Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

Temperature Controller System Market is Segmented by Product Type (On/Off Controllers, Proportional Controllers, and More), Control Method (Single-Loop, Multi-Loop, and More), Mounting Type (DIN-Rail, Panel-Mount, and More), End-User Industry (Industrial Manufacturing, and More), Application (Process Temperature Control, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

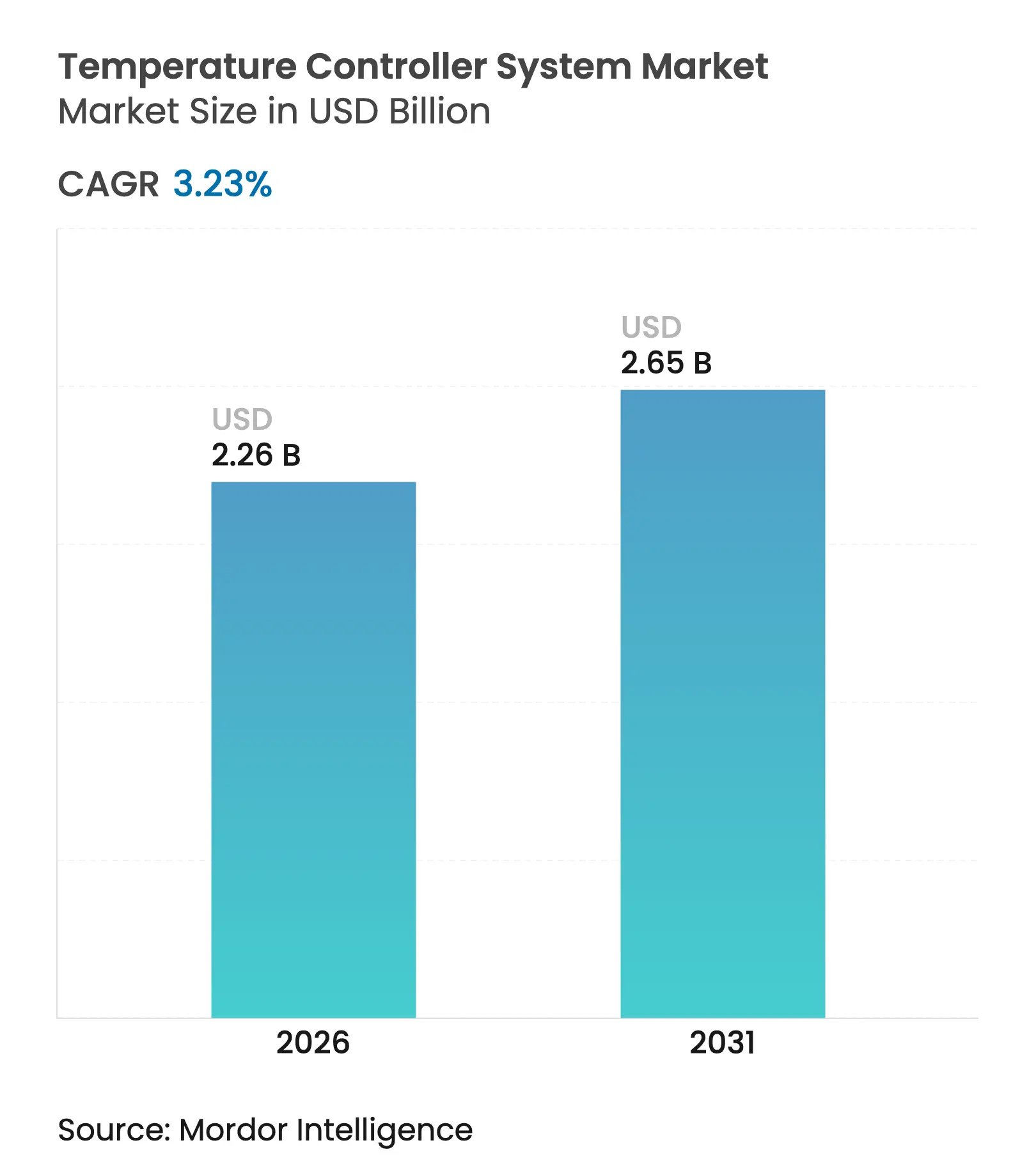

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 3.23 % CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The temperature controller system market size was valued at USD 2.19 billion in 2025 and estimated to grow from USD 2.26 billion in 2026 to reach USD 2.65 billion by 2031, at a CAGR of 3.23% during the forecast period (2026-2031). Steady expansion has been sustained by rising industrial automation, stringent efficiency mandates, and a widening set of high-precision applications that depend on stable thermal conditions. Semiconductor fab investments exceeding USD 540 billion announced by United States producers alone highlighted the centrality of temperature control to yield optimisation.[1]Semiconductor Industry Association, “SIA Comments on Section 232 Investigation,” semiconductors.org Consolidation among automation majors intensified, with acquisitions concentrating on edge computing, AI capability, and platform interoperability. Regionally, Asia-Pacific retained the lead through 2024, yet South America is accelerating as renewable-energy and modern farming projects demand dynamic thermal management.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid industrial automation boom

Rapid industrial automation boom

| +1.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, with APAC leading adoption

|

Impact Timeline

:

Medium term (2-4 years)

|

HVAC retrofits for energy-efficiency mandates

HVAC retrofits for energy-efficiency mandates

| +0.8% | North America and the EU primarily | Short term (≤ 2 years) | |||

Cold-chain expansion in pharma and F&B

Cold-chain expansion in pharma and F&B

| +0.6% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Digitization of factory floors (Industry 4.0)

Digitization of factory floors (Industry 4.0)

| +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) | |||

DRL-tuned PID for greenhouse HVAC

DRL-tuned PID for greenhouse HVAC

| +0.4% | South America, North America agricultural regions | Long term (≥ 4 years) | |||

Self-healing FDD algorithms in smart buildings

Self-healing FDD algorithms in smart buildings

| +0.3% | Urban centers globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid industrial automation boom

Global factories continued shifting toward autonomous lines that require adaptive controls capable of predicting load-induced heat swings and self-correcting in milliseconds. Honeywell’s AI-ready handhelds showcased this real-time optimisation approach, while edge processors kept latency below cloud-dependent thresholds. Mounting demand for such responsiveness explains high controller upgrade activity in semiconductor, specialty chemical, and battery cell plants.

HVAC retrofits for energy-efficiency mandates

North American and European building codes tightened after 2024, prompting owners to install smart HVAC logic that delivers verifiable consumption cuts. F.E. Moran projects demonstrated 10-40% energy savings once intelligent controllers automated demand response and fault-detection analytics. Embedded communication modules inside new chillers and rooftop units removed the need for separate control panels, accelerating swap-out cycles in office towers and data centres.

Cold-chain expansion in pharma and Food and Beverage

Pharmaceutical distributors intensified their focus on sub-degree stability after global logistics failures had cost the sector USD 35 billion annually. CDC guidance requiring buffered, certificate-calibrated data loggers lifted specification baselines for controllers across vaccine depots and bioprocessing suites. Parallel growth in ready-to-eat produce drove similar needs for thermal continuity, pressing vendors to supply lab-grade accuracy at warehouse scale.

Digitization of factory floors (Industry 4.0)

Machine-learning models trained on production schedules and ambient data cut heating energy up to 20% in IoT-enabled lines, according to peer-reviewed studies. Siemens’ Digital Industries unit pivoted to SaaS-driven optimisation services, illustrating how value is migrating toward continuous performance analytics rather than one-time hardware supply.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High lifecycle and calibration costs

High lifecycle and calibration costs

| -0.7% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Global, particularly affecting SMEs

|

Impact Timeline

:

Short term (≤ 2 years)

|

Legacy system integration complexity

Legacy system integration complexity

| -0.5% | North America and the EU industrial bases | Medium term (2-4 years) | |||

Rising cybersecurity compliance burden

Rising cybersecurity compliance burden

| -0.3% | Global, concentrated in critical infrastructure | Long term (≥ 4 years) | |||

Electronics tariff volatility on sensor ICs

Electronics tariff volatility on sensor ICs

| -0.4% | Global supply chains, US-China trade routes | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High lifecycle and calibration costs

Precision certificates and frequent multi-point calibration lifted the total cost of ownership, discouraging smaller operators from upgrading despite well-known efficiency gains. Smart Farm Innovations indicated that full-feature greenhouse controllers ranged from USD 1,000 to USD 10,000, with payback periods stretching in low-margin operations.

Legacy system integration complexity

Plants running mixed-generation PLCs and Supervisory Control and Data Acquisition software faced extensive engineering rework when grafting modern controllers onto dated buses. Honeywell’s migration toolkit employing digital twins cuts risk but remains expensive for mid-sized factories.[2]Pramesh Maheshwari, “Honeywell Innovations Target Entire Automation Lifecycle,” Control Global, controlglobal.com As a result, many facilities deferred full conversions and accepted sub-optimal thermal performance.

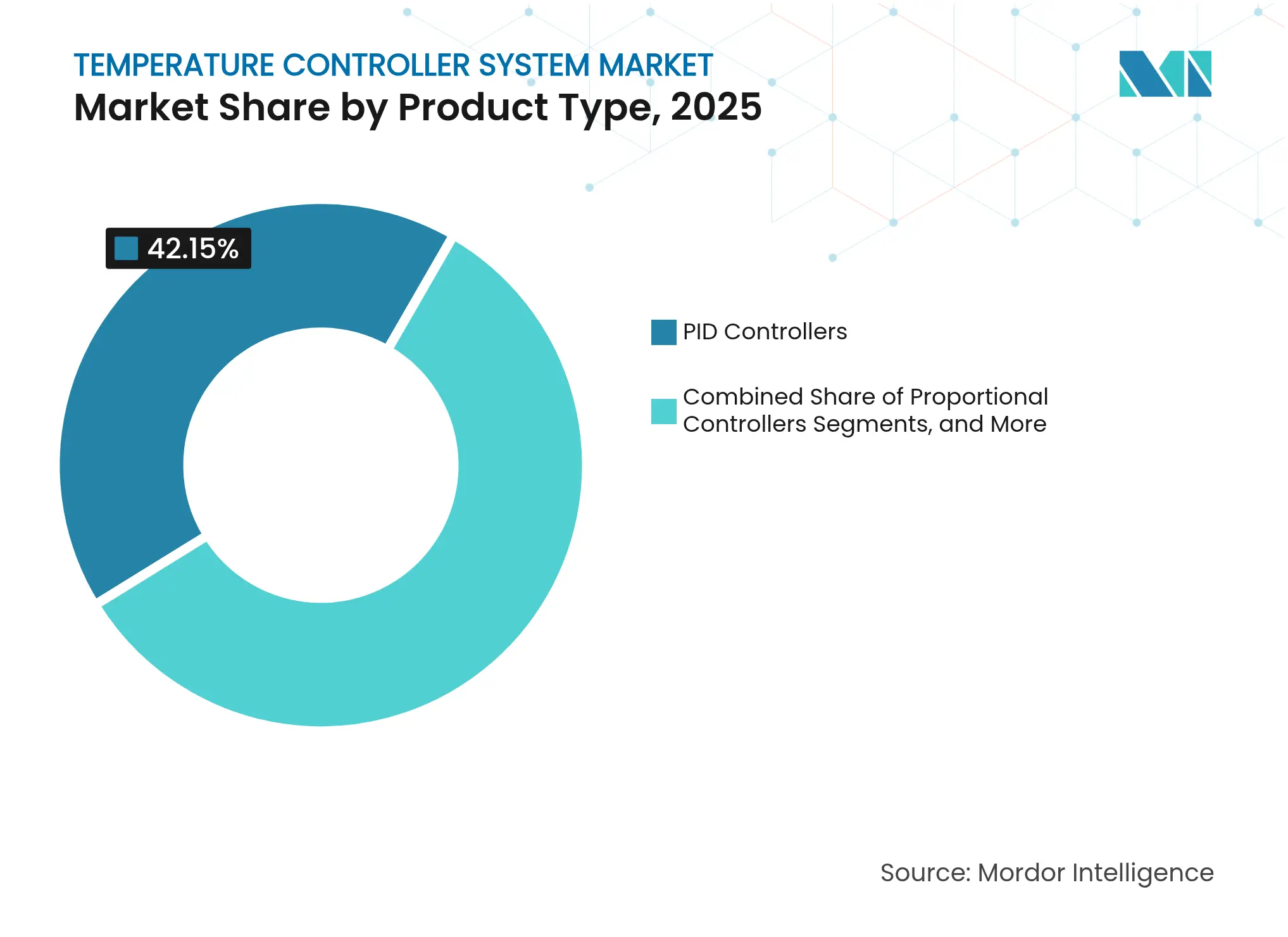

By Product Type: PID Resilience Amid AI Growth

PID controllers accounted for 42.15% of 2025 revenue, underlining their entrenched acceptance for rigorous industrial duty within the temperature controller system market share. Demand persisted because maintenance teams trust proven loop stability and prefer minimal retraining. Autotune and adaptive PID solutions, however, led growth at an 8.05% CAGR as manufacturers shifted toward self-optimising loops that slash commissioning hours. Omron’s NX-TC launch illustrated the merger of AI functions onto PID hardware, enabling automatic gain tuning without manual touch-ups.

Emerging machine-learning layers altered the product roadmap from fixed-parameter accuracy tables to dynamic improvement curves. Proportional-only units retained a niche in cost-sensitive heating lines, while high-precision controllers maintained a foothold in semiconductor lithography and aseptic filling, where a ±0.1 °C drift can translate to yield losses. The overall temperature controller system market continued rewarding suppliers that combine backward-compatible form factors with firmware capable of cloud or edge-sourced analytics updates.

Note: Segment shares of all individual segments available upon report purchase

By Control Method: Single-Loop Steadiness Versus Predictive Multivariable Control

Single-loop architectures held a 48.30% share in 2025, prized for easy maintenance and transparent tuning. Yet AI-assisted model predictive control (MPC) platforms achieved an 10.85% CAGR on the promise of multivariable optimisation for batch reactors, tunnel ovens, and large cleanroom HVAC arrays. A university study reported 15-20% energy gains when MPC replaced thermostatic logic in a pilot building system.

Edge devices now embed MPC algorithms locally, trimming latency and cyber-exposure while preserving cloud connectivity for fleet analytics. Advanced suppliers marketed subscription-based performance upgrades, turning the temperature controller system market into a recurring-revenue environment. This evolution repositioned the temperature controller system industry as a software-first arena where historical loop tuning knowledge is augmented by automated pattern discovery.

By Mounting Type: DIN-Rail Prevalence Meets Wireless Field Adoption

DIN-rail variants delivered 46.25% of 2025 shipments due to long-standing panel standards in process plants and OEM cabinets. Field-mount units, however, are the fastest risers at 7.62% CAGR, propelled by IoT rollouts that place intelligence close to the asset. Wireless designs cut conduit costs and reach previously inaccessible machinery, aligning with the distributed sensor ethos of Industry 4.0. Nordic Semiconductor’s nRF54L series gave integrators low-power Bluetooth LE options tailored to temperature loops.

Panel-mount models continue to satisfy operators who require on-site visual feedback or physical setpoint dials. Meanwhile, the temperature controller system market size for field-mount solutions is projected to expand as greenfield renewables and remote agricultural facilities prefer battery-powered nodes.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

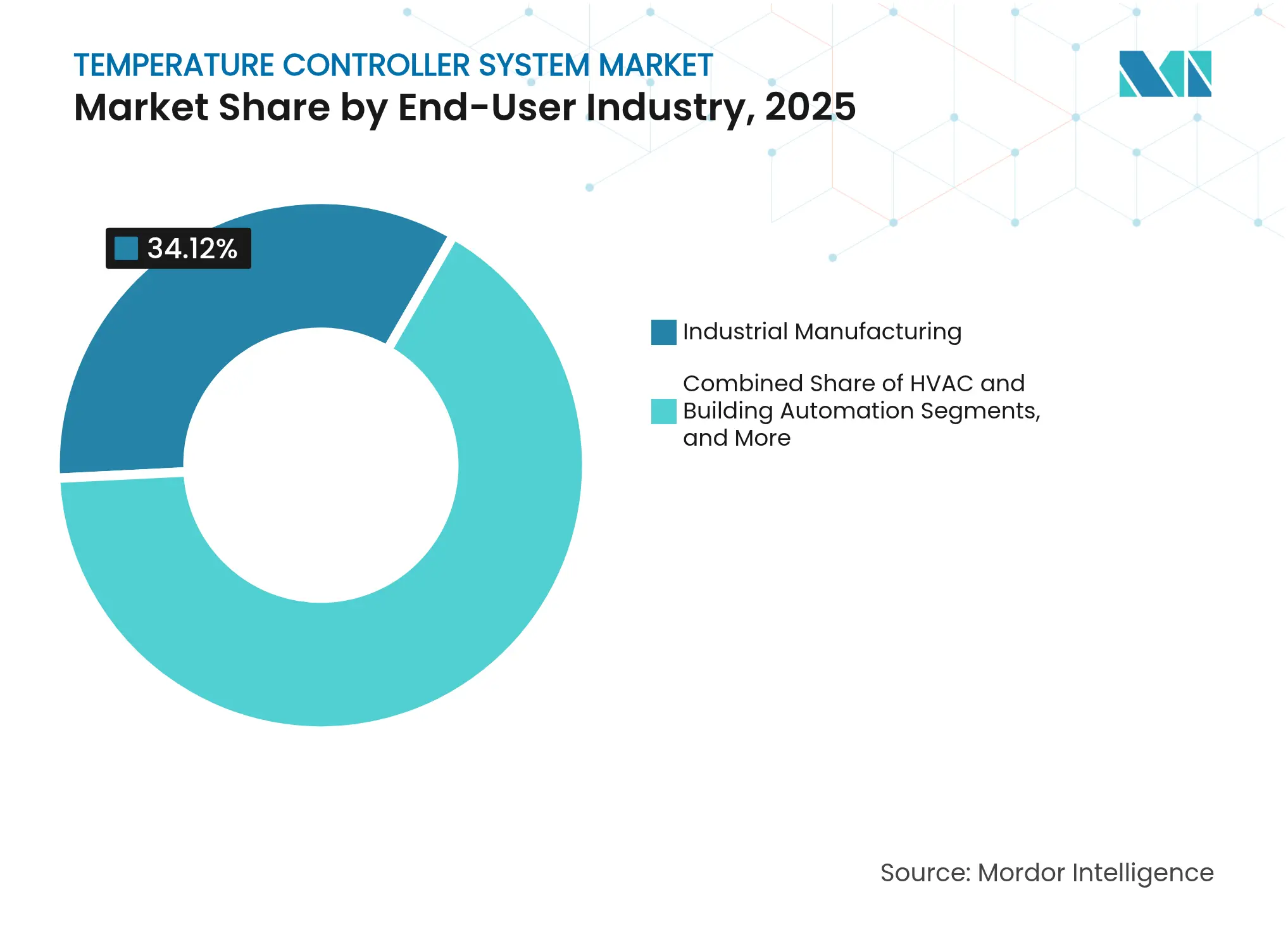

By End-User Industry: Manufacturing Core, Building Services Momentum

Industrial manufacturing retained 34.12% revenue share in 2025, reflecting its dependence on precise thermal control across semiconductor, chemical, and life-science lines. Yet HVAC and building automation posted the strongest 10.12% CAGR through 2031, spurred by carbon-reduction policies and real-estate economics that reward operational cost cuts. Schneider Electric’s USD 700 million United States expansion underscored supplier emphasis on data-centre and micro-grid climate control.

Energy utilities adopted AI-directed temperature control to protect battery farms and inverter stations from heat degradation. The temperature controller system market outlook thus tilts toward sectors where energy consumption visibility, autonomous maintenance, and ESG reporting converge.

Note: Segment shares of all individual segments available upon report purchase

By Application: Process Control Bedrock, Agri-Climate Upsurge

Process temperature control formed the cornerstone with a 28.05% share in 2025, anchoring the temperature controller system market in traditional continuous and batch processes. Precision agri-climate solutions logged a 11.65% CAGR as controlled-environment farming demanded granular control of heat, humidity, and CO₂. LoRaWAN-enabled sensor gateways now feed reinforcement-learning algorithms that balance crop growth against power use, illustrating the field’s shift from mechanism to data-driven agronomy.

Environmental chambers kept traction in product validation labs, and cold-chain logistics became a high-specification niche after vaccine spoilage incidents prompted regulators to push for real-time excursion alerts. Additive manufacturing lines also leaned on fine thermal profiling to retain metallurgical integrity, further diversifying downstream pull on the temperature controller system market.

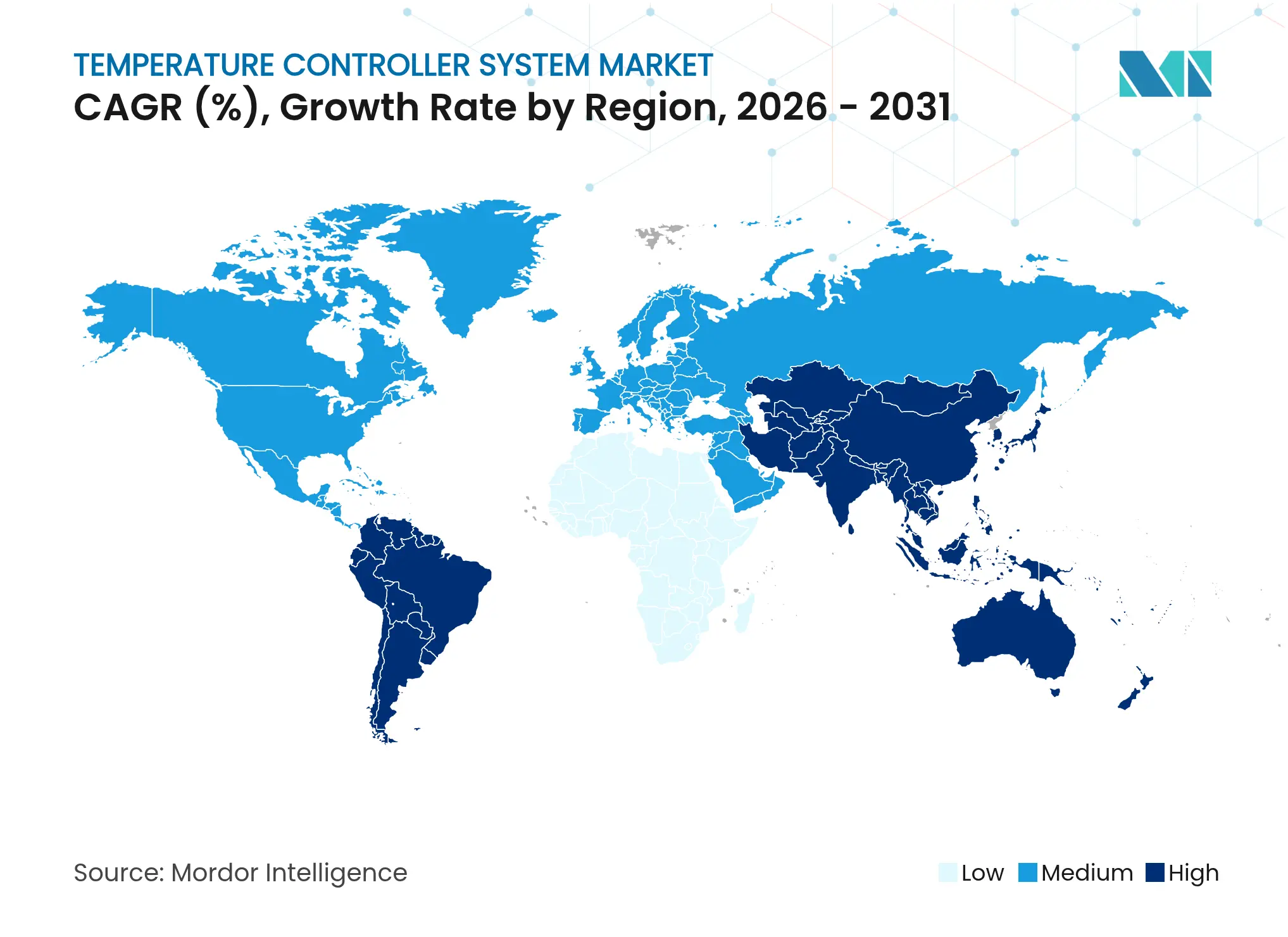

Asia-Pacific led with 39.20% of 2025 revenue, anchored by China’s electronics complex and India’s accelerating automation, which is forecast at 14.3% CAGR in machine uptake. The temperature controller system market size in fab cleanrooms benefited from multi-billion-dollar local wafer initiatives that required sub-degree repeatability in deposition stages. Japan and South Korea contributed high-reliability control modules for automotive and display glass furnaces, reinforcing a dense regional supply web.

South America, though smaller, posted the quickest anticipated 7.35% CAGR. The government's drive to install 319 GW of renewable capacity by 2030 demanded flexible thermal regulation for wind-turbine converters and lithium battery farms. Brazil’s USDA-valued USD 36.2 billion manufacturing base added automation lines in automotive and agribusiness, while Chile and Colombia sought greenhouse expansion to bolster export crops. This momentum repositioned the temperature controller system market as a strategic enabler of decarbonisation objectives in the region.

North America and Europe remained important through retrofit cycles that pivoted from analog thermostats toward cloud-linked predictive systems. Data-centre operators prioritised high-density rack cooling accuracy, driving adoption of AI-enabled PID arrays. The Middle East and Africa displayed emerging prospects, especially in LNG and petrochemical upgrading, where precise thermal ramps govern catalytic yields. Overall, geographic expansion illustrated the global migration of temperature controller know-how from discrete assembly lines to energy transition assets.

Market Concentration

The market is moderately consolidated, with platform plays replacing single-device competition. ABB, Siemens, Schneider Electric, and Honeywell deepened vertical portfolios via software acquisitions and sensor ecosystems. Honeywell partnered with Danfoss to create interoperable automation stacks targeting battery cell and specialty chemical plants.[4]Honeywell, “Honeywell and Danfoss Partner to Develop Innovative Automation Solutions,” automation.honeywell.com Trane Technologies’ 2025 purchase of Brainbox AI extended autonomous HVAC optimisation into small commercial buildings.

Niche entrants exploited gaps in the ultra-cold chain and wireless field deployments. Monnit introduced Wi-Fi sensors rated 200 °C to 125 °C aimed at biologics shippers. Edge algorithm suppliers marketed drop-in firmware that converts legacy PID blocks into self-learning devices. The battleground shifted toward lifespan services—cyber-secure firmware updates, calibration analytics, and emissions dashboards—more so than core accuracy specs, reshaping buyer criteria throughout the temperature controller system industry.

Investment bankers recorded rising deal volumes in sensors-plus-software targets as strategics paid premiums for cloud talent. Component shortages and tariff swings, meanwhile, nudged manufacturers to consider dual-sourcing fabs, highlighting supply risk as a determinant of future competitive positioning within the temperature controller system market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

According to Mordor Intelligence, the temperature controller system market covers revenues generated from dedicated electronic units that compare a sensor signal with a set-point and then switch, modulate, or proportionally adjust heating or cooling equipment in industrial, HVAC, laboratory, and process environments. Embedded logic blocks integrated in PLCs or variable-speed drives are excluded, as are purely software-only supervisory algorithms.

Scope exclusion: software-only virtual controllers and generic building BMS platforms without discrete control hardware are not part of this study.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

We interviewed control-system integrators, HVAC contractors, and factory maintenance engineers across North America, Europe, and Asia Pacific. Discussions clarified typical hardware replacement cycles, emerging AI-assisted PID adoption, and country-level pricing spreads, which strengthened assumption choices and closed data gaps found in desk research.

Desk Research

Our analysts gathered foundational data from publicly accessible tier-1 sources such as UN Comtrade shipment codes for industrial controllers, U.S. Census M334B production surveys, Eurostat PRODCOM files, and trade association bulletins from ISA and ASHRAE. Company 10-K filings, investor decks, and global customs records were mined to benchmark average selling prices and regional mix, while paid assets like D&B Hoovers and Dow Jones Factiva helped verify manufacturer revenues. These references illustrate the broader evidence base; many additional sources informed data reconciliation and narrative building.

Market-Sizing & Forecasting

A top-down construct begins with global production and trade data for discrete temperature controllers, which are then aligned to end-use demand pools through penetration ratios for key sectors such as industrial manufacturing, HVAC retrofit stock, pharmaceuticals, and food processing. Select bottom-up rollups of major supplier revenues and sampled ASP × volume checks validate direction and calibrate regional splits. Core variables include industrial automation CAPEX, installed HVAC floor space, average controller life, retrofit incidence, regulation-driven efficiency upgrades, and controller ASP degradation. Multivariate regression paired with ARIMA smoothing projects each driver, and scenario analysis reviewed with primary experts tests sensitivity around energy-efficiency mandates and semiconductor supply shifts. Gap pockets in bottom-up inputs are bridged by controlled interpolation using nearest neighbor markets.

Data Validation & Update Cycle

Before sign-off, Mordor analysts cross-check model outputs against external shipment tallies and manufacturer disclosures. Variances beyond three percentage points trigger re-contact of industry sources, after which a senior reviewer audits formulas. The report is refreshed yearly, with interim updates issued when policy or supply-chain events materially alter demand.

Why Our Temperature Controller System Baseline Holds Firm

Benchmark comparison

Published estimates often diverge because firms define hardware boundaries differently, apply assorted ASP curves, or refresh data on separate cadences.

Key gap drivers include exclusion of AI-assisted multi-loop units by some studies, differing treatment of controller cards embedded in drives, and exchange-rate translation methods that inflate or depress dollar totals relative to Mordor's constant-currency base.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.19 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.25 B (2025) | Global Consultancy A | Narrow scope omits DIN-rail industrial units and AI-assisted PID variants | ||

USD 1.30 B (2024) | Industry Association B | Uses list pricing and excludes retrofit demand, leading to lower value |

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.