Multi Domain Controller Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 4.84 Billion |

| Growth Rate (2026 - 2031) | 14.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Multi Domain Controller Market Analysis by Mordor Intelligence

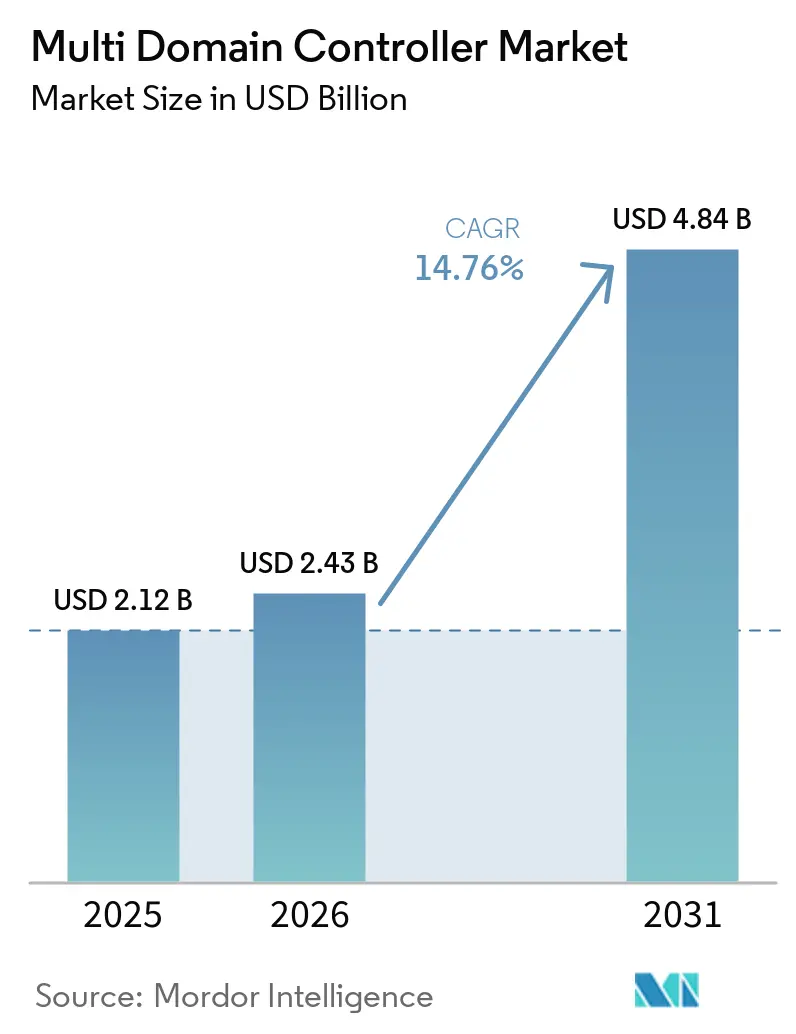

The multi-domain controller market is projected to grow from USD 2.12 billion in 2025 to USD 2.43 billion in 2026, reaching USD 4.84 billion by 2031, with a CAGR of 14.76% from 2026 to 2031. Consolidation of advanced driver-assistance, cockpit, power-train, and body functions on fewer high-performance processors is replacing the legacy network of separate electronic control units. Automakers favor this architecture because it simplifies over-the-air updates and meets new cybersecurity and functional-safety mandates. Asia-Pacific already leads revenue generation and is growing faster than North America and Europe as local brands invest in vertically integrated hardware and software stacks. Semiconductor vendors are moving up the value chain with turnkey controller kits, pressuring incumbent tier-one suppliers and accelerating platform standardization across vehicle classes.

Key Report Takeaways

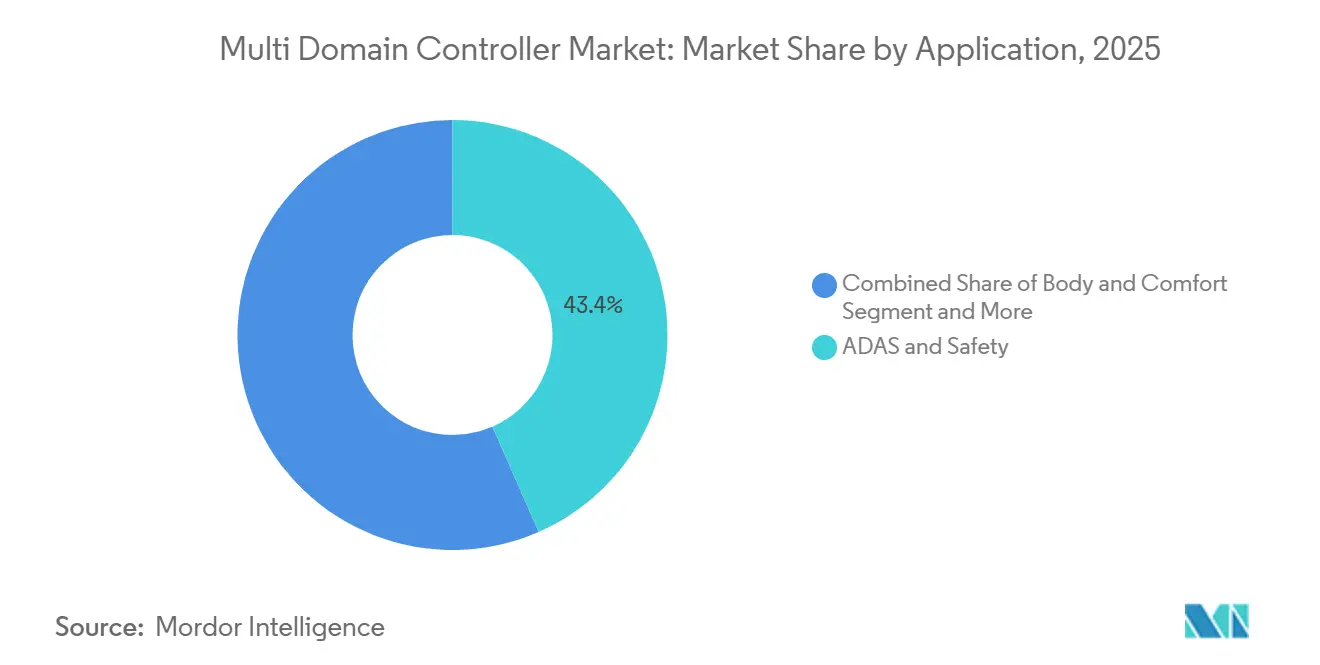

- By application, ADAS and Safety commanded 43.44% of the multi-domain controller market share in 2025, while Cockpit Electronics is advancing at an 18.21% CAGR through 2031.

- By vehicle type, passenger vehicles accounted for 66.19% of the multi-domain controller market share in 2025 and are growing at a 15.01% CAGR over 2026-2031.

- By propulsion type, battery-electric vehicles held a 39.31% of the multi-domain controller market share in 2025 and are expanding at a 18.21% CAGR to 2031.

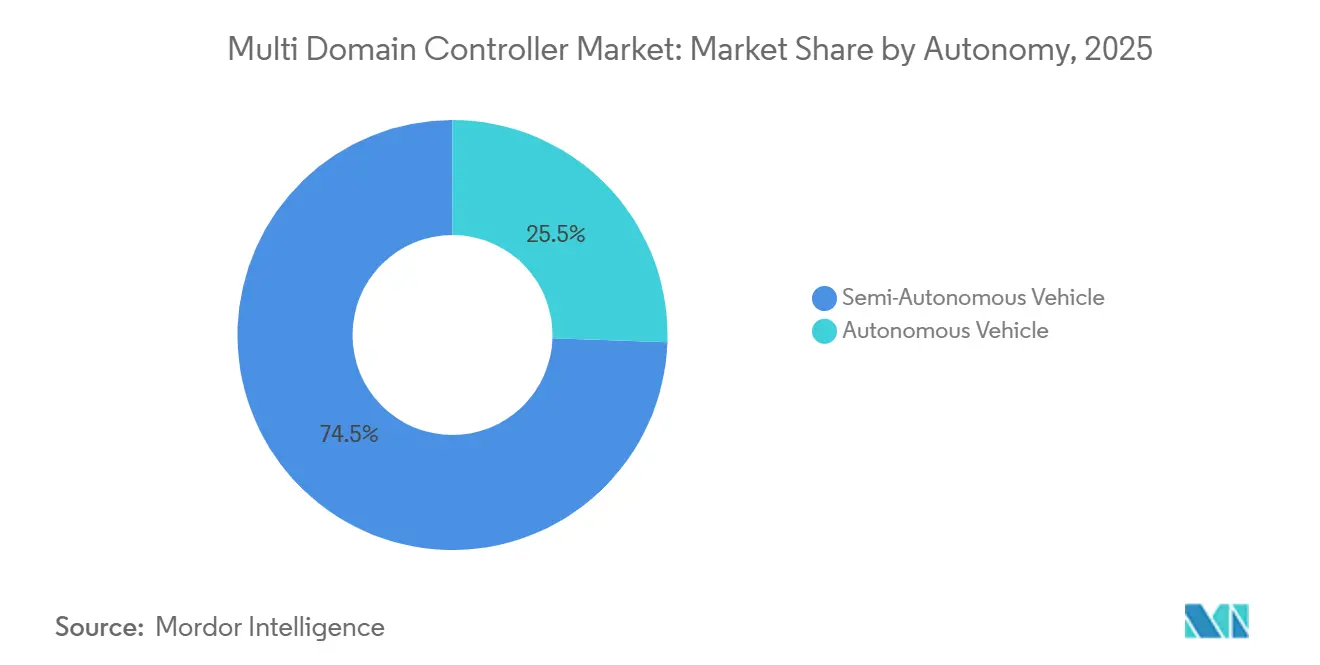

- By autonomy, semi-autonomous vehicles accounted for 74.47% of the multi-domain controller market share in 2025, whereas autonomous vehicles are projected to grow at a 21.52% CAGR through 2031.

- By operating system, QNX secured 48.61% of the multi-domain controller market share in 2025, and Linux is pacing the field with a 19.82% CAGR through 2031.

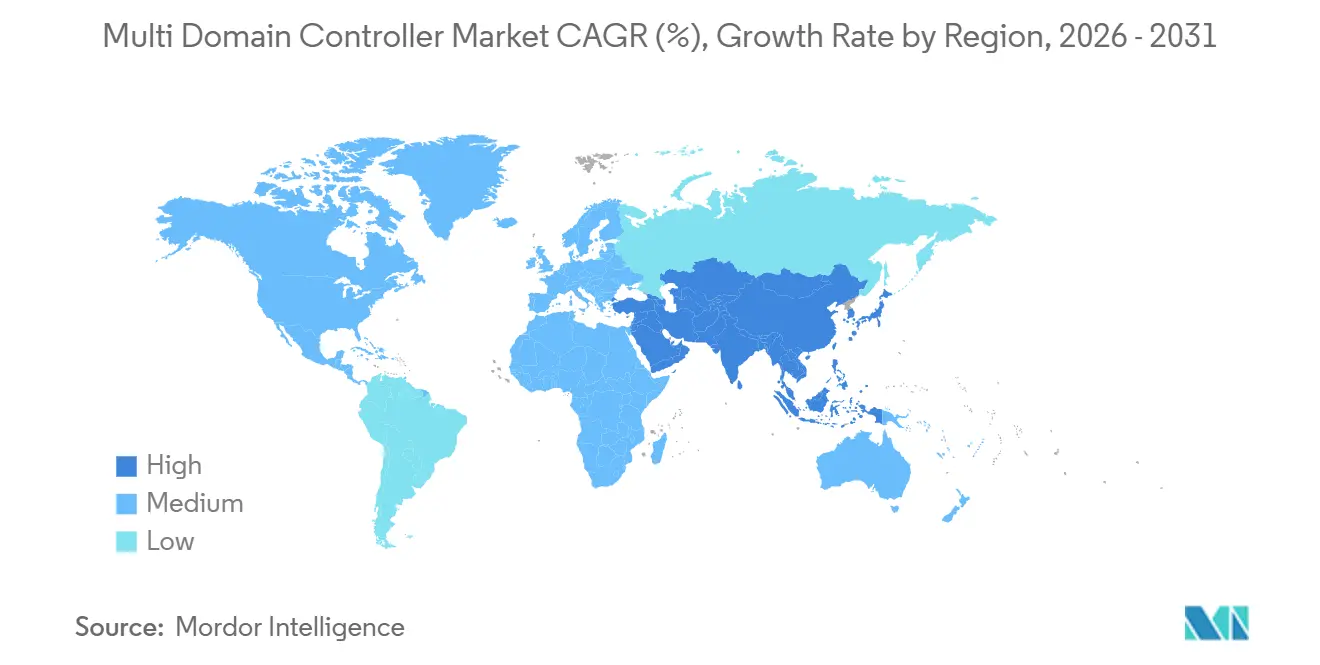

- By geography, Asia-Pacific maintained 40.34% of the multi-domain controller market share in 2025 and is poised for a 15.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi Domain Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| L2-L3 Autonomy Rollout | +2.5% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Centralized and Zonal E/E Architectures | +2.1% | North America & EU early adopters, APAC following | Long term (≥ 4 years) |

| OTA Capability | +1.6% | Global, with premium segments first | Medium term (2-4 years) |

| Functional-Safety Regulation | +0.9% | EU and North America mandatory, APAC voluntary adoption | Short term (≤ 2 years) |

| One-Board → One-Chip Fusion | +0.7% | Premium vehicle segments globally | Long term (≥ 4 years) |

| Automotive Chiplet | +0.6% | Technology leaders in US, Germany, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ADAS Penetration and L2-L3 Autonomy Rollout

Automakers are standardizing lane-keeping, automated parking, and highway pilot features that rely on fused radar, camera, and lidar data. Centralized controllers eliminate latency between separate units and trim material cost by sharing memory and power resources. Qualcomm’s latest Snapdragon platform shows how a single board can support hands-free driving in mainstream models[1]"Revolutionizing the road ahead", Qualcomm Technologies, qualcomm.com. Regulatory requirements for automatic emergency braking in China and Europe lock in minimum compute thresholds that distributed topologies struggle to meet. As sensor suites expand, bandwidth demand reinforces the move to a scalable controller that can be upgraded via software rather than hardware redesign.

Shift Toward Centralized and Zonal E/E Architectures

Zonal designs group wiring by physical location, cutting harness length and weight while simplifying software life-cycle management. BMW’s Neue Klasse platform replaces dozens of legacy units with three zone controllers that host multiple virtual machines under a single hypervisor[2]"Four 'Superbrains' for the Neue Klasse by BMW", BMW Group, bmwgroup.com. Suppliers are releasing reference boards that blend Ethernet switching, power distribution, and real-time processing, giving smaller integrators a faster route to compliance. By consolidating cybersecurity logic into a handful of nodes, automakers also meet UNECE R155 obligations with fewer penetration testing cycles. The result is a repeatable electrical backbone that supports future autonomous upgrades without re-wiring the vehicle.

OEM Push for Software-Defined Vehicles and OTA Capability

Manufacturers see recurring revenue in post-sale feature activation, remote diagnostics, and data-driven services. Centralized controllers provide spare compute headroom, allowing functions to be deployed via firmware rather than new hardware. Over-the-air rollouts cut warranty expenses and dealership visits, a benefit demonstrated by recent partnerships between cloud platform vendors and Asian OEMs. Modular application interfaces reduce supplier lock-in and encourage a competitive ecosystem of software add-ons. This business model depends on a robust, upgradeable controller that can receive security patches and performance enhancements throughout the full vehicle life cycle.

Functional-Safety Regulation (ISO 26262, UNECE R155/156)

Global regulators now require documented safety processes and continuous cybersecurity monitoring. Pre-certified domain controllers help automakers avoid multi-year validation programs, shrinking time-to-market while limiting liability. NVIDIA and other silicon vendors bundle functional-safety libraries that accelerate compliance for sensor fusion and actuation workloads. The cost of developing equivalent capability in-house is prohibitive for smaller entrants, leading to greater reliance on turnkey solutions. As enforcement widens, certification status becomes a primary selection criterion alongside raw performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-Power Limits | -1.2% | Global, particularly affecting premium vehicle segments | Short term (≤ 2 years) |

| ASIL-D Certification Cost/Time | -0.9% | EU and North America primarily, expanding to APAC | Medium term (2-4 years) |

| Tier-1 Vertical Integration | -0.8% | Global, with strongest impact in established automotive regions | Medium term (2-4 years) |

| Global AI-IP Export Controls | -0.5% | US-China trade corridors, affecting global semiconductor supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thermal-Power Limits of High-Compute SoCs

Rising inference workloads generate heat that is hard to dissipate inside dashboards and engine bays. Vendors incorporate predictive throttling and advanced cooling materials, yet sustained peak performance can still drop in extreme climates. Some automakers split tasks across multiple lower-power boards, diluting the cost savings of full consolidation. Packaging constraints are tightest in compact vehicles, where space and airflow are limited. Thermal engineering, therefore, dictates realistic performance envelopes and may slow aggressive one-chip roadmaps.

Complex ASIL-D Certification Cost/Time

Achieving the highest automotive safety integrity level requires exhaustive fault-injection testing, formal code proofs, and third-party audits. Large tier-one suppliers spread these fixed costs across many programs, but newcomers face long timelines and heavy documentation requirements. The hurdle discourages rapid iteration and favors established platforms with proven tool chains. Where certification must be reopened for software revisions, development schedules can slip, eroding first-mover advantage. The expense also narrows the pool of viable suppliers, reinforcing consolidation trends in the multi-domain controller market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: ADAS Commands Revenue While Cockpit Leads Growth

ADAS and safety accounted for 43.44% of the Multi Domain Controller market share in 2025, underscoring the compute-hungry sensor-fusion and object-classification workloads that support highway piloting and automated parking. Automakers rely on centralized boards to cut latency between radar, camera, and lidar inputs, allowing a single processor to supervise multiple perception layers. The standardized hardware also eases over-the-air safety updates, a regulatory priority as lane-keeping and emergency-braking rules widen. Suppliers bundle pre-certified functional-safety software so brands can launch across global regions without repeating long validation cycles. Competitive differentiation now centers on balancing performance, power, and cost while meeting ISO 26262 ASIL-D obligations.

Cockpit electronics is advancing at an 18.21% CAGR through 2031, the fastest pace within the segment hierarchy. Instrument clusters, infotainment, and augmented-reality head-up displays are merging onto a single system-on-chip, shrinking wiring mass and enabling synchronized graphics across screens. A hypervisor separates safety-critical telltales from rich media, allowing one board to host both workloads legally. Automakers value the extra compute headroom because it lets them deploy new user-experience features remotely rather than redesigning hardware. This shift adds subscription revenue potential yet raises thermal-management complexity as graphics and ADAS domains increasingly share silicon.

By Vehicle Type: Passenger Volume Drives Innovation

Passenger vehicles captured 66.19% of the Multi Domain Controller market share in 2025, reflecting high production scale and consumer appetite for advanced driver-assistance features in compact and midsize models. Centralized compute helps brands roll out driver-monitoring cameras, predictive maintenance alerts, and voice-controlled infotainment without adding separate control units. Higher sales volumes spread development cost across millions of cars, enabling premium silicon to reach lower price points quickly. Consumers also expect smartphone-like update cycles, which push passenger-car platforms toward software-defined architectures that permit ongoing feature drops. These dynamics forge a tight loop between cloud analytics and in-car hardware, accelerating the adoption of standardized controller reference designs.

The same passenger segment also posts the fastest 15.01% CAGR over 2026-2031, as emerging markets upgrade to ADAS-equipped vehicles and mature markets refresh fleets to enable over-the-air updates. Fleet buyers in ride-hailing and car-sharing adopt similar hardware because remote diagnostics cut downtime. Automakers offer tiered software packages unlocked by subscription, turning centralized controllers into long-term revenue engines. Competition now centers on balancing cybersecurity, data privacy, and user experience while maintaining cost discipline. Tier-one suppliers that can bundle silicon, middleware, and cloud services hold an execution edge as OEMs race to scale software-defined strategies.

By Propulsion Type: BEV Architectures Reshape Compute

Battery electric vehicles held 39.31% of the Multi Domain Controller market share in 2025, a lead driven by the need to coordinate battery, inverter, and thermal systems in real time. Removing the engine frees space for high-density boards and reduces vibration, which allows tighter packaging around advanced processors. A single controller can balance cell temperatures, schedule fast charging, and modulate regenerative braking, delivering smoother drivability and longer battery life. The integration also reduces harness complexity by routing high-voltage switching and low-voltage data lines through the same zone boxes. Regulators mandating zero-emission sales targets further accelerate the penetration of BEV controllers.

BEVs also post the fastest 18.21% CAGR through 2031 as component prices decline and charging infrastructure expands. Centralized compute supports adaptive torque vectoring and battery health analytics, increasing consumer confidence in electric platforms. Standard interfaces let OEMs swap battery chemistries without rewriting core software, shortening variant launch times. Thermal-budget advantages in engine-less bays permit higher sustained processor loads, so BEVs often debut cutting-edge silicon that later migrates into hybrids and combustion models. The architecture, therefore, sets the design cadence for future controller generations, shaping the broader Multi Domain Controller market.

By Autonomy: Semi-Autonomous Dominates, Fully Autonomous Accelerates

Semi-autonomous vehicles represented 74.47% of the Multi Domain Controller market share in 2025, reflecting regulatory acceptance of hands-free highway systems that still require driver supervision. Centralized compute aggregates environmental perception, driver monitoring, and redundancy checks to keep costs aligned with mass-market price points. Automakers blend edge inference with cloud-delivered map updates, sending new features over the air to extend system capability post-sale. Common hardware also supports comfort upgrades, such as self-parking, which shares sensor inputs with lane-keeping, thereby maximizing silicon utilization. Insurers increasingly recognize the safety benefits, nudging wider adoption across fleet and retail channels.

Autonomous vehicles show the fastest 21.52% CAGR to 2031 as robotaxi pilots graduate to scaled operations. High-reliability controllers deliver over 1,000 TOPS while fitting automotive power envelopes, a feat enabled by advanced 3-nanometer chiplets. Fail-operational architectures host duplicate operating systems and sensor stacks, so a single-board fault does not trigger loss of control. Cities that grant limited Level 4 operating zones provide early revenue for shuttle and logistics services, creating reference deployments that de-risk broader rollouts. As liability frameworks evolve toward manufacturer responsibility, demand rises for pre-certified domain controllers that integrate safety, cybersecurity, and data-logging by design.

By Operating System: QNX Holds Lead While Linux Gains Ground

QNX secured 48.61% of the Multi Domain Controller market share in 2025 because its microkernel, deterministic scheduler, and mature safety manual simplify ISO 26262 compliance. Long partnerships with tier-one suppliers embed the OS deep in legacy infotainment and ADAS stacks, creating switching friction. The vendor supplies hypervisors that isolate guest systems, enabling consolidation of cockpit, powertrain, and body functions on the same chip without cross-interference. Commercial support contracts reassure automakers that field issues will receive prompt patches, a critical need for vehicles expected to remain in service for over a decade. These factors keep QNX entrenched in projects where functional-safety certification is non-negotiable.

Linux demonstrates the fastest 19.82% CAGR to 2031 as OEMs seek royalty-free software and broader developer ecosystems. Community-driven improvements in real-time performance and memory protection make the kernel viable for non-safety workloads, while containerization simplifies application updates. Brands can customize user-interface layers freely, differentiating digital cockpits without altering underlying drivers. Hybrid strategies emerge in which QNX hosts safety functions and Linux powers infotainment, maximizing reuse of existing codebases. As hypervisors mature, the cost of running both systems on a single controller decreases, encouraging further experimentation and accelerating open-source adoption across the multi-domain controller market.

Geography Analysis

Asia-Pacific accounted for 40.34% of the Multi Domain Controller market size and continues to set the technology pace, growing at 15.41% CAGR to 2031. Chinese automakers design controllers in-house to avoid export limits, while Japanese and South Korean brands rely on long-term tier-one partnerships. A dense supplier ecosystem lowers prototype costs and speeds validation, so platforms reach showrooms more quickly. Government mandates for lane-keeping and automatic braking reinforce demand even in entry vehicles, locking in steady controller volume. This virtuous cycle of local silicon, strong policy, and supportive capital keeps the region firmly in front of rivals.

North America is the historical cradle of in-vehicle software and remains a strategic pillar for the Multi Domain Controller market. Domestic original-equipment manufacturers are rolling out highway pilot updates that require unified compute across perception, mapping, and driver monitoring. The region also houses many start-ups that license reference boards to smaller brands, adding fresh competitive pressure. Cybersecurity draft rules from NHTSA require every program to embed secure boot and intrusion detection at the hardware layer, a feature most easily implemented on centralized platforms. Fleet buyers in ride-hailing and last-mile delivery demand controllers that can be swapped curbside, creating a rich after-sales channel.

Europe’s contribution to the Multi Domain Controller market rests on engineering depth and a stringent regulatory framework. Flagship programs such as software-defined vehicle initiatives in Germany and Sweden showcase hypervisors that quarantine safety workloads from infotainment, demonstrating how a single board can respect strict functional-safety doctrine. Delays tied to liability negotiations slow consumer launches, yet the supplier base keeps refining zonal harnesses and chiplet packages so future rollouts will move faster. Middle-East importers layer premium controllers onto luxury models to meet smart-mobility targets, while Africa and parts of South America remain price-sensitive, adopting low-cost hybrids of legacy electronic control units and entry-level domain boards. The collective outcome is a tiered regional mosaic that still funnels global learning back into new silicon road maps.

Competitive Landscape

The Multi Domain Controller market shows a shifting balance between traditional tier-ones and ascendant semiconductor houses. Continental, Bosch, ZF, Aptiv, and Valeo still anchor turnkey programs, but every new request for proposal now lists openness to reference silicon from NVIDIA, Qualcomm, and NXP. Tier-ones respond by buying middleware firms or co-designing chips, hoping to keep system knowledge under one roof. Their strengths in system safety, thermal packaging, and global logistics remain hard to copy, yet price negotiations tighten each season.

Chip makers treat the Multi Domain Controller market as the natural extension of smartphone and data-center playbooks. They bundle graphics, artificial intelligence, and secure-element blocks into monolithic dies or modular chiplets, then attach real-time operating systems that shrink certification cycles. Direct engagement with automakers shortcuts the historic tier-one gatekeepers, though long automotive life cycles test the support muscle of firms used to annual handset refreshes. Volume milestones reached in Asia-Pacific now prove these players can scale, forcing incumbents to streamline quote-to-production workflows.

Software platform vendors add a third axis of competition inside the Multi Domain Controller market. Cloud-native orchestration layers promise automakers the freedom to switch hardware without rewriting applications, a seductive proposition in an era of headline supply shocks. Tier-ones counter with vertically integrated stacks that integrate diagnostics, vehicle-to-cloud gateways, and storefront billing APIs. The final winner may hinge less on raw compute and more on who delivers seamless over-the-air updates, audit-ready security logs, and lifecycle sustainability reporting at the lowest total cost.

Multi Domain Controller Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

ZF Friedrichshafen AG

-

Aptiv PLC

-

Valeo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Garmin unveiled the Nexus high-performance compute platform, built on Qualcomm silicon, to merge cockpit and driver-assistance workloads into a single housing.

- December 2025: Renesas introduced the R-Car X5H, the first automotive multi-domain system-on-chip produced on a 3-nanometer node.

- September 2025: Autolink debuted in Europe with integrated cockpit, parking, and central computing domain controllers to aid automakers upgrading electronic architectures.

- June 2025: NXP Semiconductors partnered with Rimac Technology to launch S32E2 processors for deterministic real-time domain and zonal control in software-defined vehicles.

Global Multi Domain Controller Market Report Scope

The Multi-Domain Controller market is analyzed across application, vehicle type, propulsion type, autonomy, operating system, and geography.

By Application, the market is segmented into ADAS and Safety, Body and Comfort, Cockpit Electronics, and Powertrain. By Vehicle Type, the market is segmented into Passenger Vehicles, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles. By Propulsion Type, the market is segmented into Battery Electric Vehicle, Hybrid Electric Vehicle, Plug-in Hybrid Vehicle, and Internal Combustion Engine. By Autonomy, the market is segmented into Autonomous Vehicle and Semi-Autonomous Vehicle. By Operating System, the market is segmented into QNX, Linux, and Android. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

The Market Forecasts are Provided in Terms of Value (USD).

| ADAS and Safety |

| Body and Comfort |

| Cockpit Electronics |

| Powertrain |

| Passenger Vehicle |

| Light Commercial Vehicle |

| Medium and Heavy Commercial Vehicle |

| Battery Electric Vehicle |

| Hybrid Electric Vehicle |

| Plug-in Hybrid Vehicle |

| Internal Combustion Engine |

| Autonomous Vehicle |

| Semi-Autonomous Vehicle |

| QNX |

| Linux |

| Android |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | ADAS and Safety | |

| Body and Comfort | ||

| Cockpit Electronics | ||

| Powertrain | ||

| By Vehicle Type | Passenger Vehicle | |

| Light Commercial Vehicle | ||

| Medium and Heavy Commercial Vehicle | ||

| By Propulsion Type | Battery Electric Vehicle | |

| Hybrid Electric Vehicle | ||

| Plug-in Hybrid Vehicle | ||

| Internal Combustion Engine | ||

| By Autonomy | Autonomous Vehicle | |

| Semi-Autonomous Vehicle | ||

| By Operating System | QNX | |

| Linux | ||

| Android | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Multi Domain Controller Market?

The Multi Domain Controller market size is projected to expand from USD 2.12 billion in 2025 and USD 2.43 billion in 2026 to USD 4.84 billion by 2031, registering a CAGR of 14.76% between 2026 to 2031.

Which region currently buys the most controllers?

Asia-Pacific leads because local brands integrate hardware and software internally and regulators mandate advanced driver-assistance in high-volume models.

Why are cockpit and ADAS functions merging on one chip?

Modern processors can partition workloads securely with hypervisors, so instrument-cluster graphics and sensor fusion share compute without interference, reducing bill-of-materials cost.

How do suppliers overcome heat buildup in compact cabins?

They use predictive frequency scaling, advanced heat-spreaders, and split workloads across low-power cores to keep temperatures within safe limits.

Page last updated on: