Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

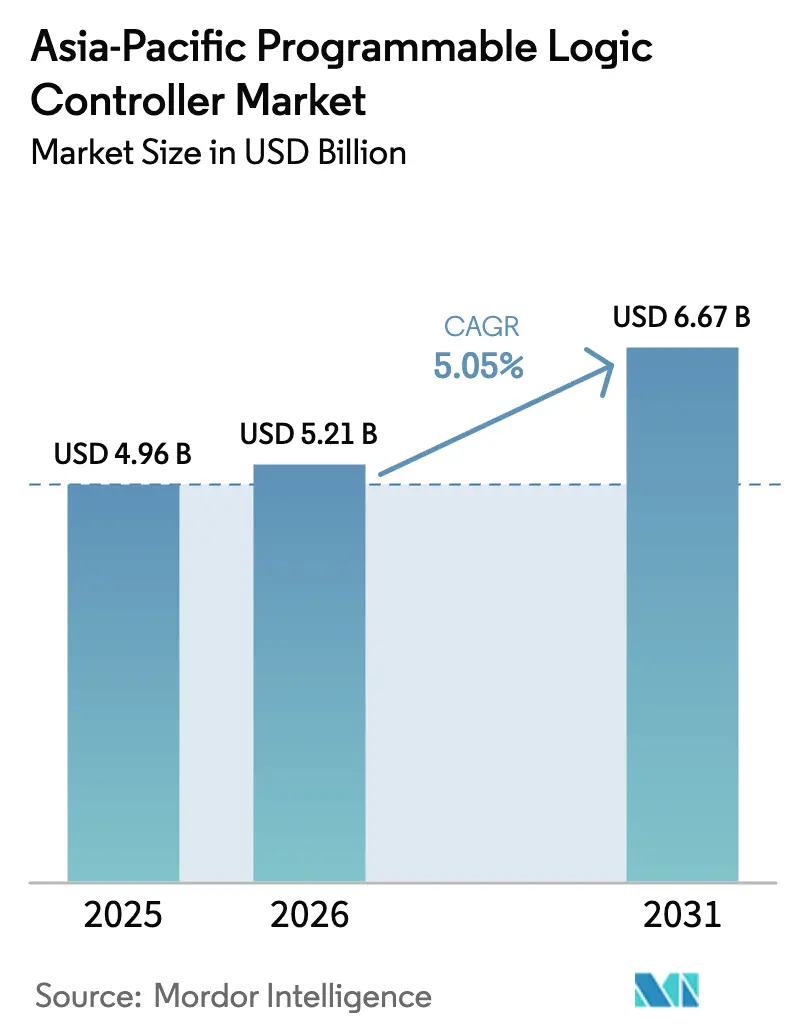

| Base Year Market Size (2025) | USD 4.96 Billion |

| Market Size (2026) | USD 5.21 Billion |

| Market Size (2031) | USD 6.67 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Programmable Logic Controller Market Analysis by Mordor Intelligence

The Asia-Pacific programmable logic controller market size is expected to grow from USD 4.96 billion in 2025 to USD 5.21 billion in 2026 and is forecast to reach USD 6.67 billion by 2031 at 5.05% CAGR over 2026-2031. Industrial digitalization programs, sovereign manufacturing policies, and the shift to cyber-physical production lines fuel this momentum. China’s 43.31% share anchors regional demand, while India’s 7.5% CAGR underscores an emerging diversification of production capacity. Hardware and software components account for 75.7% of the revenue in 2024, while the services segment’s 6.2% CAGR signals a transition toward value-added integration and lifecycle support. Modular controllers remain the preferred form factor, but soft PLC platforms are gaining ground as virtualization and edge computing mature. The automotive sector leads with 28.6% share, whereas water and wastewater treatment registers the fastest adoption, supported by smart-city infrastructure outlays. Semiconductor supply constraints, 5G-enabled time-sensitive networking, and escalating cybersecurity requirements continue to reshape price structures, performance benchmarks, and total cost of ownership calculations.[1]Reuters Staff, “China EV Production Automation Standards,” Reuters, reuters.com

Key Report Takeaways

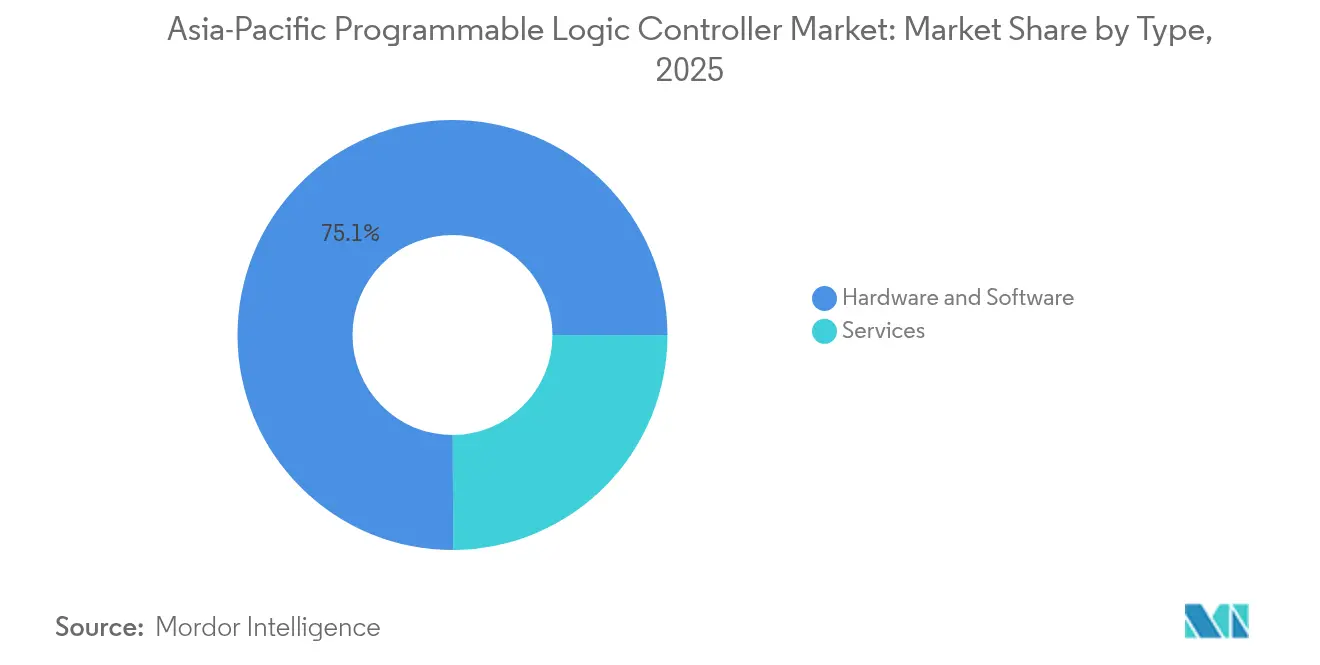

- By type, hardware and software accounted for 75.05% of the Asia-Pacific programmable logic controller market share in 2025, while services are projected to expand at a 6.05% CAGR through 2031.

- By architecture, modular PLCs led the Asia-Pacific programmable logic controller market with a 55.10% revenue share in 2025; soft PLC platforms are projected to post a 6.68% CAGR through 2031.

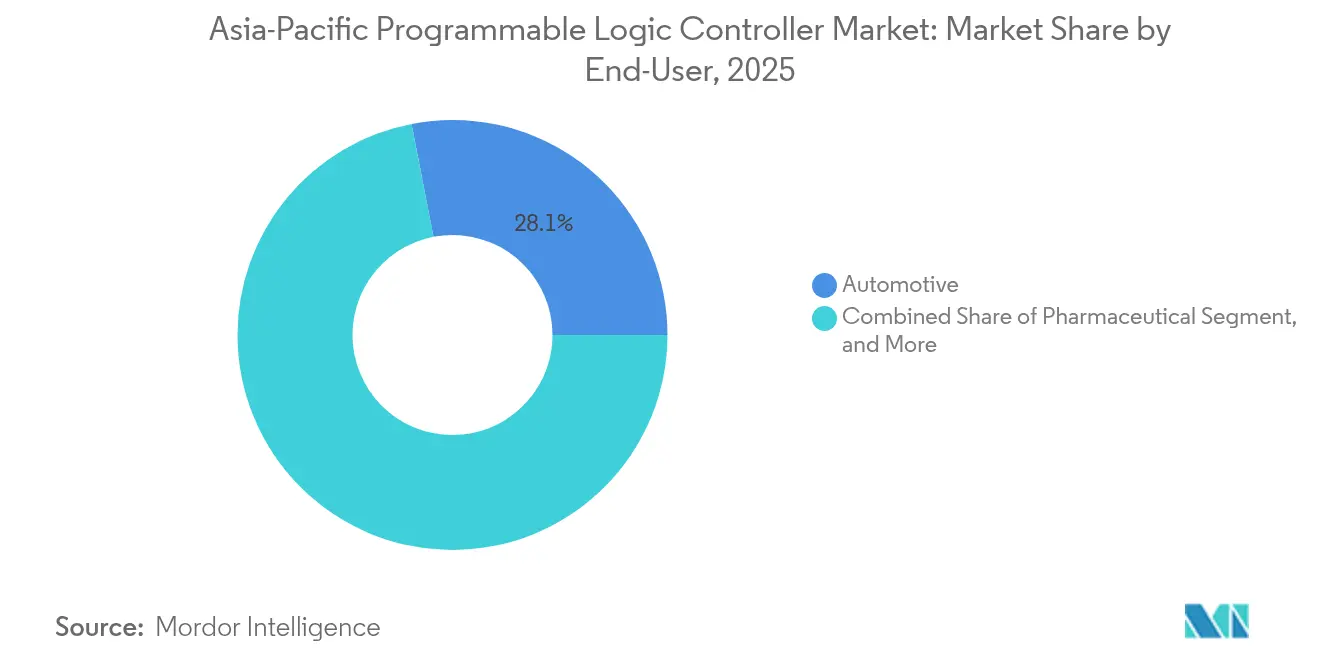

- By end-user, the automotive sector held 28.05% of the Asia-Pacific programmable logic controller market size in 2025, whereas the water and wastewater treatment sector is projected to track an 7.75% CAGR to 2031.

- By input/output type, digital I/O commanded 65.12% share of the Asia-Pacific programmable logic controller market in 2025, while mixed I/O configurations are advancing at a 6.63% CAGR through 2031.

- By geography, China dominated the Asia-Pacific programmable logic controller market with a 42.95% share in 2025, and India is forecast to deliver the fastest growth of 7.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Programmable Logic Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in automotive e-mobility production lines | +1.2% | China, Japan, South Korea, with expansion to India and Southeast Asia | Medium term (2-4 years) |

| Government-led smart-manufacturing subsidies | +0.9% | China, Japan, South Korea, India, with selective programs in Southeast Asia | Long term (≥4 years) |

| Rapid expansion of low-cost modular PLCs | +0.7% | Global, with strongest impact in India, Southeast Asia, and China's tier-2 cities | Short term (≤2 years) |

| Migration to Industry 4.0 cyber-secure PLC platforms | +0.8% | Japan, South Korea, Singapore, with gradual adoption across Asia Pacific | Medium term (2-4 years) |

| Demand for energy-efficient utility automation | +0.6% | China, India, Southeast Asia, driven by renewable energy integration | Long term (≥4 years) |

| Emerging 5G-enabled time-sensitive networking (TSN) | +0.5% | South Korea, Japan, China, with pilot deployments in Singapore and Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in Automotive E-mobility Production Lines

Electric-vehicle assembly requires precise temperature management of the battery pack, coordination of multi-axis motor windings, and certified functional safety controls. China’s OEMs have established reference automation templates that neighboring markets are now replicating, compelling PLC vendors to incorporate higher-speed processing and expanded communication stacks. ISO 26262 mandates further raising technical entry barriers as e-mobility expands beyond China. Localized line-builders in India and Southeast Asia source modular PLCs to shorten deployment times. Vendor differentiation is therefore shifting from hardware density to integrated motion libraries and EV-specific diagnostics. Continuous product updates, aligning with evolving battery chemistries, sustain long-term demand for controllers.

Government-led Smart Manufacturing Subsidies

Strategic programs such as China’s “Made in China 2025,” Japan’s Society 5.0, and South Korea’s K-Digital New Deal inject funding that accelerates automation procurement.[2]Ministry of Economy, Trade and Industry, “Connected Industries Initiative,” METI, meti.go.jp Subsidy-linked deadlines compress project timelines, benefiting suppliers with turnkey service capabilities. Tax credits and low-interest loans lower payback thresholds, drawing small and medium manufacturers into the Asia-Pacific programmable logic controller market. However, pull-forward demand risks post-incentive slowdowns. India’s Production Linked Incentive scheme fosters domestic assembly, potentially altering import patterns. Clustering of subsidized plants also enhances ecosystem knowledge transfer, reinforcing regional growth momentum.

Rapid Expansion of Low-cost Modular PLCs

Cost-competitive Chinese brands now meet baseline performance and IEC 61131-3 compliance, forcing incumbents to emphasize software value and life-cycle services.[3]Delta Electronics, “Delta Expands PLC Portfolio with Cost-Effective Solutions,” Delta, deltaww.com Modular designs enable phased investment, aligning with cash flow constraints in emerging markets. Local component sourcing in India and Vietnam helps mitigate supply risks and reduce landed costs. International vendors counter by bundling analytics, cloud gateways, and extended warranties. Commodity pricing on entry-level modules compresses margins, accelerating a pivot toward subscription-based service revenues. The trend is particularly beneficial for the Asia-Pacific programmable logic controller market, where SME automation remains under-penetrated.

Migration to Industry 4.0 Cyber-secure PLC Platforms

As OT and IT networks converge, threats migrate from enterprise domains into plant-floor controllers. IEC 62443 certification and secure-by-design architectures become mandatory procurement criteria in government and utility projects. Vendors integrate encrypted protocols, secure boot processes, and hardware root of trust, adding performance overhead that drives processor upgrades. Edge computing deployments localize data processing, limiting exposure and latency while enabling predictive analytics capabilities. Insurance carriers are increasingly discounting policies only for plants that deploy certified platforms, thereby reinforcing adoption. The Asia-Pacific programmable logic controller market, therefore, shifts toward platforms combining real-time control with embedded security functions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront integration and training costs | -0.8% | Global, with acute impact in India, Southeast Asia, and China's SME sector | Short term (≤2 years) |

| Prolonged semiconductor supply constraints | -1.1% | Global, with severe impact in Japan, South Korea, and China's electronics hubs | Medium term (2-4 years) |

| Availability of low-code soft-PLC substitutes | -0.4% | Japan, South Korea, Singapore, with gradual expansion to other markets | Long term (≥4 years) |

| Rising cyber-security compliance expenditures | -0.6% | China, Japan, South Korea, with increasing relevance in India and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration and Training Costs

Total project outlays can triple the hardware price due to system design, wiring, commissioning, and operator upskilling. SMEs in India and Southeast Asia struggle to secure financing, which delays automation despite its attractive paybacks. Shortages of qualified integrators inflate labor costs and extend timelines. Legacy equipment interfacing often requires custom gateways, which raises implementation risk. Manufacturers wary of prolonged shutdowns opt for partial or no automation, tempering near-term demand for programmable logic controllers in the Asia-Pacific market. Vendors respond with pre-engineered templates and remote training modules to compress learning curves.

Prolonged Semiconductor Supply Constraints

Industrial-grade processors remain in tight supply, extending PLC lead times beyond six months in some product lines. Automotive-safety controllers are especially affected because they require higher temperature ratings and longer lifecycle guarantees. Redesigns around available chips often result in certification delays and cost overruns. Inventory buffering ties up working capital, particularly for distributors serving fragmented customer bases. Although capacity additions are planned, shortages are likely to persist into the medium term, exerting a negative drag on the Asia-Pacific programmable logic controller market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Segment Drives Value-added Growth

Services generated the highest incremental revenue, expanding at a 6.05% CAGR, as manufacturers prioritize integration expertise, predictive maintenance, and lifecycle optimization over standalone hardware. Hardware and software components continued to dominate the Asia-Pacific programmable logic controller market share, accounting for 75.05% in 2025, reflecting ongoing capacity expansions in China and India. Services revenue benefits from multi-year contracts, delivering steadier cash flows than cyclical hardware sales. Remote monitoring and cloud-based analytics underpin this shift, reducing unplanned downtime and justifying premium service fees.

System integrators leverage domain know-how to bridge legacy equipment with modern controllers, compressing deployment timelines. Over-the-air firmware updates and flexible licensing enhance scalability, mitigating capital-expenditure hurdles. Large installations in petrochemical plants still rely on high-end hardware, but nano- and microcontrollers with SaaS packages are gaining traction in dispersed IoT nodes. Consequently, vendors reorient portfolios toward outcome-based models, expanding the Asia-Pacific programmable logic controller market’s recurring-revenue proportion.

By Architecture: Soft PLC Platforms Challenge Traditional Boundaries

Modular PLCs retained 55.10% revenue leadership in 2025, favored for their expandability in complex lines. Nonetheless, soft PLC platforms posted a 6.68% CAGR, eroding incumbents’ share as virtualization delivers deterministic performance on industrial PCs. Early adopters in automotive battery lines deploy containerized control applications to enable rapid recipe changes and centralized version management. Rack-mount configurations address dense I/O needs in process industries, whereas compact units cater to skid-mounted equipment and OEM machinery.

Edge gateways integrate programmable logic, data aggregation, and AI inference on a single board, thereby blurring the boundaries between different functions. Vendors differentiate through real-time hypervisors, secure boot sequences, and compatibility with IT orchestration tools. As a result, buyers evaluate total system architecture rather than discrete controller models, reshaping procurement criteria within the Asia-Pacific programmable logic controller market. Continued maturation of the soft platform will likely compress hardware refresh cycles, encouraging subscription-based upgrades.

By End-User: Water Treatment Automation Accelerates Infrastructure Modernization

The Asia-Pacific programmable logic controller (PLC) market size for water and wastewater applications is projected to grow at an 7.75% CAGR through 2031, driven by urbanization, environmental mandates, and smart-city funding. Municipal utilities deploy PLC-linked SCADA systems to optimize chemical dosing and pump scheduling, thereby reducing energy use and leakage. In China, stimulus packages allocate funds to upgrade legacy plants, while India channels smart-city grants into sewage-treatment automation. The automotive sector, which held a 28.05% share in 2025, continues adding lines for electric powertrains, sustaining baseline demand for safety-certified controllers.

Chemical, petrochemical, and energy utilities maintain steady replacement cycles to ensure safety and reliability standards are upheld. Meanwhile, food and beverage firms automate to ensure traceability, and pharmaceutical players invest in validated PLCs that meet electronic-record regulations. Mining, pulp and paper, and electronics plants contribute diversified needs, ensuring balanced end-market exposure for suppliers. This broad uptake underpins the resilience of the Asia-Pacific programmable logic controller market across economic cycles.

By Input/Output Type: Mixed I/O Configurations Enable Flexible Manufacturing

Digital I/O represented 65.12% of 2025 revenue, serving binary control in discrete manufacturing. Nevertheless, mixed configurations are projected to capture a rising share, advancing at a 6.63% CAGR as factories seek plug-and-play flexibility. Mixed modules combine digital, analog, and specialty channels on a single slice, reducing panel real estate and wiring labor. IO-Link-enabled smart sensors feed diagnostic data directly to controllers, supporting predictive maintenance initiatives.

Ethernet-based I/O backbones replace legacy fieldbus, offering higher bandwidth and standardized cabling that IT departments can service. Wireless I/O, recently launched by leading vendors, further expands deployment options for mobile equipment and retrofit scenarios. Enhanced diagnostics shrink mean-time-to-repair, offsetting higher module costs. Consequently, the Asia-Pacific programmable logic controller market increasingly values intelligent I/O ecosystems as much as central processing prowess.

Geography Analysis

China’s 42.95% share reflects its broad manufacturing base, encompassing everything from smartphones to shipbuilding. Continued smart-factory subsidies and 5G campus networks spur accelerated controller upgrades, with local vendors closing feature gaps against global incumbents. Environmental regulations drive rapid water-treatment automation, while electric-vehicle giants embed advanced PLCs in gigafactories.

India delivers the fastest 7.18% CAGR, driven by Production-Linked Incentive-backed capacity additions across the automotive, electronics, and renewable energy supply chains. Domestic assembly of basic PLCs is emerging, but high-end models continue to be imported, resulting in hybrid supply patterns. Infrastructure programs, including smart cities and dedicated freight corridors, stimulate demand for utility and transport automation systems.

Japan and South Korea exhibit steady replacement demand anchored in productivity gains and workforce augmentation amid aging demographics. Both nations pioneer 5G TSN pilots and AI-embedded controllers. Southeast Asia benefits from manufacturing relocation, with Vietnam and Thailand hosting electronics and automotive clusters that require scalable PLC architectures. Australia and New Zealand focus on mining and food-processing automation, which rounds out regional variety and broadens the Asia-Pacific programmable logic controller market opportunity set.

Competitive Landscape

European majors ABB, Siemens, and Schneider Electric maintain technological leadership, particularly in safety-critical and cybersecurity-certified segments, yet face increasing price pressure from Japanese peers and Chinese competitors. Chinese manufacturers leverage cost efficiencies and local support networks to win entry-level projects, while incumbents defend share via integrated software suites and cloud analytics services.[4]ABB Group, “ABB Launches New PLC Platform for Industrial Automation,” ABB, abb.com The playing field shifts from processor speed to platform ecosystems that encompass edge analytics, machine-learning libraries, and secure connectivity.

Recent investments illustrate strategic realignment: Siemens’ USD 200 million expansion in Singapore creates a regional Industry 4.0 hub, Mitsubishi Electric’s new Vietnam plant diversifies supply chains, and Rockwell’s acquisition of Beijing Wellintech deepens local software capabilities. Vendors increasingly partner with system integrators and IT firms to amplify solution coverage, as evidenced by Schneider Electric’s collaboration with Tata Consultancy Services.

Innovation now centers on AI-infused controllers, deterministic wireless networking, and zero-trust security stacks. Patent filings indicate a shift toward software and protocol intellectual property, rather than hardware designs. Competitive intensity thus transcends traditional automation boundaries, positioning the Asia-Pacific programmable logic controller market as a proving ground for converged OT-IT solutions.

Asia-Pacific Programmable Logic Controller Industry Leaders

ABB Ltd.

Mitsubishi Electric Corporation

Schneider Electric SE

Rockwell Automation Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ABB launched its AC500-eCo PLC platform, featuring embedded cybersecurity modules and 5G connectivity, targeting mid-tier smart factory applications.

- September 2025: Siemens committed USD 200 million to expand its Singapore digital-factory campus and boost SIMATIC PLC production.

- August 2025: Schneider Electric partnered with Tata Consultancy Services to co-create India-focused automation solutions on the EcoStruxure platform.

- July 2025: Mitsubishi Electric has opened a USD 150 million PLC facility in Vietnam to serve the demand of Southeast Asia.

- June 2025: Rockwell Automation acquired Beijing Wellintech for USD 180 million, strengthening Chinese software ties.

- May 2025: Omron introduced NX7 PLCs with integrated AI processors for real-time machine-learning on the shop floor.

Asia-Pacific Programmable Logic Controller Market Report Scope

PLC is the primary computing system that controls automated machines. The system also helps detect any errors or flaws and alerts the technician. PLC systems are also preferred over traditional systems, like relays and switch boxes, due to their compact sizes. Another advantage of PLCs is their multi-functionality (owing to their programmable nature that can be used for multiple operations depending on the application). The PLC consists of hardware, software, and services. The basic architecture of the PLC consists of main components: the processor module, the power supply, and the I/O modules.

The Asia-Pacific Programmable Logic Controller Market is Segmented by Type (Hardware and Software, Services), End-User (Food, Tobacco, and Beverage, Automotive, Chemical and Petrochemical, Energy and Utilities, pulp and paper, oil and gas, Water and Wastewater Treatment, Pharmaceutical), and country. The segmentation comprises an in-depth coverage of the revenue generated from the sale of Programmable Logic Controllers in the Asia Pacific region, along with the unit shipments.

By Type

| Hardware and Software | Large PLC |

| Nano PLC | |

| Small PLC | |

| Medium PLC | |

| Software | |

| Other Types | |

| Services |

By Architecture

| Compact PLC |

| Modular PLC |

| Rack-mount PLC |

| Soft PLC (PC-based) |

By End-User

| Automotive |

| Food, Tobacco and Beverage |

| Chemical and Petrochemical |

| Energy and Utilities |

| Oil and Gas |

| Water and Wastewater Treatment |

| Pharmaceutical |

| Pulp and Paper |

| Other End-Users |

By Input / Output Type

| Digital I/O |

| Analog I/O |

| Mixed I/O |

By Country

| China |

| Japan |

| India |

| South Korea |

| South-East Asia |

| Rest of Asia Pacific |

| By Type | Hardware and Software | Large PLC |

| Nano PLC | ||

| Small PLC | ||

| Medium PLC | ||

| Software | ||

| Other Types | ||

| Services | ||

| By Architecture | Compact PLC | |

| Modular PLC | ||

| Rack-mount PLC | ||

| Soft PLC (PC-based) | ||

| By End-User | Automotive | |

| Food, Tobacco and Beverage | ||

| Chemical and Petrochemical | ||

| Energy and Utilities | ||

| Oil and Gas | ||

| Water and Wastewater Treatment | ||

| Pharmaceutical | ||

| Pulp and Paper | ||

| Other End-Users | ||

| By Input / Output Type | Digital I/O | |

| Analog I/O | ||

| Mixed I/O | ||

| By Country | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific programmable logic controller market?

The market is valued at USD 5.21 billion in 2026 and is projected to reach USD 6.67 billion by 2031.

Which country leads demand for programmable logic controllers in Asia-Pacific?

China dominates with 42.95% share, driven by large-scale manufacturing across multiple sectors.

Which end-user segment is expanding fastest?

Water and wastewater treatment shows the highest growth, advancing at an 7.75% CAGR through 2031.

How are semiconductor shortages affecting controller supply?

Limited availability of industrial-grade processors extends PLC lead times and raises costs, exerting a -1.1% drag on forecast CAGR.

Why are services growing faster than hardware in this market?

Manufacturers increasingly value integration, remote monitoring, and predictive maintenance, pushing services toward a 6.05% CAGR.

What technology trend is most disruptive to traditional PLC architectures?

Soft PLC platforms running on virtualized edge hardware are challenging dedicated controllers by offering flexible deployment and centralized updates.

Page last updated on: