Single Loop Controller Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

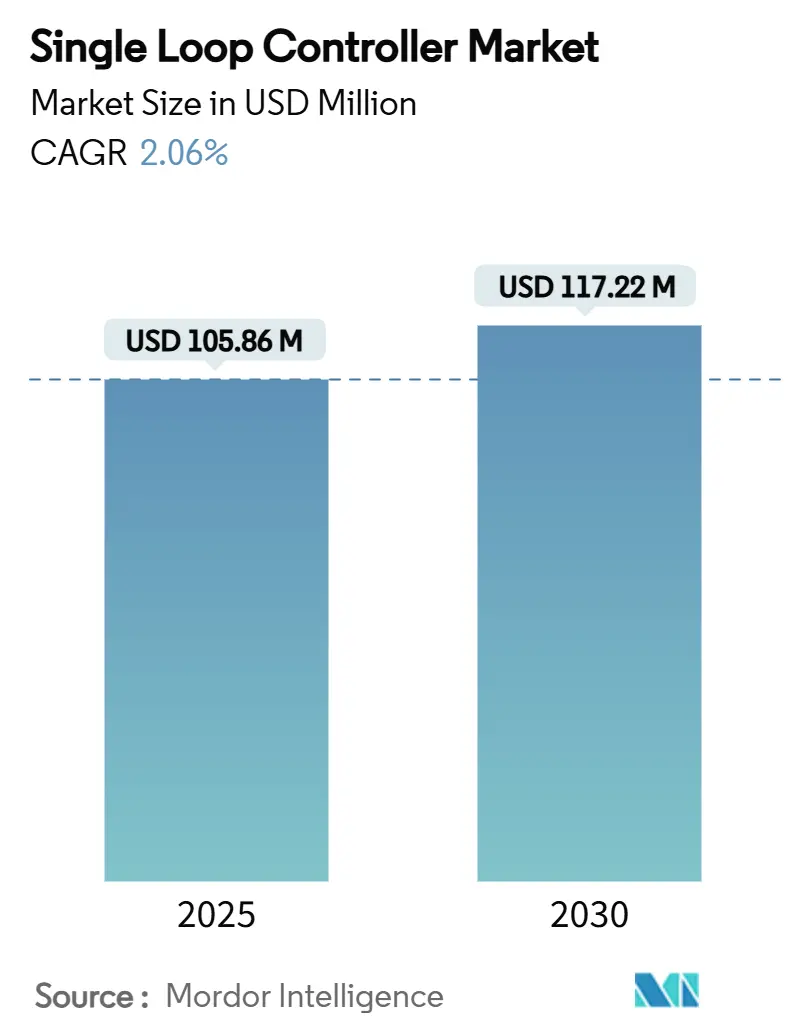

| Market Size (2025) | USD 105.86 Million |

| Market Size (2030) | USD 117.22 Million |

| Growth Rate (2025 - 2030) | 2.06% CAGR |

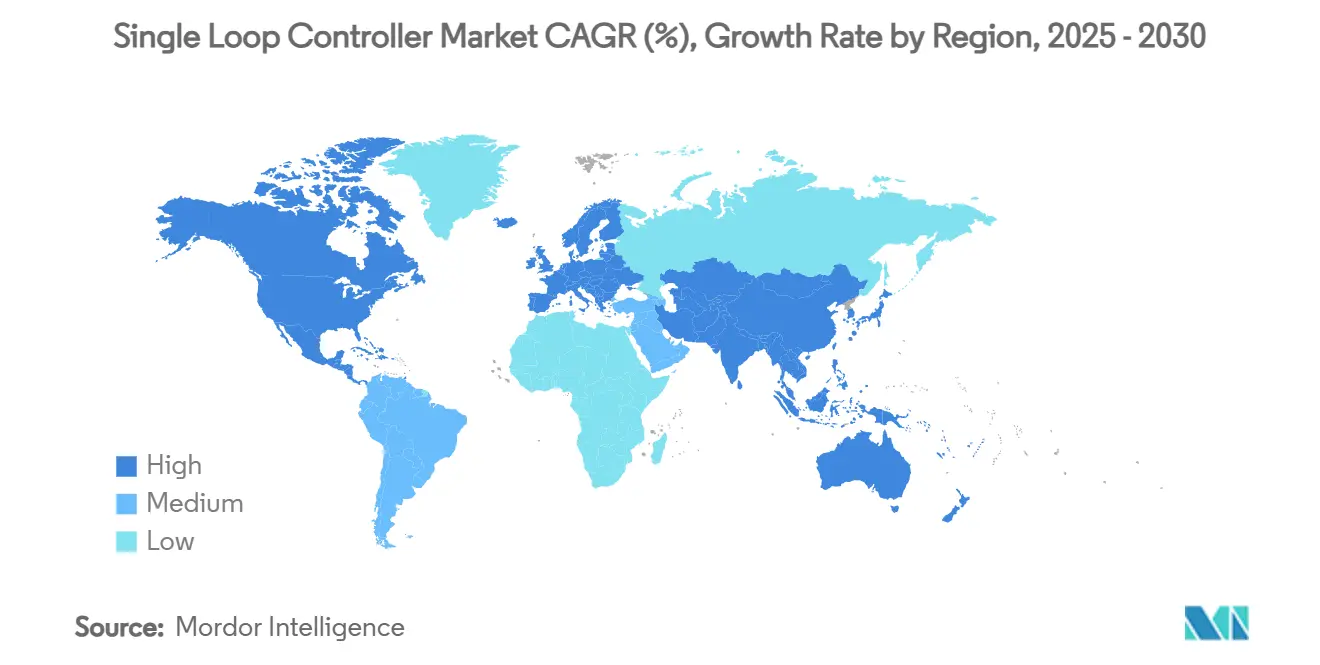

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single Loop Controller Market Analysis by Mordor Intelligence

The single loop controller market size is estimated at USD 105.86 million in 2025 and is forecast to expand to USD 117.22 million by 2030, reflecting a measured 2.06% CAGR over the period. [1]Jerry Van Staalduine, “When Pneumatic Standalone Controllers Age Out,” InTech Magazine, May 01, 2024, automation.com The growth path signals a maturing landscape in which digital transformation, energy-efficiency mandates and remote-monitoring requirements steadily displace aging pneumatic installations. Demand concentrates on retrofit activity, led by process industries that see value in plug-and-play modularity, cloud connectivity and advanced diagnostics. Competitive intensity rises as Asian vendors undercut prices, prompting established multinationals to differentiate through software-defined platforms, cybersecurity hardening and life-cycle services. Supply-chain tightness for industrial-grade microcontrollers and an industry-wide shortage of skilled PID-tuning personnel temper near-term momentum, but opportunities remain solid in safety-integrity upgrades and battery gigafactory build-outs.

Key Report Takeaways

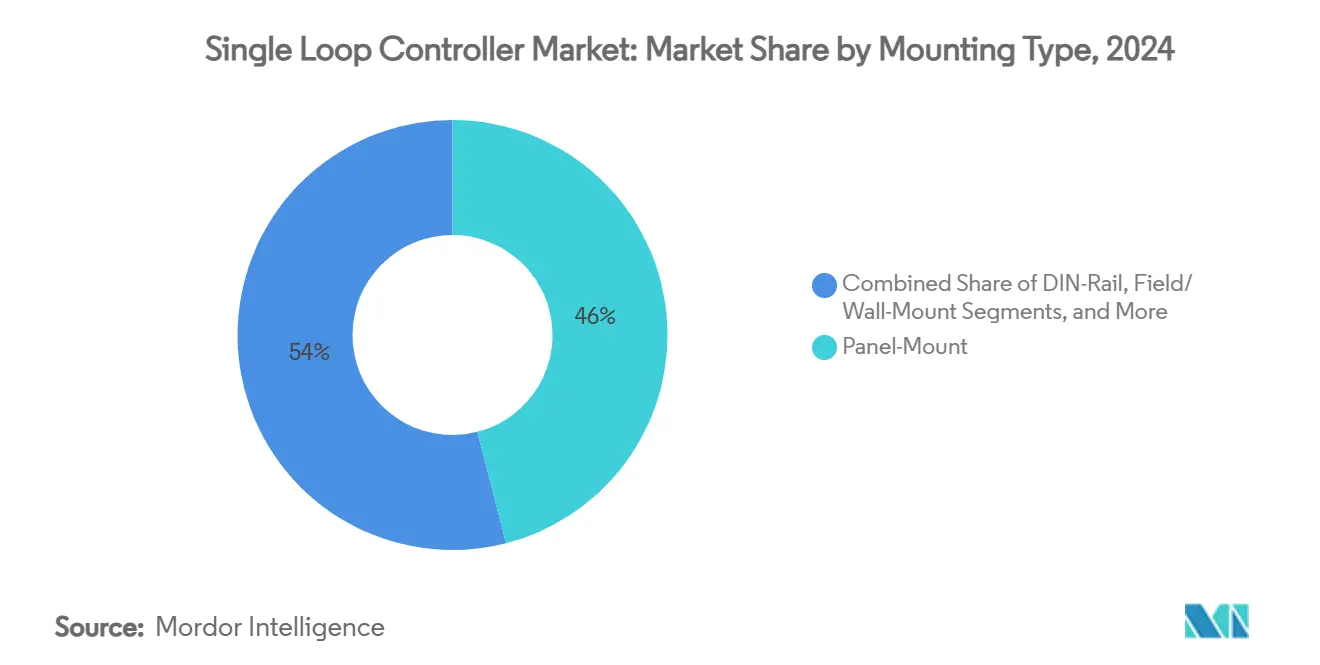

- By mounting type, panel-mount units led with 46% of the single loop controller market share in 2024, while DIN-rail devices posted the fastest 2.90% CAGR to 2030.

- By control algorithm, PID solutions accounted for 66% revenue share of the single loop controller market size in 2024; fuzzy/adaptive controllers are projected to grow at a 3.10% CAGR through 2030.

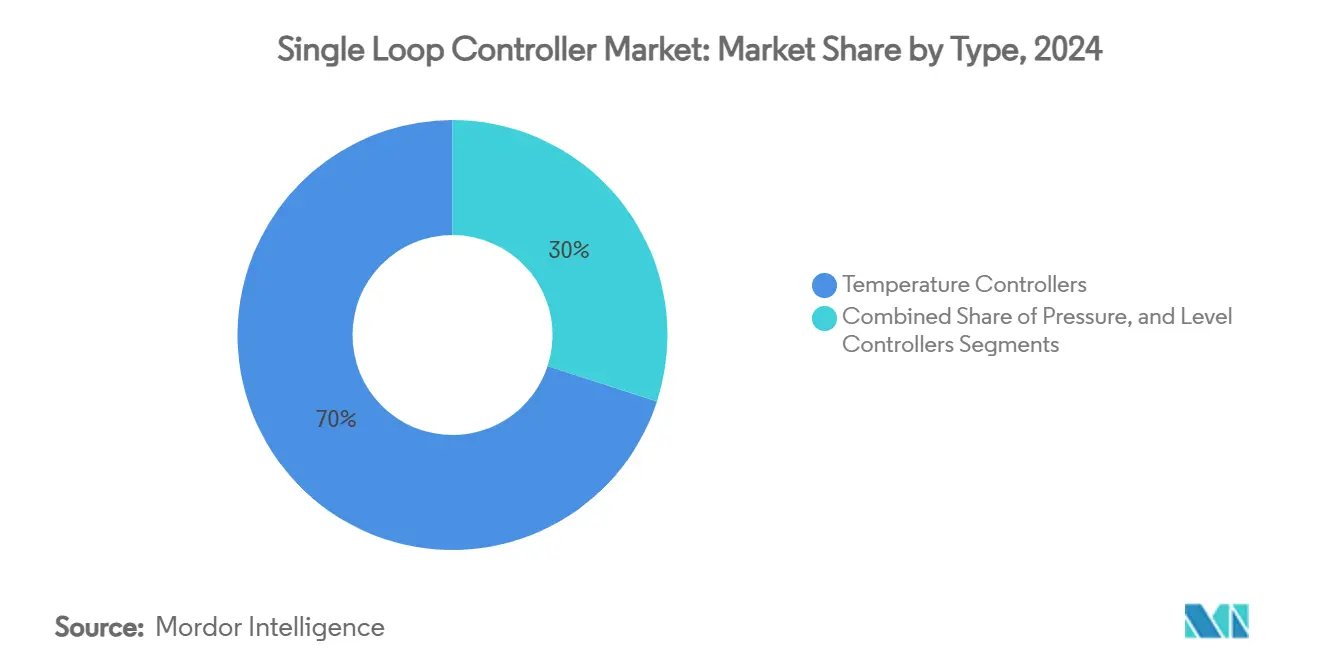

- By type, temperature controllers held 70% share of the single loop controller market size in 2024, whereas pressure controllers are on track for a 2.80% CAGR to 2030.

- By end-user industry, chemicals and petrochemicals retained 24% revenue share, and pharmaceuticals are forecast to post the highest 3.00% CAGR through 2030.

- By geography, Asia Pacific retained 43% revenue share, and is forecast to post the highest 3.20% CAGR through 2030.

Global Single Loop Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of energy-efficient HVAC retrofits | +0.40% | North America and EU core, global spill-over | Medium term (2-4 years) |

| IIoT-enabled remote monitoring roll-outs | +0.50% | APAC‐led global adoption | Short term (≤ 2 years) |

| Process-industry migration from pneumatic to digital PID | +0.30% | Global industrial hubs | Long term (≥ 4 years) |

| Rapid build-out of EV-battery gigafactories | +0.20% | APAC focus, North America and EU follow | Medium term (2-4 years) |

| Plug-and-play DIN-rail modularity | +0.20% | Advanced manufacturing clusters | Short term (≤ 2 years) |

| Safety-integrity controllers for brownfield upgrades | +0.10% | North America and EU first, APAC next | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Energy-Efficient HVAC Retrofits

Escalating utility costs and carbon-reduction mandates fuel a surge in smart HVAC conversions. Digital controllers integrated with building-management systems deliver 9-10% operational energy savings over legacy pneumatic setups and unlock remote diagnostics and flexible scheduling that enhance occupant comfort and asset valuation. [2]IEA Study Team, “Comparing the Life Cycle Costs of a Traditional and a Smart HVAC Control System for Australian Office Buildings,” Journal of Building Engineering, Aug 15, 2024, sciencedirect.com Facility owners recognise the positive net-present cost over fifty-year lifecycles and are accelerating retrofits despite higher upfront expenditure. This momentum sustains baseline demand for temperature-loop control units, reinforcing the single loop controller market’s stability in commercial and industrial buildings.

IIoT-Enabled Remote Monitoring Roll-Outs

Modern single loop controllers embed Ethernet, OPC UA and MQTT to stream real-time data into cloud dashboards and predictive-maintenance platforms. Manufacturers gain visibility across distributed sites, cut unplanned downtime and reduce maintenance costs by 10-30% through condition-based routines. [3]Bill Mueller, “AI in My PID Loops? It’s More Likely Than You’d Expect,” Automation World, Apr 07, 2025, automationworld.com Edge analytics further optimise loop performance, making IIoT connectivity a decisive purchase criterion, particularly in APAC factories aiming to leapfrog older architectures. Short-term demand uplift is therefore strongest in segments offering out-of-box secure connectivity.

Process-Industry Migration from Pneumatic to Digital PID

More than 2.3 million pneumatic controllers remain in service yet vendors have exited product support, exposing plants to reliability and compliance risks. Digital PID replacements provide tighter control, remote adjustability and advanced functions such as set-point filtering that cut variability. Chemical, refining and food plants map phased conversion strategies, sustaining long-term growth for the single loop controller market as digital devices become the de-facto standard.

Rapid Build-Out of EV-Battery Gigafactories

Battery cell production demands strict temperature, humidity and pressure tolerances; scrap rates can exceed 30% without closed-loop precision. Gigafactory projects across China, Korea, the United States and Europe therefore specify high-accuracy single loop controllers that integrate with Manufacturing Execution Systems for continuous quality assurance. Medium-term uptick in orders supports segment growth despite macroeconomic uncertainty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price erosion from low-cost Asian entrants | -0.3% | Worldwide, sharpest in Western markets | Short term (≤ 2 years) |

| Scarcity of skilled PID-tuning personnel | -0.2% | Global, acute in high-automation regions | Medium term (2-4 years) |

| Cyber-hardening compliance costs | -0.1% | Critical infrastructure worldwide | Long term (≥ 4 years) |

| Supply-chain scarcity of industrial-grade MCUs | -0.2% | Global, high-performance segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Erosion from Low-Cost Asian Entrants

Chinese and Taiwanese vendors leverage scale economies and state-backed automation programs to offer controllers at prices 20-30% below Western competitors, squeezing margins and shifting purchasing criteria from feature depth to total cost of ownership. [4]Citigroup Global Markets, “China: Rise of Industrial Robots,” Citigroup Insight, Jun 08, 2024, citigroup.com Mid-tier brands face the toughest squeeze and must pivot to value-added software and support services to retain share in the single loop controller market.

Scarcity of Skilled PID-Tuning Personnel

Without trained technicians, plants risk sub-optimal loop tuning that erodes quality and energy performance, slowing controller upgrades and increasing life-cycle costs. Moreover, many single-loop controllers remain under- or over-tuned due to a lack of skilled personnel. This mis-tuning results in problems such as oscillations, overshooting, or sluggish responses. Consequently, process efficiency diminishes, deterring end-users from adopting or upgrading to advanced controllers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mounting Type: DIN-Rail Gains Despite Panel Dominance

Panel-mount solutions contributed 46% revenue in 2024, anchored in legacy cabinets and retrofit projects across refineries and pharmaceutical clean-rooms. DIN-rail configurations, however, command a 2.90% CAGR as OEMs adopt compact enclosures that reduce wiring and speed commissioning. The single loop controller market size for DIN-rail products is expected to climb proportionally with modular production-line expansions. Field/wall-mount and embedded PCB variants fill niche roles in harsh or space-constrained environments, keeping the product mix diverse.

Adoption accelerates because DIN-rail devices align with IEC 61355 control-panel standards, accept hot-swappable I/O cartridges and integrate cybersecurity modules. Vendors market pre-engineered kits that cut panel build time by 30%, an efficiency gain attractive to systems integrators facing labour shortages. This form-factor shift underscores how hardware architecture choices can influence the single loop controller market trajectory.

By Control Algorithm: PID Dominance Faces Adaptive Challenge

PID technology retained 66% share of the single loop controller market in 2024 owing to its regulatory familiarity and proven robustness. Fuzzy/adaptive algorithms, advancing at 3.10% CAGR, appeal to operations teams seeking self-optimising loops in batch reactors and furnace controls. The single loop controller market size attached to adaptive solutions remains modest but gains visibility as AI-assisted tuning tools reduce engineering effort. On/off and proportional control maintain roles in simple HVAC dampers and pump speed loops where cost trumps precision.

Algorithmic evolution now focuses on layering machine learning on top of classical PID to preserve compliance documents while enhancing disturbance rejection. This hybrid path shields plants from validation risks and accelerates acceptance in regulated sectors such as pharma, reinforcing PID’s incumbency even as innovation advances.

By Type: Temperature Control Leadership Under Pressure

Thermal loops accounted for 70% of revenue in 2024, a reflection of heat-critical operations in food sterilisation, polymer extrusion and semiconductor wafer processes. Pressure-loop deployments, though smaller, show 2.80% CAGR driven by stricter safety requirements in high-pressure reactors and hydrogen pipelines. The single loop controller market share of temperature devices will gradually dilute as multi-parameter instrumentation integrates temperature and pressure sensing into unified modules.

Safety Integrity Level 2 mandates accelerate demand for controllers with integrated diagnostics and redundant outputs in hydroprocessing depressurisation systems. Vendors integrating SIL-rated relay drivers and proof-test routines position themselves for premium bids, particularly within oil, gas and chemical megaprojects.

By End-User Industry: Pharmaceuticals Accelerate Past Chemicals

Chemicals and petrochemicals held 24% share in 2024 owing to continuous-process dependence on stable loop control. Pharmaceutical plants, expanding at 3.00% CAGR, invest in single-purpose skids and continuous tablet-coating lines that favour dedicated single loop controllers over complex DCS nodes. Food and beverage, power generation and oil and gas provide steady baseline demand, while metals, pulp and paper and water treatment diversify revenue streams.

Within life-sciences, Process Analytical Technology initiatives drive controller count as each critical quality attribute receives its own tightly monitored loop. This requirement supports premium pricing for containment-rated enclosures and CFR 21 Part 11 compliant audit trails.

Geography Analysis

Asia Pacific owned 43% of 2024 revenue and is posting a leading 3.20% CAGR thanks to greenfield manufacturing capacity, infrastructure upgrades and automation incentives across China, India, Japan, Korea and ASEAN. China’s plan for 500 robots per 10,000 workers by 2025 drives controller adoption in ancillary hydraulic and thermal loops that surround robotic cells. Meanwhile, Singapore’s smart-nation policy and India’s PLI scheme spur demand for loop controllers embedded in new pharmaceutical and electronic factories. Regional small-to-mid-tier vendors leverage cost advantage yet high-end specifications still tilt toward global brands.

North America is a replacement-driven arena where aging refineries and chemical plants modernise control panels during scheduled shutdowns. Schneider Electric’s USD 700 million capital programme through 2027 aims to support digitalisation and meet reshoring momentum, promising incremental pull-through for connected loop devices. U.S. cybersecurity directives for water and power utilities heighten demand for hardened hardware, further differentiating premium providers.

Europe shows modest unit growth but brisk demand for energy-efficiency retrofits and safety upgrades. Germany’s process industries pursue carbon-neutral targets, adopting loop controllers that integrate energy-performance dashboards. Roland Berger notes the region’s pharmaceutical and food equipment segments could post up to 9% CAGR, cushioning softness in basic manufacturing. High regulatory compliance costs favour vendors with local service hubs and certification expertise.

The Middle East and Africa and South America remain smaller contributors. Yet petrochemical investments in Saudi Arabia and desalination infrastructure in the Gulf necessitate corrosion-resistant loop controllers, while Brazil’s ethanol and mining sectors gradually adopt advanced control to improve yields.

Competitive Landscape

The single-loop controller market is moderately fragmented. Top multinationals, Yokogawa, Honeywell, ABB, and Schneider Electric, combine legacy installed bases with cloud analytics suites, sustaining brand preference. Mid-sized European specialists and a proliferation of Asian manufacturers add depth. Competitive strategy centers on four key levers, software-defined controllers that decouple hardware from firmware, cybersecurity certifications to meet IEC 62443 standards, embedded analytics that reduce engineering hours, and X-as-a-Service commercial models.

Recent moves illustrate these priorities. ABB’s Q2 2025 record USD 9.8 billion order intake signalled a strong process-automation pull, validating its focus on digital service bundles. Emerson’s Project Beyond introduced the DeltaV IQ software-defined controller, positioning the firm for edge-to-cloud orchestration and AI loop optimisation. HMS Networks’ acquisition of Red Lion expands its protocol-conversion portfolios, which are vital for retrofit markets. Schneider Electric’s U.S. expansion funds local manufacturing to shorten lead times amid rising reshoring demand, while Omron’s data-solutions strategy highlights service revenue ambitions.

Pricing pressure remains an omnipresent theme. Asian entrants offer 20-30% discounts on conventional panel-mount units, forcing incumbents to advance modularity and security features unattractive to low-cost rivals. Supply-chain headwinds in microcontrollers also favour companies with multi-sourcing strategies and in-house firmware agility.

Single Loop Controller Industry Leaders

Yokogawa Electric Corporation

Honeywell International Inc.

Omron Corporation

ABB Ltd.

Watlow Electric Manufacturing Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Emerson launched Project Beyond with the DeltaV IQ Controller built for standard servers, embedding AI orchestration to cut deployment complexity and loop-tuning hours.

- February 2025: Delta Electronics has unveiled its DTDM Series of High-Precision Modular Temperature Controllers. Tailored for wholesalers, distribution channels, and major system integrators, especially in the semiconductor sector, the DTDM Series boasts unmatched precision, swift data exchange, and a sleek, modular design.

- October 2024: Novus Automation has unveiled its latest N1020 PID Controller, tailored for compact applications with space constraints. This model is particularly favored in laboratories, packaging equipment, and other benchtop devices.

- July 2024: Emerson’s DeltaV Version 15 Feature Pack 2 improved Ethernet protocol support and state-based execution, aligning DCS and single loop controller environments for unified analytics.

Global Single Loop Controller Market Report Scope

| Panel-Mount |

| DIN-Rail |

| Field / Wall-Mount |

| Embedded / PCB-Mount |

| On/Off |

| Proportional |

| PID |

| Fuzzy / Adaptive |

| Temperature Controllers |

| Pressure Controllers |

| Level Controllers |

| Chemicals and Petrochemicals |

| Food and Beverage |

| Power Generation |

| Pharmaceuticals |

| Oil and Gas |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| South korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Mounting Type | Panel-Mount | ||

| DIN-Rail | |||

| Field / Wall-Mount | |||

| Embedded / PCB-Mount | |||

| By Control Algorithm | On/Off | ||

| Proportional | |||

| PID | |||

| Fuzzy / Adaptive | |||

| By Type | Temperature Controllers | ||

| Pressure Controllers | |||

| Level Controllers | |||

| By End-User Industry | Chemicals and Petrochemicals | ||

| Food and Beverage | |||

| Power Generation | |||

| Pharmaceuticals | |||

| Oil and Gas | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| Singapore | |||

| South korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the single loop controller market in 2025?

It is projected to reach about USD 105.86 million in 2025, continuing its steady growth from 2024’s USD 104.4 million baseline.

Which region grows fastest for single loop controllers?

Asia Pacific leads with a 3.20% CAGR through 2030, supported by greenfield manufacturing and government automation incentives.

Why are DIN-rail controllers gaining popularity?

Their modular, hot-swappable design cuts installation time and supports Industry 4.0 connectivity, driving a 2.90% CAGR despite panel-mount dominance.

What sectors drive demand after 2025?

Pharmaceuticals, EV-battery manufacturing and energy-efficient HVAC retrofits are the prime demand engines through the decade.

Page last updated on: