records usage, and the share of transactions where signature proof is still required. After that, selective bottom-up approximations were used to keep totals realistic, including sampled vendor revenue exposure checks, channel feedback on typical deal sizes, and ASP-by-volume ranges for software and device-led deployments.

Key inputs used in the model included the split between static versus dynamic verification, cloud versus on-premise mix, average verification volumes per active enterprise account, typical price progression as accuracy and fraud analytics features are added, and regional compliance triggers that influence procurement timing. Where direct revenue mapping was not available for smaller providers, gaps were handled through conservative bundling assumptions and by anchoring to observed pricing bands from interview feedback.

For forecasting, we relied mainly on scenario analysis. This approach is practical for signature verification because regulation, digital onboarding growth, and fraud pressure can move faster than simple time-series trends. Growth paths were then adjusted using expert consensus on adoption timing by region and by high-usage verticals.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including comparing implied revenue per verification or per customer against what practitioners said is typical, and testing whether regional growth rates align with observed digitization and compliance activity. When large variances appeared, the assumptions were reopened, and specific interviews were revisited to confirm what changed, such as pricing structure, deployment mix, or a shift in policy timing.

Before sign-off, the model and narrative go through a multi-step internal review so math logic, unit consistency, and scope boundaries are aligned. Reports are refreshed annually, with interim updates triggered by material events like major regulatory actions or a noticeable shift in buyer procurement behavior. Right before delivery, a final pass is done so clients receive an updated view based on the latest available signals.

Mordor Intelligence's Signature Verification Market Size Compared With Other Published Estimates

Published market sizes for signature verification can vary even when the topic sounds similar, since firms may not match on what they count as signature verification, the year they anchor to, and how they treat hardware versus software value. Differences also show up when pricing is assumed as a flat average, rather than changing by verification method, deployment model, and usage volume.

The main gap drivers in this market usually come from scope overlap with adjacent categories like broader digital signature platforms, identity verification suites, or document management tooling, which can inflate totals if bundled value is fully counted. Another frequent driver is the time frame, since one estimate may anchor on 2025 while another uses 2026 as the current year, and currency timing and inflation assumptions can further widen the spread.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.36 B (2026) | |

| Global Research Publisher A | USD 3.40 B (2025) | Anchors the current value to 2025 and may treat some signature-adjacent authentication value as part of the same pool, which can shift the starting point versus a 2026-based model. |

| Industry Research Publisher B | USD 2.79 B (2025) | Uses a lower 2025 base and can lean on broader average pricing assumptions without fully separating cloud subscription value from device-led deployments, which tends to suppress the headline size. |

The benchmark table shows that year anchoring and what gets bundled into the definition are the two practical reasons the totals do not line up, and in Mordor Intelligence's model the 2026 value reflects signature verification counted only when it is delivered as dedicated software or hardware functionality (including static and dynamic verification) rather than as a full digital-signing platform. With inputs tied to deployment mix, verification volumes, and pricing bands validated in interviews, the result stays traceable to clear variables and can be repeated as new signals arrive.

Key Questions Answered in the Report

What is the current value of the signature verification market?

The signature verification market reached USD 3.36 billion in 2026 and is projected to grow to USD 8.35 billion by 2031 at a 19.98% CAGR.

Which deployment model is growing the fastest?

Cloud/SaaS deployments are forecast to expand at a 27.05% CAGR as organizations favor scalable, API-driven verification over on-premise systems.

Why is multimodal authentication gaining popularity?

Deepfake and synthetic-identity fraud has exposed limitations of single-factor checks, so businesses now combine signatures with liveness, ID-document, and behavioral data to raise assurance.

How do regulations impact market demand?

EIDAS 2.0 in Europe and 21 CFR Part 11 in the United States require stronger electronic-signature validation, pushing companies to upgrade legacy solutions and driving sustained market growth.

Which region will grow the quickest through 2031?

Asia Pacific is projected to lead with a 24.60% CAGR, driven by Aadhaar-linked wallets in India and the region’s expanding mobile-payment ecosystem.

Page last updated on: