Motion Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.08 Billion |

| Market Size (2031) | USD 24.23 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

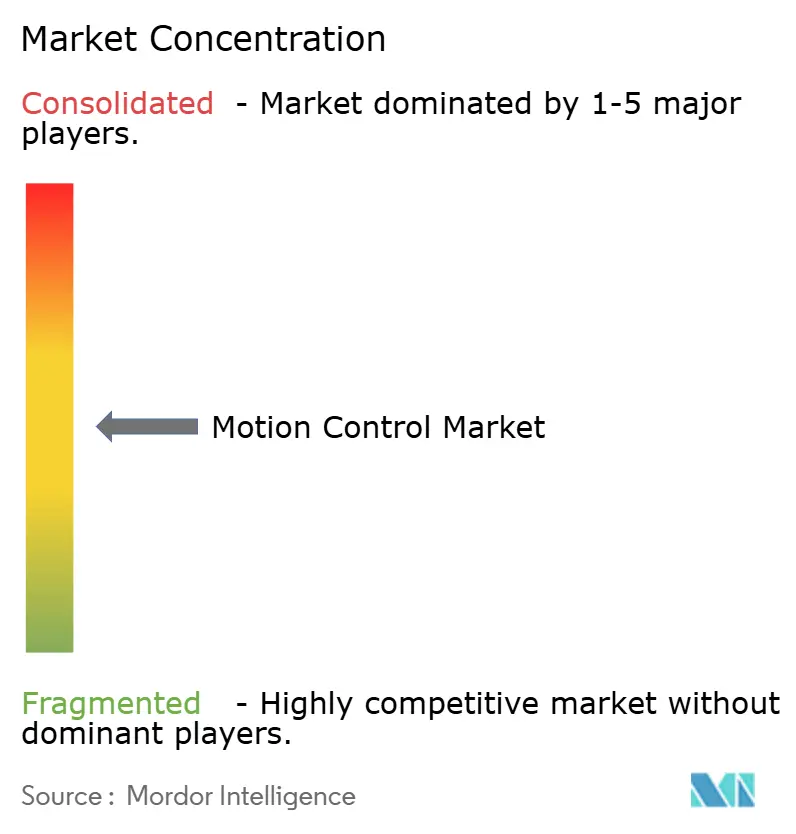

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Motion Control Market Analysis by Mordor Intelligence

The Motion Control Market size is expected to increase from USD 18.19 billion in 2025 to USD 19.08 billion in 2026 and reach USD 24.23 billion by 2031, growing at a CAGR of 4.90% over 2026-2031.

The expansion is fueled by manufacturers migrating from hydraulic and pneumatic actuation toward electrified solutions that allow precise positioning, high-speed synchronization, and real-time data capture. Artificial intelligence, embedded at the drive and controller level, is enabling autonomous mobile robots, self-optimizing servo loops, and predictive maintenance functions that cut unplanned downtime. Accelerated semiconductor investments in South Korea and India, combined with automotive electrification programs, are lifting demand for high-precision drives. Despite headwinds from rare-earth magnet price spikes and component shortages, suppliers are mitigating risk with decentralized architectures and closed-loop feedback that reduce cabling, improve energy efficiency, and simplify commissioning. [1]Rockwell Automation, “5 Key Trends Redefining Smart Manufacturing in 2025,” rockwellautomation.com

Key Report Takeaways

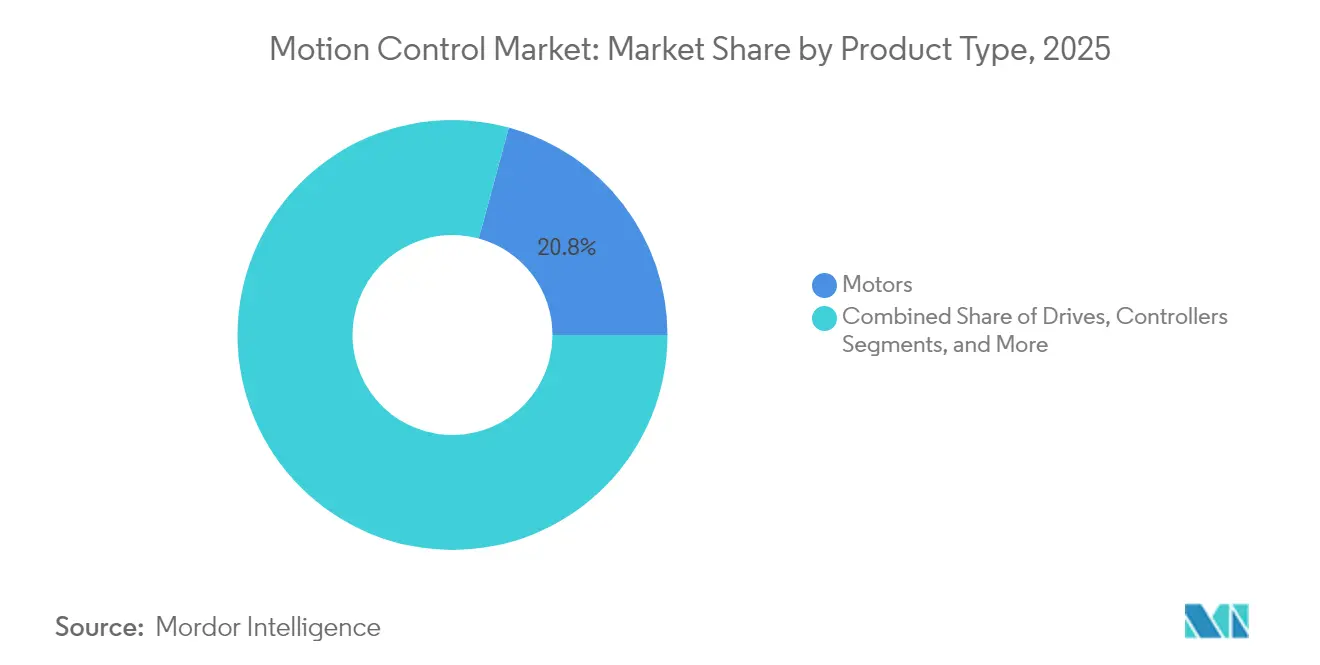

- By product type, motors led the motion control market with a 20.78% revenue share in 2025, while drives are projected to expand at a 6.65% CAGR through 2031.

- By technology, electromechanical solutions held a 60.55% share of the motion control market in 2025; pneumatic technology is forecast to grow at a 6.85% CAGR to 2031.

- By system type, closed-loop architectures accounted for 51.62% of the motion control market share in 2025 and are advancing at a 6.05% CAGR through 2031.

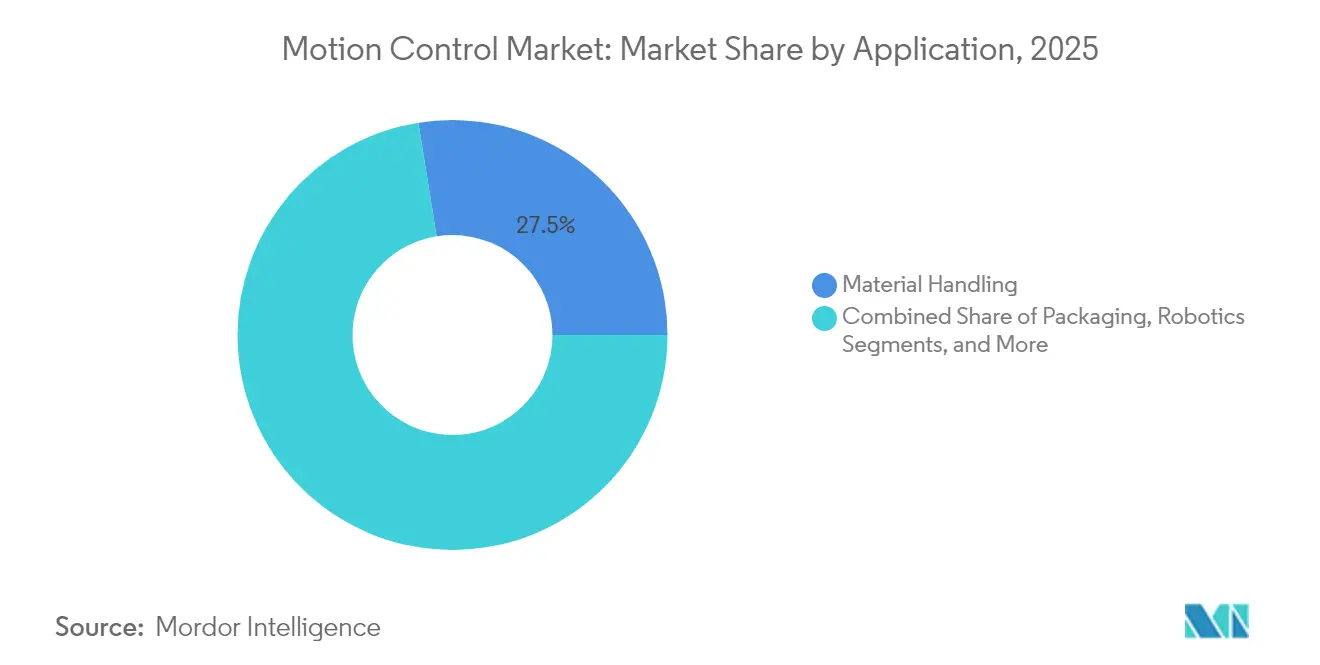

- By application, material handling held 27.54% of the motion control market size in 2025, whereas mobile robotics is set to expand at a 7.35% CAGR between 2026-2031.

- By end-user industry, automotive commanded a 23.48% share of the motion control market in 2025; pharmaceutical and life sciences is expected to record the fastest 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Motion Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for smart conveyance and machine-integrated robotics | +1.20% | Global, led by Asia Pacific and North America | Medium term (2-4 years) |

| Rapid transition to decentralised servo drives | +0.80% | Europe and North America, Asia Pacific following | Short term (≤ 2 years) |

| Semiconductor fab expansions in South Korea and Taiwan | +0.70% | Asia Pacific core, global spill-over | Long term (≥ 4 years) |

| Electrification of mobile hydraulics upgrading motion controllers | +0.60% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Post-FDA Annex 1 modernisation of pharma fill-finish lines | +0.40% | North America and Europe, expanding Asia Pacific | Short term (≤ 2 years) |

| India’s PLI-backed electronics clusters accelerating servo demand | +0.50% | Asia Pacific—India focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Smart Conveyance and Machine-Integrated Robotics

Manufacturers are deploying autonomous mobile robots and AI-driven conveyors to raise throughput and offset labor shortages. Global robotics spending is projected to climb from USD 71.78 billion in 2025 to USD 150.84 billion by 2030, intensifying the need for controllers that manage multi-axis path planning and collision avoidance. With 83% of producers planning to embed generative AI on the plant floor, motion-control firmware now incorporates predictive algorithms that schedule maintenance, balance loads, and self-tune servo gains. [2]Automation.com, “Siemens' Cooperation with Robot Vendors Targets Integrated Robot Control,” automation.com These capabilities position smart robotics as a primary catalyst for the motion control market.

Rapid Transition to Decentralised Servo Drives

Moving intelligence from the cabinet to the motor slashes cabling by up to 86% and improves electromagnetic compatibility in the motion control market. Advanced drives now integrate safety PLC, data logging, and edge computing, cutting panel space and boosting line flexibility. SEW-EURODRIVE’s MOVIMOT range, rated 0.37-7.5 kW, illustrates this shift with digital motor interfaces and built-in safe torque off functions.

Semiconductor Fab Expansions in South Korea and Taiwan

South Korea’s USD 471 billion megacluster aims for 7.7 million wafers each month by 2030, demanding ultra-precision linear motors and vibration-free stages. SK Hynix alone is channeling USD 75 billion toward HB-memory lines, reinforcing the region’s appetite for nanometer-level positioning systems. SEMI projects global fab capacity to rise 6% in 2024 and 7% in 2025, keeping pressure on suppliers of high-accuracy servo platforms. [3]SEMI, “Global Semiconductor Fab Capacity Projected to Expand 6% in 2024 and 7% in 2025,” semi.org

Electrification of Mobile Hydraulics Upgrading Motion Controllers

Electro-hydraulic conversions cut excavator fuel use by up to 30% while retaining force density, accelerating innovation in the motion control market. Direct-drive hydraulic pumps eliminate large oil reservoirs, using electric motors and feedback sensors to achieve precise speed control. With 93% of plant managers citing hydraulics as essential, controller vendors are embedding CAN-open and Ethernet interfaces to blend hydraulic power with digital motion profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price spikes from rare-earth magnet supply volatility | -0.9% | Global, with particular impact on Asia Pacific manufacturing | Short term (≤ 2 years) |

| OT-network cyber-security certification delays in Europe | -0.6% | Europe primary, with regulatory spillover to global markets | Medium term (2-4 years) |

| IGBT and MCU shortages constraining drive shipments | -0.7% | Global, with acute impact on automotive and industrial sectors | Short term (≤ 2 years) |

| Lack of unified programming standards in South America | -0.4% | South America primary, limiting automation adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Spikes from Rare-Earth Magnet Supply Volatility

Neodymium and dysprosium price swings have inflated servo motor costs by up to 25%, squeezing margins for high-torque motion platforms. Supplier diversification programs and ferrite-based motor R&D are under way, but commercial roll-out will trail the forecast window.

OT-Network Cyber-Security Certification Delays in Europe

Europe’s NIS2 directive adds rigorous encryption, segmentation, and patch-management rules for drives and controllers. Certification queues are lengthening, extending project lead times and raising compliance budgets, particularly for large automation rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motors Anchor Demand

Motors held 20.78% of the motion control market in 2025, underscoring their status as universal actuators. Growth stems from compact servomotors for robotics, large torque motors for semiconductor steppers, and frameless motors for medical devices. Drives, the intelligence layer between power and position, are the fastest risers at 6.65% CAGR, evolving into edge computers that analyze vibration, temperature, and load in real time. This hardware-software fusion enlarges service revenues as vendors sell predictive algorithms on subscription.

Miniaturization is critical in medical robots that navigate inside MRI bores, while high-power modules like Mitsubishi Electric’s 1,500 A HVIGBT raise inverter efficiency for steel mills and wind turbines. Controllers and mechanical systems enjoy steady demand as OEMs retrofit legacy lines to accommodate higher servo bandwidths and safety-rated drives.

By Technology: Electromechanical Retains Primacy

Electromechanical platforms dominated the motion control market with a 60.55% share in 2025, favored for clean operation, scalable precision, and straightforward integration with digital twins. The shift toward net-zero processes and lower utility bills accelerates adoption of servo-electric presses, replacing hydraulic counterparts. Pneumatic solutions, now equipped with pressure sensors and IO-Link valves, are expanding at 6.85% CAGR by satisfying low-force pick-and-place tasks where speed trumps accuracy.

The hybridization trend marries electric actuators with proportional hydraulics, allowing force-dense yet energy-efficient motion. Electric linear actuator revenues are projected to climb from USD 20.5 billion in 2022 to USD 34.3 billion by 2032, mirroring sustainability mandates in automotive stamping and food packaging.

By System Type: Closed-Loop Precision Prevails

Closed-loop architectures comprised 51.62% of the motion control market share in 2025, advancing at 6.05% CAGR as Industry 4.0 requires position feedback for every axis. High-resolution encoders and faster DSPs are pushing sub-micron accuracy, essential for lithography and DNA sequencers. Open-loop stepper arrays linger in cost-sensitive conveyors but gradually cede to sensorless-vector drives that approximate closed-loop performance without encoders.

Machine learning now tunes PID parameters, reducing commissioning from hours to minutes. In gantry printers, synchronized drives refine X-Y-Z interpolation to unlock complex lattice structures in aerospace parts.

By Application: Material Handling Dominates Logistics Automation

Material handling captured 27.54% of the motion control market size in 2025, fueled by e-commerce fulfillment centers that rely on high-speed sorters and AS/RS cranes. Tight labor pools and next-day delivery promises are accelerating conveyor retrofits with energy-saving regenerative drives. Mobile robotics is the breakout segment, expanding 7.35% CAGR as factories deploy AMRs for line-side replenishment and mixed-model assembly.

Packaging lines integrate vision-guided robots that adjust to new SKUs on the fly, while additive manufacturing demands non-linear acceleration profiles to print complex geometry at speed. Inspection systems leverage high-speed stages to run 100% quality checks without slowing throughput.

By End-User Industry: Automotive Commands, Pharma Accelerates

Automotive retained 23.48% share in 2025, driven by electric-vehicle battery assembly, laser welding, and end-of-line testing. OEMs are replacing hydraulic presses with servo-electric units to meet lightweighting goals and track energy consumption. Pharmaceutical and life sciences, rising at a 7.12% CAGR, are modernizing aseptic fill-finish lines in response to FDA Annex 1, demanding hygienic, stainless-steel servo actuators with redundant feedback loops.

Electronics and semiconductor fabs depend on vacuum-compatible stages for die attach and wafer handling, while food and beverage plants automate case packing under stringent hygiene rules. Aerospace manufacturers use gantry routers and fiber-placement machines that require synchronized multi-axis control to lay composites accurately.

Geography Analysis

Asia Pacific held 37.65% of global revenue in 2025, propelled by China’s shift from low-cost assembly to high-automation production and South Korea’s record semiconductor outlays. India’s Production Linked Incentive program is catalyzing electronics parks that specify servo-electric pick-and-place units in SMT lines. Regional policy support, low-cost engineering talent, and rising wages converge to make automation pay back in under two years for many factories.

North America leverages reshoring incentives and tax credits to upgrade brownfield plants with energy-efficient drives. U.S. OEMs emphasize cyber-secure architectures, a response to high-profile ransomware attacks on OT networks. ABB’s USD 100 million Wisconsin campus exemplifies investment aimed at shortening supply chains and supporting quick-turn customization.

Europe prioritizes green manufacturing; German automakers retrofit servo presses with energy-recuperation modules to meet Scope 1 targets. The NIS2 directive introduces strict encryption for motion networks, slowing some projects but ultimately fostering resilient architectures. Collaborative robot adoption is high as demographic aging creates skilled-labor gaps, particularly in Italy and Spain.

Competitive Landscape

The market remains moderately fragmented, yet consolidation is gaining momentum. Bosch’s planned acquisition of Elmo Motion Control extends its reach into high-performance servos for semiconductor tools, signalling a race to integrate hardware with advanced drive firmware. ABB’s OmniCore platform improves path repeatability to under 0.6 mm while cutting energy use 20%, positioning software and analytics as competitive differentiators.

Subscription-based “robot-as-a-service” models from startups such as Formic Technologies lower CAPEX barriers for SMEs, challenging incumbents to craft outcome-based contracts. Siemens’ Standard Robot Command Interface aligns PLCs and cobots under a single API, easing multi-vendor cell integration and reinforcing ecosystem competition.

Component shortages and magnet price hikes favor suppliers with dual-sourcing and vertical integration. Mitsubishi Electric invests in U.S. motor and compressor plants to buffer currency risk and shipping delays. Regional specialists—Hiwin in linear motion and Inovance in Chinese drives—retain share through local service networks and rapid customization.

Motion Control Industry Leaders

Siemens AG

Schneider Electric SE

Mitsubishi Electric Corporation

ABB Ltd.

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mitsubishi Electric began shipping samples of its 3.3 kV, 1,500 A XB-series HVIGBT module with 15% lower switching loss, targeting large-inverter markets.

- February 2025: Bosch agreed to acquire Elmo Motion Control, strengthening its high-performance servo portfolio.

- January 2025: Moog reported USD 910 million sales for Q1 2025, up 6% year on year, driven by aerospace demand.

- December 2024: Mitsubishi Electric announced a USD 143.5 million heat-pump compressor plant in Kentucky, supported by USD 50 million DOE funding.

Global Motion Control Market Report Scope

A motion controller contains motion profiles and target positions that create trajectories for motors and actuators. Motion control drives are a structural part of motion controllers. The scope of the study tracks the revenue accrued from the sale of various types of motion control devices that are used by different end-user industries in multiple geographies. Due to the advancement in processing speed, precision, and reliability of these systems, the controllers are widely used in industries. Further, the study also covers the impact of COVID-19 on the market.

| Motors |

| Drives |

| Controllers |

| Actuators and Mechanical Systems |

| Sensors and Feedback Devices |

| Software and Services |

| Electromechanical |

| Hydraulic |

| Pneumatic |

| Open Loop |

| Closed Loop |

| Single Axis |

| Multi-Axis |

| Material Handling |

| Packaging |

| Assembly and Disassembly |

| Inspection and Testing |

| Robotics |

| 3D Printing / Additive Manufacturing |

| Electronics and Semiconductor |

| Pharmaceutical / Life Sciences / Medical Devices |

| Oil and Gas |

| Metal and Mining |

| Food and Beverage |

| Automotive |

| Aerospace and Defense |

| Logistics and Warehousing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Motors | ||

| Drives | |||

| Controllers | |||

| Actuators and Mechanical Systems | |||

| Sensors and Feedback Devices | |||

| Software and Services | |||

| By Technology | Electromechanical | ||

| Hydraulic | |||

| Pneumatic | |||

| By System Type | Open Loop | ||

| Closed Loop | |||

| By Axis Type | Single Axis | ||

| Multi-Axis | |||

| By Application | Material Handling | ||

| Packaging | |||

| Assembly and Disassembly | |||

| Inspection and Testing | |||

| Robotics | |||

| 3D Printing / Additive Manufacturing | |||

| By End-user Industry | Electronics and Semiconductor | ||

| Pharmaceutical / Life Sciences / Medical Devices | |||

| Oil and Gas | |||

| Metal and Mining | |||

| Food and Beverage | |||

| Automotive | |||

| Aerospace and Defense | |||

| Logistics and Warehousing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the motion control systems market?

The market stands at USD 19.08 billion in 2026 and is forecast to reach USD 24.23 billion by 2031, posting a 4.9% CAGR.

Which end-user industry is expanding the fastest?

Pharmaceutical and life sciences leads, advancing at a 7.12% CAGR through 2031 on the back of FDA Annex 1 modernization.

Why are decentralized servo drives gaining popularity?

They lower cabling by up to 86% and embed safety and analytics at the motor, cutting installation time and boosting flexibility.

How are semiconductor fab investments influencing demand?

South Korea’s USD 471 billion megacluster and related Asian projects require nanometer-precision motion control, lifting servo and linear-motor orders.

What is the most significant restraint to growth today?

Rare-earth magnet price spikes increase servo-motor costs by up to 25%, pressuring OEM margins and project budgets.

Which geographical region dominates the market?

Asia Pacific holds 37.65% share, driven by aggressive automation roll-outs and government-backed electronics initiatives.

Page last updated on: