System Integrators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

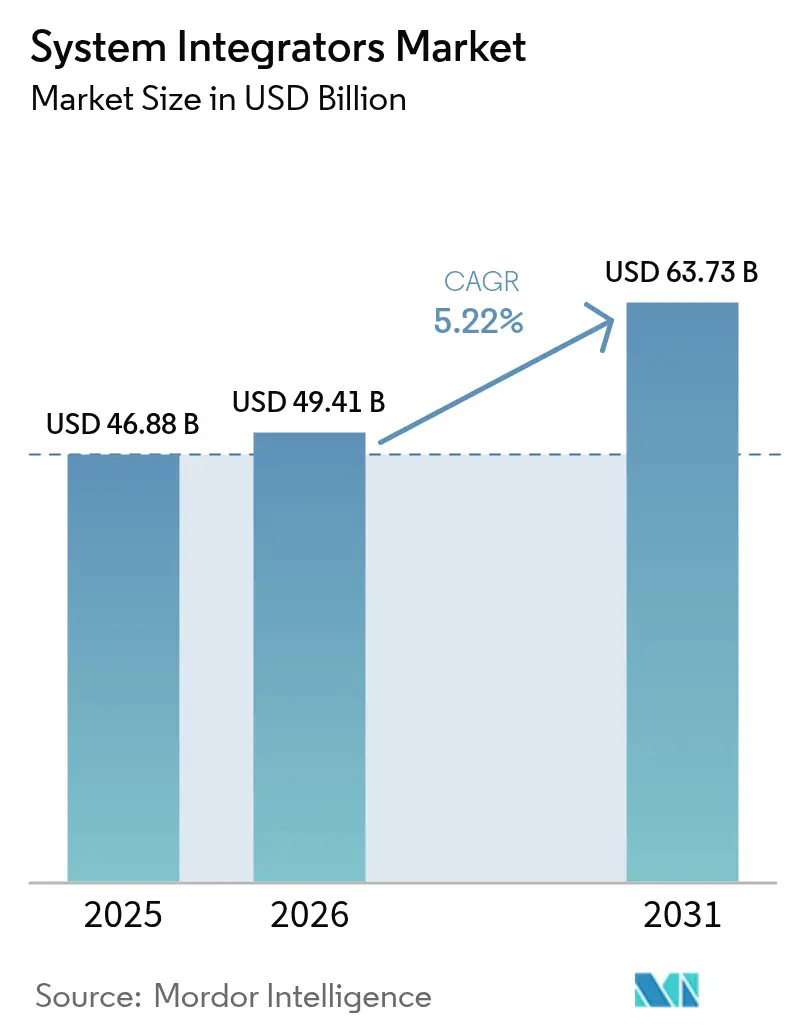

| Market Size (2026) | USD 49.41 Billion |

| Market Size (2031) | USD 63.73 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

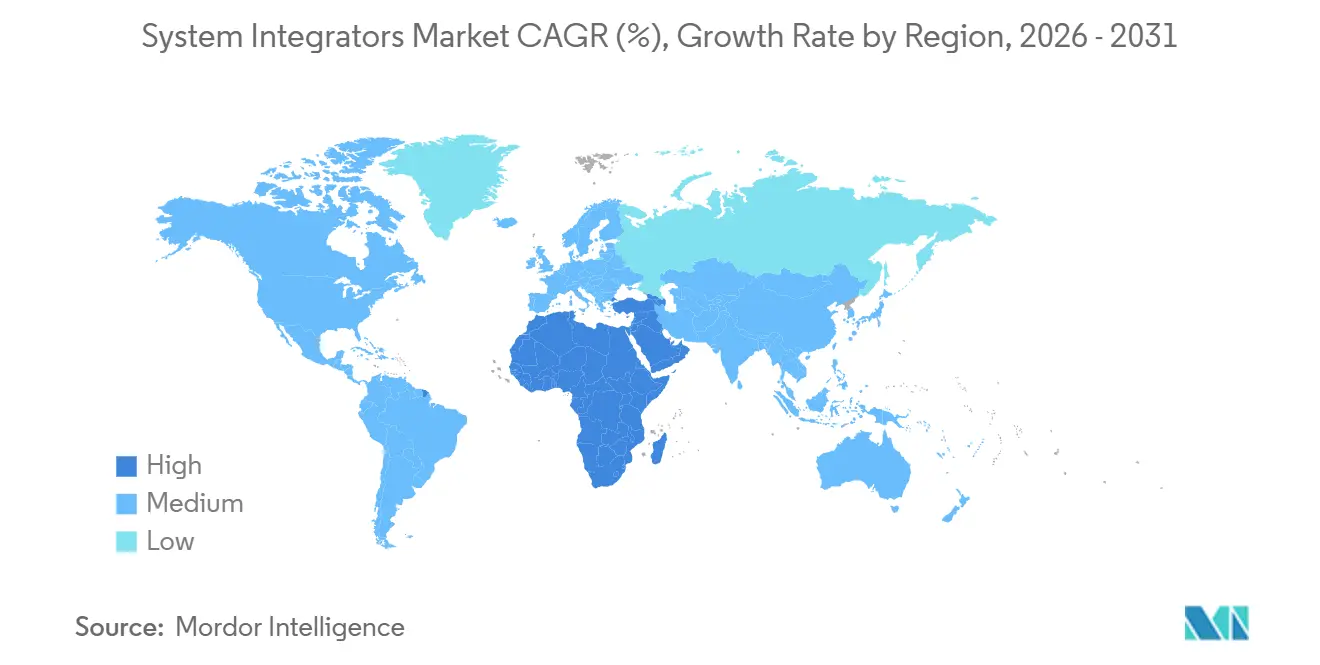

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

System Integrators Market Analysis by Mordor Intelligence

The system integrators market size was valued at USD 46.88 billion in 2025 and estimated to grow from USD 49.41 billion in 2026 to reach USD 63.73 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031). Demand is strengthening as enterprises collapse silos between operational-technology assets and information-technology applications, giving plant managers a single pane of glass for performance, energy, and security metrics. Turn-key projects dominate procurement because in-house automation talent is scarce and aging, so asset owners outsource the integration of programmable logic controllers, distributed control systems, supervisory control and data acquisition layers, manufacturing execution systems, and industrial Internet of Things gateways. Service providers are also winning long-term managed-services contracts that tie fees to uptime, production yield, and cybersecurity posture. Competitive intensity is rising because global automation vendors, consulting firms, and niche engineering houses are all chasing digital-services revenue, and each is expanding geographically to capture greenfield programs in renewables, smart-city infrastructure, and battery-manufacturing plants.

Key Report Takeaways

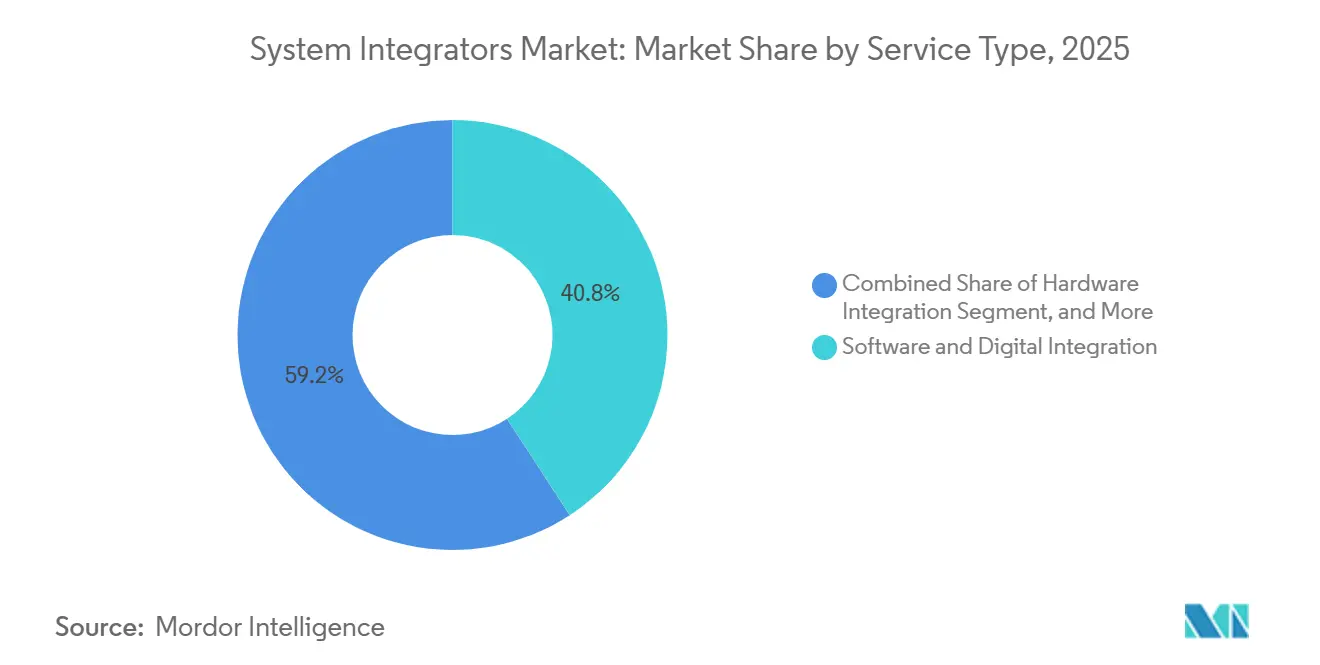

- By service type, Software and Digital Integration held 40.83% of the system integrators market share in 2025, while Hardware Integration is forecast to post a 5.27% CAGR through 2031.

- By technology, Integrated Process Control accounted for 36.71% of the system integrators market size in 2025; Industrial Internet of Things and Edge Platforms are projected to advance at a 5.31% CAGR over 2026-2031.

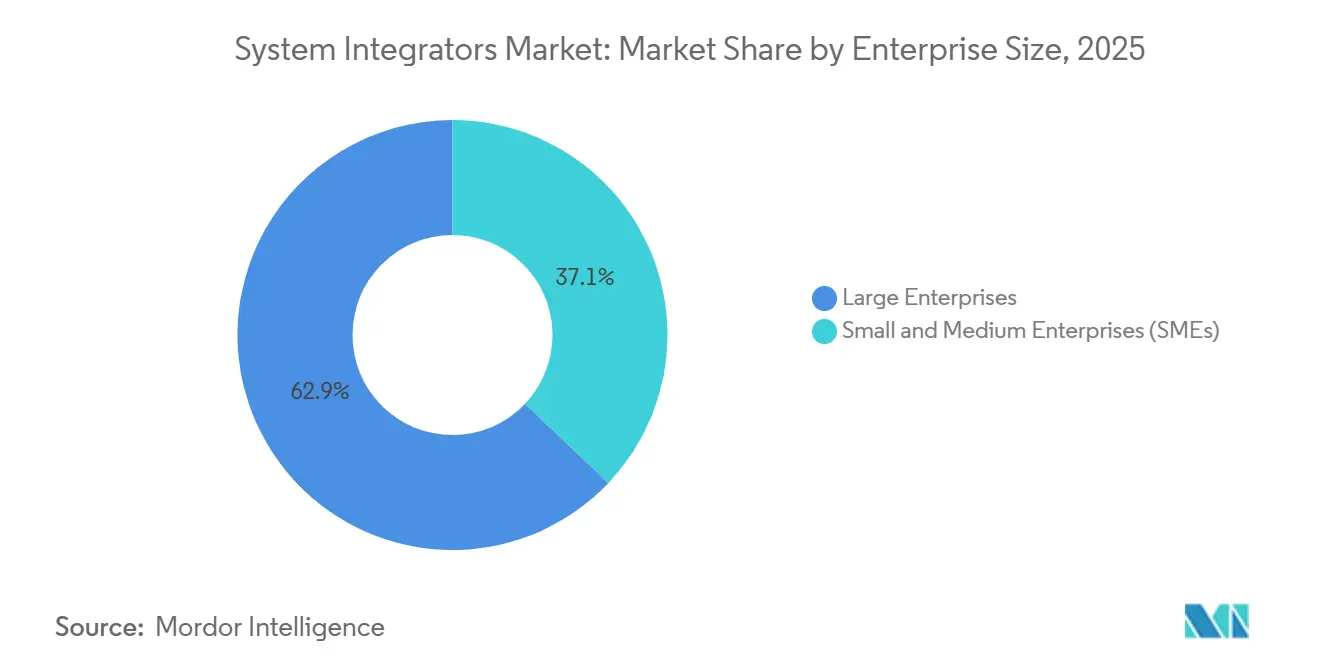

- By enterprise size, Large Enterprises captured 62.92% of spending in 2025, but Small and Medium Enterprises are anticipated to grow at a 5.34% CAGR as cloud-hosted supervisory control and data acquisition solutions lower entry barriers.

- By end-user industry, Oil and Gas represented 19.47% of demand in 2025, yet Healthcare and Life Sciences is expected to expand at a 5.39% CAGR because serialization and electronic batch-record mandates require validated integration.

- By geography, Asia-Pacific led with 33.53% of revenue in 2025, whereas the Middle East is projected to register a 5.24% CAGR through 2031 as sovereign investment funds bankroll smart-manufacturing projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global System Integrators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Turn-Key OT-IT Convergence Projects | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Acceleration of Renewable-Energy Asset Digitalization | +0.9% | Global, led by Europe, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| 5G-Enabled Edge Computing Use-Cases | +0.8% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Regulatory Push for Cyber-Secure SCADA Retrofits | +0.7% | North America and Europe, expanding to Middle East | Medium term (2-4 years) |

| Rising Adoption of Modular Automation | +0.6% | Global, with early traction in Asia-Pacific and North America | Medium term (2-4 years) |

| Shortage of Plant-Floor Automation Talent | +0.5% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Turn-Key OT-IT Convergence Projects

Enterprises want one accountable partner who can stitch programmable logic controllers, historians, manufacturing execution systems, and enterprise resource planning software into a unified architecture. In 2025, Siemens delivered more than 1,200 such projects, and 68% featured cloud-based digital twins that let operators simulate process changes before go-live.[1]Siemens AG, “Annual Report 2025,” siemens.com OMRON and Accenture formed a strategic alliance targeting USD 300 million in annual revenue by 2027, underscoring how hardware vendors are teaming up with IT integrators to pool expertise. Conformance with ISA-95 data models and IEC 62443 security controls is accelerating uptake because standardized interfaces reduce vendor lock-in. As the system integrators market evolves, turn-key scope is becoming the default contracting model, allowing asset owners to shift project-completion risk to specialists. Those integrators that master reference architectures and certification requirements gain pricing power and stickier multiyear relationships.

Acceleration of Renewable-Energy Asset Digitalization

Wind-turbine farms, solar parks, and battery-storage facilities are installing supervisory control and data acquisition and condition-monitoring layers to maximize energy yield and extend component life. Naturgy cut operations and maintenance costs by 18% after rolling out a unified supervisory control platform across its European renewable portfolio in 2025. The International Energy Agency expects annual global renewable-capacity additions to exceed 500 gigawatts through 2030, forcing integrators to harmonize data from turbines, inverters, and grid-balancing algorithms.[2]International Energy Agency, “Renewables 2025,” iea.org Edge gateways now host machine-learning models that autonomously curtail output during grid-congestion events, preserving revenue while stabilizing frequency. The opportunity for the system integrators market therefore hinges on offering cyber-secure, standards-based solutions that satisfy utilities, OEM warranties, and regulatory reporting. Regional policies that reward high availability and grid services participation further amplify project pipelines.

5G-Enabled Edge Computing Use-Cases

Private 5G networks deliver sub-10-millisecond latency, unlocking closed-loop quality control, autonomous mobile robots, and augmented-reality maintenance previously hamstrung by Wi-Fi jitter. Rockwell Automation’s 2025 launch of FactoryTalk Hub bundles 5G radios, edge analytics, and industrial-protocol translation in a single platform. Ericsson disclosed that 42% of its 2025 private-network deals landed in manufacturing and logistics, with system integrators acting as the primary channel for spectrum licensing, network design, and controller integration. Local processing slashes cloud-egress fees because time-series data are distilled on-site and only anomalies flow upstream, a cost win that resonates with finance chiefs. For the system integrators market, 5G competence is fast becoming a credential that differentiates bidders in high-speed discrete industries such as semiconductor packaging and consumer-goods bottling lines.

Regulatory Push for Cyber-Secure SCADA Retrofits

Critical-infrastructure regulators now mandate IEC 62443 zones, multifactor authentication, and real-time threat monitoring across legacy supervisory control networks. The U.S. Cybersecurity and Infrastructure Security Agency issued binding directives in 2025 requiring pipeline operators to complete retrofits by 2027. ABB’s USD 150 million acquisition of Messung Group in India targeted deeper cyber-secure integration capacity for power-generation clients facing similar mandates. Europe’s NIS2 directive compels incident reporting within 24 hours, spurring utilities to deploy security information and event-management platforms that ingest alerts from programmable logic controllers and safety systems. Integrators fluent in both functional safety and cybersecurity win preferential vendor status, allowing the system integrators market to capture premium pricing on brownfield hardening work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Project Scope-Creep Risk | −0.6% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Procurement Delays in Capital Goods | −0.5% | Global, extended lead times in Asia-Pacific supply chains | Medium term (2-4 years) |

| Fragmented Vendor Ecosystem | −0.4% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Critical Liability Exposure in Safety-Critical Plants | −0.3% | North America and Europe, stringent oversight | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Project Scope-Creep Risk

Undocumented legacy assets, late-stage cybersecurity demands, and evolving regulatory checklists frequently inflate integration scope. A 2025 McKinsey survey found 47% of automation projects blew budgets by more than 20% because of such creep. Overshoot hits profitability for integrators who operate on thin service margins and strains client trust when deadlines slip. To blunt the drag on the system integrators market, firms now run paid discovery phases that include laser scanning, network-topology mapping, and digital-twin validation to lock requirements before cost commitments. Fixed-price contracts with strict change-order governance are also commonplace, shifting some variance risk back to asset owners. While these measures temper financial volatility, they can prolong sales cycles as both sides negotiate granular responsibilities.

Procurement Delays in Capital Goods

Lead times for programmable logic controllers, variable-frequency drives, and industrial switches stretched to more than 40 weeks in 2025 amid semiconductor bottlenecks and geopolitical trade frictions. Schneider Electric noted that 23% of its integration projects slipped an average of 14 weeks due to component shortages.[3]Schneider Electric, “Annual Report 2025,” se.com Project holdups idle labor crews, extend working-capital locks, and compress integrator margins, thereby shaving momentum from the system integrators market. Countermeasures include pre-buying long-lead items, designing modular cabinets that can accept alternative vendor parts, and adopting software-defined control, where the logic runs on commercial-off-the-shelf computers. Although these tactics ease scheduling pressure, they increase inventory-holding costs and introduce new certification challenges for safety-integrity compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hardware Integration Gains as Greenfield Projects Accelerate

Hardware Integration is projected to post a 5.27% CAGR between 2026 and 2031, reversing the 2025 leadership of Software and Digital Integration that held a 40.83% revenue slice of the system integrators market. The swing reflects a surge of greenfield renewable-energy plants, petrochemical expansions in the Middle East, and battery-cell gigafactories, all of which demand physical control cabinets, field instrumentation, power-distribution boards, and hardened industrial-networking backbones before any software overlay can function. Integrators secure loyalty by shipping factory-acceptance-tested panels that arrive on-site pre-wired, cutting commissioning time and minimizing rework. Consulting and Training remains a steady earner because plant-floor talent is scarce; integrators therefore bundle skills-development modules and ongoing cybersecurity patching into managed-service contracts that guarantee uptime. After-Sales Support and Maintenance is margin rich because performance-based service-level agreements tie compensation to avoided downtime, creating alignment between integrator incentives and customer production goals.

A shift toward modular automation also shapes this segment. Emerson’s web-configurable skid systems, able to ship within 12 weeks, illustrate how standardization boosts velocity. Life-sciences clients value rapid changeovers for single-use bioreactors, while food-and-beverage firms appreciate scalable skids that can idle during off-seasons without stranding capital. As these patterns propagate, the system integrators market will see Hardware Integration teams collaborate more with software engineers to deliver converged packages, ensuring the linear workflow from physical installation to virtual commissioning collapses into a shorter critical path. Tools that auto-generate electrical schematics from process-and-instrumentation diagrams further compress engineering hours, freeing resources for higher-margin optimization services.

By Technology: IIoT and Edge Platforms Capture Predictive-Maintenance Budgets

Integrated Process Control-programmable logic controllers, distributed control systems, and supervisory control and data acquisition-accounted for 36.71% of the system integrators market share in 2025 but is approaching maturity as brownfield factories squeeze extra life from existing hardware. In contrast, Industrial Internet of Things and Edge Platforms will expand at a 5.31% CAGR through 2031, driven by stakeholders' demand for sub-second, real-time inference for anomaly detection and quality prediction. Edge nodes reduce latency, lower cloud egress costs, and address data-sovereignty rules that forbid sensitive telemetry from crossing borders. Manufacturing Execution Systems adoption is building momentum in discrete industries, especially automotive and aerospace, where serialized genealogy and compliance with ISO standards require granular orchestration of every work order. Robotics and Machine Vision integration is spilling out of automotive paint shops into ecommerce warehouses, where autonomous mobile robots and vision-guided picking systems drive 24/7 fulfillment.

Cyber-Security Solutions are now table stakes thanks to IEC 62443 mandates. Yokogawa revealed that 89% of its 2025 contracts bundled dedicated security assessments, up from 34% two years earlier, confirming that security is no longer an add-on but a default work-scope element. As technology breadth widens, the system integrators market needs multidisciplinary teams that understand real-time deterministic control, Kubernetes-based microservices, and zero-trust network architectures. Providers that create reference designs for sensor-to-cloud data paths, complete with pre-validated encryption and identity management, accelerate deployment and reduce certification friction, thereby snagging larger wallet share.

By Enterprise Size: SMEs Embrace Cloud-Hosted SCADA and Subscription Payment Models

Small and Medium Enterprises are forecast to register a 5.34% CAGR through 2031, outstripping Large Enterprises, which controlled 62.92% of 2025 spend but grow more modestly. The democratization of automation arises from cloud-native supervisory control and data acquisition platforms that convert hefty capital outlays into monthly operating charges. Subscription bundles include hardware, software, integration labor, and 24/7 help desk support, allowing SMEs to align automation expenses with production cadence. Integrators craft industry-specific templates- craft brewery batch recipes, cannabis cultivation track-and-trace, or refrigerated-storage energy dashboards-that slash engineering hours and speed go-live for firms without in-house specialists.

Large Enterprises still dominate absolute dollars because process-industry integrations, especially oil and gas or pharmaceuticals, demand multi-year programs, safety-integrity layers, and exhaustive factory-acceptance tests. Yet even these giants experiment with subscription models when piloting greenfield lines, enabling parallel evaluation of multiple technologies before standardizing across global footprints. Talent scarcity pressures both cohorts SMEs outsource entirely, while large firms retain a core team but rely on integrators for surge capacity and cybersecurity operations. For the system integrators market, tiered service catalogs that match SME affordability with enterprise rigor maximize addressable opportunity and create upgrade paths as client maturity rises.

By End-User Industry: Healthcare and Life Sciences Lead Growth Under Regulatory Intensity

Healthcare and Life Sciences will accelerate at a 5.39% CAGR to 2031, the fastest among verticals, because regulators demand electronic batch records, validated cleaning processes, and continuous-manufacturing lines that integrate real-time spectroscopy, environmental monitoring, and enterprise resource planning in a single provenance chain. Serialization mandates under the U.S. Drug Supply Chain Security Act and comparable European rules extend traceability down to the unit-dose level, compelling pharmaceutical plants to retrofit encoders, scanners, and data brokers that feed compliance dashboards. System integrators versed in Good Manufacturing Practice validation command premium fees because mistakes trigger costly regulatory delays.

Oil and Gas, with a 19.47% revenue share in 2025, continues to modernize legacy supervisory control assets but treads cautiously with greenfield commitments amid energy transition debates. Automotive producers are pivoting toward electric-vehicle platforms, prompting extensive robotics and battery-module assembly-line integration. Aerospace and Defense programs impose air-gapped networks, hardware encryption, and AS9100 quality audits, escalating integration complexity. Food and Beverage facilities use track-and-trace lines to comply with food-safety laws and enable rapid recall execution, while Chemicals and Petrochemicals require redundant safety-instrumented layers per IEC 61511 to avert runaway reactions. Because every vertical exhibits unique compliance and throughput pain points, specialization is emerging inside the system integrators market, with firms carving niches based on domain know-how, certified reference templates, and prequalified supply chains.

Geography Analysis

Asia-Pacific accounted for 33.53% of the system integrators market's revenue in 2025, reflecting China’s vast installed base, India’s production-linked incentive programs, and Southeast Asia’s role as a diversification hub for supply chains seeking resilience. Ongoing factory upgrades across electronics, pharmaceuticals, and automotive assembly lines continue to drive projects that blend hardware retrofits with edge analytics deployments, and national data-sovereignty rules create steady demand for in-country engineering resources. Integrators that cultivate local partnerships and Mandarin- or Hindi-speaking project managers consistently shorten commissioning cycles, building credibility with provincial regulators who require documented technology transfer. As 5G private-network rollouts accelerate in South Korea, Japan, and Singapore, demand for ultra-low-latency control loops is widening the addressable system integrators market across discrete manufacturing and logistics.

North America remains a heavyweight because reshoring initiatives are driving the construction of electric-vehicle battery gigafactories and semiconductor fabs that require end-to-end cybersecurity compliance under IEC 62443 and NIST frameworks. Brownfield modernizations in oil, gas, and chemicals add another tranche of work as aging control networks migrate toward software-defined architectures. Federal tax incentives that reward energy-efficient production have also unlocked funding for predictive-maintenance retrofits, prompting integrators to bundle edge gateways, historian upgrades, and digital twins in a single scope. Although capital budgets in 2026 stay cautious, multiyear master-service agreements give integrators revenue visibility, helping them keep specialized talent on the bench between megaproject releases. This dynamic underpins a stable outlook for the system integrators market even if commodity prices swing widely.

The Middle East is the fastest-growing region, with a projected 5.24% CAGR through 2031, fueled by Saudi Arabia’s Public Investment Fund allocations to NEOM’s smart-city infrastructure and the United Arab Emirates’ Operation 300bn manufacturing program. Sovereign mandates for local-content ratios oblige integrators to establish engineering centers in Riyadh, Abu Dhabi, and Muscat, often through joint ventures with national champions. Greenfield petrochemical complexes in Jubail and Ruwais, plus utility-scale solar and hydrogen plants, require integrated control rooms, safety-instrumented systems, and real-time asset-performance dashboards, expanding the system integrators market footprint across both process and power verticals. Europe shows steady but lower-trajectory growth as carbon-border adjustment rules push manufacturers to digitize for energy visibility, especially in Germany, France, and the Nordics. South America and Africa stay smaller but strategic, as Brazil, Nigeria, and South Africa channel mining and food-processing projects toward integrators who can offset infrastructure gaps with modular automation skids and remote-monitoring packages.

Competitive Landscape

The system integrators market is moderately fragmented, with the ten largest vendors accounting for a considerable share of global revenue, leaving a long tail of regional specialists to serve culturally nuanced or niche verticals. Automation-equipment majors such as ABB, Siemens, Rockwell Automation, Schneider Electric, Honeywell, Emerson, and Yokogawa continue to buy niche software firms and boutique engineering houses, creating one-stop shops that cover hardware, middleware, analytics, and managed services. Their scale secures favorable component pricing and enables them to guarantee performance-based outcomes, a capability that large energy and pharmaceutical clients prize when negotiating risk-sharing contracts. Consulting players-including Accenture and HCLTech-bring enterprise-architecture depth and global delivery centers, positioning themselves as prime contractors that orchestrate multivendor ecosystems while subcontracting plant-floor work to local engineering houses.

Warehouse-automation specialists are another competitive flank. Companies such as Swisslog, Bastian Solutions, and Hai Robotics deploy fleets of autonomous mobile robots, shuttle systems, and goods-to-person stations that integrate with programmable logic controllers and manufacturing execution systems, expanding the definition of integration beyond traditional process control. Their success in e-commerce fulfillment has sparked vertical specialization, prompting process-industry integrators to respond with pre-engineered skids for life-sciences cleanrooms and skid-mounted utilities. Intellectual-property moats are forming around digital-twin simulation, federated machine-learning algorithms for multisite optimization, and blockchain-based supply-chain traceability, as evidenced by the spike in 2025 patent filings at the U.S. Patent and Trademark Office. Providers that can prove measurable productivity or energy gains through advanced analytics win higher renew-and-extend rates on multiyear service contracts.

Cybersecurity credentials increasingly separate contenders from pretenders. IEC 62443 and ISO 27001 certifications are now threshold requirements for bidding on critical-infrastructure work, and smaller regional integrators that lack the resources to undergo third-party audits find themselves relegated to subcontract status. Strategic moves in 2025-2026-Siemens spinning off Innomotics to sharpen focus on digital-industries services, ABB acquiring Messung Group in India, Rockwell Automation purchasing Clearpath Robotics-signal an arms race for domain expertise, regional reach, and edge-analytics portfolios. As vendors jostle for end-to-end accountability, cross-industry alliances emerge, typified by the OMRON-Accenture partnership that targets USD 300 million in revenue by 2027. Overall, buyers benefit from a wide supplier slate but face diligence burdens to compare capability breadth, reference-site performance, and long-term financial stability.

System Integrators Industry Leaders

Siemens AG

ABB Ltd.

Rockwell Automation Inc.

Schneider Electric SE

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens AG completed the spin-off of Innomotics, its large-motors and drives business, valuing the new entity at EUR 3.5 billion (USD 3.9 billion), and will redirect capital toward industrial-edge platforms.

- December 2025: ABB Ltd finalized the USD 150 million acquisition of Messung Group to deepen cyber-secure integration capacity across South Asia’s power and renewables sectors.

- November 2025: Rockwell Automation bought Clearpath Robotics for USD 290 million, integrating fleet-management software with FactoryTalk Hub for unified robot and controller orchestration.

- October 2025: Schneider Electric announced a USD 200 million expansion of its Bangalore digital-services delivery center, aiming to add 2,000 engineering and data-science roles by 2027.

Global System Integrators Market Report Scope

System Integrators are the companies or individuals that implement, plan, coordinate, schedule, test, improve, and maintain a computing operation. System Integrators (SIs) include companies that integrate systems such as Supervisory Control and Data Acquisition (SCADA), Manufacturing Execution Systems (MES), and Human-Machine Interfaces (HMIs), among others.

The System Integrators Market Report is Segmented by Service Type (Hardware Integration, Software and Digital Integration, Consulting and Training, and After-Sales Support and Maintenance), Technology (Integrated Process Control, Manufacturing Execution Systems, Robotics and Machine Vision, IIoT and Edge Platforms, and Cyber-Security Solutions), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Oil and Gas, Automotive and EV Manufacturing, Aerospace and Defense, Healthcare and Life Sciences, Energy and Power, Chemicals and Petrochemicals, Food and Beverage, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware Integration |

| Software and Digital Integration |

| Consulting and Training |

| After-Sales Support and Maintenance |

| Integrated Process Control (PLC, DCS, SCADA) |

| Manufacturing Execution Systems (MES) |

| Robotics and Machine Vision |

| IIoT and Edge Platforms |

| Cyber-Security Solutions |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Oil and Gas |

| Automotive and EV Manufacturing |

| Aerospace and Defense |

| Healthcare and Life Sciences |

| Energy and Power |

| Chemicals and Petrochemicals |

| Food and Beverage |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Service Type | Hardware Integration | |

| Software and Digital Integration | ||

| Consulting and Training | ||

| After-Sales Support and Maintenance | ||

| By Technology | Integrated Process Control (PLC, DCS, SCADA) | |

| Manufacturing Execution Systems (MES) | ||

| Robotics and Machine Vision | ||

| IIoT and Edge Platforms | ||

| Cyber-Security Solutions | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-User Industry | Oil and Gas | |

| Automotive and EV Manufacturing | ||

| Aerospace and Defense | ||

| Healthcare and Life Sciences | ||

| Energy and Power | ||

| Chemicals and Petrochemicals | ||

| Food and Beverage | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving new project demand in the system integrators market after 2026?

Turn-key OT-IT convergence projects, renewable-energy digitalization, and private 5G edge deployments are the principal growth engines highlighted across recent contract awards.

Which region is expected to grow fastest for system integration work?

The Middle East leads with a projected 5.24% CAGR to 2031, propelled by Saudi and UAE industrial diversification programs.

Why are Small and Medium Enterprises adopting integration services more quickly than before?

Cloud-hosted SCADA, subscription payment models, and industry-specific templates have slashed upfront capital requirements and reduced reliance on scarce in-house automation talent.

How are vendors differentiating in an increasingly crowded competitive field?

Leaders bundle certified cybersecurity, digital-twin simulation, and managed services while pursuing domain-specific templates and regional engineering hubs.

What is the main supply-chain challenge facing integration projects?

Extended lead times for programmable logic controllers and variable-frequency drives continue to delay hardware deliveries, forcing integrators to pre-buy components or redesign with substitute parts.

Page last updated on: