Mass Flow Controller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

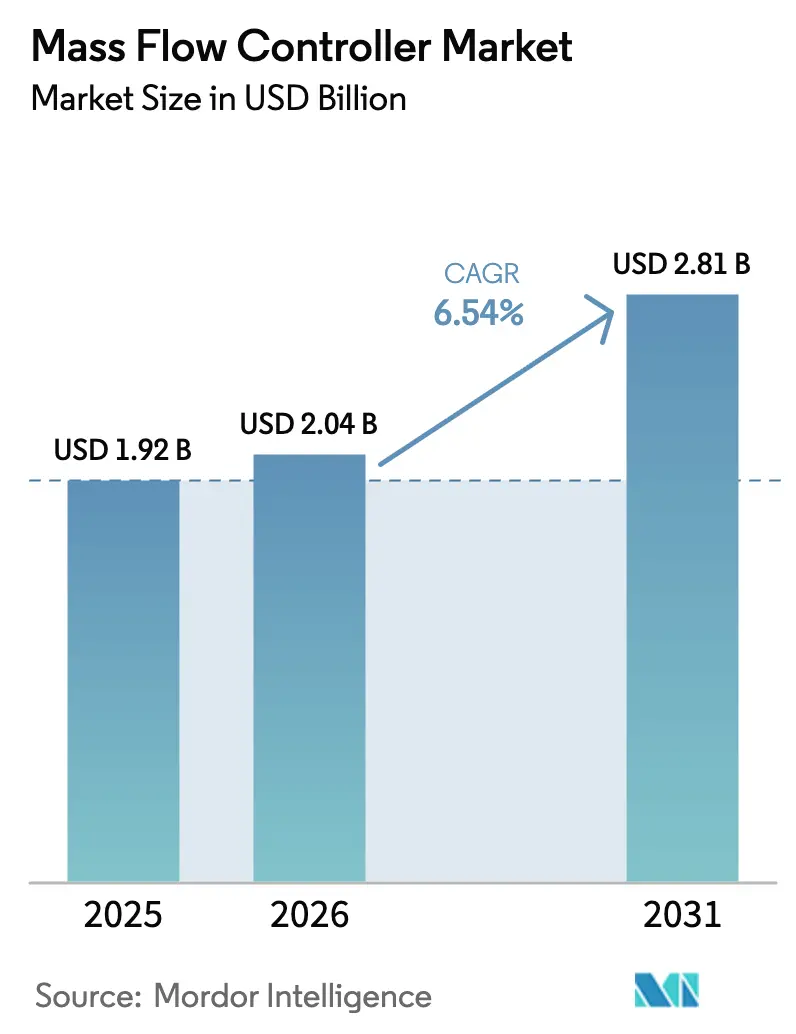

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mass Flow Controller Market Analysis by Mordor Intelligence

The mass flow controller market size is expected to grow from USD 1.92 billion in 2025 to USD 2.04 billion in 2026 and is forecast to reach USD 2.81 billion by 2031 at 6.54% CAGR over 2026-2031. This steady trajectory reflected how precision gas-flow devices shifted from a niche laboratory tool into a production-critical asset across chip fabrication, green hydrogen, additive manufacturing, and biologics processing. Customers invested in higher-purity gas lines, tighter leak tolerances, and integrated diagnostics to protect yields and minimize downtime. Semiconductor capital-expenditure commitments in Asia elevated baseline demand, while tighter environmental policies in Europe and North America spurred retrofit programs that replaced legacy flow meters with digital, self-monitoring platforms. Pricing pressure from Chinese entrants moderated average selling prices but also widened the addressable base of lower-tier users.

Key Report Takeaways

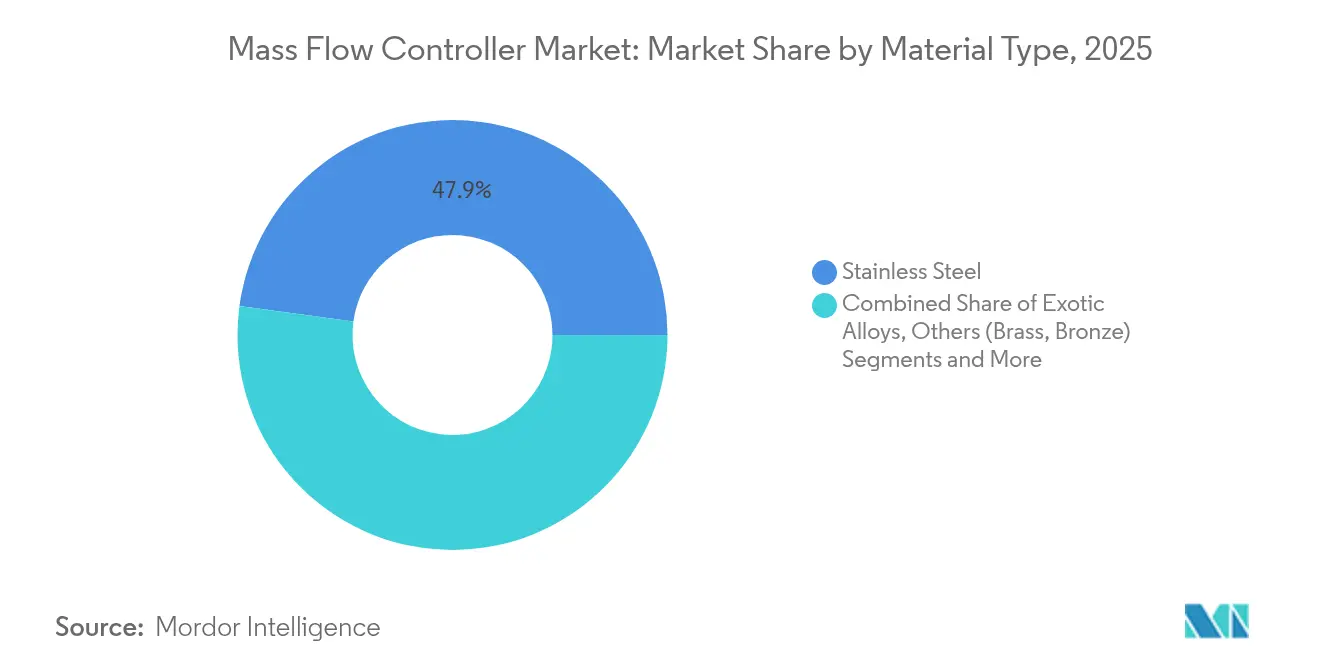

- By material type, stainless steel held 47.85% of the mass flow controller market share in 2025; exotic alloys are set to expand at an 8.35% CAGR to 2031.

- By flow rate, low-flow applications accounted for 43.90% of the mass flow controller market size in 2025, while high-flow solutions are projected to grow at 9.02% through 2031.

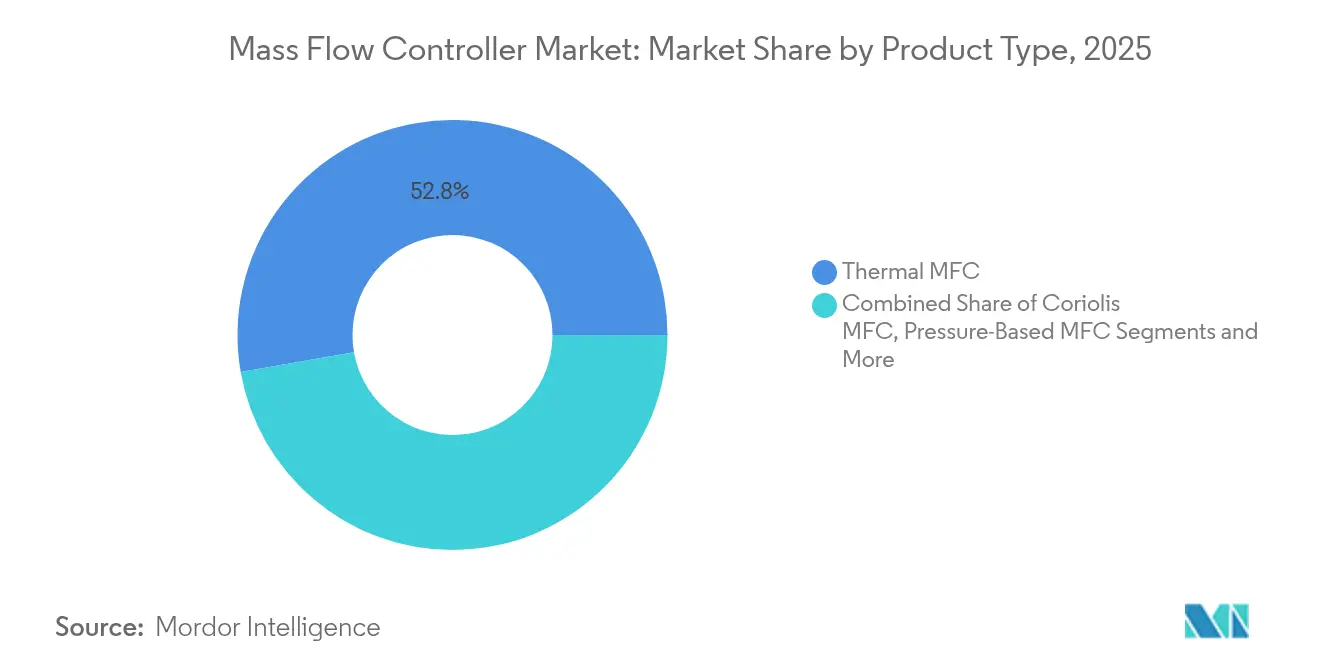

- By product type, thermal technology led with 52.75% revenue share in 2025; Coriolis units are forecast to register a 9.85% CAGR over the same horizon.

- By end-user industry, semiconductor fabrication commanded 36.85% of the mass flow controller market size in 2025; renewable energy and fuel cells are poised for a 12.1% CAGR to 2031.

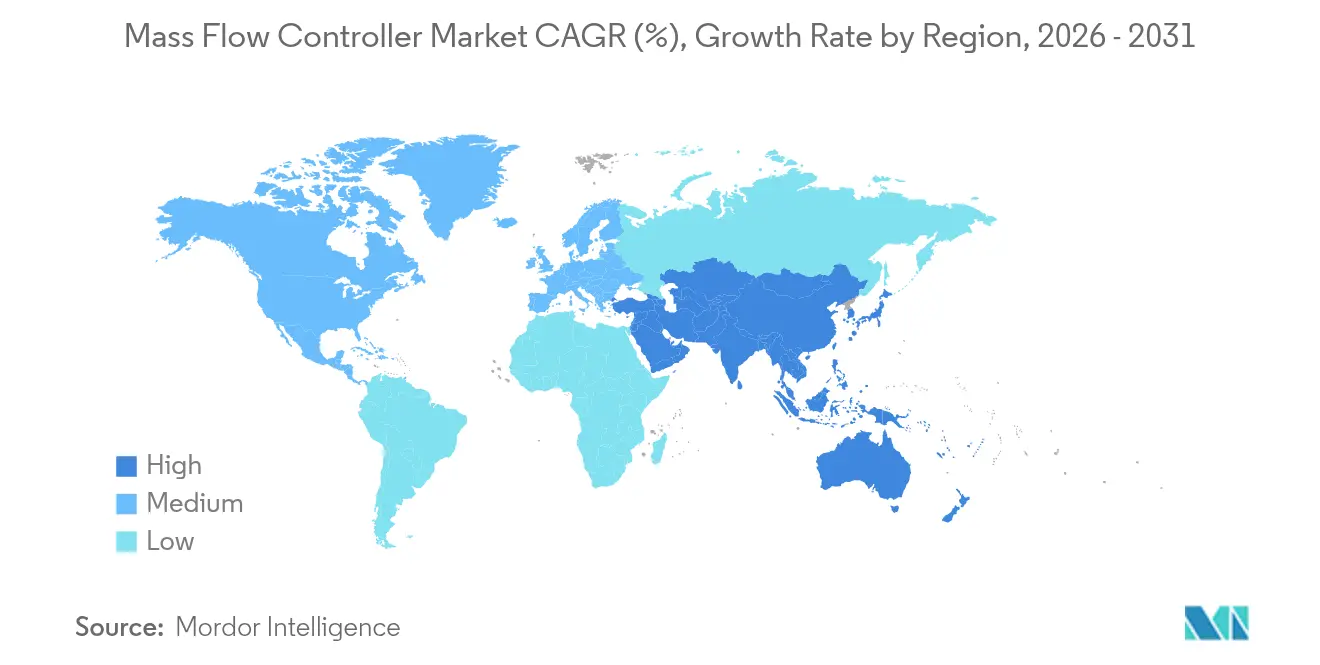

- By geography, Asia-Pacific dominated with 41.90% market share in 2025 and is on track for a 9.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Mass Flow Controller Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chip-fab CAPEX surge in Asia | +2.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Green-hydrogen electrolyzer build-out | +1.8% | Global, early gains in Europe and North America | Long term (≥ 4 years) |

| Additive-manufacturing gas demand | +1.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| IIoT-enabled self-diagnostics adoption | +0.9% | Global | Short term (≤ 2 years) |

| Biologics single-use bioreactors growth | +1.1% | North America and EU core, expanding globally | Medium term (2-4 years) |

| Emissions-regulation retrofits | +0.7% | Global, strongest in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chip-fab CAPEX Surge in Asia

Capital spending by foundries and memory producers accelerated after 2024, with wafer-fab equipment outlays projected to reach USD 165 billion by 2029. New sub-5 nm nodes imposed tighter purity specifications, making ultra-clean gas lines and leak-free valves mandatory. Local toolmakers cooperated with service partners such as ProperSys to secure TSMC vendor awards that depend on sub-ppm contamination ratings.[1]ProperSys Corporation, “About ProperSys,” propersyscorp.com Helium requirements for cooling and purge operations multiplied, and scarcity pushed fabs to deploy recovery systems that rely on high-accuracy flow feedback from digital mass controllers. Tier-1 suppliers responded by introducing corrosion-resistant alloy bodies, integrated pressure sensors, and multi-gas calibration firmware that shortened qualification loops from months to weeks. The result was a sustained baseline pull for the mass flow controller market even during memory down-cycles.

Green-hydrogen Electrolyzer Build-out

Rapid commissioning of proton-exchange-membrane electrolyzers demanded precise flow monitoring to maximize hydrogen yield and ensure safety. Flow switches such as the SIL-2-rated FS10i from Fluid Components International supplied redundant verification on cathode feed lines. System integrators bundled mass meters with purity analyzers and flame arrestors, creating turnkey skids that minimized project risk for investors. European initiatives such as the Hycamite methane-splitting plant in Finland adopted valve packages from Valmet, highlighting how flow-component choices were embedded in EPC contracts. As electrolyzer stacks scaled from megawatt to gigawatt blocks, operators demanded controllers that could handle dynamic inlet pressure swings without recalibration. This long-cycle infrastructure build locked in multi-year revenue visibility for the mass flow controller market.

Additive-manufacturing Gas Demand

Metal powder-bed fusion printers required inert atmospheres to prevent oxidation, creating continuous demand for argon and nitrogen flow control. Research at the Technical University of Denmark showed that plume clearing velocity directly correlated with part density, elevating the role of high-response mass meters in process tuning. Suppliers such as Desktop Metal patented Péclet gap seals and aerostatic elements to maintain stable enclosures, and their designs incorporated embedded flow sensors for closed-loop control. Helium blends used in wire-arc additive systems improved arc stability and deposition speed but added cost, incentivizing precise flow metering to reduce waste. As printer fleets shifted from prototypes to 24-hour production cells, users upgraded to networkable controllers capable of logging consumption, flagging leaks, and integrating with MES dashboards.

IIoT-enabled Self-diagnostics Adoption

Digitally connected mass flow controllers evolved into edge devices that stream real-time performance metrics. KROHNE’s smart meter valves combined pressure, temperature, and flow data in a single IP-enabled body, supporting condition-based maintenance strategies. Case studies in food packaging demonstrated that predictive analytics shrank fill-weight variance from ±7% to ±0.5% and lifted equipment effectiveness by more than 15%. New entrants like Sensirion leveraged CMOS-MEMS production to cut lead times to just eight weeks, giving OEMs more flexibility for design changes. Quick delivery became a competitive differentiator as fab projects sought to de-risk schedules.

Restraints Impact Analysis of Mass Flow Controller Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Helium supply tightness | -1.4% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Low-cost Chinese price competition | -0.8% | Global, strongest in price-sensitive segments | Medium term (2-4 years) |

| Lengthy multi-gas qualification cycles | -0.6% | Global | Medium term (2-4 years) |

| Particulate-induced field failures | -0.4% | Global, higher in harsh environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Helium Supply Tightness

Qatar and the United States supplied most of the world’s helium, leaving chipmakers exposed to geopolitical shocks and plant outages. South Korean fabs recorded price increases above 40% between 2020 and 2024, forcing rapid installation of recovery units. Recovery efficiency hovered at 60% on average, so high-flow cooling loops still consumed fresh helium, making every percentage point of leakage a direct cost hit. Flow-controller vendors responded with micro-leak certified seals and sub-sccm set-point stability to stretch gas inventories. Service contracts increasingly bundled helium-audit modules that benchmarked consumption and recommended purge-cycle adjustments. Despite mitigation measures, the constraint curtailed near-term installation rates for certain high-flow etch tools that rely on helium cryogenic lines.

Low-cost Chinese Price Competition

Domestic Chinese producers leveraged scale and government incentives to undercut Western incumbents, especially in general-purpose laboratory and industrial niches. Beijing Sevenstar Flow introduced multi-gas meters priced 20–30% below traditional brands, prompting customers to re-evaluate qualification thresholds.[2]Beijing Sevenstar Flow Co., “Mass Flowmeter Flow Control,” mfcsevenstar.com Established European suppliers such as Bronkhorst emphasized EU manufacturing origin to reassure buyers wary of tariff or export-control complications. The price gap eroded margins, driving incumbents toward premium features such as in-situ diagnostics, sub-ppm leak ratings, or bundled software analytics. Nonetheless, stringent semiconductor protocols and defense-related cyber-security rules still limited adoption of low-tier imports in high-value fabs, capping the overall dampening effect on the mass flow controller market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Mass Flow Controller Market Segment Analysis

By Material Type:

Exotic Alloys Extend Performance EnvelopeSales data indicated that stainless steel bodies captured 47.85% revenue in 2025 because they met the corrosion-resistance needs of most industrial gases at competitive price points. Exotic alloys such as Hastelloy and Inconel, however, posted the strongest 8.35% CAGR outlook as they enabled ultra-clean delivery of dopant gases in sub-10 nm semiconductor lines. Molybdenum price spikes near USD 90 per kg pushed fabricators to re-engineer weldments and reduce scrap rates to protect margins. Operators that upgraded to exotic alloys reported longer mean-time-between-service intervals and lower particle counts, advantages that outweighed the upfront premium.

The mass flow controller market saw material choice evolving into a procurement lever: fabs standardized alloy SKUs to simplify spares, while biotech OEMs adopted electropolished Inconel for single-use bioreactors that demanded sterility. The “others” category—brass, bronze, and polymer composites—retained niche appeal for low-pressure benchtop devices. Global buyers negotiated dual-source contracts to shield against alloy shortages, making supply-chain resilience nearly as important as metallurgical performance.

By Flow Rate:

High-Flow Solutions Gain MomentumLow-flow devices, typically rated below 20 sccm, accounted for 43.90% of the mass flow controller market in 2025 because laboratories and analytical instruments favored finely resolved set-points. Yet high-flow units above 50 slm are set to grow 9.02% annually through 2031 as hydrogen plants, large-format 3D printers, and semiconductor wet benches scale up gas volumes. HORIBA’s ultra-thin DZ-107 controller demonstrated how vendors pushed compactness while managing etch-tool flows over 200 slm. Energy project developers specified flow turndown ratios exceeding 100:1 so one meter could cover startup purge and full-load operation, boosting demand for mixed-range product portfolios.

OEMs optimized inventory by matching flow brackets precisely to duty cycles rather than oversizing, which reduced CapEx and improved control resolution. Meanwhile, medium-flow controllers remained pivotal in pharmaceutical fermentation skids and specialty chemical reactors that balanced batch accuracy with throughput. The mass flow controller market therefore fragmented into performance-tuned tiers instead of one-size-fits-all offerings, encouraging vendors to release specialized firmware and diaphragm selections for each flow band.

By Product Type:

Coriolis Measurement AcceleratesThermal MFCs led revenue with 52.75% share in 2025 due to affordability and broad gas compatibility. Sensirion’s CMOS-based SFC6000 underscored ongoing innovation in this class, delivering ±0.5% accuracy and eight-week lead times that outpaced industry norms. Coriolis technology, though pricier, posted a 9.85% CAGR outlook because it measures mass directly, bypassing density corrections and calibration drift when users switch gas mixes. Hydrogen production skids valued this versatility because feed-stocks and purge streams changed with electrolyzer duty cycles.

Differential-pressure controllers addressed niche uses where line pressure acted as the primary control variable, while pressure-based MFCs targeted legacy chemical plants that already relied on static pressure instruments. Product managers integrated multi-parameter sensing—temperature, pressure, density—into Coriolis bodies, enabling single-flange installation that saved footprint in crowded fabs. Continuous firmware upgrades added self-learning algorithms that compensated for sensor aging, extending calibration intervals and reducing total cost of ownership across the mass flow controller market.

By End-user Industry:

Renewable Energy Surges AheadSemiconductor applications held 36.85% revenue share in 2025 because every advanced tool cluster required dozens of high-precision controllers for dopant, purge, and cooling gases. Yet renewable-energy and fuel-cell installations are projected to grow 12.1% annually through 2031, powered by national hydrogen roadmaps and stationary fuel-cell deployments. Flowserve’s 2024 acquisition of severe-service valve maker MOGAS brought metallurgies suited to hot ammonia crackers, signalling how flow-control portfolios expanded into green-energy niches.

Oil and gas operations continued to invest in flare-gas monitoring to meet emissions targets, while pharmaceutical and biotechnology plants upgraded dissolved-oxygen control loops for cell-culture consistency. Food-and-beverage processors adopted nitrogen dosing to extend shelf life, and water utilities installed inline thermal meters to stabilize ozone disinfection systems. This broadened end-market mix insulated the mass flow controller market from single-sector downturns, providing a balanced revenue foundation.

Geography Analysis

APAC Mass Flow Controller Market

Asia-Pacific dominated with 41.90% revenue in 2025, buoyed by aggressive chip-fab buildouts in Taiwan, South Korea, and mainland China. Government subsidies and local content mandates accelerated adoption of domestically manufactured controllers, though multinational brands retained share in the clean-room segments that demanded sub-single-digit-sccm repeatability. The mass flow controller market size for Asia-Pacific is expected to register a 9.35% CAGR, anchored by continued hydrogen infrastructure rollouts in Japan and Australia.

North America and Europe Mass Flow Controller Market

North America benefited from the US Chips Act, which incentivized fab construction and boosted orders for corrosion-resistant alloy bodies that met ITAR and cybersecurity clauses. Fuel-cell truck pilots in California and Texas added incremental high-flow demand, while shale producers installed thermal meters for methane-leak detection. Europe advanced through decarbonization policy, channeling funds into electrolyzer plants in Germany, the Netherlands, and the Nordic region. The EU’s strict safety codes spurred uptake of SIL-rated devices.

MEA and South America Mass Flow Controller Market

Middle East and Africa witnessed selective uptake tied to LNG expansion and desalination projects, whereas South America explored green-ammonia export corridors in Chile and Brazil. Vendors tailored channel strategies—local assembly hubs in Singapore, service depots in Arizona, and joint ventures in Poland—to deliver shorter lead times and support localization requirements across the mass flow controller market.

Competitive Landscape

The market remained moderately fragmented. MKS Instruments posted USD 936 million Q1 2025 revenue, confirming a rebound in wafer-fab equipment orders. Teledyne Technologies recorded USD 1.45 billion sales during the same period after integrating recent instrumentation acquisitions. These leaders leveraged cross-portfolio synergies—plasma sources, vacuum pumps, and gas analyzers—to lock in multiyear supply agreements with tier-1 fabs.

Strategic alliances escalated. Endress+Hauser absorbed 800 SICK employees into a flow-control joint venture that targeted process-industry digitalization. Crane Company agreed to acquire Precision Sensors and Instrumentation for USD 1,060 million, adding aerospace-grade flow transducers that carry over into hydrogen aviation prototypes. [3]Crane Company, “Crane Company to Acquire Precision Sensors & Instrumentation,” investors.craneco.com

Chinese challengers improved quality but still faced barriers in export-controlled segments. Sensirion differentiated through rapid-delivery programs, while Bronkhorst emphasized EU origin to shield customers from geopolitical risk. Start-ups focused on software overlays, offering analytics subscriptions that convert anonymized flow data into predictive maintenance insights. Intellectual-property filings around additive-manufacturing gas management and hydrogen leak detection suggested that specialized application know-how, rather than raw sensor accuracy, would shape the next competitive phase of the mass flow controller market.

Mass Flow Controller Industry Leaders

HORIBA, Ltd.

Sensirion AG

MKS Instruments

Brooks Instrument LLC

Bronkhorst High-Tech B.V.

- *Disclaimer: Major Players sorted in no particular order

Mass Flow Controller Market Companies Covered in this Report

- HORIBA Ltd.

- Sensirion AG

- MKS Instruments Inc.

- Teledyne Technologies Incorporated

- Bronkhorst High-Tech B.V.

- Brooks Instrument LLC

- Christian Brkert GmbH & Co. KG

- Sierra Instruments Inc.

- Alicat Scientific Inc.

- Parker Hannifin Corporation

- Advanced Energy Industries Inc.

- Azbil Corporation

- SMC Corporation

- Fujikin Incorporated

- Hitachi Metals Ltd.

- Tokyo Keiso Co. Ltd.

- Omega Engineering Inc.

- TSI Incorporated

- Dwyer Instruments LLC

- Aalborg Instruments & Controls Inc.

- Vogtlin Instruments AG

- Fluke Corporation

- Shanghai Fengyua Fluid Technology Co. Ltd.

- Ningbo Huazhong Instrument Co. Ltd.

- KOFLOC Corporation

Recent Industry Developments in Mass Flow Controller Market

- September 2025: Crane Company announced the USD 1,060 million acquisition of Precision Sensors and Instrumentation from Baker Hughes, reinforcing aerospace and process-flow capabilities with expected USD 390 million 2025 sales.

- July 2025: SICK and Endress+Hauser launched a process-automation partnership, transferring 800 SICK staff into the new Endress+Hauser SICK GmbH+Co. KG joint venture.

- June 2025: Valmet secured a valve contract for Hycamite’s methane-splitting hydrogen plant in Finland, Europe’s largest such project.

- May 2025: MKS Instruments reported USD 936 million Q1 2025 revenue, outpacing guidance on semiconductor demand.

Global Mass Flow Controller Market Report Scope

Mass Flow Controllers (MFCs) measure and regulate the flow of gases or liquids in various systems. By adjusting the flow path, MFCs maintain a precise and consistent flow rate, compensating for fluctuations in pressure, temperature, and other influencing factors.

The study tracks the revenue accrued through the sale of mass flow controller by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The mass flow controller market is segmented by material type (stainless steel and exotic alloys), flow rate (low flow rate, medium flow rate, and high flow rate), product type (differential pressure flow meter, thermal mass flow meter, and coriolis mass flow meter), industry(oil & gas, pharmaceutical, food & beverages, chemical, healthcare & life sciences, semiconductor, water & wastewater treatment, and others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America. The market sizes and forecasts regarding value (USD) for all the above segments are provided.

Segmentation Overview

| Stainless Steel |

| Exotic Alloys |

| Others (Brass, Bronze) |

| Low Flow Rate |

| Medium Flow Rate |

| High Flow Rate |

| Differential-Pressure MFC |

| Thermal MFC |

| Coriolis MFC |

| Pressure-Based MFC |

| Semiconductor |

| Oil and Gas |

| Pharmaceutical and Biotechnology |

| Chemical |

| Food and Beverages |

| Water and Wastewater Treatment |

| Healthcare and Life Sciences |

| Renewable Energy and Fuel Cells |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Stainless Steel | ||

| Exotic Alloys | |||

| Others (Brass, Bronze) | |||

| By Flow Rate | Low Flow Rate | ||

| Medium Flow Rate | |||

| High Flow Rate | |||

| By Product Type | Differential-Pressure MFC | ||

| Thermal MFC | |||

| Coriolis MFC | |||

| Pressure-Based MFC | |||

| By End-user Industry | Semiconductor | ||

| Oil and Gas | |||

| Pharmaceutical and Biotechnology | |||

| Chemical | |||

| Food and Beverages | |||

| Water and Wastewater Treatment | |||

| Healthcare and Life Sciences | |||

| Renewable Energy and Fuel Cells | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Taiwan | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the mass flow controller market?

The market was valued at USD 2.04 billion in 2026 and is projected to reach USD 2.81 billion by 2031 at a 6.54% CAGR.

Which region leads the mass flow controller market?

Asia-Pacific led with 41.90% revenue in 2025 due to intensive semiconductor and green-hydrogen investments.

Which product technology is growing the fastest?

Coriolis mass flow controllers are forecast to expand at a 9.85% CAGR because they offer direct mass measurement and multi-parameter sensing.

How are helium shortages affecting the industry?

Supply tightness raised gas prices, prompting fabs to adopt recovery systems and ultra-tight controllers, yet it is expected to shave about 1.4 percentage points off the market’s CAGR in the short term.

Why are exotic alloys gaining traction in mass flow controllers?

Demand for ultra-high-purity and corrosive gas handling in advanced semiconductor and biotech processes is driving an 8.35% CAGR for exotic alloy-based units.

What role does IIoT play in the mass flow controller market?

Integrated diagnostics and real-time data streaming support predictive maintenance, improve yield, and differentiate premium models, contributing roughly 0.9 percentage points to forecast growth.

Page last updated on: