Multi Cloud Security Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

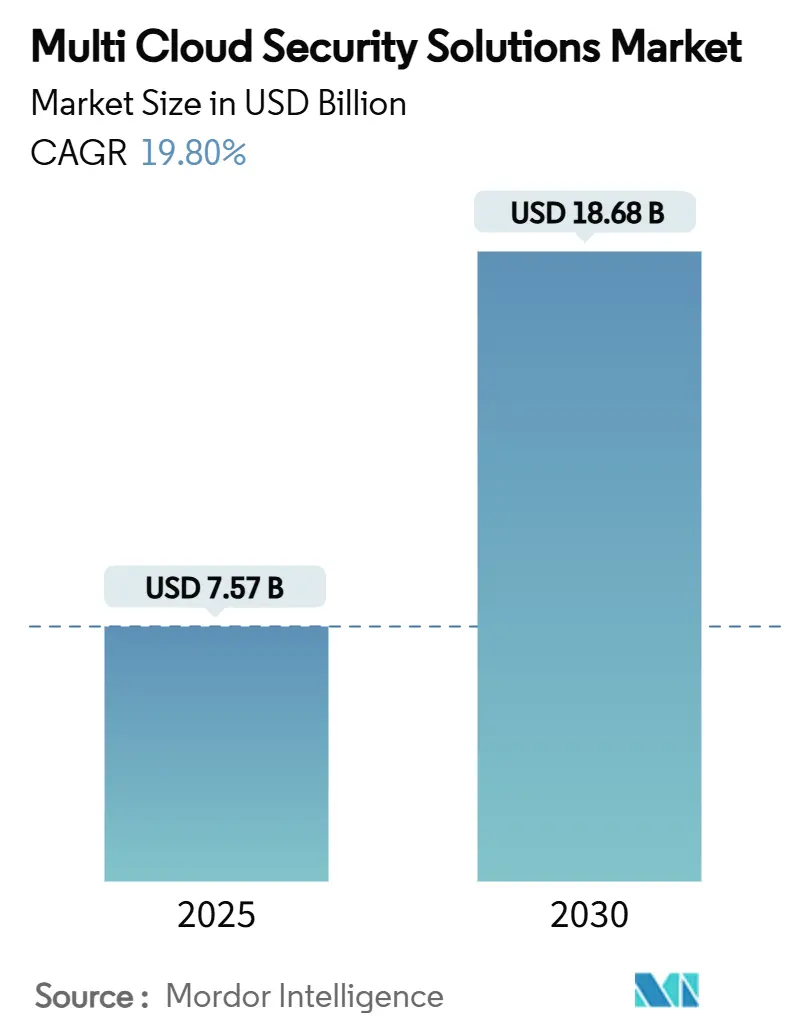

| Market Size (2025) | USD 7.57 Billion |

| Market Size (2030) | USD 18.68 Billion |

| Growth Rate (2025 - 2030) | 19.80% CAGR |

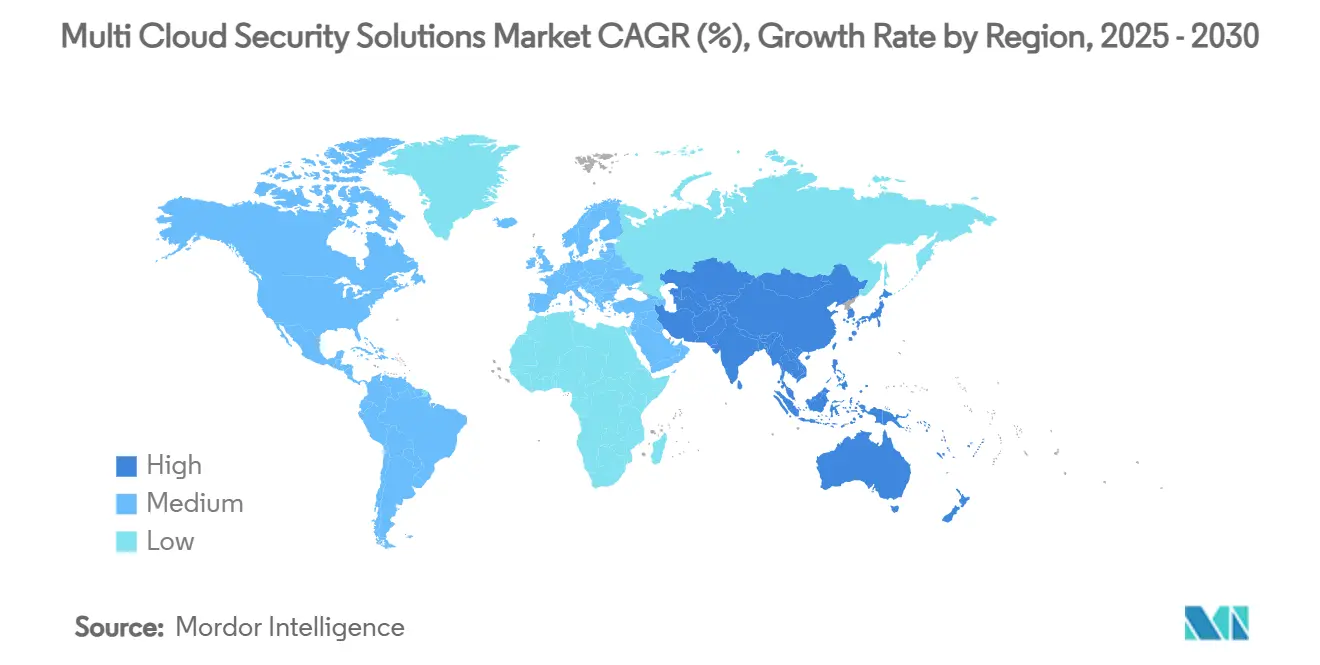

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi Cloud Security Solutions Market Analysis by Mordor Intelligence

The Multi Cloud Security Solutions Market size is estimated at USD 7.57 billion in 2025, and is expected to reach USD 18.68 billion by 2030, at a CAGR of 19.80% during the forecast period (2025-2030). Heightened cloud-native threats, widening regulatory scrutiny, and enterprises’ desire to curb vendor lock-in are amplifying demand for unified security platforms that work consistently across Amazon Web Services, Microsoft Azure, Google Cloud Platform, and private cloud estates. Investment momentum is particularly strong in Asia-Pacific as governments introduce data-sovereignty laws and companies accelerate digital-transformation programs. Software retains dominance because platforms form the technological backbone of cloud protection, yet managed security services are expanding faster as firms seek external expertise to offset the global cybersecurity skills shortfall. Consolidation among vendors is intensifying, with hyperscale providers acquiring specialized security firms to deliver end-to-end offerings that reduce tool sprawl and simplify operations.

Key Report Takeaways

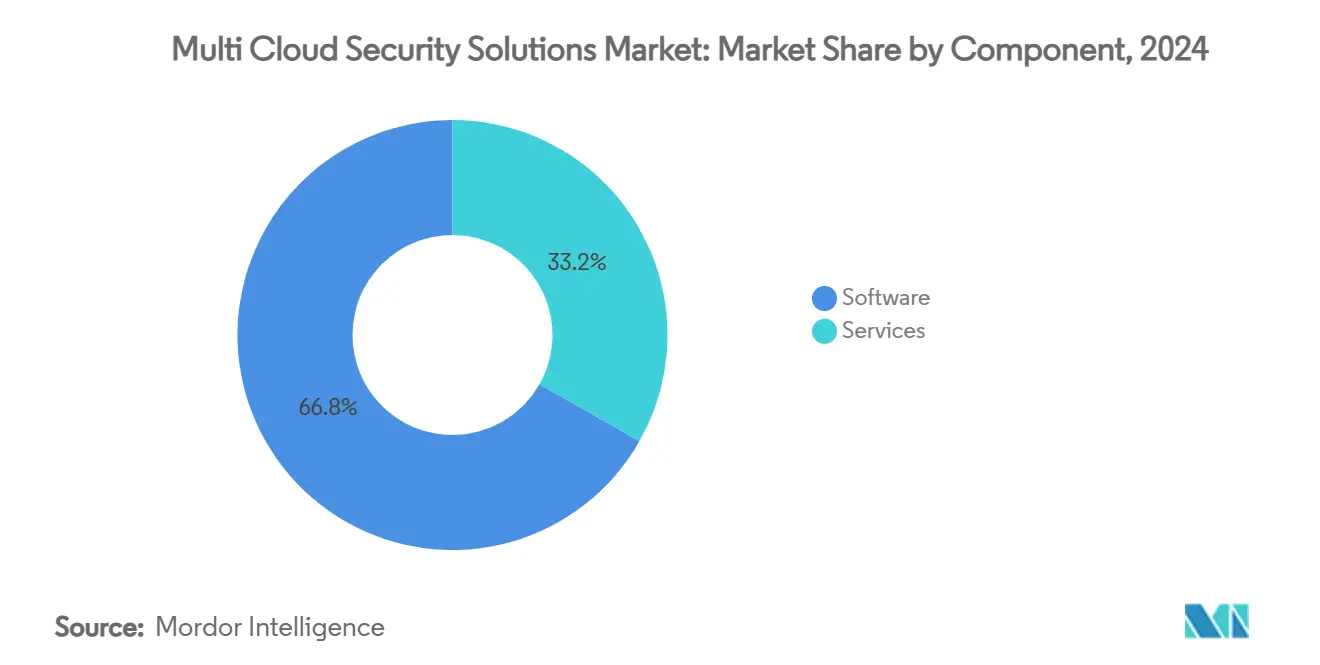

- By component, software held a 66.8% revenue share in 2024, while services are advancing at a 24.3% CAGR through 2030.

- By security type, Cloud Workload Protection Platforms captured 25.7% of the multi cloud security solutions market share in 2024, whereas Cloud Infrastructure Entitlement Management is forecast to expand at a 22.6% CAGR to 2030.

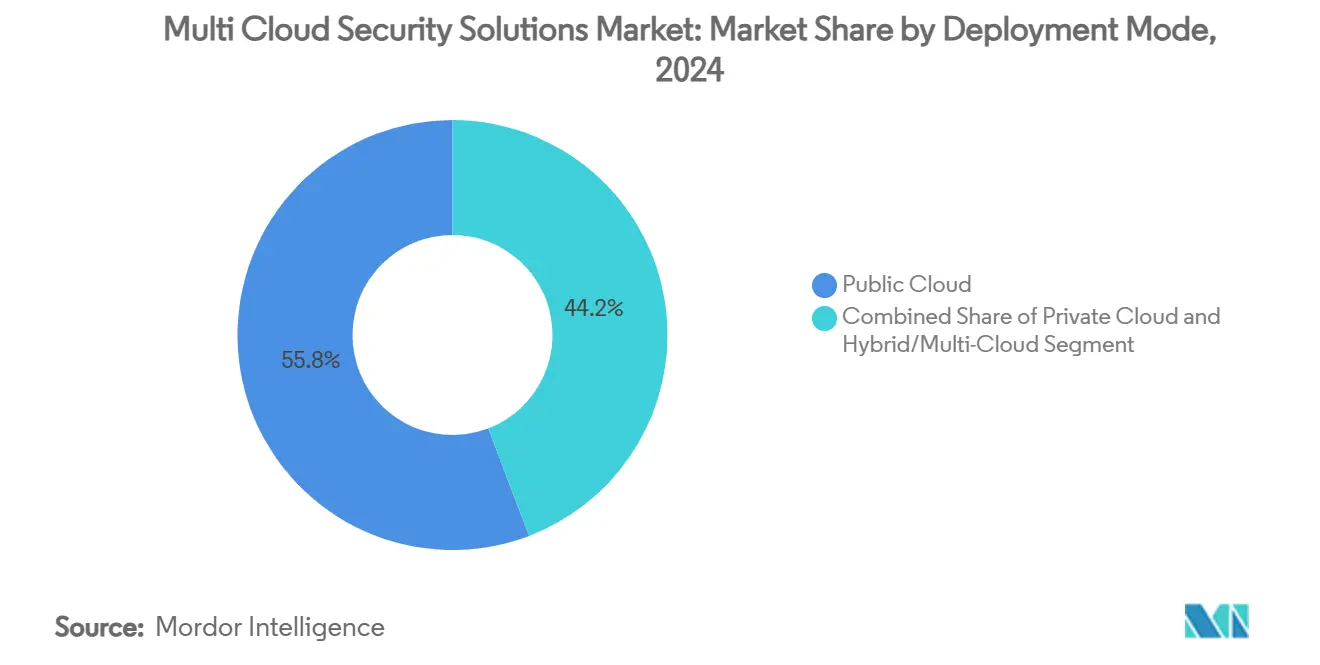

- By deployment mode, public cloud led with 55.8% share in 2024; hybrid/multi-cloud architectures are expected to grow at a 23.5% CAGR over the same period.

- By organization size, large enterprises commanded a 67.8% share of the multi cloud security solutions market size in 2024, yet small and medium enterprises are tracking a 24.1% CAGR.

- By industry vertical, BFSI contributed 28.3% revenue share in 2024, while healthcare and life sciences are growing at a 22.4% CAGR into 2030.

- By geography, North America accounted for a 38.1% share of the overall market in 2024, whereas Asia-Pacific is projected to register the fastest expansion at a 22.9% CAGR through 2030.

Global Multi Cloud Security Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in multi cloud adoption to avoid vendor lock-in | +4.2% | Global | Medium term (2-4 years) |

| Escalating cloud-native cyber threats and compliance mandates | +5.1% | Global, with early gains in North America, Europe | Short term (≤ 2 years) |

| Growing uptake of zero-trust and secure-access frameworks | +3.8% | North America and the EU, spill-over to APAC | Medium term (2-4 years) |

| Cloud-agnostic "policy-as-code" frameworks gaining traction | +2.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Expansion of confidential-computing enclaves in hyperscale DCs | +2.1% | Global, concentrated in hyperscale regions | Long term (≥ 4 years) |

| Demand for post-quantum crypto pilots across multi-cloud estates | +1.9% | North America and the EU, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Multi Cloud Adoption to Avoid Vendor Lock-In

Enterprises increasingly distribute workloads across multiple cloud providers to hedge supply-side risks and negotiate favorable pricing. Nearly 78% of global organizations now run hybrid and multi-cloud estates, driving demand for security tools that offer uniform policy enforcement regardless of underlying infrastructure. [1]Wiz, “Datavant Centralizes Cloud Security Across Six Companies,” wiz.io Firms such as Datavant consolidated seven stand-alone products into one platform, reducing vulnerabilities by 51% while managing six distinct cloud environments. The resulting need for a single pane of glass has fast-tracked the adoption of Cloud-Native Application Protection Platforms that abstract security controls away from provider-specific tooling. This driver produces a 4.2% positive lift on the market CAGR.

Escalating Cloud-Native Cyber Threats and Compliance Mandates

Sixty-one percent of enterprises faced at least one cloud security incident in 2024, and ransomware operators increasingly weaponize misconfigurations across disparate cloud accounts. [2]Fortinet, “Key Findings from the 2024 Cloud Security Report,” fortinet.com Incidents such as the 2023 attack on the Industrial and Commercial Bank of China illustrate systemic risks to global finance when multi-cloud defenses falter. Simultaneously, regulations such as the EU Digital Operational Resilience Act tighten control requirements. As a result, enterprises invest in automated threat detection and compliance monitoring that work across AWS, Azure, and Google Cloud, boosting market expansion by an estimated 5.1%.

Growing Uptake of Zero-Trust and Secure-Access Frameworks

The United States Department of Defense requires full zero-trust adoption by 2027, setting a global precedent for identity-centric architectures. Organizations deploying Microsoft’s Zero Trust portfolio have recorded a 92% return on investment by lowering breach frequency and decommissioning legacy tools. Implementation within multi-cloud settings demands orchestration layers capable of bridging disparate identity stores, propelling the driver’s 3.8% influence on forecast growth.

Cloud-Agnostic “Policy as Code” Frameworks

Infrastructure-as-code concepts are evolving into policy-as-code, allowing security rules to be version-controlled and automatically enforced across divergent cloud services. HashiCorp highlights that policy-as-code reduces configuration drift and speeds compliance audits in Asia-Pacific markets, where sovereign-cloud regulations differ country-to-country. This trend is adding 2.9% to the projected CAGR over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute global cloud-security skills shortage | -3.2% | Global, particularly acute in APAC and emerging markets | Short term (≤ 2 years) |

| High cost and complexity of toolchain integration across clouds | -2.8% | Global, with higher impact in cost-sensitive SME segments | Medium term (2-4 years) |

| Convergence of native cloud-provider security stacks | -1.9% | Global, concentrated in hyperscaler-dominated regions | Medium term (2-4 years) |

| Sovereign-cloud and residency mandates curbing multi-cloud roll-outs | -1.5% | Europe, APAC regulatory jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Global Cloud-Security Skills Shortage

Roughly 4 million cybersecurity roles remained unfilled in 2024, and 92% of enterprises reported skill gaps in cloud security specializations. Skills scarcity particularly hampers small and mid-market firms, forcing them to outsource operations to managed security providers and trimming 3.2% from potential CAGR.

High Cost and Complexity of Toolchain Integration

Organizations run more than 30 security tools on average and must juggle inconsistent APIs when workloads span several clouds. Prisma Cloud users documented 90% faster compliance reporting and 60% quicker vulnerability remediation after platform consolidation, highlighting the economic pressure created by tool sprawl. This complexity drags growth by 2.8%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge on Outsourcing Wave

Software accounted for 66.8% of the multi-cloud security solutions market revenue in 2024, reflecting the central role of platforms that deliver threat detection, posture management, and policy orchestration. Services are on track to climb at a 24.3% CAGR because enterprises lack in-house skills to operate complex environments. Managed detection and response, architecture consulting, and 24×7 incident handling are bundled into outcome-based contracts that resonate with resource-constrained IT teams. The services boom is widening access to enterprise-grade protection for small and medium organizations, lowering entry barriers and propelling overall demand.

Adoption of consumption-based pricing is another catalyst. Providers now align fees with protected assets rather than static seats, ensuring cost transparency. As a result, service vendors are embedding AI-driven automation to maintain margins while scaling support. These developments underscore why services are expected to command a larger share of incremental spend over the next five years.

By Security Type: Identity Takes Center Stage

Cloud Workload Protection Platforms controlled 25.7% of 2024 spend, safeguarding containers, virtual machines, and serverless functions across heterogeneous environments. However, Cloud Infrastructure Entitlement Management is projected to post a 22.6% CAGR as firms tackle excessive privileges granted to both human and machine identities. The rapid growth positions CIEM for a meaningful slice of the multi-cloud security solutions market size by 2030, especially as zero-trust projects hinge on least-privilege access principles.

Vendors are fusing CIEM with posture-management and data-loss-prevention modules to create unified suites. CyberArk’s collaboration with Wiz to protect cloud-created identities illustrates this convergence. [3]CyberArk, “CyberArk and Wiz Team Up to Provide Complete Visibility,” cyberark.com In parallel, Web Application and Cloud Firewalls remain vital for shielding public-facing workloads, particularly in retail and government segments that see high transaction volumes.

By Deployment Mode: Hybrid/Multi Cloud Gains Momentum

Public cloud installations commanded a 55.8% share in 2024, but hybrid/multi-cloud deployments are growing at a 23.5% CAGR because executives prefer flexibility to match workloads with optimal performance, cost, and compliance requirements. The shift is expanding addressable demand for toolsets able to monitor traffic, identities, and data uniformly across private data centers and multiple hyperscalers. Confidential-computing deployments are also maturing, giving regulated industries such as healthcare the confidence to run sensitive analytics in shared infrastructures.

Private cloud continues to serve specialized needs in defense, utilities, and critical infrastructure, where uptime and sovereignty are paramount. Yet even these operators adopt policy engines built for multi-cloud to ensure future portability, contributing incremental revenue streams for vendors offering provider-agnostic platforms.

By Organization Size: Mid-Market Ascends

Large enterprises contributed 67.8% of 2024 revenue, given their historical lead in cloud adoption and security budgeting. They average more than 250 unique SaaS subscriptions and therefore need sophisticated correlation tools and automation layers. In contrast, small and medium enterprises are forecast to grow fastest at 24.1% CAGR, assisted by pay-as-you-go services that level the playing field. Platform consolidation lowers total cost of ownership by up to 70% for hospitals with roughly 5,000 employees, demonstrating the economic appeal of unified solutions.

The democratization of AI-driven threat detection embeds enterprise-grade capabilities into starter tiers, accelerating adoption among digitally born firms that may run entirely on serverless architectures. This shift enlarges the overall customer base and infuses fresh revenue into the multi-cloud security solutions market.

By Industry Vertical: Healthcare Outpaces BFSI

BFSI captured 28.3% of 2024 spending owing to stringent payment-card standards and resilience regulations such as DORA, yet healthcare and life sciences will grow fastest at 22.4% CAGR through 2030. Telehealth expansion, genomic data analytics, and electronic health record modernization fuel cloud migration and demand for HIPAA-compliant security controls. Manufacturing firms deploying industrial IoT sensors are also accelerating investment, as evidenced by Milwaukee Electronics’ adoption of Cisco’s SASE framework that cut network outages while tightening governance.

Retailers and e-commerce players adopt web-application firewalls and tokenization to secure high-volume transaction data, whereas government agencies prioritize zero-trust frameworks to protect citizen services. These vertical dynamics collectively broaden the use cases that sustain long-run growth.

Geography Analysis

North America held 38.1% of global revenue in 2024 as early adopters pursued advanced analytics, runtime protection, and post-quantum encryption pilots. United States federal directives mandating zero-trust elevate demand across civilian and defense sectors, while Canadian financial institutions reinforce controls ahead of incoming open-banking rules. Average enterprise security spending in the region rose 37% year on year, underscoring its budgetary heft.

Asia-Pacific is the fastest-growing territory with a 22.9% CAGR, propelled by regulatory frameworks that prioritize data sovereignty and secure digital-government services. Countries such as Singapore, Japan, and Australia publish guidance that implicitly favors multi-cloud diversity, while emerging economies, including India, expand public-sector cloud programs. Sovereign-cloud initiatives drive new opportunities for providers willing to guarantee in-country data residency and open security telemetry.

Europe remains pivotal because GDPR enforcement and the looming EU Cybersecurity Certification Scheme for Cloud Services impose rigorous standards that only sophisticated platforms can fulfill. Financial services adoption climbs ahead of the Digital Operational Resilience Act’s phased deadlines. Vendors differentiate by offering turnkey compliance packs that map controls to multiple directives, helping enterprises navigate fragmented national regulations efficiently.

Competitive Landscape

Market consolidation is accelerating as buyers shift toward integrated suites. Google’s USD 32 billion purchase of Wiz in March 2025 marks the largest transaction in cybersecurity history and signals hyperscalers’ resolve to embed best-in-class capabilities natively. [4]CNBC, “Google to Acquire Wiz for USD 32 Billion,” cnbc.com Fortinet completed its Lacework acquisition to expand Cloud-Native Application Protection depth, adding 225 patents in AI and behavioral analytics.

Strategic alliances also feature prominently. CrowdStrike and Fortinet combined endpoint detection with next-generation firewall workflows to deliver correlated telemetry from device to network edge. AT&T collaborates with Palo Alto Networks on Dynamic Defense™, integrating 5G connectivity with Prisma SASE for small-office backhaul security.

The resulting environment favors vendors that deliver platform breadth, deep automation, and open APIs. Companies unable to evolve beyond point solutions risk marginalization as customers benchmark offerings against consolidated suites promising lower total cost of ownership and simplified operations.

Multi Cloud Security Solutions Industry Leaders

Palo Alto Networks, Inc.

Fortinet, Inc.

Check Point Software Technologies Ltd.

Trend Micro Incorporated

McAfee, LLC (Skyhigh Security)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Google completed its USD 32 billion acquisition of Wiz, expanding Google Cloud’s multi-cloud security coverage.

- February 2025: Palo Alto Networks introduced Cortex Cloud, unifying Prisma Cloud with Cortex CDR for real-time protection across hybrid estates.

- February 2025: Google Cloud released quantum-safe digital signatures in Cloud KMS to future-proof sensitive data.

- November 2024: Wiz acquired Dazz for USD 450 million to automate cloud vulnerability remediation.

Global Multi Cloud Security Solutions Market Report Scope

| Software |

| Services |

| Cloud Workload Protection Platform (CWPP) |

| Cloud Access Security Broker (CASB) |

| Cloud Security Posture Management (CSPM) |

| Cloud Infrastructure Entitlement Management (CIEM) |

| Web Application/Cloud Firewall |

| Encryption and Tokenization |

| Identity and Access Management (IAM) |

| Public Cloud |

| Private Cloud |

| Hybrid/Multi-Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Manufacturing |

| Government and Public Sector |

| Energy and Utilities |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Security Type | Cloud Workload Protection Platform (CWPP) | ||

| Cloud Access Security Broker (CASB) | |||

| Cloud Security Posture Management (CSPM) | |||

| Cloud Infrastructure Entitlement Management (CIEM) | |||

| Web Application/Cloud Firewall | |||

| Encryption and Tokenization | |||

| Identity and Access Management (IAM) | |||

| By Deployment Mode | Public Cloud | ||

| Private Cloud | |||

| Hybrid/Multi-Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the multi cloud security solutions market?

The market is valued at USD 7.57 billion in 2025.

How quickly is the market expected to grow?

It is forecast to register a 19.8% CAGR, climbing to USD 18.68 billion by 2030.

Which component segment is growing fastest?

Services are expanding at a 24.3% CAGR due to rising demand for managed security expertise.

Which region will post the highest growth rate?

Asia-Pacific is projected to grow at a 22.9% CAGR on the back of digital-government initiatives and data-sovereignty laws.

Why is Cloud Infrastructure Entitlement Management gaining traction?

CIEM addresses excessive privileges across fragmented cloud identities and is expected to grow at a 22.6% CAGR through 2030.

Page last updated on: