Biometric And Passwordless Authentication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

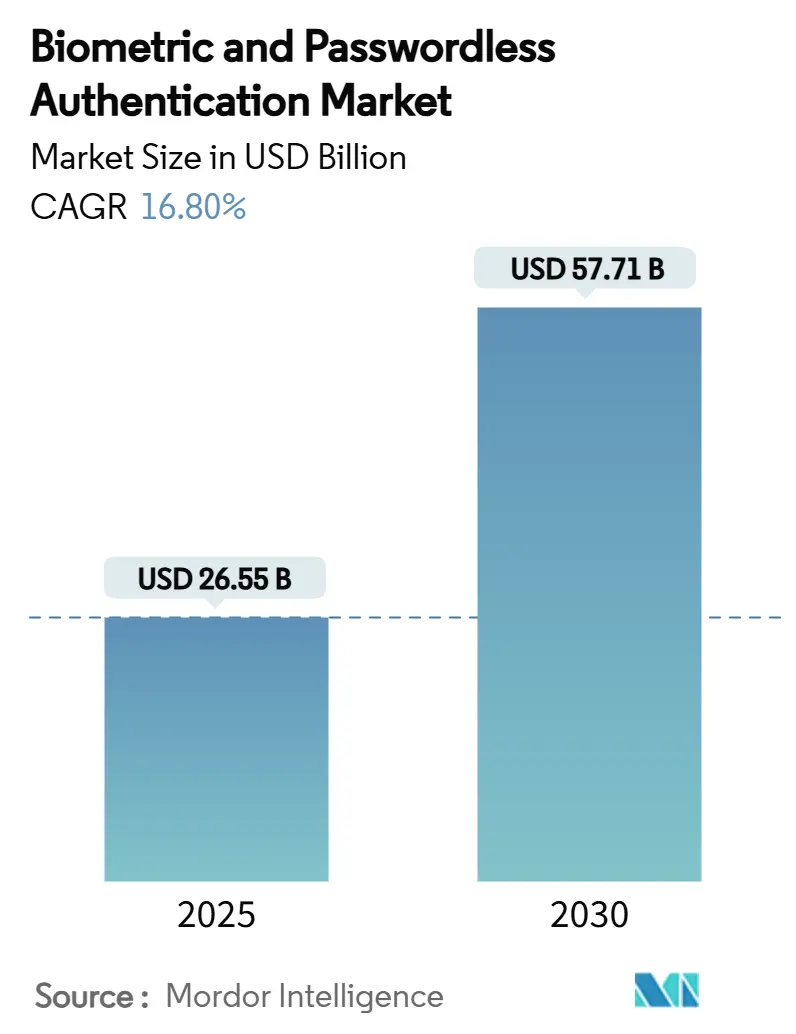

| Market Size (2025) | USD 26.55 Billion |

| Market Size (2030) | USD 57.71 Billion |

| Growth Rate (2025 - 2030) | 16.80% CAGR |

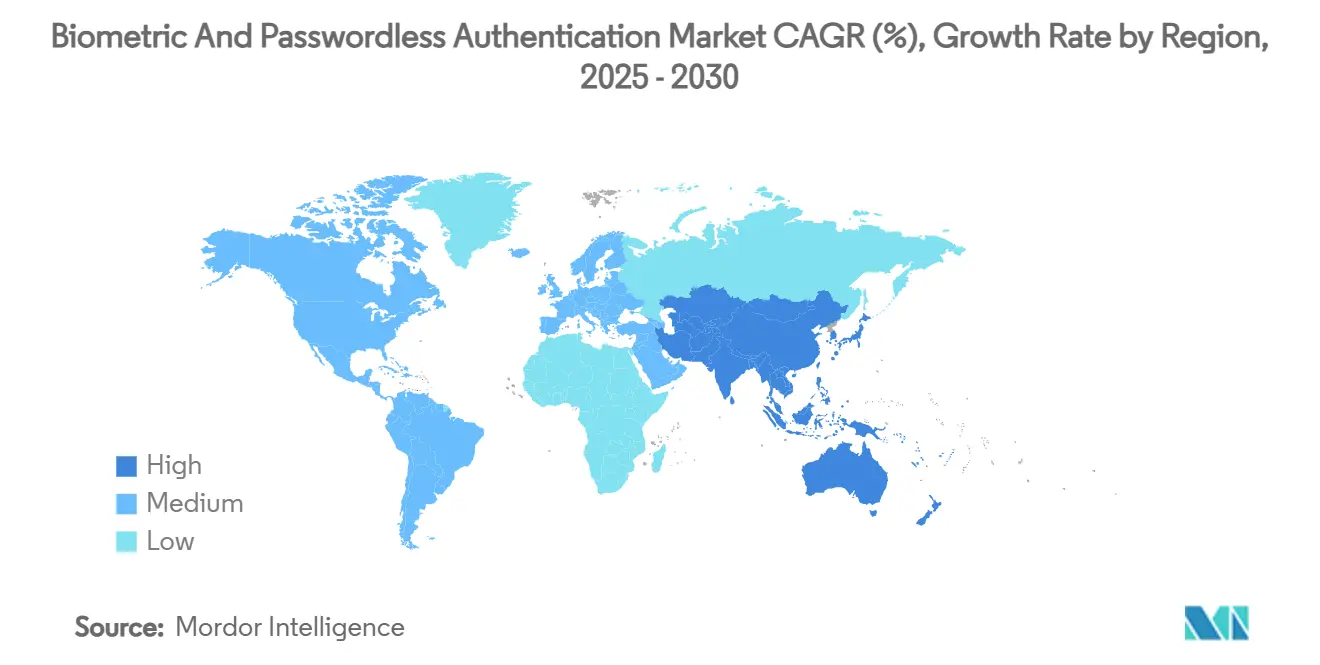

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

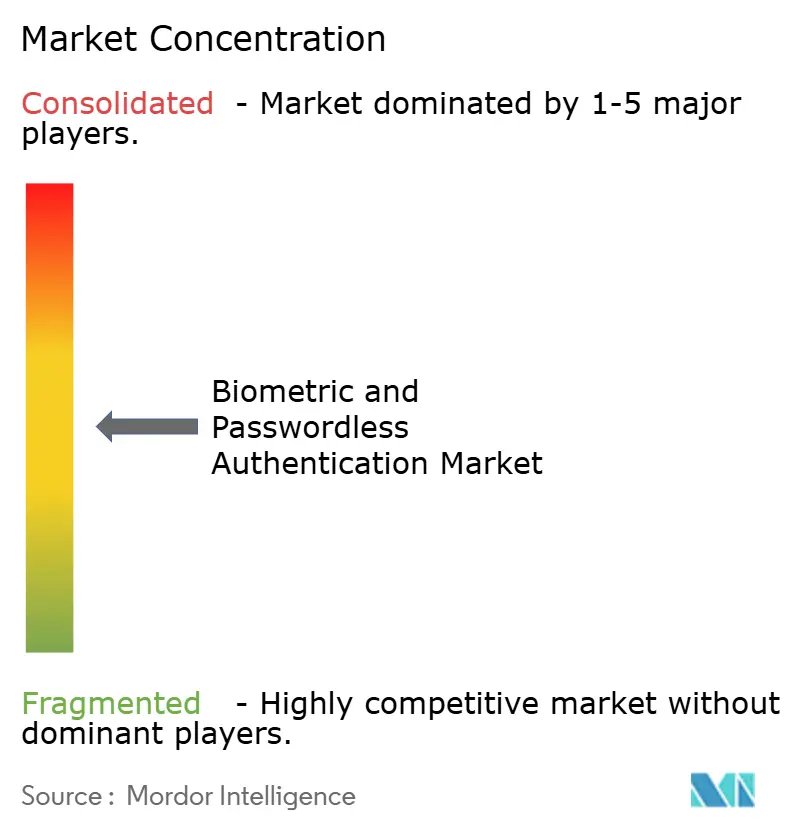

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biometric And Passwordless Authentication Market Analysis by Mordor Intelligence

The Biometric And Passwordless Authentication Market size is estimated at USD 26.55 billion in 2025 and is expected to reach USD 57.71 billion by 2030, at a CAGR of 16.80% during the forecast period (2025-2030). Strong growth stems from the near-universal enablement of FIDO2/WebAuthn protocols on 75.44% of connected devices. [1]FIDO Alliance, “FIDO2 Overview,” fidoalliance.org Widespread sensor deployment on smartphones, expanding digital-banking ecosystems in Asia-Pacific, and government e-identification programs have combined to shift investment from password-centred defences to proactive, continuous authentication frameworks. Enterprises now view passkeys and biometrics as a core pillar of zero-trust architecture, while declining hardware costs and cloud-delivered services lower adoption barriers. Competitive positioning is increasingly defined by vendors’ ability to integrate behavioural analytics and AI-driven liveness detection into frictionless user experiences.

Key Report Takeaways

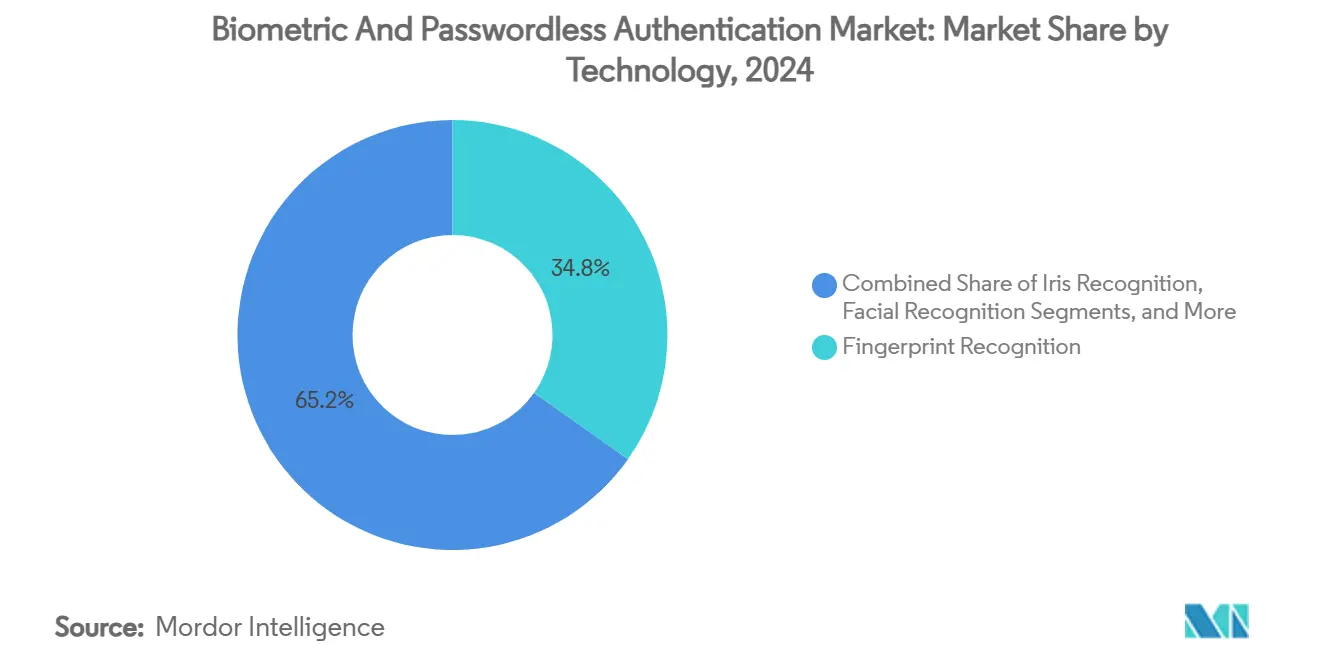

- By technology, fingerprint recognition led with 34.8% of the biometric and passwordless authentication market share in 2024; behavioural biometrics is projected to expand at a 17.8% CAGR through 2030.

- By component, hardware commanded a 57.7% share of the biometric and passwordless authentication market size in 2024, while services are expected to rise at an 18.4% CAGR to 2030

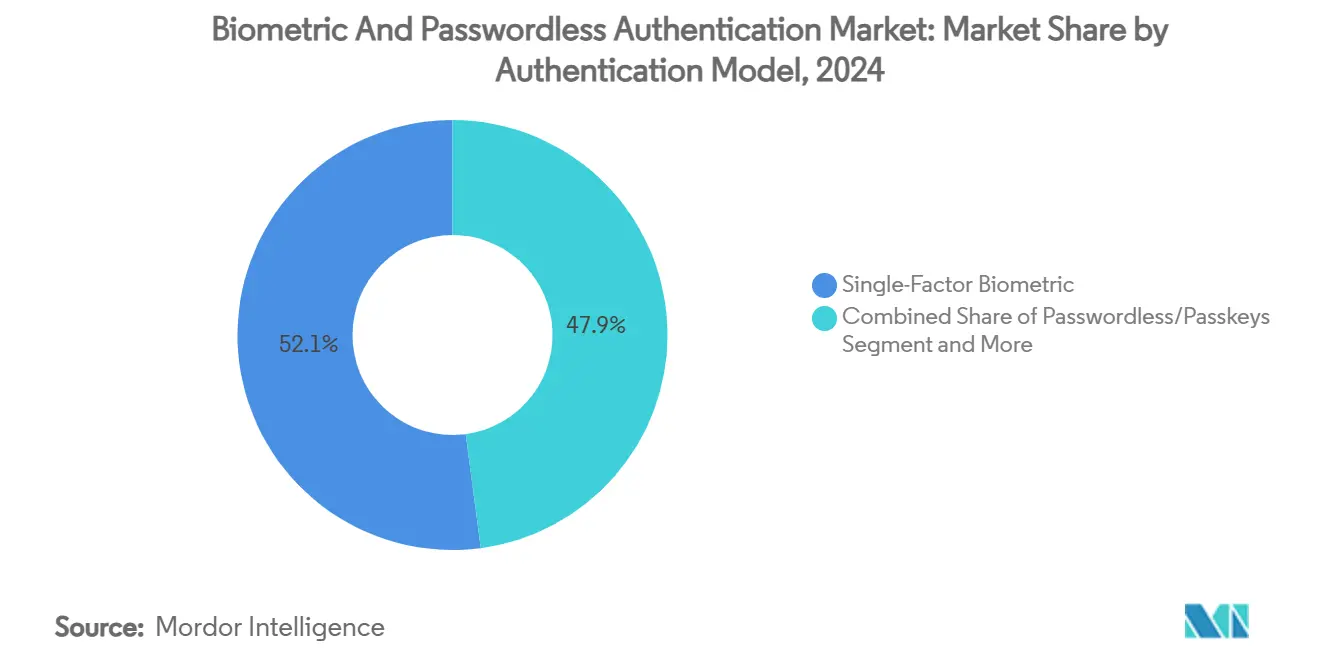

- By authentication model, single-factor biometric systems accounted for a 52.1% share of the biometric and passwordless authentication market size in 2024; passwordless/passkeys are forecast to grow at an 18.2% CAGR through 2030.

- By end-user industry, BFSI captured 28.7% of the biometric and passwordless authentication market share in 2024, whereas healthcare and life sciences are anticipated to advance at an 18% CAGR by 2030.

- By geography, North America held 38.5% revenue share in 2024, while Asia–Pacific is projected to be the fastest-growing region at an 18.1% CAGR to 2030.

Global Biometric And Passwordless Authentication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Standards-driven adoption of FIDO2/WebAuthn | +2.8% | North America, European Union | Medium term (2-4 years) |

| Sub-USD 2 biometric sensors in smartphones | +2.1% | Asia–Pacific manufacturing hubs; global distribution | Short term (≤ 2 years) |

| Digital-banking scale-up in emerging markets | +3.2% | Asia–Pacific core; Latin America and Africa spill-over | Long term (≥ 4 years) |

| Government e-ID and ICAO 9303 travel documents | +1.9% | Developing nations | Medium term (2-4 years) |

| AI-powered continuous authentication | +2.4% | North America and European enterprise markets | Medium term (2-4 years) |

| Decentralised identity wallets | +1.7% | EU leadership; global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Standards-driven adoption of FIDO2/WebAuthn protocols

The FIDO Alliance has turned WebAuthn into a de facto global baseline, enabling passwordless flows across Windows, Android, and iOS ecosystems. Financial institutions such as JPMorgan Chase and Revolut now authenticate customers with passkeys, reporting marked declines in phishing incidents and password-reset tickets. Common standards reduce integration work by roughly 40% for developers migrating from legacy MFA, while the EU Digital Identity Wallet initiative cements regulatory confidence in WebAuthn for sovereign IDs. The payoff is especially clear in sectors with stringent compliance mandates, where a platform-neutral credential mitigates vendor lock-in and long-term maintenance risk.

Smartphone OEM integration of biometric sensors at sub-USD 2 BOM

Volume production of capacitive and optical fingerprint modules has pushed bill-of-materials costs below USD 2, allowing biometrics to reach mid-range and entry-level handsets without price penalties. The downstream effect is a dramatic expansion of addressable endpoints for the biometric and passwordless authentication market. Low-cost sensors bundled with on-device AI liveness algorithms satisfy both convenience and spoof-resistance, supporting mass adoption in digital banking, retail payments, and micro-insurance apps that target first-time smartphone owners. Manufacturers also leverage sensor fusion—combining fingerprint, facial, and voice inputs—to raise security without inflating per-unit cost.

Rapid digital-banking scale-up in emerging markets

Asia’s super-apps, Latin America’s fintech cohort, and Africa’s mobile-money leaders collectively depend on strong yet effortless identity proofing. Digital wallets already account for 70% of online payments in Asia-Pacific, and user acquisition remains tied to seamless onboarding that bypasses paper IDs. [2]Charmaine Jacob, “Digital Wallets Overtake Cash in Asia,” cnbc.com Banks deploying biometric onboarding tools report faster KYC completion, lower fraud loss ratios, and higher retention among unbanked customers. Shared national databases, such as Nigeria’s Bank Verification Number registry covering 64 million citizens, accelerate cross-institution authentication and create opportunities for layered behavioural biometrics that spot suspicious anomalies in real time.

Government e-ID and travel credential roll-outs (ICAO 9303)

Ethiopia’s February 2025 launch of an e-passport in full ICAO 9303 compliance demonstrates how sovereign programmes can galvanise domestic demand for biometric modules, personalisation software, and enrolment services. [3]Government of Ethiopia, “e-Passport Launch Speech,” gov.et Similar initiatives in Indonesia and Ghana are standardising chip-embedded credentials across immigration, tax, and healthcare portals. Once citizen wallets exist, private-sector actors—from insurers to telcos—quickly plug into the same verification rails, reinforcing a virtuous adoption cycle. Vendors that provide enrolment hardware, PKI, and life-cycle management gain first-mover advantage in these long-term public contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for multimodal sensor fusion | -1.8% | Global; SME budgets most affected | Short term (≤ 2 years) |

| Inter-vendor interoperability gaps | -1.2% | Legacy enterprise estates worldwide | Medium term (2-4 years) |

| Synthetic-identity fraud and biometric spoofing | -2.1% | North America, Europe | Long term (≥ 4 years) |

| Deepfake-driven liveness attacks | -1.4% | High-security use cases across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for multimodal sensor fusion

Enterprises seeking ≥99.9% match rates often deploy fingerprint, face, and iris scanners in tandem, but each added modality inflates hardware and integration budgets. Full-scale roll-outs can cost USD 50,000–500,000, a hurdle for small and mid-size firms weighing benefits against single-modality systems that offer 95–98% accuracy at a fraction of the spend. On-premise middleware, custom SDKs, and regulatory certification can double initial equipment outlays, extending payback periods and pushing buyers toward subscription-based managed services instead of outright procurement.

Inter-vendor interoperability gaps outside the FIDO umbrella

Most proprietary biometric SDKs still rely on closed APIs, impeding plug-and-play integration with identity governance, IAM, and fraud analytics stacks. Migrating from entrenched smart-card or OTP frameworks frequently requires costly middleware and retraining of help-desk staff. Where native WebAuthn support is absent—especially in legacy banking software—projects risk delays that erode executive support and inflate total cost of ownership. Industry coalitions are pushing shared schema for metadata, event logging, and liveness attestation, but broad harmonisation remains several years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Behavioural Analytics Drive Next-Generation Security

Fingerprint modules retained 34.8% of the biometric and passwordless authentication market share in 2024, thanks to entrenched smartphone integration and widespread reader availability. Facial recognition gained ground in retail payments and access control as camera quality and edge-AI models improved, although privacy rules in parts of Europe constrained public-space deployments. Iris scanning preserved a niche in defence and healthcare where near-perfect accuracy offsets higher cost, while voice recognition found use in call-centre authentication and smart-speaker ecosystems. Palm and vein technologies have advanced in hospital admission workflows due to hygiene advantages. The biometric and passwordless authentication market size for behavioural biometrics is poised to outpace all other modalities, rising at a 17.8% CAGR on the back of continuous, invisible authentication that profiles typing, swipes, and gait patterns. Enterprises blending face and fingerprint modalities report a 40% uplift in match precision versus single-factor designs. AI models embedded directly on sensors enable real-time threat scoring, reducing latency and preserving user privacy by keeping templates on-device.

Behavioural solutions such as keystroke analytics processed 979,000 workforce logins in a single US healthcare network without a drop in clinical productivity. Larger-scale pilots across regional banks demonstrate fraud-loss reductions and customer-satisfaction gains when behavioural risk signals are fused with transactional data. Sensor-fusion roadmaps point toward multimodal smartphones that leverage camera, accelerometer, and microphone streams without draining battery life. As enterprises normalise remote work, behavioural tools sit at the heart of zero-trust, providing step-up verification when risk metrics spike mid-session.

By Component: Services Accelerate Integration Complexity

Hardware captured 57.7% revenue in 2024, reflecting the sheer volume of fingerprint, camera, and infrared modules embedded in consumer electronics and corporate access points. Yet services can claim the steepest trajectory, climbing at an 18.4% CAGR through 2030 as organisations rely on specialised partners to stitch biometric workflows into IAM back ends, SIEM dashboards, and governance frameworks. The biometric and passwordless authentication market size tied to software engines also expands steadily as AI-centric models require frequent updates to counter evolving attack vectors. Sensors continue to benefit from scale economies, with sub-USD 2 fingerprint units catalysing uptake in entry-level smartphones and smartcards.

Professional services revenue often equals 40–60% of project totals once consulting, customisation, and managed operations are included. Mergers like Vitaprotech’s acquisition of Identiv’s reader business illustrate consolidation aimed at bundling advisory, deployment, and life-cycle support under one umbrella. Cloud-first authentication APIs reduce upfront capital but shift spending toward subscription OPEX, giving vendors predictable recurring income while letting customers flex capacity on demand.

By Authentication Model: Passkeys Transform Enterprise Identity

Single-factor biometrics accounted for 52.1% of 2024 adoption, reflecting years of smartphone fingerprint and face unlock habits. The biometric and passwordless authentication market size linked to passkeys and other passwordless constructs is, however, forecast to surge at 18.2% CAGR as FIDO2/WebAuthn attains near-ubiquitous client support. Enterprises deploying passkeys report 90% drops in password-related help-desk calls and marked declines in account-takeover fraud. Multi-factor biometric schemes retain importance in high-assurance settings that demand more than one modality; hardware tokens are gradually displaced by device-bound credentials that use public-key cryptography under the hood.

Retail banking pilots demonstrate frictionless checkout at staffed and self-service terminals where face and palm recognition validate both identity and payment instrument in under two seconds. Browser-synced passkeys allow secure credential roaming without centralised password databases, thereby shrinking the attack surface. CIOs increasingly cite passkey roll-outs as foundational to zero-trust roadmaps, paving the way for conditional-access policies that reference real-time behavioural signals.

By End-user Industry: Healthcare Leads Digital Transformation

Financial institutions held the largest slice at 28.7% as of 2024, driven by anti-fraud mandates, PSD2 compliance, and customer expectations for app-level biometrics. Healthcare and life sciences exhibit the fastest ascent at an 18% CAGR, propelled by patient-safety imperatives, drug-diversion monitoring, and stringent data-handling regulations. The biometric and passwordless authentication market size attached to hospital admission, e-prescription, and telemedicine flows climbs steadily as institutions aim to prevent mis-identification-related errors. Government programmes continue to modernise border control and social-benefit disbursement through e-ID platforms, guaranteeing steady demand for high-security modules.

Retail and e-commerce leverage biometric checkout to curb cart abandonment, while IT-telecom operators integrate behavioural analytics into SIM-swap prevention and customer-care authentication. Manufacturing plants adopt biometric access control for critical machinery locks, improving safety compliance. Travel and hospitality add face-enabled kiosks that expedite check-in and boarding, aligning with post-pandemic expectations for contactless experiences.

Geography Analysis

North America controlled 38.5% of global revenue in 2024, sustained by mature cybersecurity ecosystems, early zero-trust programmes, and comprehensive regulatory oversight. Banks and federal agencies running large-scale passkey pilots provide proof points that ripple into healthcare and retail, accelerating supplier sales. Vendors headquartered in the region invest aggressively in edge-AI and privacy-preserving computation, helping offset a rise in synthetic-identity fraud that regulators flagged as a 60% year-on-year surge.

Asia–Pacific is forecast to post an 18.1% CAGR, the fastest among all regions. Governments in Indonesia, Singapore, and India have institutionalised biometric credentials across visas, welfare, and payments, fuelling mass-market familiarity. Chinese and Indian consumers already use biometrics for more than 70% of e-commerce and point-of-sale digital-wallet transactions. Domestic handset makers bundle low-cost fingerprint readers and camera-based face unlock across sub-USD 200 models, broadening reach to first-time online shoppers. Fintechs focus on behavioural signals to serve unbanked segments lacking conventional ID histories.

Europe delivers steady, regulated growth under GDPR and eIDAS frameworks that demand explicit privacy safeguards and local data residency. The forthcoming EU Digital Identity Wallet scheme anchors long-range investment in decentralised verifiable credentials. National health systems in France, Germany, and the Nordics deploy palm-vein and facial solutions to streamline patient enrolment while maintaining consent controls. South America, along with the Middle East and Africa, shows nascent but accelerating uptake: initiatives like Nigeria’s biometric banking registry and Ghana’s e-passport illustrate how public-sector projects seed private-sector adoption across retail, telecoms, and remittances.

Competitive Landscape

The biometric and passwordless authentication market is moderately concentrated. Legacy champions—IDEMIA, NEC, and Thales—retain dominance in government tenders owing to decades of AFIS expertise, global enrolment infrastructure, and strong trust marks. They supplement hardware with cloud orchestration, PKI, and professional services, achieving high switching costs for clients. Mid-tier specialists such as Yubico and Daon compete through FIDO2-certified platforms that integrate quickly with SaaS applications. Behavioural analytics innovators like BioCatch and BehavioSec differentiate through risk engines that score interactions continuously, winning deployments in remote banking and healthcare.

M&A activity underscores a pivot toward platform breadth. Entrust’s USD 6 billion acquisition of Onfido welded document verification to facial biometrics, addressing end-to-end digital onboarding. [4]Entrust Corporation, “Entrust Completes Onfido Acquisition,” entrust.com Private-equity deals—most notably Permira’s USD 1.3 billion majority stake in BioCatch—signal confidence in continuous-authentication IP and subscription revenue. Patent filings from Apple, Samsung, and Google covering gaze tracking, neuromuscular signals, and sub-dermal gesture sensing hint at future modalities that could upset incumbent share. To stay competitive, vendors embed AI accelerators on devices, cutting cloud round-trips while safeguarding templates against exfiltration.

Partnership ecosystems also matter. Leading system integrators now bundle passkey orchestration with IAM migration playbooks, shortening deployment cycles for enterprises. Sensor makers co-design silicon with mobile chipset suppliers, ensuring liveness-detection engines run at the edge without draining battery life. Vendors openly document APIs conforming to FIDO, OAuth, and OpenID Connect, a prerequisite for large-scale enterprise contracts that insist on vendor portability and standards compliance.

Biometric And Passwordless Authentication Industry Leaders

IDEMIA Group S.A.S.

NEC Corporation

Thales Group S.A.

Fingerprint Cards AB

HID Global Corporation (ASSA ABLOY AB)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ethiopia launched a nationwide e-passport compliant with ICAO 9303, creating sustained demand for biometric enrolment and verification solutions.

- January 2025: JPMorgan Chase announced the rollout of facial and palm-recognition payment terminals across US retail sites, marking one of the largest passkey-enabled payment initiatives in North America.

- January 2025: Suprema debuted the BioEntry W3 AI facial device and CoreStation 20 controller at Intersec 2025, targeting large-scale physical-access deployments.

- January 2025: HID Global introduced the Amico facial reader at Intersec Dubai 2025 to serve Middle-East projects seeking frictionless entry control.

- January 2025: Suprema AI secured the CES 2025 Best of Innovation Award for its Q-Vision Pro on-device AI module, integrating facial recognition and behaviour analysis for ATM fraud prevention.

- December 2024: Indonesia completed full nationwide issuance of e-passports, standardising biometric credentials across all passport offices.

Global Biometric And Passwordless Authentication Market Report Scope

| Fingerprint Recognition |

| Facial Recognition |

| Iris Recognition |

| Voice Recognition |

| Palm and Vein Recognition |

| Behavioral Biometrics |

| Multimodal / Hybrid |

| Hardware |

| Software |

| Services |

| Single-Factor Biometric |

| Multi-Factor Biometric |

| Passwordless/Passkeys |

| Hardware Token-based |

| BFSI |

| Government and Homeland Security |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| IT and Telecommunication |

| Travel and Hospitality |

| Consumer Electronics |

| Manufacturing and Industrial |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Fingerprint Recognition | ||

| Facial Recognition | |||

| Iris Recognition | |||

| Voice Recognition | |||

| Palm and Vein Recognition | |||

| Behavioral Biometrics | |||

| Multimodal / Hybrid | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Authentication Model | Single-Factor Biometric | ||

| Multi-Factor Biometric | |||

| Passwordless/Passkeys | |||

| Hardware Token-based | |||

| By End-user Industry | BFSI | ||

| Government and Homeland Security | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| IT and Telecommunication | |||

| Travel and Hospitality | |||

| Consumer Electronics | |||

| Manufacturing and Industrial | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast growth rate for the biometric and passwordless authentication market?

The biometric and passwordless authentication market is projected to grow at a 16.8% CAGR from USD 26.55 billion in 2025 to USD 57.71 billion by 2030.

Which technology segment is growing fastest?

Behavioural biometrics is expected to record the highest growth at a 17.8% CAGR through 2030 as enterprises adopt continuous, invisible authentication.

Why is Asia–Pacific the fastest-growing regional market?

Rapid digital-banking adoption, government e-ID programmes and widespread low-cost smartphone penetration underpin an 18.1% regional CAGR.

How do passkeys improve enterprise security?

Passkeys eliminate centralised password storage, reduce help-desk resets by up to 90% and cut account-takeover incidents by two-thirds when tied to on-device biometrics.

What restrains wider deployment of multimodal biometrics?

High capital expenditure for multi-sensor hardware and integration, combined with the need for advanced liveness detection, raises total cost of ownership for smaller enterprises.

Which industries beyond finance show strong adoption momentum?

Healthcare leads non-financial uptake thanks to patient-safety mandates, while retail, telecom and government sectors deploy biometrics to streamline customer experience and fortify security.

Page last updated on: