Server Security Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

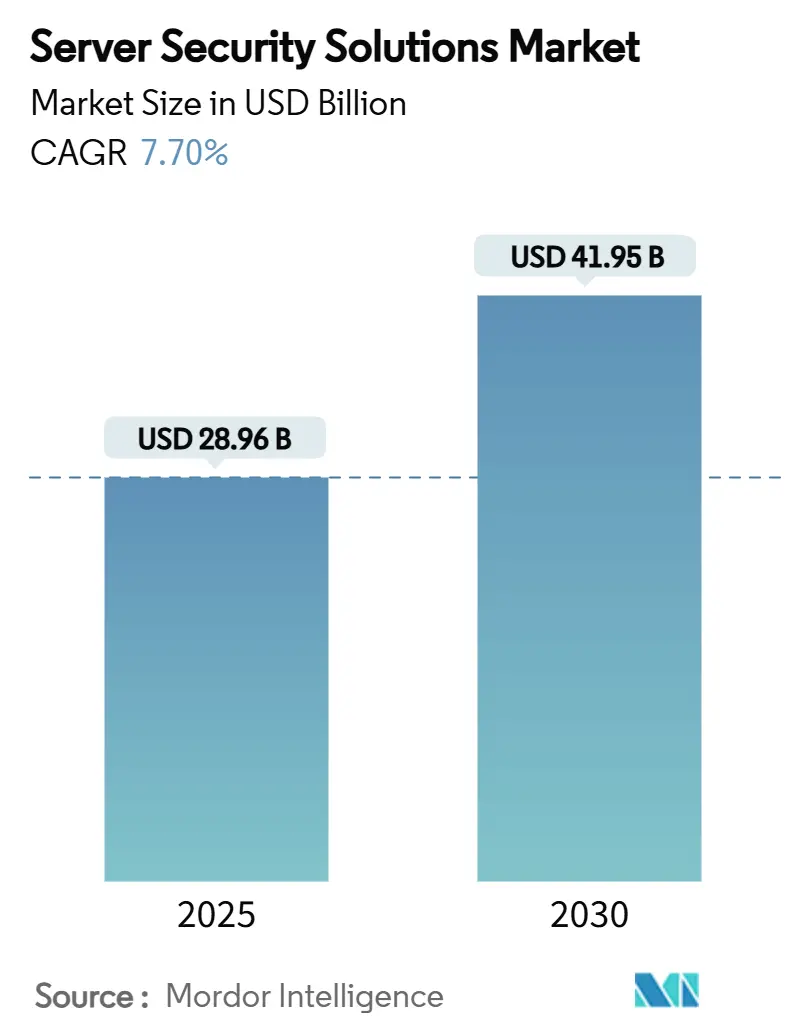

| Market Size (2025) | USD 28.96 Billion |

| Market Size (2030) | USD 41.95 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

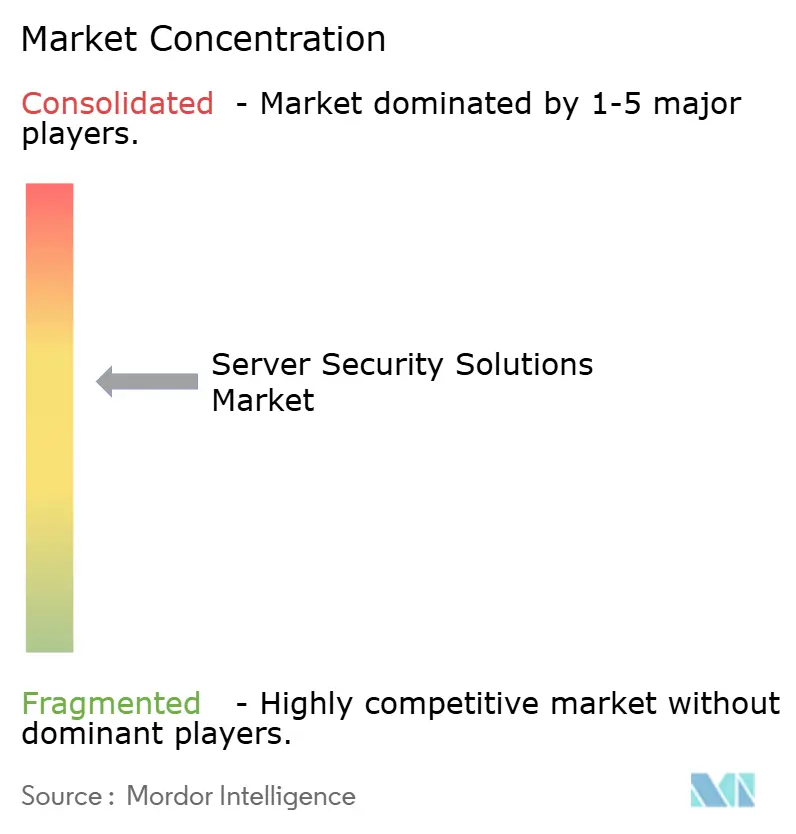

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Server Security Solutions Market Analysis by Mordor Intelligence

The server security solutions market size reached USD 28.96 billion in 2025 and is forecast to climb to USD 41.95 billion by 2030, registering a 7.7% CAGR over the period. Growing digitization of critical infrastructure, the sharp rise in multi-layer ransomware campaigns, and the widening cybersecurity skills gap are the primary forces expanding the server security solutions market. Intensifying regulatory oversight, rapid adoption of Zero Trust programs, and the integration of confidential computing features inside server silicon further reinforce spending momentum. Consolidation among platform vendors accelerates as enterprises pursue tool rationalization to lower compliance costs that average USD 3.5 million each year while avoiding non-compliance penalties that average USD 9.4 million.[1]Ellen Messmer, “Cost of Regulatory Security Compliance? On Average, USD 3.5M,” networkworld.com The market’s resilience reflects the shift from viewing server protection as a compliance obligation to treating it as a board-level business risk.

Key Report Takeaways

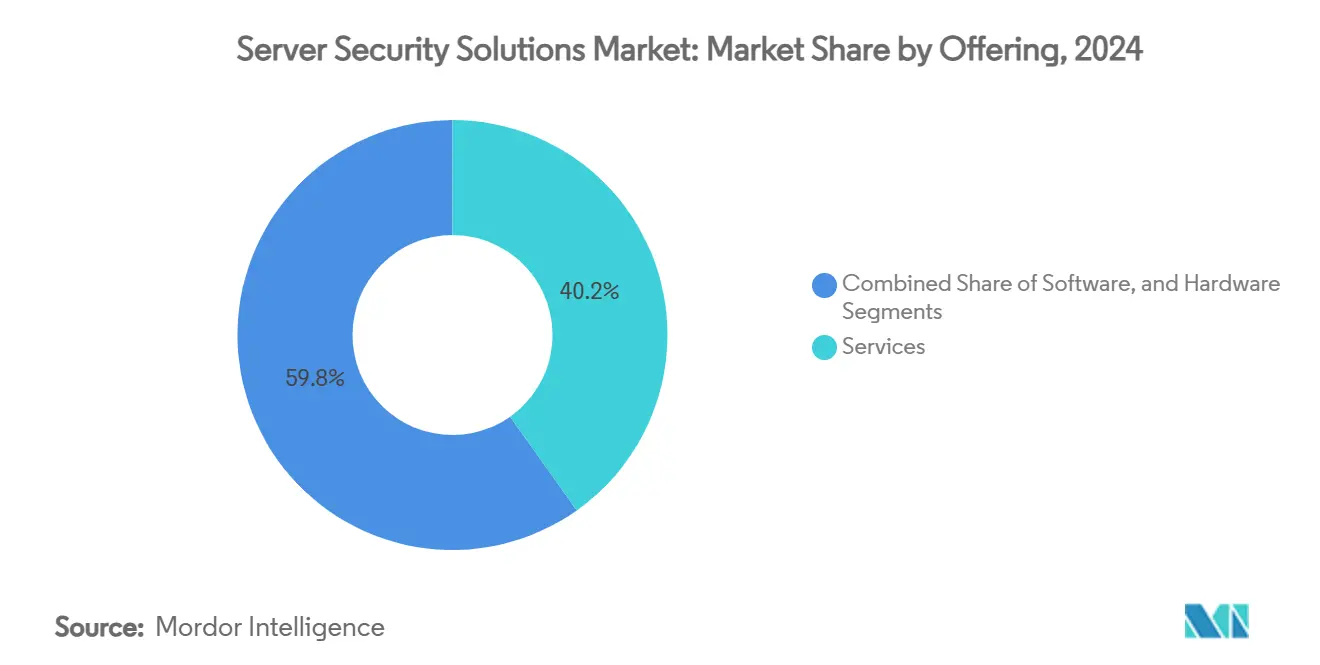

- By offering, services led with 40.2% revenue share in 2024, while managed security services are projected to expand at a 9.5% CAGR through 2030.

- By deployment mode, cloud-based deployment captured 64.3% of the server security solutions market share in 2024, and this segment is forecast to grow at a 11.1% CAGR to 2030.

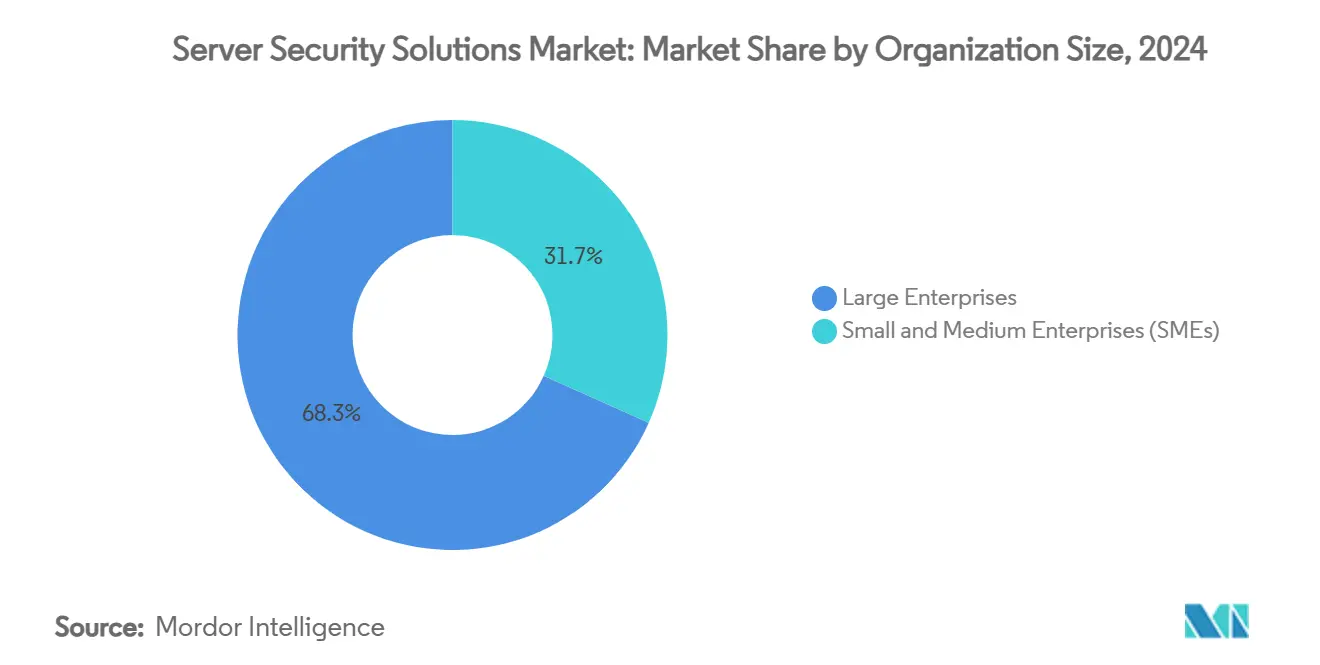

- By organization size, large enterprises accounted for 68.3% of the 2024 revenue pool, whereas small and medium enterprises are set to record the fastest 9.2% CAGR through 2030.

- By end-use industry, banking, financial services, and insurance firms held 27.1% of spending in 2024; healthcare is the fastest-growing vertical at 10.8% CAGR to 2030.

- By geography, North America maintained a 35.2% share in 2024, while Asia-Pacific is projected to post the strongest 11.2% CAGR over the forecast horizon.

Global Server Security Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of hybrid cloud deployments requires unified server protection | +1.2% | Global, with early adoption in North America and the EU | Medium term (2-4 years) |

| Increasing sophistication and frequency of ransomware attacks on critical servers | +1.8% | Global, particularly North America, Europe, and the Asia-Pacific | Short term (≤ 2 years) |

| Growing regulatory mandates for data protection and cybersecurity compliance | +1.1% | EU (GDPR), North America (SOX, HIPAA), expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising adoption of Zero-Trust architecture across large enterprises | +0.9% | North America and the EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Integration of confidential computing, enabling secure processing of workloads | +0.7% | North America, EU, select Asia-Pacific markets | Long term (≥ 4 years) |

| Shift to composable infrastructure, boosting east-west traffic inspection demand | +0.5% | North America, EU, advanced Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hybrid Cloud Deployments Requiring Unified Server Protection

Hybrid environments enlarge the threat surface by dispersing workloads across public and private clouds where inconsistent policies prevail. Ninety-five percent of enterprises reported at least one cloud breach in the past 18 months, largely tied to misconfigurations and weak workload controls, underscoring demand for platforms that guard any server, anywhere. Composable infrastructure deepens this need as dynamic resource provisioning calls for real-time security enforcement. Organizations, therefore, pivot to unified solutions that monitor east-west traffic and apply consistent policies across mixed estates.

Increasing Sophistication and Frequency of Ransomware Attacks on Critical Servers

Threat groups such as RansomHub center attacks on data theft and lateral movement within server environments, sidestepping legacy detection tools. Median ransom payments continue to escalate as attackers hit high-value healthcare and financial servers. The 2024 CrowdStrike outage, which cost Fortune 500 companies USD 5.4 billion, illustrated the business continuity risk tied to server downtime. Enterprises now invest in redundant server protection and immutable backups.

Growing Regulatory Mandates for Data Protection and Cybersecurity Compliance

GDPR Article 32, HIPAA, and new SEC disclosure rules require demonstrable safeguards around the confidentiality, integrity, and availability of server systems. Annual compliance spending averages USD 5.47 million, yet non-compliance fines average USD 14.82 million, driving consolidation toward platforms that map directly to multiple standards.

Rising Adoption of Zero Trust Architecture Across Large Enterprises

Zero Trust erases implicit trust inside data centers by demanding continual identity, device, and context verification before server access is granted. Pilot deployments at large US banks cut lateral-movement incidents, reinforcing demand for policy engines that integrate with multifactor authentication and micro-segmentation controls.[2]NIST, “Implementing a Zero Trust Architecture,” nist.gov Adoption accelerates in hybrid architectures where static perimeter controls falter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of qualified cybersecurity personnel is driving service gaps | -1.4% | Global, acute in North America and the EU | Short term (≤ 2 years) |

| High initial cost of advanced server security solutions for SMEs | -0.8% | Global, particularly emerging markets | Medium term (2-4 years) |

| Performance overhead concerns with in-line deep packet inspection | -0.6% | Global, critical in high-performance computing environments | Short term (≤ 2 years) |

| Fragmentation of security-telemetry standards is hindering cross-platform visibility | -0.4% | Global, affecting multi-vendor environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified Cybersecurity Personnel Driving Service Gaps

Four million open cybersecurity roles worldwide leave 56% of organizations exposed to server security risks stemming from understaffed teams. Managed security providers partially offset the gap, yet heavy reliance on external talent introduces oversight and continuity risks. The United Kingdom alone must add 17,500 professionals annually, demonstrating the scale of the challenge.

High Initial Cost of Advanced Server Security Solutions for SMEs

Comprehensive server defense stacks require sizable licensing and professional-service outlays that strain SME budgets. Average annual compliance bills of USD 3.5 million outpace many SME IT budgets, though the USD 9.4 million non-compliance penalty potential forces decision-makers to weigh risk over cost. Vendors respond with consumption-based pricing and automated configurations to lower entry barriers, but adoption remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain from Outsourcing Momentum

Services held the largest slice of 40.2% in 2024 as enterprises turned to managed detection and response and advisory engagements to bridge skill shortages. Software platforms comprising server antivirus, EDR, CWPP, and CSPM form the next-largest pool, led by CrowdStrike’s USD 1 billion SaaS milestone. Hardware demand remains steady as confidential-computing-enabled processors improve data-in-use protection.

The segment advances as professional services around Zero Trust, hybrid cloud integration, and regulatory audits grow faster than product licenses. Alliances between hardware vendors and software platforms, such as Intel and leading CSPM providers, heighten differentiation around secure workload processing. Services, therefore, underpin platform value and accelerate the server security solutions market.

By Deployment Mode: Cloud-Based Defenses Prevail

Cloud models accounted for 64.3% of 2024 revenue because enterprises require unified policies that travel with workloads across hybrid estates. CSPM tools slash misconfiguration incidents by up to 80%, reinforcing preference for SaaS delivery.[3]Tenable, “What is cloud workload protection (CWP)?” tenable.com On-premise platforms persist for air-gapped and regulated workloads.

Hybrid strategies gain traction as Asia-Pacific sovereign-cloud frameworks obligate local processing while boards still value global scalability. Vendors embed identical policy engines across all deployment types, ensuring deterministic controls regardless of location and propelling the server security solutions market further into the cloud era.

By Organization Size: Enterprises dominate yet SMEs accelerate

Large enterprises contributed 68.3% of 2024 spending, leveraging capital and skilled teams to deploy Zero Trust and confidential computing at scale. However, SME outlays are forecast to grow at a 9.2% CAGR as attackers intensify focus on lightly defended businesses. Consumption-based licensing and automated hardening scripts help SMEs close exposure gaps without hiring full security teams.

The server security solutions market size for SMEs is anticipated to expand steadily as regulatory bodies extend oversight to smaller data processors. Managed security subscriptions, bundled with cloud infrastructure, lower entry hurdles, and will keep fueling SME adoption.

By End-Use Industry: Financial Services lead, Healthcare surges

BFSI organizations held 27.1% of 2024 spending, anchored by strict audit trails and high-value data that require layered defenses. Healthcare workloads will post the fastest 10.8% CAGR to 2030 as electronic records expansion and medical IoT devices widen the attack surface under HIPAA safeguards.

Confidential computing and AI-enhanced anomaly detection appeal strongly to life-science researchers who process genomic data. Government, telecom, and manufacturing segments also elevate spending as operational technology converges with IT, thus widening demand across the broader server security solutions market.

Geography Analysis

North America commanded 35.2% revenue in 2024, benefiting from mature cybersecurity ecosystems and early Zero Trust rollouts. The region also shoulders the largest talent shortfall, driving uptake of automated threat-response orchestration. High-profile breaches, including the CrowdStrike outage, kept board attention fixed on server resilience, further enlarging regional budgets.

Asia-Pacific recorded the fastest 11.2% CAGR forecast to 2030, underpinned by sovereign-cloud mandates, explosive data-center construction, and rising regulation of critical infrastructure. Nations such as Australia, Japan, and India accelerate the adoption of confidential computing to reconcile local residency requirements with global cloud architectures, fueling incremental server security investment.

Europe remains driven by GDPR enforcement, which mandates “appropriate technical and organizational measures” for any server processing personal data, forcing sustained compliance investment. Meanwhile, Middle East and Africa markets see emerging demand tied to national digital agendas but still depend heavily on managed security due to limited in-region expertise.

Competitive Landscape

Competition centers on platform breadth, AI-driven analytics, and integration depth. CrowdStrike became the first pure-play SaaS vendor to exceed USD 1 billion in sales, underscoring demand for single-agent architectures that shield both endpoints and servers. Palo Alto Networks continues an aggressive roll-up strategy, acquiring Protect AI for USD 700 million and evaluating a USD 7 billion bid for SentinelOne to enhance unified detection capabilities.[4]MacKenzie Sigalos, “Palo Alto Networks acquiring Protect AI,” cnbc.com

Fortinet strengthens through its Lacework purchase, integrating cloud-workload defenses inside its security fabric, while Google’s reported USD 23 billion talks to buy Wiz highlight hyperscaler appetite for cloud-native posture management. Start-ups focusing on confidential computing, such as Enclave Labs, gain attention as enterprises evaluate server-side cryptographic isolation to secure high-value data in use. Market consolidation is expected to continue as buyers favor end-to-end suites over point products.

A handful of incumbents collectively control well over half of global revenue, yet a vibrant pipeline of innovative challengers pushes incumbents toward continual platform expansion. Strategic alliances across hardware and software stacks accelerate the development of server-specific protections that address emerging east-west threats.

Server Security Solutions Industry Leaders

Trend Micro Incorporated

CrowdStrike Holdings, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fortinet posted USD 1.54 billion Q1 revenue, up 14% year-over-year, with Security Operations ARR rising 30%.

- May 2025: Palo Alto Networks increased next-generation security ARR to USD 5 billion and closed the Protect AI deal for USD 700 million.

- April 2025: CrowdStrike launched an AI-powered Network Vulnerability Assessment for Falcon Exposure Management, eliminating hardware dependencies.

- March 2025: Google entered advanced talks to acquire Wiz for USD 23 billion, signaling the cloud giant’s intent to scale its security portfolio.

Global Server Security Solutions Market Report Scope

| Software (Server AV, EDR, XDR, CSPM, CWPP) |

| Hardware (HSMs, Secure NICs, Firewall Appliances) |

| Services (Managed Security, Consulting, Integration) |

| On-Premise |

| Cloud-Based |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Government and Defense |

| Manufacturing and Industrial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Software (Server AV, EDR, XDR, CSPM, CWPP) | ||

| Hardware (HSMs, Secure NICs, Firewall Appliances) | |||

| Services (Managed Security, Consulting, Integration) | |||

| By Deployment Mode | On-Premise | ||

| Cloud-Based | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-Use Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Government and Defense | |||

| Manufacturing and Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the server security solutions market in 2025?

The server security solutions market size is USD 28.96 billion in 2025.

What growth rate is projected for server security solutions through 2030?

Revenue is forecast to advance at a 7.7% CAGR, reaching USD 41.95 billion by 2030.

Which segment holds the largest share of spending?

Services lead with 40.2% revenue share, driven by demand for managed and professional security offerings.

Which geography is expanding the fastest?

Asia-Pacific is projected to grow at a 11.2% CAGR, propelled by sovereign-cloud mandates and data-center expansion.

Why are SMEs increasing their security budgets?

SMEs face rising ransomware attacks and a stark gap between compliance costs and non-compliance penalties, encouraging new investment in managed and cloud-based protections.

How are vendors differentiating their server security platforms?

Providers integrate AI analytics, unified policy engines, and confidential-computing support while pursuing acquisitions to offer broad, end-to-end protection suites.

Page last updated on: