Advanced Process Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

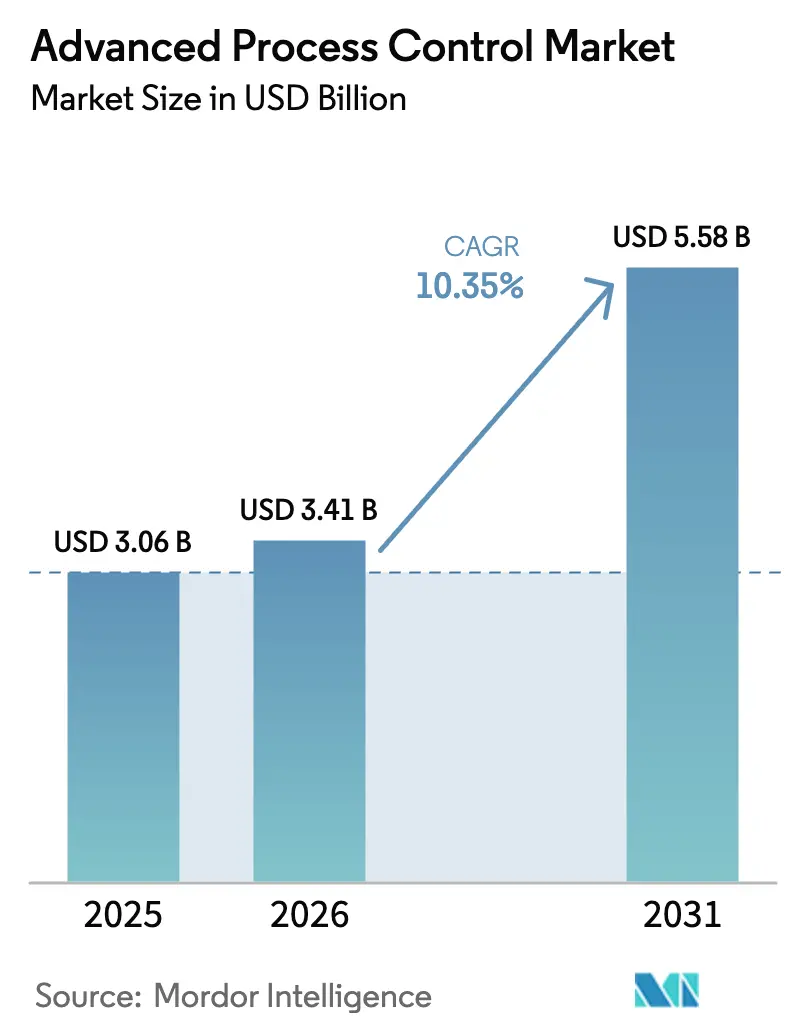

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 5.58 Billion |

| Growth Rate (2026 - 2031) | 10.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Process Control Market Analysis by Mordor Intelligence

The Advanced Process Control Market size was valued at USD 3.06 billion in 2025 and is estimated to grow from USD 3.41 billion in 2026 to reach USD 5.58 billion by 2031, at a CAGR of 10.35% during the forecast period (2026-2031).

Escalating energy volatility, carbon-reduction mandates, and the spread of cloud-native architectures are nudging plant operators away from reactive troubleshooting toward predictive, AI-assisted optimization that lifts throughput and trims emissions. Real-time electricity price swings of EUR 50–100 (USD 56–113) per megawatt-hour now force refiners and chemical producers to re-balance heat, steam, and power every 15–30 minutes, a pace that legacy distributed control systems cannot maintain without model predictive overlays. Simultaneously, hybrid cloud deployment dissolves the barrier between on-site historians and remote analytics, letting mid-tier specialty chemical firms and modular LNG operators tap enterprise-grade optimization without heavy capital layouts. Competitive intensity is rising as AI-native startups compress commissioning from months to weeks, while incumbents respond with acquisitions, cloud subscriptions, and edge-embedded neural models. These shifts open opportunities for recurring services, particularly cybersecurity audits and digital-twin upkeep, which augment traditional software licenses.

Key Report Takeaways

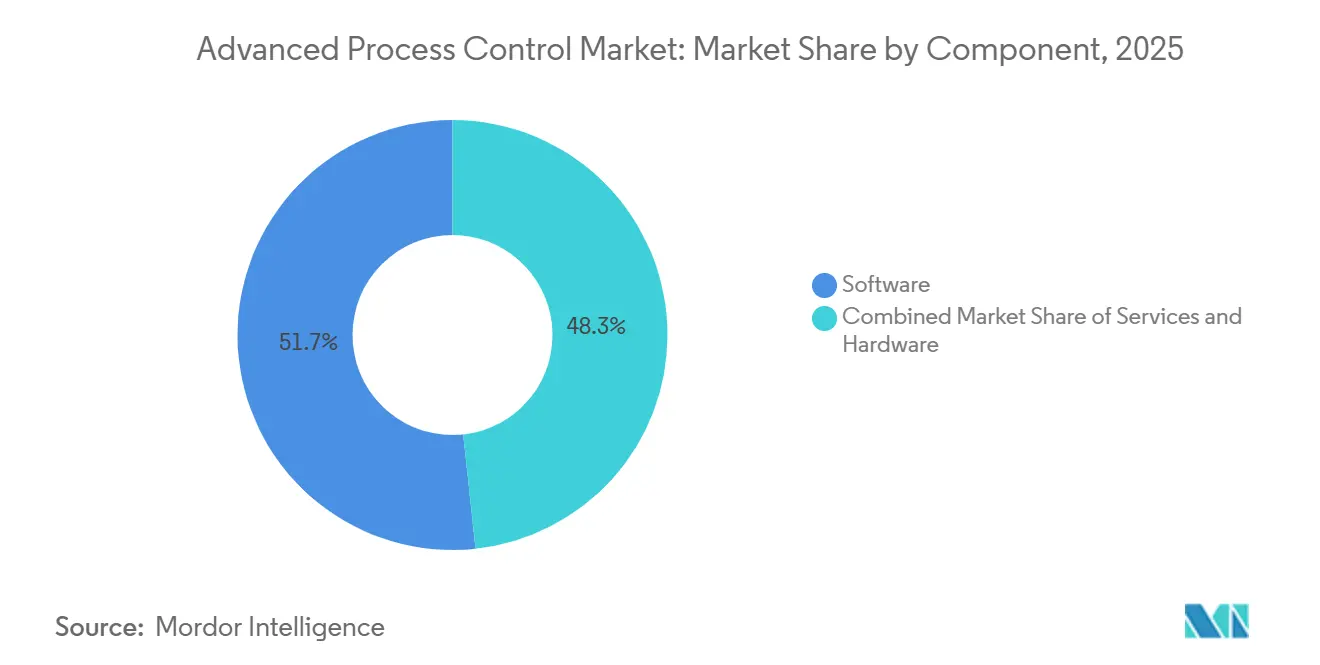

- By component, software captured 51.71% of revenue in 2025, while services are projected to grow at an 11.22% CAGR through 2031.

- By product type, advanced regulatory control led with 38.28% revenue share in 2025, and non-linear MPC is forecast to grow at a 10.84% CAGR to 2031.

- By deployment mode, on-premises accounted for 62.06% of installations in 2025, whereas cloud-based configurations are advancing at a 10.96% CAGR to 2031.

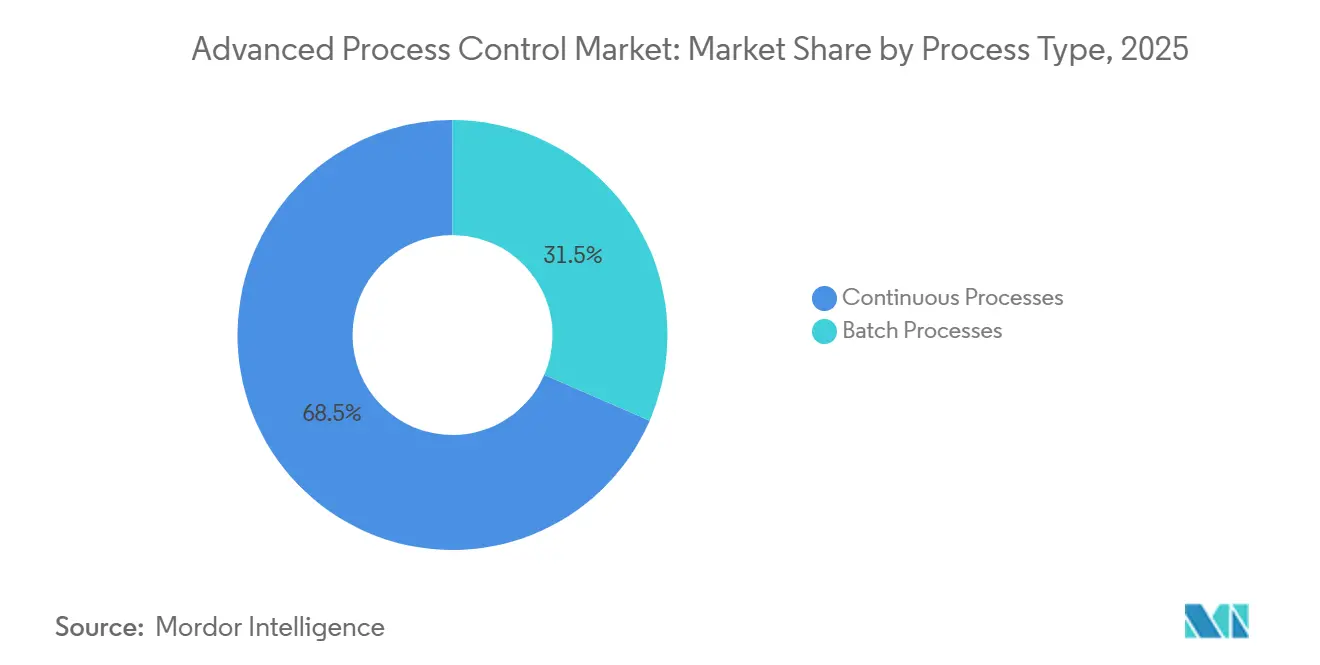

- By process type, continuous operations held 68.48% of the advanced process control market share in 2025 and batch applications are expanding at an 11.22% CAGR through 2031.

- By end-user industry, oil and gas commanded 31.45% of spending in 2025, while pharmaceutical is the fastest-growing segment at an 11.47% CAGR to 2031.

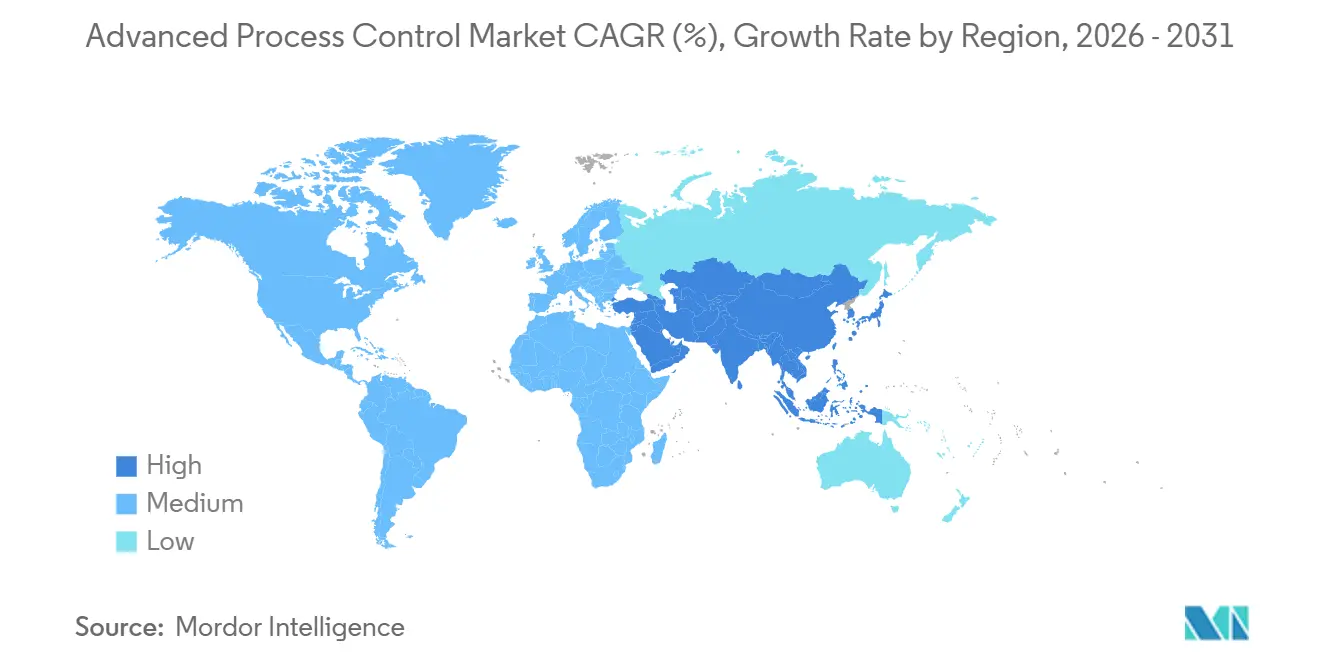

- By geography, Asia Pacific generated 34.53% of 2025 revenue and is projected to increase at an 11.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Process Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Time Energy Cost Optimisation Needs | +2.10% | Global, with peak impact in Europe and North America due to deregulated electricity markets | Short term (≤ 2 years) |

| Integration of APC with IIoT and AI Analytics | +2.50% | Global, led by Asia Pacific manufacturing hubs and North American chemical corridors | Medium term (2-4 years) |

| Emission-Driven Regulatory Stringency | +1.80% | Europe (EU ETS Phase 4, Industrial Emissions Directive), North America (EPA methane rules), China (dual carbon targets) | Long term (≥ 4 years) |

| Complexity of Mega Specialty Chemical and LNG Projects | +1.30% | Middle East (Qatar North Field, Saudi Jafurah), North America (Gulf Coast LNG), Asia Pacific (Australia LNG expansions) | Medium term (2-4 years) |

| Plug-and-Play Cloud APC for Modular Skids | +1.00% | Global, with early adoption in North America modular refining and Asia Pacific distributed chemical production | Medium term (2-4 years) |

| Edge-Embedded AI Enables Self-Optimising Remote Operations | +1.40% | Global, concentrated in remote oil and gas fields (Middle East, Russia, offshore platforms) and mining operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Real-Time Energy Cost Optimisation Needs

Volatile spot power and gas prices are forcing plant economics teams to treat energy as a moving constraint, not a fixed line item. In Germany’s liberalized market, day-ahead auction prices now swing by more than EUR 100 (USD 113) within a single session, compelling chemical complexes to shift batch starts to off-peak windows or curtail load during spikes.[1]EPEX SPOT, “European Power Exchange Market Data,” epexspot.com Advanced process control loops ingest tariff feeds, then automatically trim reflux ratios, compressor draws, and steam let-downs to preserve margin. U.S. Gulf Coast refiners face similar pressure when regional gas hubs decouple from Henry Hub; controllers capable of re-routing feed and adjusting heater duty every few minutes can unlock double-digit percentage savings in utility spend.[2]U.S. Energy Information Administration, “Natural Gas Weekly Update,” eia.gov Plants that deploy these capabilities typically recover software subscription costs within 12–18 months, accelerating board approval for follow-on optimization projects.

Integration of APC with IIoT and AI Analytics

Edge gateways now preprocess vibration, temperature, and spectral data locally, pushing anomaly scores straight into model predictive constraint matrices. This fusion lets controllers derate equipment before failure rather than reacting to alarms. Emerson’s DeltaV Edge Environment embeds TensorFlow-Lite models on field controllers, using pressure-drop and heat-flux proxies to estimate composition and sidestep the 10-minute lag of on-line chromatographs.[3]Emerson Electric, “DeltaV Distributed Control System,” emerson.com When AspenTech coupled Mtell predictive maintenance with DMC3 control at a Gulf Coast cracker, turnaround intervals stretched by nearly a year, freeing USD 25 million of uptime. Policy adds tailwinds: China’s State Council wants half of large factories to run smart manufacturing systems by 2025, making IIoT-APC convergence a board-level metric.

Emission-Driven Regulatory Stringency

Tightened caps reposition advanced process control from performance enhancer to compliance essential. Europe’s 2024 Industrial Emissions Directive lowered refinery NOx thresholds by up to 40%, forcing dynamic combustion tuning that only multivariable control can execute repeatably. The U.S. EPA methane rule now mandates quarterly leak detection plus real-time monitoring of pneumatic valves, pushing operators toward low-bleed actuators whose movements are logged and optimized in historian databases. China’s dual-carbon pathway adds intensity benchmarks that penalize cement, steel, and petrochemical plants unless they can prove continuous optimisation via certified APC software.[4]Ministry of Ecology and Environment of China, “Dual Carbon Strategy,” mee.gov.cn Vendors bundle ISO 14001 and IEC 62443 documentation with licenses to shorten permitting cycles.

Complexity of Mega Specialty Chemical and LNG Projects

Megaprojects integrate dozens of units with shared utilities, so disturbances propagate in seconds. QatarEnergy’s North Field expansion will coordinate eight liquefaction trains sharing refrigerant loops, a task that demands plant-wide optimisation rather than unit-level loops. Venture Global’s mid-scale LNG trains start and stop to chase spot cargoes; non-linear MPC sequences the rapid swings without breaching pressure limits. Specialty chemical giants such as BASF operate 200 interlinked plants; a steam imbalance in one reactor can ripple across the site unless advanced regulatory control maintains overall mass-energy balance. Each project earmarks 3–5% of installed cost for automation, creating multi-million-dollar tenders that reward vendors with deep domain models and onsite expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Integration Complexity | -1.20% | Global, with acute impact in South America and Africa due to limited capital availability and fragmented industrial base | Short term (≤ 2 years) |

| Scarcity of APC Expertise and Model Maintenance Burden | -0.90% | Global, particularly severe in Middle East and Africa where industrial automation talent pools are thin | Medium term (2-4 years) |

| Cybersecurity Exposure in Cloud-Native Control Loops | -0.60% | North America and Europe, where critical infrastructure regulations mandate air-gapped OT networks | Short term (≤ 2 years) |

| Model Degradation in Bio-Based Continuous Fermentation Lines | -0.40% | North America and Europe pharmaceutical and bio-refinery clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Integration Complexity

Full-plant optimisation can cost USD 500 000 for a single controller or USD 10 million for a site-wide suite. Retrofitting older control systems demands historian upgrades, segmented networks, and custom fieldbus gateways, stretching budgets and schedules. A recent industry survey found 42% of operators delayed projects when commissioning overshot vendor timelines by more than 30 percent, usually due to unplanned loop interactions. South American plants built with 1980s pneumatic instrumentation must first digitize analog signals, adding months of work and pushing payback beyond corporate hurdles. Subscription licensing eases the initial cash hit, yet annual fees above USD 100 000 still deter companies whose balance sheets require two-year payback.

Scarcity of APC Expertise and Model Maintenance Burden

Multivariable controllers need retuning every 6–12 months as catalysts age and fouling shifts heat transfer. The global pool of engineers who can perform step tests and update gains is thinning; many baby-boomer specialists retire by 2030 while university enrolment in chemical engineering contracts. Middle East refineries rely on expatriates who rotate every two to three years, preventing deep process knowledge accumulation. Vendors now market auto-tuning algorithms and cloud model-management hubs, but these add dependency on proprietary ecosystems and raise intellectual-property concerns when sensitive models sit on third-party servers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

In 2025, software represented 51.71% of revenue as model predictive control packages, inferential sensors, and real-time optimizers formed the core of advanced process control market value. Services, however, are forecast to expand at an 11.22% CAGR through 2031, outpacing hardware because plants need quarterly retuning, digital-twin synchronization, and IEC 62443 penetration tests to keep controllers at peak performance. Subscription models convert capital expense to operating expense, aligning with financial preferences in cyclical industries. Emerson’s DeltaV SaaS bundles licenses, hosting, and quarterly health checks under a per-controller fee, cutting entry friction for mid-tier producers. Hardware still matters where latency permits no cloud round-trip; polymer reactors and catalytic crackers keep edge servers local to maintain sub-100 millisecond loop times.

Second-generation deployments expose a hard lesson: neglected models decay. Two decades ago, nearly half of installed controllers drifted out of service within three years. Today, vendors bake maintenance into contracts, and some even guarantee performance; if KPI thresholds slip, subscription discounts kick in. This service-heavy approach not only stabilizes revenue but also tightens customer lock-in, intensifying competition among suppliers that can marshal deep benches of domain specialists.

By Product Type: Non-Linear MPC Tackles Complex Processes

Advanced regulatory control accounted for 38.28% of revenue in 2025, yet non-linear MPC is projected to rise at a 10.84% CAGR thanks to feedstock variability and biologics fermentation that linear models cannot capture. Multivariable predictive control remains the backbone for steady-state units such as crude distillation where gains stay quasi-linear. Inferential controls flourish where analyzers are scarce; a Middle East refinery replaced six chromatographs with neural soft sensors and saved USD 400 000 in annual maintenance.

Continuous pharmaceutical fermenters illustrate the shift. Cell growth kinetics vary almost hourly, so Aspen Hybrid Models blend first-principles and machine learning to update gains on the fly, cutting potency variation by 18%. Polymer producers echo the need; melt-index targets move with catalyst lot changes, making adaptive models essential. While regulators scrutinize black-box AI, vendors improve transparency with bound-constrained optimization and model explainability modules, satisfying safety-instrumented-system auditors.

By Deployment Mode: Cloud Gains Despite Latency Concerns

On-premises installations held 62.06% of 2025 projects as critical-infrastructure regulations still favour air-gapped networks. Yet cloud-based setups will grow at a 10.96% CAGR to 2031 because hybrid architectures keep fast loops on edge devices while offloading model training and fleet benchmarking to hyperscale data centers. Honeywell Forge running in Microsoft Azure lets refiners compare energy intensity across multiple sites in real time, then download optimized constraint matrices overnight. Data-sovereignty rules temper uptake in the Middle East, but North American chemicals already pilot cloud APC on one in five greenfield projects.

Edge AI resolves the latency impasse. ABB Edgenius runs TensorFlow on rugged servers next to the control room, sustaining sub-100 millisecond execution and synchronizing weights with the cloud daily. Modular LNG skids exploit this model: pre-configured strategies arrive from vendor repositories, load in hours, and start optimizing before first product. The remaining barrier is cyber-risk; the Colonial Pipeline ransomware episode triggered mandatory segmentation and multi-factor authentication, so vendors race to document IEC 62443 compliance.

By Process Type: Batch Grows as Pharma Shifts to Continuous

Continuous processes delivered 68.48% of advanced process control market revenue in 2025 as refining and petrochemicals squeezed 2–5% more yield from model predictive control. Batch operations, mainly in pharma and specialty chemicals, will expand at an 11.22% CAGR because regulators now encourage real-time release testing and single-use bioreactors that need adaptive recipes. Siemens SIMATIC Batch uses gain-scheduled models that adjust control weights during every phase, trimming off-spec material by 12% in fine-chem plants. The line between batch and continuous blurs in modern biologics, where perfusion reactors run for weeks but still require periodic biomass purges that traditional steady-state MPC cannot accommodate alone.

Food processors join the trend under FSMA. Inferential sensors predict microbial load from pH and dissolved oxygen, letting pasteurizers fine-tune duty in real time and preserve flavour. In bio-based chemicals, pseudo-steady fermenters run continuously yet face feed-sugar swings, so hybrid control that blends batch recipe logic with continuous MPC emerges as the best fit.

By End-User Industry: Pharma Accelerates on Continuous Manufacturing

Oil and gas spent 31.45% of total in 2025, leveraging APC to maximize valuable light products, adjust crude blends, and shave energy from steam networks. Pharmaceutical outpaces every other vertical with an 11.47% CAGR to 2031. Continuous direct-compression tablet lines hold API concentration within ±2% by adjusting feed rates based on Raman spectroscopy, a precision unattainable in legacy batch suites. Regulators grant expedited review for facilities that prove real-time quality assurance, turning APC from optional to obligatory.

Chemicals and petrochemicals rely on multivariable control to tame polymer reactors where temperature, pressure, and catalyst charge interact within seconds. Energy and power firms use APC on combined-cycle turbines to balance steam extraction and combustor splits, squeezing extra megawatts when renewables depress wholesale prices. Cement, metals, pulp, and paper apply controllers mostly for energy and emissions, yet even small savings on thousand-ton-per-day kilns or digesters mean millions in annual cost avoidance.

Geography Analysis

Asia Pacific held 34.53% of 2025 revenue and will advance at an 11.81% CAGR through 2031, the fastest pace worldwide. China backs smart-factory retrofits with grants that refund up to 20% of automation spend, prompting coal-to-chemicals complexes in Inner Mongolia and refinery-petrochemical hubs in Zhejiang to install plant-wide MPC. India’s Production-Linked Incentive scheme reimburses greenfield pharmaceutical automation, with twelve plants commissioning cloud-hosted controllers in 2025 alone. Japan’s Society 5.0 policy steers aging food and fine-chemical lines toward intuitive operator support, while South Korean petrochemical clusters retrofit 1990s control systems to meet 35% greenhouse-gas cut mandates by 2030.

North America and Europe grow nearer to the overall market rate yet lead in advanced deployments. Fifteen ethylene crackers added since 2020 on the U.S. Gulf Coast all include optimisation suites that juggle furnace duty, quench cooling, and separation to maximize olefin yields. Europe’s stricter emissions limits push cement and steel mills to integrate continuous monitoring with combustion control, a match suited to multivariable algorithms. German chemical complexes facing triple the U.S. gas cost rely on steam-network balancing MPC to hit one-year paybacks.

Middle East and Africa, South America, and emerging Asian nations display mixed adoption. Saudi Arabia’s Jafurah gas program installs edge AI on remote skids so technologists in Dhahran supervise wells hundreds of kilometers away. Offshore Brazil fields use subsea multiphase optimisation to lift production when topside Asia Pacific pinches. South Africa’s coal-to-liquid plants adopt regulatory-driven control of Fischer-Tropsch reactors to curb CO₂ intensity under a ZAR 190 (USD 10) per ton carbon tax. Barriers persist; scarce local talent, lean capital budgets, and patchy vendor support often limit projects to single-unit pilots rather than full-site rollouts.

Regulatory Landscape

Regulation impacting advanced process control (APC) is increasingly shaped by cybersecurity obligations for connected industrial automation and by quality-system expectations in regulated manufacturing, notably pharmaceuticals. The EU NIS2 Directive pushes operators toward demonstrable OT risk management, with compliance commonly mapped to IEC 62443 controls, while the EU Cyber Resilience Act introduces product side vulnerability reporting duties starting September 11, 2026, followed by broader cybersecurity requirements from December 11, 2027. In regulated process industries, standards and policy signals sharpen expectations for validated, audit-ready control strategies rather than ad hoc tuning. ASTM E3424-25 released May 1, 2025 provides guidance for development and validation considerations of APC in commercial pharmaceutical manufacturing, supporting approaches that link control models, data integrity, and change management under GMP. Policy shifts also influence project timelines: the European Commission proposed an Industrial Accelerator Act in March 2026 to streamline permitting for net-zero industrial projects through single access points and digitized procedures, while in the United States a July 2026 Presidential Proclamation granted a 2 year compliance extension for certain stationary sources under the EPA HON Rule, affecting how some chemical operators sequence compliance and modernization initiatives.

Competitive Landscape

The advanced process control market is moderately consolidated; the top five suppliers account for roughly 60% of global revenue. ABB, Emerson, Honeywell, Siemens, and Yokogawa leverage their distributed control footprints to cross-sell optimisation modules bundled with multi-year service. Emerson’s USD 11 billion acquisition of AspenTech in 2022 knit simulation, asset performance, and real-time control into a single stack, echoing Rockwell’s 2023 purchase of Plex Systems that aligned MES with batch optimisation. Each incumbent now competes on cloud ease-of-use and edge AI latency rather than core MPC math, which has commoditized.

Disruptors such as Imubit and C3 AI train neural controllers directly on historian data, bypassing the months-long step-test routine. Imubit’s installation at the San Roque refinery in Spain claims 2–5% margin uplift within weeks, challenging the consulting-heavy model of traditional vendors. Cybersecurity certification emerges as a new moat; IEC 62443 audits consume scarce expertise and budget, giving global conglomerates an edge. Regional preferences also shape the field. Chinese producers buy from domestic suppliers like SUPCON due to procurement policies and sovereignty concerns, while multinational LNG operators demand worldwide 24/7 support that only the largest firms can deliver.

Advanced Process Control Industry Leaders

ABB Ltd.

Aspen Technology Inc.

Emerson Electric Co.

Honeywell International Inc.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace for APC vendors sits at the intersection of industrial AI adoption and the practical readiness gaps plants cite in networking, security, and IT/OT operating models. Cisco reported in March 2026 that 61 percent of organizations use AI in live industrial operations, while only 20 percent describe deployments as mature, a gap that aligns with demand for packaged, supported APC plus data, cybersecurity, and model governance offerings rather than stand-alone software. Large greenfield and expansion projects in LNG and petrochemicals anchor high value control, safety, and optimization scopes, broadening the base for APC layers on top of integrated control and safety systems. In 2026, ABB expanded its automation and electrical scope for Rio Grande LNG Trains 4 and 5 in Texas, and Yokogawa secured the Main Automation Contractor role for the USD 13 billion Commonwealth LNG project in Louisiana (9.5 mtpa), signaling demand for plant wide integration where APC and optimization modules are typically bundled into commissioning and lifecycle support. In emerging market petrochemicals and refining, Honeywell agreed in April 2026 to supply process technologies and catalysts for Dangote Petroleum Refinery and Petrochemicals expansion (including new propylene and linear alkylbenzene output targets), while Schneider Electric partnered with Petrobras on automation and electrical systems for Abreu e Lima refinery Train 2 resumption, highlighting opportunities tied to modernization, throughput debottlenecking, and energy efficiency programs in brownfield assets.

Recent Industry Developments

- June 2026: Honeywell announced the global rollout of Experion Cognition, an AI enabled platform targeting more autonomous control room operations, and showcased a deployment at the Ruwais facility for Borouge International. The rollout extends Honeywell's control software stack toward AI assisted decisioning and operator workload reduction, aligning APC with workforce constraints and higher frequency optimization use cases.

- November 2025: ADNOC announced framework agreements totaling AED 2.6 billion with major automation suppliers including ABB, Emerson, Schneider Electric, Honeywell, and Yokogawa for integrated control, safety, and automation systems to be manufactured in the UAE.

- April 2024: Emerson deployed DeltaV PredictPro at Covestro's Barcelona facility to optimize polyester production as part of Covestro's net-zero 2035 program.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending on advanced process control used to stabilize, predict, and optimize industrial processes in continuous and batch plants. It includes APC software, the supporting hardware that is directly tied to the APC layer, and related services such as implementation and ongoing support.

Scope exclusions: Stand-alone PLC, SCADA, and basic DCS or PID-only control functions without embedded APC logic are excluded.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Product Type

- Advanced Regulatory Control (ARC)

- Model Predictive Control (MPC)

- Non-Linear MPC

- Multivariable Predictive Control

- Inferential and Other Controls

- By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid

- By Process Type

- Continuous Processes

- Batch Processes

- By End-User Industry

- Oil and Gas

- Chemicals and Petrochemicals

- Pharmaceutical

- Food and Beverage

- Energy and Power

- Cement

- Metal Processing

- Pulp and Paper

- Rest of End-User Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work begins by building the demand picture by industry and region, then aligning it to what APC solutions are deployed to do in plants. We reference public sources such as the US Energy Information Administration, the International Energy Agency, the USGS for metals and mining indicators, trade bodies for refining and chemicals, and the World Bank for industrial output and investment signals.

To keep assumptions grounded, we also use annual reports, investor decks, product documentation, and reputed press coverage to map how APC is packaged in practice (licenses, subscriptions, upgrades, and maintenance). In some cases, paid subscriptions for company financials, patent databases, and news and financials are used to track product emphasis and major contract activity that can shift near-term demand. This desk source list is illustrative only, and other public references were also used to collect data, validate direction, and clarify open questions.

Primary Interviews and Surveys

Primary conversations were used to check what is being counted as APC in real buying cycles, and how much of the spend sits in software versus attached services and integration time. We spoke with solution providers, system integrators, plant engineering teams, and process control specialists across APAC, EMEA, and the Americas to pressure-test adoption drivers, pricing movement, and the timing of modernization projects.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 29% | EMEA: 30% |

| Smaller Players: 16% | Managers: 58% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up model sequence. Process-industry activity levels and automation intensity are translated into an addressable APC demand pool, then converted into spend using adoption and pricing assumptions. To keep the outputs practical, we corroborate results with selective bottom-up approximations such as sampled license and service pricing, channel checks with integrators, and a roll-up of visible revenue signals from APC-focused offerings. Where gaps show up, the totals are adjusted.

Key inputs in the model include capacity additions in refining and chemicals, plant utilization and throughput trends, the rate of control system modernization, APC penetration in brownfield upgrades, the typical software plus services mix, and the pace of subscription shifts versus perpetual licensing. When data is incomplete for a specific country or end use, we fill gaps using proxy indicators such as industrial output growth and project pipeline signals, and then validate the implied spend per site through primary feedback.

Forecasting uses scenario analysis, since capex cycles and retrofit timing can swing year to year. Adoption curves and ASP progression are set using expert consensus and checked against macro indicators so the outlook aligns with realistic plant investment behavior.

Data Validation & Update Cycle

Outputs are validated through multiple checks, starting with reconciling the model with independent signals such as process-industry investment trends and automation spending direction. If a region shows an unusual jump or decline, the drivers are re-tested, assumptions are revisited, and follow-up calls are triggered to confirm whether the change is real or a modeling artifact.

Before publication, the work is reviewed in steps so definitions, currency handling, and year alignment stay consistent across tables and narratives. Reports are refreshed annually, and interim updates are made when a material event changes demand expectations. Right before delivery, a final pass is done so clients receive the most current view available at that time.

Mordor Intelligence's Global Advanced Process Control Market Industry Analysis Gro Market Size Versus Other Published Estimates

Published APC market numbers often do not match because the included product layers and revenue types vary, and the year used for currency conversion and inflation treatment can change the total. Differences in how services, upgrades, and maintenance are treated can also move the estimate up or down, especially when multi-year projects are involved.

Some published figures run broader by blending basic control layers or adjacent automation software into the APC total. For Mordor Intelligence, the count is limited to advanced, model-based or inferential APC logic and the related software, plus supporting hardware tied to the APC layer. It also includes associated services such as implementation, upgrades, and maintenance, which keeps the spend aligned to true APC deployments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.41 B (2026) | |

| Industry Publisher A | USD 2.05 B (2024) | Uses an earlier base year and a different forecast window, and the scope emphasizes software and services by type. This can undercount APC-linked hardware and later-period subscription uplift. |

| Industry Publisher B | USD 2.73 B (2025) | Anchors the market in a different base year and applies a component split that can shift what is labeled as APC. There is limited clarity on how upgrades, maintenance, and multi-site rollouts are normalized across regions. |

The spread in values is mainly explained by timing and by which product layers get counted around the APC function, not by a single pricing assumption. When scope rules are written clearly and checked against plant activity signals, the market size becomes easier to trace and repeat from one update cycle to the next.

Key Questions Answered in the Report

What is the current value of the advanced process control market?

The advanced process control market size is USD 3.41 billion in 2026 and is set to climb steadily to USD 5.58 billion by 2031.

Which component segment is growing the fastest?

Services covering commissioning, retuning, and cybersecurity are projected to expand at an 11.22% CAGR through 2031 as plants prioritize continuous optimization.

Why is Asia Pacific the fastest-growing region?

Public subsidies for smart-factory retrofits in China and incentive schemes in India propel Asia Pacific to an 11.81% CAGR, the highest regional rate.

How are cloud deployments addressing latency concerns?

Hybrid architectures keep sub-second loops on local edge servers while moving model training and analytics to the cloud, delivering performance without sacrificing security.

Which industries will add the most new APC projects?

Pharmaceutical facilities shifting to continuous manufacturing show the quickest uptake, followed by specialty chemicals and modular LNG plants that demand agile optimization.

Page last updated on: