Market Overview

| Study Period | 2020 - 2031 |

|---|---|

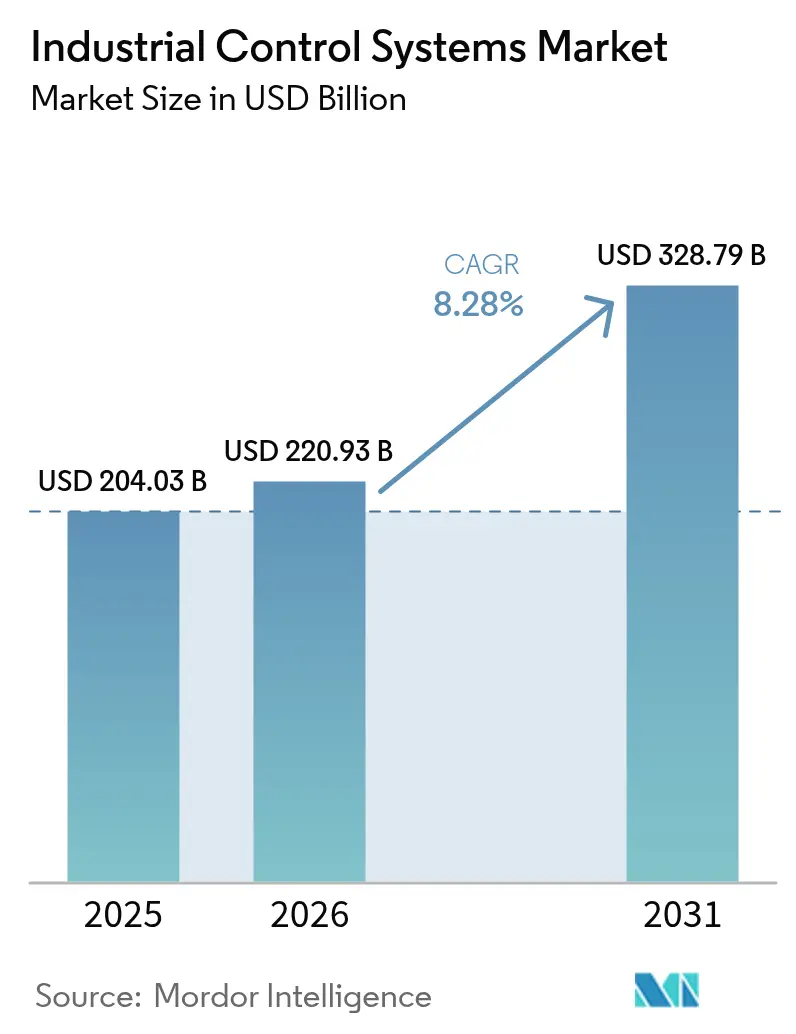

| Market Size (2026) | USD 220.93 Billion |

| Market Size (2031) | USD 328.79 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Control Systems Market Analysis by Mordor Intelligence

industrial control systems market size in 2026 is estimated at USD 220.93 billion, growing from 2025 value of USD 204.03 billion with 2031 projections showing USD 328.79 billion, growing at 8.28% CAGR over 2026-2031. Accelerated digitalization under Industry 4.0, mounting cybersecurity obligations, and the growing appeal of open, vendor-neutral architectures are reinforcing automation as an operational cornerstone rather than an efficiency add-on. Heightened supply-chain risk during the 2024 semiconductor squeeze underscored the value of software-defined control platforms that detach functionality from dedicated hardware, while government incentives in Europe and North America widened the capital pool for retrofit projects. Cloud, edge, and on-premise deployments now coexist as manufacturers seek analytics at scale without surrendering low-latency process control. Competitive positioning increasingly favors vendors that combine interoperable hardware with AI-enabled software and integrated security, especially in high-precision sectors such as electronics and life sciences.

Key Report Takeaways

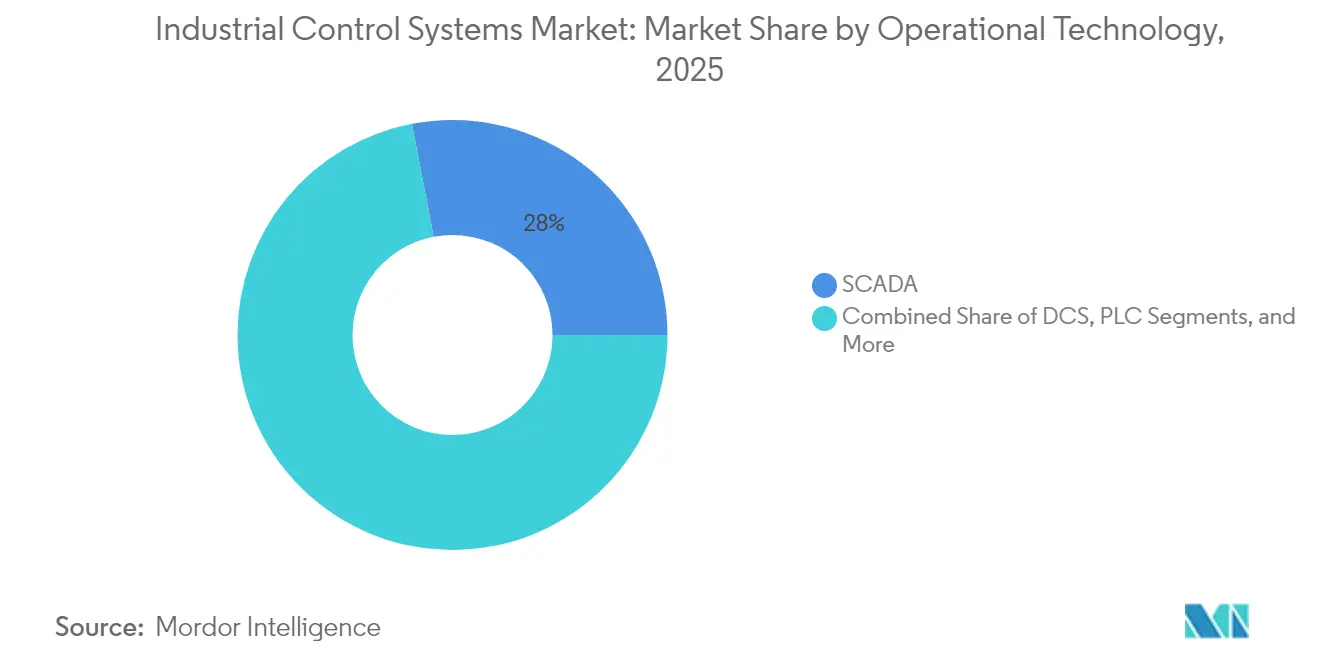

- By operational technology, SCADA held 28.02% of industrial control systems market share in 2025, while edge-enabled PLCs are forecast to expand at 11.24% CAGR through 2031.

- By software, Asset Performance Management led with 23.18% revenue share in 2025; industrial cybersecurity platforms record the highest projected CAGR at 12.55% to 2031.

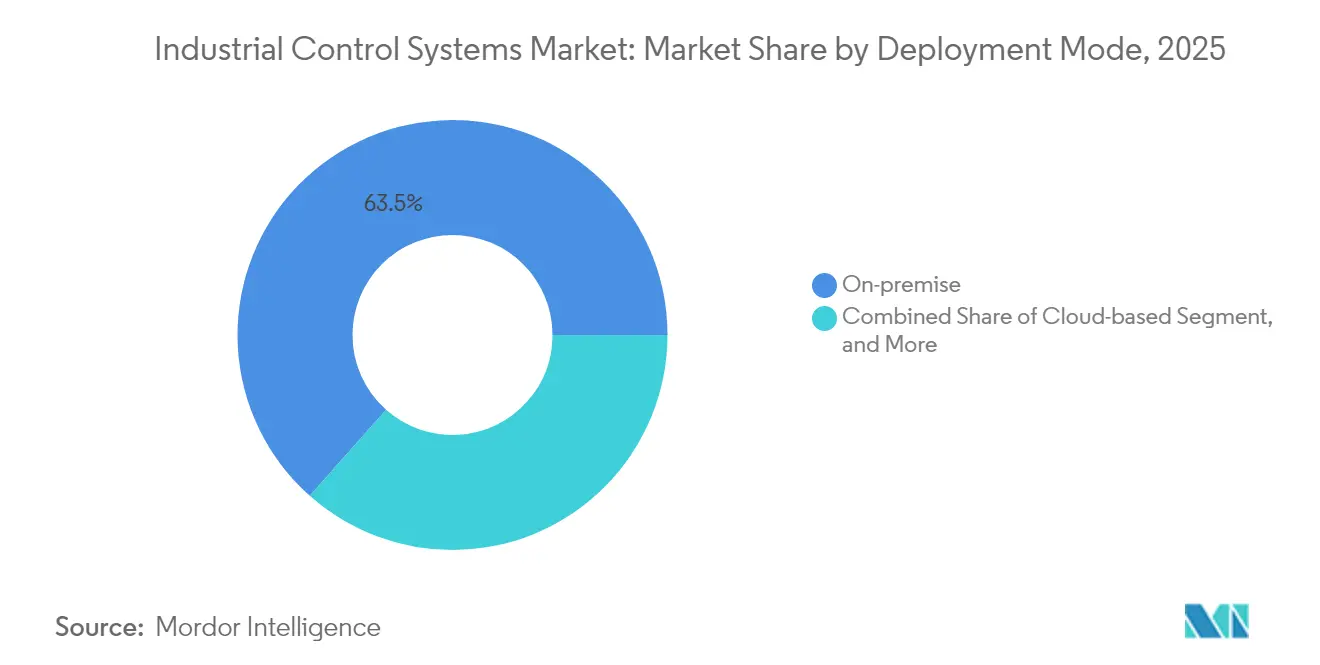

- By deployment mode, on-premise systems accounted for 63.45% of revenue in 2025, whereas cloud-based deployments are set to rise at 13.09% CAGR.

- By end-user industry, oil & gas commanded 25.05% share in 2025; electronics & semiconductor manufacturing is advancing at 12.47% CAGR to 2031.

- By geography, Europe led with 28.12% share in 2025, while Asia-Pacific is the fastest-growing region at 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 roll-outs accelerating plant-wide automation | +2.1% | Global, with concentrated gains in Germany, US, China | Medium term (2-4 years) |

| Growing emphasis on industrial safety and functional-safety compliance | +1.8% | Europe & North America core, spill-over to APAC | Long term (≥ 4 years) |

| Surge in demand for real-time data-driven mass-customisation | +1.5% | Global, with early gains in automotive and electronics hubs | Short term (≤ 2 years) |

| Government incentives for smart-factory retrofits | +1.2% | Europe, North America, selective APAC markets | Medium term (2-4 years) |

| Open Process Automation (O-PAS) architecture gaining traction | +0.8% | Global, with early adoption in oil & gas and chemicals | Long term (≥ 4 years) |

| Shift to "OT-as-a-Service" edge platforms | +0.7% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 Roll-outs Accelerating Plant-wide Automation

Manufacturers are extending automation from isolated lines to enterprise-wide networks that merge operational, engineering, and business data. AI-ready edge nodes such as Siemens SINUMERIK ONE now execute predictive maintenance and adaptive feed-rate control directly on the machine floor, shrinking decision latency.[1]Siemens Press, “SINUMERIK ONE Enables Digital-Native Machine Tools,” siemens.com Broader connectivity generates compound value, which explains why average OT budgets grew 30% in 2025 despite macro headwinds. As a result, interoperable offerings are edging out proprietary point products, reshaping competitive dynamics across the industrial control systems market.

Growing Emphasis on Industrial Safety and Functional-Safety Compliance

Industrial regulations are converging around dual mandates of safety integrity (IEC 61508/61511) and cybersecurity resilience (IEC 62443). Tools such as Siemens SIBERprotect isolate compromised assets within milliseconds while keeping safety loops intact, making certified safety PLCs and secure communication protocols indispensable. With CISA releasing 24 advisories on OT vulnerabilities in 2024, buyers now factor cyber-safety credentials into capital planning, nudging the industrial control systems market toward vendors that offer natively integrated capabilities.

Surge in Demand for Real-time Data-driven Mass-customisation

As high-mix, low-volume production becomes the norm, plants require modular cells that can swap product variants via software. Virtual commissioning using Rockwell Automation’s Emulate3D tied to NVIDIA Omniverse allows engineers to stress-test automation before hardware arrives, slashing changeover time.[2]Rockwell Automation, “Rockwell and NVIDIA Expand Digital Twin Collaboration,” rockwellautomation.com The capability to reconfigure lines overnight is emerging as a purchase trigger, driving incremental spend across the industrial control systems market.

Government Incentives for Smart-factory Retrofits

Public funding now targets specific digital stack components. Germany’s Manufacturing-X scheme channels EUR 150 million (USD 161 million) into shared data-spaces that favor open standards over proprietary ecosystems.[3]BMWK, “Funding Guideline for Manufacturing-X,” bmwk.de Similarly, the US CHIPS Manufacturing USA Institute commits USD 200 million to semiconductor digital twins. Such programs de-risk adoption and allow suppliers to frame ROI beyond traditional cost-savings narratives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled OT/ICS engineers | -1.4% | Global, with acute impact in North America and Europe | Long term (≥ 4 years) |

| High capex and long pay-back periods | -0.9% | Global, with concentrated impact on SMEs | Medium term (2-4 years) |

| Semiconductor lead-time volatility disrupting controller supply | -0.6% | Global, with severe impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Legacy-system integration complexity | -0.5% | Global, with concentrated impact on mature industrial regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled OT/ICS Engineers

Deloitte estimates 1.9 million US manufacturing roles may go unfilled by 2033, many requiring hybrid IT-OT skills. Scarcity inflates labor costs and prolongs commissioning cycles, prompting vendors to bundle managed services and low-code configuration to soften onboarding friction.

High Capex and Long Pay-back Periods

Full-stack automation retrofits often demand dual operations during cut-over, doubling equipment exposure and stretching ROI horizons. Semiconductor shortages in 2024 pushed controller lead-times past 50 weeks, elevating working capital requirements. Vendors that can stage deployments or price via consumption models gain an edge with capital-constrained buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operational Technology: Edge Intelligence Reshapes Hierarchies

SCADA platforms retained a 28.02% slice of the industrial control systems market in 2025, yet their centralized approach is being contested by edge-enabled PLCs that are posting 11.24% CAGR through 2031. The influx of micro-AI chips allows PLCs to process condition-monitoring and quality-inspection workloads locally, reducing data backhaul and network congestion. In oil & gas and chemicals, Distributed Control Systems still govern continuous processes, but customers are layering predictive algorithms over legacy DCS to extend asset life. Human-Machine Interfaces have evolved into decision-support consoles incorporating AR overlays for on-the-spot troubleshooting. Intelligent Electronic Devices are gaining traction in utilities as grid operators pursue faster fault isolation. Across these use cases, the industrial control systems market rewards suppliers that embed open APIs, enabling plant managers to mix best-of-breed components without vendor lock-in.

With SCADA still contributing USD 57.18 billion to industrial control systems market size in 2025, upgrade cycles center on container-based micro-services that keep supervisory layers intact while injecting analytics. Meanwhile, pilot programs in discrete manufacturing show edge PLC clusters trimming unplanned downtime by up to 20%, accelerating payback. Vendors able to harmonize lifecycle services for both centralized and distributed architectures are expected to capture disproportionate share.

By Software: Cybersecurity Gains Momentum beside APM Dominance

Asset Performance Management generated 23.18% of 2025 revenue as plants chase overall equipment effectiveness and schedule-free maintenance. Looking ahead, cybersecurity suites are set to outpace all other categories at 12.55% CAGR, a reaction to increased ransomware targeting OT assets. Integrated offerings that fuse vulnerability scanning, zero-trust segmentation, and safety-PLC hardening resonate with risk-averse sectors such as pharmaceuticals. Manufacturing Execution Systems now bundle quality analytics and electronic batch records, while Product Lifecycle Management tools couple with digital twins to bridge design and production. ERP vendors are exposing OT data models via REST APIs, feeding demand-driven planning algorithms. The industrial control systems market is therefore tilting toward platforms that orchestrate cross-domain data rather than discrete modules.

Industrial cyber platforms, forecast to exceed USD 15.26 billion in industrial control systems market size by 2031, are attracting venture funding and prompting established vendors to buy niche specialists. Suppliers competent in synchronizing APM, MES, and cyber layers position themselves as single-throat-to-choke partners for digital transformation roadmaps.

By Deployment Mode: Hybrid Architectures Take Center Stage

On-premise installations still generate 63.45% of segment revenue because many operators prioritize deterministic latency and IP control. However, cloud services are rising at 13.09% CAGR as firms offload data-lake management and model training to hyperscalers. Edge nodes mediate the two realms, executing sub-20 millisecond control loops locally while passing aggregated insights to the cloud. Private 5G networks amplify this design by offering predictable bandwidth, enabling mobile robots and wearable HMIs. For brownfield sites, vendors now market micro-data-centers that retrofit into existing control rooms, providing a stepping-stone to hybrid rollouts. As cybersecurity postures mature, segment leaders will monetize subscription analytics layered atop perpetual on-premise licences, driving recurring revenue within the industrial control systems market.

Cloud-hosted analytics tied to USD 30 billion of industrial control systems market size could eclipse on-premise growth by 2028 if data-residency concerns ease, highlighting the strategic importance of sovereign-cloud partnerships.

By End-user Industry: Electronics Fab Leads Automation Intensity

Oil & gas retained 25.05% revenue leadership due to continuous-process complexity and hazardous conditions that necessitate advanced control. Yet electronics and semiconductor fabs are scaling expenditure at 12.47% CAGR, motivated by nanometer-level tolerances and clean-room yields. Chemical producers remain avid adopters of model-predictive control to squeeze efficiency from thin margins, while utilities digitize substations for distributed energy integration. Automotive plants, grappling with ICE-to-EV transitions, favor modular conveyor cells programmable for mixed-model output. Life sciences manufacturers deploy closed-loop environmental controls to meet regulatory validation. Each vertical values domain templates embedded in vendor libraries, minimizing commissioning overhead. Consequently, vendors are tailoring verticalized reference architectures, a trend that will re-shape account segmentation across the industrial control systems industry.

Electronics fabs alone are on track to contribute USD 44.58 billion to industrial control systems market size by 2031, underscoring why suppliers are opening dedicated semiconductor centers of excellence in Asia and North America.

Geography Analysis

Europe steers 28.12% of 2025 revenue, driven by rigorous functional-safety statutes and sustainability mandates that reward high-efficiency automation. Funding schemes such as Manufacturing-X distribute EUR 150 million (USD 161 million) to projects that emphasize data sovereignty, giving domestic vendors an early-mover edge. Capital projects increasingly bundle carbon-footprint dashboards, aligning with the EU’s Green Deal reporting. Eastern European clusters act as near-shore capacity for Western OEMs, stimulating incremental demand for mid-tier control gear.

Asia-Pacific, advancing at 10.12% CAGR, benefits from large-scale capacity expansions in electronics, EV batteries, and renewable components. China’s demographic headwinds and wage inflation accelerate factory automation, while Southeast Asian nations leverage tax incentives to lure reshoring projects. Domestic PLC and robot suppliers are gaining share, but multinational incumbents retain dominance in high-end safety and motion solutions. Government cyber rules, notably China’s Critical Information Infrastructure law, push buyers toward products with verifiable security lineage, shaping procurement shortlists.

North America sustains momentum through reshoring initiatives and the CHIPS Act’s USD 200 million digital-twin program. Energy transition spending in the US Gulf Coast is spawning demand for open-process automation to retrofit LNG, hydrogen, and CCS facilities. Canada’s NGen USD 35 million sustainable manufacturing challenge propels SME adoption of modular control kits. Heightened cyber directives from CISA elevate procurement specifications, giving advantage to suppliers with IEC 62443 certifications. Collectively, these trends keep the industrial control systems market on a diversified regional growth footing.

Competitive Landscape

The market shows moderate concentration as the top five suppliers account for roughly 55% of revenue, yet open-standard tailwinds enable niche players to punch above their weight. Incumbents such as Siemens, ABB, Rockwell Automation, Schneider Electric, and Honeywell are pivoting from hardware moats to software ecosystems, investing heavily in AI engines and digital-thread integration. Rockwell’s tie-up with NVIDIA embeds physics-based simulation into controls design, shaving months off factory-acceptance testing. Siemens deepens alliances with DMG MORI and Renishaw to tether machine-tool digital twins to in-process metrology, driving closed-loop quality. ABB’s purchase of Siemens Gamesa’s power-electronics line expands its grid-edge footprint, complementing its forthcoming robotics IPO.

Disruptors leverage open-process automation to insert specialized modules—cyber micro-gateways, real-time middleware, or sustainability optimizers—into brownfield estates. ExxonMobil’s first-of-a-kind O-PAS deployment validates multi-vendor interoperability, prompting conservative sectors such as chemicals to re-evaluate procurement criteria. Venture funding flows to firms offering low-code OT-as-a-Service, compressing deployment cycles for SMEs. Strategic collaborations proliferate; Komatsu partners with ABB to hybridize mining equipment, while Sick and Endress+Hauser pool sensor know-how to accelerate turnkey process skids.

Competitive differentiation increasingly hinges on lifecycle services that mitigate the global OT skills deficit. Vendors extend remote diagnostics, cyber-patch orchestration, and AI model retraining as managed offerings. Those demonstrating quantified sustainability gains—energy cutbacks, waste minimization—win board-level sponsorships. As a result, the industrial control systems market is transitioning from product-centric sales toward outcome-based engagements, pressuring laggards to refresh business models.

Industrial Control Systems Industry Leaders

Siemens AG

Omron Corporation

Honeywell International Inc.

Rockwell Automation Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens unveiled Gridscale X and Xcelerator enhancements at DISTRIBUTECH to position its stack as an end-to-end grid-automation backbone. The strategy aligns its OT suite with utilities’ push for predictive asset health while locking in cloud subscriptions for analytics.

- March 2025: Rockwell Automation launched Emulate3D Factory Test on NVIDIA Omniverse, letting customers perform virtual FAT. By virtualizing acceptance, Rockwell lowers commissioning risk, aiming to shorten sales cycles in capital-intensive verticals.

- February 2025: ExxonMobil rolled out the world’s first commercial Open Process Automation installation in Baton Rouge, citing ≥20% lifecycle cost savings. The move pressures suppliers to certify O-PAS components or risk exclusion from future brownfield bids.

- December 2024: ABB acquired Siemens Gamesa’s power-electronics business to deepen renewables integration and bulk up its portfolio before carving out the robotics unit. The add-on bolsters ABB’s cross-selling leverage in energy-transition projects.

Global Industrial Control Systems Market Report Scope

Industrial control systems comprise various automation equipment, machines, and components. These systems are developed to monitor, control, perform multiple industrial tasks and automate processes with high precision, improving product quality and reliability. Organizations are adopting industrial control systems from various industries due to the increasing focus on attaining energy efficiency in manufacturing processes.

The ICS market is segmented by operational technology (Supervisory Control and Data Acquisition (SCADA), Distributed Control System (DCS), Programmable Logic Controller (PLC), Intelligent Electronic Devices (IED), Human Machine Interface (HMI), and other systems), by software (Asset Performance Management (APM), Product Lifecycle Management (PLM), Manufacturing Execution System (MES), Enterprise Resource Planning (ERP)), by end-user industry (oil and gas, chemical and petrochemical, power and utilities, food and beverages, automotive and transportation, life sciences, water and wastewater, metal and mining, pulp and paper, electronics/semiconductor, other end-user industries), and by North America (United States, Canada), Europe (Germany, United Kingdom, France, and the rest of Europe), Asia Pacific (China, India, Japan, and the rest of Asia Pacific), Latin America (Brazil, Argentina, Mexico, and the rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and the rest of Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Operational Technology

| Supervisory Control and Data Acquisition (SCADA) |

| Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) |

| Intelligent Electronic Devices (IED) |

| Human-Machine Interface (HMI) |

| Other Systems |

By Software

| Asset Performance Management (APM) |

| Product Lifecycle Management (PLM) |

| Manufacturing Execution System (MES) |

| Enterprise Resource Planning (ERP) |

| Industrial Cyber-security Platforms |

| Other Software |

By Deployment Mode

| On-premise |

| Cloud-based |

| Edge / Hybrid |

By End-user Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Power and Utilities |

| Food and Beverages |

| Automotive and Transportation |

| Life Sciences |

| Water and Wastewater |

| Metal and Mining |

| Pulp and Paper |

| Electronics and Semiconductor |

| Other End-user Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Operational Technology | Supervisory Control and Data Acquisition (SCADA) | |

| Distributed Control System (DCS) | ||

| Programmable Logic Controller (PLC) | ||

| Intelligent Electronic Devices (IED) | ||

| Human-Machine Interface (HMI) | ||

| Other Systems | ||

| By Software | Asset Performance Management (APM) | |

| Product Lifecycle Management (PLM) | ||

| Manufacturing Execution System (MES) | ||

| Enterprise Resource Planning (ERP) | ||

| Industrial Cyber-security Platforms | ||

| Other Software | ||

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| Edge / Hybrid | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power and Utilities | ||

| Food and Beverages | ||

| Automotive and Transportation | ||

| Life Sciences | ||

| Water and Wastewater | ||

| Metal and Mining | ||

| Pulp and Paper | ||

| Electronics and Semiconductor | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the industrial control systems market?

The market was valued at USD 220.93 billion in 2026 and is forecast to reach USD 328.79 billion by 2031.

Which operational technology segment is expanding fastest?

Edge-enabled PLCs lead growth at 11.24% CAGR through 2031.

Why is cybersecurity spending rising in industrial automation?

Increased OT-focused ransomware and dual safety-cyber compliance requirements push cybersecurity platforms to 12.55% CAGR.

Which region shows the strongest growth outlook?

Asia-Pacific posts the highest regional CAGR at 10.12% due to electronics capacity build-out and labor-scarcity automation.

How are open-process automation standards affecting vendors?

O-PAS adoption allows end-users to mix components from multiple suppliers, pressuring incumbents to certify open interfaces or risk share erosion.

What is the biggest barrier to wider automation adoption?

A persistent shortage of OT-skilled engineers is subtracting an estimated 1.4 percentage points from forecast CAGR.

Page last updated on: