Flow Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.85 Billion |

| Market Size (2031) | USD 11.17 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flow Control Market Analysis by Mordor Intelligence

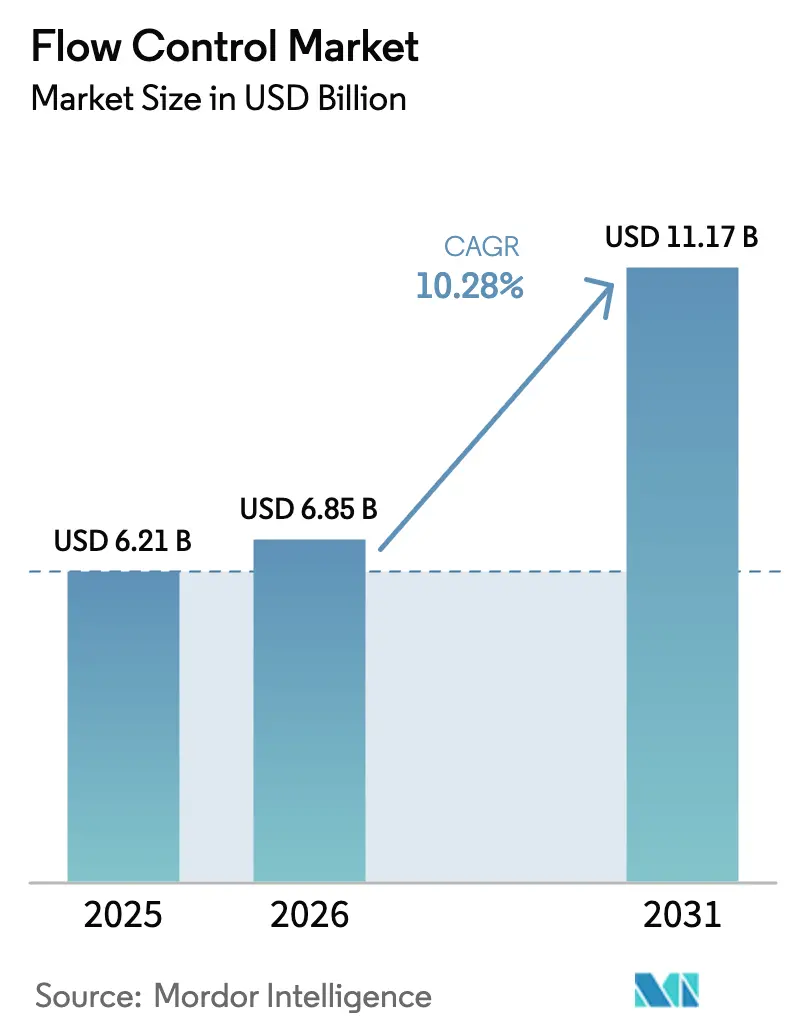

The Flow Control market size is expected to grow from USD 6.21 billion in 2025 to USD 6.85 billion in 2026 and is forecast to reach USD 11.17 billion by 2031 at 10.28% CAGR over 2026-2031. This continued expansion reflects simultaneous investments in industrial digitization, infrastructure renewal, and stricter environmental oversight, which are reshaping process-control architectures. Enterprise spending focuses on smart devices that support predictive maintenance while ensuring uptime. End users are increasingly favoring suppliers that combine mechanical expertise with secure, cloud-ready analytics. Asia Pacific maintains the strongest regional pull, underpinned by China’s automation drive, India’s Production Linked Incentive schemes, and steady LNG terminal construction across Southeast Asia.[1]Economic Times, “PLI Scheme for Electronics Manufacturing Gets Extension Till 2025-26,” economictimes.indiatimes.com In parallel, the tightening EU and U.S. emission norms accelerate the replacement of legacy valves with certified low-leakage designs, even as specialty alloy shortages and cybersecurity threats introduce cost volatility and risk.

Key Report Takeaways

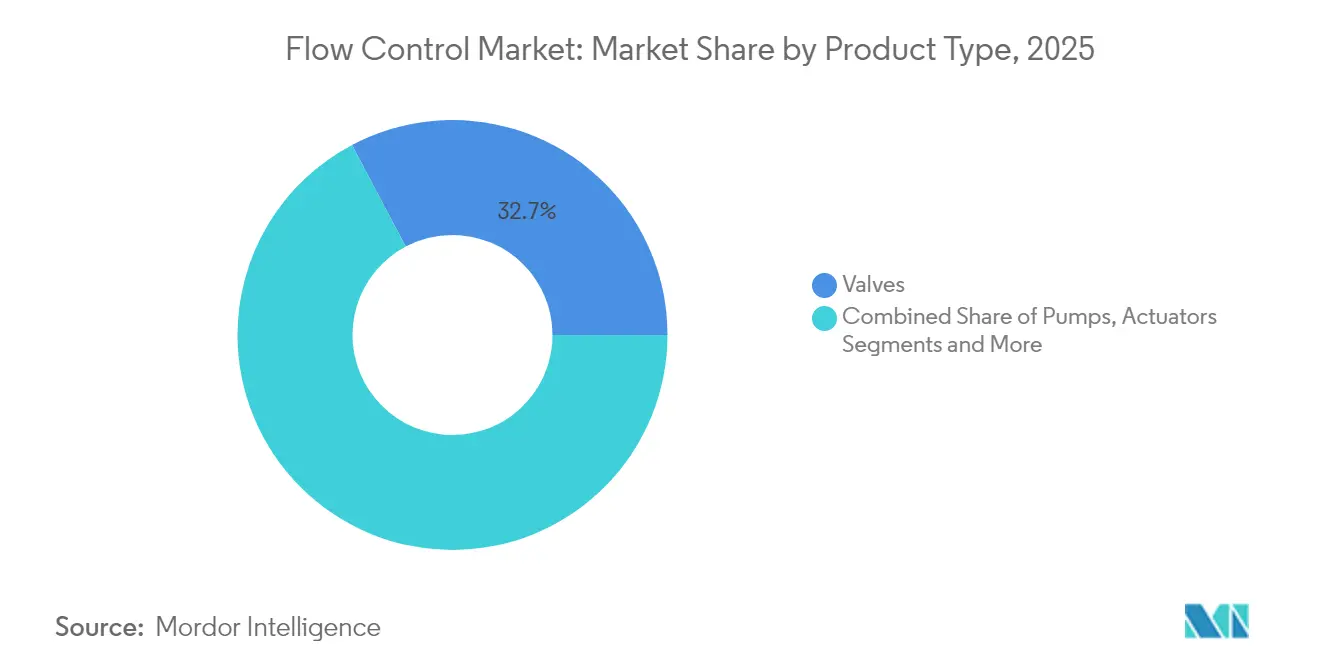

- By product type, valves led with 32.74% revenue share of the flow control equipment market in 2025 and is projected to expand at a 13.16% CAGR through 2031.

- By end-user industry, oil and gas held 28.12% of the flow control equipment market share in 2025, while pharmaceuticals and biotechnology recorded the highest projected CAGR at 11.3% through 2031.

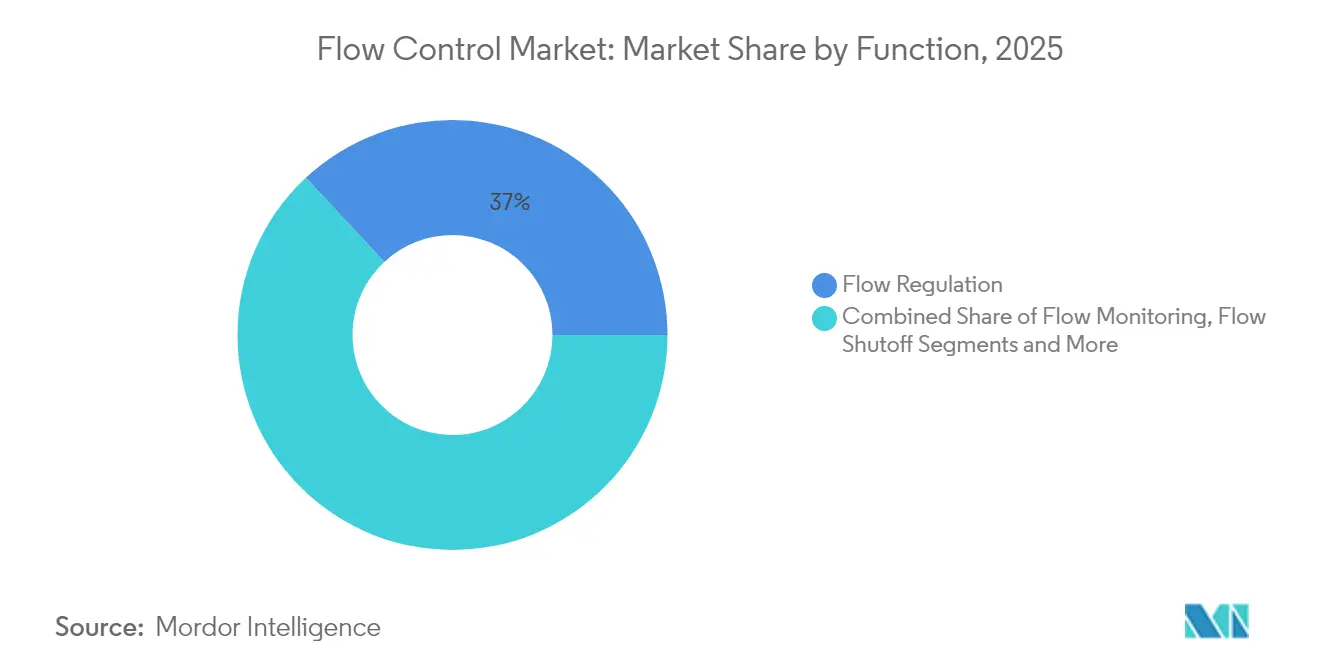

- By function, flow regulation accounted for a 36.95% share of the flow control equipment market size in 2025, and flow monitoring is advancing at a 12.55% CAGR through 2031.

- By technology, electric systems commanded 31.12% of the flow control equipment market size in 2025 and smart/digital solutions are set to rise at a 13.07% CAGR to 2031.

- By region, Asia Pacific captured 41.55% of the flow control equipment market share in 2025; the same region is projected to post a 9.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flow Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of legacy flow control infrastructure | +2.8% | North America, Europe, global roll-outs | Medium term (2-4 years) |

| Surge in LNG terminal investments across emerging economies | +2.1% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Rapid uptake of modular chemical plants | +1.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Sustainability mandates driving water reuse systems | +1.9% | Global, Europe leadership | Long term (≥ 4 years) |

| Tightening fugitive-emission regulations | +1.4% | North America, Europe | Short term (≤ 2 years) |

| Micro-precision flow for cell and gene therapies | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitization of Legacy Flow Control Infrastructure

Manufacturers are replacing pneumatic or hydraulic loops with sensor-rich electric assemblies that integrate seamlessly into plant SCADA systems. Real-time telemetry, combined with AI, reduces unscheduled downtime by as much as 30% and ensures tighter process tolerances, especially in chemical and petrochemical processes where grade yields hinge on flow accuracy.[2]ABB, “Flow Measurement Products,” new.abb.com The retrofit model appeals to mature plants because it lowers capex versus full replacement, while cloud dashboards give executives immediate visibility into energy and maintenance metrics.

Surge in LNG Terminal Investments Across Emerging Economies

Vietnam, India, and Indonesia are adding greenfield terminals that require cryogenic-ready valves, actuators, and flow meters capable of operating at temperatures of≥ –160 °C. Vietnam alone plans five new facilities worth USD 12 billion by 2030. Each terminal integrates redundant digital shutoff loops to meet safety integrity levels, opening premium niches for suppliers that can certify both extreme-temperature metallurgy and SIL-3 electronics.

Rapid Uptake of Modular Chemical Plants

Short product cycles in the specialty chemicals industry have driven the adoption of skid-mounted reactors. These modules rely on standardized connection points, enabling flow control equipment suppliers to deliver pre-engineered, drop-in packages that compress site-build schedules by 30% and reduce labor risk. The template design lets OEMs leverage common part numbers and predictive spares stocking.

Sustainability Mandates Driving Water Reuse Systems

The updated EU Urban Wastewater Treatment Directive requires a 90% reuse rate by 2030, prompting utilities and industrial parks to deploy high-accuracy magnetic flow meters and variable-speed pumps for closed-loop networks. Advanced control strategies balance nutrient removal efficiency against energy use, a calculation possible only with continuous flow telemetry at each stage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain volatility for specialty alloys | −1.8% | Global high-performance sectors | Short term (≤ 2 years) |

| Cybersecurity vulnerabilities in IIoT-enabled devices | −1.3% | Global, critical infrastructure | Medium term (2-4 years) |

| Capital expenditure cuts in upstream oil | −1.1% | Global oil and gas | Short term (≤ 2 years) |

| Fragmented aftermarket service in developing regions | −0.9% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility for Specialty Alloys

Price swings of more than 40% in nickel-based superalloys have resulted in extended lead times of over 40 weeks for severe-service valve bodies.[3]London Metal Exchange, “Stainless Steel Market Data,” lme.com Engineering teams cannot readily substitute metals without requalification, and buyers often resort to dual sourcing or maintaining inventory buffers, which can increase working capital.

Cybersecurity Vulnerabilities in IIoT-Enabled Devices

Industrial control system advisories increased by 34% in 2024, and flow devices with open-source stacks were frequently listed on exploit lists. Vendors now embed hardware roots of trust and partner with certified secure-development lifecycles, but compliance adds cost and extends validation timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Devices Outperform Traditional Hardware

Traditional valves held a 32.74% market share of the flow control equipment market in 2025 and are advancing at a 13.16% CAGR. Pumps and actuators remain essential for bulk fluid movement; however, their growth trails that of the intelligent valve segment, as predictive algorithms have proven to reduce maintenance outlays. Flow meters benefit from compliance-driven demand for accurate discharge reporting. Collectively, upgraded smart assemblies are expanding the installed base for diagnostics platforms, supporting aftermarket revenues that now account for more than 20% of vendor totals.

The retrofit wave favors hybrid solutions, where digital positioners are bolted onto legacy bodies, creating cost-effective pathways to analytics without halting production. Vendors with modular electronics platforms offer tailored signal protocols, including HART, Modbus, and OPC UA, which support multi-vendor architectures within brownfield plants. Suppliers also preload calibration curves that meet ISO 5167 traceability standards, thereby accelerating regulatory audits.

By End-User Industry: Life-Science Demand Accelerates

Oil and gas companies maintained a 28.12% market share of flow control equipment in 2025, driven by LNG expansion and methane leak reduction initiatives. Yet pharmaceuticals and biotechnology lead growth at 11.3% CAGR as cell and gene therapy lines proliferate. Water and wastewater utilities sit close behind, catalyzed by circular-economy projects. Power generators retrofit flow circuits to manage varying renewable inputs while maintaining grid inertia, which boosts demand for fast-response control valves. Chemical firms are shifting toward modular pilot plants that require reconfigurable flow skids, and hygienic food and beverage processors are buying sanitary diaphragm valves compatible with automated clean-in-place cycles.

The life-science boom hinges on validated documentation; suppliers that bundle electronic records with each skid reduce customer qualification effort. Meanwhile, conventional energy firms concentrate their spending on safety-critical units that deliver quantifiable reductions in leaks, tying equipment choices to emissions-credit strategies.

By Function: Monitoring Overtakes Pure Regulation

Flow regulation accounted for 36.95% of the flow control equipment market size in 2025. Monitoring, however, advances at a 12.55% CAGR because data-centric management unlocks incremental energy savings and enables rapid anomaly detection. Shutoff functions grow in tandem with stricter process-safety mandates, and diversion devices support multi-product production lines seeking agile changeovers.

Real-time monitoring is no longer optional under tightened environmental permits. Continuous data streams feed historian databases and predictive models that can forecast seal degradation weeks in advance. Plants that exploit these insights report a 20% reduction in emergency call-outs.

By Technology: Electric Platforms Dominate While Digital Layers Scale

Electric actuation accounted for 31.12% of 2025 revenue, thanks to its precision and ease of wiring. Smart/digital overlays are projected to grow at a 13.07% CAGR through 2031 as OEMs release wireless-ready boards and cloud-based dashboards. Pneumatics remain prevalent in explosion-prone zones, although the costs of air compression and decarbonization targets constrain their adoption. Hydraulics cater to heavy-thrust niches but suffer weight and maintenance drawbacks. Edge gateways now sit atop valve or pump housings, enabling encrypted MQTT data transfer to plant clouds within minutes of installation.

Geography Analysis

Asia Pacific’s 41.55% share illustrates unmatched project volume ranging from Chinese semiconductor plants to Indian biomanufacturing parks. Government incentives, low labor costs, and rapid permitting compress asset lifecycles. Digital retrofit programs trail greenfield build-outs but are gaining traction as multinationals demand common OT standards across regions.

North American buyers allocate budgets for cyber-secure upgrades to safety-instrumented nodes, encouraged by federal critical infrastructure directives. U.S. LNG export expansion likewise sustains cryogenic valve demand. European end users earmark capex for leak-detection-and-repair equipment to meet Industrial Emissions Directive revisions, and municipal utilities have begun multi-year upgrades to achieve 2030 water reuse targets.

Gulf Cooperation Council members are integrating IIoT-based smart district cooling networks that run on looped chilled water, driving sales of corrosion-resistant butterfly valves. South American mining output boosts slurry-duty valve consumption, but macroeconomic volatility hinders capital cycles. African water-treatment build-outs are in their early stages; development banks stipulate that hardware include remote diagnostics to minimize site visits.

Competitive Landscape

The flow control market remains moderately fragmented. However, hundreds of regional specialists compete in niche alloys, hygienic skids, or service contracts. M&A momentum favors digital capability gaps; Emerson’s USD 11 billion purchase of AspenTech in 2024 merged sensing hardware with AI-powered optimization suites.[4]Reuters, “Emerson Completes Acquisition of AspenTech,” reuters.com Siemens invested USD 2.1 billion to expand smart-instrument manufacturing footprints in Germany and China, ensuring capacity near end markets while introducing carbon-neutral production lines.

Flowserve secured a USD 850 million, multi-terminal LNG contract in Vietnam, its largest win in the Asia Pacific region, leveraging its proven cryogenic performance and local service centers. Honeywell’s Experion HS SCADA release embeds secure-boot firmware and anomaly-based intrusion detection, underscoring the centrality of cybersecurity. Emerging software-only firms monetize valve data via subscription dashboards, tempting asset owners keen to move capex to opex, while legacy OEMs counter by bundling lifetime analytics within hardware list prices.

Patent filings underscore innovation pressure: more than 200 smart-valve submissions landed at the USPTO during 2024 alone, covering wireless power harvesting, self-calibrating trim, and edge AI diagnostics. Suppliers that can certify both process safety and data security stand best placed to command premium margins.

Flow Control Industry Leaders

Emerson Electric Company

Flowserve Corporation

Siemens AG

Honeywell International Inc.

Alfa Laval AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Emerson completed the USD 11 billion acquisition of AspenTech, bolstering its hybrid hardware-software offering and positioning the firm as a single-source vendor for predictive maintenance and autonomous optimization platforms.

- December 2024: Siemens has announced a USD 2.1 billion capacity expansion in Germany and China, focusing on IIoT-enabled valves and flow meters, designed to meet demand from chemical and pharmaceutical digitization programs.

- November 2024: Flowserve won a USD 850 million supply contract for three Vietnamese LNG terminals, securing multiyear services agreements that underpin aftermarket revenue visibility.

- October 2024: Honeywell launched Experion HS SCADA with integrated cybersecurity modules, addressing rising IIoT threat vectors while locking customers into its software ecosystem.

Global Flow Control Market Report Scope

Flow control is a part of the more comprehensive industrial sector, which consists of firms that provide products or services concerning the management and control of liquids and gases. Such products comprise pumps, valves, meters, and other related equipment. The Global Flow Control Market is Segmented by Equipment Type(Pumps, Valves, Meters, and others), By Application (Oil & Gas, Power, Marine, Mining, Electronics), and Geography.

| Valves |

| Pumps |

| Actuators |

| Flow Meters |

| Oil and Gas |

| Water and Wastewater |

| Power Generation |

| Chemical and Petrochemical |

| Pharmaceuticals and Biotechnology |

| Food and Beverage |

| Flow Monitoring |

| Flow Regulation |

| Flow Shutoff |

| Flow Diversion |

| Pneumatic |

| Hydraulic |

| Electric |

| Smart/Digital |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Valves | ||

| Pumps | |||

| Actuators | |||

| Flow Meters | |||

| By End-user Industry | Oil and Gas | ||

| Water and Wastewater | |||

| Power Generation | |||

| Chemical and Petrochemical | |||

| Pharmaceuticals and Biotechnology | |||

| Food and Beverage | |||

| By Function | Flow Monitoring | ||

| Flow Regulation | |||

| Flow Shutoff | |||

| Flow Diversion | |||

| By Technology | Pneumatic | ||

| Hydraulic | |||

| Electric | |||

| Smart/Digital | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Singapore | |||

| Australia | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

Which region holds the largest share of global demand?

Asia Pacific captured 41.55% of 2025 spending, driven by automation-intensive industrial expansion.

Which product segment is forecast to grow fastest?

Smart and digital valves are set to expand at 13.07% CAGR as plants retrofit predictive capabilities.

Why are pharmaceuticals and biotechnology driving orders?

Cell and gene therapy lines require ultra-clean, precision flow systems, propelling a segment CAGR of 11.3%.

What risks could slow adoption of IIoT-ready devices?

Heightened cybersecurity threats and specialty-alloy shortages could temper near-term deployment.

Page last updated on: